Information

Has the Midcap–Smallcap Panic Finally Ended? Signs the Market May Have Formed a Bottom

.webp)

Key Takeaways

- Panic selling in midcap and smallcap indices has eased, showing early signs of bottom formation.

- Valuations have cooled, SIP flows remain steady, and regulatory interventions have stabilised sentiment.

- Institutional buying and volatility compression signal returning confidence.

- Investors should stay selective, focusing on quality, earnings visibility, and balance-sheet strength.

- Swastika Investmart’s research-driven approach can help navigate this recovery phase.

The recent sell-off in India’s midcap and smallcap space sent shockwaves through the market. After months of outperformance, these segments corrected sharply as investors reacted to frothy valuations, regulatory caution from SEBI, and global uncertainty.

But the big question now is: Has the panic finally ended? There are early signs that the market may be stabilising — and possibly forming a short-term bottom.

Let’s break down what’s happening, what signals matter, and how investors should position themselves.

What Triggered the Panic in Midcap and Smallcap Stocks?

The correction didn’t happen in isolation. Multiple triggers set the tone:

1. Valuation Excesses

Midcaps and smallcaps had rallied far beyond their historical averages. Many stocks were trading at 30–50% premiums despite modest earnings visibility.

This stretched the risk-reward equation, making the segment vulnerable to a correction.

2. SEBI’s Risk Alert

SEBI issued cautionary comments regarding overheating in smaller companies, urging mutual funds to reassess risk frameworks.

While not a direct intervention, it created a sentiment shock, leading to profit-booking and fund rebalancing.

3. Global Uncertainty

Concerns over US bond yields, geopolitical tensions, and FII outflows added fuel to the fire. With risk-off sentiment globally, smallcaps took the hardest hit.

4. Mutual Fund Rebalancing

Many schemes faced pressure to rebalance portfolios due to size restrictions and liquidity management rules, further accelerating the decline.

Is the Midcap–Smallcap Bottom In? Key Signs of Stabilisation

Now, the dust is beginning to settle — and several indicators suggest a bottom may be forming.

1. Selling Pressure Has Eased

The pace of declines has slowed significantly. Earlier, deep cuts of 4–6% were common in a day; now, volatility has tapered.

This cooling-off reflects reduced panic and more measured trading activity.

2. Volatility Compression

The India VIX remains within a controlled range, signalling improving risk appetite. Historically, midcap recoveries begin when volatility stabilises first.

3. Steady SIP Inflows

Despite sharp corrections, SIP contributions hit all-time highs, showing unwavering domestic investor faith.

Consistent inflows act as shock absorbers, reducing the likelihood of prolonged downturns.

4. Institutional Buying Is Back

Domestic institutional investors have started nibbling into quality smallcap and midcap names—especially in sectors like capital goods, defense, manufacturing, and financial services.

When institutions buy during corrections, it often marks the beginning of base formation.

5. Earnings Have Held Up

Indian corporates have delivered stable earnings. Several smaller companies reported healthy margins, strong order books, or improved cash flows — not characteristics of a market in deep distress.

6. Regulatory Clarity from SEBI

SEBI’s recent stance has shifted from caution to structured monitoring. Clear guidelines always reduce fear-driven volatility.

Once the overhang of regulatory uncertainty eases, quality stocks typically rebound sooner.

7. Historical Cycles Support the Trend

Past midcap–smallcap corrections (2013, 2018, 2020) show a similar pattern:

- Sharp decline

- Panic selling

- Sentiment stabilisation

- Slow accumulation phase

- Sectoral rotation

- Recovery

Markets seem to be entering the accumulation zone now.

What Should Investors Do Now? A Practical Guide

A bottoming market can be a golden opportunity — but only with the right strategy.

1. Focus on Quality Over Momentum

Companies with:

- Low leverage

- Consistent cash flows

- Strong promoters

- Predictable earnings

… are likely to lead the recovery.

2. Avoid “Penny Move” Traps

A rising tide won’t lift all boats. Many questionable smallcaps jumped in the rally but lack fundamentals.

Stay selective and avoid speculative bets.

3. Use SIPs and STPs Smartly

Instead of trying to catch the exact bottom, stagger your entry over 4–6 months.

This cushions volatility and improves long-term returns.

4. Look at Sectors with Structural Tailwinds

Segments showing resilience include:

- Capital goods

- Manufacturing and industrials

- Financial services

- Defense

- Railways

- Renewables

- Building materials

These sectors continue to receive policy support and strong domestic demand.

5. Review Portfolio Allocation

If your equity allocation has fallen due to the correction, rebalancing can boost long-term compounding.

6. Use Research-backed Tools

Platforms with robust screening tools, research reports, and advisory support can help you avoid mistakes.

This is where a trusted financial partner becomes invaluable.

Why Swastika Investmart Can Help You Navigate This Phase

Swastika Investmart, a SEBI-registered financial services provider, offers:

- In-depth equity research backed by data and market experience

- Advanced screening and analytics tools

- Dedicated customer support for investors across segments

- Tech-enabled platforms for effortless trading and investing

- Investor education initiatives designed to enhance financial literacy

In volatile markets, having a research-driven approach matters more than ever.

👉 Open an account today:

https://trade.swastika.co.in/?UTMsrc=HasTheMidcapSmallcapPanicFinallyEnded

FAQs

1. Are midcap and smallcap stocks safe to invest in now?

They are safer than during the peak, but selectivity is essential. Focus on companies with strong fundamentals.

2. Has the market definitely bottomed?

Not guaranteed — but key indicators show stabilisation and early signs of accumulation.

3. Should I stop SIPs during a correction?

No. Corrections increase long-term returns by lowering average cost.

4. Which sectors look promising after this correction?

Manufacturing, capital goods, financial services, and defense are showing resilience.

5. How long do recoveries usually take?

Historically, midcap–smallcap recoveries take 3–6 months to gain momentum after major corrections.

Conclusion

The midcap–smallcap panic appears to be cooling, with several signals pointing towards a potential bottom. While uncertainty remains, disciplined investing, quality stock selection, and data-backed decisions can turn this volatility into opportunity.

If you’re looking to navigate this phase with expert guidance, Swastika Investmart’s research-driven tools and advisory support can help you make informed decisions.

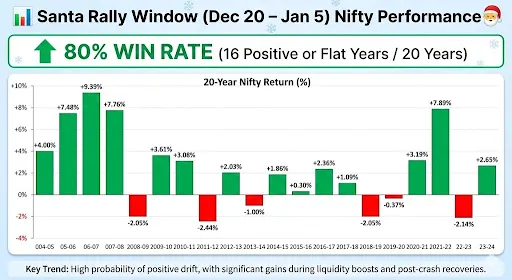

Nifty’s Santa Rally Pattern: Is December 20–Jan 5 Still a High-Probability Window for Returns?

Key Takeaways

- Historical data shows Nifty has delivered an 80% win rate during the Santa Rally window.

- Liquidity, festive spending, and global risk appetite often support this pattern.

- Not all years are positive—macros like FIIs, crude oil, and Fed policy matter.

- This year’s setup depends on domestic flows, RBI stance, and global volatility.

- Investors should stay data-driven and avoid emotional trading during year-end rallies.

Nifty’s Santa Rally Pattern: Is December 20–Jan 5 Still a High-Probability Window for Returns?

Every December, a familiar question resurfaces among Indian market participants:

“Will we see a Santa Rally this year?”

The Santa Rally—a phase between December 20 and January 5—is historically known for delivering strong positive returns in global equity markets. While the concept originated from US markets, the pattern has quietly taken shape in India as well.

And the numbers speak for themselves.

Over the last 20 years, Nifty has shown an 80% win rate during this period. That means in 16 out of 20 years, markets ended flat or positive.

Before we explore whether this year can repeat history, let’s look at the Table.

The Table highlights how often Nifty has delivered gains during this specific trading window. Notably big gains were observed in years following liquidity expansion phases or post-correction rebounds.

Some standout years include:

- 2005–06: +9.33%

- 2020–21: +7.89%

- 2006–07: +7.76%

Even in difficult cycles such as 2011–12 or 2015–16, the dips remained relatively contained.

The data hints at something deeper:

Investor behaviour, liquidity conditions, and institutional rebalancing consistently influence year-end trends.

Why Does the Santa Rally Happen in India?

1. Global Risk-On Sentiment

International markets often rally on:

- Year-end portfolio rebalancing

- Lower institutional trading volumes

- Festive optimism and reduced volatility

Nifty mirrors this behaviour, especially when FIIs turn buyers.

2. Domestic Liquidity Dominance

India’s rising SIP culture—now over ₹20,000 crore per month—creates a dependable liquidity cushion. Even when FIIs stay cautious, domestic institutions and retail flows provide strong support.

3. Corporate and Macro Visibility

By December:

- Most earnings downgrades are factored in

- Q3 outlook becomes clearer

- Global central bank signals stabilize

This reduces uncertainty, which markets love.

4. Event-Light Period

With major policy decisions and earnings behind us, markets enter a quieter news cycle—ideal for rallies.

Will Nifty See a Santa Rally This Year? Key Factors to Watch

Whether the Santa Rally returns this year depends on several moving parts.

1. FII and DII Behaviour

FIIs have been extremely sensitive to:

- US bond yields

- Dollar strength

- Emerging market valuations

If global yields cool and India remains the preferred EM destination, FIIs could drive a meaningful rally.

Meanwhile, DIIs continue to provide steady inflows regardless of global conditions.

2. RBI Policy Tone

A neutral-to-dovish stance from the RBI generally:

- Supports banking and rate-sensitive sectors

- Encourages broader market risk-taking

If inflation stays within comfort levels, the backdrop improves for a year-end run-up.

3. Crude Oil Volatility

For India, crude oil is the single biggest macro swing factor.

A stable or falling crude environment increases the probability of a Santa Rally.

4. Global Market Mood

If the US markets — especially S&P 500 and Nasdaq — carry momentum into the year-end, Nifty tends to follow suit.

Historically, India rarely rallies alone.

5. Technical Setup

Nifty’s technical structure going into December matters:

- Higher highs support continuation

- Consolidation ranges often lead to a breakout

- Overbought zones may limit upside

A neutral–positive structure improves the setup.

What Should Investors Do During a Potential Santa Rally?

1. Avoid Chasing Short-Term Euphoria

While Santa Rallies are common, relying on them as guaranteed is risky.

2. Keep Focus on High-Quality Stocks

Large caps tend to perform better due to stable liquidity.

3. Use Corrections to Accumulate

If volatility emerges, staggered buying helps reduce timing risk.

4. Don’t Ignore Global Triggers

Fed commentary, dollar index movement, and geopolitical risks can break the trend quickly.

5. Use Tools and Advisory Support

Platforms like Swastika Investmart, with SEBI-registered research and actionable insights, help investors stay aligned with data—not emotions.

FAQs

1. Does the Santa Rally always work in India?

No. While Nifty has delivered positive or flat returns in 80% of the last 20 years, external shocks or high valuations can offset historical patterns.

2. Why does Nifty usually rise between Dec 20 and Jan 5?

A mix of lower volatility, festive sentiment, portfolio rebalancing, and strong domestic flows often lifts markets.

3. Which sectors benefit the most during Santa Rallies?

Historically, banking, autos, consumer, and large-cap IT have shown stronger year-end momentum.

4. Is it safe to invest only for the Santa Rally?

Short-term bets are riskier. Long-term investors should view the rally as an opportunity, not a strategy.

5. What can break the Santa Rally this year?

Unexpected Fed remarks, Middle-East tensions, crude spikes, or heavy FII selling may cap returns.

Conclusion

The Santa Rally pattern in Nifty remains one of the most intriguing behavioural trends in the Indian market. Past data provides confidence—but not certainty. Whether this year repeats the 80% positive trend will depend on macro stability, global liquidity, and the market’s risk appetite.

For investors, the smartest approach is to stay data-driven and avoid knee-jerk decisions. Platforms like Swastika Investmart offer research-backed insights, strong customer support, and tech-enabled investing tools to help you navigate market opportunities confidently.

.webp)

Silver Supercycle 2025: Could Prices Really Shoot Up to ₹2 Lakh?

Key Takeaways

- Global supply constraints and rising industrial demand are reviving talks of a 2025 silver supercycle.

- Silver’s dual nature—industrial and precious metal—makes it highly sensitive to macro cycles.

- A ₹2 lakh/kg target is aggressive, but not impossible if inflation, clean energy demand, and geopolitical risks rise.

- Indian investors should track import duty policies, rupee movement, and global ETF flows.

- Silver remains a high-volatility asset; diversification is essential.

Silver Supercycle 2025: Could Prices Really Shoot Up to ₹2 Lakh?

Silver has always been the quieter cousin of gold—less flashy, more volatile, and often overlooked until a big move happens. But the conversation is heating up again. Several analysts and commodity strategists believe that 2025 could be the start of a major silver supercycle, one strong enough to push prices to ₹2,00,000 per kg in India.

Is this realistic or just another hype cycle?

Let’s break it down using real-world data, global trends, and India-specific context.

Why “Silver Supercycle 2025” Is Gaining Attention

A supercycle typically refers to a long, sustained rise in commodity prices caused by structural demand and limited supply. Historically, metals like copper, iron ore, and oil have experienced supercycles during periods of global expansion.

Silver is now entering a similar setup because of three major forces:

1. Exploding Industrial Demand

Silver is a critical input in:

- Solar panels

- Electric vehicles

- 5G devices

- Semiconductor manufacturing

- AI-driven hardware

- Medical equipment

The Solar Energy Industries Association estimates a gigantic jump in photovoltaic demand, potentially making silver one of the fastest-growing industrial metals in 2025.

2. Global Liquidity and Possible Rate Cuts

If the US Federal Reserve and other central banks move toward easing monetary policy, precious metals like silver typically rise due to:

- Lower real yields

- Weaker dollar

- Higher speculative interest

We saw this pattern during 2008–2011, when silver surged over 400%.

3. Tightening Supply and Mining Challenges

Mine production has lagged behind demand for years. Several major silver miners have reported:

- Lower ore grades

- Higher extraction costs

- Regulatory hurdles in Latin America

This mismatch between supply and demand is a classic trigger for a supercycle.

Can Silver Realistically Touch ₹2 Lakh per Kg in 2025?

Let’s look at the numbers.

Silver currently trades at approximately:

- ₹70,000–₹80,000 per kg (India)

- $22–$25 per ounce globally

For silver to reach ₹2,00,000 per kg, we would need:

- A 150%–180% price rise globally

- A stable to moderately weakening rupee

- Strong investment flows in global ETFs

- A surge in industrial consumption

While this is not the base-case expectation for most analysts, it is possible under a high-stress macro environment, such as:

- A global recession

- Major geopolitical escalation

- Aggressive central bank rate cuts

- Supply chain breakdowns

- A massive shift to renewable energy

Think of it this way:

Silver has rallied 10x in past cycles, most notably between 2003–2011. When silver runs, it really runs.

But it also corrects sharply.

This is why investors need a balanced view, not blind optimism.

How a Silver Supercycle Would Impact Indian Markets

India is one of the world’s largest consumers of silver—both industrially and as jewellery. The effects of a supercycle would be mixed:

1. Higher Import Bills

India imports most of its silver. A spike to ₹2 lakh/kg would put upward pressure on:

- Trade deficit

- Current account balance

- Rupee stability

This could indirectly influence stock markets via FII sentiment.

2. Boost for Solar and EV Stocks

Domestic companies in:

- renewable energy

- power equipment

- battery technology

- specialty chemicals

may face cost pressure but benefit from rising demand.

3. Increased Retail Participation

Indians traditionally buy silver during festivals and weddings. A price boom could push demand toward:

- Silver ETFs

- Silver ETPs

- Digital silver

- MCX silver derivatives

This aligns with India’s wider shift to formal financial instruments.

4. Impact on Jewellers

Jewellery players may see mixed results:

- Higher inventory values

- Lower retail demand

- Better margins if priced strategically

What Indian Investors Should Watch in 2025

Before assuming a supercycle, track these triggers:

1. RBI Policy and Rupee Movement

A weakening rupee can amplify silver prices far more than global moves.

2. India’s Import Duties

Any change in customs duty on silver impacts price directly.

3. MCX Volume Trends

Rising volumes can indicate rising speculative interest.

4. Global Silver ETF Flows

Institutional money is the real driver of supercycles.

5. Industrial Demand Data from China

China consumes nearly 50% of global silver. Its industrial recovery will be crucial.

FAQs

1. What is a silver supercycle?

It refers to a long-term surge in silver prices driven by strong structural demand and tight supply conditions across the global market.

2. Can silver really hit ₹2,00,000 per kg?

It’s an optimistic target. Achievable only if global liquidity, industrial demand, and supply disruptions align. Investors should consider it a possibility, not a certainty.

3. Is silver a better investment than gold in 2025?

Silver is more volatile but can deliver higher percentage returns during bull cycles. Gold, on the other hand, is more stable and defensive.

4. How should Indian investors buy silver?

Silver ETFs, MCX futures, and digital silver offer regulated and transparent access. Physical silver carries storage and purity risks.

5. Is now the right time to enter silver?

It depends on your risk profile. A staggered approach or SIP-style buying may help manage volatility.

Conclusion

The idea of a Silver Supercycle 2025 is exciting—and in many ways, credible. Industrial demand from solar and EVs is rising sharply, supply constraints are real, and global monetary cycles may turn favourable. But the jump to ₹2 lakh per kg requires an extraordinary combination of global events.

For Indian investors, the key is to stay informed, avoid speculative bets, and balance silver exposure within a diversified portfolio.

If you want expert guidance, market insights, and research-backed strategies, Swastika Investmart’s SEBI-registered advisory team and tech-enabled platforms can help you navigate commodity trends with confidence.

Fed Cuts Rates to 3.50%–3.75%: How Will This Impact Indian Stock Markets and Nifty?

Key Takeaways

- The US Federal Reserve has cut rates to 3.50%–3.75%, signaling a shift toward easing.

- Indian markets may see short-term volatility, but medium-term sentiment remains constructive.

- FIIs could increase flows into emerging markets if the dollar weakens.

- Rate-sensitive sectors in India—banks, NBFCs, real estate, autos—may see improved momentum.

- Nifty’s direction will depend on inflation, crude oil, domestic earnings, and global liquidity.

Fed Cuts Rates to 3.50%–3.75%: How Will This Impact Indian Stock Markets and Nifty?

The US Federal Reserve’s decision to cut interest rates to 3.50%–3.75% marks one of the most important policy shifts of the year. Whenever the Fed moves, global markets listen. And for India — now one of the world’s most influential emerging market economies — such a decision has both direct and indirect consequences.

Investors often wonder:

Will this boost Nifty?

Will FIIs return?

Will the market rally or consolidate?

This blog simplifies the answer with data-driven insights, Indian context, and real-world examples — written in a clear, natural, and professional style.

Why Did the Fed Cut Rates? A Quick Look at the Global Context

The Fed’s move comes on the back of a slowing US economy, easing inflation, and a need to support consumption and business borrowing. This pivot toward rate cuts signals:

- A softer interest-rate environment going forward

- Higher global liquidity

- A potential reversal of the strong US dollar trend

- Lower yields on US treasury bonds

Any of these factors can quickly alter the risk appetite of global investors — especially FIIs who influence Indian equity markets significantly.

How Fed Rate Cuts Affect the Indian Stock Market

Let’s break it down into simple, relatable impacts:

1. Impact on FIIs: Will Flows Return to India?

Generally, when US interest rates drop:

- US bond yields fall

- Dollar weakens

- Emerging markets become more attractive

For India, this is usually positive. Historically, we’ve seen this during:

- 2014–2015: Fed pause and liquidity boost → Heavy FII inflows → Nifty rallied

- 2020: Ultra-low US rates → Record inflows → Sensex touched new highs

If the current cut leads to a weaker dollar index, India could see:

- Renewed FII buying in banks, IT, capital goods

- Stabilizing currency volatility

- Higher participation in large-cap stocks

However, India is no longer dependent only on FIIs — strong domestic inflows provide a cushion even during global uncertainty.

2. Impact on Nifty: Short-Term Volatility, Medium-Term Tailwinds

Nifty’s immediate reaction may be choppy because markets had partially priced-in the rate cut.

But over the next quarter:

- Lower global borrowing costs

- Strong domestic GDP growth

- A supportive budget cycle

…could create a healthy setup for Nifty to trend positively, barring external shocks.

A key indicator to watch:

Crude oil. If oil stays below $85, India benefits.

3. Impact on the Indian Rupee

A Fed cut often reduces pressure on emerging market currencies. For the rupee:

- A stable or stronger INR reduces imported inflation

- Makes foreign borrowing cheaper for Indian corporates

- Improves investor confidence in rate-sensitive and import-dependent sectors

IT companies may see mild margin pressure if the rupee strengthens, but the overall direction remains sector-specific.

4. Sector-wise Impact on Indian Markets

Banking & NBFCs

Lower borrowing costs and better liquidity often support credit growth. Nifty Bank tends to benefit when yields soften globally.

IT & Tech

A weaker US dollar can reduce rupee revenues, but improved US business activity typically boosts demand for Indian IT services.

Real Estate

This sector thrives in lower-rate environments. Home loans could become more competitive if Indian rates also follow a softening path.

Autos

Lower global rates help reduce financing costs and also soften commodity prices — a positive for auto manufacturers.

Metals & Commodities

If global growth expectations rise due to Fed easing, metals could see revival.

What Should Indian Investors Do Now?

1. Avoid knee-jerk decisions

Markets may react sharply in the first few sessions, but stability often follows.

2. Focus on strong fundamentals

Companies with resilient earnings, low leverage, and steady cash flows are better positioned to benefit from liquidity-driven rallies.

3. Watch macro indicators

- Dollar Index (DXY)

- US 10-year bond yield

- Indian inflation and RBI commentary

- Crude oil trends

4. Maintain a diversified portfolio

A mix of large caps, sectors with strong earnings visibility, and long-term SIP flows can help ride global cycles smoothly.

FAQs

1. Will the Fed rate cut directly impact Indian interest rates?

Not immediately. The RBI considers domestic inflation and growth, though global cues like Fed policy indirectly influence its stance.

2. Will Nifty rise after the Fed rate cut?

Short-term volatility is possible, but medium-term sentiment tends to be positive due to better liquidity and improved risk appetite.

3. Are FIIs likely to return to Indian markets?

Yes, if global yields remain soft and the dollar cools, India becomes attractive due to strong economic fundamentals.

4. Which sectors will benefit the most?

Banks, NBFCs, real estate, IT, and autos could see improved sentiment depending on secondary macro factors.

5. Should retail investors make changes to their portfolios?

Only after evaluating risk tolerance and goals. Long-term investors should stay disciplined.

Conclusion

The Fed’s move to cut rates to 3.50%–3.75% is a significant turning point for global liquidity and market momentum. For India, the impact is likely to be constructive over the medium term — supported by strong domestic growth, healthy corporate earnings, and robust retail participation.

Investors who balance patience with informed decision-making stand to benefit the most.

If you're looking to analyze markets with expert guidance, real-time insights, and SEBI-registered research support, Swastika Investmart offers a tech-enabled platform to help you invest smarter.

ICICI AMC IPO: Complete Breakdown for Investors : Read This to Know If You Should Apply

Key Takeaways

- ICICI Prudential AMC is launching a ₹10,602 crore 100% OFS IPO.

- Strong financials: EBITDA margin 73%, RoNW 82.8%, consistent growth.

- Diversified AUM and strong brand help maintain stable long-term cash flows.

- Valuation at P/E 40.37x (FY25) seems reasonable vs peers.

- Good for long-term investors; listing gains may be moderate.

ICICI AMC IPO: Complete Breakdown for Investors — Read This to Know If You Should Apply

ICICI Prudential Asset Management Company (ICICI AMC) is finally coming to the public markets, and investor interest is already buzzing. Backed by ICICI Bank and Prudential Group — two respected names in the financial world — this IPO has become one of the most anticipated listings of the year.

In this detailed breakdown, we analyse the company’s business model, strengths, risks, financial performance, valuation, peer comparison, and whether investors should consider applying. This analysis follows SEBI-aligned transparency, Indian market context, and strong research methodology backed by Swastika Investmart’s expertise.

What Does ICICI Prudential AMC Really Do?

ICICI AMC is an Asset Management Company — meaning it manages money on behalf of retail and institutional investors. This money is pooled through mutual fund schemes like:

- Equity funds

- Debt funds

- Hybrid funds

- ETFs and Index funds

- PMS, AIFs

- Offshore advisory mandates

The company’s core responsibility is simple:

Invest clients’ money responsibly and generate long-term returns while managing risk.

They earn revenue primarily from management fees, which are linked to their AUM (Assets Under Management). So, higher AUM → higher income → stable profitability.

As of September 2025, ICICI AMC reported a Quarterly Average AUM of ₹10,147.6 billion, reflecting its large market dominance.

IPO Details

Issue Type: 100% Offer for Sale (OFS)

Total Issue Size: ₹10,602.65 crore

Fresh Issue: NIL

Offer for Sale: ₹10,602.65 crore

Price Band: ₹2061–₹2165

Market Lot: 6 shares

Issue Opens: 12 December 2025

Issue Closes: 16 December 2025

Listing: BSE & NSE

Market Cap at Upper Band: ₹1,07,006.97 crore

Basis of Allotment: 17 Dec 2025

Refunds: 18 Dec 2025

Shares in Demat: 18 Dec 2025

Listing Date: 19 Dec 2025

This IPO is purely OFS — no new money comes into the company, as existing shareholder Prudential Corporation is reducing its stake.

Company Financial Performance (FY23–FY25)

Below is a clean text summary of the company’s consolidated financial performance:

Equity Share Capital

- FY23: ₹17.6 crore

- FY24: ₹17.6 crore

- FY25: ₹17.6 crore

Net Worth

- FY23: ₹2,313.06 crore

- FY24: ₹2,882.84 crore

- FY25: ₹3,516.94 crore

Total Income

- FY23: ₹2,838.18 crore

- FY24: ₹3,761.21 crore

- FY25: ₹4,979.67 crore

EBITDA Margin

- FY23: 73.02%

- FY24: 73.91%

- FY25: 73.04%

Net Profit

- FY23: ₹1,515.78 crore

- FY24: ₹2,049.73 crore

- FY25: ₹2,650.66 crore

Observation:

There is consistent revenue and profit growth, stable margins, strong balance sheet expansion, and market-leading profitability.

Key Strengths of ICICI AMC

1. Strong Brand Backing

ICICI Bank + Prudential Group = instant trust among investors.

2. Diversified Product Mix

Equity, debt, hybrid, ETFs, PMS, AIF — all major asset classes covered.

3. High and Stable Margins

EBITDA margin ~73% indicates superior cost efficiency.

4. Robust Distribution Network

272 offices across 23 states + strong digital onboarding ecosystem.

5. High Return on Net Worth

RoNW of 82.8% is among the best in the financial sector.

Competition & Peer Comparison

Key Interpretation:

ICICI AMC leads the industry in RoNW, revenue scale, and premium brand value.

Outlook & Valuation

ICICI AMC is valued at P/E 40.37x (FY25). While not cheap, the valuation seems justified because:

- High investor trust in ICICI brand

- Strong and predictable fee-driven income

- Massive AUM backing

- Sector tailwinds (financialization of savings)

- Consistent profitability

- Low capital requirements + high operating leverage

Swastika Investmart’s research outlook suggests the IPO is positioned as a long-term compounding opportunity.

Risks to Consider

- 100% OFS — no fresh capital for future expansion

- Regulatory tightening (SEBI norms impact mutual funds)

- High dependence on distributor networks

- Market volatility may affect AUM inflows

- Rising competition from HDFC AMC, Nippon, SBI MF, Axis MF, etc.

Should You Apply for ICICI AMC IPO?

Here’s the balanced view:

Short-Term (Listing Gains)

- Since it is a full OFS, listing pop may be moderate.

- Demand looks strong due to brand name + financial quality.

Long-Term Investors

- Stable business model

- Industry tailwinds

- Strong balance sheet

- High margins and high RoNW

- Brand credibility

Verdict:

If your aim is long-term wealth creation, this IPO is worth considering.

FAQs

1. Is ICICI AMC a debt-free company?

Yes, the company operates with minimal debt due to its asset-light model.

2. What is the biggest risk for mutual fund AMCs?

Regulatory changes from SEBI and market volatility impacting AUM growth.

3. Is the IPO fully OFS?

Yes, 100% OFS, meaning no new shares are issued.

4. What makes ICICI AMC different from competitors?

Its scalable digital ecosystem, massive distribution, and industry-leading RoNW.

5. Can retail investors apply easily?

Yes, through broker apps, UPI, or via Swastika Investmart’s seamless platform.

Conclusion: Should You Apply?

ICICI Prudential AMC stands out for its strong financials, brand backing, diversified product portfolio, and superb profitability metrics. While the IPO is a pure OFS, long-term investors may find significant value as the Indian asset management industry continues to expand with rising financialization.

If you're looking for stability, trust, and steady compounding, ICICI AMC can be a strong addition to your long-term portfolio.

Explained: Why AU Small Finance Bank’s FDI Limit Increase Matters and What Investors Should Watch Next

Key Takeaways

- AU Small Finance Bank receives approval to raise foreign investment limit from 49% to 74%.

- Move can improve liquidity, capital access, and global investor participation.

- Could reshape competition within the small finance bank sector.

- Watch asset quality, capital deployment, and interest rate cycles in the coming quarters.

- Swastika Investmart’s SEBI-registered research can help investors interpret such regulatory shifts.

The Indian banking industry has been transforming rapidly, especially with growing digital adoption, tighter regulatory frameworks, and stronger capital adequacy norms. In this evolving landscape, the Finance Ministry’s approval allowing AU Small Finance Bank (AU SFB) to raise its foreign investment limit from 49% to 74% marks a significant policy milestone.

This development is not just a technical regulatory update—it is a signal that could reshape the bank’s capital flexibility, global investor interest, and long-term growth trajectory. For investors, understanding the implications of this move is essential, particularly at a time when the BFSI sector is witnessing steady credit offtake and rising competition.

Let’s break down what this approval means, why it matters, and what you—as an investor—should track in the coming months.

Why Raising the FDI Limit Is a Big Deal

1. Stronger Access to Global Capital

By increasing the foreign direct investment ceiling to 74%, AU SFB gains access to a broader pool of international investors. This is important because:

- Global investors bring long-term, patient capital

- They often support governance reforms and operational strengthening

- FDI helps reduce dependency on domestic markets during tight liquidity cycles

For a bank aiming to scale lending, digital infrastructure, and geographical footprint, additional foreign capital improves both capacity and resilience.

2. Enhances Market Perception and Institutional Trust

Banks with higher FDI participation often gain better visibility among global funds and rating agencies. AU SFB could see:

- Improved perception of governance quality

- Strengthened institutional confidence

- Enhanced long-term investor base

In previous regulatory instances—such as when HDFC Bank or ICICI Bank saw increased foreign investor interest—market visibility improved significantly.

3. Potential Boost to Capital Adequacy and Expansion Plans

Additional foreign capital can support AU SFB’s long-term growth roadmap, which typically includes:

- MSME and retail credit expansion

- New branch launches in underserved regions

- Investments in digital banking and fintech partnerships

- Better underwriting capabilities

Higher capital levels also act as a buffer during stressed credit cycles, ensuring healthier balance sheet stability.

Impact on the Indian Markets

The FDI increase aligns with India’s broader efforts to attract overseas capital into regulated sectors. For the BFSI space, such policy green signals generally:

- Improve foreign investor sentiment toward Indian financials

- Encourage capital flows into mid-tier banks

- Strengthen the SFB segment’s competitive landscape

In recent years, foreign flows into financial services have been closely tied to India’s interest rate cycles and macroeconomic stability. This announcement may help AU SFB attract incremental FPI/FII inflows, especially from global funds focused on emerging market banking stories.

What Investors Should Watch Next

1. How Much Capital AU SFB Actually Raises

FDI limit enhancement is only the first step. Investors should monitor:

- Size of capital infusion

- Type of investors participating

- Pricing and dilution impact

- Deployment strategy

Large long-term funds coming in could boost the stock’s institutional credibility.

2. Asset Quality Trends

With growth comes risk. Key metrics to follow:

- GNPA and NNPA movement

- Restructured book performance

- Collection efficiency

- Exposure to MSME and unsecured portfolios

A stable or improving asset quality trend will be a positive indicator.

3. Impact on Margins and Profitability

Capital infusion gives AU SFB the ability to expand lending, but investors should track:

- Net Interest Margin (NIM) trends

- Cost of funds

- Operating leverage gains

- Credit cost movements

If the bank maintains strong profitability while scaling, the FDI hike will translate into real value creation.

4. Regulatory Landscape for Small Finance Banks

The RBI has been vigilant with SFB compliance on:

- Lending norms

- Priority sector guidelines

- Capital adequacy ratios

Any shift in regulatory expectations could influence AU SFB’s growth trajectory.

FAQs

1. What does AU SFB’s FDI limit increase mean?

It allows foreign investors to own up to 74% of the bank, expanding its ability to attract global capital for growth and strengthening its balance sheet.

2. Will the bank immediately raise funds after this approval?

The approval only increases the permissible limit; actual fundraise depends on market conditions and management decisions.

3. How will this impact retail shareholders?

Higher FDI may improve liquidity, valuation visibility, and future growth prospects, though short-term market reactions may vary.

4. Is this positive for the small finance bank sector?

Yes. It may enhance global confidence in the SFB model and set the stage for similar policy flexibility for other players.

5. What risks should investors be aware of?

Asset quality pressures, credit cycle sensitivity, regulatory changes, and execution challenges during expansion.

Conclusion

The Finance Ministry’s approval for AU Small Finance Bank to raise its foreign investment limit from 49% to 74% is more than a policy update—it’s a strategic catalyst. It enhances the bank’s capacity to raise high-quality capital, strengthens institutional credibility, and opens doors for long-term expansion in a competitive banking ecosystem.

For investors, the next few quarters will be crucial to understand how the bank deploys new capital, manages its asset quality, and leverages growth opportunities.

For data-backed insights, investor education, and SEBI-registered guidance, platforms like Swastika Investmart empower you to make smarter, informed decisions—whether analysing regulatory updates or navigating market trends.

Park Medi World IPO Review (Dec 10–12): Business Model, Valuation & Investment Call

Key Takeaways

- Park Medi World operates 14 NABH-accredited multi-super speciality hospitals across North India.

- IPO size is ₹920 crore with a price band of ₹154–162.

- Healthy FY25 performance: ₹1,425.97 crore revenue and 26.11% EBITDA margin.

- Strong RoNW of 20% and reasonable valuation at 29.21x P/E.

- Suitable for medium to long-term investors seeking healthcare growth exposure.

India’s healthcare sector has been one of the most resilient and fast-evolving spaces, backed by rising demand for speciality care, medical infrastructure expansion, and increasing insurance penetration. Against this backdrop, the Park Medi World IPO has generated noticeable investor interest ahead of its December 10–12 bidding window.

The company operates a large network of multi-super speciality hospitals under the “Park” brand and is already one of the largest private healthcare providers in North India. Given the strong fundamentals and sectoral momentum, the IPO has become a talking point among retail and institutional investors.

Let’s dive deeper into its business model, financials, valuation, strengths, and key risks.

About Park Medi World

Park Medi World runs 14 multi-super speciality hospitals across Haryana, Delhi, Punjab, and Rajasthan. Its hospitals offer more than 30 speciality and super-speciality services including:

- Internal Medicine

- Neurology

- Oncology

- Orthopaedics

- Gastroenterology

- General Surgery

- Urology

All hospitals are NABH accredited, and eight facilities also hold NABL accreditation, reflecting strong clinical standards. The diverse speciality mix positions the group as a reliable healthcare provider across major population clusters.

IPO Details at a Glance

Issue Open: 10 December 2025

Issue Close: 12 December 2025

Total IPO Size: ₹920 crore

Fresh Issue: ₹770 crore

Offer for Sale: ₹150 crore

Price Band: ₹154–162

Market Lot: 92 shares

Face Value: ₹2

Listing: BSE, NSE

Expected Market Cap: ₹6,997.28 crore

Issue Break-up:

- QIBs: 50%

- NII: 35%

- Retail: 15%

Indicative Timetable:

- Basis of Allotment: 15 Dec 2025

- Refunds/ASBA Unblocking: 16 Dec 2025

- Shares to Demat: 16 Dec 2025

- Listing Date: 17 Dec 2025

Objects of the Issue

The company plans to deploy the fresh capital for:

- Expansion of 117 new company-operated (COCO) stores

- Lease and license fee payments for existing centres

- Purchase of new medical equipment and machinery

- Marketing and brand-building activities

- Debt repayment (a major positive)

- General corporate purposes

The ₹380 crore earmarked for debt repayment is expected to instantly improve net margins post-listing.

Valuation Metrics

- EPS (Pre-IPO): 5.55

- P/E (Post Issue): 29.21x

- RoNW: 20.08%

The valuation is reasonable when compared with premium-listed peers like Apollo Hospitals, Max Healthcare, Global Health, Krishna Institute of Medical Sciences, etc.

Strengths of Park Medi World

1. Strong Presence in North India

It is the second largest private hospital chain in North India and the largest in Haryana, offering deep regional penetration.

2. Diverse Speciality Mix

From oncology to orthopaedics, the wide range of specialities creates a stable revenue stream and enhances patient retention.

3. Accredited and Quality-Driven Network

NABH and NABL certifications across multiple hospitals strengthen clinical credibility.

4. Scalable Operating Model

A proven track record of acquiring and integrating hospitals gives the company an edge in expansion-driven growth.

5. Healthy Financial Profile

Consistent revenue growth, strong margins, and improving net worth make the financials robust.

Risks to Consider

High Operating Costs

Running large multi-speciality hospitals demands constant capex and skilled manpower, impacting cost structures.

Healthcare Regulatory Environment

The sector faces strict regulatory oversight relating to pricing, reporting, and medical standards.

Competitive Pressure

Private hospital chains and government institutions both create competitive intensity in major markets.

Dependence on Medical Professionals

Availability and retention of skilled doctors and staff remain critical to operational stability.

Seasonality in Patient Footfall

Certain treatments and admission rates fluctuate seasonally, affecting quarterly performance.

Competitive Landscape

Although the company claims no direct comparable peers with the same business model, listed players in the broader healthcare space include:

- Apollo Hospitals

- Narayana Hrudalaya

- Fortis Healthcare

- Max Healthcare

- KIMS

- Global Health

- Jupiter Hospitals

Park Medi World’s valuation is noticeably lower compared to many of these, offering an attractive entry point for long-term investors seeking healthcare exposure.

Should You Subscribe? – Valuation & Investment View

The IPO arrives with a favorable mix of growth, profitability, and reasonable valuation. Key positives include:

- Strong RoNW of 20%

- 26.11% EBITDA margin in FY25

- Debt reduction expected to boost profitability

- Large and expanding hospital network

- Healthy demand outlook in India’s healthcare sector

With growing healthcare consumption, rising insurance penetration, and government-backed initiatives supporting medical infrastructure, Park Medi World is well-positioned to benefit from structural sectoral demand.

For medium to long-term investors, the IPO appears to offer a solid combination of stable business fundamentals and attractive valuation.

Frequently Asked Questions

1. What is the price band of the Park Medi World IPO?

The IPO is priced at ₹154 to ₹162 per share.

2. How is the company financially performing?

In FY25, Park Medi World generated ₹1,425.97 crore in revenue, with a 26.11% EBITDA margin and ₹213.22 crore net profit.

3. What will the company use the IPO proceeds for?

Funds will be used for expansion, equipment purchase, marketing, and debt repayment.

4. Is the valuation attractive?

At 29.21x P/E, the valuation is reasonable compared to major listed hospital chains with significantly higher multiples.

5. Is this IPO suitable for long-term investors?

Given the strong operating performance and regional leadership, the IPO suits investors seeking long-term exposure to India’s healthcare growth story.

Conclusion

Park Medi World’s IPO comes at a time when healthcare demand in India is rising rapidly. With strong financials, expanding capacity, and a track record of consistent execution, the company presents a compelling long-term investment case. As always, aligning IPO investments with your risk appetite and financial goals is important.

For deeper insights, SEBI-registered guidance, and easy investing tools, platforms like Swastika Investmart help investors make informed decisions with confidence.

Nephrocare IPO Opens Dec 10–12: Should Investors Back Asia’s Largest Dialysis Provider?

Key Takeaways

- Nephrocare is Asia’s largest dialysis provider with 519 centers across India and international markets.

- IPO opens December 10–12; price band ₹438–460; total issue size ₹4,615 crore.

- Revenues grew from ₹443 crore in FY23 to ₹770 crore in FY25; FY25 profit stood at ₹67 crore.

- Valuation appears aggressive at a P/E of 63.52x vs listed healthcare peers.

- Suitable primarily for aggressive long-term investors; short-term listing gains uncertain.

India’s healthcare ecosystem has transformed rapidly over the past decade, with specialized service providers playing a crucial role in bridging critical care gaps. One segment that has grown consistently is dialysis care, driven by rising chronic kidney disease (CKD) cases and limited access to quality treatment in Tier II and Tier III cities.

Against this backdrop, Nephrocare Health Services, Asia’s largest dialysis care provider and the world’s fifth-largest by treatment volume, is launching its IPO from December 10 to December 12. The company’s scale, operational footprint, and unique service model have attracted strong investor attention.

This analysis breaks down whether the Nephrocare IPO deserves a spot in your portfolio.

Company Overview

Founded in 2010, Nephrocare offers end-to-end dialysis services, including diagnosis, haemodialysis, mobile dialysis, home dialysis, and wellness programs. The company also runs an in-house pharmacy, which enhances value per patient and operational efficiency.

As of September 30, 2025, Nephrocare operated:

- 519 dialysis centers

- 51 international centers across the Philippines, Uzbekistan, and Nepal

- Presence in 288 cities across 21 states and 4 union territories

- 77.53% centers in Tier II and III regions

Its international presence includes the world’s largest dialysis clinic in Uzbekistan, highlighting its execution capability outside India as well.

Nephrocare also partners with major hospitals such as Max Super Speciality Hospital, Fortis Escorts, Care Hospitals, Wockhardt Hospitals, Paras Healthcare, Jehangir Hospital, and Ruby Hall Clinic—strengthening credibility and patient inflows.

IPO Details

Here is the IPO information converted from the table into clean descriptive text:

- IPO Date: December 10–12, 2025

- Total Issue Size: ₹4,615 crore

- Fresh Issue: ₹3,534 crore

- Offer for Sale (OFS): ₹1,080+ crore (11.25 million shares)

- Price Band: ₹438–460

- Market Lot: 32 shares

- Face Value: ₹2

- Market Capitalization at Upper Band: ₹4,615 crore

- Listing: NSE and BSE

- QIB Allocation: 50%

- NII Allocation: 15%

- Retail Allocation: 35%

Important dates:

- Basis of Allotment – December 15

- Refunds/ASBA Unblocking – December 16

- Credit to Demat – December 16

- Listing – December 17

Objects of the Issue

According to the RHP and uploaded note, the proceeds will be used for:

- Opening new dialysis centers in India

- Repayment/prepayment of certain borrowings

- General corporate purposes

This aligns with Nephrocare’s expansion-led growth model.

Financial Performance

Here is the table translated into simple text:

FY23 to FY25 Financial Trend

- Revenue:

- FY23: ₹443.26 crore

- FY24: ₹574.72 crore

- FY25: ₹769.92 crore

- EBITDA Margin:

- FY23: 11%

- FY24: 17.3%

- FY25: 21.6%

- Net Profit/Loss:

- FY23: –₹11.79 crore (loss)

- FY24: ₹35.13 crore (profit)

- FY25: ₹67.10 crore (profit)

- Net Worth:

- FY23: ₹384.73 crore

- FY24: ₹423.55 crore

- FY25: ₹594.21 crore

This financial trajectory shows that Nephrocare has achieved consistent revenue growth, margin expansion, and a turnaround from losses to profits within two years.

However, the note also highlights that higher finance costs affected profitability in H1 FY26, indicating the impact of expansion-related borrowing.

Key Strengths

- Asia’s largest dialysis provider, serving over 33,000 patients annually

- Extensive clinic network across India and key international markets

- Deep penetration in underserved Tier II and III markets

- Strategic partnerships with major hospital chains

- Operational excellence backed by an experienced management team

Key Risks

- Capital-intensive expansion demands continuous funding

- Maintaining quality control across 500+ clinics is challenging

- Profit margins vulnerable to policy changes in dialysis reimbursement

- Rising competition from hospital chains and local providers

- High OFS component may reflect partial exits by existing shareholders

Valuation and Peer Comparison

The IPO is valued at 63.52x earnings, based on FY25 EPS of ₹8.28.

When compared with listed Indian healthcare players:

- Narayana Health – 45.21x

- Jupiter Lifeline Hospitals – 51.10x

- Rainbow Children’s Hospital – 56.84x

- Dr. Lal Path Labs – 52.47x

- Metropolis Healthcare – 69.48x

- Vijaya Diagnostics – 73.14x

While a direct comparison is difficult due to Nephrocare’s unique dialysis-focused model, the valuation appears aggressive, especially considering its relatively smaller scale compared to multispecialty hospital chains.

This suggests that strong listing gains are not guaranteed unless subscription is exceptionally high.

Market Context and Regulatory Relevance

Dialysis demand in India is rising sharply due to:

- Increasing CKD prevalence

- Limited access to kidney care in semi-urban regions

- Supportive government schemes like Ayushman Bharat

- Public-private partnership models for dialysis centers

The sector’s growth is resilient and relatively non-cyclical, which helps companies like Nephrocare maintain steady patient footfall regardless of market cycles.

SEBI’s oversight on IPO disclosures and IRDA/RBI-backed financial compliance add another layer of investor protection.

Should You Apply for the Nephrocare IPO?

Nephrocare presents a strong long-term growth opportunity powered by scale, rising healthcare demand, and a proven operating model. However, the valuation premium and capital-intensive nature of the business require cautious optimism.

Best suited for:

✔ Aggressive long-term investors

✔ Those who believe in chronic-care healthcare models

✔ Investors comfortable with higher valuations

Not ideal for:

✘ Risk-averse investors

✘ Those seeking guaranteed short-term listing gains

FAQs

1. Is Nephrocare IPO good for long-term investment?

Yes, provided you are comfortable with higher valuations and expect steady growth in healthcare services.

2. How has Nephrocare performed financially?

The company grew revenues from ₹443 crore in FY23 to ₹770 crore in FY25, with profits improving sharply.

3. Why is the valuation considered aggressive?

Its P/E of 63.52x is higher than many listed healthcare peers, despite smaller revenue size.

4. What makes Nephrocare different from hospital chains?

It is a pure-play dialysis provider, giving it specialization advantage but also limiting diversification.

5. Who should avoid this IPO?

Investors seeking low-risk opportunities or short-term listing gains may skip.

Conclusion

Nephrocare’s IPO brings a unique healthcare opportunity to the Indian markets. The company’s strong presence in underserved regions, international expansion, and improving financials make it a compelling option for long-term investors. However, the valuation premium means investors must balance growth potential with cautious expectations.

For investors who want expert research, seamless IPO application, and tech-enabled investing backed by a SEBI-registered entity, Swastika Investmart provides a trusted platform.

Fino Payments Bank Gets Green Light from RBI - Will This Fuel New Growth in Financial Inclusion?

Key Takeaways

- RBI lifts restrictions on Fino Payments Bank, enabling a fresh start.

- Move expected to boost last-mile digital banking and rural inclusion.

- Strengthens the role of fintech-led micro-banking ecosystems.

- Could influence investor sentiment across small finance and fintech players.

- Swastika Investmart highlights investor education and data-backed insights for smarter decisions.

The recent approval granted to Fino Payments Bank by the Reserve Bank of India (RBI) has revived conversations around the future of digital banking and financial inclusion in India. The lifting of restrictions marks a crucial turning point for a bank that has always positioned itself as a last-mile service provider, especially across Tier-3 and rural regions.

With India’s financial ecosystem becoming more digital and regulated than ever, this move carries significant implications—not just for customers, but also for fintech competition, investor sentiment, and the overall payments landscape.

Let’s break down what this development means, why it matters, and how it may shape the future of India's financial inclusion efforts.

Why RBI's Green Light Matters

Stronger Trust in the Payments Bank Model

Payments banks were conceptualized to bridge India’s financial inclusion gap by offering safe, low-cost digital banking services. When the RBI reinstates operational clarity to such a player, it sends a signal that the model still holds value—especially for enabling micro-transactions, doorstep banking, Aadhaar-enabled services, and cash-in/cash-out points.

Fino has a strong presence across rural pockets, functioning like a bridge between formal banking systems and underserved communities. With the recent approval, the bank can accelerate operations that were earlier limited or paused.

What This Means for Customers

1. Revival of Digital Banking Services

Customers can expect smoother access to services like:

- Digital savings account operations

- Micro-ATM withdrawals

- Aadhaar-enabled payment services

- Utility bill payments

- Remittance services

This is crucial for regions where traditional banking infrastructure remains limited.

2. Boost for Rural & Semi-Urban Banking

Fino’s vast merchant network—spanning kirana stores, CSCs, and micro-businesses—supports millions of small-value transactions daily. With RBI’s go-ahead, these services resume normalcy, ensuring uninterrupted financial activity in remote areas.

3. Increased Security & Compliance Assurance

RBI oversight ensures improved operational controls, cybersecurity protocols, and customer protection—important for users who rely heavily on cash-led transactions.

Impact on the Indian Financial Markets

While the development does not directly move major indices, it does influence sentiment across:

- Payments and fintech companies

- Small finance banks

- NBFC-MFI players

- Rural banking solution providers

Investors read RBI’s decision as a signal of stability and consistency in the regulatory stance toward digital financial models. This comes at a time when India is rapidly advancing toward a less-cash economy driven by UPI, Aadhaar-based verification, and interoperable infrastructure.

Real-World Parallel

When Airtel Payments Bank received regulatory clarity in the past after temporary restrictions, customer activity rebounded quickly. A similar rejuvenation could occur for Fino, particularly in domestic remittances and agent-assisted banking.

How This Shapes the Future of Financial Inclusion

1. Strengthening the “Phygital” Model

India’s unique financial landscape requires both digital and physical touchpoints. Fino’s large on-ground network complements digital interfaces, making it easier for first-time users to adopt formal banking.

2. Support for Government-Led Initiatives

Reforms such as:

- Jan Dhan Yojana

- PM Kisan

- Direct Benefit Transfers (DBT)

- Digital literacy programs

get a direct operational boost as the last-mile delivery channel becomes more robust.

3. Job Creation & Local Enterprise Support

Banking correspondents, micro-merchants, and rural service points benefit economically from resumed services.

Competitive Landscape: Navigating Neutrally but Smartly

While players like Airtel Payments Bank, India Post Payments Bank, and small finance banks continue strengthening their digital stack, the reinstatement allows Fino to re-align its position.

Amid this, Swastika Investmart stands apart in helping investors interpret such developments with:

- SEBI-registered advisory

- Strong research-backed insights

- Tech-enabled platforms for smooth investing

- Focus on investor education

- Reliable customer support for new and seasoned investors

These strengths matter when markets move on regulatory developments, especially in emerging sectors like fintech and digital banking.

FAQs

1. Why did RBI’s approval for Fino Payments Bank create buzz?

Because it restores full operational capacity, enabling the bank to continue serving millions of customers in rural and semi-urban India.

2. Will this impact other fintech or payments bank stocks?

Not directly, but it improves confidence in the payments bank ecosystem, which can positively influence sectoral sentiment.

3. Does Fino's reinstatement help financial inclusion?

Yes. It strengthens last-mile service delivery, which is central to India’s financial inclusion mission.

4. Are customers safe using services after RBI’s nod?

Yes. RBI clearance indicates adherence to regulatory norms, improving trust and operational transparency.

5. Should investors consider fintech or banking stocks now?

Investors should evaluate fundamentals, compliance track record, and growth opportunities—preferably with guidance from a SEBI-registered advisor like Swastika Investmart.

Conclusion

RBI’s approval for Fino Payments Bank is more than a compliance milestone—it’s a reaffirmation of India’s vision of inclusive, accessible, and digitally empowered banking. As demand for low-cost, last-mile financial services grows, players like Fino will continue shaping the future of rural and semi-urban banking.

For investors, staying informed about such regulatory developments is essential. That’s where Swastika Investmart, with its strong research tools and investor-first approach, empowers you to make smarter decisions.

Monetary Policy 2025: RBI Cuts Repo Rate to 5.25% : December Policy Explained & Its Impact on India’s Economy

Key Takeaways

- RBI reduced the repo rate by 25 bps to 5.25% in its December 2025 monetary policy.

- The move aims to support growth, ease borrowing costs, and improve liquidity.

- Inflation is expected to moderate gradually, giving RBI space to adjust rates.

- Borrowers may see lower EMIs, while banks gain better credit demand visibility.

- Financial markets may react positively as rate cuts usually support economic momentum.

The Reserve Bank of India (RBI) delivered its much-awaited December 2025 Monetary Policy, announcing a 25 bps cut in the repo rate, bringing it down to 5.25%. This move signals the central bank’s intent to revive economic momentum while ensuring inflation stays within the target band.

For the Indian financial markets, banks, borrowers, and businesses, this rate cut carries significant implications. Here’s a detailed breakdown of what the latest monetary policy means and how it shapes the economic landscape going into 2026.

Why Did RBI Cut the Repo Rate?

The repo rate—the rate at which banks borrow funds from the RBI—plays a key role in controlling inflation and supporting growth.

Key reasons behind the 25 bps cut:

1. Easing Inflation Pressures

Despite temporary spikes due to food inflation, core inflation has stayed within the comfort zone. This gave the RBI room to support growth through a moderate rate cut.

2. Boosting Consumption & Investment

A lower repo rate makes loans cheaper.

This helps push consumer spending in sectors like real estate, auto, and fintech lending—critical pillars of India’s economy.

3. Supporting Economic Growth

With global economic uncertainty and weakening exports, domestic growth needs a push. The rate cut aims to strengthen India’s economic resilience.

How the Rate Cut Impacts Inflation, Liquidity & Growth

Inflation Impact

A rate cut can potentially increase demand, which may push inflation slightly higher.

However, RBI expects food inflation to soften and supply chains to improve, keeping overall inflation manageable.

Liquidity Impact

Lower repo rates make borrowing easier for banks, improving overall systemic liquidity.

This helps NBFCs, fintech lenders, and sectors dependent on credit availability.

Economic Growth Impact

A 25 bps cut boosts:

- Housing demand

- Auto sales

- SME and MSME borrowing

- Corporate capex plans

Economic activity tends to pick up when borrowing becomes cheaper.

What the Rate Cut Means for Borrowers

1. EMIs May Reduce

Borrowers with floating-rate home loans, car loans, and personal loans could see reduced EMIs in the coming cycles.

2. Faster Loan Approvals

Banks may push more credit to accelerate growth, improving overall lending conditions.

3. Refinancing Becomes Attractive

Borrowers may consider switching lenders to take advantage of lower interest rates.

Impact on Banks and NBFCs

1. Improved Credit Demand

With cheaper loans, demand for retail and business credit may rise.

2. Pressure on NIMs (Net Interest Margins)

Lower rates can reduce banks’ margins, especially for those with higher cost of funds.

3. Stronger Retail Lending Cycle

Banks in home loans, vehicle financing, and personal loans may see stronger growth.

How the Indian Stock Market May React

Stock markets generally react positively to rate cuts because they improve economic outlook.

Potential Beneficiaries:

- Banks & NBFCs

- Real estate developers

- Automobile companies

- Rate-sensitive sectors like capital goods and consumer durables

Market Caution Areas:

- PSU banks with high deposit costs

- Sectors facing global headwinds (IT, exports)

Does This Mark the Start of a Rate-Cut Cycle?

While the RBI did not commit to future cuts, the tone of the policy was accommodative.

Future rate cuts will depend on:

- Inflation trajectory

- Global economic conditions

- Crude oil prices

- Domestic demand patterns

FAQs

1. Why did RBI cut the repo rate to 5.25%?

To support economic growth, improve liquidity and encourage borrowing while inflation remains manageable.

2. Will loan EMIs come down after this rate cut?

Yes, floating-rate loans are likely to see reduced EMIs as banks gradually pass on the rate cut.

3. What are the risks of this rate cut?

Inflation may rise if demand shoots up aggressively, and bank margins may remain under pressure.

4. Which sectors benefit the most?

Real estate, auto, banks, NBFCs, and consumer discretionary typically gain from lower interest rates.

5. Is this the beginning of a rate cut cycle?

Not confirmed, but RBI’s stance appears accommodative, opening the door for further adjustments depending on inflation data.

Conclusion

RBI’s December 2025 monetary policy marks a key moment for India’s economic road ahead.

The 25 bps cut to 5.25% aims to strike a balance between supporting growth and keeping inflation under control. Borrowers, banks, and financial markets stand to benefit from improved liquidity and cheaper credit.

As India heads into 2026, monitoring inflation, global cues, and domestic demand will be important to understanding RBI’s next moves.

If you want to navigate such market shifts with expert-backed research, tools, and dedicated support, Swastika Investmart can be your trusted partner.

%20(7)%20(2).webp)

Why Kaynes Tech Shares Are Falling: A Breakdown of Kotak’s Critical Report

Key Takeaways

- Kaynes Tech shares fell sharply after Kotak Institutional Equities raised concerns over its FY25 disclosures.

- Issues flagged: negative cash flows, higher CCC days, questionable accounting of technical know-how, and lack of clarity in disclosures.

- Market reacted before the exchange filing, showing shaken investor confidence.

- The concerns do not automatically mean fraud—but they highlight the need for stronger governance and transparency.

- Investors should track future disclosures closely and assess fundamentals before taking decisions.

Kaynes Technology, one of India’s most-watched electronics manufacturing services (EMS) companies, has recently come under pressure. The stock fell 4.56% in a single day, dropped 7% over the last five days, and is down 22.7% in one month—raising eyebrows across the market.

The trigger?

A critical report by Kotak Institutional Equities questioning the company’s FY25 financial disclosures, accounting treatment, cash flow quality, and transparency.

This blog breaks down:

- What Kotak flagged

- Why the market reacted so strongly

- What this means for investors

- Broader implications for the Indian markets

All in a simple, fact-driven, educational manner.

Kaynes Tech: What Triggered the Sell-Off?

In early December, Kotak Institutional Equities released a report raising significant concerns about Kaynes Technology’s FY25 numbers. Interestingly, the market reacted even before the official exchange filing, suggesting the concerns circulated among institutions ahead of time.

As a result, the stock—already under pressure—fell even more sharply.

Major Concerns Raised by Kotak (Explained Simply)

1. Negative Cash Flow Despite Revenue Growth

Kotak pointed out that Kaynes reported negative operating cash flow for the year.

Why?

- Cash conversion cycle increased by 22 days

- Higher working capital requirements

- Increased capital expenditure

In the EMS business, where efficiency and cash turnaround are crucial, this is a red flag.

2. Questionable Accounting of Technical Know-How

One of the most debated points:

Kaynes capitalised ₹180 crore (about 6.5% of revenue) as technical know-how.

Kotak said:

- No sufficient detail was provided on what this know-how is

- Why such a large amount was capitalised

- How it contributes to future revenue or margins

When companies capitalise expenses aggressively, profitability can appear inflated.

This raised investor suspicion.

3. Concerns Over Smart Metering Acquisition

Kotak questioned the accounting treatment of Kaynes’s smart metering acquisition.

The report pointed out:

- Lack of clarity in disclosures

- Unexplained adjustments

- Uncertain financial synergies

Since acquisitions are a major growth lever for EMS companies, transparency becomes essential.

4. Inconsistencies in Cash Flow Reporting

Kotak flagged:

- Gaps in related-party disclosures

- Variance between reported profit vs. cash flow

- Unexplained changes in working capital items

Such inconsistencies usually make analysts more cautious, especially in a high-growth sector.

5. Market Sentiment Turned Risk-Off

The overall Indian market has been cautious in December due to global volatility.

Small and mid-cap stocks have been under pressure, and reports like this amplify the sell-off.

For a stock like Kaynes—which previously traded at a premium valuation—any governance or disclosure concern triggers a strong reaction.

Why the Market Reacted So Quickly

Even though companies often clarify such issues later, markets tend to price in risk immediately.

Three reasons:

1. High valuations = Low tolerance for bad news

Kaynes traded at rich multiples, so even small concerns can cause a steep correction.

2. Institutions act fast

When institutional brokerages flag issues, FII and DII flows adjust quickly.

3. Cash Flow concerns scare long-term investors

Profit can be adjusted.

Cash cannot.

Negative cash flow instantly triggers caution.

Impact on the Indian Market & EMS Sector

1. EMS sector under scrutiny

Kaynes' situation has led to broader questions on:

- Governance

- Transparency

- Capital allocation practices in EMS companies

Rivals like Syrma SGS, Dixon, and Amber also saw intraday volatility.

2. Regulators may seek clarity

Accounting treatment of technical know-how and related-party reporting may draw attention from SEBI.

3. Investors becoming more selective

High-growth sectors now face closer scrutiny.

This is healthy for long-term market quality.

What Should Investors Watch Next (Educational Checklist)

This is not investment advice, but a general educational guide on what key areas matter:

1. Clarification from Management

Watch for detailed explanations on:

- Technical know-how capitalisation

- Smart metering acquisition accounting

- Related-party disclosures

2. Q3 & Q4 Cash Flow Trends

Sustained cash burn could become a bigger concern.

3. Auditor Notes

Any emphasis of matter in annual reports is important.

4. Working Capital Cycle

EMS companies must maintain discipline here.

5. Institutional Activity

Track FII/DII buying or selling patterns.

Frequently Asked Questions

1. Why did Kaynes Tech shares fall sharply?

Due to concerns raised by Kotak about FY25 disclosures, accounting treatment, cash flows, and transparency.

2. Is this a sign of fraud?

No. Kotak’s report highlights red flags—not fraud.

It simply calls for clearer disclosures.

3. Should investors panic?

Investors should wait for management clarification and analyse fundamentals.

Corrections often happen when valuations are high.

4. How does this affect the EMS sector?

It creates short-term volatility but may improve governance and transparency long-term.

5. What should retail investors track?

Cash flows, working-capital cycle, disclosures, and management commentary.

Conclusion

Kaynes Technology’s recent stock correction reflects how sensitive markets are to financial reporting clarity and governance standards. Kotak’s report has raised valid questions that the company needs to address clearly and transparently.

For investors, this is a reminder that:

- Cash flow matters more than reported profit

- High valuations demand high governance

- Transparency builds trust in the long run

If you want research-backed insights, tools, and support for your investing journey, Swastika Investmart offers SEBI-registered advisory, robust platforms, and a customer-first approach to simplify decision-making.

Operational Disruptions at IndiGo: How Operational Disruptions Could Impact Aviation Stocks in the Short Term

Key Takeaways

- IndiGo’s recent operational disruptions may trigger short-term volatility across aviation stocks.

- Flight cancellations, delays, and crew shortages directly influence costs and passenger sentiment.

- The aviation sector is already facing elevated fuel prices and capacity constraints.

- Investors should track DGCA updates, operational metrics, and forward-booking trends.

- Long-term structural growth in Indian aviation remains strong despite near-term pressures.

Operational disruptions in the aviation industry are not uncommon, but when they occur at scale—especially at India’s largest airline—markets tend to react sharply. IndiGo, which commands more than half of India’s domestic aviation market, has recently faced operational challenges ranging from flight cancellations to crew shortages. These issues have not only inconvenienced passengers but have also raised questions about the short-term outlook for aviation stocks.

In a sector where margins are thin and operating costs are unpredictable, even temporary disruptions can create ripple effects in stock performance. This blog explores what IndiGo’s operational issues could mean for the broader aviation sector and what investors should monitor going forward.

Understanding the Nature of IndiGo’s Operational Disruptions

IndiGo’s disruptions typically stem from a combination of internal and external factors. Recent incidents have included:

- Large-scale delays due to crew availability

- Weather-related disturbances impacting key hubs

- Aircraft groundings for maintenance and safety checks

- Supply chain bottlenecks affecting spare parts and engine components

Since IndiGo operates a massive fleet network with tight turnaround times, even small inefficiencies can snowball across multiple routes.

India’s aviation regulator, the Directorate General of Civil Aviation (DGCA), closely monitors such disruptions and may issue advisories or require corrective action when they impact flight safety or scheduling reliability.

Immediate Market Impact: Why Aviation Stocks React Quickly

Short-Term Hit to Investor Sentiment

When operational disruptions become news headlines, airline stocks often witness immediate selling pressure. The reasons are straightforward:

- Investors fear rising operational costs

- Disruptions affect passenger satisfaction and brand perception

- Short-term revenue may drop due to cancellations and reimbursements

For example, during earlier disruptions across airlines in 2019 and 2023, market leaders like Indigo and SpiceJet observed swift intraday declines as uncertainty mounted.

Higher Operating Costs and Fuel Sensitivity

Even under normal operations, aviation companies struggle with fluctuating ATF (Aviation Turbine Fuel) prices, which account for nearly 35–40% of an airline’s operating expenses. When disruptions occur:

- Turnaround times increase

- Aircraft utilisation drops

- Compensation and refund costs rise