Canara Bank Delivers Strong Q3 FY26 Results as Asset Quality Improves

.webp)

Canara Bank Delivers Strong Q3 FY26 Results as Asset Quality Improves

Canara Bank’s Q3 FY26 performance marks another important milestone in the transformation journey of India’s public sector banks. The lender reported a solid rise in profitability, supported by healthier core income, tighter control on bad loans, and a comfortable capital buffer.

At a time when investors are closely tracking bank earnings for signs of sustainability rather than one-off gains, Canara Bank’s latest numbers point toward structural improvement rather than temporary relief. For market participants, this quarter offers useful insights into how PSU banks are evolving in a more disciplined credit environment.

Key Highlights from Canara Bank Q3 FY26 Results

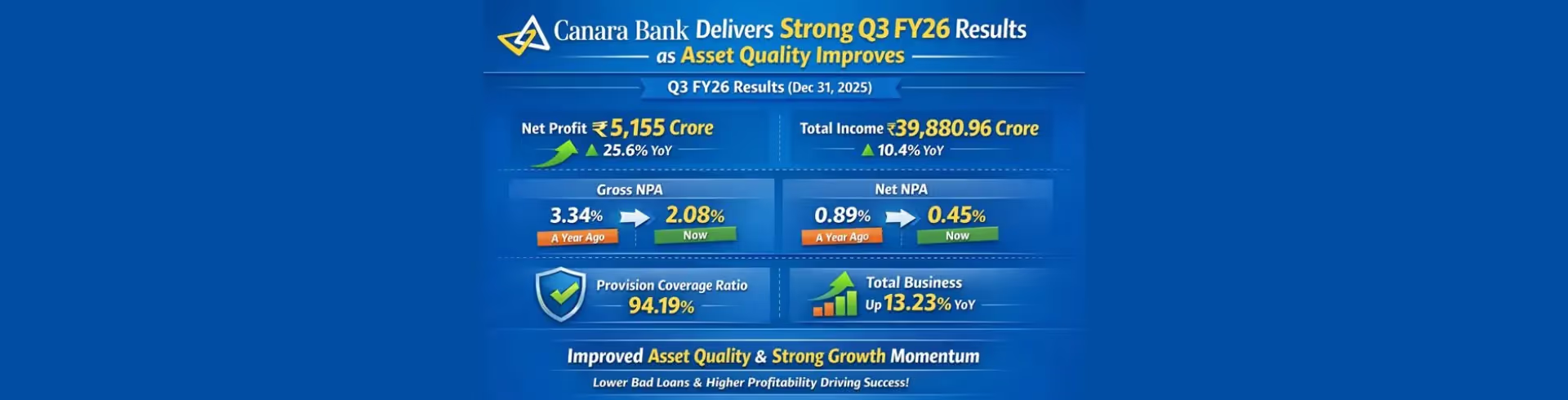

- Standalone net profit rose sharply to ₹5,155 crore

- Asset quality improved with Gross NPAs falling close to 2 percent

- Core income remained stable with healthy Net Interest Income

- Capital adequacy stayed well above RBI requirements

- Treasury and retail segments supported overall profitability

These indicators together suggest that the bank’s earnings quality has strengthened, a factor increasingly valued by long-term investors.

Profit Growth Reflects Better Balance Sheet Management

Net Profit Growth Signals Stability

For the quarter ended December 2025, Canara Bank reported a standalone net profit of ₹5,155 crore, a significant improvement compared to the same period last year. This growth was not driven by aggressive risk-taking but by steady income generation and controlled provisioning.

Unlike earlier cycles where PSU bank profits were volatile due to stressed assets, the current earnings trajectory appears more predictable and resilient.

Net Interest Income Remains the Backbone

Net Interest Income for the quarter crossed ₹9,250 crore, indicating that the bank continues to earn well from its lending operations despite fluctuations in interest rates. Stable spreads and controlled funding costs helped protect margins.

For investors, consistent NII growth is crucial because it reflects the strength of the bank’s core business rather than reliance on market-linked gains.

Asset Quality Improvement Continues to Build Confidence

Sharp Decline in NPAs

One of the most positive aspects of Canara Bank’s Q3 FY26 results is the improvement in asset quality. The Gross NPA ratio declined to around 2.08 percent, while Net NPAs fell to 0.45 percent.

This reflects years of focused recovery efforts, cautious loan approvals, and better monitoring of stressed accounts. In practical terms, it means fewer surprises on the balance sheet and lower credit risk going forward.

High Provision Coverage Adds Comfort

The Provision Coverage Ratio stood above 94 percent, offering a strong safety cushion against potential loan slippages. A high PCR reduces the probability of sudden profit shocks in future quarters.

Additionally, the absence of major divergences in asset classification under RBI supervision strengthens the credibility of reported asset quality numbers.

Segment Performance Shows Balanced Business Mix

Treasury Segment Boosts Earnings

The Treasury division played a major role in supporting profitability during the quarter. Gains from investments and bond portfolio management contributed meaningfully to overall profits.

While treasury income can fluctuate, its contribution in this quarter helped offset pressures in other segments.

Retail Banking Remains a Steady Contributor

Retail Banking delivered stable profits, backed by demand in home loans, vehicle loans, and personal finance. Retail loans typically offer better risk-adjusted returns and are less vulnerable to large defaults.

This segment’s performance highlights the gradual shift of PSU banks toward a more retail-oriented lending model.

Wholesale Banking Faces Selective Stress

The Wholesale Banking segment reported a loss during the quarter. However, this should be seen in the context of a cautious stance toward large corporate exposures.

Rather than chasing volume, the bank appears focused on asset quality, even if it means short-term pressure on profitability.

Consolidated Performance and Strategic Changes

On a consolidated basis, Canara Bank posted a net profit of over ₹5,250 crore for Q3 FY26. This includes contributions from associate companies such as Canfin Homes and Canara Robeco Asset Management.

During the quarter, the bank reclassified certain entities from subsidiaries to associates following stake dilution through Offer for Sale. This move unlocked value and resulted in a notable one-time gain at the consolidated level, improving overall shareholder returns.

Capital Position Strengthens Growth Visibility

Canara Bank’s capital adequacy ratio under Basel III norms stood at a healthy 16.50 percent, with CET-1 capital above 12 percent. These levels provide ample headroom for future loan growth without immediate dilution concerns.

The successful raising of Additional Tier 1 bonds during the quarter further reinforced the balance sheet. A strong capital base is especially important as credit demand gradually picks up across sectors.

Regulatory Comfort and Risk Management

The bank confirmed that there were no defaults on loans or debt obligations during the quarter. It also noted that the implementation details of new labour codes are awaited, and any financial impact will be assessed once clarity emerges.

Such disclosures reflect improved transparency and governance standards, which are increasingly important for institutional and retail investors alike.

What Canara Bank Q3 FY26 Results Mean for Investors

From a market perspective, Canara Bank’s performance reinforces the broader narrative that PSU banks are no longer just turnaround candidates. Many are now delivering consistent profits with manageable risk.

For equity markets, stable bank earnings support index strength, given the heavy weight of financial stocks. For retail investors, the results underline the importance of tracking asset quality trends rather than focusing solely on profit growth.

Tracking Bank Stocks with Research-Driven Support

Analysing banking results requires a clear understanding of financial ratios, regulatory norms, and economic context. This is where a structured research approach becomes essential.

Swastika Investmart, a SEBI-registered intermediary, offers robust equity research tools, detailed result breakdowns, and investor education initiatives. Its tech-enabled investing platform and responsive customer support help investors navigate complex market data with confidence.

Open your trading and investment account today

Frequently Asked Questions

How did Canara Bank perform in Q3 FY26?

The bank reported strong profit growth, improved asset quality, and stable core income during the quarter.

Is the improvement in NPAs sustainable?

The consistent decline in Gross and Net NPAs over multiple quarters suggests structural improvement rather than a temporary trend.

Which segment contributed the most to profits?

The Treasury segment was a major contributor, while Retail Banking provided stable support.

Does Canara Bank have sufficient capital for growth?

Yes, its capital adequacy ratios are well above regulatory requirements, offering growth flexibility.

How should investors view PSU banks after these results?

Investors may consider PSU banks as part of a diversified portfolio, focusing on asset quality and earnings consistency.

Final Thoughts

Canara Bank’s Q3 FY26 results highlight a bank that is steadily strengthening its foundations rather than chasing short-term gains. With improving asset quality, stable income streams, and a strong capital position, the bank reflects the broader recovery underway in India’s PSU banking space. For investors seeking disciplined exposure to financial stocks, staying informed through research-backed platforms like Swastika Investmart can add meaningful value.

Open your trading and investment account today

Smart investors do not just follow the news. They understand it.

.avif)

.avif)

.avif)