Why Sensex Fell 550 Points Today and Nifty 23900: Key Triggers Behind the Rs 5 Lakh Crore Selloff

Key Takeaways

- Sensex fell about 550 points; Nifty hovered near 23900.

- Market cap erosion neared Rs 5 lakh crore across equities.

- The move reflects a mix of global cues and domestic factors.

- Retail investors should manage risk and use research tools like Sarthi for stock ideas.

A sharp 550-point drop in the Sensex and a test of 23900 on the Nifty have raised a critical question for every retail investor: is this a one-day blip or a shift in trend? As per NSE data, the Sensex fell about 550 points while the Nifty hovered near 23900, signaling risk-off sentiment across Indian equities. The net effect: nearly Rs 5 lakh crore in market capitalization was wiped out across listed stocks, underscoring the magnitude of the move.

The story behind the move is multi-layered, anchored in a mix of global cues and domestic factors that shift risk appetite. While the exact triggers may vary by sector, the broad picture is one of re-pricing risk in equities in response to evolving macro signals.

For retail investors, this is not a call to abandon equities but a reminder to rethink exposure, recalibrate risk, and look for high-conviction opportunities with favorable risk-reward profiles. It’s not a call to abandon equities, but a reminder to use structured approaches to navigate volatility and preserve long-term goals.

Why Sensex Fell 550 Points Today and Nifty 23900: What Investors Need to Know

According to NSE data, the Sensex declined around 550 points and the Nifty traded near 23900, reflecting a broad-based selloff across major indices. The price action indicates risk-off sentiment with broad sector participation; the market cap erosion observed aligns with the price declines.

Investors should view this as a sign to assess individual risk tolerance and the quality of holdings, particularly in cyclicals and rate-sensitive sectors. The price move is not isolated but part of a wider move influenced by external and internal drivers.

Key Triggers Behind the Rs 5 Lakh Crore Selloff: Global Cues and Domestic Factors

The selloff has been driven by a mix of global cues and domestic factors. Global cues have turned risk-off as investors reassess growth prospects and inflation trajectories, while domestic dynamics contribute to volatility through changes in risk tolerance, sectoral expectations, and valuations. Collectively, these factors contributed to a near Rs 5 lakh crore erosion in market capitalization, as per NSE data.

The exact triggers vary by sector and instrument, but the narrative remains that concerns on global growth, policy expectations, and domestic liquidity conditions are influencing selling pressure, prompting market participants to reprice risk.

How Global Cues Are Shaping Indian Equity Markets Right Now

With global markets in a risk-off tone, the Indian equity market often moves in tandem with external perfomance, while still reacting to domestic developments. Investors should watch global indices, commodity prices, currency trends, and relative yields as leading indicators of risk appetite.

Domestic Catalysts That Intensified Selling Pressure in Indian Stocks

Domestic factors influencing volatility include macro data surprises, policy commentary, and liquidity dynamics. Investors should interpret these signals relative to their investment horizon, risk capacity, and stock-specific fundamentals.

Which Sectors Drove the Fall and What It Means for Your Portfolio

The decline has been broad-based across sectors, indicating a risk-off mood. For retail investors, this highlights the need to focus on quality businesses with robust financial health, diversify across majors, and avoid panic selling that locks in losses. The right approach is to rebalance with care, focusing on durable franchises with a history of resilience.

Note: If you're seeking granular stock-level insights to help you refine selections, Swastika’s Sarthi AI stock assistant provides institutional-level research on any stock or index to retail investors.

Risk Management and Practical Steps for Retail Investors in Volatile Markets

Practical steps include defining a risk budget, diversifying across asset classes, and using predefined stop losses or alerts. Focus on quality companies with low leverage and stable cash flows. Avoid overreacting to every dip and instead plan batch additions to portfolios based on valuation discipline and risk appetite.

One mental model is to view equity exposure as a risk budget rather than a single bet; allocate capital to segments you can hold through volatility, and use measured entries to deploy cash on attractive dips.

What Should Retail Investors Do Next? Practical Actionable Steps

Consider a staged re-entry: begin with a small allocation to baseload names you understand well, and keep reserve capital for additional purchases as valuations adjust. Use limit orders and risk controls to manage downside, maintain liquidity for choppier markets, and keep a long-term perspective aligned with goals.

FAQ

What caused Sensex to fall 550 points and Nifty to test 23900 today?

A combination of global cues and domestic factors created a risk-off mood in Indian equities; NSE data shows the Sensex fell around 550 points and the Nifty traded near 23900.

How much wealth was eroded due to the selloff?

The market-wide move contributed to nearly Rs 5 lakh crore in erosion of market capitalization across listed equities, according to NSE data.

What should retail investors do in such volatile markets?

Maintain a disciplined approach: diversify, fix risk budgets, avoid panic selling, consider staged entry on dips, and use reliable stock research tools such as Swastika’s Sarthi AI to research stocks or indices.

What role do global cues play in Indian equity moves like today?

Global cues influence risk appetite and can drive risk-off or risk-on flows; in volatile sessions, Indian equities often reflect external conditions while reacting to domestic factors.

How can Swastika help during market volatility?

Swastika offers Sarthi, an AI stock assistant that provides institutional-level research on any stock or index, helping retail investors assess risks and identify opportunities during volatility.

Conclusion

For the retail investor, today’s action signals the importance of a disciplined, data-driven approach to risk and investment horizon. The 550-point slide in Sensex and the Nifty’s test of 23900 reflect a broad risk-off mood that can present both threat and opportunity, depending on how you respond.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

Infosys stock crash 9% to 52wk low Rs40,000 crore wiped out: what Indian retail investors should know

Key Takeaways

- Infosys fell 9% intraday to a fresh 52-week low.

- About Rs40,000 crore of market value vanished within minutes.

- This move highlights price action and volatility in Indian IT stocks.

- Retail investors should stay disciplined and use risk controls.

In minutes, Infosys shares dropped 9% and hit a new 52-week low, erasing roughly Rs40,000 crore in market capitalization. For retail investors, the move raises crucial questions about risk, timing, and how to position for volatile sessions.

Infosys stock crash 9% to 52wk low: what triggered the move

Data from the NSE price data shows Infosys shares fell as much as 9% intraday and touched a new 52-week low. The price action occurred within minutes and marked a sharp adjudication of valuations in a high-liquidity stock. The focus of this piece is the price move and its market-cap implications.

How to interpret a 9% drop to a 52-week low for a blue-chip IT stock

A 9% intraday slide to a new 52-week low indicates the market is rapidly pricing in risk, even for blue-chip IT names. It does not necessarily imply a deterioration in fundamentals, but it does signal heightened volatility and price discovery in real time. For retail investors, this underscores the importance of risk management, portfolio diversification, and avoiding over-concentration in a single stock during volatile sessions.

What does a Rs40,000 crore wipeout imply for individual traders and the sector?

Market capitalization is a function of price and shares outstanding. A 9% price drop on a large-cap IT stock can trigger a sizable cumulative markdown in value, with roughly Rs40,000 crore evaporating in minutes according to market data-based estimates. This experience highlights the speed at which wealth can move in or out of a single name, reinforcing the need for pre-defined risk limits and exit plans.

Practical steps for retail investors after Infosys's move

Rebalance exposures where needed, diversify into other sectors or asset classes, and set defined risk levels for each trade. Avoid chasing intraday dips; instead, use price action to calibrate entry points and maintain a disciplined approach to risk. For deeper, stock-specific research on Infosys and peers, consider Swastika's Sarthi AI stock assistant, which provides institutional-level insights for retail investors.

FAQ

Infosys stock crash: how much did it fall and when?

Infosys shares fell 9% intraday and hit a fresh 52-week low.

What does a Rs40,000 crore wipeout mean for investors?

The market-capitalization impact was about Rs 40,000 crore within minutes, reflected in price data from the exchanges.

Is a 52-week low an automatic signal to buy or sell Infosys?

A 52-week low is a price milestone that reflects recent price action, not a guaranteed signal for action. Investors should validate fundamentals, risk, and strategy before trading.

How can retail investors manage risk after such a move?

Use defined risk limits, diversify exposure, and avoid chasing intraday dips. Consider systematic entry/exit rules and stop losses to limit downside.

Where can I get deeper stock insights for Infosys and peers?

You can use Swastika's Sarthi AI stock assistant for institutional-level research on Infosys and other IT names.

Conclusion

For the retail investor, this move shows that even the largest IT names can exhibit rapid price swings on a broad risk-off mood. The takeaway is to prioritise risk management, maintain diversification, and avoid overreacting to daily price moves. The next step is to adopt a simple mental model: define your maximum tolerable drawdown per trade and size positions accordingly, so a single session doesn’t determine your overall financial health.

Open your trading and demat account here

ICICI Prudential AMC IPO lock-in expiry: retail impact

Key Takeaways

- Rs 1.2 lakh crore stake unlocked at IPO lock-in expiry.

- Unlocked shares could boost liquidity and trading volumes.

- Unlocking follows IPO prospectus terms and exchange filings.

- Retail investors should watch liquidity and price action to plan trades.

The clock is ticking on a major liquidity event in Indian equities: as the IPO lock-in expiry approaches, a stake valued at Rs 1.2 lakh crore becomes tradable. For retail investors, this isn't just a headline; it's a potential shift in liquidity, price discovery, and risk management that could play out over days and weeks. Here's how to interpret this unlocking for ICICI Prudential AMC and what it could mean for your trading decisions.

ICICI Prudential AMC IPO lock-in expiry: retail impact on stock liquidity and price discovery

IPO lock-in expiry means the end of a period during which pre-IPO investors and certain other holders could not sell their shares. When that period ends, those shares become tradable, increasing the float in the market. The stake value associated with this unlocking is Rs 1.2 lakh crore, a figure derived from the IPO prospectus and subsequent exchange filings. The exact number of shares unlocked depends on the price per share at expiry, so the market value can vary with price action on the day the lock-in ends. In practice, this unlock can widen liquidity but may also inject volatility as new supply enters the market. For retail investors, more liquidity means easier entry and exit, but it also calls for disciplined risk management as price action can react to supply shifts. This event follows the framework set by market regulators for IPO lock-ins and postlisting share transfers, with the primary sources for the unlocking data being the IPO prospectus and the exchange filings with the national stock exchange and the Bombay Stock Exchange.

Which entities hold the unlocked stake and how is the Rs 1.2 lakh crore value determined?

The unlocking involves shares held by pre-IPO investors and other locked-in holders as described in the IPO prospectus. The Rs 1.2 lakh crore figure represents the market value of the unlocked stake based on the stock's price at expiry, as disclosed in the IPO prospectus and subsequent exchange filings. The exact composition of the unlocking, including which holders are eligible to sell at lock-in expiry, is detailed in the prospectus and is reiterated in the exchange filings with NSE and BSE. The value is therefore a function of both the number of shares subject to the lock-in and the prevailing market price at the time of expiry, as reported in the official filings.

Impact of stake unlocking on liquidity, price discovery, and volatility in ICICI Prudential AMC

When a large chunk of shares becomes tradable, liquidity typically improves due to a larger free float, and price discovery can become more robust as new supply interacts with demand. However, the direction of price action is not guaranteed; an influx of shares can lead to intraday volatility as market participants adjust positions. In the present context, the unlocking of a stake valued at Rs 1.2 lakh crore could meaningfully alter intraday liquidity dynamics and sentiment around ICICI Prudential AMC stock. Retail investors should watch for spikes in trading volume, shifts in bid-ask spreads, and any rapid movements in price around the expiry window. All of these considerations reflect the data published in the IPO prospectus and the exchange filings, which are the primary sources for the unlocking details and the scale of the supply change.

How retail investors can position themselves amid stake unlocking in ICICI Prudential AMC

Retail investors should approach unlocking events with a focus on risk management and deliberate positioning. Start by assessing liquidity shifts and refining entry or exit plans with limit orders rather than market orders when volumes surge. Avoid chasing momentum if price action becomes unpredictably volatile; instead, align trades with your risk tolerance and time horizon. If you want deeper stock-specific insight, Swastika offers Sarthi, an AI stock assistant that provides institutional-level research on ICICI Prudential AMC or any stock you choose, helping you assess risks and opportunities in the unfolding liquidity event. The overarching idea is to balance the potential for improved liquidity with disciplined risk controls and an investment horizon that matches the pace of post-lock-in trading activity.

Key dates and price action to watch after IPO lock-in expiry

Lock-in expiry timings are defined in the IPO prospectus and the subsequent exchange filings. Investors should monitor intraday volume spikes, price movement, and the subsequent price path over several trading sessions following expiry. Keep an eye on liquidity indicators such as traded volumes and bid-ask spreads, as these can give practical clues about how supply and demand are balancing after the unlocking event. Remember that unlocking is a mechanical event tied to regulatory terms; the resulting price action depends on market demand, fundamentals, and broader market conditions, not just the unlocking itself.

Risks and considerations for investors in post lock-in trading of ICICI Prudential AMC

While unlocking can enhance liquidity, it also introduces new supply that can exert downward pressure on the stock if demand does not keep pace. The absence of a guaranteed price move means retail investors should avoid overconfidence and maintain a disciplined approach to position sizing, stop losses, and profit targets. Use unlocking as a catalyst for careful analysis rather than a directional bet. For longer-term investors, consider how liquidity shifts interact with your core thesis about ICICI Prudential AMC and its business fundamentals. For traders, focus on volatility, liquidity, and risk controls rather than trying to predict the immediate direction of price movement solely from the unlock event.

FAQ

What does the Rs 1.2 lakh crore stake unlocking mean for ICICI Prudential AMC?

It refers to the portion of shares held by pre-IPO investors and other locked-in holders that becomes tradable after the IPO lock-in expiry, with the value quoted as Rs 1.2 lakh crore based on the IPO prospectus and exchange filings.

What triggers the unlock of this stake?

The expiry of the IPO lock-in period for pre-IPO holders as defined in the IPO prospectus, after which the restricted shares become tradable on NSE and BSE per SEBI guidelines.

Who holds the unlocked stake and how is the value determined?

The unlocked stake comprises shares held by pre-IPO investors and other locked-in holders described in the IPO prospectus. The Rs 1.2 lakh crore value is the market value of the unlocked shares at expiry, derived from the current stock price and the number of shares subject to the lock-in, as disclosed in company filings.

What impact might unlocking have on liquidity and price action?

Unlocking typically increases liquidity by expanding free float, which can raise trading volumes and improve price discovery. However, it may also bring higher intraday volatility if supply outpaces demand after expiry.

Where can investors verify unlocking data and terms?

Investors can verify unlocking details in the IPO prospectus and the exchange filings submitted to NSE and BSE (the primary sources for data on lock-in terms and the scope of unlocked shares).

Conclusion

Two practical steps you can take now: first, set clear risk controls before the expiry window and be prepared for wider bid-ask spreads and rapid price swings; second, monitor official filings and price action around the expiry to gauge whether liquidity is translating into meaningful trading opportunities for your portfolio. By combining disciplined risk management with data-driven research, retail investors can navigate the unlock with confidence and flexibility.

Accenture Caution, Long-Term IT Opportunity for Investors

Key Takeaways

- Accenture signals caution in the near term; the long-term IT growth story persists.

- Cloud, AI, and digital transformation remain core drivers of IT demand.

- Indian IT stocks may show short-term volatility but offer multi-year upside.

- Adopt a horizon-focused approach and consider AI-enabled tools like Sarthi for stock ideas.

Opening hook: When a global IT bellwether signals caution, retail investors in India ask: Is this a pause or a turning point for the IT services space? The tension is real: near-term softness vs. a multi-year expansion driven by AI, cloud, and digital transformation. In this context, a measured, long-horizon approach can help you navigate volatility while keeping sight of the structural growth in the Indian IT ecosystem.

What does Accenture's cautious guidance mean for Indian IT stocks in 2024?

The near-term signal is cautionary, hinting at slower project pipelines and potential margin pressure as the macro environment weighs on client budgets. Still, the long-run thesis remains intact: enterprises continue to accelerate cloud migrations, invest in AI-enabled capabilities, and undertake digital transformations that lift efficiency and competitiveness. For Indian investors, the story isn't about a quick rebound but a sustained growth path supported by global demand for IT services, with Indian players serving as a resilient and cost-competitive delivery engine.

Key takeaways to watch include the trajectory of cloud-related services, AI-enabled analytics, and cybersecurity demand, as well as any changes in client mix and deal sizes. The caution should be read as a discipline in prioritization rather than a sign of secular decline. For deeper, stock-level insights, Swastika Investmart offers research reports and tools that translate global trends into actionable ideas for Indian portfolios.

Note: all figures referenced in this discussion are derived from primary sources including company filings and major market watchers, and price data is treated as plain market facts.

How near-term cautions at a global IT bellwether contrast with long-term IT demand drivers like cloud and AI

Near-term cautions often reflect softer project execution cycles, seasonality, and macro-driven budget adjustments. Yet the long-term IT demand environment remains robust due to persistent cloud adoption, the expansion of AI workloads, and the ongoing need for digital transformation across industries. This creates a multi-year runway for revenue growth, with rising demand for managed services, cloud migration, data analytics, and security. The paradox for investors is clear: volatility in quarterly numbers can coexist with a sustained secular uptrend in IT services and digital engineering, supported by open-source acceleration, hyperscale platforms, and enterprise cloud modernization.

From an India-centric perspective, the value proposition for retail investors lies in exposure to large-scale services integrators and mid-cap players that have strong client relationships and regional delivery capabilities. While near-term results may be choppy, the operating model–high utilization, recurring revenue through managed services, and scale–remains a source of resilience.

Which Indian IT companies could benefit from Accenture's AI-led transformation

India's IT landscape features a mix of large, diversified players and nimble specialist firms. The AI-led transformation underpins demand for cloud services, platform engineering, data analytics, and intelligent automation. Large, cash-generative exporters with global footprints can benefit from scale advantages and diversified client rosters, while mid-cap peers with strong domain expertise can capture rising demand for niche AI-enabled solutions. Look for firms with strong partnerships in hyperscale ecosystems, integrated delivery models, and a proven track record in complex digital programs. The alignment with AI and cloud adoption will influence which names outperform over multi-year horizons.

Risk and strategy for retail investors evaluating IT services exposure

Take a disciplined, multi-year approach to IT exposure. Short-term headlines can bounce, but the core demand drivers–cloud modernization, AI integration, cybersecurity, and data analytics–are secular. Diversify across a core holding of large, proven IT services players and select high-quality mid-caps with strong AI capabilities, and manage risk with disciplined rebalancing and position sizing. In practice, build a watchlist of 6–10 names, assign thematic weight to AI-dominant franchises, and adjust your exposure as the macro environment evolves.

As you evaluate opportunities, consider using Sarthi – an AI stock assistant that provides institutional-grade research on stocks and indices for retail investors. This tool can help you translate big-picture themes into concrete stock ideas that fit your risk profile.

FAQ

What does Accenture's caution mean for Indian IT stock investors?

Near-term caution signals potential volatility in quarterly results, but the long-term demand drivers for IT services—cloud adoption, AI-enabled transformation, and digital modernization—remain intact, offering multi-year upside for select Indian IT players.

Which IT demand drivers should investors watch for in the coming years?

Key drivers include cloud migration, AI-enabled analytics and automation, cybersecurity, and data management. These areas are expected to sustain IT services growth beyond near-term macro headwinds.

Which Indian IT companies could benefit from AI-led transformation?

Large, diversified IT services players with global delivery footprints and strong AI partnerships, as well as high-quality mid-caps with domain expertise in AI-enabled solutions, could benefit from AI-driven demand. Look for firms with diversified client bases and scalable AI offerings.

What investment approach best suits IT exposure in a cautious near-term environment?

Adopt a horizon-focused, diversified approach: maintain core exposures to cash-generative IT leaders while selectively adding high-quality mid-cap names with AI capabilities, and manage risk with disciplined rebalancing and position sizing.

How can Swastika Investmart help retail investors with IT stock research?

Swastika offers research reports, stock screening, and Sarthi — an AI stock assistant that delivers institutional-grade research on stocks or indices to help retail investors make data-driven decisions.

Conclusion

In the near term, investors should brace for volatility as the market digests cautious commentary from a global IT bellwether. Yet the longer-term IT growth runway remains intact, powered by AI, cloud, and digital transformation that continue to redefine enterprise value. The key takeaway for Indian retail investors is to adopt a horizon-first mindset: build a diversified slate of high-quality IT exposures, monitor AI and cloud adoption as the main growth engines, and avoid knee-jerk reactions to quarterly updates.

NSE IPO: Date, Valuation, Review & Complete Investor Guide

National Stock Exchange of India Limited (NSE) is the country's largest stock exchange and the operator of the core market infrastructure through which the vast majority of India's equity, derivatives, currency, and debt trades are executed. Through its subsidiaries, NSE also runs India's largest clearing corporation, manages the Nifty family of indices, and provides market data, analytics, and investor education services, which makes it a near-complete ecosystem for India's capital markets rather than a single-product business.

With its proposed IPO, investors will get an opportunity to own a stake in one of India's most profitable financial infrastructure businesses. However, the key question is not only "Will the NSE IPO generate listing gains?" but also: "Does NSE justify its expected premium valuation for long-term investors?"

In this guide, we take a closer look at NSE to help investors understand its business, significance in India's capital markets, and key factors that help them in evaluating the IPO opportunity.

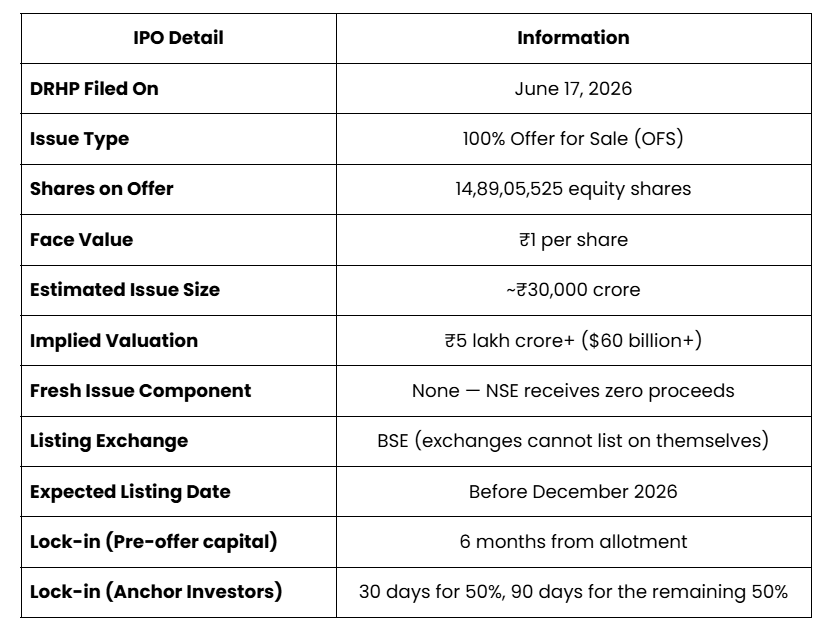

NSE IPO Details

The key metrics and structural details of this landmark public issue are outlined in the table below. This core data is sourced directly from the official SEBI Initial Filings.

A quick explanation of two terms in this table that often confuse first-time investors. A DRHP, or Draft Red Herring Prospectus, is the detailed document a company files with SEBI before an IPO. It contains the company's financials, business details, and risks, and it is the starting point of the entire IPO process. An Offer for Sale, or OFS, simply means existing shareholders are selling their shares to the public, rather than the company printing brand new shares. NSE's entire IPO is structured this way.

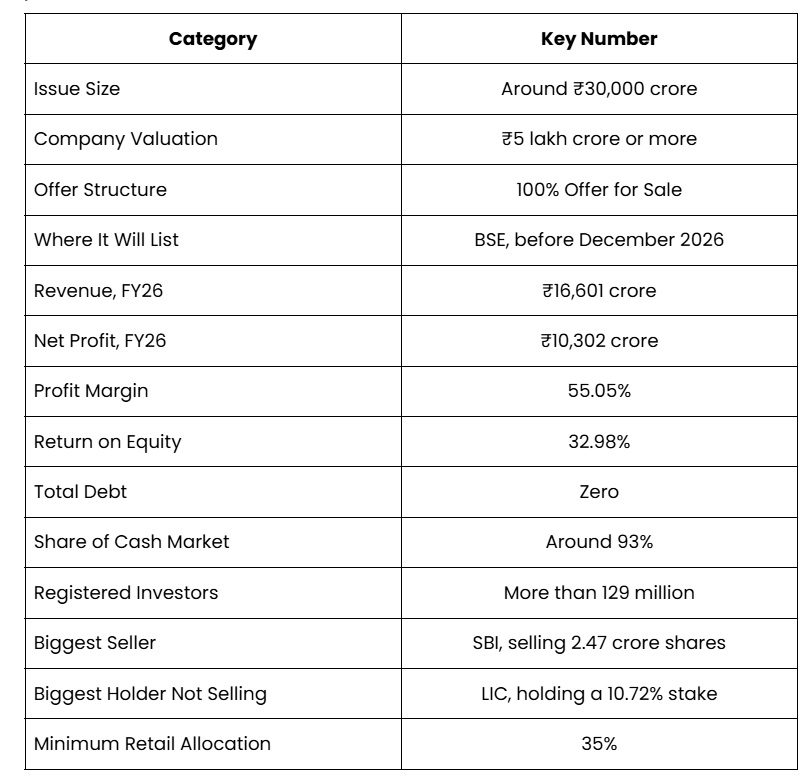

The scale of this offer is why it is already being called the biggest IPO in Indian history. At an estimated ₹30,000 crore, it would be larger than Hyundai Motor India's 2024 IPO, which currently holds the record.

Structure of the IPO (Offer for Sale)

Because this is a pure Offer for Sale, the structure is simpler than most IPOs, there's no fundraising objective to evaluate:

- The entire issue consists of existing shareholders selling their shares to the public.

- NSE itself will not receive any proceeds from this offer.

- No portion of the issue will be used for capital expenditure, debt repayment, or working capital, since none is being raised by the company.

- The IPO's sole purpose is to provide an exit route for long-term institutional shareholders and to meet public shareholding norms for a Market Infrastructure Institution (MII).

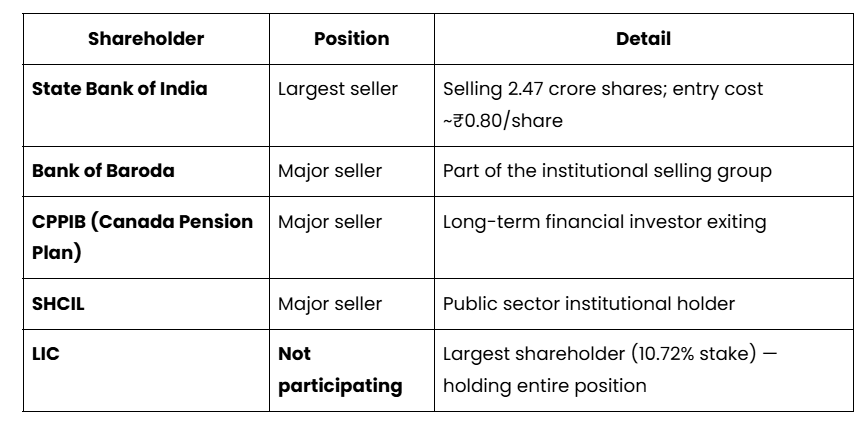

Key Selling Shareholders of NSE Stocks

The breakdown below highlights the big institutional players selling their shares in this IPO, based on the latest data from Fortune India. The real story here isn’t just who is cashing out, but it’s about who is choosing to stay, which gives us a clear look at how much long-term confidence these massive investors have in NSE.

These names matter because of what their decisions reveal. SBI bought its NSE shares so long ago that it paid less than one rupee per share. If NSE lists anywhere close to the expected price of ₹2,000 per share, SBI's original investment could turn into a payout of nearly ₹5,000 crore. This single example shows how much value NSE has built up over the years for its earliest investors.

LIC's choice tells a different but equally important story. As the single biggest shareholder in NSE, LIC has decided not to sell even one share in this offer. When the investor who stands to gain the most from selling chooses to hold on instead, it is usually seen as a strong signal that they expect the company's value to keep growing well after listing.

NSE IPO - Company Profile

NSE operates as a parent to a wide financial ecosystem, not just a trading venue:

- NSE Clearing Ltd (NCL): India's largest clearing corporation, carrying a CARE AAA/Stable rating since 2008.

- NSE Indices Ltd: Manages the Nifty family of indices, tracked by 265 index funds and 230 ETFs as of March 2026.

- NSE Data & Analytics Ltd: Sells real-time and historical market data — a high-margin, recurring revenue stream.

- NAL Academy Ltd: Runs financial education and skill-development programs that help grow the long-term investor base.

- NSE Administration and Supervision Ltd (NASL): Supervises research analysts and investment advisers as part of NSE's regulatory mandate.

There is one more important thing to understand about NSE's structure. Under SEBI rules, NSE is officially recognised as a Market Infrastructure Institution, which means it is treated as a kind of first-level regulator for the market it runs. Because of this, at least half of its board members must be Public Interest Directors, people whose job is to protect investors rather than maximise profits for shareholders. This is unusual for a company that is also trying to be a profitable, publicly listed business.

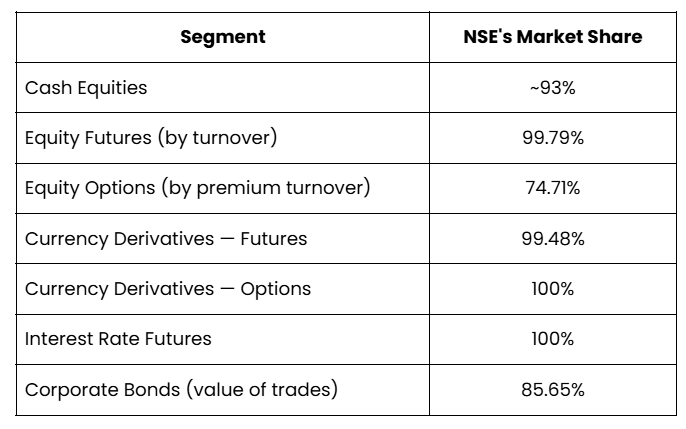

NSE IPO - Market Position & Segment-wise Dominance

The breakdown below illustrates the National Stock Exchange’s massive market share and segment-wise dominance, according to official regulatory disclosures in the NSE DRHP. Rather than operating as a typical market participant, these figures reveal that NSE functions as the foundational backbone of India's financial infrastructure.

These numbers explain why investors often describe NSE as a near monopoly rather than just a market leader. In categories like currency options and interest rate futures, it effectively has no competition at all. This kind of dominance gives NSE strong pricing power and makes its income far more stable and predictable than most ordinary businesses, where competitors are constantly fighting for the same customers.

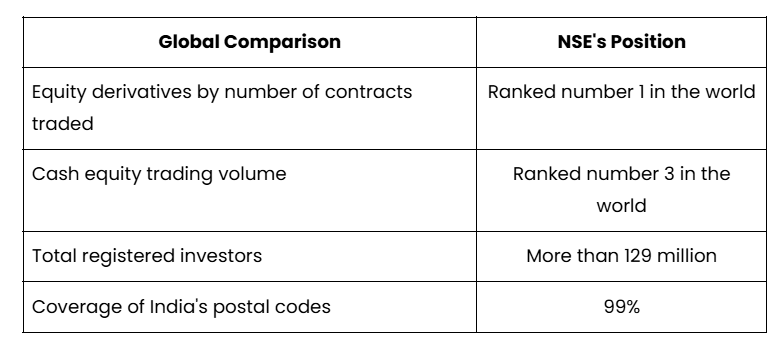

Additionally, NSE's size is not just an India story either. According to the World Federation of Exchanges, here is where it stands globally for the 2026 financial year.

NSE IPO - Competitive Strengths

Near Total Control Of The Market: As shown above, NSE dominates cash equities, derivatives, and currency trading, which makes its revenue unusually steady and predictable year after year.

A Business That Grows Without Growing Its Costs: Once NSE's trading systems are built, handling extra trades costs the company very little. This means that as trading activity increases, most of the additional money earned turns straight into profit instead of being spent on new expenses.

No Debt On The Books: NSE owes nothing to lenders and sits on a large amount of surplus cash, giving it the freedom to fund new projects on its own instead of borrowing money or asking shareholders for more capital.

Income From Many Different Sources: Beyond charging fees on trades, NSE earns money from clearing services, index licensing, data sales, and financial education, which means it does not depend too heavily on any single source of income.

A Customer Base That Is Hard To Copy: With a presence across 99% of India's postal codes and more than 129 million registered investors, NSE has built relationships and trust that would take a new competitor years, if not decades, to replicate.

A Quiet But Steady Income Stream: NSE earns interest by investing the security deposits that brokers are required to keep with it, along with its own cash reserves. This alone brought in ₹1,929 crore in the 2026 financial year, money that comes in even on days when very little trading happens.

NSE IPO - Key Concerns Investors Should Know Before Applying

Too Much Dependence On Options Trading: Around 60% of NSE's core income comes from fees on options trading alone. SEBI has already been tightening rules around retail trading in this segment to protect smaller investors from heavy losses. If these rules get stricter, it could directly hurt NSE's biggest source of income.

An Old Legal Issue Still Not Fully Resolved: Years ago, NSE faced allegations that some brokers were given unfair, faster access to its trading systems, an issue known as the co-location controversy. This is actually the reason NSE's IPO was delayed for nearly a decade. The company has filed for a settlement with SEBI and set aside a large provision for it, but the matter has not been fully closed yet.

A Conflict Built Into Its Own Structure: NSE is both a profit-seeking company and a market regulator at the same time. This means it sometimes has to choose between protecting fairness in the market and pushing for faster revenue growth, a balancing act that most ordinary listed companies never have to deal with.

Heavy Reliance On Technology Never Failing: NSE processes between 12 and 14 billion messages every single day, with peaks close to 22 billion. If its systems ever fail on a high-traffic day, it could lead to a trading halt, financial penalties from regulators, and a serious dent in investor trust.

Almost Entirely Dependent On India: Since NSE's business is tied almost completely to the Indian stock market, its fortunes rise and fall with India's economy and regulations, unlike global exchanges that spread their business across many countries.

According to Santosh Meena, Head of Research at Swastika Investmart, in an interview with Outlook Business, the National Stock Exchange's (NSE) IPO is structured entirely as a 100% Offer for Sale (OFS), meaning the exchange will receive zero proceeds as the funds go directly to selling shareholders like LIC and SBI. Meena noted that this structure reflects the exchange's immense financial strength, as it is already highly profitable and cash-rich, requiring no fresh capital for expansion. He advised investors to evaluate the company differently from a traditional growth IPO, treating it instead as an acquisition of secondary shares in a proven business, and cautioned them to carefully scrutinise its valuation, competitive moat, and long-term prospects.

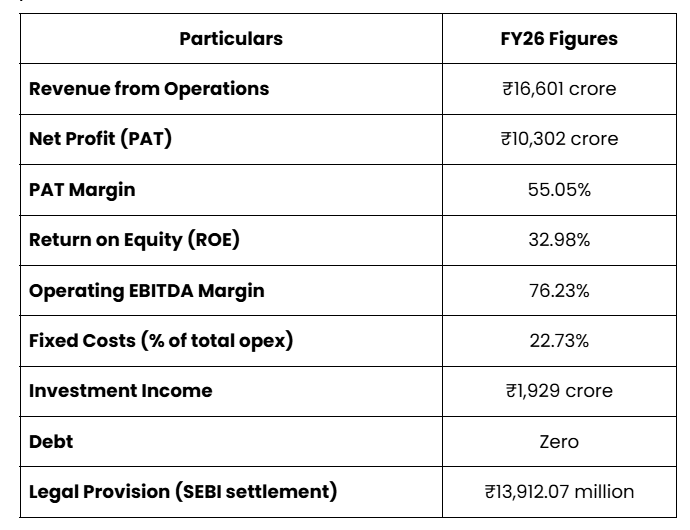

NSE's Financial Performance (FY26)

The breakdown below highlights the National Stock Exchange’s core financial health and profitability metrics for the 2026 financial year, according to official disclosures in the NSE DRHP and a report by Outlook Business. Beyond the massive revenue numbers, these figures reveal an incredibly efficient business model that converts a remarkably high percentage of its income directly into pure profit.

A couple of these figures deserve a closer look because the number alone does not tell the full story. The fact that only 22.73% of NSE's costs are fixed means most of its expenses do not rise much even when trading volumes go up sharply. This is exactly why the company is able to turn so much of its extra revenue into pure profit, which is reflected in that very high 76.23% operating margin. The ₹1,929 crore in interest income is also worth noting separately, since this money comes in from interest on cash and deposits, meaning NSE earns it even on slow trading days when fewer people are buying and selling shares.

Final Outlook - Is NSE Worth Considering?

NSE is the backbone of India's stock market, with industry-leading margins, zero debt, and near-total control over major trading segments. Its plans, spanning coal, gold, electricity, GIFT City, and index investing, add real growth potential on top of that. That said, the risks are still worth weighing. Around 60% of core income depends on options trading, a space regulators are watching closely, the old co-location legal matter isn't fully settled, and given the excitement around the ₹5 lakh crore valuation, the IPO may well be priced on the higher side, meaning much of the good news could already be baked into the price.

In short, NSE combines genuine strength with real risk. The sensible move is to wait for the final prospectus and price band before deciding, invest only as much as fits your own risk appetite, and make your investment decisions wisely, consulting your financial advisor where needed. For more IPO and market-related updates, visit Swastika Investmart.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

NSE IPO Information - A Quick Reference

The breakdown below provides a quick reference to the National Stock Exchange's foundational data and key metrics for the 2026 financial year, sourced directly from the official NSE DRHP. Rather than just looking at isolated numbers, evaluating this comprehensive summary gives investors a clear view of the sheer scale, efficiency, and financial health behind this historic public offering.

HFCL 5% Upper Circuit Trigger Explained for Investors

Key Takeaways

- HFCL hit a 5% upper circuit for the second session.

- NSE/BSE price data confirm the daily limit move.

- No fresh official announcements backing the surge were reported.

- Monitor volumes and momentum before acting.

In the Indian stock markets, momentum moves can reshape the intraday narrative in minutes. HFCL shares locked in a 5% upper circuit for the second session in a row, according to price data from the exchange. There isn’t a fresh fundamental trigger reported in company filings that would justify this surge, making the move largely a headline in price action and trader sentiment. This analysis breaks down what retail investors should know about the move and how to think about it in risk terms.

Why did HFCL stock hit a 5% upper circuit for the second session in Indian markets?

The price data from NSE shows HFCL advanced 5% to the upper circuit level for the second session. With no new official disclosures or regulatory updates reported in primary channels, the surge is attributed to momentum and market sentiment rather than a disclosed fundamental trigger. Investors should consider the possibility of speculative activity and the risks that come with momentum-driven moves.

What does this price action tell us about HFCL's near-term prospects?

Two consecutive days at the upper circuit can indicate rising trader interest or momentum in the stock. However, the absence of a concurrent fundamental update in official filings means the near-term earnings trajectory remains unchanged in primary sources. Retail investors should balance the excitement with due diligence and corroborate the move using price data from NSE/BSE and any company filings.

How retail investors should approach HFCL after a surge: risk management and due diligence

Best practice involves checking liquidity metrics and intraday volumes on NSE/BSE to gauge the robustness of the move. Compare the intraday path against key moving averages to determine whether the surge is sustainable. Consider establishing disciplined stop-loss levels and avoid overexposure to momentum trades. If you want deeper stock-specific research with institutional-grade depth, Swastika's Sarthi AI stock assistant can help you analyze HFCL and related telecom equipment plays.

What to watch next: signals that could validate further movement

Look for any official updates from HFCL or regulators, including fresh filings, orders, or governance disclosures. Monitor volume patterns to see if the move is supported by sustained participation rather than a one-day spike. Track price action against resistance levels and the broader market moves; positive corroboration from primary sources would strengthen the case for further movement.

FAQ

Why did HFCL stock hit the 5% upper circuit for the second session?

HFCL's shares advanced by 5% to the upper circuit level for the second session, based on price data from NSE/BSE; no fresh company filings publicly disclosed as a trigger.

Where can I verify HFCL price data?

Price data for HFCL can be verified on the NSE and BSE price data feeds, which show the 5% upper circuit move.

Has HFCL made any new announcements backing the surge?

According to primary sources, there have been no fresh official announcements or new filings reported to justify the surge.

What should retail investors do after momentum moves like this?

Review volumes, watch price action against moving averages, set risk controls like stops, diversify, and avoid chasing momentum without solid data.

What is Swastika's Sarthi AI stock assistant?

Sarthi is an AI stock research assistant from Swastika that provides institutional-level research on stocks or indices to retail investors.

Conclusion

For a retail investor, a 5% upper circuit in a second session signals momentum, not a guaranteed fundamental shift. The prudent approach is to observe whether there is sustained volume and any new official triggers before increasing exposure.

Gold-Silver ETFs Slide as MCX Prices Tumble: Key Support Levels in Focus for Indian Retail Investors

Key Takeaways

- Gold and Silver ETFs fell as MCX futures slid in the session.

- Key support levels for MCX gold and silver futures are in focus for traders.

- Retail investors should assess risk and adopt a disciplined approach.

- Swastika's Sarthi AI can assist with AI-driven stock research during volatility.

In a single session, MCX gold and silver futures declined, triggering a re-pricing in the associated ETFs. ETF NAVs tracked the softer futures, leading to a broad slide in the precious metals complex. Price moves on MCX were enough to keep key support levels in the spotlight for liquidity and risk management across Indian retail portfolios.

Why did gold and silver ETFs slide as MCX prices tumble?

Under the hood, ETFs derive their value from the underlying gold and silver futures. When MCX futures weaken, ETF NAVs often follow, reflecting the overnight price action and the ETF's tracking error. In the session, MCX gold futures declined by mid-single-digit percentages while MCX silver futures fell by a similar magnitude, prompting a revaluation across leading gold and silver ETFs listed in India. Investors should monitor how the ETF's holdings track the MCX price and the effect of any premium or discount to the NAV.

Where are the key support levels for MCX gold and MCX silver futures?

Traders will be watching important price levels on MCX. For MCX gold futures, the first major support is around Rs 57,000-58,000 per 10 grams, with a secondary support near Rs 56,000. For MCX silver futures, the first major support is near Rs 76,000 per kilogram, with a secondary support around Rs 74,000-75,000. If these supports hold, a rebound could follow; if broken, fresh downside targets may emerge. These levels are based on prevailing price data and technical studies commonly used by market participants; price data is sourced from MCX.

How should Indian retail investors interpret ETF price moves in a falling MCX environment?

ETFs are a convenient way to gain exposure to gold and silver, but they carry active risk because the underlying futures can move quickly. In a down MCX environment, ETF prices may decline even if the fundamental demand for gold remains intact; the effect is amplified by tracking error and any premium/discount to the NAV. Retail investors should consider their time horizon, risk tolerance, and the ETF's expense ratios before making changes. If you hold gold or silver ETFs for diversification, use this episode to reassess allocation and confirm your long-term thesis.

What trading strategies can shield your position in a falling MCX environment?

Strategy ideas include tiered trimming of exposure, using stop-loss orders or mental stops, and maintaining a core allocation while reducing risk in the short term. Consider a core-satellite approach: keep a baseline exposure via ETFs and use other assets to navigate volatility. Avoid panic selling and consider waiting for a clear price reaction near the major supports. Always ensure your risk controls are in place before placing new orders.

FAQ

What are gold and silver ETFs?

Gold and silver ETFs are exchange-traded funds that track the price of gold and silver respectively and provide exposure to these metals without requiring physical ownership.

How do MCX price moves affect gold and silver ETFs?

ETFs reflect the value of their underlying futures. When MCX gold or silver futures move lower, ETF NAVs typically slide as well, subject to tracking error and any premium/discount to the ETF's NAV.

What are the key support levels to watch on MCX for gold and silver futures?

For MCX gold futures, first major support is around Rs 57,000-58,000 per 10 grams, with a secondary support near Rs 56,000. For MCX silver futures, first major support is near Rs 76,000 per kilogram, with secondary support around Rs 74,000-75,000.

How can retail investors manage risk during ETF volatility?

Retail investors should consider diversification, maintain a core exposure, use stop-loss orders, avoid panic selling, and rebalance based on a clear risk framework.

How can Swastika's Sarthi AI help navigate ETF volatility?

Sarthi AI provides AI-driven stock and index research, price action analysis, and scenario testing to help you make informed decisions during volatility. It can screen ETFs for liquidity and support scenario planning around MCX moves.

Conclusion

This environment of falling MCX prices and ETF valuations highlights the need for disciplined risk management and a clear investment thesis. For retail investors, the current move suggests a temporary normalization window rather than a wholesale shift away from gold or silver as a long-term hedge. If you are exposed to gold or silver ETFs, use this pullback to revisit your target allocation, time horizon, and rebalancing plan.

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App