.png)

The US economy remains the single most influential force in global financial markets. From equity flows to currency movements and commodity prices, decisions taken in Washington and by the US Federal Reserve ripple across economies worldwide. As we look ahead, understanding what to expect from the US economy in 2026 becomes essential for Indian investors, traders, exporters and policymakers.

In this blog, we break down the expected economic trends in the US for 2026 and explain how these developments could shape Indian stock markets, interest rates, currency movements and investment strategies.

After years of post pandemic recovery and policy tightening, the US economy is expected to enter 2026 with stable momentum. Most global institutions expect GDP growth to remain around the long term average rather than the sharp expansion seen earlier in the decade.

Key drivers include strong consumer spending, government infrastructure investment and continued capital expenditure in technology and artificial intelligence. At the same time, high base effects and tighter financial conditions could limit rapid growth.

For Indian investors, stable US growth is generally positive as it supports global risk appetite without creating excessive inflationary pressure.

Inflation is expected to trend closer to the US Federal Reserve’s comfort zone by 2026, though it may not settle perfectly at two percent. Wage pressures, energy prices and supply chain restructuring will continue to influence price levels.

Lower inflation reduces the need for aggressive monetary tightening and supports equity markets globally.

One of the most watched elements of the US economy in 2026 will be interest rates. If inflation continues to ease, the Federal Reserve may shift towards a more accommodative stance or maintain stable rates.

For India, this matters because lower US interest rates often lead to increased foreign portfolio inflows into emerging markets like India, improving liquidity and supporting equity valuations.

The US dollar’s trajectory in 2026 will depend largely on interest rate differentials and economic confidence. A stable or slightly weaker dollar typically benefits emerging market currencies, including the Indian rupee.

A stronger rupee can help reduce imported inflation for India, especially in crude oil and raw materials. However, exporters may face margin pressure if currency appreciation becomes sharp.

Foreign Institutional Investors closely track US bond yields and equity performance. If US yields remain stable and growth continues without shocks, India is likely to attract sustained FII inflows.

Historically, periods of US economic stability have coincided with strong performance in Indian sectors such as IT, banking, capital goods and consumer discretionary.

Trade policy remains a key variable. Any shift towards protectionism or tariff changes can affect Indian exports to the US, particularly in textiles, engineering goods and specialty chemicals.

However, diversification away from China continues to create long term opportunities for Indian manufacturers under the China plus one strategy.

From an Indian regulatory standpoint, SEBI continues to emphasize transparency, investor protection and risk management. Global volatility originating from the US economy reinforces the importance of disciplined investing, asset allocation and regulatory compliance.

Platforms like Swastika Investmart, a SEBI registered intermediary, play a crucial role by offering research backed insights, technology driven trading platforms and investor education that helps clients navigate global uncertainty confidently.

👉 Open your trading and investment account today

Long term wealth creation depends on staying invested with a clear strategy rather than timing global events perfectly.

How will the US economy in 2026 affect Indian stock markets?

A stable US economy usually supports global risk appetite, leading to better FII inflows and positive sentiment in Indian equities.

Will US interest rate changes impact Indian investors?

Yes. Lower or stable US rates often encourage foreign investments into India, improving liquidity and market valuations.

Which Indian sectors are most influenced by the US economy?

IT, pharmaceuticals, metals and export oriented manufacturing sectors are most sensitive to US economic trends.

Is a weaker US dollar good for India?

Generally yes, as it supports the rupee and reduces import costs, though exporters may face some pressure.

Understanding what to expect from the US economy in 2026 is essential for making informed investment decisions in India. While global uncertainties will always exist, a balanced US growth outlook combined with easing inflation could create a supportive environment for Indian markets.

With expert research, robust trading platforms and strong customer support, Swastika Investmart helps investors stay ahead of global trends while focusing on long term financial goals.

Crude oil prices slipping to a four-year low has caught global markets off guard. For an asset that often reacts sharply to geopolitical risks, supply disruptions, and economic cycles, this sustained decline signals a deeper shift in global demand and supply dynamics.

Brent crude and WTI have both corrected significantly from their earlier highs. Unlike short-lived volatility, this fall reflects a combination of macroeconomic slowdown, rising production, and structural changes in energy consumption.

For Indian investors, crude oil movements matter more than headline inflation data. India imports over 80 percent of its crude oil requirements, making oil prices a powerful lever for the economy, corporate earnings, and market sentiment.

One of the biggest reasons behind falling crude prices is slowing global demand. China, the world’s largest oil importer, has seen weaker industrial activity and slower recovery than expected. Manufacturing data from Europe also points to contraction rather than expansion.

When large economies consume less fuel, oil inventories build up quickly, putting pressure on prices. Airlines, shipping companies, and heavy industries are all using less energy than they did during the post-pandemic rebound phase.

While demand has softened, supply has remained resilient. The US continues to produce crude at near-record levels. Shale producers have become more efficient and can sustain output even at lower prices.

At the same time, OPEC+ supply cuts have not been aggressive enough to offset global oversupply. Some member nations continue producing above quotas due to fiscal pressures, adding further weight on prices.

Crude oil is priced in US dollars. A strong dollar makes oil more expensive for non-US economies, dampening demand further. Tight monetary policies in developed markets have reduced liquidity, limiting speculative buying in commodities.

This environment discourages large funds from taking aggressive long positions in oil futures, keeping prices under pressure.

Longer-term factors are also at play. Increased adoption of electric vehicles, renewable energy, and energy efficiency norms have gradually reduced incremental oil demand growth. While oil is far from obsolete, markets are beginning to price in slower long-term consumption growth.

Lower crude oil prices directly reduce input costs for transportation, logistics, and manufacturing. This helps keep retail inflation under control, giving the Reserve Bank of India more flexibility on interest rates.

Stable or lower inflation improves consumer purchasing power and supports economic growth.

Cheaper crude reduces India’s import bill, improving the current account balance. It also lowers the government’s subsidy burden on fuels, LPG, and fertilizers, offering fiscal breathing room.

This macro stability is usually welcomed by equity markets.

Oil marketing companies often benefit from lower crude prices due to improved margins, provided retail fuel prices remain stable.

Aviation, paints, chemicals, cement, and FMCG companies typically see margin expansion as raw material and logistics costs fall.

On the other hand, upstream oil producers may face earnings pressure due to lower realizations, although currency movements and government policies can soften the impact.

Trying to time the bottom in crude oil prices is risky. Commodity prices are influenced by unpredictable geopolitical and macro factors. Retail investors are often better served by indirect exposure rather than direct futures trading.

Lower oil prices act like a tax cut for oil-importing economies. Investors can look at sectors that benefit structurally from cheaper energy rather than betting on oil prices themselves.

For example, logistics-heavy businesses, consumer-facing companies, and industrials with high fuel dependency may see sustained margin improvement.

Fuel pricing policies, excise duties, and subsidies play a big role in determining how much benefit flows to corporates and consumers. Indian regulatory decisions can amplify or dilute the impact of falling crude prices.

Keeping track of policy signals is as important as tracking global oil data.

Crude oil cycles often trigger emotional reactions in markets. This is where disciplined, research-backed investing makes a difference.

Swastika Investmart supports investors with SEBI-registered research, detailed sector analysis, and tech-enabled tools that help identify real beneficiaries of macro trends rather than chasing short-term noise. Strong customer support and continuous investor education further help investors navigate such complex global developments with confidence.

Why did crude oil fall to a four-year low?

Crude oil prices fell due to weak global demand, excess supply from major producers, a strong US dollar, and structural shifts towards cleaner energy.

Is falling crude oil good for the Indian economy?

Yes, lower crude prices generally benefit India by reducing inflation, improving fiscal balance, and lowering import costs.

Which Indian sectors benefit the most from lower crude prices?

Aviation, FMCG, paints, chemicals, cement, and oil marketing companies typically benefit from lower energy and input costs.

Should investors invest in oil stocks now?

Upstream oil stocks may face pressure, while downstream and consumption-driven sectors may offer better risk-reward depending on fundamentals.

The fall in crude oil to a four-year low is not just a commodity story. It is a macro signal with wide-ranging implications for inflation, interest rates, corporate earnings, and equity markets in India.

Instead of reacting to price headlines, investors should focus on how lower crude reshapes sector profitability and long-term growth trends. With the right research framework and disciplined strategy, such macro shifts can become meaningful portfolio opportunities.

If you want to invest with clarity backed by strong research, smart tools, and reliable support, Swastika Investmart offers a robust platform for informed investing.

The Indian insurance sector is back in the spotlight as the Lok Sabha takes up the Insurance Amendment Bill today. For investors, this is more than just a regulatory update. It is a potential structural shift that could reshape how insurance companies raise capital, expand distribution, and improve profitability.

India’s insurance penetration remains significantly lower than global averages despite a large underinsured population. Policymakers have repeatedly highlighted insurance as a critical pillar for financial inclusion and long-term economic stability. This amendment is part of that broader reform agenda.

Markets typically react not only to the passage of such bills but also to the tone of discussions and clarity on implementation timelines. That is why insurance stocks, brokers, and related financial services companies are being closely tracked today.

While the final contours will be clear after parliamentary debate, the Insurance Amendment Bill is widely expected to focus on three major areas.

One of the most discussed aspects is easing foreign investment norms in insurance companies. Earlier reforms already raised the FDI limit, and further flexibility could help insurers attract global capital, advanced underwriting practices, and better risk management systems.

The bill aims to reduce operational friction by streamlining compliance requirements. A more predictable regulatory environment can improve return ratios and reduce cost burdens, especially for fast-growing private insurers.

Digital distribution, embedded insurance, and micro-insurance products are expected to get regulatory support. This aligns with the government’s broader push towards tech-enabled financial services.

Private life insurers could be among the biggest beneficiaries. Access to foreign capital can support expansion into Tier 2 and Tier 3 cities, product innovation, and digital onboarding. Over time, this may improve persistency ratios and margins.

Public sector insurers may see slower immediate gains but could benefit indirectly from sector-wide growth and improved consumer awareness.

General insurers stand to benefit from regulatory clarity and product expansion. Segments such as health insurance and motor insurance are already growing rapidly, and easier capital access can help companies scale underwriting capacity.

Insurance brokers, web aggregators, and corporate agents may gain from simplified rules and higher product penetration. As insurers expand their offerings, intermediaries often see volume-led growth without heavy balance sheet risks.

A growing insurance sector boosts long-term domestic capital formation. This can indirectly benefit asset management companies, market-linked products, and capital markets over time.

Investors should track companies with strong execution history, scalable business models, and efficient distribution networks.

Private life insurers with diversified product portfolios may see valuation re-rating if reforms translate into sustained growth.

Listed general insurers with focus on retail health and motor insurance could benefit from rising premium income and better pricing power.

Insurance brokers and platform-based players may attract investor interest due to their asset-light nature and operating leverage.

As always, stock-specific outcomes will depend on earnings quality, solvency ratios, and management execution rather than policy announcements alone.

Historically, insurance reforms have led to short-term volatility followed by medium-term re-rating when growth visibility improves. If the Insurance Amendment Bill provides clear timelines and implementation certainty, insurance stocks could outperform broader indices in the coming quarters.

From a macro perspective, a stronger insurance sector supports household financial security and long-term savings, which is structurally positive for Indian markets.

Retail investors should avoid chasing sharp intraday moves purely based on news flow. A better approach is to assess companies with consistent premium growth, improving combined ratios, and strong governance.

This is where research-backed investing becomes crucial. Platforms like Swastika Investmart help investors navigate such policy-driven themes through SEBI-registered research, sector reports, and data-backed stock insights rather than speculation.

What is the Insurance Amendment Bill about?

The bill aims to modernise India’s insurance laws by improving capital access, simplifying regulations, and encouraging innovation in insurance products and distribution.

Will insurance stocks react immediately to the bill?

Short-term market reactions are possible, but sustainable stock performance will depend on earnings growth and execution after the reforms are implemented.

Which insurance segment benefits the most?

Private life and general insurers, along with insurance brokers, are expected to benefit more due to scalability and capital flexibility.

Is this good for long-term investors?

Structurally, a growing insurance sector is positive for long-term investors, provided stock selection is based on fundamentals.

The Insurance Amendment Bill being taken up in Lok Sabha today is a reminder that regulatory reforms often create long-term investment opportunities rather than instant gains. For investors willing to look beyond headlines, this could mark another step in India’s evolving financial ecosystem.

Navigating such sectoral shifts requires disciplined research, timely insights, and a reliable investment platform. Swastika Investmart stands out with its SEBI-registered research framework, robust analytical tools, responsive customer support, and strong focus on investor education and tech-enabled investing.

If you are looking to align your portfolio with India’s long-term financial growth story, now is a good time to get started.

India’s largest airline, IndiGo, went through a challenging phase over the past few months. Frequent flight delays, cancellations, and aircraft groundings created frustration among passengers and raised concerns among investors. Social media complaints, airport congestion, and global engine supply issues added to the pressure.

For a business that thrives on punctuality and scale, these disruptions naturally sparked the question: is this just a temporary rough patch or a sign of deeper operational stress?

The aviation sector is inherently complex. Aircraft availability, crew scheduling, weather disruptions, and global supply chain issues can quickly snowball into large-scale operational problems. IndiGo was not alone in facing these challenges, but given its market leadership, the impact was more visible.

Over recent weeks, IndiGo flights have shown clear signs of stabilisation. The airline has gradually improved on-time performance, reduced cancellations, and normalised schedules across major domestic routes. Passenger feedback has also turned relatively positive compared to the peak disruption period.

IndiGo’s management has taken corrective steps, including better aircraft rotation planning and closer coordination with airport operators. These efforts are crucial in a country like India, where air traffic continues to rise sharply post-pandemic.

With India now among the fastest-growing aviation markets globally, operational stability is not just a short-term fix but a necessity for sustaining leadership.

Despite short-term turbulence, the long-term demand story for Indian aviation remains intact. Rising disposable incomes, expanding middle-class travel, corporate mobility, and regional connectivity under the UDAN scheme continue to support air travel growth.

IndiGo, with its extensive domestic network and cost-efficient model, is well positioned to benefit from this trend. High passenger load factors indicate that demand has not weakened even during operational hiccups.

From a market perspective, strong demand helps airlines absorb temporary shocks faster, provided cost controls remain disciplined.

While flight operations are improving, cost pressures remain a reality. Aviation turbine fuel prices, currency fluctuations, and maintenance costs continue to influence profitability. IndiGo’s scale provides some buffer, but margin volatility is part of the airline business.

Investors should also factor in aircraft grounding risks linked to global engine issues, which have affected multiple airlines worldwide. Regulatory oversight by the Directorate General of Civil Aviation plays a key role in ensuring safety compliance and operational discipline.

The broader Indian equity market generally reacts positively to signs of operational recovery in large consumer-facing companies. However, sustained financial performance matters more than short-term sentiment.

IndiGo continues to hold a dominant market share in India’s domestic aviation space. While competition has intensified, its low-cost structure, fleet size, and network depth provide a clear advantage.

Competitors are also expanding aggressively, but IndiGo’s ability to deploy capacity quickly and manage costs efficiently remains a key differentiator. That said, aviation is a cyclical business, and leadership positions must be defended continuously through execution.

A neutral view suggests that while competition is rising, IndiGo’s scale still offers resilience in volatile phases.

For investors tracking aviation stocks, the recent recovery in IndiGo flights offers cautious optimism. Operational normalisation reduces near-term uncertainty and improves revenue visibility.

However, aviation stocks demand patience and risk awareness. Fuel costs, global supply constraints, and regulatory compliance can impact earnings unpredictably. Long-term investors may view stability as a positive signal, while short-term traders should remain mindful of sector volatility.

Indian markets tend to reward companies that demonstrate quick corrective action, especially in consumer-driven industries like aviation.

Understanding aviation stocks requires more than tracking headlines. Investors need clarity on financial sustainability, operational execution, and regulatory developments.

Swastika Investmart, a SEBI registered entity, supports investors with in-depth research, real-time market tools, strong customer support, and continuous investor education. Whether you are tracking aviation stocks or building a diversified portfolio, access to structured insights can make decision-making more confident.

IndiGo flights resuming strong operations suggest that the worst phase of recent disruptions may be behind the airline. Improved punctuality, stable schedules, and robust demand offer reassurance. However, aviation remains sensitive to external risks, and sustained execution will determine long-term performance.

For investors, the situation calls for balanced optimism rather than blind confidence. Tracking fundamentals, costs, and regulatory developments remains essential.

If you are planning to invest or track aviation stocks more closely, consider opening an account with Swastika Investmart for research-backed insights and a tech-enabled investing experience.

Why were IndiGo flights disrupted recently?

Operational challenges such as aircraft availability, engine issues, and airport congestion contributed to delays and cancellations.

Are IndiGo flights operating normally now?

Flight operations have largely stabilised, with improved on-time performance and reduced cancellations.

Does strong demand support IndiGo’s recovery?

Yes, India’s growing air travel demand provides a strong tailwind for recovery.

Is IndiGo a long-term investment opportunity?

Long-term potential exists, but investors should consider sector volatility and cost risks.

How can investors track aviation stocks better?

Using research platforms and expert guidance, such as those provided by Swastika Investmart, helps investors make informed decisions.

KSH International is engaged in the manufacturing and export of magnet winding wires, a critical component used in motors, transformers, generators and other electrical equipment. These products play a vital role in sectors such as power transmission, renewable energy, electric vehicles, railways, industrial machinery and automotive applications.

The company offers a wide range of products including enamelled copper and aluminium winding wires, paper insulated rectangular wires, continuously transposed conductors and specialised insulated conductors. These products are supplied to large original equipment manufacturers across India and overseas markets.

What makes KSH International relevant in today’s market environment is its direct linkage to India’s long-term infrastructure story. With rising investments in power generation, EV manufacturing and renewable energy, demand for efficient and reliable magnet winding wires is expected to remain strong.

KSH International operates three manufacturing facilities in Maharashtra located at Taloja and Chakan, with a total installed capacity of 29,045 metric tonnes per annum. A fourth manufacturing facility at Supa in Ahilyanagar is under development and expected to commence operations in FY26, further strengthening capacity.

As per industry data, the company ranks as India’s third-largest manufacturer and the largest exporter of magnet winding wires in FY25. Its strong export presence provides diversification and reduces dependence on a single geography.

The company has also received quality and supplier excellence awards from reputed clients such as Toshiba T&D India, GE Power Grid and BHEL, reinforcing its credibility in a highly technical manufacturing segment.

KSH International has demonstrated consistent financial improvement over the last three years. Total income increased from ₹1,056.60 crore in FY23 to ₹1,938.19 crore in FY25, reflecting strong demand across end-use industries.

Profitability has improved steadily, with net profit rising from ₹26.61 crore in FY23 to ₹67.99 crore in FY25. EBITDA margins expanded from 4.72 percent to 6.32 percent during the same period, indicating better operating efficiency and cost control.

Return on equity for FY25 stands at a healthy 22.77 percent, which is higher than many listed peers in the magnet wire segment. This reflects effective capital utilisation and disciplined execution by the management.

The KSH International IPO is a book-built issue with a price band of ₹365 to ₹384 per share. The issue opens for subscription on December 16, 2025 and closes on December 18, 2025. The shares are proposed to be listed on both BSE and NSE.

The total issue size is ₹2,601.82 crore, consisting of a fresh issue of ₹710 crore and an offer for sale of ₹1,891.82 crore. The face value of each share is ₹5 and the market lot is 39 shares.

Post issue, the company’s market capitalisation is estimated at approximately ₹2,602 crore at the upper price band.

The company plans to utilise fresh issue proceeds primarily for repayment of certain borrowings, purchase and installation of new machinery at two manufacturing plants, and setting up a rooftop solar power plant at its Supa facility.

These initiatives are expected to support capacity expansion, improve energy efficiency and reduce power costs over the long term. Investment in renewable energy also aligns with sustainability goals and may provide cost advantages as electricity prices remain volatile.

At the upper price band, KSH International is valued at a pre-IPO P/E of around 32 times FY25 earnings. Compared with listed peers such as Precision Wires India and Ram Ratna Wires, the valuation appears reasonable but not deeply discounted.

While KSH International offers superior ROE and strong growth visibility, its debt levels are relatively higher than some peers. This may limit near-term re-rating potential, especially for investors focused on short-term listing gains.

From a long-term perspective, the valuation reflects the company’s growth prospects, export leadership and exposure to high-growth sectors like EVs and renewables.

The company derives a significant portion of its revenue from a limited number of large customers, which could impact earnings if client concentration increases. Raw material price volatility, particularly in copper and aluminium, can also affect margins.

Manufacturing operations involve operational risks such as equipment failure and force majeure events. Additionally, differences in accounting standards across jurisdictions may impact financial interpretation for some investors.

For listing gains seekers, the IPO may offer limited upside due to fair valuation and higher leverage compared to peers. However, for long-term investors, KSH International presents a strong structural growth story driven by electrification, EV adoption and infrastructure spending in India.

Investors with a long-term horizon and moderate risk appetite may consider the IPO as part of a diversified portfolio, keeping expectations realistic in the short term.

Choosing the right IPO is not just about numbers but about understanding risk, valuation and timing. Swastika Investmart, a SEBI registered entity, provides in-depth research, advanced trading tools, strong customer support and investor education to help retail investors make informed decisions.

If you are planning to apply for IPOs or build a long-term equity portfolio, opening an account with Swastika Investmart gives you access to professional insights and a tech-enabled investing experience.

What does KSH International do?

KSH International manufactures magnet winding wires used in motors, transformers, EVs and power equipment.

Is KSH International profitable?

Yes, the company reported a net profit of ₹67.99 crore in FY25 with an ROE of 22.77 percent.

What is the IPO price band?

The IPO price band is ₹365 to ₹384 per share.

Is the IPO good for listing gains?

Listing gains may be moderate as the valuation is fair but not cheap.

Is it suitable for long-term investors?

Yes, long-term investors may find value due to strong industry tailwinds and expansion plans.

The recent sell-off in India’s midcap and smallcap space sent shockwaves through the market. After months of outperformance, these segments corrected sharply as investors reacted to frothy valuations, regulatory caution from SEBI, and global uncertainty.

But the big question now is: Has the panic finally ended? There are early signs that the market may be stabilising — and possibly forming a short-term bottom.

Let’s break down what’s happening, what signals matter, and how investors should position themselves.

The correction didn’t happen in isolation. Multiple triggers set the tone:

Midcaps and smallcaps had rallied far beyond their historical averages. Many stocks were trading at 30–50% premiums despite modest earnings visibility.

This stretched the risk-reward equation, making the segment vulnerable to a correction.

SEBI issued cautionary comments regarding overheating in smaller companies, urging mutual funds to reassess risk frameworks.

While not a direct intervention, it created a sentiment shock, leading to profit-booking and fund rebalancing.

Concerns over US bond yields, geopolitical tensions, and FII outflows added fuel to the fire. With risk-off sentiment globally, smallcaps took the hardest hit.

Many schemes faced pressure to rebalance portfolios due to size restrictions and liquidity management rules, further accelerating the decline.

Now, the dust is beginning to settle — and several indicators suggest a bottom may be forming.

The pace of declines has slowed significantly. Earlier, deep cuts of 4–6% were common in a day; now, volatility has tapered.

This cooling-off reflects reduced panic and more measured trading activity.

The India VIX remains within a controlled range, signalling improving risk appetite. Historically, midcap recoveries begin when volatility stabilises first.

Despite sharp corrections, SIP contributions hit all-time highs, showing unwavering domestic investor faith.

Consistent inflows act as shock absorbers, reducing the likelihood of prolonged downturns.

Domestic institutional investors have started nibbling into quality smallcap and midcap names—especially in sectors like capital goods, defense, manufacturing, and financial services.

When institutions buy during corrections, it often marks the beginning of base formation.

Indian corporates have delivered stable earnings. Several smaller companies reported healthy margins, strong order books, or improved cash flows — not characteristics of a market in deep distress.

SEBI’s recent stance has shifted from caution to structured monitoring. Clear guidelines always reduce fear-driven volatility.

Once the overhang of regulatory uncertainty eases, quality stocks typically rebound sooner.

Past midcap–smallcap corrections (2013, 2018, 2020) show a similar pattern:

Markets seem to be entering the accumulation zone now.

A bottoming market can be a golden opportunity — but only with the right strategy.

Companies with:

… are likely to lead the recovery.

A rising tide won’t lift all boats. Many questionable smallcaps jumped in the rally but lack fundamentals.

Stay selective and avoid speculative bets.

Instead of trying to catch the exact bottom, stagger your entry over 4–6 months.

This cushions volatility and improves long-term returns.

Segments showing resilience include:

These sectors continue to receive policy support and strong domestic demand.

If your equity allocation has fallen due to the correction, rebalancing can boost long-term compounding.

Platforms with robust screening tools, research reports, and advisory support can help you avoid mistakes.

This is where a trusted financial partner becomes invaluable.

Swastika Investmart, a SEBI-registered financial services provider, offers:

In volatile markets, having a research-driven approach matters more than ever.

👉 Open an account today:

https://trade.swastika.co.in/?UTMsrc=HasTheMidcapSmallcapPanicFinallyEnded

1. Are midcap and smallcap stocks safe to invest in now?

They are safer than during the peak, but selectivity is essential. Focus on companies with strong fundamentals.

2. Has the market definitely bottomed?

Not guaranteed — but key indicators show stabilisation and early signs of accumulation.

3. Should I stop SIPs during a correction?

No. Corrections increase long-term returns by lowering average cost.

4. Which sectors look promising after this correction?

Manufacturing, capital goods, financial services, and defense are showing resilience.

5. How long do recoveries usually take?

Historically, midcap–smallcap recoveries take 3–6 months to gain momentum after major corrections.

The midcap–smallcap panic appears to be cooling, with several signals pointing towards a potential bottom. While uncertainty remains, disciplined investing, quality stock selection, and data-backed decisions can turn this volatility into opportunity.

If you’re looking to navigate this phase with expert guidance, Swastika Investmart’s research-driven tools and advisory support can help you make informed decisions.

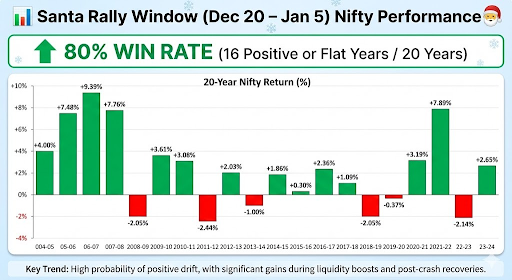

Every December, a familiar question resurfaces among Indian market participants:

“Will we see a Santa Rally this year?”

The Santa Rally—a phase between December 20 and January 5—is historically known for delivering strong positive returns in global equity markets. While the concept originated from US markets, the pattern has quietly taken shape in India as well.

And the numbers speak for themselves.

Over the last 20 years, Nifty has shown an 80% win rate during this period. That means in 16 out of 20 years, markets ended flat or positive.

Before we explore whether this year can repeat history, let’s look at the Table.

The Table highlights how often Nifty has delivered gains during this specific trading window. Notably big gains were observed in years following liquidity expansion phases or post-correction rebounds.

Some standout years include:

Even in difficult cycles such as 2011–12 or 2015–16, the dips remained relatively contained.

The data hints at something deeper:

Investor behaviour, liquidity conditions, and institutional rebalancing consistently influence year-end trends.

International markets often rally on:

Nifty mirrors this behaviour, especially when FIIs turn buyers.

India’s rising SIP culture—now over ₹20,000 crore per month—creates a dependable liquidity cushion. Even when FIIs stay cautious, domestic institutions and retail flows provide strong support.

By December:

This reduces uncertainty, which markets love.

With major policy decisions and earnings behind us, markets enter a quieter news cycle—ideal for rallies.

Whether the Santa Rally returns this year depends on several moving parts.

FIIs have been extremely sensitive to:

If global yields cool and India remains the preferred EM destination, FIIs could drive a meaningful rally.

Meanwhile, DIIs continue to provide steady inflows regardless of global conditions.

A neutral-to-dovish stance from the RBI generally:

If inflation stays within comfort levels, the backdrop improves for a year-end run-up.

For India, crude oil is the single biggest macro swing factor.

A stable or falling crude environment increases the probability of a Santa Rally.

If the US markets — especially S&P 500 and Nasdaq — carry momentum into the year-end, Nifty tends to follow suit.

Historically, India rarely rallies alone.

Nifty’s technical structure going into December matters:

A neutral–positive structure improves the setup.

While Santa Rallies are common, relying on them as guaranteed is risky.

Large caps tend to perform better due to stable liquidity.

If volatility emerges, staggered buying helps reduce timing risk.

Fed commentary, dollar index movement, and geopolitical risks can break the trend quickly.

Platforms like Swastika Investmart, with SEBI-registered research and actionable insights, help investors stay aligned with data—not emotions.

1. Does the Santa Rally always work in India?

No. While Nifty has delivered positive or flat returns in 80% of the last 20 years, external shocks or high valuations can offset historical patterns.

2. Why does Nifty usually rise between Dec 20 and Jan 5?

A mix of lower volatility, festive sentiment, portfolio rebalancing, and strong domestic flows often lifts markets.

3. Which sectors benefit the most during Santa Rallies?

Historically, banking, autos, consumer, and large-cap IT have shown stronger year-end momentum.

4. Is it safe to invest only for the Santa Rally?

Short-term bets are riskier. Long-term investors should view the rally as an opportunity, not a strategy.

5. What can break the Santa Rally this year?

Unexpected Fed remarks, Middle-East tensions, crude spikes, or heavy FII selling may cap returns.

The Santa Rally pattern in Nifty remains one of the most intriguing behavioural trends in the Indian market. Past data provides confidence—but not certainty. Whether this year repeats the 80% positive trend will depend on macro stability, global liquidity, and the market’s risk appetite.

For investors, the smartest approach is to stay data-driven and avoid knee-jerk decisions. Platforms like Swastika Investmart offer research-backed insights, strong customer support, and tech-enabled investing tools to help you navigate market opportunities confidently.

Trust Our Expert Picks

for Your Investments!

.webp)

.png)

.png)

%20(7)%20(2).png)

%20(6).png)