.png)

Shares of Multi Commodity Exchange of India (MCX) are firmly in the spotlight as the stock trades ex-date for its first-ever stock split. This corporate action marks a historic moment for MCX since its listing in 2012 and has drawn strong attention from investors tracking capital market and exchange-related stocks.

The development has sparked discussion not only because of the sharp price adjustment seen on trading screens, but also due to what it means for liquidity, retail participation, and long-term investor sentiment in the Indian stock market.

MCX has approved a 5:1 stock split, meaning one equity share with a face value of ₹10 has been subdivided into five equity shares of face value ₹2 each.

The company fixed January 2, 2026, as the record date to determine shareholder eligibility. As a result, MCX shares traded ex-date on this day, leading to a proportionate adjustment in the share price.

This is the first stock split in MCX’s history, making it a significant corporate milestone.

To understand this clearly, consider a simple example.

If an investor held 10 MCX shares before the record date, those holdings will now convert into 50 shares after the split. While the number of shares increases fivefold, the overall investment value remains unchanged.

Before the split, MCX shares closed around ₹11,015. Post split, the stock naturally trades at a much lower price, reflecting the revised face value and increased share count.

Any sharp fall visible on trading apps is purely technical, not a reflection of value erosion.

Many investors may notice an apparent drop of nearly 80 percent in MCX share price on certain platforms. This happens because some trading apps initially display the unadjusted pre-split price.

There is no cause for concern. Once prices are fully adjusted for the stock split, the charts normalize. The company’s market capitalisation and investor wealth remain exactly the same.

Such adjustments are standard for stock splits and are regulated under SEBI’s corporate action framework.

Eligibility is straightforward.

Investors who held MCX shares in their demat accounts as of January 1, 2026, before market close, are eligible for the split.

Those purchasing MCX shares on or after the ex-date will not receive additional shares under this corporate action.

Typically, shares arising from a stock split are credited to demat accounts within one to two working days after the record date.

Stock splits are often undertaken to make shares more accessible to a broader investor base.

For MCX, the stock had reached a 52-week high of ₹11,218 in December 2025, making the ticket size relatively high for smaller investors. A lower post-split price improves affordability and encourages wider retail participation.

Additionally, stock splits tend to:

However, it is important to note that stock splits do not alter earnings, profitability, or business strength.

The stock split does not change MCX’s underlying business fundamentals. The exchange continues to benefit from strong momentum in commodity derivatives trading and rising participation across energy, bullion, and metals.

Brokerage commentary has highlighted sustained volume growth and elevated commodity volatility as near-term drivers. Profit growth expectations remain supported by increased trading activity and product expansion.

Upside risks include higher traction in commodity options and new product introductions, while risks may arise from regulatory changes, technology transitions, or lower volatility impacting volumes.

While stock splits and bonus issues may appear similar, their objectives differ.

A stock split reduces the face value and increases the number of shares, keeping share capital unchanged. Dividend per share adjusts proportionately.

A bonus issue distributes free shares from accumulated reserves without changing face value. Dividend entitlement remains unchanged in a bonus issue.

Understanding this distinction helps investors interpret corporate actions more clearly.

For existing shareholders, no action is required. The split is automatic, and holdings adjust accordingly.

For new investors, the lower post-split price makes MCX more accessible, but entry decisions should always be backed by research rather than corporate actions alone.

Long-term returns will continue to depend on MCX’s trading volumes, regulatory environment, and growth in India’s commodity markets.

Tracking corporate actions, understanding technical price adjustments, and evaluating fundamentals requires timely insights. Swastika Investmart, a SEBI-registered financial services provider, supports investors with strong research tools, tech-enabled platforms, and responsive customer support.

With a focus on investor education and data-backed analysis, Swastika helps clients navigate events like stock splits with clarity and confidence.

Why are MCX shares in focus today

MCX shares are in focus as they are trading ex-date for their first-ever 5:1 stock split.

What is the MCX stock split ratio

MCX has announced a 5:1 stock split, where one ₹10 face value share becomes five ₹2 shares.

Does the MCX stock split affect fundamentals

No, the stock split does not impact MCX’s business, earnings, or market value.

Who is eligible for the MCX stock split

Investors holding MCX shares before market close on January 1, 2026, are eligible.

Why does the share price look sharply lower after the split

The price drop is a technical adjustment due to the increased number of shares.

The MCX stock split is a structural move aimed at improving liquidity and accessibility, not a reflection of changes in business strength. For investors, understanding the mechanics behind such corporate actions is far more important than reacting to headline price movements.

If you are looking to track stocks in focus, corporate actions, and market trends with expert-backed insights, Swastika Investmart can be your trusted investing partner.

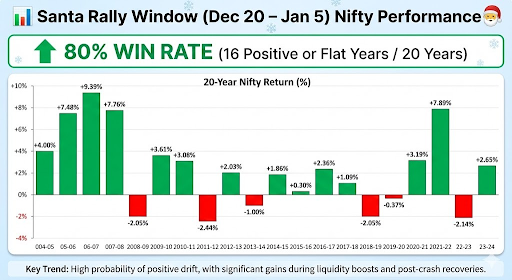

Every December, a familiar question resurfaces among Indian market participants:

“Will we see a Santa Rally this year?”

The Santa Rally—a phase between December 20 and January 5—is historically known for delivering strong positive returns in global equity markets. While the concept originated from US markets, the pattern has quietly taken shape in India as well.

And the numbers speak for themselves.

Over the last 20 years, Nifty has shown an 80% win rate during this period. That means in 16 out of 20 years, markets ended flat or positive.

Before we explore whether this year can repeat history, let’s look at the Table.

The Table highlights how often Nifty has delivered gains during this specific trading window. Notably big gains were observed in years following liquidity expansion phases or post-correction rebounds.

Some standout years include:

Even in difficult cycles such as 2011–12 or 2015–16, the dips remained relatively contained.

The data hints at something deeper:

Investor behaviour, liquidity conditions, and institutional rebalancing consistently influence year-end trends.

International markets often rally on:

Nifty mirrors this behaviour, especially when FIIs turn buyers.

India’s rising SIP culture—now over ₹20,000 crore per month—creates a dependable liquidity cushion. Even when FIIs stay cautious, domestic institutions and retail flows provide strong support.

By December:

This reduces uncertainty, which markets love.

With major policy decisions and earnings behind us, markets enter a quieter news cycle—ideal for rallies.

Whether the Santa Rally returns this year depends on several moving parts.

FIIs have been extremely sensitive to:

If global yields cool and India remains the preferred EM destination, FIIs could drive a meaningful rally.

Meanwhile, DIIs continue to provide steady inflows regardless of global conditions.

A neutral-to-dovish stance from the RBI generally:

If inflation stays within comfort levels, the backdrop improves for a year-end run-up.

For India, crude oil is the single biggest macro swing factor.

A stable or falling crude environment increases the probability of a Santa Rally.

If the US markets — especially S&P 500 and Nasdaq — carry momentum into the year-end, Nifty tends to follow suit.

Historically, India rarely rallies alone.

Nifty’s technical structure going into December matters:

A neutral–positive structure improves the setup.

While Santa Rallies are common, relying on them as guaranteed is risky.

Large caps tend to perform better due to stable liquidity.

If volatility emerges, staggered buying helps reduce timing risk.

Fed commentary, dollar index movement, and geopolitical risks can break the trend quickly.

Platforms like Swastika Investmart, with SEBI-registered research and actionable insights, help investors stay aligned with data—not emotions.

1. Does the Santa Rally always work in India?

No. While Nifty has delivered positive or flat returns in 80% of the last 20 years, external shocks or high valuations can offset historical patterns.

2. Why does Nifty usually rise between Dec 20 and Jan 5?

A mix of lower volatility, festive sentiment, portfolio rebalancing, and strong domestic flows often lifts markets.

3. Which sectors benefit the most during Santa Rallies?

Historically, banking, autos, consumer, and large-cap IT have shown stronger year-end momentum.

4. Is it safe to invest only for the Santa Rally?

Short-term bets are riskier. Long-term investors should view the rally as an opportunity, not a strategy.

5. What can break the Santa Rally this year?

Unexpected Fed remarks, Middle-East tensions, crude spikes, or heavy FII selling may cap returns.

The Santa Rally pattern in Nifty remains one of the most intriguing behavioural trends in the Indian market. Past data provides confidence—but not certainty. Whether this year repeats the 80% positive trend will depend on macro stability, global liquidity, and the market’s risk appetite.

For investors, the smartest approach is to stay data-driven and avoid knee-jerk decisions. Platforms like Swastika Investmart offer research-backed insights, strong customer support, and tech-enabled investing tools to help you navigate market opportunities confidently.

.png)

Silver has always been the quieter cousin of gold—less flashy, more volatile, and often overlooked until a big move happens. But the conversation is heating up again. Several analysts and commodity strategists believe that 2025 could be the start of a major silver supercycle, one strong enough to push prices to ₹2,00,000 per kg in India.

Is this realistic or just another hype cycle?

Let’s break it down using real-world data, global trends, and India-specific context.

A supercycle typically refers to a long, sustained rise in commodity prices caused by structural demand and limited supply. Historically, metals like copper, iron ore, and oil have experienced supercycles during periods of global expansion.

Silver is now entering a similar setup because of three major forces:

Silver is a critical input in:

The Solar Energy Industries Association estimates a gigantic jump in photovoltaic demand, potentially making silver one of the fastest-growing industrial metals in 2025.

If the US Federal Reserve and other central banks move toward easing monetary policy, precious metals like silver typically rise due to:

We saw this pattern during 2008–2011, when silver surged over 400%.

Mine production has lagged behind demand for years. Several major silver miners have reported:

This mismatch between supply and demand is a classic trigger for a supercycle.

Let’s look at the numbers.

Silver currently trades at approximately:

For silver to reach ₹2,00,000 per kg, we would need:

While this is not the base-case expectation for most analysts, it is possible under a high-stress macro environment, such as:

Think of it this way:

Silver has rallied 10x in past cycles, most notably between 2003–2011. When silver runs, it really runs.

But it also corrects sharply.

This is why investors need a balanced view, not blind optimism.

India is one of the world’s largest consumers of silver—both industrially and as jewellery. The effects of a supercycle would be mixed:

India imports most of its silver. A spike to ₹2 lakh/kg would put upward pressure on:

This could indirectly influence stock markets via FII sentiment.

Domestic companies in:

may face cost pressure but benefit from rising demand.

Indians traditionally buy silver during festivals and weddings. A price boom could push demand toward:

This aligns with India’s wider shift to formal financial instruments.

Jewellery players may see mixed results:

Before assuming a supercycle, track these triggers:

A weakening rupee can amplify silver prices far more than global moves.

Any change in customs duty on silver impacts price directly.

Rising volumes can indicate rising speculative interest.

Institutional money is the real driver of supercycles.

China consumes nearly 50% of global silver. Its industrial recovery will be crucial.

1. What is a silver supercycle?

It refers to a long-term surge in silver prices driven by strong structural demand and tight supply conditions across the global market.

2. Can silver really hit ₹2,00,000 per kg?

It’s an optimistic target. Achievable only if global liquidity, industrial demand, and supply disruptions align. Investors should consider it a possibility, not a certainty.

3. Is silver a better investment than gold in 2025?

Silver is more volatile but can deliver higher percentage returns during bull cycles. Gold, on the other hand, is more stable and defensive.

4. How should Indian investors buy silver?

Silver ETFs, MCX futures, and digital silver offer regulated and transparent access. Physical silver carries storage and purity risks.

5. Is now the right time to enter silver?

It depends on your risk profile. A staggered approach or SIP-style buying may help manage volatility.

The idea of a Silver Supercycle 2025 is exciting—and in many ways, credible. Industrial demand from solar and EVs is rising sharply, supply constraints are real, and global monetary cycles may turn favourable. But the jump to ₹2 lakh per kg requires an extraordinary combination of global events.

For Indian investors, the key is to stay informed, avoid speculative bets, and balance silver exposure within a diversified portfolio.

If you want expert guidance, market insights, and research-backed strategies, Swastika Investmart’s SEBI-registered advisory team and tech-enabled platforms can help you navigate commodity trends with confidence.

The US Federal Reserve’s decision to cut interest rates to 3.50%–3.75% marks one of the most important policy shifts of the year. Whenever the Fed moves, global markets listen. And for India — now one of the world’s most influential emerging market economies — such a decision has both direct and indirect consequences.

Investors often wonder:

Will this boost Nifty?

Will FIIs return?

Will the market rally or consolidate?

This blog simplifies the answer with data-driven insights, Indian context, and real-world examples — written in a clear, natural, and professional style.

The Fed’s move comes on the back of a slowing US economy, easing inflation, and a need to support consumption and business borrowing. This pivot toward rate cuts signals:

Any of these factors can quickly alter the risk appetite of global investors — especially FIIs who influence Indian equity markets significantly.

Let’s break it down into simple, relatable impacts:

Generally, when US interest rates drop:

For India, this is usually positive. Historically, we’ve seen this during:

If the current cut leads to a weaker dollar index, India could see:

However, India is no longer dependent only on FIIs — strong domestic inflows provide a cushion even during global uncertainty.

Nifty’s immediate reaction may be choppy because markets had partially priced-in the rate cut.

But over the next quarter:

…could create a healthy setup for Nifty to trend positively, barring external shocks.

A key indicator to watch:

Crude oil. If oil stays below $85, India benefits.

A Fed cut often reduces pressure on emerging market currencies. For the rupee:

IT companies may see mild margin pressure if the rupee strengthens, but the overall direction remains sector-specific.

Lower borrowing costs and better liquidity often support credit growth. Nifty Bank tends to benefit when yields soften globally.

A weaker US dollar can reduce rupee revenues, but improved US business activity typically boosts demand for Indian IT services.

This sector thrives in lower-rate environments. Home loans could become more competitive if Indian rates also follow a softening path.

Lower global rates help reduce financing costs and also soften commodity prices — a positive for auto manufacturers.

If global growth expectations rise due to Fed easing, metals could see revival.

Markets may react sharply in the first few sessions, but stability often follows.

Companies with resilient earnings, low leverage, and steady cash flows are better positioned to benefit from liquidity-driven rallies.

A mix of large caps, sectors with strong earnings visibility, and long-term SIP flows can help ride global cycles smoothly.

1. Will the Fed rate cut directly impact Indian interest rates?

Not immediately. The RBI considers domestic inflation and growth, though global cues like Fed policy indirectly influence its stance.

2. Will Nifty rise after the Fed rate cut?

Short-term volatility is possible, but medium-term sentiment tends to be positive due to better liquidity and improved risk appetite.

3. Are FIIs likely to return to Indian markets?

Yes, if global yields remain soft and the dollar cools, India becomes attractive due to strong economic fundamentals.

4. Which sectors will benefit the most?

Banks, NBFCs, real estate, IT, and autos could see improved sentiment depending on secondary macro factors.

5. Should retail investors make changes to their portfolios?

Only after evaluating risk tolerance and goals. Long-term investors should stay disciplined.

The Fed’s move to cut rates to 3.50%–3.75% is a significant turning point for global liquidity and market momentum. For India, the impact is likely to be constructive over the medium term — supported by strong domestic growth, healthy corporate earnings, and robust retail participation.

Investors who balance patience with informed decision-making stand to benefit the most.

If you're looking to analyze markets with expert guidance, real-time insights, and SEBI-registered research support, Swastika Investmart offers a tech-enabled platform to help you invest smarter.

ICICI Prudential Asset Management Company (ICICI AMC) is finally coming to the public markets, and investor interest is already buzzing. Backed by ICICI Bank and Prudential Group — two respected names in the financial world — this IPO has become one of the most anticipated listings of the year.

In this detailed breakdown, we analyse the company’s business model, strengths, risks, financial performance, valuation, peer comparison, and whether investors should consider applying. This analysis follows SEBI-aligned transparency, Indian market context, and strong research methodology backed by Swastika Investmart’s expertise.

ICICI AMC is an Asset Management Company — meaning it manages money on behalf of retail and institutional investors. This money is pooled through mutual fund schemes like:

The company’s core responsibility is simple:

Invest clients’ money responsibly and generate long-term returns while managing risk.

They earn revenue primarily from management fees, which are linked to their AUM (Assets Under Management). So, higher AUM → higher income → stable profitability.

As of September 2025, ICICI AMC reported a Quarterly Average AUM of ₹10,147.6 billion, reflecting its large market dominance.

Issue Type: 100% Offer for Sale (OFS)

Total Issue Size: ₹10,602.65 crore

Fresh Issue: NIL

Offer for Sale: ₹10,602.65 crore

Price Band: ₹2061–₹2165

Market Lot: 6 shares

Issue Opens: 12 December 2025

Issue Closes: 16 December 2025

Listing: BSE & NSE

Market Cap at Upper Band: ₹1,07,006.97 crore

Basis of Allotment: 17 Dec 2025

Refunds: 18 Dec 2025

Shares in Demat: 18 Dec 2025

Listing Date: 19 Dec 2025

This IPO is purely OFS — no new money comes into the company, as existing shareholder Prudential Corporation is reducing its stake.

Below is a clean text summary of the company’s consolidated financial performance:

Observation:

There is consistent revenue and profit growth, stable margins, strong balance sheet expansion, and market-leading profitability.

ICICI Bank + Prudential Group = instant trust among investors.

Equity, debt, hybrid, ETFs, PMS, AIF — all major asset classes covered.

EBITDA margin ~73% indicates superior cost efficiency.

272 offices across 23 states + strong digital onboarding ecosystem.

RoNW of 82.8% is among the best in the financial sector.

Key Interpretation:

ICICI AMC leads the industry in RoNW, revenue scale, and premium brand value.

ICICI AMC is valued at P/E 40.37x (FY25). While not cheap, the valuation seems justified because:

Swastika Investmart’s research outlook suggests the IPO is positioned as a long-term compounding opportunity.

Here’s the balanced view:

Verdict:

If your aim is long-term wealth creation, this IPO is worth considering.

Yes, the company operates with minimal debt due to its asset-light model.

Regulatory changes from SEBI and market volatility impacting AUM growth.

Yes, 100% OFS, meaning no new shares are issued.

Its scalable digital ecosystem, massive distribution, and industry-leading RoNW.

Yes, through broker apps, UPI, or via Swastika Investmart’s seamless platform.

ICICI Prudential AMC stands out for its strong financials, brand backing, diversified product portfolio, and superb profitability metrics. While the IPO is a pure OFS, long-term investors may find significant value as the Indian asset management industry continues to expand with rising financialization.

If you're looking for stability, trust, and steady compounding, ICICI AMC can be a strong addition to your long-term portfolio.

The Indian banking industry has been transforming rapidly, especially with growing digital adoption, tighter regulatory frameworks, and stronger capital adequacy norms. In this evolving landscape, the Finance Ministry’s approval allowing AU Small Finance Bank (AU SFB) to raise its foreign investment limit from 49% to 74% marks a significant policy milestone.

This development is not just a technical regulatory update—it is a signal that could reshape the bank’s capital flexibility, global investor interest, and long-term growth trajectory. For investors, understanding the implications of this move is essential, particularly at a time when the BFSI sector is witnessing steady credit offtake and rising competition.

Let’s break down what this approval means, why it matters, and what you—as an investor—should track in the coming months.

By increasing the foreign direct investment ceiling to 74%, AU SFB gains access to a broader pool of international investors. This is important because:

For a bank aiming to scale lending, digital infrastructure, and geographical footprint, additional foreign capital improves both capacity and resilience.

Banks with higher FDI participation often gain better visibility among global funds and rating agencies. AU SFB could see:

In previous regulatory instances—such as when HDFC Bank or ICICI Bank saw increased foreign investor interest—market visibility improved significantly.

Additional foreign capital can support AU SFB’s long-term growth roadmap, which typically includes:

Higher capital levels also act as a buffer during stressed credit cycles, ensuring healthier balance sheet stability.

The FDI increase aligns with India’s broader efforts to attract overseas capital into regulated sectors. For the BFSI space, such policy green signals generally:

In recent years, foreign flows into financial services have been closely tied to India’s interest rate cycles and macroeconomic stability. This announcement may help AU SFB attract incremental FPI/FII inflows, especially from global funds focused on emerging market banking stories.

FDI limit enhancement is only the first step. Investors should monitor:

Large long-term funds coming in could boost the stock’s institutional credibility.

With growth comes risk. Key metrics to follow:

A stable or improving asset quality trend will be a positive indicator.

Capital infusion gives AU SFB the ability to expand lending, but investors should track:

If the bank maintains strong profitability while scaling, the FDI hike will translate into real value creation.

The RBI has been vigilant with SFB compliance on:

Any shift in regulatory expectations could influence AU SFB’s growth trajectory.

1. What does AU SFB’s FDI limit increase mean?

It allows foreign investors to own up to 74% of the bank, expanding its ability to attract global capital for growth and strengthening its balance sheet.

2. Will the bank immediately raise funds after this approval?

The approval only increases the permissible limit; actual fundraise depends on market conditions and management decisions.

3. How will this impact retail shareholders?

Higher FDI may improve liquidity, valuation visibility, and future growth prospects, though short-term market reactions may vary.

4. Is this positive for the small finance bank sector?

Yes. It may enhance global confidence in the SFB model and set the stage for similar policy flexibility for other players.

5. What risks should investors be aware of?

Asset quality pressures, credit cycle sensitivity, regulatory changes, and execution challenges during expansion.

The Finance Ministry’s approval for AU Small Finance Bank to raise its foreign investment limit from 49% to 74% is more than a policy update—it’s a strategic catalyst. It enhances the bank’s capacity to raise high-quality capital, strengthens institutional credibility, and opens doors for long-term expansion in a competitive banking ecosystem.

For investors, the next few quarters will be crucial to understand how the bank deploys new capital, manages its asset quality, and leverages growth opportunities.

For data-backed insights, investor education, and SEBI-registered guidance, platforms like Swastika Investmart empower you to make smarter, informed decisions—whether analysing regulatory updates or navigating market trends.

India’s healthcare sector has been one of the most resilient and fast-evolving spaces, backed by rising demand for speciality care, medical infrastructure expansion, and increasing insurance penetration. Against this backdrop, the Park Medi World IPO has generated noticeable investor interest ahead of its December 10–12 bidding window.

The company operates a large network of multi-super speciality hospitals under the “Park” brand and is already one of the largest private healthcare providers in North India. Given the strong fundamentals and sectoral momentum, the IPO has become a talking point among retail and institutional investors.

Let’s dive deeper into its business model, financials, valuation, strengths, and key risks.

Park Medi World runs 14 multi-super speciality hospitals across Haryana, Delhi, Punjab, and Rajasthan. Its hospitals offer more than 30 speciality and super-speciality services including:

All hospitals are NABH accredited, and eight facilities also hold NABL accreditation, reflecting strong clinical standards. The diverse speciality mix positions the group as a reliable healthcare provider across major population clusters.

Issue Open: 10 December 2025

Issue Close: 12 December 2025

Total IPO Size: ₹920 crore

Fresh Issue: ₹770 crore

Offer for Sale: ₹150 crore

Price Band: ₹154–162

Market Lot: 92 shares

Face Value: ₹2

Listing: BSE, NSE

Expected Market Cap: ₹6,997.28 crore

Issue Break-up:

Indicative Timetable:

The company plans to deploy the fresh capital for:

The ₹380 crore earmarked for debt repayment is expected to instantly improve net margins post-listing.

The valuation is reasonable when compared with premium-listed peers like Apollo Hospitals, Max Healthcare, Global Health, Krishna Institute of Medical Sciences, etc.

It is the second largest private hospital chain in North India and the largest in Haryana, offering deep regional penetration.

From oncology to orthopaedics, the wide range of specialities creates a stable revenue stream and enhances patient retention.

NABH and NABL certifications across multiple hospitals strengthen clinical credibility.

A proven track record of acquiring and integrating hospitals gives the company an edge in expansion-driven growth.

Consistent revenue growth, strong margins, and improving net worth make the financials robust.

Running large multi-speciality hospitals demands constant capex and skilled manpower, impacting cost structures.

The sector faces strict regulatory oversight relating to pricing, reporting, and medical standards.

Private hospital chains and government institutions both create competitive intensity in major markets.

Availability and retention of skilled doctors and staff remain critical to operational stability.

Certain treatments and admission rates fluctuate seasonally, affecting quarterly performance.

Although the company claims no direct comparable peers with the same business model, listed players in the broader healthcare space include:

Park Medi World’s valuation is noticeably lower compared to many of these, offering an attractive entry point for long-term investors seeking healthcare exposure.

The IPO arrives with a favorable mix of growth, profitability, and reasonable valuation. Key positives include:

With growing healthcare consumption, rising insurance penetration, and government-backed initiatives supporting medical infrastructure, Park Medi World is well-positioned to benefit from structural sectoral demand.

For medium to long-term investors, the IPO appears to offer a solid combination of stable business fundamentals and attractive valuation.

1. What is the price band of the Park Medi World IPO?

The IPO is priced at ₹154 to ₹162 per share.

2. How is the company financially performing?

In FY25, Park Medi World generated ₹1,425.97 crore in revenue, with a 26.11% EBITDA margin and ₹213.22 crore net profit.

3. What will the company use the IPO proceeds for?

Funds will be used for expansion, equipment purchase, marketing, and debt repayment.

4. Is the valuation attractive?

At 29.21x P/E, the valuation is reasonable compared to major listed hospital chains with significantly higher multiples.

5. Is this IPO suitable for long-term investors?

Given the strong operating performance and regional leadership, the IPO suits investors seeking long-term exposure to India’s healthcare growth story.

Park Medi World’s IPO comes at a time when healthcare demand in India is rising rapidly. With strong financials, expanding capacity, and a track record of consistent execution, the company presents a compelling long-term investment case. As always, aligning IPO investments with your risk appetite and financial goals is important.

For deeper insights, SEBI-registered guidance, and easy investing tools, platforms like Swastika Investmart help investors make informed decisions with confidence.

Trust Our Expert Picks

for Your Investments!

.webp)

.png)

.png)

%20(2).png)