Information

Trent ₹6 Dividend — Buy Before Jun 11, 2026 — Should You?

.webp)

Key Takeaways

- Trent Limited declares a ₹6 dividend per share with the record date of 12-Jun-2026.

- To qualify for the dividend, you must buy before 11-Jun-2026 and ensure settlement.

- Top priority sectors: Consumer discretionary (retail) and dividend-focused equity strategies.

- Action: If you want the payout, consider buying before 11-Jun-2026; otherwise wait and assess fundamentals.

What Happened

Trent Limited announced a dividend of ₹6 per share for equity shareholders. The payout comes with a record date of 12-Jun-2026, and the last date to buy the stock to qualify is 11-Jun-2026. In practical terms, investors need to own the shares before 11-Jun to be eligible for the cash payout.

Key Details

Dividend payments are cash returns on top of any price appreciation. The settlement cycle in India suggests you should consider the T+2 timeline when placing orders to ensure settlement before or on the cut-off date. If you currently own the stock, this dividend increases your yield for the next 1-2 quarters, though price movements around payout can offset some gains.

Why This Matters

Dividend announcements indicate cash generation capability and can attract income-focused investors. For Trent, a ₹6 per-share payout may modestly improve total returns for holders, especially if the stock price doesn't swing wildly around the payout window. For you, the practical takeaway is to assess whether this dividend aligns with your income goals and risk profile, and whether you are comfortable with potential price volatility in the near term.

Market Context

In the current retail landscape, Trent's dividend yield should be weighed against its earnings growth, store expansions, and competitive dynamics with peers. If you already own Trent, the payout could slightly boost your realized return; if you're contemplating entry, you must factor in valuation and the stock's longer-term earnings trajectory. Your decision should hinge on fundamentals rather than chasing a cash yield alone.

What This Means For Your Portfolio

MOST IMPORTANT SECTION — direct investor impact: - Which stocks or sectors are affected: Trent's dividend affects your exposure to consumer discretionary and adds a cash component to returns for holders. - Should investor buy, hold, or wait: If you need income and the stock's fundamentals look solid, buying before 11-Jun-2026 can be reasonable; otherwise, consider your overall risk and diversify. - Any risk to existing portfolio: Dividend-driven moves can lead to concentration risk; price adjustments around the payout can create temporary drawdowns if not managed carefully.

Direct Implications

For you, the central question is whether to add or maintain a position in Trent to capture the ₹6 per share payout. If you already hold the stock, the dividend enhances your yield but do not rush to pay a higher entry price. If you are new to the stock, weigh the dividend along with business prospects such as store expansion, brand strength, and consumer demand trends.

Swastika Investmart notes that dividend announcements can lead to short-term price moves. If you are a retail investor, assess whether the yield justifies the risk and whether you already own the stock. The long-term case for Trent depends on its earnings, store expansion, and consumer demand, not just the dividend.

Sectors To Watch — Priority Order

1st Priority: Consumer Discretionary / Retail — aligned with Trent's core business and potential dividend-driven returns. 2nd Priority: Equity Markets / Dividend Income — compare yields and payout stability across the sector. Avoid Now: Fixed Income Funds — if you chase this dividend for income, you may miss better risk-adjusted opportunities in a balanced portfolio.

Action Points For Investors

- SIP investors: Rebalance gradually; don't overweight Trent solely for the dividend; keep your systematic plans intact. - Lumpsum investors: If you plan to deploy cash, align your entry with your risk tolerance and desired yield; don't chase the dividend alone. - Traders: Monitor price moves around the payout window; consider take-profit levels or hedging as needed.

Key Risks To Watch

2-3 risks investor should monitor: Dividend expectations may not sustain, price can drop around payout, and overall market volatility can impact both yield and valuation.

FAQ Details

What is the eligibility date for Trent's ₹6 dividend?

To receive ₹6 per share, you must own Trent shares before the last date to buy (11-Jun-2026) and have your trade settled.

How does this dividend affect my portfolio?

If you qualify, you will receive ₹6 per share as cash; the stock price may adjust near the payout, so total return depends on price movement as well as the dividend.

Should you buy Trent now for dividend income?

If your goal is dividend income and you are comfortable with the stock's fundamentals, buying before 11-Jun-2026 can be reasonable, but beware price risk and tax implications.

What other factors should investors consider with Trent?

Consider Trent's earnings growth, store expansion, consumer demand, competition, and overall market conditions; dividend alone should not drive allocation.

Conclusion

Trent's ₹6 dividend offers a potential income boost for shareholders, but entry decisions should hinge on your risk tolerance and the stock's fundamentals. If you aim to capture the payout, consider your timing carefully and balance with a view on long-term growth.

Tech Mahindra ₹36 Dividend — Should You Buy Before 02-Jul-2026, Your Move?

Key Takeaways

- Tech Mahindra has announced a dividend of ₹36 per share on equity shares.

- To receive the payout, you should buy before 02-Jul-2026 to become eligible.

- Direct impact includes potential yield and a short-term price adjustment around the payout window.

- Action: Consider buying before the cutoff if appropriate for your risk and income goals.

What Happened

Tech Mahindra has announced a dividend of ₹36 per share on its equity shares. The eligibility cutoff to receive this payout is 02-Jul-2026, so investors who want to capture the dividend should own the stock by that date. As is common with dividend announcements, the stock may experience some price movement around the payout window.

Why This Matters

Dividends add a steady income component to your portfolio, especially in a large IT services company with a history of stable cash flows. For retail investors in India, such payouts can help improve overall yield without requiring new investments. It is important to remember that the stock price often adjusts after the payout, so total returns depend on both yield and price movement. If you already own Tech Mahindra, evaluate whether this dividend aligns with your income goals and risk appetite.

What This Means For Your Portfolio

Direct investor impact includes potential immediate income of ₹36 per share and possible short-term price adjustment around the payout window. If you are overweight in IT services, this payout can boost your current yield, but it does not change the long-term growth story of the company. New buyers should weigh the dividend yield against the cost of the stock and the sector's growth outlook. For existing portfolios, ensure your overall risk is aligned with IT sector volatility; buying just for the dividend should not compensate for price risk.

Swastika Investmart notes that dividend-focused investors should pair this with overall IT exposure and risk tolerance. The payout size of ₹36 per share is attractive, but you should not chase the dividend alone; monitor the stock price and your cost of holding. The brokerage also suggests evaluating the stability of Tech Mahindra's order book and software services demand as it adds to the credibility of the dividend.

Sectors To Watch — Priority Order

1st Priority: IT Services — dividend news underscores cash flow stability and recurring revenue in this sector for investors who want yield.

2nd Priority: Financials — market sentiment and liquidity in equities can influence dividend stock prices; keep this sector on watch if you're considering adding yields.

Avoid Now: Real Estate — higher interest rate sensitivity and valuations can weigh on diversification; avoid increasing exposure to this sector around this payout.

Action Points For Investors

- SIP investors: Maintain your regular SIP into IT exposure; dividend receipts will supplement returns but should not drive allocation changes.

- Lumpsum investors: If you're adding Tech Mahindra for the dividend, ensure your price entry is reasonable; don't chase the payout and risk paying a premium.

- Traders: Use limit orders around the payout window; set stop-loss to protect capital and avoid overtrading on the news.

Tax Considerations

Dividends are taxed in the hands of investors according to applicable slab; consult your tax advisor for precise amounts. In India, the tax treatment depends on the investor's category and the company's payout history; keep this in mind when calculating net returns.

Key Risks To Watch

2-3 risks investor should monitor include IT sector demand sensitivity and client spend patterns, execution risk in large deals that could impact cash flows and dividend sustainability, and potential short-term price adjustments around the payout window that can affect overall returns.

FAQ Details

What does the ₹36 dividend mean for Tech Mahindra shareholders?

It is a payout per share on eligible holdings; you receive ₹36 for each share you own by the last date to buy.

Should you buy Tech Mahindra before 02-Jul-2026 to get the dividend?

If you want the payout, buying before 02-Jul-2026 can allow you to receive the dividend, but consider price movement and your risk tolerance.

Will the stock price drop after the dividend is paid?

Typically the stock may adjust for the payout amount, leading to short-term price movement that investors should be prepared for.

What are tax implications on dividend income in India?

Dividend income is taxed in the hands of the investor as per applicable slab; check guidance from your tax advisor for your situation.

Conclusion

Tech Mahindra's ₹36 per share dividend provides a tangible income opportunity for eligible investors. If you want to capture the payout, plan to buy before 02-Jul-2026 and monitor price movement around the payout window. Align this with your overall IT exposure and risk tolerance to decide your next step.

Prudential Buys ₹3,500 Cr Bharti Life — 75% Stake — Should You React?

Key Takeaways

- Prudential to acquire 75% stake in Bharti Life Insurance for ₹3,500 crore.

- Direct impact on your portfolio: exposure to life insurance and financial services shifts.

- Top priority sector to watch: Indian life insurance growth and regulatory developments.

- One clear action: review your exposure to life insurers and rebalance if needed.

\n\n

What Happened

Prudential plc will acquire a 75% stake in Bharti Life Insurance for ₹3,500 crore, buying from Bharti Life Ventures and 360 ONE Asset Management. The transaction marks a strategic move by an international insurer into India's fast-expanding life-insurance market.

Why This Matters

India's life-insurance sector has shown resilient growth driven by rising income levels, penetration potential, and regulatory clarity around solvency and product standards. A sizeable stake sale can unlock capital, speed up product launches, and expand distribution for Bharti Life, potentially sharpening competition in the sector. For your portfolio, this signals a long-term growth story in life insurance, but it also introduces regulatory and integration risks that you should monitor.

Key Takeaways

Prudential's entry via a 75% stake indicates strong confidence in Bharti Life's business model and long-term India growth prospects. The deal could improve Bharti Life's capital position and product capabilities, potentially boosting margins over time. For you, the move reinforces why focusing on governance, profitability, and solvency metrics matters more than headline deal size.

What This Means For Your Portfolio

Expect a re-rating dynamic within life-insurance names and allied financials as the market digests a new majority owner. Bharti Life could accelerate product innovation and distribution reach, while peers may face heightened competition and pricing pressure. As an investor, treat this as a long-term growth signal for life-insurer exposure, but avoid chasing near-term price moves or overexposure to any single name. Your portfolio should prioritize quality, stable earnings, and sensible risk controls rather than a speculative pivot.

Sectors To Watch — Priority Order

\n1st Priority: Life Insurance — strong long-term growth potential; regulatory clarity will shape profitability.\n2nd Priority: Financial Services / Asset Management — synergy with cross-sell and distribution; watch capital flows and governance.\nAvoid Now: Real Estate — limited relevance to this deal and higher cycle risks.\n

Action Points For Investors

\n- SIP investors: Maintain disciplined exposure to insurance and financials; rebalance if your portfolio is overweight in non-insurance names.\n- Lumpsum investors: Consider a staged entry into well-managed life-insurance plays, focusing on solid solvency and consistent earnings growth.\n- Traders: Monitor regulatory milestones, management commentary, and earnings signals for Bharti Life and Prudential; look for a re-rating on clarity around profitability and synergy realization.\n

Swastika Investmart perspective: This deal highlights India's growing appeal for long-term insurers and the importance of disciplined due diligence. For you, it underscores the need to diversify within financials and avoid chasing quick gains on regulatory announcements. We continue to monitor regulatory clearances and integration milestones for Bharti Life's business.

Key Risks To Watch

2-3 risks to monitor: regulatory approval timelines, execution risk in integrating Bharti Life's operations with Prudential, and valuation/growth projection uncertainties.

FAQ Details

What happened with Prudential and Bharti Life Insurance?

Prudential plc will acquire a 75% stake in Bharti Life Insurance for ₹3,500 crore from Bharti Life Ventures and 360 ONE Asset Management, subject to regulatory approvals.

How could this deal affect Bharti Life's policyholders and products?

The deal aims to provide stronger capital support and distribution reach, potentially enabling more product launches and better service over the long term, though changes will occur gradually.

Should I buy Bharti Life or other Indian life insurers after this deal?

This is not personalized investment advice. Consider overall fundamentals, governance, solvency, and regulatory trajectory before increasing exposure to any single insurer.

What are the main risks of this deal for investors?

Regulatory approval timelines, integration execution risk, and possible gaps between growth expectations and actual performance are the key risks to monitor.

Conclusion

The Prudential-Bharti Life deal underscores a longer‑term growth thesis for India's life-insurance sector, with regulatory and execution risks that require a measured, diversified approach.

Muthoot ₹4,000cr IPO — Gold loan expansion — Are You Ready?

Key Takeaways

- Muthoot FinCorp approved plans to raise up to ₹4,000 crore via an IPO to expand its gold loan business.

- Direct impact on your portfolio could come from NBFC exposure; pricing and post-listing performance matter.

- Top priority sector to watch: gold-linked lending and NBFC funding environment.

- Action: wait for pricing details and fundamentals before subscribing; do not rush into the IPO.

What Happened

Muthoot FinCorp has approved plans to raise up to ₹4,000 crore through an initial public offering to fund expansion in the gold loan business. The issue will include a fresh portion of shares and comes as the sector benefits from strong gold prices and rising demand. Investor implication: You should monitor the pricing and post-listing performance to judge whether this IPO fits your risk appetite.

Why This Matters

Gold loan NBFCs have shown resilience with higher gold prices and steady retail credit demand, which can translate into stronger loan growth for players with proven risk controls. The IPO signals confidence in a niche but also tests management’s ability to scale operations and manage liquidity as the company grows. Investor implication: You should assess whether the valuation reflects growth prospects and the underwriting quality before taking a position.

What This Means For Your Portfolio

Direct impact: A large NBFC-focused IPO like this could alter the risk–return profile of your financials exposure, especially if you already hold or plan to hold gold-linked lending assets. The sector could benefit from easier access to capital and higher growth, but pricing discipline and liquidity after listing are key risks. Investor implication: Consider a cautious stance until the issue price and long-term fundamentals are clear; avoid over-concentration in a single IPO.

Sectors To Watch — Priority Order

1st Priority: Gold loan NBFCs — Growth potential supported by strong collateral and rising gold prices.

2nd Priority: Financial services overall — Continued demand for affordable credit and stable funding.

Avoid Now: Real estate stocks — Higher interest-rate sensitivity and cyclicality could weigh on leverage players.

Action Points For Investors

- SIP investors: Consider diversified exposure to financials with a focus on risk-managed NBFCs; keep cumulative allocation moderate until clarity on IPO pricing.

- Lumpsum investors: Wait for the price band, anchor bids, and subscription numbers before committing new capital.

- Traders: Be prepared for volatility around listing day and use strict risk controls; avoid chasing hype.

Swastika Investmart Note: Gold loan lenders have benefited from stronger gold prices and steady credit growth. We will monitor the IPO's pricing and post-listing performance to guide clients. This note is for informational purposes and not a buy/sell recommendation.

Key Risks To Watch

Pricing realism vs. expectations, execution risk in scaling up operations, post-listing liquidity and short-term volatility, and sensitivity to gold price fluctuations. Investor implication: You should assess your risk tolerance, diversify across financials, and avoid aggressive bets on a single IPO.

FAQ Details

What is the size and nature of the Muthoot FinCorp IPO?

The company plans to raise up to ₹4,000 crore through a fresh issue to fund expansion in its gold loan lending business.

Why is Muthoot FinCorp pursuing this IPO now?

To fuel growth in a high-demand gold loan niche and strengthen its capital base for expansion.

Should retail investors apply for this IPO?

Investors should wait for the price band and fundamentals; assess valuation, risk, and diversification before subscribing.

What are the key risks for gold loan NBFC IPOs?

Pricing risk, execution risk, post-listing liquidity, and exposure to gold price volatility and credit risk.

Conclusion

Muthoot FinCorp’s ₹4,000 crore IPO signals expansion in a niche but competitive gold lending space. For retail investors, wait for pricing details and validate the long-term fundamentals before increasing exposure.

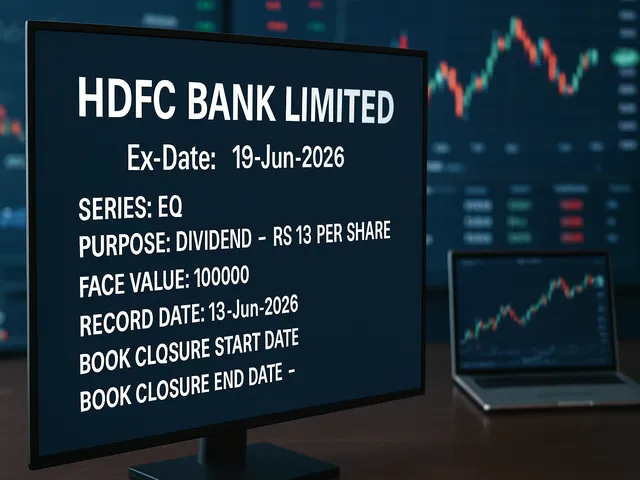

HDFC Bank Limited - Ex-Date: 19-Jun-2026

Quick Takeaways

• HDFC Bank announces a Rs 13 per share dividend for the EQ series with ex-date and record date on 19-Jun-2026.

• Ex-date explains eligibility: ownership before 19-Jun-2026 qualifies for the payout.

• Dividend yield depends on the stock price and may affect short-term price movements around the ex-date.

• Book closure dates aren’t specified in the notice; verify timings through official filings and exchanges.

Overview of the announcement

HDFC Bank has announced a dividend on its equity shares for the series EQ, with a payout of Rs 13 per share. The ex-date and the record date are both set for 19 June 2026. The notice lists the face value as Rs 100,000 per share, a nominal value used in regulatory filings. No book-closure dates are specified in the notice, so investors should verify the final dates with the exchange or the bank's investor relations portal. This dividend reflects the bank's ongoing practice of returning capital to shareholders at regular intervals, a common feature among large Indian lenders.

What ex-date means and why it matters

Ex-date is the key cutoff for eligibility. If you buy shares on or after the ex-date, you will not receive the declared dividend for this cycle. Those who hold shares before the ex-date qualify for the payout, subject to being registered as a shareholder on the record date. On or around the ex-date, the stock price often adjusts downward to reflect the impending dividend, though market moves can overshadow this adjustment. The record date confirms who is entitled to receive the dividend, and in this case it is 19 June 2026. For investors, understanding these dates helps avoid missing out on expected income and ensures correct settlement timing across brokers and exchanges.

Dividend yield and portfolio impact

The Rs 13 per-share dividend provides a clear income component, but the realized benefit depends on the share price at the ex-date. Yield is calculated as annual dividend divided by the market price, so higher prices reduce the percentage yield and lower prices increase it, all else equal. Remember that total return includes price movement and taxes, not just the dividend amount. This means a stock could deliver a modest dividend but strong price appreciation, or vice versa, influencing overall performance. For those comparing dividend opportunities, it helps to look at historical payout consistency and the longer-term trend in the stock's returns rather than a single payout event.

Yield calculation basics

As a simple illustration, if a share trades around Rs 6,000 and pays Rs 13 in annualized dividend, the nominal yield from this payout is about 0.22% before tax and after price effects are considered. That figure would change with the actual trading price on the ex-date. In practice, many investors weigh such dividends against alternative income options and volatility risk, while also considering how the dividend aligns with their investment horizon and risk profile.

Practical steps for investors

To qualify for the Rs 13 dividend, you should hold HDFC Bank shares before the ex-date of 19 June 2026 and remain registered on the record date. If you acquire shares on or after the ex-date, you would typically miss this payout. Since the notice does not provide book closure dates, it is wise to confirm the exact timeline from official filings or the exchange. Aligning trading plans with corporate actions helps ensure you receive expected income without disrupting other parts of your strategy.

For retail investors, platforms like Swastika Investmart provide research snippets and market updates that help track corporate actions such as dividends. These resources can simplify understanding of when payouts are expected and how to position your portfolio accordingly. By staying informed, investors can avoid missing out on eligible dividends due to timing issues.

It is also worth noting the tax implications of cash dividends. In India, dividend incomes are generally taxable as part of total income, and tax treatment can vary across regimes and years. Investors should consult a tax advisor to understand how the Rs 13 per share payout fits into their personal tax situation and overall investment plan.

Tax considerations and corporate actions

Dividend payments are a form of shareholder value distribution and are distinct from capital gains. Regulatory filings and exchange notices remain the most reliable source for payout timing and any related corporate actions, including changes in capital structure or shareholder registers. Keeping an eye on these sources can help investors adjust expectations and avoid surprises around payout timing or eligibility.

Conclusion

The Rs 13 per share dividend for HDFC Bank, with ex-date and record date lined up for 19 June 2026, provides a defined income event for shareholders. While the headline amount is straightforward, the real takeaways include understanding eligibility, the interaction with stock price on the ex-date, and how this payout fits into a broader investment plan. Staying informed through official channels and reliable market updates supports a disciplined approach to dividend investing.

Frequently Asked Questions

What is the ex-date for HDFC Bank's dividend?

The ex-date is 19 June 2026, which determines who qualifies to receive the Rs 13 per share dividend.

How much dividend is being paid per share?

Rs 13 per equity share for the series EQ.

Why is the record date important?

The record date identifies shareholders who are eligible to receive the dividend; you must be registered as a holder by the record date.

Rupee almost breaches 96/$ before clawing back

Quick Takeaways

• Rupee approached 96 per dollar due to foreign outflows, oil costs, and BoP concerns.

• RBI intervened intraday to curb volatility, but the close remained weaker.

• Possible tax cuts for foreign bondholders could influence capital flows.

• Oil prices, inflation trends, and BoP data will shape the next move.

Across trading sessions, the Indian rupee edged toward the 96 per dollar level, stirring attention from policymakers, traders, and households. A combination of sustained foreign fund outflows, higher prices for crude oil, and lingering concerns about the balance of payments contributed to the slide. While the move was sharp at times, the intraday recovery shown by the RBI's intervention reminded markets that currency stability remains a priority for the authorities.

The Drivers: Outflows, Oil, and BoP

Foreign money has been shifting away from Indian assets amid broader risk-off sentiment and global rate moves. Such outflows reduce demand for the rupee and press the currency lower as investors convert holdings into dollars.

At the same time, rising oil costs—India's large importer—feed through into the import bill and pressure the current account. Even with robust growth, energy and commodity prices can tilt the macro balance and influence exchange rate expectations. The BoP position remains a focal point for traders tracking the currency's medium-term path.

RBI’s Response and Market Signals

Market participants noted RBI steps that appeared aimed at curbing excessive volatility. The central bank managed liquidity and used its market tools to cushion the fall, helping the rupee claw back from the intraday low. The rally was modest, and the currency ended the session softer than the start, signaling limits to intervention in a volatile environment.

Market Signals and Policy Credibility

Comments from traders and analysts suggest that while the RBI can stabilize price action in the near term, sustained gains depend on clear macro signals and credible inflation management. The currency's resilience will hinge on how policy remains aligned with external developments and how quickly domestic data support a disciplined stance.

Bond Tax Breaks and Global Flows

In market notes, Swastika Investmart analysts point to a mix of oil-driven inflation and persistent outflows as the main drivers of the rupee's weakness. They say policy signals like potential tax cuts for foreign bondholders could influence investor appetites, though much depends on global risk sentiment. The note also highlights that the rupee's path remains highly responsive to oil prices and BoP data.

Beyond these considerations, any policy proposals that could alter foreign appetite for Indian bonds will be watched closely. If the government signals credibility and fiscal support, foreign participation might rise in the debt market, easing some external pressures. Still, markets will test the durability of such measures against evolving global financial conditions.

Implications for Markets and Households

For importers and borrowers with dollar-linked obligations, a weaker rupee translates into higher local-currency costs. Banks may adjust lending rates and hedging costs as currency risk is priced into financial products. Consumers can feel the impact through energy bills and prices for items tied to global commodity prices, even when headline inflation shows signs of cooling.

Exporters could benefit from a softer rupee by converting foreign earnings into more rupees, supporting margins in sectors tied to overseas demand. The real-world outcome, however, depends on how long external shocks persist and how quickly inflation and oil prices settle. In short, currency dynamics add a practical layer to daily financial decisions for households and firms alike.

Conclusion

The near-96 per dollar level is a stark reminder of the balance between external forces and domestic policy. RBI interventions can stabilize sentiment in the short run, but the longer arc will hinge on inflation trajectories, energy prices, and the evolution of foreign capital flows. With BoP data and global market conditions continuing to drive sentiment, investors and watchers will stay tuned to both data releases and policy messaging.

Frequently Asked Questions

Why did the rupee approach 96 per dollar?

A mix of foreign fund outflows, higher oil prices that raise import costs, and concerns about the balance of payments pushed the currency toward the 96/$ level.

How does RBI intervention affect currency moves?

Intervention can stabilize sentiment in the short term by providing liquidity or signaling commitment, but it may not reverse longer-term trends if fundamentals remain weak.

What impact could bond tax breaks have on foreign investment?

Tax incentives could attract more foreign capital into India's debt market, potentially easing external pressures if credibility and policy framework remain solid.

What should investors watch next for the rupee?

Key factors include oil prices, inflation trends, BoP data, and any new policy signals regarding foreign investment in bonds.

Tata Motors PV shares rally 8% even as Q4 net profit drops 32% YoY. Here's what Macquarie, Jefferies & other brokerages say

Quick Takeaways

• Shares of Tata Motors Passenger Vehicles rose about 8% even as Q4 FY26 net profit declined 32% YoY.

• Revenue from operations increased and a final dividend was recommended.

• Brokerages offered mixed views, with some bullish and others cautious about Jaguar Land Rover and the outlook.

• Key risk remains Jaguar Land Rover performance and the timing of product launches and margin recovery.

Tata Motors PV rally amid mixed Q4 signals

Q4 FY26 numbers and dividend cue

Tata Motors Passenger Vehicles reported a 32 percent year on year decline in the fourth quarter net profit, a drop that many saw as a test of how well the company can manage costs and push margins higher. At the same time, revenue from operations rose, supported by a steady demand for passenger cars in India and a favorable mix of higher value models. The company also recommended a final dividend, signaling cash generation remained healthy despite the profit dip.

Brokerage views split on the stock

Brokerages offered a range of opinions. Macquarie and a handful of other brokers stayed constructive about Tata Motors, pointing to domestic market strength and the potential for margin expansion as new models land and cost controls take hold. Jefferies took a more cautious tone, flagging that the performance of Jaguar Land Rover remains a key risk and that external factors like currency and inflation could limit upside in the near term. Several other brokers acknowledged upside if JLR stabilizes and the Indian PV business accelerates, but warned that failure to translate revenue growth into steady profit could cap gains.

Jaguar Land Rover under the spotlight

Jaguar Land Rover continues to cast a shadow over the group's earnings trajectory. Analysts cite softer demand in key markets, pricing pressures, and the challenge of bringing a competitive product lineup to market in a timely fashion. While Tata Motors has been gaining ground in India with affordable and feature-rich PVs, JLR's profitability remains the swing factor that could determine the overall margin profile of the parent company.

Swastika Investmart notes that while the day's stock move reflects some optimism around Tata Motors' domestic PV prospects, investors should remain mindful of JLR risks and the timing of new launches. The broker also suggests monitoring the cost structure and any progress on reducing debt, as these levers could tilt the risk-reward balance in coming quarters.

Takeaways for investors

Investors should watch for signs of margin recovery in the auto maker's global operations and whether the domestic PV demand can sustain revenue gains. The dividend proposal adds a cash return aspect that can support stock appeal, but profitability must improve to sustain upside. The trajectory of Jaguar Land Rover will likely set the pace for the overall stock's risk/reward, especially if European markets stabilize and new models enter high-demand segments.

What to watch next

Beyond quarterly numbers, the focus will be on product launches, cost management, and how Tata Motors balances growth with profitability across its two main geographies. If JLR can improve its margin profile while Tata Motors PVs gain share in the Indian market, the stock could extend its rally. Conversely, sustained pressure at JLR or a slower-than-expected ramp in new models could temper gains as investors reprice risk in the broader auto landscape.

Conclusion

Tata Motors PV's stock movement reflects a balance between near term profit softness and improving top line momentum, with a continued emphasis on JLR performance and new product execution as key drivers of the next leg of its rally.

Frequently Asked Questions

Why did Tata Motors PV shares rally despite a fall in quarterly profit?

Investors focused on rising revenue momentum, a proposed final dividend, and potential for margin improvement driven by product mix and cost actions, which offset the profit drop in the near term.

What role does Jaguar Land Rover play in Tata Motors' outlook?

JLR is the key earnings swing factor. Soft demand, pricing pressures, and execution of new models affect overall profitability and the potential upside from Tata Motors' India PV business.

What did brokerages say about Tata Motors after Q4 results?

Views were mixed: some firms remained bullish on long term growth and the domestic PV opportunity, while others cautioned about JLR headwinds and near term margin pressure.

What should investors monitor going forward?

Watch Jaguar Land Rover's performance and product launches, the pace of margin recovery, cash generation and dividend policy, and the strength of domestic PV demand.

Stocks To Watch Today: HAL, IRFC, Bharti Airtel, Zydus Lifesciences Among Key Shares In Focus

Quick Takeaways

• HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel are in focus for May 14.

• Sector impact spans defense, infra financing, telecom, pharma, and steel with potential intraday moves.

• Catalysts include earnings, order flow, policy cues, and macro data shaping sentiment.

• Watch price action around key levels and upcoming results to gauge near-term direction.

May 14 Stocks to Watch: HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel

May 14 could shape up as a day of selective moves in Indian markets, with a handful of heavyweight names in focus as traders digest a mix of company updates, sector catalysts, and global cues. While broad questions about the macro environment linger, stock-specific developments in defense, rail capex, telecom, pharma, and steel are likely to drive intraday action. For new investors, this is a day to observe how price action responds to fresh information rather than rushing into trades on headlines alone. The current setup underscores the importance of liquidity, risk control, and a clear plan for entry and exit around key levels.

Market backdrop

Across the broader market, liquidity conditions and the trajectory of interest rates shape how investors react to stock-specific catalysts. The sectors represented by HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel tend to move in response to government spending signals, regulatory updates, and macro data prints. Traders will be watching how indices handle the day’s news flow, whether there is broad participation or a dispersion where only select names push higher. In such environments, stickiness around technical support and resistance can offer clues about the prevailing momentum and risk appetite.

As noted by market observers, the day’s rhythm may hinge on how upcoming earnings and guidance align with the sector’s longer-term narratives. In a market that has shown sensitivity to policy commentary and earnings cadence, price action around key moving averages and volume spikes often serves as a proxy for conviction. With May’s agenda centering on macro resilience and corporate updates, active traders may look for signals that confirm a sustainable tilt rather than isolated bursts of volatility.

As highlighted by Swastika Investmart, traders should watch for price consolidation around key moving averages as today’s session unfolds. This approach helps capture intraday volatility linked to the stock-specific catalysts on HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel. The note emphasizes disciplined position sizing and attention to liquidity, given that results and commentary can trigger quick moves.

Hindustan Aeronautics Limited (HAL)

HAL’s price action is closely tied to the defense budget calendar and the pace at which programs move from order to delivery. Investors will scrutinize the company’s latest project updates, export orders, and the mix between domestic procurement and overseas contracts. A steady stream of orders and clear milestones on helicopter and aircraft programs can bolster earnings visibility, potentially supporting upside momentum. Conversely, delays or shifts in program timelines can weigh on sentiment, making risk management essential in intraday trading and swing setups alike. The stock often experiences volatility around quarterly results as margins hinge on production efficiency and cost controls within a defense-heavy revenue stream.

Indian Railway Finance Corporation (IRFC)

IRFC’s fortunes ride on the rail capex cycle and the financing mix it can offer to infrastructure projects. With the government’s emphasis on rail modernisation and capacity expansion, IRFC’s borrowing program and yield profile are watched for signs of stabilisation or re-pricing in a rising rate environment. Investors will look for clarity on debt maturity profiles, credit outlook, and the companys capital allocation strategy as indicators of how sustainable its growth trajectory is. In trading terms, IRFC can attract interest when there is broader appetite for infra trades or when bonds rally on favorable liquidity conditions, but it may also correct if credit concerns surface or if financing costs climb faster than anticipated.

Bharti Airtel

Bharti Airtel remains at the center of telecom momentum, driven by 5G deployment, data consumption growth, and competitive dynamics with peers. Market participants will parse updates on ARPU trends, customer churn, and network expansion investments that support a stronger data experience. Tariff actions and regulatory developments can also influence near-term price action, as investors assess how much pricing power the company can sustain in a highly competitive landscape. Positive cues around subscriber growth and monetisation of 5G services could lift sentiment, while slower progress on tariff realignment or regulatory headwinds might constrain gains.

Zydus Lifesciences

Zydus Lifesciences offers exposure to a diverse generics portfolio and a pipeline of new products that can drive future growth. The stock reacts to regulatory updates, US approvals, and progress on key launches, as these elements impact both top-line expansion and margins. Pricing pressure in the generics market and competitive intensity pose challenges that traders monitor closely. Positive developments—such as timely regulatory clearances or successful launches—can provide a catalyst for a run-up, while setbacks on approvals or delays in launches may cap upside in the near term.

JSW Steel

JSW Steel sits at the intersection of global steel demand, input costs, and capacity utilization. The company’s margins depend on iron ore and coal prices, exchange rate movements, and the health of end-use sectors such as construction and manufacturing. If demand signals stay firm and input costs remain contained, JSW Steel could see supportive price action tied to a broader commodity cycle. Risks include spikes in raw material costs, potential demand-softening cues from external markets, or any policy shifts that alter steel pricing dynamics. Investors should watch volume trends and price resilience around key technical levels to gauge sustainability.

Trading considerations on May 14

Given the mix of sector themes, traders should focus on risk controls and liquidity. Tracking intraday price action around moving averages, watching for breakout or breakdown against volume, and keeping position sizes aligned with risk tolerance can improve the odds of capturing meaningful moves. It is also wise to monitor commentary from management teams and any regulatory updates that could derail or accelerate the pace of stock-specific changes. A disciplined approach—blending a short-term view with a sense of the underlying sector momentum—tends to serve beginners well on days with multiple catalysts.

Conclusion

HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel are likely to drive select intraday moves on May 14 as investors digest sector catalysts and corporate updates. A balanced view that respects risk controls and a clear plan for观察 entry and exit can help navigate potential volatility while keeping focus on the bigger story across defense, infra, telecom, pharma, and steel.

Frequently Asked Questions

Which stocks are in focus for May 14?

HAL, IRFC, Bharti Airtel, Zydus Lifesciences, and JSW Steel are highlighted as stocks to watch on May 14.

What factors could move these stocks today?

Earnings updates, order inflows or policy cues, sector-specific catalysts, and macro data can drive intraday moves for these names.

How should a beginner approach trading on such a day?

Focus on risk management, set clear stop-loss levels, monitor liquidity and volume, and avoid overexposure to a single stock amid mixed catalysts.

Where can I find more information about market movements today?

Refer to credible market analyses and news updates; this blog summarizes the key themes and stock-specific considerations for the day.

How to Read a Balance Sheet Without Being a CA

Quick Takeaways

- A balance sheet helps investors understand a company’s financial health.

- You do not need to be a CA to analyze assets, liabilities, and debt.

- Key sections include assets, liabilities, and shareholder equity.

- Simple ratios like debt-to-equity can reveal financial strength quickly.

- Reading balance sheets can help investors avoid weak companies and identify quality businesses.

Why Every Investor Should Learn to Read a Balance Sheet

Many retail investors in India avoid reading company financial statements because they believe balance sheets are only for Chartered Accountants or finance experts.

That is simply not true.

A balance sheet is actually one of the easiest financial statements to understand once you know what to look for. In fact, learning to read a balance sheet can help you make smarter investment decisions and avoid financially weak companies.

Think of it like a health report card for a business.

Just as doctors check blood pressure and sugar levels to understand your health, investors use balance sheets to understand a company’s financial condition.

If you invest in stocks directly or even follow the Indian markets regularly, knowing how to read a balance sheet is an extremely valuable skill.

What Is a Balance Sheet?

A balance sheet is a financial statement that shows:

- What a company owns

- What a company owes

- What remains for shareholders

It gives a snapshot of a company’s financial position at a specific point in time.

Every listed company in India is required to publish financial statements under SEBI and Companies Act regulations.

The balance sheet is generally divided into three major parts:

- Assets

- Liabilities

- Shareholders’ Equity

The basic formula is simple:

Assets = Liabilities + Shareholders’ Equity

This equation always balances, which is why it is called a balance sheet.

Understanding Assets

What Are Assets?

Assets are things a company owns that have value.

These could include:

- Cash

- Buildings

- Machinery

- Inventory

- Investments

- Receivables

Assets help a company run operations and generate revenue.

Current Assets vs Non-Current Assets

Current Assets

These are short-term assets that can be converted into cash within one year.

Examples include:

- Cash and bank balance

- Inventory

- Trade receivables

Higher current assets generally improve liquidity.

Non-Current Assets

These are long-term assets used for business operations.

Examples include:

- Land

- Plants and machinery

- Long-term investments

For example, companies like Tata Steel or Reliance Industries typically have large non-current assets because they operate capital-intensive businesses.

Understanding Liabilities

What Are Liabilities?

Liabilities are obligations or debts the company must pay.

In simple terms, this is the money the company owes to others.

Examples include:

- Loans

- Borrowings

- Creditors

- Outstanding expenses

Current Liabilities vs Long-Term Liabilities

Current Liabilities

These are obligations due within one year.

Examples include:

- Short-term loans

- Unpaid supplier bills

- Taxes payable

Long-Term Liabilities

These include debt payable over several years.

Examples include:

- Corporate bonds

- Bank loans

- Debentures

A company with excessively high debt can face financial stress during economic slowdowns.

This is why investors often monitor borrowing levels carefully.

Understanding Shareholders’ Equity

What Is Shareholders’ Equity?

Shareholders’ equity represents the owners’ stake in the company after subtracting liabilities from assets.

It includes:

- Share capital

- Retained earnings

- Reserves and surplus

In simple terms, this is what belongs to shareholders if all assets are sold and liabilities are repaid.

Companies with consistently growing reserves often indicate strong profitability over time.

Key Things Beginners Should Check First

Cash Position

A strong cash balance gives companies financial flexibility.

Companies with healthy cash reserves can:

- Handle economic slowdowns

- Invest in expansion

- Pay dividends

- Reduce debt

For example, several Indian IT companies maintain strong cash positions, which improves investor confidence.

Debt Levels

One of the easiest ways to judge financial health is by checking debt.

Too much debt can become dangerous, especially during rising interest rates.

A commonly used ratio is:

Debt-to-Equity Ratio

Debt-to-Equity Ratio=Total DebtShareholders’ Equity\text{Debt-to-Equity Ratio} = \frac{\text{Total Debt}}{\text{Shareholders' Equity}}Debt-to-Equity Ratio=Shareholders’ EquityTotal Debt

Generally:

- Lower ratio = safer company

- Higher ratio = more financial risk

However, acceptable debt levels vary across sectors.

Infrastructure and telecom companies usually carry higher debt compared to FMCG businesses.

Reserves and Surplus

Growing reserves often indicate the company is consistently profitable.

Investors usually prefer companies that steadily build reserves instead of depending heavily on borrowed money.

How to Spot Red Flags in a Balance Sheet

Rising Debt With Weak Profit Growth

If debt rises rapidly while profits remain stagnant, it could indicate financial pressure.

Declining Cash Reserves

Shrinking cash balances over multiple quarters may signal operational weakness.

High Receivables

If customers are delaying payments, receivables rise sharply.

This can create liquidity problems.

Frequent Equity Dilution

If companies repeatedly issue new shares to raise money, existing shareholders may face dilution.

Real-World Example

Imagine two companies in the same sector.

Company A has:

- Strong cash reserves

- Low debt

- Consistent reserves growth

Company B has:

- High debt

- Weak cash flow

- Falling reserves

Even if both companies report similar revenues, long-term investors are more likely to trust Company A because its balance sheet is healthier.

This is exactly why professional investors spend so much time analyzing financial statements before investing.

Why Balance Sheets Matter in Indian Markets

Indian markets have become more data-driven over the years.

Retail participation has increased sharply, especially after the rise of digital investing platforms.

Today, investors are not just looking at stock prices. They are evaluating:

- Debt levels

- Cash flows

- Corporate governance

- Financial strength

Companies with strong balance sheets often outperform during economic uncertainty because they can survive difficult market conditions more comfortably.

Simple Tips for Beginners

Start With Large Companies

Begin by reading balance sheets of large listed companies like Infosys, HDFC Bank, or TCS.

Their financial statements are easier to understand.

Compare Multiple Years

Do not analyze a single year in isolation.

Track trends across 3 to 5 years.

Use Annual Reports

Annual reports contain detailed explanations from management about business performance and risks.

Focus on Simplicity

You do not need to calculate dozens of ratios initially.

Even basic understanding of debt, cash, and reserves can improve your investing decisions significantly.

Final Thoughts

Reading a balance sheet is not as complicated as many investors think.

You do not need an accounting degree to understand whether a company is financially strong or weak.

By focusing on:

- Assets

- Debt

- Cash reserves

- Equity

- Financial trends

you can develop better confidence as an investor.

Over time, balance sheet analysis becomes one of the most powerful tools for identifying quality companies and avoiding unnecessary investment risks.

At Swastika Investmart, investors get access to SEBI-registered research insights, advanced trading tools, investor education resources, and dedicated customer support designed to simplify investing for beginners and experienced traders alike.

Frequently Asked Questions

What is the main purpose of a balance sheet?

A balance sheet shows a company’s financial position, including assets, liabilities, and shareholder equity.

Can beginners understand a balance sheet easily?

Yes, beginners can understand balance sheets by focusing on basic concepts like debt, cash, assets, and liabilities.

Why is debt important while analyzing a company?

High debt can increase financial risk, especially during economic slowdowns or rising interest rates.

What are current assets?

Current assets are short-term assets that can be converted into cash within one year.

Who regulates company financial reporting in India?

Listed companies in India follow financial reporting norms regulated by SEBI and the Companies Act.

Fixed Deposit vs Debt Mutual Fund — Which Is Actually Better?

Quick Takeaways

- Fixed Deposits offer stable returns and capital safety, making them suitable for conservative investors.

- Debt Mutual Funds provide better liquidity and potential tax efficiency for some investors.

- Interest rate cycles can impact debt fund returns more than FDs.

- Both investment options serve different financial goals and risk profiles.

- Choosing the right option depends on your investment horizon, taxation, and liquidity needs.

Why the FD vs Debt Mutual Fund Debate Matters

Indian investors have always loved Fixed Deposits. For decades, FDs have been the default investment option for people looking for stable returns and peace of mind. But over the last few years, Debt Mutual Funds have become increasingly popular among investors seeking flexibility and potentially better post-tax returns.

Now the big question is simple.

Which is actually better: Fixed Deposit or Debt Mutual Fund?

The answer depends on your financial goals, risk appetite, tax bracket, and investment timeline.

With interest rates changing frequently and market-linked products gaining traction, understanding the difference between these two options is more important than ever.

Understanding Fixed Deposits

What Is a Fixed Deposit?

A Fixed Deposit is a financial product offered by banks and NBFCs where investors deposit money for a fixed tenure at a predetermined interest rate.

The return is fixed at the time of investment, which makes FDs predictable and simple.

For example, if you invest Rs 5 lakh in a bank FD offering 7% annual interest for three years, you already know your maturity value in advance.

This certainty is the biggest reason why FDs remain popular among retirees and conservative investors.

Advantages of Fixed Deposits

Stable Returns

FDs are not affected by stock market volatility. Investors know exactly how much they will earn.

Capital Protection

Scheduled bank FDs are considered relatively safe. Deposits up to Rs 5 lakh per depositor per bank are insured under DICGC guidelines regulated by the Reserve Bank of India.

Simplicity

FDs are easy to understand and require minimal monitoring.

Drawbacks of Fixed Deposits

Taxation Can Reduce Real Returns

FD interest is fully taxable according to your income tax slab.

For investors in the 30% tax bracket, post-tax returns may fall significantly.

Inflation Risk

If inflation rises above FD returns, the real purchasing power of your money declines.

Limited Liquidity

Premature withdrawals may attract penalties and lower interest payouts.

Understanding Debt Mutual Funds

What Are Debt Mutual Funds?

Debt Mutual Funds invest in fixed-income securities such as:

- Government bonds

- Treasury bills

- Corporate bonds

- Commercial papers

- Certificates of deposit

These funds are managed by professional fund managers and regulated by SEBI.

Unlike FDs, debt fund returns are not fixed. They fluctuate based on interest rates, bond yields, and market conditions.

Advantages of Debt Mutual Funds

Better Liquidity

Most debt funds allow investors to redeem units quickly, often within one or two business days.

Potentially Higher Returns

In certain interest rate environments, debt funds can outperform traditional FDs.

Wide Range of Choices

Investors can choose funds based on duration and risk profile, including:

- Liquid funds

- Short-duration funds

- Corporate bond funds

- Gilt funds

Professional Management

Fund managers actively manage portfolios to optimize returns and manage risks.

The Taxation Difference Matters

FD Taxation

Interest earned on Fixed Deposits is added to your taxable income every year.

Banks also deduct TDS if interest exceeds prescribed limits.

Debt Mutual Fund Taxation

Debt mutual fund taxation changed significantly after recent amendments.

For investments made after April 1, 2023, gains from many debt mutual funds are taxed according to the investor’s income tax slab, similar to FDs.

This reduced one of the biggest historical tax advantages debt funds previously enjoyed.

However, debt funds may still offer flexibility in terms of timing withdrawals and tax planning.

Which One Performs Better During Interest Rate Changes?

FDs Benefit Slowly

When RBI increases repo rates, banks gradually raise FD rates.

New investors benefit from higher rates, but existing FD holders remain locked into older rates unless they reinvest.

Debt Funds React Faster

Debt mutual funds are directly impacted by bond market movements.

When interest rates fall, bond prices rise, which can boost debt fund returns.

This is why many investors prefer debt funds during anticipated rate-cut cycles.

However, rising interest rates can temporarily hurt debt fund performance.

Risk Comparison: FD vs Debt Mutual Fund

Fixed Deposits Carry Lower Risk

Bank FDs are generally safer, especially with large established banks.

Returns are fixed, and capital volatility is minimal.

Debt Funds Carry Market Risk

Debt funds are not risk-free.

Risks include:

- Interest rate risk

- Credit risk

- Liquidity risk

The Franklin Templeton debt fund crisis in 2020 reminded Indian investors that debt funds can face unexpected stress during market disruptions.

This is why investors must evaluate the quality of the underlying portfolio before investing.

Which Option Is Better for Different Investors?

Fixed Deposits May Be Better If:

- You want guaranteed returns

- You are risk-averse

- You are a retiree seeking predictable income

- You prefer simplicity

Debt Mutual Funds May Be Better If:

- You want higher liquidity

- You can tolerate some volatility

- You have short- to medium-term financial goals

- You understand interest rate cycles

Real-World Example

Suppose two investors each invest Rs 10 lakh.

Investor A chooses a 3-year FD at 7%.

Investor B invests in a short-duration debt fund during a falling interest rate cycle.

If bond yields decline over the next year, Investor B may generate better returns due to mark-to-market gains in the debt fund portfolio.

However, if interest rates rise sharply, FD returns may appear more stable and predictable.

This example shows that market conditions matter greatly in debt fund investing.

What Indian Investors Are Doing Today

Many Indian investors are now combining both products instead of choosing just one.

A common strategy includes:

- FDs for emergency funds and guaranteed income

- Debt funds for liquidity management and short-term investments

This balanced approach helps manage both safety and return expectations.

Final Verdict: Which Is Actually Better?

There is no one-size-fits-all answer in the Fixed Deposit vs Debt Mutual Fund debate.

If your priority is safety and guaranteed returns, Fixed Deposits remain a strong option.

If you want flexibility, liquidity, and the potential for better risk-adjusted returns, Debt Mutual Funds may suit you better.

The ideal choice depends on your:

- Financial goals

- Risk tolerance

- Tax situation

- Investment horizon

Before investing, it is important to evaluate your portfolio carefully and understand how each product fits into your broader financial plan.

At Swastika Investmart, investors get access to SEBI-registered research insights, smart investing tools, investor education resources, and dedicated customer support to make informed financial decisions confidently.

Frequently Asked Questions

Are Debt Mutual Funds safer than Fixed Deposits?

No, Debt Mutual Funds carry market-related risks, while bank Fixed Deposits generally offer more stable and predictable returns.

Can Debt Mutual Funds give higher returns than FDs?

Yes, in certain interest rate environments, debt funds may outperform Fixed Deposits.

Is FD interest taxable in India?

Yes, FD interest is fully taxable according to the investor’s income tax slab.

Who should invest in Debt Mutual Funds?

Investors seeking liquidity, diversification, and potentially better returns with moderate risk may consider Debt Mutual Funds.

Are Debt Mutual Funds regulated in India?

Yes, Debt Mutual Funds are regulated by the Securities and Exchange Board of India (SEBI).

.webp)

Q4 Earnings Roundup: Winners, Losers & Stocks in Spotlight After Market Hours

Quick Highlights

- Tata Motors CV, Oil India, NLC India, and Metropolis Health emerged as major earnings winners.

- DLF, Redington, and Man Infraconstruction reported pressure on margins and profitability.

- Several companies announced dividends, bonus issues, and expansion plans after market hours.

- Strong earnings momentum in energy, healthcare, and industrial stocks lifted investor sentiment.

- Q4 results continue to drive stock-specific action in the Indian market.

Q4 Earnings Season Keeps Dalal Street Busy

India’s Q4 earnings season is entering a crucial phase, and after-market-hour announcements are creating sharp movements in individual stocks. While benchmark indices have remained volatile due to global uncertainty and mixed macroeconomic signals, company-specific earnings continue to dictate market direction.

This earnings cycle has clearly shown one trend. Investors are rewarding companies with stronger profitability, stable margins, and clear growth visibility, while punishing businesses struggling with cost pressures and weak operational performance.

From Tata Motors Commercial Vehicles to Oil India and Bharti Airtel, several companies delivered strong quarterly numbers. On the other hand, companies like DLF, Redington, and Man Infraconstruction faced pressure on profitability despite revenue growth.

Let’s look at the biggest winners, losers, and stocks that could remain in focus in the coming sessions.

Earnings Winners That Stood Out

Tata Motors CV Delivered a Strong Quarter

Tata Motors’ commercial vehicle business reported an impressive operational performance in Q4.

Key highlights included:

- Revenue growth of 22.3%

- EBITDA growth of 35.6%

- Net profit jump of nearly 70%

- EBITDA margin expansion of 130 basis points

The company also announced a dividend of Rs 4 per share.

Despite higher input costs limiting margin expansion, investors may take comfort from the company receiving most regulatory approvals for the Iveco acquisition.

The strong numbers indicate healthy demand recovery in the commercial vehicle segment, which is closely linked to economic activity and infrastructure spending in India.

Oil India Surprised Positively

Oil India emerged as one of the strongest performers this earnings season.

The company reported:

- EBITDA growth of 30.7%

- Margin expansion of 530 basis points

- Net profit growth of 75.7%

Higher crude oil production and improved price realizations supported profitability.

The company’s move to form a joint venture for compressed biogas projects also aligns with India’s broader clean energy transition goals.

Energy stocks have remained in focus due to global crude oil volatility, and strong earnings from PSU oil companies are improving market sentiment.

Metropolis Health Showed Margin Strength

Healthcare diagnostics player Metropolis Health delivered a solid earnings performance.

The company reported:

- Revenue growth of 23%

- EBITDA growth of 73%

- Margin expansion of 740 basis points

- Net profit more than doubling YoY

This reflects improving operational efficiency and rising demand for organized diagnostic services in India.

Healthcare remains a structural long-term growth sector, supported by rising health awareness and increasing insurance penetration.

NLC India Posted Massive Profit Growth

NLC India surprised the Street with a sharp improvement in profitability.

Highlights included:

- Revenue growth of 31.5%

- EBITDA more than doubling

- Margin expansion of 1,270 basis points

- Net profit nearly tripling YoY

Strong operational performance in the power and mining business helped the company deliver one of the strongest quarters among PSU names.

Stocks That Stayed Resilient Despite Margin Pressure

Bharti Airtel Continued Stable Growth

Bharti Airtel posted steady quarterly numbers with healthy profit growth.

The telecom giant reported:

- Revenue growth of 2.6%

- Net profit growth of 10.5%

- Stable EBITDA margins near 57%

The company also declared a final dividend of Rs 24 per share.

India’s telecom sector continues to benefit from premiumization, rising data usage, and 5G expansion. Airtel’s consistent execution is helping maintain investor confidence despite intense competition in the sector.

LIC Housing Finance Maintained Profit Stability

LIC Housing Finance reported a slight decline in total income, but net profit still increased by 8.7%.

Housing finance companies remain closely linked to India’s interest rate cycle and property demand. With expectations of stable borrowing costs, investors are monitoring the sector carefully.

Zaggle Prepaid Continued Growth Momentum

Fintech player Zaggle Prepaid reported double-digit growth in revenue and profit.

The company’s corporate expense management and prepaid card business continues gaining traction as Indian businesses increase digital adoption.

Earnings Losers That Disappointed Investors

DLF Reported Weak Operational Numbers

Real estate giant DLF posted disappointing operational performance.

Key concerns included:

- Revenue decline of 42%

- EBITDA decline of 58%

- Margin contraction of 870 basis points

Although net profit remained largely stable due to one-time gains, the operational weakness could keep the stock under pressure in the near term.

The real estate sector has seen strong demand recovery recently, so weaker earnings from a market leader tend to attract investor attention.

Redington Faced Profit Pressure

Redington reported strong revenue growth, but profitability disappointed.

Net profit declined more than 41%, while EBITDA margins weakened.

This indicates that rising competitive intensity and cost pressures may be impacting earnings quality.

Man Infraconstruction Saw Sharp Margin Erosion

The company reported a major decline in operational performance.

Key concerns included:

- EBITDA down more than 82%

- Margin decline of over 2,300 basis points

- Net profit down 44%

Infrastructure and construction companies remain vulnerable to raw material inflation and project execution delays.

Dividend Announcements Added More Buzz

Several companies also announced shareholder-friendly actions.

Key announcements included:

- Bharti Airtel dividend of Rs 24 per share

- Tata Motors dividend of Rs 4 per share

- ZF Commercial dividend of Rs 4 per share and 5:1 bonus issue

- Balaji Amines dividend of Rs 11 per share

- CARE Ratings dividend of Rs 14 per share

- DLF dividend of Rs 8 per share

Dividend-paying companies often attract long-term investors seeking stable cash returns alongside capital appreciation.

What These Earnings Mean for Indian Markets

This earnings season highlights a broader market trend.

Companies with:

- Strong balance sheets

- Better margin management

- Stable demand outlook

- Sectoral tailwinds

are outperforming significantly.

Meanwhile, businesses facing cost inflation, margin pressure, or slower demand are witnessing stock-specific volatility.

The Indian market is currently highly selective. Investors are no longer rewarding revenue growth alone. Profitability, cash flow quality, and future guidance matter more than ever.

Sectors currently showing relative strength include:

- Telecom

- Energy

- Healthcare

- PSU power companies

- Industrial manufacturing

Why Investors Must Track After-Market Earnings Closely

Many sharp stock movements happen after earnings announcements made post market hours.

Professional traders and institutional investors analyze:

- Margin trends

- Management commentary

- Future guidance

- Dividend announcements

- Regulatory developments

before the next trading session begins.

This is why earnings season often creates overnight opportunities and risks for retail investors.

Using strong research tools and disciplined investing strategies becomes extremely important during such volatile phases.

Final Thoughts

The latest Q4 earnings batch delivered a mixed but insightful picture of India Inc.

While companies like Oil India, Tata Motors CV, Metropolis Health, and NLC India impressed with strong profitability and margin expansion, names like DLF and Man Infraconstruction faced operational stress.

As markets remain stock-specific, investors should focus on quality businesses with strong earnings visibility rather than reacting to short-term noise.

At Swastika Investmart, investors get access to SEBI-registered research support, advanced trading platforms, investor education, and responsive customer service designed to help navigate earnings season confidently.

Open your account today and stay updated with smarter market insights:

Open Account with Swastika Investmart

Frequently Asked Questions

Why are Q4 earnings important for investors?

Q4 earnings provide insights into a company’s annual financial performance, future outlook, profitability trends, and sector strength.

Which sectors performed well this earnings season?

Telecom, energy, healthcare, and PSU power companies showed relatively strong earnings momentum.

Why do stocks move sharply after market hours?

Companies announce earnings after market close, and investors react to revenue, profit, margins, and management commentary before the next session.

What is EBITDA margin?

EBITDA margin measures a company’s operating profitability as a percentage of revenue before interest, tax, depreciation, and amortization.

Why are dividend announcements important?

Dividends provide direct returns to shareholders and often indicate management confidence in the company’s financial strength.

Why Bharti Airtel's Africa Bet Could Be Its Biggest Wealth Creator in the Next 5 Years

Key Takeaways

- Bharti Airtel’s Africa business is becoming a major profit engine for the company.

- Rising smartphone adoption and digital payments in Africa offer massive growth potential.

- Airtel Africa’s improving margins and strong cash flow can boost shareholder value.

- Indian investors are closely tracking Airtel Africa as telecom growth in India matures.

- Long-term investors may see Africa as the next big trigger for Bharti Airtel stock.

Bharti Airtel’s Africa Story Is Getting Hard to Ignore

For years, Bharti Airtel’s Africa operations were seen as a risky international expansion. Many investors believed the company had overpaid when it entered Africa through the Zain Telecom acquisition in 2010. The business struggled with debt, currency volatility, and operational challenges across multiple countries.

But the narrative is changing rapidly.

Today, Airtel Africa is emerging as one of Bharti Airtel’s most valuable assets. With rising mobile penetration, increasing internet usage, and rapid digital payment adoption, Africa may become the company’s biggest wealth creator over the next five years.

As India’s telecom market becomes more mature and competitive, Airtel Africa gives Bharti Airtel a fresh runway for growth. This is one reason why many analysts now view the Africa business as a hidden gem within the telecom giant.

Why Africa Is Becoming a High-Growth Telecom Market

A Young and Digitally Hungry Population

Africa has one of the youngest populations in the world. Millions of consumers are entering the digital economy every year. Smartphone adoption is increasing rapidly, especially in countries like Nigeria, Kenya, Tanzania, and Uganda.

This creates massive demand for:

- Mobile internet

- Digital payments

- Online entertainment

- Financial services

- Data consumption

Unlike developed telecom markets where growth is slowing, many African nations are still in the early stages of digital transformation.

For telecom operators, this creates a long-term opportunity.

Low Banking Penetration Creates a Big Opportunity

One of the biggest growth drivers for Airtel Africa is mobile money.

In many African countries, traditional banking penetration remains low. Millions of people rely on mobile wallets for payments, transfers, and savings.

Airtel Africa’s mobile money platform is benefiting directly from this trend.

The company has been steadily increasing its customer base and transaction value in digital financial services. This segment also generates better margins compared to traditional telecom operations.

This is similar to how digital payment ecosystems transformed businesses in India after UPI adoption.

Airtel Africa Is No Longer Just a Revenue Story

Profitability Is Improving

Earlier, investors worried that Airtel Africa was only adding subscribers without generating meaningful profits.

That concern is fading.

The company has improved:

- Average revenue per user (ARPU)

- Data monetisation

- Operating margins

- Free cash flow generation

As data usage rises, telecom operators benefit because internet services are more profitable than traditional voice services.

Airtel Africa has also been reducing debt steadily, which improves investor confidence.

Currency Challenges Are Becoming More Manageable

African currencies have historically been volatile. This impacted Airtel Africa’s earnings in the past.

However, the company has improved its financial structure and diversified operations across several countries. This reduces dependence on a single economy.

While currency fluctuations still remain a risk, the business is now operationally stronger than it was a few years ago.

How This Impacts Bharti Airtel Shareholders

Africa Could Unlock Higher Valuation

Many market experts believe Bharti Airtel’s India business alone does not fully reflect the company’s future growth potential.

Airtel Africa adds another layer of value.

If the Africa business continues delivering strong growth in:

- Data subscribers

- Mobile money users

- Profit margins

- Cash generation

then investors may assign a higher valuation multiple to Bharti Airtel stock.

This can become a long-term wealth creation trigger.

Diversification Reduces Dependence on India

India’s telecom sector is already highly competitive despite tariff hikes.

Bharti Airtel’s international exposure helps diversify revenue streams. This reduces dependence on a single market and gives the company access to faster-growing economies.

For long-term investors, diversification is often viewed positively.

Comparison With Indian Telecom Trends

India’s telecom market has already seen massive consolidation. The focus now is on monetisation through:

- 5G services

- Premium data plans

- Enterprise solutions

- Digital ecosystems

Growth still exists, but subscriber expansion is slowing compared to earlier years.

In contrast, many African markets are where India was nearly a decade ago in terms of digital adoption.

That gives Airtel Africa significant room for expansion.

What Investors Should Watch Going Forward

Mobile Money Growth

This remains the biggest long-term opportunity.

If Airtel Africa successfully scales its fintech ecosystem, the business could evolve beyond telecom into a broader digital platform.

ARPU Expansion

Higher ARPU means customers are spending more on data and digital services.

Consistent ARPU growth is a strong indicator of improving profitability.

Regulatory Stability

Telecom businesses are heavily regulated. Investors should monitor policy changes across African countries, especially around spectrum, taxation, and digital payment services.

Indian investors are already familiar with how telecom regulations from authorities like TRAI impact company performance. Similar regulatory developments in Africa can influence Airtel Africa’s profitability.

Risks Investors Should Not Ignore

While the growth opportunity is large, risks remain.

These include:

- Currency depreciation

- Political instability in some regions

- Regulatory uncertainty

- Competition from local telecom players