The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

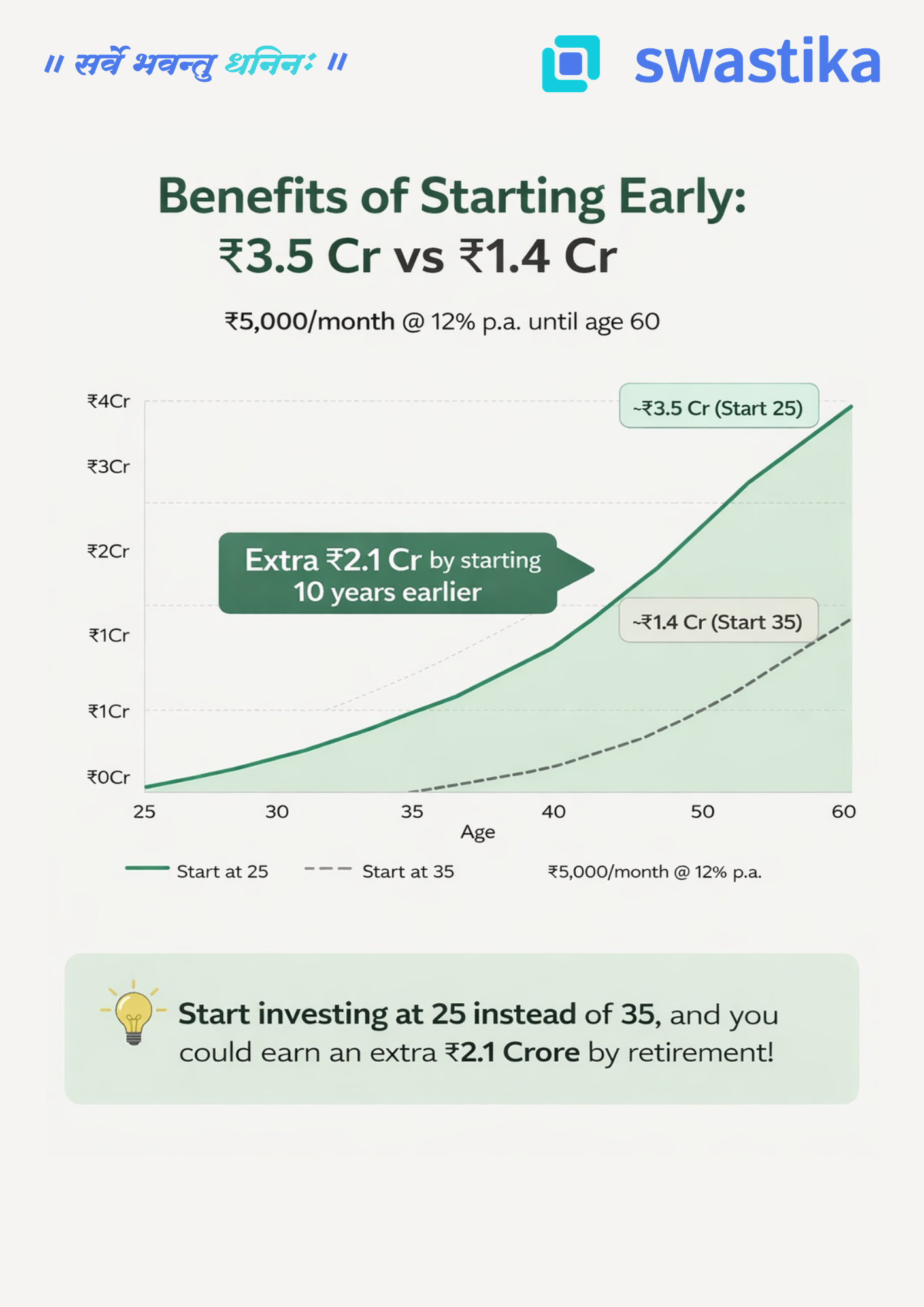

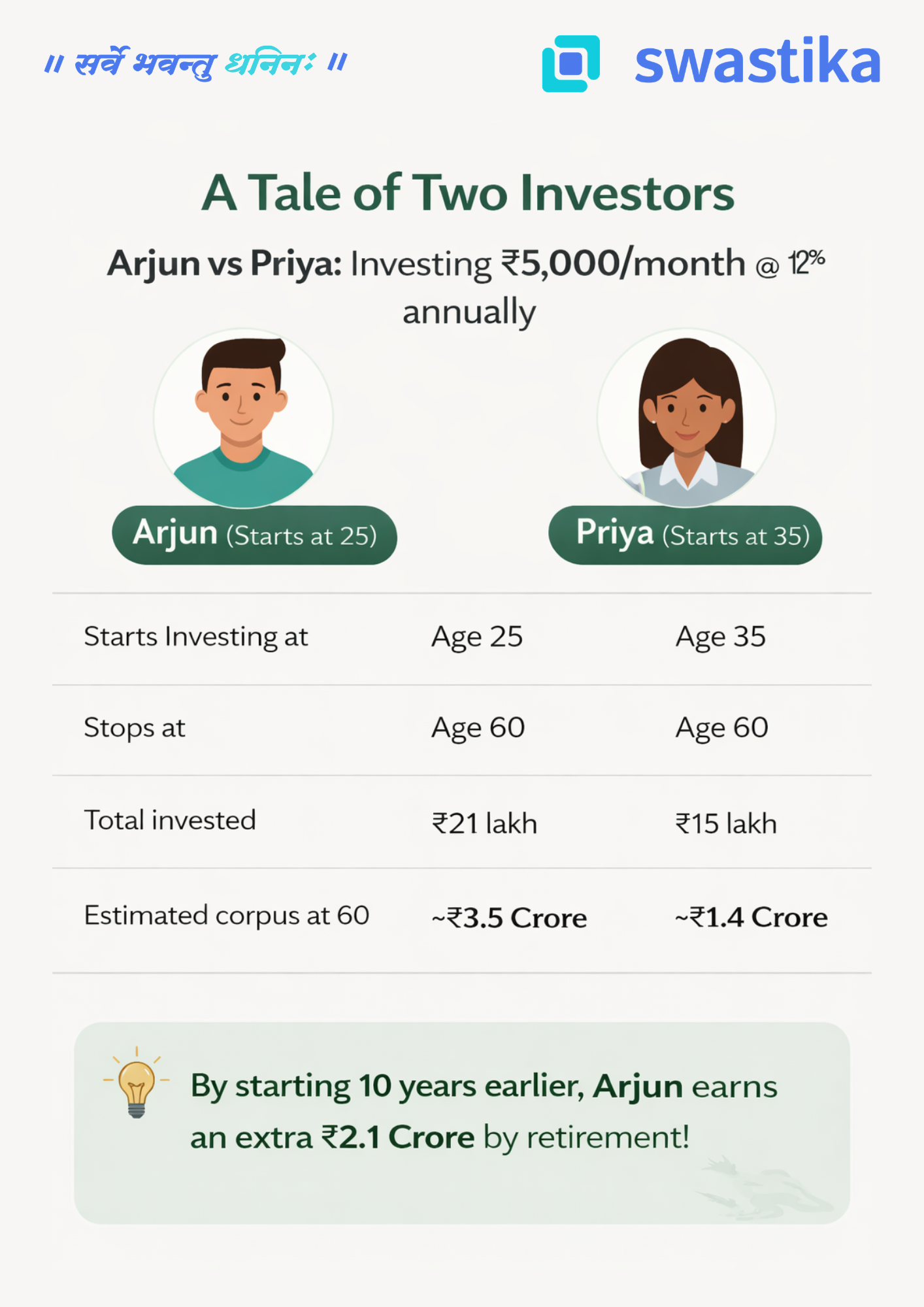

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

Dhanteras Investment Dilemma: Gold vs. Silver in the Current Market - Which is the Smarter Buy?

Key Takeaways

- Gold prices remain strong amid global uncertainty and central bank buying.

- Silver offers higher growth potential but comes with volatility.

- Experts suggest balancing both assets for portfolio stability.

- Gold ETFs and digital gold simplify investing for modern investors.

- Swastika Investmart helps you make smarter, research-backed investment decisions this festive season.

The Festive Gold Rush: Why Dhanteras Matters

Every Dhanteras, Indian households turn into mini investment hubs. It’s a day deeply rooted in tradition — symbolizing wealth, prosperity, and new beginnings. But this year, amid fluctuating global markets, rising inflation, and geopolitical tensions, one question stands out: “Should I invest in gold or silver this Dhanteras?”

Let’s decode this Dhanteras investment dilemma with a data-driven and research-backed approach.

Gold: The Timeless Guardian of Wealth

Gold has long been India’s favorite asset — not just for cultural reasons but for its proven ability to preserve value during uncertainty.

In 2025, gold prices have shown resilience, hovering around ₹71,000 per 10 grams (as of mid-October 2025), driven by:

- Central Bank Buying: Global central banks continue to accumulate gold to hedge against economic instability.

- Rupee Depreciation: The weaker rupee has further boosted domestic gold prices.

- Inflation Hedge: With inflation still a global concern, gold remains a safe haven.

Example: During 2020–2023, when equity markets were volatile, gold delivered an average annualized return of 10–12%, protecting investor portfolios.

However, the current trend indicates a consolidation phase — meaning that while gold remains a long-term wealth preserver, short-term upside could be limited.

Best Ways to Invest in Gold (2025):

- Gold ETFs (available on Swastika Investmart’s platform)

- Sovereign Gold Bonds (offered by RBI with 2.5% annual interest)

- Digital Gold via trusted platforms

- Physical gold (for traditional buyers)

Silver: The Underdog with Industrial Spark

Silver may not have the same emotional appeal as gold, but its dual nature — both as a precious and industrial metal — makes it extremely relevant in today’s green-tech economy.

In 2025, silver has been gaining traction due to:

- Industrial Demand: Silver is crucial for solar panels, EV batteries, and semiconductor production.

- Undervalued Pricing: At around ₹90,000 per kg, silver remains significantly cheaper than gold on a per-ounce basis.

- Volatility Advantage: While prices fluctuate more, they offer stronger returns during economic recovery phases.

Example: In FY24, silver outperformed gold globally, delivering ~20% returns amid the clean energy push.

However, investors must be prepared for price swings since silver’s demand is heavily tied to industrial growth cycles.

Ways to Invest in Silver (2025):

- Silver ETFs or ETPs

- Silver mini contracts on commodity exchanges

- Digital silver platforms

- Physical bars and coins

Comparing Gold vs. Silver: The 2025 Outlook

What Are Experts Saying This Dhanteras?

Market analysts believe that 2025 could be a pivotal year for precious metals. With the US Fed nearing rate cuts and global inflation cooling down, both gold and silver could shine — but in different ways.

- Short-Term (3–6 months): Silver may outperform gold due to industrial momentum.

- Long-Term (3–5 years): Gold remains the better hedge against systemic risks.

According to Swastika Investmart’s commodity research team, investors should consider a balanced allocation — 70% gold and 30% silver — to capture both stability and growth.

Real-World Scenario: How Investors Are Reacting

Let’s take an example — Meera, a 35-year-old professional from Mumbai. Last Dhanteras, she invested ₹1 lakh in gold ETFs and ₹50,000 in silver coins.

Today, her gold investment has grown moderately (~7%), while silver has delivered nearly double-digit gains, thanks to industrial demand. This diversified approach helped her balance returns and risk — a strategy that reflects modern investor sentiment.

How to Make Smarter Investments This Dhanteras

Dhanteras investments should not just be emotional but strategic.

Here’s how you can approach it smartly with Swastika Investmart:

- Use Research-Backed Insights: Get expert market research on gold and silver price trends.

- Invest Digitally: Access Gold and Silver ETFs directly through Swastika’s user-friendly platform.

- Diversify Smartly: Allocate based on your financial goals and risk appetite.

- Stay Educated: Learn through Swastika’s investor education resources and webinars.

👉 Open your investment account today:

Start Investing with Swastika Investmart

FAQs

1. Is gold still a good investment in 2025?

Yes. Gold remains a strong hedge against inflation and global uncertainty, especially with central banks increasing their gold reserves.

2. Why should I consider silver this Dhanteras?

Silver offers higher potential returns due to its growing industrial demand, particularly in renewable energy and electric vehicles.

3. Which is safer: Gold or Silver?

Gold is safer due to lower volatility, while silver offers better short-term growth potential. A mix of both can balance risk and reward.

4. Are Gold ETFs better than physical gold?

Yes, for investors seeking liquidity, safety, and no storage hassles, Gold ETFs are a practical alternative.

5. How can I invest in precious metals with Swastika Investmart?

You can open an account online and invest in gold/silver ETFs, sovereign bonds, or other digital options easily through Swastika’s platform.

Conclusion

Dhanteras 2025 is not just about tradition — it’s about making informed financial choices. Whether you choose gold for stability or silver for growth, remember that the smartest investment is one backed by research and discipline.

Swastika Investmart empowers investors with expert insights, reliable tools, and tech-enabled platforms — making your festive investments secure and future-ready.

🎉 Invest Smartly. Celebrate Prosperity.

Open Your Account with Swastika Investmart

.webp)

Supply Glut Fears Hit Crude Oil — How Should Investors Position Themselves Now?

Key Takeaways

- The International Energy Agency forecasts a record oil glut of 4 million barrels per day in 2026.

- Oil prices have slid nearly 17% in 2025, trading near multi-month lows.

- Supply growth outpaces demand as OPEC+ ramps up production and demand remains weak.

- Indian markets are influenced by both price falls and currency movement, impacting inflation and sectoral performance.

- Investors should focus on sector rotations, hedging, and informed portfolio moves in this volatile environment.

Crude Oil Supply Glut: What’s Happening?

Global crude oil markets are undergoing a significant shift. After years of supply cuts, OPEC+ (including Russia) has started rolling back production curbs sooner than expected. The International Energy Agency predicts that the world could face a surplus of up to 4 million barrels per day in 2026, roughly 4% of worldwide demand. This surplus is intensified by tepid demand, with economic growth forecasts being trimmed for major markets. As a result, oil prices dropped by 17% so far in 2025, with Brent trading near $62 and WTI below $59 per barrel — the lowest levels seen in five months.

Real-World Example:

In April 2025, OPEC+ announced faster output restoration. By September, global supply had already risen by more than 3 million barrels per day, outstripping demand growth. The result: traders now anticipate Brent staying below $60 for an extended period, with timespreads flipping into contango — signaling excess near-term supply and lower spot prices moving forward.

How Does This Impact Investors?

For Indian Market Participants:

Crude oil is central to India’s economy, with over 80% of consumption met via imports. Low prices can ease inflation pressures, improve trade deficits, and strengthen the rupee in the short term. However, sectors that rely on oil, such as upstream exploration and refining, may see profit margins squeezed, while downstream users (aviation, paints, adhesives, transport) could benefit from reduced costs.

Market Context:

- Oil exploration companies (ONGC, Oil India) typically suffer from low prices, whereas refiners and large consumers gain.

- Currency impacts: Cheaper oil can help stabilize the rupee, cushion inflation, and influence RBI policy.

- Equity flows: Lower oil prices may support equity valuations in affected sectors and help dampen overall inflation.

Regulatory Perspective:

India’s government and RBI closely monitor import bills, currency flows, and inflation data. Decisions on fiscal and monetary policy — such as interest rates or excise duties — are often calibrated with crude price movements.

Investor Strategies in an Oil Glut

With record supply likely to depress prices further, investors should consider these approaches:

- Sector Rotation: Focus on industries benefiting from lower input costs (aviation, paints, chemicals, transport), and remain cautious with oil producers.

- Hedging & Diversification: Use commodity-linked ETFs or futures, and diversify portfolios to mitigate sector-specific risk.

- Currency Watching: Track rupee-dollar movements to anticipate potential gains or risks for export-oriented and import-dependent sectors.

- Policy Signals: Watch for RBI and government interventions that may impact interest rates, excise duties, or sectoral support.

Relatable Scenario:

An investor exposed to ONGC shares may consider trimming positions or switching to airline stocks or FMCG firms that gain from cheaper energy costs. Portfolio balance is critical, and commodities can be used for hedging when markets are volatile.

Frequently Asked Questions

Q: Why are oil prices falling despite OPEC+ supply actions?

A: OPEC+ is increasing output faster than demand growth, resulting in oversupply and downward price pressure.

Q: What does a supply glut mean for Indian investors?

A: It can support sectors consuming oil, reduce inflation, and influence government monetary policy — but could hurt oil producers and exporters.

Q: Should I buy or avoid energy stocks now?

A: Consider sector trends; downstream users often benefit when oil is cheap, while upstream producers risk margin contraction. Diversification is key.

Q: How does the rupee respond to falling oil prices?

A: Lower oil import bills strengthen the rupee and dampen inflation, but global currency trends can still introduce volatility.

Q: Where can I learn to position my portfolio more effectively?

A: Leverage platforms like Swastika Investmart for comprehensive research, strategy tools, and investor education on commodity market trends.

Conclusion

The record oil surplus reshaping markets in 2025–26 means investors must adapt. Focusing on sector rotation, hedging, and attention to macro trends will help navigate volatility and identify new opportunities. With Swastika Investmart’s SEBI registration, advanced research, and pro investor support, you can position your portfolio smartly for evolving market conditions.

.webp)

Persistent Systems Q2 2025 Performance Analysis: Revenue, Profit & Outlook

Key Takeaways

- Q2 2025 revenue jumped 23.6% YoY to ₹3,580 crore; profit rose 45% YoY to ₹471 crore.

- EBIT margin expanded to 16.3% and operational efficiency improved significantly.

- Order bookings remained strong with $609.2 million TCV.

- Share price jumped 7% post-results, reflecting investor confidence.

- Swastika Investmart offers robust research tools and support for tech sector investing.

Persistent Systems Q2 2025: Revenue, Profit & Outlook

India’s mid-cap IT giant Persistent Systems continues to deliver robust results despite global and domestic market challenges. The Q2 2025 earnings not only surpassed analyst expectations but also highlighted Persistent’s operational agility, AI strategy, and broad-based demand.

Persistent’s Q2 FY26 Financial Performance: By the Numbers

For the quarter ended September 30, 2025, Persistent Systems reported consolidated revenue of ₹3,580 crore — a 23.6% year-on-year surge, and an impressive 7.5% sequential growth over Q1. Dollar revenue rose to $406.2 million, up 17.6% YoY.

Bottom line performance was even stronger:

- Net profit (PAT) soared 45.1% YoY to ₹471.4 crore, beating estimates handsomely.

- EBIT (operating profit) rose 43.7% YoY to ₹583 crore, giving an expanded margin of 16.3%, up 71 basis points QoQ.

The EBIT margin expansion signals a sharp improvement in operational efficiency, even as global IT spending showed signs of volatility during the period.

Order Wins, Business Momentum & AI Edge

Persistent’s order book momentum remained strong with Total Contract Value (TCV) for the quarter at $609.2 million and Annual Contract Value (ACV) at $447.9 million. Growth was broad-based across BFSI, healthcare, and product engineering services, with the company leveraging its domain strengths and proprietary AI solutions for digital transformation.

Leadership cited their platform-led AI strategy as a key differentiator, helping global clients modernize operations and drive measurable business value. The company’s ongoing partnerships with hyperscalers and strategic enterprise customers continue to drive annuity revenues.

Market Impact & Share Price Response

Persistent’s strong results led to a 6–8% rally in its stock price, touching new highs as investors and brokers upgraded their outlook for the stock and sector. The company’s consistency, marked by its 22nd consecutive quarter of revenue growth, has bolstered market confidence even as some peers struggle with margin compression.

Examples from the recent analyst calls include enthusiastic responses to Persistent’s ability to manage wage hikes and cost pressures, with management sharing a clear roadmap to sustain margins even as wage costs rise in Q3.

Indian Market Context & Regulatory Notes

Persistent’s performance comes amid a broader wave of resilience among India’s leading IT and digital engineering firms. The company operates in full compliance with SEBI and Indian IT regulatory frameworks, maintaining best-in-class transparency in reporting and IR practices. As India’s digital transformation deepens — supported by government initiatives and Digital India policy — Persistent’s services remain well-placed to benefit from expanding technology adoption.

Swastika Investmart: Smart Investing in the Indian Tech Sector

For investors aiming to participate in the tech sector’s growth, Swastika Investmart offers a SEBI-registered platform with excellent research, tech-powered tools, and customer support. Its ongoing commitment to investor education ensures smarter decisions and a seamless investing experience in Indian and global IT stocks.

FAQs

Q: What was Persistent Systems’ Q2 2025 revenue and profit?

A: Revenue was ₹3,580 crore (up 23.6% YoY), and net profit was ₹471.4 crore (up 45% YoY).

Q: Why did margins improve this quarter?

A: Expanded EBIT margin (16.3%) was due to operational efficiency, higher-value order wins, and cost management.

Q: How did the market respond to Persistent’s Q2 results?

A: The stock rallied 6–8% post-results, reflecting investor optimism and positive broker upgrades.

Q: What is the outlook for upcoming quarters?

A: Persistent targets continued growth, with a focus on AI, digital platforms, and managing wage-cost impacts in Q3.

Q: Why should investors consider Swastika Investmart?

A: For research-backed IT stock investing, SEBI compliance, and investor support, Swastika Investmart stands out in the market.

Conclusion

Persistent Systems’ Q2 2025 performance underscores its operational excellence, tech-forward growth strategy, and resilience in a competitive sector. As digital acceleration in India creates new investment opportunities, aligning with a trusted platform like Swastika Investmart can help investors make informed, confident choices.

.webp)

ICICI Lombard Q2 Earnings Breakdown: What the Numbers Mean for Investors

Key Takeaways

- ICICI Lombard’s Q2 FY26 net profit surged 18% YoY to ₹820 crore.

- Gross Direct Premium Income (GDPI) declined 1.9% YoY, but core business showed resilience.

- Board declared interim dividend of ₹6.50/share, up from ₹5.50 last year.

- Retail health and fire segments led growth; motor insurance faced moderate challenges.

- Swastika Investmart empowers investors with research, tech tools, and education.

ICICI Lombard Q2 Earnings 2025: What the Numbers Mean for Investors

India’s non-life insurance sector continues to show dynamism, and ICICI Lombard’s Q2 FY26 results are an eye-opener for investors tracking the industry’s future trajectory. As the second largest private insurer, ICICI Lombard’s latest financial disclosures highlight resilience in a mixed market environment.

Understanding ICICI Lombard’s Q2 FY26 Performance

ICICI Lombard reported an 18% year-on-year rise in net profit for the second quarter, reaching ₹820 crore compared to ₹694 crore last year. This growth came despite a small dip in its Gross Direct Premium Income (GDPI), which stood at ₹6,596 crore—a decline of 1.9% YoY. Excluding crop and mass health business, core GDPI rose 3.5%, showing strength across retail health and fire segments.

Key Financial Metrics

Investors and industry watchers closely monitor the combined ratio—a measure of underwriting profitability. ICICI Lombard’s combined ratio in Q2 was 105.1%, slightly up from 104.5% a year ago but competitive for the sector. The company maintained a healthy solvency ratio of 2.73x, well above the regulatory minimum of 1.5x.

- Net Profit: ₹820 crore (+18% YoY)

- GDPI: ₹6,596 crore (-1.9% YoY; +3.5% ex-crop & mass health)

- Combined Ratio: 105.1%

- Interim Dividend: ₹6.50/share

- Solvency Ratio: 2.73x

Real-world Market Impact

ICICI Lombard shares responded positively to earnings, rallying by 7–8% after the release, reaching multi-month highs and drawing robust volumes on NSE. Investors noted strong momentum in retail health and fire insurance, with revenue from retail health premiums up over 12% YoY. The motor insurance segment underperformed due to subdued vehicle sales and competitive pricing pressures, but sector analysts maintain optimism for recovery as government and GST-led vehicle sales rebound.

Regulatory Landscape and Accounting Adjustments

This quarter’s GDPI numbers are not directly comparable with last year, as India’s insurance regulator introduced the “1/N accounting method” for long-term products, impacting premium recognition timing. The solvency ratio, however, remained sturdy and comfortably above regulatory requirements by IRDAI (Insurance Regulatory and Development Authority of India).

What It Means for Investors

Strong net profit, interim dividend, and robust solvency metrics highlight ICICI Lombard’s ability to navigate sector headwinds and regulatory changes. Leadership set an ambitious ROE target of 18–20% for the full year, signaling continued focus on shareholder value. Retail health and fire insurance are clear growth drivers, while the motor insurance segment remains a watchpoint for Q3 and Q4.

Swastika Investmart: Your Trusted Partner for Informed Investing

For those seeking to invest in India’s financial markets, Swastika Investmart offers SEBI-registered reliability, comprehensive research, customer support, and technology-enabled execution—integral for making informed insurance sector investments. The platform’s ongoing investor education ensures you stay ahead in a rapidly evolving landscape.

FAQ Section

Q: What was ICICI Lombard’s net profit in Q2 FY26?

A: The company posted a net profit of ₹820 crore, an 18% increase YoY.

Q: Why did GDPI decline this quarter?

A: GDPI dipped 1.9% YoY due to new accounting standards and a drop in crop and mass health segments, but core business showed growth.

Q: What is ICICI Lombard’s combined ratio for Q2 FY26?

A: The combined ratio stood at 105.1%, reflecting underwriting pressure but operational resilience.

Q: Was a dividend declared?

A: Yes, an interim dividend of ₹6.50 per share was announced, up from the previous year.

Q: What segments are driving growth?

A: Retail health and fire insurance outperformed this quarter, while motor insurance faced challenges.

Conclusion

ICICI Lombard’s Q2 results offer important signals for investors—core profitability remains robust despite market and regulatory pressures. With leadership targeting further ROE growth and new insurance regulations in play, now is a strong time to evaluate opportunities in Indian insurance stocks. Swastika Investmart’s research, tech tools, and investor education can help you make smarter decisions in this dynamic sector. Take the next step in your investing journey today.

%20(1)%20(4).webp)

Muhurat Trading 2025: Date, Time, and Historical Market Trends You Must Know

Key Takeaways

- Muhurat Trading 2025 falls on 21st October, Tuesday, from 1:45 PM to 2:45 PM IST .

- This auspicious one-hour trading marks the start of the Hindu new financial year (Samvat 2082).

- Historically, Muhurat Trading blends tradition with modern investing optimism in India.

- Key stocks to focus on from Diwali 2025 to Diwali 2026 include INDIGO, MCX, SBIN, BAJAJFINANCE, and others.

- Swastika Investmart offers a powerful blend of SEBI registration, tech tools, and investor education for smart trading.

Introduction

Muhurat Trading is a unique tradition in Indian stock markets where exchanges open for a symbolic one-hour session on Diwali day. This year, the special session will be held on Tuesday, 21st October 2025, from 1:45 PM to 2:45 PM IST. Marking the beginning of the Hindu Samvat year 2082, this session brings together centuries-old auspicious beliefs with today’s vibrant market sentiment.

What is Muhurat Trading?

The word ‘Muhurat’ signifies an auspicious time when planetary alignments are thought to favor positive outcomes. Muhurat Trading is the practice of executing trades during this spiritually auspicious hour, believed to bring wealth and prosperity through the year. Since the Bombay Stock Exchange began this in 1957, and the NSE since 1992, Muhurat Trading has evolved into a cherished blend of culture and commerce, carrying deep symbolic value for investors.

Muhurat Trading 2025 Timings & Market Context

In 2025, Muhurat Trading will take place from 1:45 PM to 2:45 PM IST, an afternoon slot different from the usual evening hours. Both NSE and BSE participate in this session, which follows a pre-open session and a block deal segment to facilitate smooth trading. Though the market remains closed for the rest of the Diwali day, this hour sees heightened trading activity, marking the hopeful start of the new financial year. Trades carried out follow regular settlement rules while symbolizing good fortune for investors.

Historical Market Trends and Significance

The tradition is more than symbolic; it encourages investment spirit and positive market sentiment at the year’s start. Over decades, Muhurat Trading has often coincided with bullish trends post-Diwali, reflecting renewed investor confidence and fresh capital inflows. It’s also common for families to perform a ritualistic puja of their trading accounts, blending spiritual faith with financial ambitions. Many investors treat this session as a time to buy blue-chip stocks or quality assets they intend to hold long-term.

Top Diwali Picks 2025 (Duration:1 Year)

Why Choose Swastika Investmart for Muhurat Trading?

Swastika Investmart stands out with SEBI registration ensuring compliance and trustworthiness. The platform delivers powerful research tools enabling data-driven decisions. Its customer support aids investors at every stage, and tech-enabled services simplify trading experiences. Moreover, Swastika Investmart’s commitment to investor education helps novices and experts to align strategies with market realities, making it an excellent choice this Muhurat Trading season.

Frequently Asked Questions

Q: When is Muhurat Trading in 2025?

A: Muhurat Trading will be held on Tuesday, 21st October 2025, from 1:45 PM to 2:45 PM IST.

Q: What is the significance of Muhurat Trading?

A: It marks an auspicious start to the Hindu new financial year, blending tradition with optimism for market growth.

Q: Can anyone participate in Muhurat Trading?

A: Yes, any investor with a trading account can trade during the Muhurat session.

Q: Are trades during Muhurat Trading treated like regular trades?

A: Yes, all trades have the same settlement rules as regular trading days.

Q: Which stocks are recommended for investment from Diwali 2025 to Diwali 2026?

A: Stocks like INDIGO, MCX, SBIN, BAJAJFINANCE, and others are promising based on market trends.

Conclusion

Muhurat Trading 2025 offers a special opportunity to blend heritage and modern investing, marking a hopeful start to Samvat 2082. By focusing on promising stocks like INDIGO and BAJAJFINANCE through the next year and leveraging platforms like Swastika Investmart for smart, compliant trading, investors can set a prosperous financial journey in motion. Open your account today and embrace this auspicious season with confidence.

.webp)

LG IPO: Will the Tech Giant’s Listing Be the Next Big Opportunity for Investors?

Key Takeaways

- LG Group is preparing for its IPO, expected to attract massive investor attention worldwide.

- The company’s strong brand equity and diversified product portfolio make it a potential blue-chip listing.

- Market experts foresee long-term growth, but valuations and global market volatility need careful assessment.

- The IPO could influence investor sentiment across the global tech and consumer electronics sectors.

- Swastika Investmart offers SEBI-registered research and expert guidance to help investors make informed IPO decisions.

Introduction

In the ever-evolving global tech landscape, LG’s upcoming IPO is generating significant buzz among investors. Known for its innovation-driven products and global presence, LG is reportedly planning to list a key subsidiary — a move that could redefine its corporate structure and unlock immense shareholder value.

But the big question remains — Is LG IPO the next big opportunity for investors? Let’s dive deeper into the company’s fundamentals, market potential, and what this IPO could mean for Indian investors looking beyond domestic markets.

LG: A Global Powerhouse with Deep Market Roots

Founded in South Korea, LG has evolved from a home appliance manufacturer into a global technology conglomerate spanning electronics, chemicals, batteries, and renewable energy. The company has operations in over 100 countries, with India being one of its top-performing markets.

Its flagship arm, LG Electronics, is a household name in India, known for TVs, refrigerators, and smart appliances. Meanwhile, subsidiaries like LG Chem and LG Energy Solution (LGES) dominate sectors such as EV batteries and advanced materials.

LG’s strength lies in its diversified business portfolio — ensuring that a slowdown in one segment doesn’t drastically affect overall performance. This stability and global brand recognition make the IPO particularly appealing to both institutional and retail investors.

What Makes the LG IPO Stand Out

- Strong Brand Equity

LG’s consistent focus on innovation and product quality has positioned it as a premium brand globally. Investors often favor companies with durable brand value, as it translates to pricing power and market resilience. - Diversified Revenue Streams

From consumer electronics to EV batteries, LG operates across sectors that are shaping the future economy. This diversification reduces risk and offers exposure to multiple high-growth industries through a single investment. - Global Expansion Strategy

With rising demand for smart technology and green energy solutions, LG is expanding aggressively in emerging markets, including India and Southeast Asia. - Technological Innovation

LG’s R&D investments in AI, IoT, and renewable technology continue to strengthen its competitive edge, aligning with global sustainability goals.

Financial Overview and IPO Expectations

While the exact valuation and size of the LG IPO are yet to be finalized, early reports suggest a multi-billion-dollar offering. Market analysts believe that proceeds from the IPO may be used to:

- Expand battery and semiconductor capacity

- Strengthen R&D in AI and green technologies

- Pay down existing debt and improve liquidity

LG’s listed subsidiaries like LG Energy Solution have already demonstrated strong post-listing performance. If history repeats itself, this IPO could mirror similar success — offering long-term value creation.

However, investors should also note that global tech valuations have been volatile due to fluctuating interest rates and supply chain concerns. This makes it crucial to evaluate LG’s pricing carefully before subscribing.

Impact on Indian Investors and Markets

Although LG is a South Korean entity, its strong business presence in India means the IPO could indirectly benefit Indian investors and suppliers connected to its value chain — especially in electronics manufacturing, semiconductors, and renewable energy sectors.

For Indian retail investors exploring international opportunities, this IPO represents a way to diversify globally and gain exposure to the booming EV and tech ecosystem through international investment platforms.

Regulatory frameworks by SEBI and RBI’s Liberalized Remittance Scheme (LRS) allow Indian residents to invest in overseas IPOs via registered brokers — making global participation seamless.

Investor Perspective: Should You Consider the LG IPO?

The LG IPO could be a game-changer for investors seeking exposure to a strong, innovation-led multinational. However, investors should weigh the following before investing:

- Valuation Check: Ensure the issue price aligns with sector peers like Samsung, Sony, and Panasonic.

- Long-Term Outlook: The company’s focus on green energy and smart technologies bodes well for sustained growth.

- Risk Factors: Currency fluctuations, global economic conditions, and tech competition could impact returns.

In summary, the IPO may offer substantial long-term potential but requires careful analysis and expert research support before subscribing.

Why Choose Swastika Investmart

For investors aiming to make informed decisions on upcoming IPOs — both domestic and international — Swastika Investmart stands out as a trusted partner.

- SEBI-Registered Research & Advisory

- Comprehensive Research Reports & Valuation Tools

- Tech-Enabled Trading Platform for IPO Applications

- Dedicated Investor Education Initiatives

- Prompt Customer Support & Transparent Advisory

With Swastika’s expert guidance, investors can evaluate IPO opportunities like LG with confidence and clarity.

👉 Open your Swastika Investmart account today

Frequently Asked Questions

1. What is the LG IPO about?

The LG IPO refers to the public listing of one of LG Group’s key subsidiaries, likely to raise funds for expansion, R&D, and debt repayment.

2. Can Indian investors apply for the LG IPO?

Yes, through international investment platforms and SEBI-registered brokers under RBI’s LRS framework.

3. Is LG IPO a good investment?

Given LG’s global brand, diversified business, and tech focus, it holds strong long-term potential — though investors should evaluate valuation and market conditions.

4. How does LG’s IPO compare to Indian tech listings?

While Indian tech IPOs like MapmyIndia or Tata Technologies cater to domestic growth, LG offers global exposure and scale advantage.

5. Where can I get research-backed IPO insights?

Swastika Investmart provides expert analysis, IPO valuation insights, and investment guidance tailored for all investor segments.

Conclusion

The LG IPO could emerge as one of the most exciting listings in the global tech space, reflecting the company’s innovation-driven legacy and growth potential. For investors looking to participate in a globally recognized brand with strong fundamentals, this IPO offers a promising avenue.

However, like all investments, research and timing are key. With Swastika Investmart’s SEBI-registered advisory and robust research tools, investors can confidently analyze, subscribe, and track IPOs that align with their goals.

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App