TCS Share Price And Sector Outlook: Motilal Oswal Q1FY27 Earnings Preview

Key Takeaways

- Nifty earnings are forecast to grow 10% YoY in Q1FY27, the strongest pace in four quarters.

- Financials remain the biggest earnings contributor, with NBFCs, private banks, and metals leading growth; telecom shows strong uplift.

- Oil & gas profits are set to decline sharply; OMCs face losses, while building materials and EMS show robust momentum.

- Retail investors should align sector bets with earnings trends and use Swastika's Sarthi AI stock assistant for stock-by-stock insights.

As Q1FY27 earnings season kicks off, the TCS share price reaction is a sharp signal of the market's appetite for domestic demand and earnings momentum. Motilal Oswal's view shows Nifty earnings growing 10% YoY in Q1FY27, the strongest pace in four quarters, with broad-based improvements across sectors. The full coverage universe is expected to report a 3% YoY decline in earnings, the weakest since September 2020; while the small-cap universe is forecast to post a robust 20% YoY growth. Revenue growth is projected at 17% for large-caps, 15% for mid-caps, and 16% for small-caps.

Motilal Oswal's baseline is that Nifty earnings will grow 10% YoY in Q1FY27, the strongest pace in four quarters, arising from broad-based growth across sectors. They foresee PAT for its large-cap and mid-cap coverage universe to decline 2% and 14% YoY, respectively, in Q1FY27, while the small-cap universe is expected to deliver about 20% YoY PAT growth. Revenue growth is forecast at 17% for large-cap, 15% for mid-cap, and 16% for small-cap. EBITDA margins, excluding financials, are seen contracting: large-caps by 2%, mid-caps by 7%, and small-caps rising about 12% YoY.

Excluding financials, EBITDA margin for its coverage universe is expected to contract by 330 basis points to 14.2%, the lowest in 15 quarters. For the Nifty-50, the EBITDA margin excluding financials is projected to decline by 90 basis points to 20.5% during the quarter. Motilal Oswal also marginally lowered its FY27 and FY28 Nifty EPS estimates by 0.8% each, with Nifty EPS seen at Rs 1,225 in FY27 and Rs 1,422 in FY28.

On sectoral bets, financials remain the biggest contributor; NBFC-lending 27% YoY profit growth; private banks 10%; PSU banks 9%; Metals 31%; Tech 14%; Capital Goods 10%; Retail 27%; Consumer Durables 27%; Consumer sector 6%; Telecom profits are projected to surge about 3.3x YoY, driven by bharti airtel stock price and narrowing losses at Vodafone Idea. Oil and gas sector profits are expected to fall about 94% YoY, with Oil Marketing Companies (OMCs) posting a combined loss of Rs 36,400 crore. Automobiles and Healthcare are each expected to report about a 3% decline, and Cement profits are likely to fall 13% YoY. Building materials show momentum with 36% YoY profit growth, while EMS rises 29% YoY.

Margin dynamics remain a focus. Excluding financials, the coverage universe is expected to contract by 330 basis points to 14.2%, while the Nifty-50 ex-fin margin is seen easing to 20.5% in the quarter. The earnings path for FY27 and FY28 hints at slower momentum than some earlier hopes: Nifty EPS is forecast to grow 15% YoY to Rs 1,225 in FY27 and 16% to Rs 1,422 in FY28, with a minor 0.8% downward revision for both years.

Sector by sector, the mix matters. NBFC-lenders lead with 27% YoY profit growth; private banks 10%; PSU banks 9%; Metals 31%; Tech 14%; Capital goods 10%; Retail 27%; Consumer Durables 27%; Consumer sector 6%; Telecom profits travel higher by about 3.3x; the laggards include oil & gas. In the same frame, the building materials and EMS segments show very strong momentum, with 36% and 29% YoY profit growth, respectively.

Motilal Oswal's top picks include the following names in the Nifty universe: bharti airtel stock price, sbi stock price, icici bank stock, stock price of titan, Eternal, Shriram Finance, stock price of interglobe aviation, stock price of m&m finance, HDFC AMC and BSE. For non-Nifty ideas, consider TVS Motor, Radico Khaitan, Indian Hotels, RBL Bank, Dixon Technologies, Coforge, Kirloskar Oil Engines (KOEL), Arvind and Delhivery.

In a market that has seen volatility in recent years due to policy shifts, energy price shocks, and supply disruptions, this earnings view suggests a path where financials anchor profits while other sectors contribute in pockets. Investors should monitor the earnings trajectory across market caps and be prepared for margin pressure in non-financials. For deeper stock-by-stock insights across sectors, consider Swastika's Sarthi AI stock assistant.

TCS Share Price Implications For Q1FY27 And Beyond

This section discusses how the tcs share price reacts to the earnings backdrop and what it may signal for the rest of the quarter. The tcs share price is influenced by large-caps' earnings momentum and guidance for FY27. If the broad earnings trajectory remains intact, the tcs share price could reflect a continuation of gains into the next quarter, with a bias toward sector leadership from financials and technology names.

Nifty Earnings Growth And Sector Mix: A 10% YoY Kickoff

The base case remains that Nifty earnings will grow 10% YoY in Q1FY27–the strongest pace in four quarters. The growth will be broad-based but led by financials and commodity sectors, while oil & gas faces headwinds. The large-cap, mid-cap, and small-cap revenue growth is expected to be 17%, 15%, and 16% YoY, respectively. EBITDA margins ex-fin for the universe are projected to contract, with large-caps at -2%, mid-caps at -7%, and small-caps showing a +12% YoY variant, driven by cost management and price realisations in select industries.

Excluding financials, the EBITDA margin for the coverage universe is expected to contract by 330 bps to 14.2%, the lowest in 15 quarters, and for the Nifty-50 ex-fin, margins are expected to slip 90 bps to 20.5% in the quarter. FY27 and FY28 EPS estimates were trimmed by 0.8% each; Nifty EPS is now seen at Rs 1,225 in FY27 and Rs 1,422 in FY28, implying continued earnings momentum but with some sector-specific downgrades baked in.

Sector By Sector Growth And The Drivers Of Profit

Financials remain the backbone of profitability: NBFC-lending companies exhibit about 27% YoY profit growth, private banks 10%, and PSU banks 9%. Metals deliver 31% YoY profit growth, technology 14%, capital goods 10%, retail 27%, and consumer durables 27%. The consumer sector grows 6%, and telecom profits are projected to surge roughly 3.3x YoY, driven by bharti airtel stock price. Oil & gas lag, with profits shrinking about 94% YoY; OMCs are expected to post a combined loss of Rs 36,400 crore. Automobiles and Healthcare are forecast to decline about 3% YoY, while cement profits may drop 13% YoY. Building materials lead with 36% YoY profit growth, EMS up 29% YoY.

Top Stock Picks And What They Signal For Retail Investors

Motilal Oswal's top picks include the following names in the Nifty universe: bharti airtel stock price, sbi stock price, icici bank stock, stock price of titan, Eternal, Shriram Finance, stock price of interglobe aviation, stock price of m&m finance, HDFC AMC and BSE. Non-Nifty ideas include TVS Motor, Radico Khaitan, Indian Hotels, RBL Bank, Dixon Technologies, Coforge, Kirloskar Oil Engines (KOEL), Arvind and Delhivery.

Valuation And Risk: What Could Change The Trajectory?

Investors should stay mindful of the macro and policy environment, as any external shock can tilt earnings and valuations. The 94% YoY decline in oil & gas profits and the Rs 36,400 crore loss for OMCs highlight how energy prices and supply dynamics can weigh on profitability. Margin pressure outside financials calls for careful stock selection and risk management. The earnings map remains constructive if policy supports sustained growth and sector leadership continues to deliver.

Frequently Asked Questions

What is Motilal Oswal's forecast for Nifty earnings growth in Q1FY27?

Nifty earnings are expected to grow 10% YoY in Q1FY27, the strongest pace in four quarters.

Which sectors are expected to contribute most to earnings growth in Q1FY27?

Financials remain the biggest contributor, with NBFC-lenders growing about 27% YoY, private banks 10%, PSU banks 9%; Metals 31%, Tech 14%, Capital Goods 10%, Retail 27%, and Consumer Durables 27%. Telecom profits are projected to surge 3.3x YoY.

What are Motilal Oswal's EPS forecasts for Nifty in FY27 and FY28?

Nifty EPS is seen at Rs 1,225 in FY27 and Rs 1,422 in FY28, representing 15% and 16% YoY growth respectively, with a 0.8% downward revision for both years.

Who are Motilal Oswal's top picks and non-Nifty ideas?

Top picks include bharti airtel stock price, sbi stock price, icici bank stock, stock price of titan, Eternal, Shriram Finance, stock price of interglobe aviation, stock price of m&m finance, HDFC AMC and BSE. Non-Nifty ideas include TVS Motor, Radico Khaitan, Indian Hotels, RBL Bank, Dixon Technologies, Coforge, Kirloskar Oil Engines (KOEL), Arvind and Delhivery.

What are the key risk factors highlighted in Motilal Oswal's view?

Oil & Gas profits are expected to fall about 94% YoY; OMCs may post a combined loss of Rs 36,400 crore; Automobiles and Healthcare are each expected to decline about 3%; Cement profits may fall 13% YoY; margin pressures persist outside financials.

Conclusion

For the retail investor, the Q1FY27 earnings snapshot signals a more inclusive earnings recovery where financials keep the engine running while non-financials contribute in pockets. The practical takeaway is to tilt allocations toward the leaders in the earnings upgrade cycle, use disciplined risk controls, and stay nimble as sector dynamics evolve. To enhance decision-making with stock-level insights, consider Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

In practical terms, a retail investor can pair a core allocation to financials with selective exposure to high-growth tech, consumer, and select infra plays, while keeping a watchful eye on margin trends and energy sector risk. The next step is to monitor the earnings trajectory in Q1FY27 and test assumptions against real-time stock price movements. The market's next move will likely be driven by how well the top picks deliver on earnings upgrades and how risk factors evolve in the coming quarters.

Latest Articles

Understanding In-The-Money (ITM) Options

In a call option, you have the right, but not the obligation, to buy a stock for a set price (strike price) by a certain date (expiry date). There are different types of call options, and today we'll focus on In-the-Money (ITM) call options. Let's break it down:

- Call Option: You're basically hoping the stock price will go up so you can buy it cheap and then sell it for a profit.

- In-the-Money (ITM): This means the stock's current price is higher than the strike price of your call option.

Example:

Let's say the current price (spot price) of a stock is ₹8,300

- You buy a call option with a strike price of ₹8,200 (your agreed upon this purchase price)

- Since the stock price (₹8,300) is higher than your strike price (₹8,200), your call option is In-the-Money (ITM).

Options can be categorized as:

- In-The-Money (ITM)

- At-The-Money (ATM)

- Out-Of-The-Money (OTM)

These terms help investors decide which options to buy or sell.

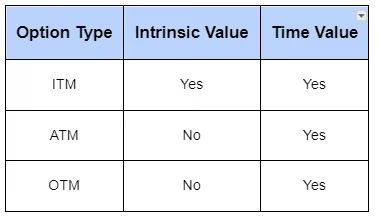

- Intrinsic Value: This is the actual value of an option if you used it today. It’s the difference between the current stock price and the strike price.

ITM Options

- Call Option: ITM if the strike price is lower than the current stock price.

Example: Current stock price is ₹1000, and the call option strike price is ₹900. This option is ITM because ₹1000 (current price) - ₹900 (strike price) = ₹100.

- Put Option: ITM if the strike price is higher than the current stock price.

Example: Current stock price is ₹1000, and the put option strike price is ₹1100. This option is ITM because ₹1100 (strike price) - ₹1000 (current price) = ₹100.

Option Premium Components

The price you pay for an option (option premium) has two parts:

- Intrinsic Value

- Time Value

Formula: Option Premium=Intrinsic Value+Time ValueOption Premium=Intrinsic Value+Time Value

Characteristics of ITM, ATM, and OTM Options

- Intrinsic Value: The real value of an ITM option. It’s the difference between the stock price and the strike price.

- Time Value: The extra amount you pay because the option might become more valuable before it expires. This value decreases as the expiration date gets closer.

Let’s take another example to understand an ITM Call Option:

An ITM call option has a strike price lower than the current stock price.

Example:

- Current Price: ₹8300

- ITM Call Option: Any strike price below ₹8300

- Example Option: NIFTY FEB 8200 CALL (Strike Price = ₹8200, Current Price = ₹8300)

Benefits of ITM Call Options

- Lower Risk: ITM options are less likely to expire worthless because the stock price is already in your favor.

- Good Balance of Leverage and Risk: You can get good returns with a smaller investment compared to buying the stock itself.

- Less Volatile: ITM options are less affected by sudden market changes compared to other options.

Things to Consider with ITM Call Options

- Higher Cost: ITM options cost more because they already have some built-in profit potential.

- Lower Leverage: Higher cost means you have less money left for other investments.

- Time Decay: As the option gets closer to its expiration date, its value decreases faster.

- Limited Profit: Your profit is capped at the strike price plus the premium you paid.

Who Should Use ITM Call Options?

- Investors who are bullish (optimistic) on a stock's price and want to profit from an increase.

- Investors seeking to hedge (protect) their existing stock holdings.

- Investors looking for a balanced approach with some level of built-in profit potential and lower risk.

Conclusion

ITM call options can be a powerful tool, but it's important to understand the costs, risks, and limitations before using them. Carefully consider your investment goals and risk tolerance before diving in.

What is a Circuit Breaker?

A circuit breaker in the stock market is a mechanism that sets a price band within which a stock can be traded on a given day. Circuit breakers operate automatically by halting trading when global exchange values reach predetermined levels. This band includes a lower limit (lower circuit) and an upper limit (upper circuit).

Why is a Circuit Breaker Needed?

Stock prices often fluctuate due to market sentiments, influenced by positive or negative news. Circuit breakers are set up to prevent extreme price movements, protecting investors from sudden, unexpected changes. They also help reduce price manipulation to some extent.

The Securities and Exchange Board of India (SEBI) has defined various circuit levels: 2%, 5%, 10%, and 20%. These levels are based on the stock's closing price from the previous day.

Example:

If XYZ stock closed at ₹100 yesterday and has a 10% circuit limit, today it can only be traded between ₹90 (lower limit) and ₹110 (upper limit). If the stock reaches either limit, trading is halted.

How Circuit Breakers Work

In the trade world, a circuit breaker serves the same purpose as it does in residential electrical circuits. It engages and cuts the circuit when it senses an overload. Circuit breakers are emergency safeguards in the trading industry put in place by stock markets to temporarily or permanently halt trading activity when market prices decline drastically.

Individual Stocks:

If the price hits the upper or lower limit, trading in that particular stock is halted.

Market Indices:

A 10%, 15%, or 20% change triggers a market-wide halt.

Upper and Lower Circuit Limits

The limits prevent excessive speculation and volatility. Depending on the stock category, a stock can shift by 5%, 10%, or a maximum of 20% during a trading day.

Example of Upper Circuit and Lower Circuit

Let's say XYZ stock closed at ₹100 yesterday. If it has a 10% circuit limit:

- Upper Circuit: The upper limit would be ₹110 (10% above ₹100). If the stock price reaches ₹110, trading is halted because it has hit the upper circuit. This indicates strong buying interest, and the price can't go higher for the rest of the day.

- Lower Circuit: The lower limit would be ₹90 (10% below ₹100). If the stock price drops to ₹90, trading is halted because it has hit the lower circuit. This indicates strong selling pressure, and the price can't go lower for the rest of the day.

Market-Wide Circuit Breakers

Time-Based Rules:

- Before 1 PM: A 15% movement halts the market for 1 hour and 45 minutes, followed by a 15-minute pre-opening session.

- Between 1 PM and 2 PM: A 15% movement halts the market for 45 minutes, followed by a 15-minute pre-opening session.

- After 2 PM: A 15% movement halts the market for the rest of the day.

- At Any Time: A 20% movement halts the market for the entire day.

Summary Table of Circuit Breaker Durations

Conclusion

Circuit breakers play a important role in stabilizing the stock market by preventing excessive volatility and protecting investors from sudden, significant price changes.

Understanding Market Capitalization: Meaning, Importance

Ever wondered how much a company is "worth"? The answer lies in a key metric: Market Capitalization. In the stock market, it shows a company's total value based on its current share price and the number of shares available for trading. Instead of looking at revenue or total asset worth, investors use this number to assess a company's size. The market capitalization of a takeover candidate aids in evaluating whether the acquirer will receive a decent deal from the deal.

Formula:

Market Cap = Current Share Price * Total Outstanding Shares

So, if Company W share price is Rs. 200 and there are 5 crore outstanding shares, its Market Cap would be Rs. 1,000 crore (200 * 5 crore).

Why does it matters?

It gives you a snapshot of where a company stands:

- Growth Potential: A smaller company might be newer and have more room to grow, making it an attractive option for growth investors.

- Stability: Larger companies are more stable and less affected by market fluctuations. They often have more financial reserves to cover losses and recover from downturns.

- Risk and Volatility: Small-cap companies can offer high growth potential but come with higher risk and volatility. Large-cap companies are generally more stable but may grow more slowly.

Using Market Capitalization to Diversify Your Portfolio

Diversification is about spreading your investments to manage risk:

- Across Asset Classes: For example, investing in both stocks and bonds.

- Within Asset Classes: Investing in a mix of small-cap, mid-cap, and large-cap stocks to balance potential risks and returns.

Types of Companies

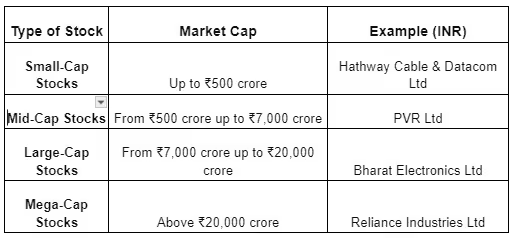

Companies are categorized into different types based on their market capitalization. This helps investors balance their portfolios to minimize risk.

Categories

Small-Cap Stocks

- Market Cap: Up to ₹500 crore.

- Growth Potential: Small-cap companies are often in their early stages and have growth potential. However, they are also more risky.

- High Risk, High Reward: These companies can offer high returns during favorable economic conditions but are more affected by market fluctuations and economic downturns.

- Examples: Hathway Cable & Datacom Ltd.

Mid-Cap Stocks

- Market Cap: From ₹500 crore up to ₹7,000 crore.

- Balanced Growth: Mid-cap companies have a balance between growth potential and stability. They are more established than small-cap companies but still have space for growth.

- Moderate Risk: These companies are less risky than small-caps but more volatile than large-caps. They can provide returns with moderate risk.

- Examples: PVR Ltd.

Large-Cap Stocks

- Market Cap: From ₹7,000 crore up to ₹20,000 crore.

- Stability: Large-cap companies are well-established and financially sound. They are market leaders with a proven track record.

- Lower Risk, Steady Returns: These companies offer more stability and are less likely to experience volatility. They are suitable for conservative investors seeking steady returns.

- Examples: Bharat Electronics Ltd.

Mega-Cap Stocks

- Market Cap: Above ₹20,000 crore.

- Market Dominance: Mega-cap companies are the largest and dominant in their industries. They are often multinational corporations with influence on the market.

- Very Low Risk: These companies provide the highest level of stability and are considered safe investments. While the growth potential might be lower, they offer reliable returns and are ideal for risk-avoid investors.

- Examples: Reliance Industries Ltd.

Conclusion

Market capitalization is an important factor in evaluating stocks and mutual funds. It helps investors take decisions based on their risk tolerance and return expectations. However, while it is a valuable indicator of a company’s financial health, investors should not rely solely on it. A thorough analysis of the company’s overall performance and market conditions is essential before making investment decisions.

How Do Election Results Impact the Indian Stock Market?

Elections are crucial events in any democracy, and India is no exception. The outcomes of elections can have significant impacts on the stock market. This blog explores how election results influence the Indian stock market and what the potential impacts of Prime Minister Narendra Modi’s third term could be.

Political Factors Affecting the Stock Market

Market Sentiment and Stability:

- Market Sentiment: Elections often bring a sense of uncertainty. Investors generally prefer stability, and election outcomes can either boost or reduce their confidence. If the results are in favor of a party or leader perceived to be business-friendly and stable, the market reacts positively.

- Policy Predictability: Stable governments are often able to implement policies more predictably. Investors like predictability as it reduces the risks associated with sudden policy changes.

Economic Policies:

- Pro-Growth Policies: If the elected government has a track record or a plan focusing on economic growth, infrastructure development, and business-friendly regulations, the stock market usually reacts positively.

- Reform Initiatives: Governments promising and delivering structural reforms (like tax reforms, deregulation, and infrastructure spending) can boost investor confidence and drive market rallies.

Fiscal Management:

- Budget and Spending: Election outcomes can impact fiscal policies. Governments that promise sensible fiscal management and reduced deficits tend to be favored by the markets.

- Spending Programs: Conversely, if a new government is expected to increase public spending significantly without a clear plan for managing the budget, it may cause concern among investors about inflation and fiscal health, potentially leading to market volatility.

Global Perception:

- Foreign Investments: Global investors closely watch Indian elections. A government perceived as stable and reform-oriented can attract more Foreign Direct Investment (FDI) and Foreign Institutional Investment (FII), positively influencing the stock market.

- Geopolitical Stability: Election results that contribute to regional stability or enhance diplomatic relations can positively impact the stock market.

Narendra Modi’s Potential Third Term and Its Impact

Prime Minister Narendra Modi, known for his strong leadership and decisive economic policies, could significantly impact the stock market if he secures a third term. Here’s how:

Continuation of Economic Reforms:

Modi’s government has been known for several landmark economic reforms such as the Goods and Services Tax (GST), Insolvency and Bankruptcy Code (IBC), and digitalization initiatives. A third term could mean the continuation and deepening of these reforms, providing a stable and predictable policy environment that is likely to be welcomed by investors.

Infrastructure and Development Projects:

Modi’s focus on infrastructure development, including projects like smart cities, improved transportation networks, and digital infrastructure, could continue. These initiatives can stimulate economic growth, create jobs, and increase demand in various sectors, positively influencing the stock market.

Foreign Investment and Economic Relations:

Under Modi’s leadership, India has improved its ease of doing business rankings and attracted significant foreign investments. A third term could further strengthen India’s global economic relations, encouraging more foreign investments and boosting market confidence.

Political Stability:

A third term for Modi could imply political stability, which is generally favorable for the stock market. Stability reduces uncertainty and helps in long-term planning for both domestic and foreign investors.

Focus on Technology and Innovation:

Modi’s government has also emphasized technology and innovation through initiatives like Digital India and Make in India. Continued focus in these areas could foster a more robust tech ecosystem, providing growth opportunities for tech stocks and start-ups.

Potential Risks:

Implementation Risks: While Modi’s policies are generally market-friendly, the actual implementation of large-scale reforms can sometimes face hurdles, leading to temporary market fluctuations.

Global Economic Conditions: The global economic environment can also impact the effectiveness of Modi’s policies. Trade wars, global slowdowns, or geopolitical tensions can affect market performance regardless of domestic policies.

Conclusion

Election results have a deep impact on the Indian stock market, primarily due to changes in market sentiment, policy direction, and fiscal management. A potential third term for Prime Minister Narendra Modi is expected to bring continued economic reforms, infrastructure development, and political stability, all of which are likely to positively influence the stock market. However, investors should remain mindful of implementation challenges and global economic conditions that can also affect market dynamics. As always, a balanced and insightful approach to investing is crucial in navigating the impacts of election results on the stock market.

Learn more about stock market with Swastika!

What is Prospectus?

A prospectus is a formal document that gives information about an investment offering to the public and is required by the Securities and Exchange Commission (SEC) to be filed. Bonds, mutual funds, and stock offers need the filing of a prospectus. Because it includes a wealth of pertinent information about the investment or security, the prospectus can assist investors in making better-informed investing decisions.

- Preliminary Prospectus

This is the initial offering document provided by the company. It contains most details about the business and the transaction. However, it doesn't include the number of shares or the price.

- Final Prospectus

This document provides all the details of the investment offering to the public. It includes background information, the number of shares or certificates to be issued, and the offering price.

Prospectus Example

In mutual funds, the prospectus covers objectives, investment strategies, risks, and performance, fees, and fund management details.

Requirements for Issuing a Prospectus

To issue a prospectus, a company must:

- File it with local regulatory bodies like SEBI and stock exchanges.

- It must be dated and signed.

- Include all necessary information outlined in the Companies Act 2013.

- Avoid providing misleading information.

Why Read a Prospectus? Here's Why It Matters:

An SEC-mandated prospectus gives investors crucial information regarding an offering of securities.

It disseminates risk information to the public and compiles important details about the investment and the business being invested in.

Investors should take into account the type and degree of risk involved, which is why those facts are usually included early in the prospectus and in more depth later on.

Investors want to know that the firm they are investing in is financially stable enough to fulfill its obligations, therefore the financial standing of the business is also crucial.

Types of Prospectuses

- Red Herring Prospectus: Filed with the registrar before offering shares. Usually lacks details like quantity or price.

- Abridged Prospectus: A brief summary with essential offer details. Must include all documents needed for purchasing the security.

- Deemed Prospectus: Considered deemed if it details the company’s investment offer to the public.

- Shelf Prospectus: Distributed by banks or financial institutions, containing details of multiple investment types.

Details Included in a Prospectus

A prospectus contains the following details:

- Company Information: Name, registered office address, objectives, and background.

- Offer Details: Number of shares or certificates to be issued, offering price, and any minimum subscription amount.

- Financial Information: Audited financial reports, including profit and loss statements, balance sheets, and cash flow statements.

- Management Details: Information about the company's directors, management team, and key personnel.

- Risk Factors: An overview of the risks associated with the investment, including market risks, regulatory risks, and operational risks.

- Legal and Regulatory Information: Details of any legal proceedings, regulatory compliance, and agreements relevant to the offering.

- Use of Proceeds: How the funds raised from the offering will be used by the company.

- Fees and Expenses: Details of any fees, expenses, or charges associated with the investment, including management fees and transaction costs.

- Offering Structure: Any special terms or conditions of the offering, such as underwriting arrangements or distribution channels.

- Other Relevant Information: Any additional information deemed relevant to investors, such as industry trends, competitive landscape, and future growth prospects.

Conclusion

By reading the prospectus carefully, you can:

- Compare different investment options.

- Spot any potential risks.

- See if the investment aligns with your goals and risk tolerance

What is a Covered Call? Overview of a Covered Call Strategy

As an investor, navigating the stock market can often involve balancing potential profits with risks. One strategy that stands out for its is the Covered Call Strategy. This approach allows you to generate income from your stock holdings Let's dive into what a covered call is and how this strategy can benefit you as an investor.

Understanding a Covered Call Strategy

Imagine you own shares of a company. You believe the stock may rise in the long run but don't expect gains in the near term. However, you still want to earn some income from these shares in the meantime. This is where a covered call strategy comes in

In a covered call strategy, an investor sells a call option on a stock they already own. This nets them a premium from the sale of the option. the call option is sold as an Out of The Money (OTM) call, meaning the option's strike price is higher than the current stock price. The call option would not get exercised unless the stock price increases above the strike price. Until then, the investor retains the premium as income, making this strategy attractive for those who are neutral to moderately bullish about their stock.

How a Covered Call Strategy Works

To use a covered call option strategy, you must first own the stock of a company. Let's assume you already hold the stock, showing a bullish movement. Over time, you become unsure about the stock's short-term upside potential and don't expect a significant price increase. Here's what you can do:

- Sell a Call Option: You sell a call option contract at a strike price higher than your stock's purchase price. The buyer of the call option pays you a premium for this contract.

- Collect the Premium: Regardless of whether the option is exercised, you keep the premium. This becomes your immediate income from the stock.

- Outcome Scenarios: After executing a covered call strategy, one of three scenarios can occur:some text

- Stock Price Remains Stable or Falls: The call option expires worthless, and you keep both the premium and your shares.

- Stock Price Rises Slightly: The stock price increases but remains below the strike price. The call option still expires worthless, allowing you to keep the premium and benefit from the stock's appreciation.

- Stock Price Rises Significantly: The stock price rises above the strike price. The call option is exercised, and you must sell your shares at the strike price. You keep the premium and receive the strike price for your shares, potentially missing out on further gains beyond the strike price.

When to Use a Covered Call

The covered call strategy works particularly well in the following situations:

Generating Income

The primary use of the covered call strategy is to generate income. If you own assets like stocks or ETFs that you're willing to sell at a certain price, selling a covered call can help generate additional income.

Neutral or Slightly Bullish Market

The covered call strategy is effective in a neutral or slightly bullish market. If you expect the price of an asset to remain relatively stable or increase slightly, selling a covered call can allow you to generate income while still owning the asset and benefiting from modest price increases.

Reducing Risk/Hedging

By selling a call option, you can theoretically limit downside risk if the price of the underlying stock falls. If the stock price drops below the strike price of the call option, the option will expire worthless, and you'll still own the underlying stock, which you can sell or hold for potential future gains.

When to Avoid a Covered Call

A covered call should be avoided in the following situations:

Expecting a Stock Price Rise

If you expect the stock to rise significantly in the near future, selling a covered call may limit your potential upside. It's better to hold onto the stock and let it appreciate.

Facing Serious Downside

If the stock looks like it's going to drop significantly, using a covered call to get extra cash might not be wise. In such cases, it’s probably best to sell the stock or consider short selling to profit from its decline.

Advantages of a Covered Call Strategy

- Generates Income: Covered calls generate income from holdings that wouldn't otherwise provide a cash flow stream.

- Adds to Returns: Investors periodically sell covered call options to enhance a position's return.

- Acts as a Hedge: A covered call offers some protection by reducing the breakeven price due to the premium.

- Low-Risk Strategy: Selling covered calls is easy and low-risk because the stock position "covers" the short call.

Conclusion

In summary, covered calls can be a strategy for investors looking for risk management and income generation. By merging stock ownership with the sale of call options, investors can increase their potential returns in a moderate appreciation of stock price. This strategy provides a balance between earning additional income and managing risks, making it a valuable tool for an investor.

Learn more about financial terminologies with Swastika!

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App