Reliance Industries Share Price In Market Selloff: A Retail Investor Guide

Key Takeaways

- NSE Nifty 50 traded 1.3% lower at 24,088.60; Sensex declined 998 points to 77,183, signaling a broad market pullback.

- Investors lost over Rs 4.07 lakh crore in wealth as geopolitical tensions weighed on sentiment.

- Reliance Industries share price led the declines alongside icici bank share price, bharti airtel stock price, hdfc bank stock price, and axis bank stock price.

- Sector moves showed Nifty Oil & Gas and Nifty FMCG among the biggest drags, while Nifty Realty bucked the trend with gains.

Investors woke up to a market-crushing reality on a day defined by renewed geopolitical tensions. The NSE Nifty 50 traded 1.3% lower at 24,088.60, while the Sensex slid 998 points to 77,183, painting a portrait of risk-off sentiment across Indian equities. In total, investors saw wealth shrink by over Rs 4.07 lakh crore as the selloff broadened and traders reassessed risk premia. Within this broad slide, the reliance industries share price and other heavyweight names acted as primary catalysts for the day’s weakness, underscoring how a handful of large constituents can drive index-level moves even when many mid- and small-cap names trade in a different mood.

Among the heaviest weights, Reliance Industries Ltd. stood out as a major drag, contributing to the Nifty’s decline alongside ICICI Bank, Bharti Airtel, HDFC Bank and Axis Bank. Specifically, Reliance Industries erased 30.68 points from the benchmark index, ICICI Bank shaved off 28.48 points, and Bharti Airtel trimmed 18.16 points. These numbers highlight how a handful of giants can swing index levels on news-driven days, even as other sectors attempt to cushion the overall picture.

From a sectoral lens, the day’s moves were telling. Nifty Oil & Gas fell 1.57%, Nifty FMCG slipped 1.33%, and Nifty Media dropped 1.29%. The broader financial complex also softened, with Nifty Financial Services down 0.92%; Nifty Rural down 0.88%; Nifty Bank down 0.78%; Nifty Consumption down 0.75%; Nifty PSU Bank down 0.74%; and Nifty Auto down 0.58%. On the other hand, pockets of resilience appeared in parts of the market: Nifty Metal rose 0.03%, Nifty Pharma gained 0.07%, and Nifty Realty stood out with a 0.59% gain, bucking the broader trend.

In parallel, global headlines added fresh fuel to risk-off trades. The day’s focus centered on geopolitical tensions around Iran, including remarks suggesting a potential end to ceasefire efforts, and reports of U.S. strikes in response to attacks on civilian shipping in the Strait of Hormuz. The U.S. Treasury also revoked a license that had permitted certain transactions involving Iranian crude oil, with the revised license taking effect on July 7. Tehran vowed to safeguard its interests in response to these measures, while tensions remained high as markets weighed the implications for global supply chains and energy prices.

For a real-time, data-driven approach to stock-specific research, traders can leverage Swastika's Sarthi AI stock assistant to gain institutional-level insights on any stock or index. Swastika's Sarthi AI stock assistant offers a structured way to assess risk, valuation, and catalysts beyond headline news.

Reliance Industries Share Price In Market Selloff: What Drove The Downtick

The day’s trajectory was heavily influenced by the fundamental sensitivity of the market to heavyweight components. The reliance industries share price, together with other top-contributing stocks, manifested a clear drag on the Nifty. The broader move reflects a combination of sector rotation and risk-off sentiment, with investors weighing macro signals alongside geopolitical developments. For retail investors, this underscores the risk of concentrated exposure to a handful of large-cap names during volatile sessions and highlights the importance of diversification and disciplined position sizing.

Even as Reliance Industries Limited moved, the rest of the market displayed mixed behavior across sectors. The drop in Nifty Oil & Gas and Nifty FMCG indicates that defensive and energy-linked exposures were not immune to selling pressure, while the positive turn in Nifty Realty showed that real estate-linked exposure could offer pockets of relative strength in an otherwise risk-off environment. The day’s numbers suggest a cautious stance for near-term momentum traders and underscore the need to validate price levels with robust risk controls.

Infosys Stock Price Movements And Sectoral Impact In The Selloff

Tech-oriented equities were not immune to the broad retreat. In the context of the day’s slide, infosys stock price moves contributed to the softened mood around the IT sector, as the Nifty IT index declined by about 0.52%. While global technology cycles remain important, the day’s action reminded investors that even defensive tech names aren’t guaranteed safe harbors in times of macro-driven risk, especially when overall liquidity is constrained by risk-off flows.

For retail traders, it is essential to monitor stock-specific catalysts–earnings, guidance, or management commentary–that can either cushion or amplify sectoral moves. A structured process that combines price-action analysis with fundamentals can help in spotting mean-reversion opportunities or identifying stocks with resilient downside risk profiles.

Hdfc Bank Stock Price And Nifty Banking Drag

The banking complex was a major drag, with hdfc bank stock price playing a notable but not uniformly quantified role in the day’s decline. The bank index underperformed as investors priced in cautious macro cues and the ongoing cycle of policy and macro uncertainty. Axis Bank stock price similarly contributed to the broader weakness in the financials space, reinforcing a mood of risk aversion among sector-focused investors.

For risk-conscious investors, such days highlight the importance of evaluating loan books, asset quality signals, and the impact of macro-level policy changes on bank margins. While banks often lead declines in risk-off sessions, disciplined diversification and clear stop-loss discipline can prevent single-stock moves from driving outsized losses.

Icici Bank Share Price And Its Contribution To The Nifty Drop

ICICI Bank share price was among the top contributors to the Nifty’s downside, underscoring the weight of private sector lenders in the index. When a single stock has a meaningful impact on index performance, it amplifies the effect of sectoral reallocations and can help identify where risk concentrations lie within a portfolio. For investors tracking icici bank share price movements, the emphasis should be on price structure, support zones, and any catalysts that could alter the trend in the near term.

As part of a broader strategy, investors could consider balancing exposures by evaluating non-banking financials, infrastructure plays, or defensive sectors that historically demonstrate resilience in volatility. A measured approach to stock selection–grounded in price action and risk controls–can help navigate similar days in the future.

Axis Bank Stock Price And The Banking Sector Drag

Axis Bank stock price, a key member of the private banking cohort, contributed to the breadth of the banking sector’s pullback. The day’s environment favored risk-off behavior that weighed on financials, with the Axis Bank touchpoint reflecting broader concerns about macro stability and potential credit-cycle implications. Traders should watch Axis Bank’s price action around key moving averages and any directional cues from earnings or sector commentary to gauge whether this drag persists or recedes in subsequent sessions.

Bharti Airtel Stock Price And The Communication Sector's Role

Bharti Airtel stock price was among the names that contributed to the index’s weakness, illustrating how even high-visibility telecom players can be pulled down in a risk-off day. The communication sector’s contribution to the day’s declines underscores the interconnected nature of equities where macro sentiment can overshadow sector-specific narratives. For investors with exposure to telecom, reviewing tariff cycles, capex plans, and ARPU trends can help in making more informed mid- to long-term decisions.

Sectoral Roundup: Oil &Amp Gas, FMCG And Media On The Decline; Realty's Gains

On balance, the sectoral moves painted a mixed picture. Nifty Oil & Gas declined 1.57%, Nifty FMCG shed 1.33%, and Nifty Media fell 1.29%, reflecting the broad risk-off environment. In contrast, Nifty Realty bucked the trend, gaining 0.59%, suggesting selective strength in that segment perhaps linked to risk dispersion or stock-specific catalysts. The resilience in Realty highlights that even in a risk-off phase, some subsectors can exhibit relative strength driven by domestic demand drivers, urbanization trends, or policy tailwinds.

For a practical view, consider mapping sector exposure against your risk tolerance. A diversified blend that avoids overweight bets on single blocks of the market can help maintain resilience through choppier sessions.

Global Tensions And The Price Action: The Iran-Related Market Dynamics

The day’s price action did not occur in isolation. Renewed geopolitical tensions and comments from international leadership influenced global risk appetite. Separately, the U.S. Central Command reported strikes against Iran in response to attacks on civilian shipping in the Strait of Hormuz, a move that can alter energy prices and global risk sentiment. The U.S. Treasury’s revocation of a particular oil-related license added to the complexity of energy markets and cross-border trade considerations, with the revised license taking effect on July 7. Iran criticized these actions as violations of international norms, and Tehran signaled it would safeguard its national interests and security. Investors should be mindful of how such geopolitical developments feed into risk premia, currency moves, and commodity price trajectories, all of which can ripple through equity markets.

What Retail Investors Should Do Next: A Practical Playbook

Today’s session reinforces several timeless tenets for individual investors: don’t chase headlines, align trades with a well-defined risk framework, and rebalance to maintain a risk profile that suits your time horizon. In volatile markets, price action often tests the resolve of one’s investment plan. Consider revisiting your asset mix to ensure you are not overly exposed to any single stock or sector, implementing protective stops where appropriate, and maintaining sufficient liquidity to avoid forced trades during sharp moves. For those seeking deeper, stock-specific analysis, the Sarthi AI stock assistant can help tailor research to your holdings and watchlists, offering institutional-grade insights in a retail-friendly format.

In a market where the reliance industries share price and other heavyweight weights can sway daily outcomes, a disciplined approach to risk and a clear plan for capital deployment become more valuable than ever. The goal is not to predict every tick, but to position with a margin of safety and a process you trust. That’s the essence of building long-term resilience in portfolios during episodes of volatility.

Related Reads

- Reliance Industries Share Price: Nifty 50 Five-Year Performance And What It Means For Retail Investors

- RIL BEL Lenskart Delhivery: Motilal Oswal's Top Monthly Stock Picks for Indian Retail Investors

Frequently Asked Questions

What caused the market to slump today?

Geopolitical tensions and fresh comments from international leaders, along with geopolitical risk and global risk-off sentiment, contributed to a broad market selloff, pulling major indices lower and erasing wealth as investors reassessed risk.

Which stocks contributed most to the Nifty’s decline?

The top contributors were Reliance Industries Ltd., ICICI Bank, Bharti Airtel, HDFC Bank and Axis Bank, with Reliance Industries erasing 30.68 index points, ICICI Bank 28.48 points, and Bharti Airtel 18.16 points from the Nifty. Other names weighed on the mood as well.

Which sectors dragged the most on the day?

Nifty Oil & Gas fell 1.57%, Nifty FMCG declined 1.33%, and Nifty Media dropped 1.29%. The broader financials complex softened, with Nifty Financial Services down 0.92% and Nifty Bank down 0.78%. Realty bucked the trend with gains of 0.59%.

What should a retail investor do next after such a session?

Focus on risk management, review asset allocation, and consider disciplined rebalancing. Avoid overexposure to single stocks like the heavyweights that drove today’s declines, and use structured research tools, such as Swastika's Sarthi AI stock assistant, to gain data-driven insights into individual stocks and indices.

Where can I find deeper stock research and insights?

For institutional-level research in a retail-friendly format, use Swastika's Sarthi AI stock assistant:Swastika's Sarthi AI stock assistant.

Conclusion

The retail investor’s takeaway is simple: volatility is the price of admission for an open, globally connected market. Use days like today to reassess risk, confirm your time horizon, and ensure your exposure aligns with your financial goals. As the market digests geopolitical headlines and policy signals, seek a balanced approach that blends cautious risk management with opportunistic stock selection grounded in discipline and credible research.

Table: Sectoral Moves On The Day

| Sector | Move |

|---|---|

| Nifty Oil & Gas | -1.57% |

| Nifty FMCG | -1.33% |

| Nifty Media | -1.29% |

| Nifty Financial Services | -0.92% |

| Nifty Rural | -0.88% |

| Nifty Bank | -0.78% |

| Nifty Consumption | -0.75% |

| Nifty PSU Bank | -0.74% |

| Nifty Auto | -0.58% |

| Nifty IT | -0.52% |

| Nifty Energy | -0.47% |

| Nifty India Defence | -0.07% |

| Nifty Metal | +0.03% |

| Nifty Pharma | +0.07% |

| Nifty Realty | +0.59% |

Note: All price data and index levels reflect real-time market facts as published in today’s session. Values are subject to change as markets oscillate and new information surfaces. Catch all the live updates on stock markets here.

Open your trading and demat account here

Reference :

1 : Ndtvprofit

Latest Articles

Why Rising Oil Prices and Inflation May Force RBI to Pause Rate Cuts

Key Takeaways

- Rising crude oil prices are pushing inflation risks higher

- Higher inflation limits the ability of RBI to cut interest rates

- Rate pause can impact equity markets and borrowing costs

- Oil-sensitive sectors may face pressure in the short term

- Investors should focus on diversification and quality stocks

Introduction

The global economic environment is once again turning uncertain, with crude oil prices inching higher and inflation concerns resurfacing. For India, this combination creates a challenging situation for policymakers, especially the Reserve Bank of India.

At a time when markets were expecting further rate cuts to support growth, rising inflationary pressures may force the central bank to take a pause. This shift has important implications for investors, borrowers, and the overall market direction.

The Link Between Oil Prices and Inflation

India is heavily dependent on crude oil imports, which makes it highly sensitive to global price movements.

How Rising Oil Prices Impact Inflation

- Higher fuel costs increase transportation expenses

- Logistics costs rise across industries

- Raw material prices move up

- End consumers face higher prices

👉 This leads to cost-push inflation, where rising input costs push overall prices higher

Real-World Context

Whenever crude oil prices spike globally, India often experiences a rise in retail fuel prices. This directly affects household budgets and reduces disposable income, slowing consumption demand.

Why RBI May Pause Rate Cuts

Central banks balance two key objectives:

- Supporting economic growth

- Controlling inflation

When inflation rises, controlling it becomes the priority.

The Policy Dilemma

- Rate cuts help boost growth by making loans cheaper

- But they can also increase inflation by boosting demand

👉 In a high inflation environment, cutting rates becomes risky

Current Scenario

- Rising oil prices are adding inflationary pressure

- Global uncertainties are increasing volatility

- Currency fluctuations can further amplify imported inflation

👉 This leaves the Reserve Bank of India with limited room to ease monetary policy

Impact on Indian Markets

A pause in rate cuts can influence multiple segments of the market.

📊 1. Equity Markets

- Rate-sensitive sectors may underperform

- Valuations may remain under pressure

- Market sentiment could turn cautious

🏦 2. Banking and NBFC Sector

- Loan growth may stabilize rather than accelerate

- Margins could remain steady but not expand significantly

🏠 3. Realty and Auto

- Higher borrowing costs may impact demand

- Consumer financing becomes less attractive

🛢️ 4. Energy Sector

- Upstream companies may benefit from higher oil prices

- Downstream companies may face margin pressure

Bond Market Perspective

Bond markets react quickly to inflation and interest rate expectations.

What Happens When Inflation Rises

- Bond yields tend to move higher

- Bond prices fall

- Long-duration bonds become less attractive

👉 Investors may prefer shorter-duration fixed income instruments during such phases

What Should Investors Do?

Market conditions like these require a balanced and disciplined approach.

🧠 1. Focus on Asset Allocation

Maintain a mix of equity, debt, and other asset classes

📉 2. Avoid Overexposure to Rate-Sensitive Stocks

Sectors like real estate and auto may face short-term pressure

📊 3. Look for Quality Businesses

Companies with:

- Strong pricing power

- Stable demand

- Healthy balance sheets

tend to perform better during inflationary periods

⏳ 4. Stay Invested for the Long Term

Short-term volatility should not derail long-term investment goals

A Broader Perspective

Historically, periods of rising oil prices and inflation have led to cautious monetary policy globally. India is no exception.

For example, during earlier commodity cycles, central banks often paused or delayed rate cuts until inflation showed signs of cooling. This pattern reinforces the importance of monitoring macroeconomic indicators.

Key Indicators to Watch

- Crude oil price trends

- CPI inflation data

- RBI policy statements

- Global economic developments

Tracking these indicators can provide early signals of policy direction.

FAQs

1. Why do rising oil prices impact inflation?

Because oil affects transportation and production costs, which increases the overall price of goods and services.

2. Why might RBI pause rate cuts?

To control inflation and maintain economic stability, especially when price pressures are rising.

3. How does this affect stock markets?

It can lead to cautious sentiment, especially in rate-sensitive sectors, while some sectors like energy may benefit.

4. What happens to bond yields in this scenario?

Bond yields usually rise when inflation increases, leading to a fall in bond prices.

5. What should investors do during such phases?

Maintain diversification, focus on quality investments, and avoid making decisions based on short-term volatility.

Conclusion

Rising oil prices and inflation are key factors shaping the current economic landscape. While markets were hoping for continued rate cuts, the reality is that the Reserve Bank of India may need to stay cautious.

For investors, this is not a time to panic but to adapt. A well-diversified portfolio, combined with a focus on quality and long-term discipline, can help navigate such phases effectively.

At Swastika Investmart, we empower investors with research-driven insights, advanced trading tools, and strong customer support to make informed decisions in changing market conditions.

21 Hours, No Agreement: What’s Next After US-Iran Talks Collapse?

Key Takeaways

- US-Iran talks ended without a deal after 21 hours of negotiations

- Rising tensions may lead to supply risks and higher oil prices

- Global markets could see increased volatility in the near term

- Indian markets may face pressure via inflation and currency movement

- Investors should stay cautious and focus on diversified portfolios

Introduction

After nearly 21 hours of intense negotiations, the much-anticipated US-Iran talks ended without any agreement. The development has once again brought geopolitical tensions into focus, with potential ripple effects across global markets.

Statements from leaders like Donald Trump and JD Vance indicate that the situation could escalate further, with options such as restricting Iran’s oil exports being considered.

For investors, especially in India, this is not just a political headline. It is a macro event that can influence oil prices, inflation, currency, and overall market sentiment.

What Happened in the US-Iran Talks?

The talks, held in Islamabad, were aimed at reaching a breakthrough on key issues, particularly Iran’s nuclear-related commitments. However, despite prolonged discussions, both sides failed to reach common ground.

Key Highlights:

- Negotiations lasted around 21 hours

- The US presented what it called its “final and best offer”

- No agreement was reached on core demands

- Strategic pressure options, including trade and oil restrictions, are being discussed

This outcome signals a shift from diplomacy toward increased geopolitical pressure.

Why This Matters Globally

The US and Iran are critical players in the global energy ecosystem. Any disruption in their relationship can have far-reaching consequences.

1. Oil Supply Risks

Iran is a key oil exporter. Any restriction on its exports can tighten global supply.

👉 Result: Oil prices may rise sharply

2. Inflation Concerns

Higher oil prices directly impact:

- Transportation costs

- Manufacturing expenses

- Consumer prices

This can push global inflation higher, complicating central bank policies.

3. Market Volatility

Geopolitical uncertainty often leads to:

- Equity market corrections

- Flight to safe-haven assets like gold

- Currency fluctuations

Impact on Indian Markets

India, being a major oil importer, is particularly sensitive to such developments.

📊 1. Crude Oil and Inflation

- India imports more than 80 percent of its crude oil needs

- Rising oil prices can increase inflation

👉 This may limit the flexibility of the Reserve Bank of India in cutting interest rates

📉 2. Equity Market Reaction

- Sectors like aviation, paints, and logistics may face cost pressures

- Oil marketing companies could see margin volatility

- Energy producers may benefit

💱 3. Currency Pressure

- Higher oil import bills can weaken the Indian Rupee

- This may lead to foreign investor outflows in the short term

Sector-Wise Impact: Winners and Losers

🚀 Likely Beneficiaries

- Oil and gas companies

- Upstream energy players

- Commodity-linked businesses

⚠️ Under Pressure

- Aviation sector

- FMCG companies facing input cost pressure

- Auto sector due to higher fuel costs

What Should Investors Do Now?

Geopolitical events are unpredictable, but your investment strategy does not have to be.

🧠 1. Stay Diversified

Avoid overexposure to a single sector or theme

📊 2. Focus on Quality Stocks

Companies with:

- Strong balance sheets

- Pricing power

- Stable demand

tend to perform better during uncertain times

⏳ 3. Avoid Panic Decisions

Short-term volatility is common during geopolitical tensions. Long-term investors should stay disciplined

🔍 4. Track Key Indicators

- Crude oil prices

- Inflation data

- Central bank commentary

A Real-World Perspective

We have seen similar situations in the past where geopolitical tensions led to temporary spikes in oil prices and market volatility. However, markets tend to stabilize once clarity emerges.

For example, during previous Middle East tensions, oil prices surged in the short term but normalized over time as supply adjusted.

This highlights an important lesson:

Markets react quickly, but they also adapt quickly

Why This Event Is Different

What makes this situation noteworthy is the potential policy shift toward stronger economic measures, including restrictions on oil exports.

If such actions are implemented, the impact could be more prolonged compared to past events.

FAQs

1. Why did the US-Iran talks fail?

The talks failed due to disagreements on key issues, particularly around nuclear-related commitments and compliance expectations.

2. How can this impact oil prices?

Any restriction on Iran’s oil exports can reduce global supply, leading to higher crude oil prices.

3. What does this mean for Indian investors?

It may lead to higher inflation, market volatility, and sector-specific impacts, especially in oil-sensitive industries.

4. Should investors be worried?

Short-term volatility is expected, but long-term investors should stay focused on fundamentals and avoid panic selling.

5. Which sectors benefit from rising oil prices?

Energy and oil-producing companies generally benefit, while fuel-dependent sectors may face pressure.

Conclusion

The collapse of the US-Iran talks is a reminder of how quickly global events can influence financial markets. While the immediate reaction may be volatility, the long-term impact will depend on how the situation evolves.

For Indian investors, the key is to stay informed, remain disciplined, and focus on quality investments.

At Swastika Investmart, we provide research-backed insights, advanced tools, and investor education to help you navigate such uncertain environments with confidence.

RBI’s New NBFC Rules Explained: Who Falls in the Upper Layer and Why It Matters

Key Takeaways

- RBI has simplified NBFC classification based on size and risk

- NBFCs with ₹1 lakh crore+ assets fall under the Upper Layer

- These entities will face stricter regulations and possible listing requirements

- The move aims to reduce systemic risk and improve transparency

- It can impact investors, markets, and large financial groups

Introduction

India’s financial ecosystem has evolved rapidly over the past decade, with Non-Banking Financial Companies (NBFCs) playing a critical role in credit growth. However, with size comes risk. To address this, the Reserve Bank of India has introduced a more streamlined framework to identify and regulate large NBFCs.

The new classification, especially the Upper Layer NBFCs, is a significant step toward strengthening financial stability. But what exactly does this mean, and why should investors care?

Understanding NBFC Layers: What Has Changed?

Earlier, RBI used a mix of factors like asset size, interconnectedness, and complexity to classify NBFCs. While comprehensive, this approach often lacked clarity.

The New Approach

Now, RBI has simplified the framework:

- Asset size becomes the primary criterion

- Any NBFC with ₹1 lakh crore or more in assets is categorized under the Upper Layer

This makes the system more transparent and predictable for both companies and investors.

What is an Upper Layer NBFC?

Upper Layer NBFCs are essentially systemically important financial institutions. Their size and interconnected nature mean that any disruption in their operations can impact the broader financial system.

Key Characteristics:

- Large balance sheets (₹1 lakh crore+ assets)

- High market influence

- Strong linkages with banks, markets, and borrowers

Examples (Contextual):

Large housing finance companies, infrastructure financiers, and diversified NBFC groups often fall into this category.

Stricter Rules for Upper Layer NBFCs

RBI’s objective is simple: bigger the institution, tighter the regulation.

Key Regulatory Changes:

1. Enhanced Compliance Requirements

- Tighter governance norms

- Stronger risk management frameworks

2. Mandatory Listing (in some cases)

- Upper Layer NBFCs may be required to list on stock exchanges

- This increases transparency and public accountability

3. Bank-Like Regulations

- Closer alignment with banking regulations

- Increased scrutiny on capital adequacy and asset quality

Why RBI Is Tightening the Rules

NBFCs are often referred to as “shadow banks” because they perform bank-like functions without being full-fledged banks.

The Risk Factor:

- Large NBFCs are deeply interconnected

- A failure can trigger system-wide stress

We have already seen examples in the past where NBFC stress impacted liquidity and market sentiment.

RBI’s Strategy:

- Identify large players early

- Reduce systemic risk

- Improve transparency through listing and disclosures

Market Impact: What It Means for Investors

This regulatory shift is not just a policy change. It has real implications for markets and portfolios.

1. Increased Transparency

Listed NBFCs provide:

- Better disclosures

- Regular financial reporting

👉 This helps investors make informed decisions

2. Valuation Re-rating Potential

- Companies moving toward listing may unlock value

- Institutional participation can increase

3. Short-Term Volatility

- Stricter norms may impact profitability in the short term

- Compliance costs could rise

4. Sector Consolidation

- Smaller NBFCs may struggle to scale

- Larger players could gain market share

The Tata Sons Case: A Real-World Complexity

One of the most talked-about cases is Tata Sons.

- Massive asset size puts it within the Upper Layer threshold

- However, it had surrendered its NBFC license earlier

The Dilemma:

- Should it still be regulated as an NBFC?

- If yes, will it be forced to list?

This case highlights that while the rule is simple, real-world application can be complex.

How Should Investors Approach NBFC Stocks Now?

With regulatory tightening, investors need a more selective approach.

Key Factors to Track:

- Asset quality (NPAs)

- Capital adequacy

- Governance standards

- Growth vs compliance balance

Practical Strategy:

- Prefer well-governed, large NBFCs

- Avoid over-leveraged or opaque balance sheets

- Diversify across financial sectors

Why This Move Matters for India’s Financial System

This is not just about NBFCs. It is about financial stability.

Long-Term Benefits:

- Reduced systemic risk

- Improved investor confidence

- Stronger credit ecosystem

Bigger Picture:

India’s financial markets are maturing, and such regulations bring them closer to global standards.

FAQs

1. What is an Upper Layer NBFC?

An NBFC with assets of ₹1 lakh crore or more, considered systemically important and subject to stricter regulations.

2. Why is RBI focusing on large NBFCs?

Because their failure can impact the entire financial system due to their size and interconnectedness.

3. Will all Upper Layer NBFCs be listed?

Not all, but RBI may require certain large NBFCs to list to improve transparency.

4. How does this impact investors?

It improves transparency but may also lead to short-term volatility due to stricter compliance.

5. Is this good for the market?

Yes, in the long run. It strengthens the financial system and builds investor trust.

Conclusion

RBI’s new NBFC framework marks a decisive shift toward simplification and stronger oversight. By clearly identifying large and systemically important players, the regulator aims to reduce risks before they become crises.

For investors, this creates a more transparent environment but also demands a sharper focus on quality and governance.

At Swastika Investmart, we help investors navigate such regulatory changes with in-depth research, advanced tools, and expert insights. Whether you are tracking NBFC stocks or building a diversified portfolio, staying informed is key.

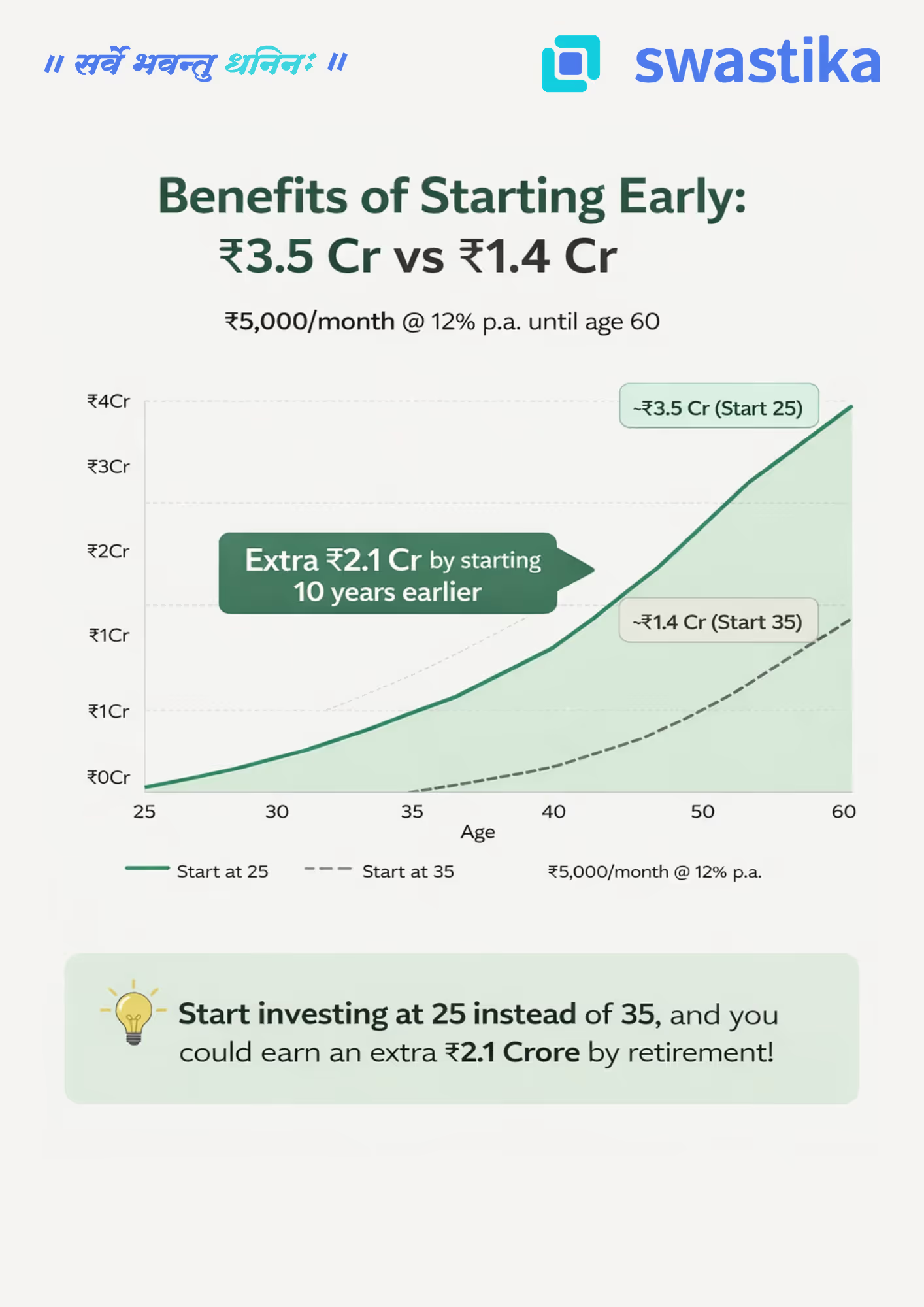

The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

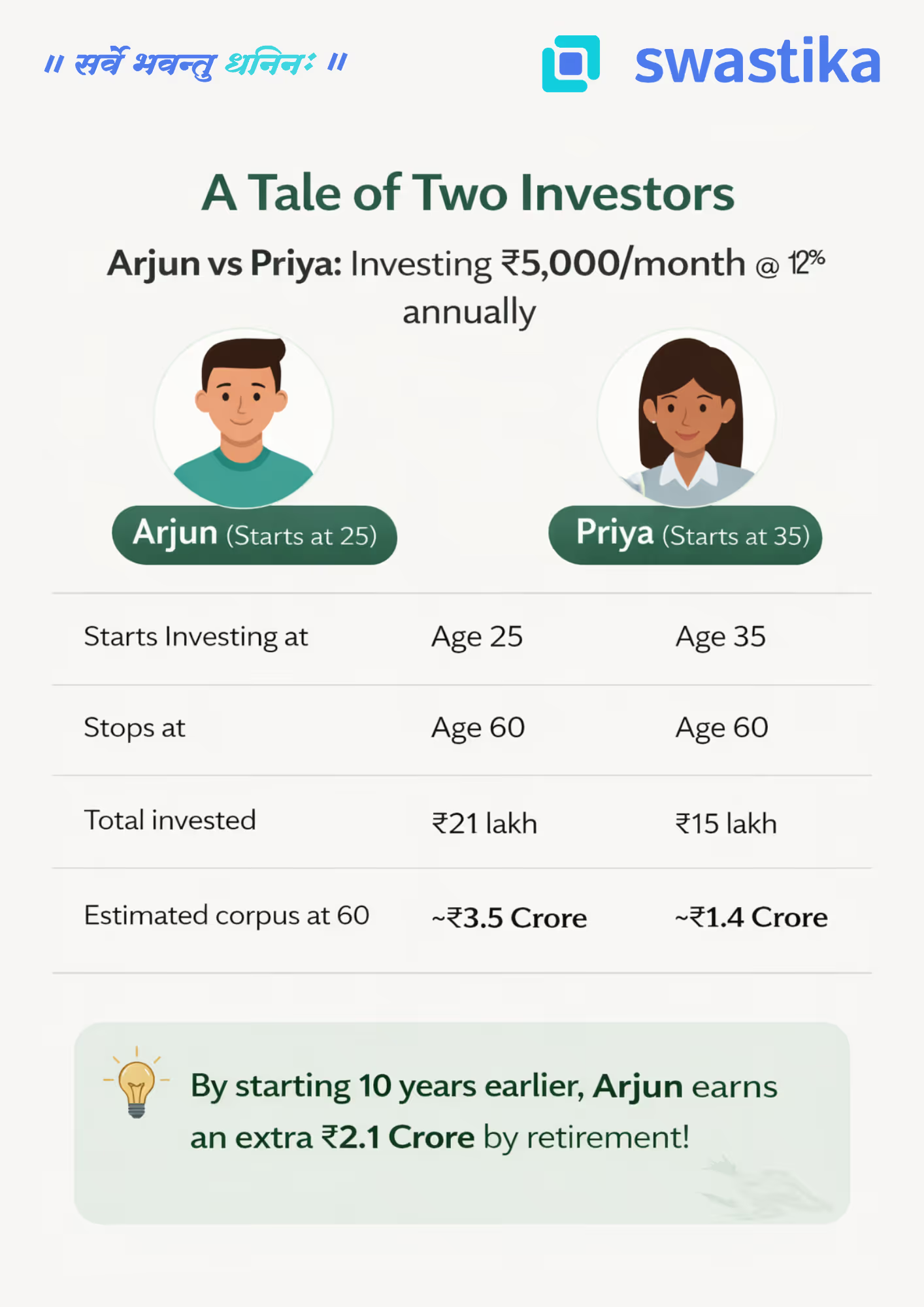

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

HRA, LTA, and Standard Deduction – Are You Claiming All Your Benefits?

Key Takeaways

- Many salaried individuals miss out on tax benefits due to lack of awareness

- HRA, LTA, and standard deduction can significantly reduce taxable income

- Choosing between old and new tax regime is crucial

- Proper documentation and planning can maximize savings

Are You Leaving Money on the Table?

Every year, millions of salaried employees in India file their income tax returns without fully utilizing available deductions.

If your salary structure includes House Rent Allowance, Leave Travel Allowance, and standard deduction, you could be saving a significant amount of tax. Yet, many people either misunderstand these benefits or fail to claim them properly.

Understanding how these components work can make a real difference in your take-home income.

Understanding HRA: More Than Just Rent

House Rent Allowance is one of the most commonly used tax-saving components for salaried individuals.

Who can claim HRA?

- Salaried employees receiving HRA as part of salary

- Individuals living in rented accommodation

How is HRA exemption calculated?

HRA exemption is the lowest of the following:

- Actual HRA received

- 50% of salary for metro cities or 40% for non-metros

- Rent paid minus 10% of salary

Real-life example

Suppose you earn ₹10 lakh annually and pay ₹25,000 monthly rent in Mumbai.

- Annual rent: ₹3 lakh

- 10% of salary: ₹1 lakh

- Eligible exemption: ₹2 lakh

This amount reduces your taxable income significantly.

Common mistake

Many taxpayers either do not submit rent receipts or assume full HRA is exempt. This leads to higher tax liability.

LTA: Travel Smart, Save Tax

Leave Travel Allowance allows you to claim tax exemption on travel expenses within India.

Key points to remember

- Covers only travel costs, not hotel or food

- Valid for two journeys in a block of four years

- Only domestic travel is allowed

Example

If you travel with your family from Delhi to Goa and spend ₹40,000 on flight tickets, this amount can be claimed under LTA.

Important tip

If you do not use LTA within the block period, the benefit lapses. Planning your travel can help you maximize this exemption.

Standard Deduction: The Simplest Tax Benefit

Standard deduction is the easiest and most straightforward tax benefit available.

Current benefit

- ₹50,000 deduction available for salaried individuals and pensioners

No bills or proofs are required. It is automatically deducted from your salary income.

Why it matters

Even though it looks small, it directly reduces taxable income and applies to almost every salaried taxpayer.

Old vs New Tax Regime: The Big Decision

One of the most critical decisions today is choosing between the old and new tax regimes.

Old Tax Regime

- Allows HRA, LTA, and other deductions

- Suitable for individuals with multiple tax-saving components

New Tax Regime

- Lower tax rates

- Limited deductions available

- Standard deduction is still applicable

What should you choose?

If your salary includes HRA and you actively claim deductions, the old regime may be more beneficial.

However, if you prefer simplicity and fewer compliances, the new regime might work better.

Impact on Indian Investors

Tax savings directly influence disposable income.

Higher savings can be redirected into:

- Equity investments

- Mutual funds

- Retirement planning

For example, saving ₹50,000 annually in taxes and investing it in equities over 10 years can create substantial wealth.

This is why tax planning is not just about saving money, but also about building long-term financial security.

Regulatory Perspective

Tax benefits like HRA, LTA, and standard deduction are governed under the Income Tax Act.

Authorities like Income Tax Department of India ensure compliance and transparency.

Taxpayers are required to maintain proper documentation and file accurate returns to avoid penalties.

Practical Tips to Maximize Benefits

1. Maintain Proper Documentation

Keep rent receipts, travel tickets, and salary slips ready.

2. Plan Travel in Advance

Use LTA strategically within block periods.

3. Review Salary Structure

Understand how your salary components are structured.

4. Choose the Right Tax Regime

Compare both regimes before filing returns.

How Swastika Investmart Can Help

Tax planning is the first step toward smart investing.

Swastika Investmart helps investors make the most of their savings through:

- SEBI-registered credibility ensuring trust

- Research-backed insights for investment planning

- Tech-enabled platforms for easy investing

- Dedicated customer support

- Strong focus on investor education

Instead of letting tax savings sit idle, you can channel them into wealth creation opportunities.

FAQs

1. Can I claim both HRA and standard deduction?

Yes, both can be claimed together under applicable conditions.

2. Is LTA available every year?

No, it is available for two journeys in a block of four years.

3. Can I claim HRA if I live in my own house?

No, HRA is only applicable if you live in rented accommodation.

4. Which tax regime is better for salaried individuals?

It depends on your deductions. The old regime is better if you claim multiple exemptions.

5. Do I need proof for standard deduction?

No, standard deduction does not require any documentation.

Conclusion

HRA, LTA, and standard deduction are powerful tools that can significantly reduce your tax burden. Yet, many individuals fail to use them effectively.

A little awareness and planning can help you retain more of your hard-earned money and put it to better use.

If you want to turn your tax savings into long-term wealth with expert guidance and smart tools, you can get started here:

From Power to Data: How Adani Is Creating a 360° Growth Engine in Odisha

Key Takeaways

- Adani Group is investing ₹33,081 crore in Odisha across power, data centers, and cement

- Strategy focuses on building an integrated ecosystem, not standalone projects

- Data center expansion aligns with India’s digital growth story

- The move could boost regional economy and long-term investor confidence

A Strategic Shift Beyond Infrastructure

When Adani Group announced its ₹33,081 crore investment in Odisha, it was not just another infrastructure expansion headline.

It signaled a deeper strategic shift.

The group is not building isolated assets. Instead, it is creating a 360 degree growth engine by combining power generation, data infrastructure, and manufacturing. This integrated approach could redefine how large conglomerates scale in India.

For investors, the bigger question is not what Adani is building, but why Odisha and why now.

Why Odisha Is Becoming a Strategic Hub

Odisha has quietly emerged as one of India’s most attractive investment destinations.

Key advantages

- Abundant natural resources

- Strong port connectivity

- Proactive state government policies

- Availability of land for large-scale projects

Odisha already hosts major steel and mining operations. Now, with increasing focus on industrial corridors and digital infrastructure, it is evolving into a multi-sector hub.

For companies like Adani, this offers a unique opportunity to build integrated ecosystems at scale.

The Three Pillars of Adani’s Odisha Strategy

Adani’s ₹33,081 crore plan revolves around three core sectors. Each plays a specific role, but together they create a powerful growth engine.

1. Power: The Backbone of Everything

Energy remains the foundation of Adani’s business model.

The group is setting up a large power plant in Odisha, which will not only supply electricity to industries but also support its own future projects.

Why this matters

- Data centers require uninterrupted power supply

- Manufacturing units depend on stable energy

- Owning power assets improves cost efficiency

In simple terms, power is the base layer that enables everything else.

2. Data Centers: Betting Big on Digital India

India’s data consumption is growing at an exponential pace.

With rising internet users, cloud adoption, and AI applications, the demand for data storage and processing is exploding.

Adani’s entry into data centers in Odisha is a strategic move to capture this opportunity.

Real-world context

Think about how platforms like OTT streaming, fintech apps, and e-commerce rely on data centers. As usage increases, companies need more infrastructure to handle traffic.

Growth drivers

- Digital India initiatives

- AI and cloud adoption

- Rising smartphone penetration

Data centers are expected to become one of the fastest-growing infrastructure segments in India.

3. Cement: Supporting Infrastructure Boom

The third pillar is cement manufacturing.

This aligns with India’s ongoing infrastructure push, including roads, housing, and industrial projects.

Why cement matters

- Completes the infrastructure value chain

- Supports internal projects and external demand

- Benefits from government spending on construction

By adding cement capacity, Adani strengthens its presence in core infrastructure.

The Power of Integration: A 360 Degree Model

What makes this investment unique is the integration across sectors.

How the ecosystem works

- Power plant supplies energy to data centers and cement units

- Cement supports construction of infrastructure projects

- Data centers create high-value digital assets

This creates a self-sustaining cycle.

Instead of depending on external suppliers, Adani builds internal efficiencies. This not only reduces costs but also improves scalability.

Impact on Indian Markets

Adani’s Odisha strategy has broader implications beyond the company itself.

1. Boost to Infrastructure and Capex Cycle

Large investments signal confidence in India’s growth story. This can trigger more private sector capex.

2. Positive for Power and Cement Stocks

Companies in these sectors may benefit from increased demand and pricing power.

3. Data Center Theme Gains Momentum

The data center story is still in its early stages in India. Adani’s aggressive push validates this emerging theme.

4. Regional Economic Growth

Odisha could see job creation, improved infrastructure, and higher industrial activity.

Regulatory and Policy Context

India’s regulatory environment plays a key role in enabling such investments.

- SEBI ensures transparency for listed entities and investor protection

- State governments offer incentives for industrial projects

- Policies supporting renewable energy and digital infrastructure add tailwinds

Odisha’s investor-friendly approach has been a major enabler for large-scale investments like this.

What Should Investors Watch?

While the strategy looks promising, investors should track execution closely.

Key factors

- Project timelines and cost management

- Demand growth in data centers

- Power sector regulations and tariffs

- Cement pricing trends

Execution risk is always present in large capex projects. However, successful implementation can create long-term value.

A Ground-Level Perspective

Consider a simple example.

A new data center comes up in Odisha. It requires uninterrupted electricity, which Adani’s power plant provides. The construction uses cement produced by its own unit.

Over time, this data center attracts global tech companies. This creates jobs, increases demand for services, and boosts the local economy.

This is how a single integrated investment multiplies impact.

How Swastika Investmart Helps You Track Such Opportunities

Large investment themes can be complex to decode.

Swastika Investmart helps investors navigate such opportunities with:

- SEBI-registered credibility ensuring trust

- In-depth research on sectors like infrastructure, power, and digital

- Advanced tools for tracking market trends

- Strong customer support

- Focus on investor education

Instead of chasing headlines, investors can build a structured approach based on insights and data.

FAQs

1. What is Adani’s total investment in Odisha?

Adani Group has announced an investment of ₹33,081 crore across power, data centers, and cement.

2. Why is Odisha important for this investment?

Odisha offers resources, connectivity, and supportive policies, making it ideal for large-scale integrated projects.

3. How do data centers contribute to growth?

Data centers support digital services, cloud computing, and AI, making them a key growth driver in the digital economy.

4. What sectors benefit from this investment?

Power, cement, infrastructure, and digital technology sectors are expected to benefit.

5. Is this positive for Indian markets?

Yes, it signals strong private sector investment and supports long-term economic growth.

Conclusion

Adani’s Odisha investment is more than a capex announcement. It reflects a well-thought-out strategy to build an integrated growth engine spanning power, data, and infrastructure.

For investors, the opportunity lies in understanding the broader theme rather than focusing on short-term movements.

India’s growth story is increasingly driven by such large-scale, multi-sector investments.

If you want to stay ahead of such opportunities with expert-backed insights and powerful tools, you can begin here:

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App