RBI currency intervention And The Rupee Open: Navigating The 94.2-94.75 Band For Retail Investors

Key Takeaways

- The rupee opened weaker at 94.57 per USD, staying within a 94.20-94.75 band.

- The US Dollar Index rose to 101.28 while crude stayed above $70.

- RBI currency intervention has been buying dollars around 94.10-94.20 to support exporters with hedging opportunities.

- Near-term rupee direction is expected to stay within Finrex's band despite dollar strength.

RBI currency intervention remains central as the rupee starts the session with a slight weakness. The rupee opened at 94.57 per U.S. dollar, down 4 paise from the previous close of 94.53. The trading band for the session is expected to be 94.20-94.75, a range Finrex has flagged as the near-term anchor. The U.S. Dollar Index strengthened to 101.28 from around 101, while crude oil prices stayed above the $70 per barrel mark. In this environment, rbi currency intervention has included dollar purchases around the 94.10-94.20 levels, a policy move that supports exporters with hedging opportunities and helps importers manage near-term obligations.

RBI currency intervention And The Rupee Open: What It Means For Retail Investors

The opening tells you the scene remains delicate. The rupee’s early move reflects the tug-of-war between dollar strength and policy-backed support. For a retail investor, the key takeaway is not a single number but the recurring anchor: the 94.20-94.75 band. If the rupee tests the upper end of that range, importers could face higher USD-based costs, while exporters gain a hedging edge. The central bank’s currency intervention around 94.10-94.20 levels is designed to smooth volatility and provide a more predictable environment for hedging. This is also where Swastika’s AI stock assistant, Sarthi, can help translate macro FX signals into stock ideas that fit your risk profile.

Rupee Open At 94.57 Today: Decoding The 94.20-94.75 Band And What It Means For Your FX Hedging

At 94.57, the rupee sits in a zone where market participants expect the band to hold. A move toward 94.75 could signal a test of the upper bound, while a fall toward 94.20 might reflect stronger importer demand. The Finrex-drawn band of 94.20-94.75 remains the near-term guide, and the range could be reinforced by ongoing dollar strength and risk sentiment. The USD index at 101.28 and crude above 70 dollars keep pressure on the rupee, suggesting hedging strategies should account for notable volatility ahead. In such conditions, exporters often rely on hedging structures to lock in favorable rates, while importers manage near-term payment obligations through streamlined FX operations.

Dollar Strength And Asian Currency Moves: Implications For Indian Markets

Asian currencies traded mixed amid a firmer dollar. The Malaysian ringgit rose 0.52 percent, the Indonesian rupiah gained 0.40 percent, the Chinese renminbi inched up 0.07 percent, and the Taiwan dollar added 0.06 percent. Despite these moves, the rupee could remain under pressure if underlying market flows continue to favour the dollar. The 101.28 level on the USD Index acts as a global anchor, with crude sustaining above the $70 threshold. While the macro backdrop remains supportive of dollar strength, you should monitor how domestic policy and corporate earnings interact with currency trends to inform your portfolio allocations.

Market Movers In Indian Stocks: reliance industries limited stock price, state bank of india stock price, infosys stock price, stock price of tcs, hdfc bank stock price, icici bank stock

In the domestic market, traders often look at major names as a quick read on sentiment. The set of keywords you’ll encounter includes reliance industries limited stock price and the state bank of india stock price, both reflecting the scale and sensitivity of India’s economy to currency shifts. Infosys stock price and the stock price of tcs are other benchmarks for how non-commodity sectors ride macro cues. The larger banks, including hdfc bank stock price and icici bank stock, also respond to liquidity and FX expectations. While these moves are not a direct forecast of currency policy, they offer a practical read on how global dollar strength, oil, and policy action translate into equity performance. For retail investors, it’s useful to track these stocks alongside FX signals to gauge potential hedges or positional adjustments to your portfolio.

Frequently Asked Questions

What is RBI currency intervention?

RBI currency intervention refers to the central bank's actions to influence currency markets by buying or selling foreign currency to moderate volatility. In this context, the central bank has been purchasing dollars around the 94.10-94.20 levels to cushion the rupee.

How does the rupee perform in the current session?

The rupee opened at 94.57 per USD, down 4 paise from the previous close of 94.53, and is expected to trade in a 94.20-94.75 band.

What does Finrex’s band imply for traders?

Finrex indicates a near-term trading band of 94.20-94.75 for the rupee, which helps guide hedging decisions and domestic liquidity considerations during the session.

What is the impact of dollar strength on Indian markets?

A firmer U.S. dollar, with the U.S. Dollar Index around 101.28 and crude above $70, tends to pressurize the rupee and influence debt and equity markets in India.

What should retail investors do with RBI currency intervention knowledge?

Retail investors can use this information to inform hedging strategies, balance currency exposure, and consider stock ideas via Swastika's Sarthi AI stock assistant.

Conclusion

you can use a rules-based approach–such as hedging near the upper bound when USD strength is persistent and reducing exposure when the rupee tests the lower end–so you stay within your targeted risk envelope. The macro environment remains supportive of dollar strength given crude above 70 and a USD Index around 101.28, so you should expect volatility to persist in the near term. The most important next step is to incorporate FX risk into your investment thesis and use hedging tools to maintain portfolio resilience.

Latest Articles

RBI currency intervention And The Rupee Open: Navigating The 94.2-94.75 Band For Retail Investors

Key Takeaways

- The rupee opened weaker at 94.57 per USD, staying within a 94.20-94.75 band.

- The US Dollar Index rose to 101.28 while crude stayed above $70.

- RBI currency intervention has been buying dollars around 94.10-94.20 to support exporters with hedging opportunities.

- Near-term rupee direction is expected to stay within Finrex's band despite dollar strength.

RBI currency intervention remains central as the rupee starts the session with a slight weakness. The rupee opened at 94.57 per U.S. dollar, down 4 paise from the previous close of 94.53. The trading band for the session is expected to be 94.20-94.75, a range Finrex has flagged as the near-term anchor. The U.S. Dollar Index strengthened to 101.28 from around 101, while crude oil prices stayed above the $70 per barrel mark. In this environment, rbi currency intervention has included dollar purchases around the 94.10-94.20 levels, a policy move that supports exporters with hedging opportunities and helps importers manage near-term obligations.

RBI currency intervention And The Rupee Open: What It Means For Retail Investors

The opening tells you the scene remains delicate. The rupee’s early move reflects the tug-of-war between dollar strength and policy-backed support. For a retail investor, the key takeaway is not a single number but the recurring anchor: the 94.20-94.75 band. If the rupee tests the upper end of that range, importers could face higher USD-based costs, while exporters gain a hedging edge. The central bank’s currency intervention around 94.10-94.20 levels is designed to smooth volatility and provide a more predictable environment for hedging. This is also where Swastika’s AI stock assistant, Sarthi, can help translate macro FX signals into stock ideas that fit your risk profile.

Rupee Open At 94.57 Today: Decoding The 94.20-94.75 Band And What It Means For Your FX Hedging

At 94.57, the rupee sits in a zone where market participants expect the band to hold. A move toward 94.75 could signal a test of the upper bound, while a fall toward 94.20 might reflect stronger importer demand. The Finrex-drawn band of 94.20-94.75 remains the near-term guide, and the range could be reinforced by ongoing dollar strength and risk sentiment. The USD index at 101.28 and crude above 70 dollars keep pressure on the rupee, suggesting hedging strategies should account for notable volatility ahead. In such conditions, exporters often rely on hedging structures to lock in favorable rates, while importers manage near-term payment obligations through streamlined FX operations.

Dollar Strength And Asian Currency Moves: Implications For Indian Markets

Asian currencies traded mixed amid a firmer dollar. The Malaysian ringgit rose 0.52 percent, the Indonesian rupiah gained 0.40 percent, the Chinese renminbi inched up 0.07 percent, and the Taiwan dollar added 0.06 percent. Despite these moves, the rupee could remain under pressure if underlying market flows continue to favour the dollar. The 101.28 level on the USD Index acts as a global anchor, with crude sustaining above the $70 threshold. While the macro backdrop remains supportive of dollar strength, you should monitor how domestic policy and corporate earnings interact with currency trends to inform your portfolio allocations.

Market Movers In Indian Stocks: reliance industries limited stock price, state bank of india stock price, infosys stock price, stock price of tcs, hdfc bank stock price, icici bank stock

In the domestic market, traders often look at major names as a quick read on sentiment. The set of keywords you’ll encounter includes reliance industries limited stock price and the state bank of india stock price, both reflecting the scale and sensitivity of India’s economy to currency shifts. Infosys stock price and the stock price of tcs are other benchmarks for how non-commodity sectors ride macro cues. The larger banks, including hdfc bank stock price and icici bank stock, also respond to liquidity and FX expectations. While these moves are not a direct forecast of currency policy, they offer a practical read on how global dollar strength, oil, and policy action translate into equity performance. For retail investors, it’s useful to track these stocks alongside FX signals to gauge potential hedges or positional adjustments to your portfolio.

Frequently Asked Questions

What is RBI currency intervention?

RBI currency intervention refers to the central bank's actions to influence currency markets by buying or selling foreign currency to moderate volatility. In this context, the central bank has been purchasing dollars around the 94.10-94.20 levels to cushion the rupee.

How does the rupee perform in the current session?

The rupee opened at 94.57 per USD, down 4 paise from the previous close of 94.53, and is expected to trade in a 94.20-94.75 band.

What does Finrex’s band imply for traders?

Finrex indicates a near-term trading band of 94.20-94.75 for the rupee, which helps guide hedging decisions and domestic liquidity considerations during the session.

What is the impact of dollar strength on Indian markets?

A firmer U.S. dollar, with the U.S. Dollar Index around 101.28 and crude above $70, tends to pressurize the rupee and influence debt and equity markets in India.

What should retail investors do with RBI currency intervention knowledge?

Retail investors can use this information to inform hedging strategies, balance currency exposure, and consider stock ideas via Swastika's Sarthi AI stock assistant.

Conclusion

you can use a rules-based approach–such as hedging near the upper bound when USD strength is persistent and reducing exposure when the rupee tests the lower end–so you stay within your targeted risk envelope. The macro environment remains supportive of dollar strength given crude above 70 and a USD Index around 101.28, so you should expect volatility to persist in the near term. The most important next step is to incorporate FX risk into your investment thesis and use hedging tools to maintain portfolio resilience.

Hdfc Bank Share Price Insights: hdfc bank share price Signals From Board Appointments and Fresh Fundraising

Key Takeaways

- hdfc bank share price may move on board changes and fundraising signals.

- axis bank stock price context shifts after CFO resignations.

- sbi bonds issuance underscores liquidity in the Indian banking space.

- kec international orders and renewables wins widen the infra and energy backdrop.

Today’s market narrative for Indian banks and infrastructure names is thick with boardroom shifts, fundraising approvals, and fresh order inflows. hdfc bank share price watchers are watching HDFC Bank as independent director Rajiv Kumar eyes a four-year term from June 30, 2026, with a potential three-year chairmanship subject to approvals. As other large banks announce funding and debt moves, the sector's risk-reward is shifting. These developments come as several listed banks in India report corporate actions that could shape liquidity, valuations, and investor focus for the next few weeks.

In a sector-wide update, HDFC Bank named Rajiv Kumar as an independent director for a four-year term starting June 30, 2026, who is also proposed as Part-time Chairman for three years subject to regulatory and shareholder approvals. This governance refresh is part of a broader trend of leadership changes across Indian lenders, where institutions blend governance with growth strategy. The timing matters because the market often prices in such changes into the hdfc bank share price and other bank valuations as investors reassess risk and opportunity in a more volatile macro backdrop.

The Yes Bank fundraising story features a board approved plan to raise up to ₹7,500 crore equity and up to ₹8,500 crore via debt securities. This is a strong signal of capital adequacy strengthening and growth ambitions within the bank's strategy as of now. Investors will be evaluating the plan against the bank's current capital adequacy ratio, provisioning levels, and the trajectory of non-performing assets in the near term. If the plan is executed in full and the greenshoe option is utilized, the stock could see re-rating potential relative to its peers in the sector.

State Bank of India tapped the international debt market, raising 300 million dollars through three-year senior unsecured floating-rate sbi bonds issued via its London branch. The move underscores the bank's liquidity position and the willingness of global investors to participate in Indian banking credits, which may influence the pricing of bank stocks in Friday's session. Axis Bank CFO Puneet Sharma has resigned, a development that could affect the axis bank stock price as investors reprice risk and reassess financial strategy execution in the near term. Bandhan Bank CFO Rajeev Mantri resigned, underscoring a similar theme across private lenders about governance continuity during a period of sector transformation.

On the infrastructure and capital goods front, KEC International reported fresh orders worth ₹1,754 crore across its businesses, boosting its order book and signaling a continued pipeline across its engineering services, manufacturing and infrastructure segments. Investors will weigh the mix of orders to gauge revenue visibility and margin potential in the near to medium term. In transmission and energy infrastructure, Power Grid Corporation acquired a 100% stake in Kakinada I Transmission SPV for ₹20.5 crore, linking to a green hydrogen and green ammonia initiative in Andhra Pradesh. The project includes a 765/400 kV GIS substation, a STATCOM installation and transmission line works, highlighting the synergy between transmission capacity expansion and green fuels deployment.

In renewable energy, Sterling and Wilson Renewable Energy has secured a letter of award for a 1,000 MWac solar photovoltaic project along with a 600 MWh battery energy storage system project in Egypt; the contract is valued at 560 million dollars. This international contract underscores the expansion of Indian renewable developers into offshore markets and signals strong demand for large-scale solar plus storage projects. Within financial services, Aditya Birla Capital allotted non-convertible debentures worth ₹300 crore through private placement with a greenshoe option of ₹100 crore. This indicates continued appetite for debt financing among diversified financial services players and supports growth initiatives and balance-sheet management.

Balkrishna Industries expanded its carbon black manufacturing capacity to 3.6 lakh MTPA by adding 95,000 MTPA, while captive power generation capacity rose to 64 MW with an additional 24 MW installation. The expansion enhances capacity to meet rising demand while improving cost efficiency and margins. In technology leadership, Coforge appointed Anup Nair as Chief AI Commercial Officer as part of leadership expansion to leverage AI for improved client outcomes. NLC India allotted commercial papers worth ₹400 crore on June 29, 2026, signaling continued financing activity in the power space. Juniper Hotels reported the resignation of CFO Tarun Jaitly, prompting questions about financial oversight during expansion across hospitality assets.

Manorama Industries approved a QIP with a fixed floor price of ₹1,547.18 per share and regulatory permission to offer a discount up to 5 percent on the floor price. This setup provides a capital-raising pathway while offering downside protection and potential upside if market conditions support the issue. Taken together, these announcements reflect a broad spectrum of fundraising, expansion, and governance actions across sectors that could keep the market in focus on Tuesday’s trading session. Investors should weigh how macro variables like rates and inflation interact with sector-specific catalysts to define risk and opportunity today.

Retail investors can benefit from a disciplined approach to digesting a diverse set of headlines. If you want deeper, institution-grade research to translate these actions into price implications, Swastika Investmart offers Sarthi, an AI stock assistant that delivers actionable insights on any stock or index. The tool helps you synthesize corporate actions into clear investment theses and supports risk management in a volatile environment.

Note: All figures referenced are based on public disclosures and post-close information. These announcements are expected to keep listed stocks in focus during Tuesday's trading session as investors assess fundraising plans, management changes, order inflows and expansion initiatives.

Yes Bank Fundraising

The Yes Bank fundraising plan to raise up to ₹7,500 crore through equity and up to ₹8,500 crore through debt securities signals capital adequacy strengthening and growth ambitions across the sector. The move is designed to bolster the bank’s balance sheet and support future lending and investment initiatives, with investors closely watching how the plan affects capital adequacy ratios and potential dilution.

Axis Bank Stock Price Context

Axis Bank stock price dynamics could be influenced by the resignation of CFO Puneet Sharma, as investors reassess risk and the bank’s financial strategy execution. The leadership change may invite closer scrutiny of cost management, capex plans, and growth trajectories across retail and corporate banking segments, potentially affecting near-term pricing and sentiment.

KEC International Orders

KEC International reported fresh orders worth ₹1,754 crore across its businesses, expanding the companys order book and offering visibility into earnings potential and margin trajectory as projects advance. The breadth of the order mix across engineering services, manufacturing and infrastructure suggests a diversified revenue profile that could support resilience in earnings through cycles.

Power Grid and Green Energy Projects

Power Grid’s acquisition of a 100% stake in Kakinada I Transmission SPV for ₹20.5 crore aligns with a broader push to develop transmission infrastructure for green hydrogen and green ammonia projects in Andhra Pradesh. The project includes a 765/400 kV GIS substation, STATCOM installation and transmission line works, reflecting the intersection of grid modernization with the energy transition–an area that could contribute to durable long-term demand for grid equipment and related services.

Sterling and Wilson Renewable Energy Egypt Contract

Sterling and Wilson Renewable Energy has secured a 1,000 MWac solar photovoltaic project along with a 600 MWh battery energy storage system project in Egypt; the contract is valued at 560 million dollars. International project wins of this scale demonstrate the growth and diversification of Indian renewable players, with potential implications for margins and execution capability as projects scale globally.

Aditya Birla Capital NCDs

Aditya Birla Capital allotted non-convertible debentures worth ₹300 crore through private placement with a greenshoe option of ₹100 crore. The instrument highlights ongoing demand for structured debt within financial services and demonstrates the ability of major groups to mobilize capital efficiently to support growth strategies and refinance obligations.

Balkrishna Industries Capacity Expansion

Balkrishna Industries expanded its carbon black manufacturing capacity to 3.6 lakh MTPA by adding 95,000 MTPA; captive power generation capacity rose to 64 MW with an additional 24 MW installation. The expansion helps the company maintain competitiveness by balancing volume growth with input costs and energy efficiency in a price-sensitive global market.

Coforge Leadership Expansion

Coforge appointed Anup Nair as Chief AI Commercial Officer as part of leadership expansion aimed at accelerating AI-driven offerings for enterprise clients. This move underscores AI's importance in enterprise software services and signals a strategic pivot toward more data-driven, AI-enabled client solutions.

NLC India CPs

NLC India allotted commercial papers worth ₹400 crore on June 29, 2026, indicating ongoing financing activity in the power sector and supporting project execution timelines in an environment of dynamic power demand and growth expectations.

Juniper Hotels CFO Resignation

Tarun Jaitly resigned as CFO at Juniper Hotels, highlighting the ongoing governance considerations as hospitality players expand and invest in new properties and services. CFO changes in this sector can affect capital allocation, debt management, and cost control strategies in the near term.

Manorama Industries QIP

Manorama Industries approved a QIP with a fixed floor price of ₹1,547.18 per share and may offer a discount up to 5 percent on the floor price, aligning with regulatory provisions for capital raising while balancing investor interest and potential dilution. The QIP mechanism provides a funding channel for expansion plans while signaling market reception for the companys growth strategy.

Note on Context and Tuesday Focus

These announcements are likely to keep the market focused on banks, infra and renewables stocks during Tuesday trading as investors weigh fundraising plans, management changes, order inflows and expansion initiatives. The diverse mix of corporate actions across these sectors suggests that differentiating between value and growth opportunities will be critical for retail investors navigating volatility.

Frequently Asked Questions

What board changes did HDFC Bank announce?

Independent Director Rajiv Kumar has been appointed for a four-year term beginning June 30, 2026, and is proposed as Part-time Chairman for three years, subject to regulatory and shareholder approvals.

What are Yes Bank fundraising plans?

The Yes Bank board approved plans to raise up to ₹7,500 crore through equity instruments and up to ₹8,500 crore via debt securities.

How did SBI raise funds recently?

State Bank of India raised 300 million dollars through three-year senior unsecured floating-rate bonds issued via its London branch.

What CFO resignations occurred at Axis Bank and Bandhan Bank?

Axis Bank CFO Puneet Sharma resigned; Bandhan Bank CFO Rajeev Mantri resigned.

What are the key KEC International and infrastructure order updates?

KEC International reported fresh orders worth ₹1,754 crore across its businesses, adding to its order pipeline and improving revenue visibility.

Conclusion

Retail investors should interpret these headlines as a dynamic set of catalysts rather than a single directional signal. The hdfc bank share price could respond to governance and fundraising signals, while axis bank stock price and sbi bonds developments offer a broader sense of risk appetite and liquidity in the sector. A disciplined framework can help, such as comparing price action around governance events with peers and testing theses against order inflows. If you want deeper, actionable research, Sarthi provides tailored analyses on any stock or index to support your decisions.

Kirloskar Oil Engines Ltd Share Price Outlook: Motilal Oswal's Bullish Triggers and Target

Key Takeaways

- Motilal Oswal reiterates Buy on kirloskar oil engines ltd share price and raises FY27/FY28 earnings estimates by 3% and 10%, with Rs 2,750 as the revised target.

- Growth levers span powergen, industrial, and exports, supported by a strong order pipeline including a hyperscaler win.

- Execution visibility and ongoing capex could unlock more upside for kirloskar oil engines ltd share price over the next 12-18 months.

- Key risks include demand slowdowns, aggressive competition, and commodity-price volatility; investors should monitor order execution and margins.

Is kirloskar oil engines ltd share price poised for a new leg up? As Motilal Oswal reiterates a Buy rating and lifts earnings estimates for FY27 and FY28, investors are weighing a mix of catalysts across powergen, industrial, and export segments. The revised target price of Rs 2,750 signals a path to earnings visibility through FY27 and FY28. The story is not just about a single number; it is about a set of growth levers that could lift the share price trajectory over the next 12-18 months.

The brokerage has raised its earnings estimates for FY27 by 3% and for FY28 by 10%, reflecting stronger demand and execution potential. This update comes with a positive read on the overall demand environment in Kirloskar's current operating segments – powergen, industrial, and exports. A large order win from a hyperscaler adds a new dimension to the growth story, with execution to be completed during this fiscal year and potential spillovers into future data centre projects. Ongoing capex will enable capacity expansion and better utilization of the asset base, while the company's initiatives on new product development are expected to yield results over time.

For retail investors, these dynamics translate into a clearer earnings trajectory and the potential for a re-rating if execution remains confident. The institutional note highlights a strong order pipeline and demand visibility across the operating segments, which could help kirloskar oil engines share price maintain an uptrend even in a rising rate environment. As you digest this update, make a habit of cross-checking headlines with the underlying execution metrics–such as order wins, capex spend, and new product launches–before making any allocation decisions. If you want deeper, data-driven analysis and scenario planning, Swastika's Sarthi AI stock assistant offers institutional-grade research on kirloskar oil engines ltd share price and other stocks.

Kirloskar Oil Engines Share Price Outlook After Motilal Oswal Bullish Call

The core implication for the kirloskar oil engines share price is an alignment of earnings visibility with an improved demand environment. The revised Rs 2,750 target price signals that Motilal Oswal expects the company's earnings growth across FY27 and FY28 to underpin a meaningful re-rating if execution sticks to plan. The growth levers are broad-based: powergen remains a stabilizing engine as demand for reliable, efficient gensets and LCVs continues to accelerate in a developing economy. Industrial applications, including motive power for manufacturing and automation lines, are also poised to benefit from capex cycles, fueling a steady revenue stream. Exports, traditionally a smaller but high-margin segment, are catching up as the company broadens its footprint beyond the domestic market. In this context, kirloskar oil engines share price could respond to a confluence of faster-than-expected order execution and a sustained recovery in industrial capex. Management commentary and the broker’s note converge on a more optimistic near-term trajectory, with the hyperscaler order representing a potential inflection point. The timing of this execution matters: if the company can complete the order within this fiscal year, it not only rewards the order win but also de-risks the project pipeline for other data centre opportunities. This is particularly important for the kirloskar oil engines share price because a few high-visibility wins help reduce execution risk and improve the reliability of earnings estimates. The combination of a robust order book, capacity expansion, and product development pipelines should bolster investor confidence in the stock’s ability to navigate a challenging macro backdrop.

From a broader perspective, the investor takeaway is straightforward: the stock’s fate now hinges on translating orders into revenue growth and sustainable margins. The revised earnings estimates are a positive signal, but they will depend on execution speed and the company’s ability to manage cost pressures that arise from raw material inflation. For traders, the risk-reward looks balanced if one assumes a few quarters of steady progress on the order book and a modest recovery in global demand for powergen and industrial equipment. For long-term investors, the story remains constructive but requires patience as capex cycles mature and new products reach scale.

Kirloskar Oil Engines Share Price Target Drivers Across Powergen, Industrial, and Exports

At the heart of the kirloskar oil engines share price narrative are three demand pockets where the company has historically demonstrated execution discipline: powergen, industrial, and exports. In powergen, rising demand for dependable, fuel-efficient engines supports steady order intake as customers seek to modernize and replace aging fleets. The ongoing capex cycle in this segment–backed by engineering teams and a global supplier network–will enable the company to capture a larger share of total addressable market. In industrial, the story hinges on revenue visibility from domestic and international clients who are expanding their manufacturing footprints and investing in automation. A healthy industrial capex cycle translates into a more predictable revenue mix and higher utilization of existing capacity. Exports remain a growth vector, with the company leveraging its engineering capabilities to serve overseas customers and diversify away from a single market. The combination of growth in these segments underpins the revised earnings outlook of FY27 and FY28 and supports the price target embedded in the latest broker note.

From a valuation perspective, the revisited targets reflect the improved visibility around order execution and capex-driven demand growth. The target price of Rs 2,750 sits on a foundation of capacity expansion and a diversification of revenue streams into exports and data-centre-related deployments. The kirloskar oil engines share price could gain if the company sustains its product development cycle–introducing new models and enhancements that improve efficiency and reliability. It is worth noting that the market often prices in such product milestones alongside earnings upgrades, which underscores the importance of monitoring announcements around new product lines and the pace of capex spend.

| Metric | Value |

|---|---|

| Target Price | Rs 2,750 |

| FY27 Earnings Revision | +3% |

| FY28 Earnings Revision | +10% |

| Order Pipeline | Strong; includes hyperscaler win |

The market reaction often hinges on how well the company translates orders into revenue and how efficiently it executes capex. For kirloskar oil engines ltd share price, the key risk is that execution delays or a softer demand environment could temper the upside. But with ongoing capex, a diversified product mix, and a rising sense of demand across powergen and industrial segments, the stock could maintain a constructive trajectory as long as management keeps delivering on the pipeline commitments. For retail investors, this is a narrative worth watching; the next few quarters will be crucial to confirm the pace of order execution and the sustainability of the demand environment.

Hyperscaler Order Win: Its Impact on Kirloskar Oil Engines Ltd Share Price

The hyperscaler order win is a central growth catalyst in the current cycle. While the exact scale of the order isn’t disclosed in the summary, the note emphasizes that the execution will be completed during the current fiscal year. If realized on schedule, such a contract helps de-risk future project pipelines and could act as a proof point for other data centre projects on the horizon. The kirloskar oil engines ltd share price could respond positively to the higher load factor that accompanies a large, high-visibility order and the momentum that such a win often spawns–especially if the company demonstrates steady ramp-up and reliable on-time delivery. Investors should watch for updates on the order’s milestones and any additional orders from related clients in adjacent data centre ecosystems.

In addition, the hyperscaler order underscores the company’s ability to diversify its revenue base and to move beyond traditional, domestic demand drivers. It also highlights the role of capex cycles in creating shared value for customers and suppliers as digital infrastructure expands globally. A successful, timely completion could unlock opportunities in existing and upcoming data centre projects, and would be a meaningful driver for kirloskar oil engines ltd share price in the near term.

Key Risks To Kirloskar Oil Engines Ltd Share Price And How To Manage Them

As with any industrial engine maker, the risk landscape for kirloskar oil engines ltd share price includes a handful of macro and company-specific challenges. The most immediate risk is a slowdown in key end-markets such as powergen or industrial applications, which can translate into softer order intake and lower utilization. While the current demand environment appears supportive, a protracted downturn in capex could compress margins and weigh on earnings growth. Aggressive competition in the engine segment is another risk; new entrants or price competition could erode market share and compress pricing power. Commodity prices–especially steel, aluminum, and other critical inputs–can also spike, threatening margins if the company cannot fully pass costs to customers.

To manage these risks, a disciplined approach to capacity management and cost control is essential. The ongoing capex program should be aligned with a measured ramp-up in production, ensuring that added capacity translates into incremental utilization rather than idle assets. The product development pipeline–if it accelerates, it can introduce differentiated offerings that improve gross margins and create defensible market positions. For retail investors, the key to navigating these risks is to monitor the pace of order execution, the cadence of new product introductions, and the company’s ability to maintain a healthy cash flow position while expanding capacity.

From a portfolio perspective, aligning exposure to kirloskar oil engines ltd share price with your risk tolerance is important. A patient investor could wait for more clarity on the order pipeline execution before making an incremental investment; a risk-tolerant investor might choose to participate in tranches as milestones are achieved and the valuation is revisited by the market. Either way, the evolving demand story across powergen, industrial, and export segments remains the central driver behind the stock’s potential upside.

Frequently Asked Questions

What is Motilal Oswal's revised view on Kirloskar Oil Engines Ltd?

Motilal Oswal reiterates a Buy rating on Kirloskar Oil Engines Ltd, raises FY27 earnings by 3% and FY28 by 10%, and sets a revised target price of Rs 2,750, citing growth triggers across powergen, industrial, and exports and a strong order pipeline.

Which segments support Kirloskar Oil Engines' growth?

Growth is supported by powergen, industrial, and exports, with a hyperscaler order enhancing demand visibility and potential data centre project opportunities.

What is the significance of the hyperscaler order for Kirloskar Oil Engines' share price?

The hyperscaler order provides near-term demand visibility, can de-risk future project pipelines, and may unlock additional data centre project opportunities, positively impacting kirloskar oil engines ltd share price if execution remains timely.

What are the key risks to Kirloskar Oil Engines' share price?

Risks include a slowdown in key segments, aggressive competition, and volatility in commodity prices that could affect margins and earnings.

What should retail investors do next regarding kirloskar oil engines ltd share price?

Retail investors should monitor order execution, capex ramp, and new product introductions while considering scenario planning. They can also use Swastika's Sarthi AI stock assistant for institutional-grade research and to model kirloskar oil engines ltd share price outcomes under different macro scenarios.

Conclusion

Retail investors should view this update as a sign that kirloskar oil engines ltd share price could enter a more navigable phase if execution keeps pace with rising demand expectations in powergen, industrial, and export markets. Motilal Oswal’s revised target price of Rs 2,750, alongside FY27/ FY28 earnings upgrades of 3% and 10%, signals a path to earnings visibility that investors can factor into their time horizons. The hyperscaler order win adds a crucial layer–potentially unlocking future deal flows in data centre projects that could extend the growth runway beyond the base business. In practice, this means the stock may re-rate as investors gain confidence in a clearer revenue trajectory and a manageable risk profile.

Markets Near 24,000 Again: maruti suzuki share price Drives Nifty Momentum For Retail Investors

Key Takeaways

- Nifty opened 0.36% higher, crossing the 24,000 mark; Sensex joined above 77,000.

- Maruti Suzuki share price led gains as autos outperformed while IT remained the laggard.

- Persistent Systems stock crashed nearly 11% to a 52-week low amid Nagarro buyout concerns.

- Dow closed above 52,000; S&P 500 up 1.18%; Nasdaq surged past 2% on favorable global cues.

In a market where every tick matters, the maruti suzuki share price captured investor attention as Nifty opened higher by 0.36% and crossed the 24,000-mark. The Sensex followed suit, crossing the 77,000-level in today’s trade. This session also marks Nifty's weekly expiry and the close of the June quarter, a combination that has historically tested trader nerves and liquidity. The mood leaned on a mix of domestic cues and easing global tensions, helping to keep risk assets buoyant into the session.

As initial data streamed in, Nifty 50 traded up 0.36% to above 24,000, while Sensex gained 0.36% to hover around 77,000. In pre-market trades, Nifty 50 was at 24,057.30, up 0.50%, and Sensex stood at 77,076.05, up about 0.45%. The market’s footing remained tentative but constructive, with Maruti Suzuki share price taking a prominent spot on the gainers board as the autocycle led the rally amid a broader risk-on backdrop.

Monday’s session had seen a pullback: the Sensex fell 372 points and Nifty closed below 23,950, underscoring a consolidation phase that traders are trying to exit. Today’s mood was influenced by easing US-Iran tensions and the prospect of fresh Doha talks, which contributed to a firmer tone for risk assets as the week unfolds.

Maruti suzuki share price And Auto Sector Momentum: What It Signals For Retail Investors

The maruti suzuki share price moved higher as auto stocks outperformed, positioning the auto sector as a potential leader when risk appetite improves. This dynamic matters for retail investors because auto demand often serves as a proxy for consumer sentiment and rural/urban discretionary expenditure. While the IT sector lagged, autos demonstrated relative strength that can help cushion portfolios during choppier times. With technicals showing the 23,900–24,000 zone as a key support and 24,200–24,300 as resistance, the market’s next move could hinge on whether buyers sustain momentum beyond 24,000 and push toward the 24,300 mark, or whether sellers reassert around 24,200–24,300.

The day’s micro-structure also featured Waaree Energies dynamics: it opened at 0.48%, rose to 1.69% to trade around Rs 2,935, and then pulled back to Rs 2,885 by 9:35 am, illustrating intraday volatility that active traders should monitor. In the broader context, the persistent strength in autos contrasted with IT weakness, creating a case study in sector rotation that has become a recurring theme in this phase of the market.

On the macro front, the Dow Jones Industrial Average closed above 52,000 for the first time ever, with the S&P 500 up 1.18% and Nasdaq surging past 2%. Alphabet jumped nearly 5% on its debut as a Dow component (replacing Verizon); Tesla rallied 8.45%. The uplift in U.S. equities contributed to a global risk-on tone, aiding Indian markets in navigating the session’s local catalysts. The broader narrative remains the balancing act between valuation multiples and growth expectations, particularly as investors digest a mix of global liquidity conditions and domestic policy signals.

From a stock-specific lens, the persistent systems stock has been under pressure, crashing nearly 11% in the wake of Nagarro’s buyout deal, which brokerages flagged as pricey in the near term even as long-term rationale remains intact. The Nagarro deal is a reminder that large acquisitions can trigger short-term volatility even when the strategic logic is intact. The aurobindo pharma stock price action, in contrast, reflects company-specific news dynamics that can orient a stock differently from the broader IT or auto themes.

Infosys stock price Trends In The IT Sector: Evidence From The Session

The IT index persisted as the laggard this session, with the infosys stock price and the tcs stock price today moving in negative territory as all constituents traded red. The infosys stock price has retreated toward levels not seen since September 2020, while the tcs stock price today reflected continued softness despite the sector’s long-term growth prospects. The hcl tech stock price also touched multi-year lows, reinforcing the narrative of a structurally challenged IT space in the near term. These dynamics underline how broad market leadership can swing between cyclical and defensive pockets depending on macro and policy signals.

In this context, observing the eicher motors stock price becomes a useful contrarian indicator: Eicher Motors slid on concerns from Delhi’s EV policy 2.0, illustrating how policy risk can separate top-line narratives from micro-price action at the stock level. Meanwhile, the aurobindo pharma stock price movement sits more in line with sector momentum and healthcare-specific catalysts, illustrating the diversity of moves within the market’s breadth.

Tcs stock price today: IT Sector Momentum And Price Action

The day’s price action in the IT space keeps reminding investors that sector leadership can shift quickly. The tcs stock price today trend mirrored that of the broader IT segment: softness in large-cap IT names amid concerns over growth trajectories and margin pressure. The infosys stock price trajectory while weak, must be considered alongside other tech headlines, including new product cycles and potential foreign exchange influences that frequently drive near-term moves. For a retail investor, this means maintaining a balanced IT exposure while leveraging sectors like autos for potential upside when broader risk appetite returns.

Aurobindo pharma stock price And The US Market's Influence

The aurobindo pharma stock price action, in the meantime, benefits from company-specific drivers and a market environment that remains constructive on global risk appetite. The Dow’s run above 52,000, combined with a resilient S&P 500 and Nasdaq, offers a supportive backdrop for Indian pharma and healthcare names that often perform in line with global liquidity. Alphabet’s near-5% one-day surge on its Dow debut and a strong tech rally in the U.S. contribute to a global risk-on tone that can spill over to Indian equities as liquidity conditions remain conducive for cross-border investment activity.

Eicher motors stock price And The Delhi EV Policy 2.0 Impact

The eicher motors stock price moved lower by about 6.5% in response to the Delhi EV policy 2.0, highlighting the policy-sensitive nature of auto names with significant exposure to regulatory shifts. Royal Enfield’s product mix and export dynamics can influence the stock’s trajectory, even as the broader autos space exhibits resilience in certain market segments. This divergence between policy sensitivity and underlying demand underscores the need for careful stock-level due diligence and a robust risk framework for retail traders navigating sectoral winds.

Beyond individual stock stories, the market’s story includes the Vizhinjam Port deal: valued at $2.85 billion, TiL committing $1.4 billion for the stake, with $539 million paid toward initial acquisition of 49% and $858 million allocated for port expansion by December 2028. APSEZ will retain 51% and AVPPL remains a consolidated subsidiary of Adani Ports. Such megadeals show how infrastructure investment themes continue to influence sentiment, particularly for Indian logistics and port equities that stand to gain from expansion plans and regulatory clarity.

On the IPO front, Prism’s updated papers for a Rs 6,650 crore IPO reflect a mix of fresh issue and pre-IPO placement, with the proceeds earmarked to repay borrowings (Rs 4,987.5 crore to repay/prepay borrowings; a Rs 6,650 crore fresh issue and up to Rs 1,330 crore pre-IPO placement). These fund-raising dynamics remind retail investors that capital structure changes in high-growth areas can alter the risk-reward calculus for companies pursuing aggressive expansion strategies.

Frequently Asked Questions

What were the Nifty and Sensex levels near today's opening?

Nifty opened higher by 0.36% and crossed 24,000, with Nifty 50 at 24,057.30 in pre-market trade, up 0.50%. Sensex opened higher by 0.36% and crossed 77,000, with the index around 77,076.05 in pre-market trade.

Which stock led the gains on the Nifty today and what happened to IT?

Maruti Suzuki share price led the gains among Nifty constituents, while the IT sector remained the laggard with all major IT names in red and declines in large-cap names like infosys stock price and tcs stock price today.

What happened to Persistent Systems stock and why is Nagarro involved?

Persistent Systems stock crashed nearly 11% to a 52-week low after Nagarro's €1.27 billion buyout, which brokerages viewed as pricey in the near term even as they backed its long-term logic.

What are the key technical levels to watch for the next session?

The key support is in the 23,900–24,000 zone, with resistance in the 24,200–24,300 band. A breakout beyond 24,300 or a breakdown below 23,900 could set the next directional move.

What global cues supported the market today?

The Dow closed above 52,000 for the first time, with the S&P 500 up 1.18% and Nasdaq up over 2%. Alphabet jumped nearly 5% on its Dow debut, and Tesla rose 8.45%, while easing US-Iran tensions and Doha talks added to the risk-on mood.

What should retail investors do next, and how can Swastika help?

Retail investors should align with price levels around 23,900–24,000 for support and 24,200–24,300 for resistance, while watching sector leadership (autos vs IT). For deeper, AI-assisted stock analysis, Swastika's Sarthi can provide tailored insights aligned with your risk tolerance and horizon.

Conclusion

In a market where price action matters as much as headlines, retail investors should focus on the key levels that tend to govern next moves: keep a close watch on the 23,900–24,000 zone as a critical support and the 24,200–24,300 band as a resistance. The day’s dynamics suggest a bifurcated market where autos show leadership while IT lags, and global cues offer a tailwind that can sustain risk appetite if domestic catalysts align. The practical takeaway is to calibrate exposure to cyclicals when the price action confirms momentum, while maintaining risk discipline to navigate the consolidation that often precedes a more decisive move.

One actionable step for a retail investor is to set price-level alerts around the indicated zones and use a simple risk framework that caps position sizes during choppy sessions. For deeper, institution-level insights and tailored stock analysis–covering maruti suzuki share price and other key tickers–consider Swastika’s Sarthi AI stock assistant, a tool designed to translate complex market signals into practical decisions aligned with your investment horizon.

.jpg)

SBI Funds Management IPO: Complete Guide for Investors in 2026

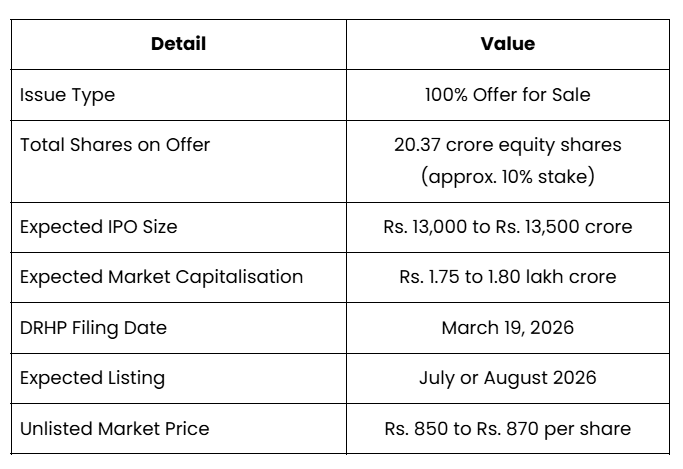

India's largest asset management company is heading to the public markets. SBI Funds Management Limited, the AMC behind SBI Mutual Fund, filed its Draft Red Herring Prospectus with SEBI on March 19, 2026. With an expected fundraise of Rs. 13,000 to Rs. 13,500 crore and a potential market capitalisation approaching Rs. 1.75 to 1.80 lakh crore, this is one of the most significant listings in India's financial services sector this year.

This guide covers everything an investor needs to know before applying, from how the IPO is structured and what the financials look like, to the risks the company itself has disclosed and the factors that will determine whether this IPO makes sense at the offer price.

About SBI Funds Management Company, and Why is This IPO Seeking Investors’ Attention?

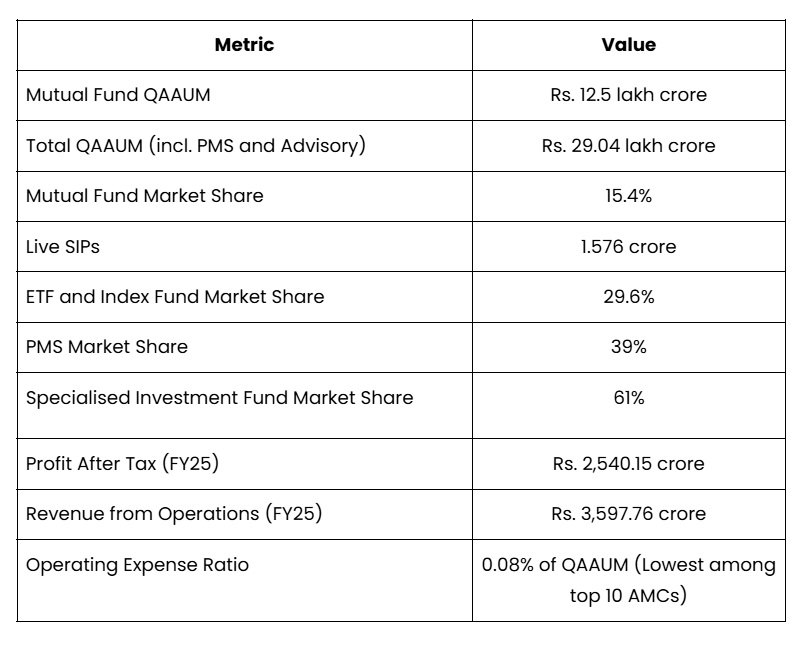

SBI Funds Management is India's largest asset management company, and it is not close. It manages a mutual fund quarterly average AUM of Rs. 12.5 lakh crore with a 15.4% market share as of December 31, 2025. When you include its institutional portfolio management and advisory books, total AUM reaches Rs. 29.04 lakh crore, making it one of the largest asset managers in Asia.

The company leads in two of India's fastest-growing investment categories simultaneously: actively managed mutual funds and passive products like ETFs and index funds. That dual dominance is rare, and it is a key reason this IPO is generating significant institutional and retail interest.

To understand the scale of what is being listed, here is a snapshot of where SBI Funds Management stands today across its key business metrics:

IPO Structure of SBI Funds Management: 100% Offer for Sale

The SBI Funds Management IPO is a 100% Offer for Sale. This is the most important structural fact investors must understand before applying. No new shares are being issued, and SBI Funds Management itself will not receive a single rupee from the IPO proceeds. All the money raised goes directly to the two selling shareholders. Before you apply, here are the core IPO details you need to have in front of you:

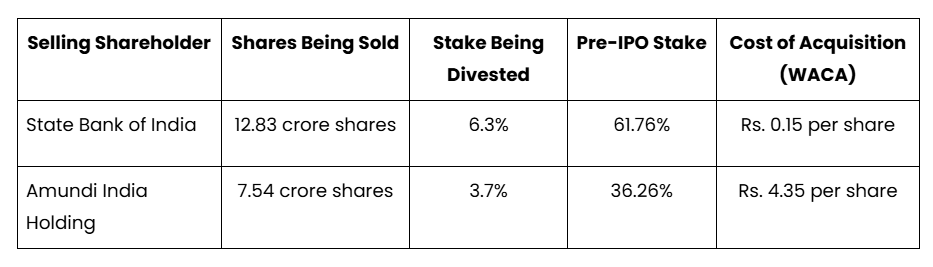

Who is Selling and at What Profit?

Understanding who is selling, how much they paid for their shares, and how much they stand to gain puts the IPO in its proper context. The numbers below tell an important story about where the value creation has already happened.

SBI acquired its stake at effectively Rs. 0.15 per share and Amundi at Rs. 4.35 per share. At an expected valuation of Rs. 1.75 to 1.80 lakh crore, both sellers are realising extraordinary returns on their original investments. IPO investors should assess honestly whether meaningful upside still remains after this re-rating has already occurred.

Revenue, Profit, and Dividends: How Has SBI Funds Management Performed Financially?

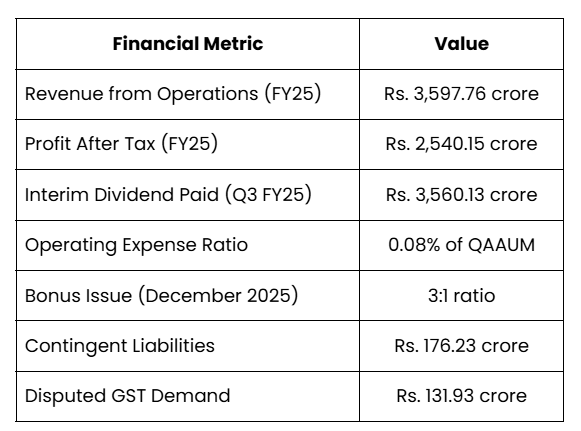

SBI Funds Management is a genuinely profitable and cash-rich business. It reported a profit after tax of Rs. 2,540.15 crore on revenue from operations of Rs. 3,597.76 crore for fiscal 2025. Its operating expense ratio of 0.08% of QAAUM is the lowest among India's top 10 AMCs, a direct result of the cost efficiency that comes with managing assets at this scale.

The dividend number is particularly telling. In just the third quarter of fiscal 2025, the company paid an interim dividend of Rs. 3,560.13 crore to its shareholders. A dividend larger than the full-year profit figure signals two things: the company carries significant retained earnings, and management is confident in the continuity of cash generation. In December 2025, the board also executed a 3:1 bonus share issue, tripling the share count, another signal of financial confidence.

The full financial picture, including contingent liabilities that investors should not overlook, is presented below:

According to CS Setty, Chairman of State Bank of India, speaking at the Citi India 2026 Conference, investors should stop watching daily market movements and start thinking about India as a long-term opportunity. He acknowledged that global geopolitical pressures have made markets choppy but urged investors not to lose sight of the bigger picture, describing India as one of the defining growth stories of this century that has moved well beyond the catch-up phase. 2.

What Makes SBI Funds Management Difficult to Compete With?

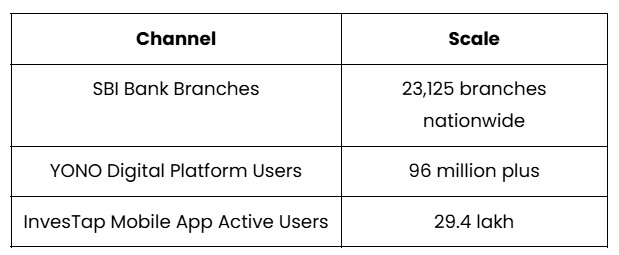

Distribution Through SBI Branches is an Unmatched Advantage

No AMC in India can replicate SBI Funds Management's distribution reach without the backing of a parent like State Bank of India. SBI operates 23,125 branches nationwide, covering urban centres, semi-urban towns, and rural areas that private sector banks and independent distributors rarely penetrate at comparable depth. Alongside this physical network, SBI's YONO digital platform serves over 96 million users, each of whom is a potential mutual fund investor already within the SBI ecosystem.

This is not a passive advantage. Every SBI account holder nudged toward an SIP through a branch visit, a teller recommendation, or a YONO notification adds to an AUM base that compounds over years. Building a comparable network from scratch would take decades and hundreds of thousands of crores. No private competitor can do it.

Amundi Provides the Investment Expertise Behind the Scenes

SBI brings distribution. Amundi brings investment depth. As Europe's largest asset manager, Amundi has embedded its risk management processes, investment frameworks, and product development capabilities into SBI Funds Management over a partnership spanning more than a decade. The stake now held by Amundi India Holding was originally held by Societe Generale S.A. before being transferred in June 2011, reflecting the long-standing and evolving nature of this international collaboration.

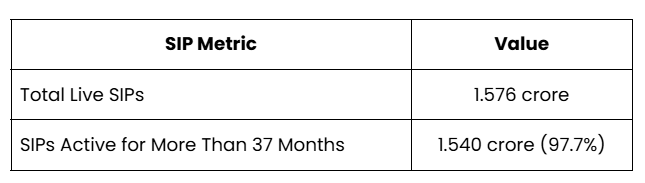

The SIP Book is One of the Stickiest in the Industry

SBI Funds Management runs 1.576 crore live SIPs. What makes this number particularly valuable is not its size but its staying power. The stickiness of this investor base is best captured by looking at how long those SIPs have remained active:

When 97.7% of SIP investors have stayed for more than three years without stopping their plan, it means they have already weathered market corrections and continued investing. For the AMC, this translates into a highly predictable monthly inflow of capital that grows AUM steadily regardless of short-term market sentiment. That predictability is itself a competitive advantage.

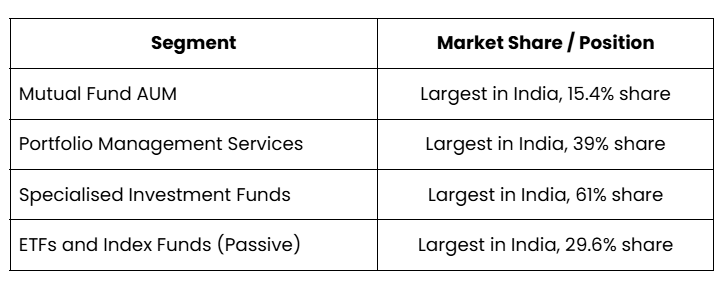

Leadership Across Multiple Business Segments

Most AMCs are dominant in one segment. SBI Funds Management holds the number one position across four separate business lines simultaneously. This breadth of leadership provides revenue diversification that most competitors simply do not have. The four segments and the company's standing in each are as follows:

A Research Engine That Supports Active Management

The company's investment decisions are supported by a research framework covering more than 400 listed companies and more than 200 fixed income issuers. This analytical infrastructure is a genuine entry barrier. Smaller AMCs operating at a fraction of SBIFM's scale simply cannot afford research teams of comparable depth, giving SBIFM a sustainable edge in active fund management quality.

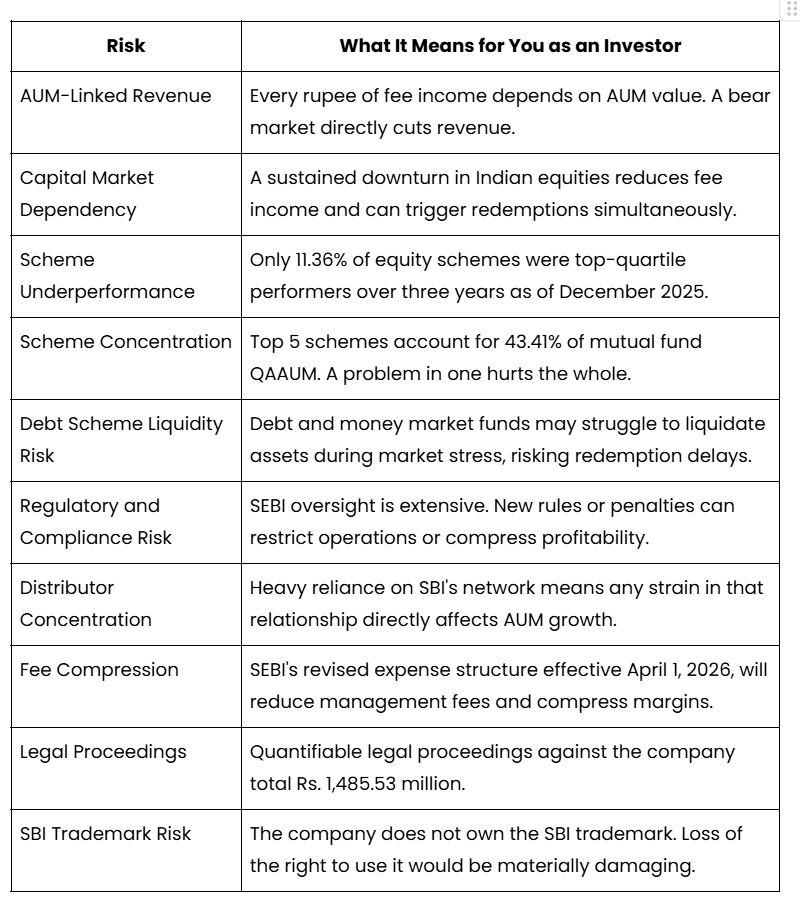

Key Risks: What Has SBI Fund Management Disclosed in Its DRHP That Investors Must Read?

The DRHP for SBI Funds Management is candid about a substantial set of risks, and every investor should read them before applying. These are not hypothetical concerns invented by analysts. They are disclosures made by the company itself under regulatory obligation. Here is what the company has flagged and translated into what each risk actually means for you as a shareholder:

The trademark risk is worth pausing on because it has no easy fix. SBI Funds Management's brand identity, and a significant portion of its ability to attract and retain retail investors, is built around a name it does not legally own. The promoter relationship makes disruption unlikely, but the structural vulnerability is real and cannot be hedged away.

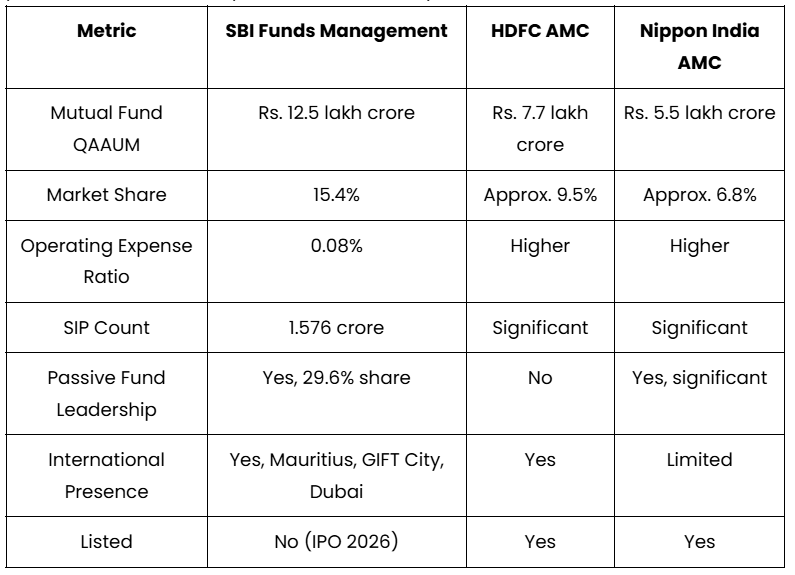

Peer Comparison: How Does SBIFM's Valuation Stack Up Against HDFC AMC and Nippon AMC?

Valuing the SBIFM IPO in isolation is difficult. The most practical approach is to benchmark it against its two closest listed peers, HDFC AMC and Nippon India AMC. This comparison reveals where SBIFM has a clear edge, where it falls short, and what those gaps mean for the multiple it should reasonably command.

The comparison below shows why SBIFM deserves a premium on AUM scale and cost efficiency, but why that premium may be partially offset by lower active equity performance and a compressed blended fee yield:

This comparison matters because HDFC AMC and Nippon India AMC are the reference points the market will use to price SBI Funds Management. SBI's AUM is significantly larger than both, and its cost efficiency is superior. However, its active equity performance metrics lag, and its blended fee yield is lower due to its heavy passive fund exposure. These factors will weigh on the valuation multiple relative to HDFC AMC's historical premium.

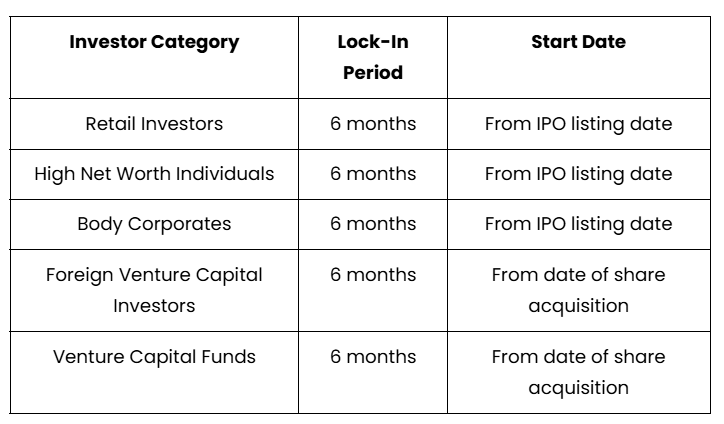

Pre-IPO Lock-In Rules: Can You Sell Your Unlisted Shares After Listing?

If you currently hold pre-IPO unlisted shares of SBI Funds Management, you cannot sell them immediately after the stock lists. SEBI's lock-in regulations determine when you are permitted to exit, and the rules differ depending on what category of investor you are and, in some cases, when you originally bought the shares.

The category-wise lock-in rules are straightforward, but the starting date of the lock-in period differs for institutional investors:

These rules follow SEBI's August 2021 regulatory amendments. With unlisted shares recently trading at Rs. 850 to Rs. 870 per share, investors holding pre-IPO stock should factor in this six-month restriction before making any assumptions about post-listing liquidity or exit timing.

Domestic and Global Reach: How Does SBI Fund Management Distribute and Serve Investors?

Domestic Investor Touchpoints

SBIFM's domestic distribution infrastructure combines physical branch access through SBI with a growing digital presence through its own platforms. The scale of this network is what gives SBIFM a sustainable AUM mobilisation advantage that no standalone private AMC can replicate:

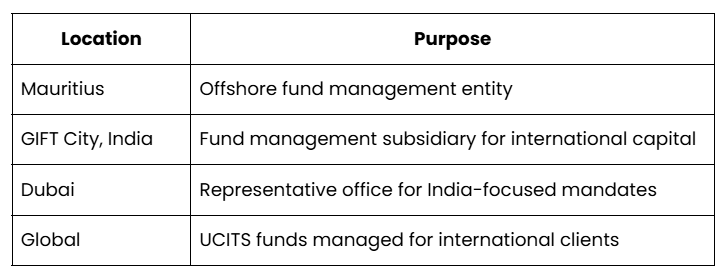

International Investor Access

Beyond India, SBIFM has built a multi-entity international structure to capture demand from global investors seeking India-focused investment products. Each entity serves a specific regulatory or investor purpose in its respective jurisdiction:

Should You Apply for the SBIFM IPO? The Bull Case and the Bear Case

The Bull Case: Why SBIFM Is Worth Owning for the Long Term

SBI Funds Management holds a market position that is structurally protected in ways that most businesses are not. Its SBI branch distribution network is irreplaceable. Its SIP book, with 97.7% of plans active for more than 37 months, delivers a recurring, compounding inflow of capital that cushions revenue even in difficult markets. Its simultaneous leadership across mutual funds, PMS, specialised investment funds, and passive products provides genuine revenue diversification.

For investors who believe in India's long-term financialisation story, SBIFM is one of the most direct and defensible ways to participate. Every new SIP started, every mutual fund account opened, and every ETF unit purchased through its channels strengthens the AUM base that drives fee income. The tailwind is structural and multi-decade in nature.

The Bear Case: What Could Disappoint Investors Post-Listing

The active equity performance gap is the most immediate concern. With only 11.36% of equity schemes in the top performance quartile over three years, SBIFM is not consistently winning on the dimension that matters most to active fund investors. In a maturing market where investors increasingly compare performance data before choosing an AMC, this could pressure active equity AUM retention over time.

SEBI's fee compression effective April 2026 is already confirmed and will reduce management fees across the industry. Given SBIFM's already significant exposure to low-fee passive products, its blended fee yield will come under further pressure even as total AUM continues to grow. Revenue growth will lag AUM growth, and margin expansion will be harder to achieve than historical trends suggest.

Finally, the pure OFS structure means that at the IPO price of Rs. 850 to Rs. 870 in the unlisted market, you are buying at a valuation where both promoters, who acquired shares at Rs. 0.15 and Rs. 4.35 respectively, have already realised the bulk of the value creation. The upside from here depends entirely on future earnings growth and multiple expansion, not on any post-IPO transformation of the business.

Final Verdict: Is the SBIFM IPO a Buy, Hold Off, or Avoid?

SBI Funds Management is a rare business. It is profitable, cash-rich, debt-free, and sits at the centre of India's growing mutual fund industry. The fundamentals are hard to argue with. The only real debate is whether the IPO price leaves enough room for the next investor to make a meaningful return.

If the price band is set reasonably, this is a quality business worth holding for the long term. If it comes at a premium that already prices in years of future growth, patience may serve you better than enthusiasm on listing day.

Either way, this is not a straightforward IPO to evaluate on your own. The OFS structure, SEBI's new fee regulations, the trademark dependency, and the active fund performance gap all carry different implications depending on where you stand financially. What makes sense for one investor may not make sense for another.

That is exactly where a conversation with an expert helps. Swastika Investmart's research team has been closely following the SBI Fund Management IPO since its DRHP filing and can walk you through the valuation, the risks, and the right entry strategy based on your specific goals and portfolio.

Reach out to Swastika Investmart before the subscription window opens. A ten-minute conversation could make a meaningful difference to the decision you take.

Frequently Asked Questions About SBI Fund Management IPO

What is the SBI Funds Management IPO date?

The SBI Funds Management IPO is expected to open for subscription in July or August 2026. The DRHP was filed with SEBI on March 19, 2026, and the listing is targeted for the same calendar year.

What is the price band of the SBI Funds Management IPO?

The official price band for the SBI Funds Management IPO has not yet been announced. Based on unlisted market activity, shares have recently traded between Rs. 850 and Rs. 870, though the IPO price band may be set at a discount to these levels.

What is the GMP of the SBI Funds Management IPO?

Unlisted shares of SBI Funds Management have recently traded between Rs. 850 and Rs. 870 in the grey market, reflecting strong investor interest ahead of the official listing.

What is the issue size and valuation of the SBI Funds Management IPO?

The SBI Funds Management IPO is expected to raise between Rs. 13,000 and Rs. 13,500 crore through a 100% Offer for Sale of approximately 20.37 crore equity shares. The implied market capitalisation is estimated at Rs. 1.75 to 1.80 lakh crore based on current unlisted market prices.

Is the SBI Funds Management IPO a fresh issue or an OFS?

The SBI Funds Management IPO is a 100% Offer for Sale. No new shares are being created, and the company itself will not receive any proceeds from the listing. All funds raised go directly to the selling shareholders, State Bank of India and Amundi India Holding.

Should I invest in the SBI Funds Management IPO?

SBI Funds Management is a fundamentally strong business with consistent profitability, a debt-free balance sheet, and dominant market positions across mutual funds, PMS, and passive funds. Whether the IPO is right for you depends on the final price band, your investment horizon, and your personal financial goals. Consult a SEBI-registered financial advisor before applying.

What are the allotment and listing dates for the SBI Funds Management IPO?

The official allotment and listing dates have not yet been announced. The IPO is expected to list in July or August 2026. Check the Swastika Investmart website for updates as the listing timeline is confirmed.

Kec International Limited Share Price Surges on Rs 1,754 Crore Orders Across T&D and Cables

Key Takeaways

- Rs 1,754 crore orders across T&D and Cables lift near-term visibility.

- Largest-ever tower order from the USA expands global footprint in T&D.

- YTD order intake crosses Rs 4,000 crore, improving revenue visibility.

- Q4 FY2026 profit falls 28.11% YoY to Rs 192.79 crore; revenue down 7.01% to Rs 6,389.75 crore; price action around Rs 539.15 and 4.63% uptick.

KEC International Limited's stock moved higher as fresh order wins spark renewed interest in its growth path. The kec international limited share price ticked higher after the company bagged Rs 1,754 crore in new orders across Transmission & Distribution (T&D) and Cables & Conductors, including the largest-ever tower order from the United States. This signal of momentum comes as YTD order intake crosses Rs 4,000 crore, signaling improved revenue visibility in the coming quarters.

For retail investors tracking Indian infrastructure players, the story is less about a single quarter and more about a rising order book that could translate into higher execution activity in 2026-27 and beyond. KEC International operates across multiple verticals–Power Transmission & Distribution, Civil, Transportation, Renewables, Oil & Gas pipelines, and Cables–providing a diversified exposure to varied infrastructure cycles. The latest win highlights the company's strength in the tower supply business, a core lever for revenue and margin recognition in the long cycle of EPC projects.

Kec international limited share price reaction to Rs 1,754 crore orders in T&D and Cables

The market interpretation of these orders is that KEC's execution structure and project management capabilities are aligned to capture larger deals, particularly in the Americas. The Transmission & Distribution towers segment has historically been a major portion of the order mix, and this latest order underscores the robustness of demand in the American T&D market. In the near term, investors will watch for how quickly the company can convert these orders into revenue and how margins hold up across the larger project pipeline. The new wins also reflect ongoing diversification away from a region-heavy mix toward a more balanced global footprint.

Vimal Kejriwal, MD & CEO, emphasised the strategic importance of the tower business, noting that repeat orders from customers in the Americas, including the US, signal momentum in this market. With these orders, the YTD order intake stands at over Rs 4,000 crore. This contextual backdrop matters because a growing order book is typically a precursor to revenue visibility and potential margin leverage, especially for a capital-intensive, EPC player like KEC International.

How the Rs 1,754 crore orders impact kec international orders backlog and revenue visibility

Beyond the headline number, the deal mix underlines a few practical implications. The total order backlog is extended, and there is renewed optimism around the conversion of orders into revenue in the quarters ahead. The company has a multi-vertical footprint across T&D, Cables, and other infrastructure EPC segments, which can provide revenue diversification during global capex cycles. The new orders align with the company’s stated strategic focus on strengthening its tower sales business globally, which should bolster the consistency of cash flows in the medium term.

In terms of geography, the United States remains a critical growth market for towers–a sector where KEC International has been steadily expanding its presence. The combination of domestic and international projects across the T&D and cable segments reduces reliance on any single region, providing a more resilient order book. The immediate takeaway for investors is that a stronger order book can translate into better revenue visibility and potentially higher execution efficiency as KEC scales up its tower supply operations.

Kec international quarterly results: dissecting Q4 FY2026 performance vs orders

Turning to the quarterly numbers, KEC International reported a consolidated net profit of Rs 192.79 crore for the quarter ended 31 March 2026, down 28.11% from Rs 268.19 crore in the corresponding quarter last year. Revenue from operations declined 7.01% year-on-year to Rs 6,389.75 crore. The results reflect the ongoing pressures from project mix and execution cycles even as the company benefits from order wins across its T&D and cables verticals. The juxtaposition of rising order intake with softer quarterly profits highlights the risk-reward balance for investors: execution pulse can improve with a larger backlog, but near-term profitability may be pressured by project mix, commodity costs, and currency movements.

From a valuation perspective, the stock price action around Rs 539.15 reflects a positive near-term mood on the order wins, though investors must weigh the longer cycle nature of EPC projects and potential margin volatility. The company’s presence across international markets, coupled with the existing order book, suggests that revenue visibility could improve over the next few quarters if execution stays on track and capital expenditure cycles globally stabilize.

Current kec international stock price and momentum: what retail investors should watch

As of now, the stock price stands around Rs 539.15, with the day showing a 4.63% rise. Price momentum is likely to be influenced by the pace at which new orders translate into revenue and the company’s ability to manage margins amidst the inflationary environment and currency headwinds. For retail investors, the key questions are: how sustainable is this momentum beyond a single set of orders, and what is the trajectory for the order book over the next two to four quarters? In this context, tracking the quarterly results and the management’s commentary on cost control and margin protection will be important. From a risk perspective, execution delays and client concentration in certain geographies could temper upside if not managed well. In the interim, a more diversified project pipeline can help cushion potential volatility in the short run.

For those seeking deeper, institutional-level research on KEC International, Swastika's Sarthi AI stock assistant can help you compare the company’s order book growth, segment mix, and market-specific opportunities across geographies. This tool can be a practical complement to traditional disclosures, particularly for retail investors evaluating long-term growth trajectories.

Geographic and segment mix: Americas growth boosts T&D and Cables across markets

The company’s footprint spans power transmission & distribution, civil, transportation, renewables, oil & gas pipelines, and cables. The latest orders reinforce a broader strategy of expanding the tower sales business globally, especially in the Americas, while continuing to win cables and other EPC projects in India and international markets. The USA’s demand for high-voltage transmission infrastructure aligns well with KEC International’s capability to supply towers and related components to major utilities and developers. In India, domestic infrastructure spending, including power transmission expansion, remains a meaningful growth anchor, while the presence in renewables and oil & gas projects adds optionality in the longer term.

From an investment perspective, observers will be watching for how the company manages working capital and project execution across its diversified project portfolio. The margin profile across T&D towers and cables may diverge, given the different capital intensity and supply chain considerations. Yet, the broad-based footprint reduces geographic risk, and a solid order book provides a cushion against a softer quarter here or there. Investors should also track macro factors such as currency movements, commodity prices, and interest rates, which can influence project costs and profitability.

Frequently Asked Questions

What is the Rs 1,754 crore order and which segments does it cover?

The Rs 1,754 crore order wins span Transmission & Distribution (T&D) and Cables & Conductors, including a large tower supply order in the United States, marking a significant uplift in the company's order book.

What is the YTD order intake for KEC International?

The year-to-date order intake stands at over Rs 4,000 crore, signaling momentum in the company’s global T&D and cables businesses.

What were KEC International's Q4 FY2026 results?

In the quarter ended 31 March 2026, the consolidated net profit declined 28.11% year-on-year to Rs 192.79 crore, while revenue from operations fell 7.01% to Rs 6,389.75 crore.

What is the current kec international stock price and its movement?

The current price is Rs 539.15, with the stock moving up about 4.63% on the day.

What is the strategic significance of the US tower order for KEC International?

The largest-ever tower order from the USA underscores momentum in the American T&D market and strengthens KEC's global tower sales strategy, potentially enhancing revenue visibility and diversification.

Conclusion

In the near term, KEC International’s Rs 1,754 crore order win across T&D and Cables strengthens revenue visibility and signals a strategic shift toward a more diversified, global tower sales footprint. The resulting movement in the kec international share price reflects investor optimism about the company’s ability to monetize a growing order book, particularly in the Americas. However, the quarter ended 31 March 2026 showed a profit decline, underscoring the caution investors must exercise regarding margin trajectory and execution risk as projects scale up.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App