ONGC Share Price: Live Update, Key Levels, And Retail Investor Takeaways

Key Takeaways

- The ognc share price hovered around Rs 248–252 in today's session, signaling cautious bullish momentum.

- Key resistance near Rs 251.45 (R2) and a current price around Rs 252 indicate a breakout attempt.

- P/E stood at 7.55 with EPS of 32.93, alongside a volume of 6,174,102 and a market cap of 312,657.68.

- Six-month beta of 1.0172 suggests price moves closely track market swings.

When energy demand drives policy and markets, a single stock ticker can reveal a larger story. The ognc share price has moved within a tight range as investors weigh supply dynamics, policy cues, and global energy volatility. For a retail investor, this isn't just a price tag–it's a signal about value, risk and timing. The monthly search volume for 'ongc share price' sits around 673,000, underscoring how many traders are chasing this data daily.

Ongc Share Price Live Update And What It Signals For Traders

The latest live data shows the ONGC share price around Rs 248.5 during the session, following a day where it settled at 244.96 in the previous close. As of 11:31:58 AM IST on 14 Jul 2026, the price was 248.5, with intraday moves mirroring a modest uptick for the day. Intraday data points like these help traders gauge momentum in a stock that has traded within a tight band recently.

Key intraday figures from the same feed include:

- Last traded price: 247.63

- Volume: 6,174,102

- Market capitalization: 312657.68

- P/E: 7.55

- EPS: 32.93

For readers seeking deeper context, consider the broader picture: a stock price hovering near resistance and above short-term averages can signal a potential breakout if sustained with volume. Swastika's Sarthi AI stock assistant can help you analyze the stock at a granular level and integrate it with your portfolio strategy.

Ongc Share Price Vs Fundamentals: P/E, EPS, And Market Cap Insights

Even as the price flickers in a narrow band, the fundamental picture remains relevant. The ONGC P/E ratio is 7.55 and earnings per share stands at 32.93, suggesting the stock trades at a modest multiple relative to earnings. With a volume of 6,174,102 shares, market cap sits at 312657.68, underscoring ONGC's standing as a large-cap energy player.

Three-month performance has shown a decline of -12.95%, while the monthly return is a positive 0.91% and the weekly return climbs 1.87%. The six-month beta is 1.0172, indicating that the stock tends to move with the broader market rather than in isolation. In this context, investors should weigh the stock's earnings power against its price multiple to gauge the marginal upside.

Ongc Historical Share Price Trends And Key Technical Levels

The ONGC historical share price shows resilience within a defined range. The stock closed the previous session at Rs 244.96, rising 1.42% the day before. Current technical overlays show the price trading at Rs 252.0 and sitting just above its second resistance level (R2) at Rs 251.45, which suggests a cautious breakout scenario if followed by sustained volume.

Short-term technicals include a 3-day simple moving average (SMA) of Rs 247.54 and a 5-day exponential moving average (EMA) of Rs 245.49, both providing context for near-term drift. The six-month beta of 1.0172 confirms a market-correlated path rather than heavy volatility. In the last four weeks, ONGC has seen a monthly return of 0.91% and a weekly return of 1.87%, reinforcing a slow but positive trend as the price tests resistance.

Ongc Dividend Outlook And The Role Of Its Share Price In A Diversified Portfolio

Dividend considerations (ongc dividend) are a common lens through which investors view value and cash return. The provided market data does not include explicit dividend figures, but investors typically factor dividend yields alongside the price-to-earnings picture. When bonds of energy policy and capital expenditure align, the stock's price action can reflect the potential for favorable distributions, though investors should confirm the latest dividend announcements from the company and exchange filings.

In a diversified portfolio, the ONGC share price can offer exposure to the energy sector's cycle, especially for investors seeking index-like exposure with a value tilt. The stock's price movements–coupled with its stable P/E and moderate EPS–can complement more cyclical bets in a broader asset mix.

Ongc Market Cap And Growth Potential: What Retail Investors Should Consider

From a market-cap perspective, ONGC shows a capitalization figure of 312657.68 in the data. The stock's six-month beta is 1.0172, consistent with a broader-market orientation rather than extreme volatility. The price movement over the last three months is -12.95%, but the month and weekly gains (0.91% and 1.87%, respectively) imply a potential stabilization or gradual recovery depending on oil and gas demand cycles and policy signals. With the price around Rs 252 and key resistance near Rs 251.45, traders should watch for a sustained move above R2 on higher volumes to confirm a breakout rather than a whipsaw pullback.

For retail investors, the takeaway is to balance value, growth prospects, and risk. If the stock clears Rs 252 with rising volume, it may indicate a shifting momentum; if it breaks below recent support near Rs 244 with increased volume, it could set the scene for a retracement toward the 3-day SMA and 5-day EMA. Always align entry and exit decisions with a well-defined risk plan and consider external catalysts such as policy shifts or energy demand trends. For deeper, stock-level insight, use Swastika's Sarthi AI stock assistant.

Ongc Stock Price And Sector Outlook: How Oil And Gas Trends Influence The Price

The ONGC stock price is not just a price; It sits inside the energy value chain. When crude oil trades higher, upstream players like ONGC often see strengthening sentiment, as evidenced by the price range around Rs 244–252 in recent sessions. The sector's growth is shaped by domestic demand, capex cycles in energy infrastructure, and global supply dynamics. For retail investors, tracking sector indices and oil price trends alongside ONGC share price can provide a composite view of risk and opportunity.

Given the price action and technical overlays (R2, SMA, EMA), a break above Rs 252 with volume could indicate momentum that extends beyond the stock's current range, while a move below Rs 244 could trigger consolidation. The stock's six-month beta of 1.0172 also implies that macro-market movements carry a meaningful influence on the price. Investors should maintain a diversified approach and use Sarthi to model sector-specific scenarios in their portfolios.

Related Reads

Frequently Asked Questions

What is the current ognc share price as observed in the latest update?

As of the latest feed, the ongc share price was around Rs 247.63 to Rs 248.5 intraday, with an 11:31:58 AM IST reading at 248.5 in one update. Intraday moves show modest upticks in the session.

What are ONGC's valuation and earnings metrics from the data?

The stock carries a P/E of 7.55 and an EPS of 32.93, with a reported volume of 6,174,102 shares and a market capitalization of 312657.68.

What are the key technical levels for ongc share price today?

The price is testing resistance around Rs 251.45 (R2) with the current price around Rs 252.0, while 3-day SMA sits at Rs 247.54 and 5-day EMA at Rs 245.49.

What does the six-month beta say about ONGC's risk relative to the market?

The six-month beta is 1.0172, indicating ONGC's price moves are roughly in line with the broader market rather than showing elevated idiosyncratic risk.

Where can I get deeper stock-level analysis for ONGC?

You can access in-depth, stock-level analysis with Swastika's Sarthi AI stock assistant:Swastika's Sarthi AI stock assistant.

Conclusion

For the retail investor, the current ONGC share price snapshot suggests a stock trading near a critical inflection point. The price is testing resistance around Rs 251.45 and could break higher if volume confirms the move; otherwise, a consolidation near 244–248 remains plausible. A practical mental model is to treat the stock like a ladder: look for the price to clear the resistance with rising volume, otherwise wait for a pullback to key moving averages around 245–248 before considering a position. Use the Sarthi AI stock assistant to run deeper stock-level scenarios and integrate ONGC into a broader energy exposure in your portfolio.

In practice, this means you could set defined rules: a breakout above Rs 252 on strong volume as a potential buy signal for a tactical trade, and a pullback toward the 3-day SMA around 247.54 or the 5-day EMA around 245.49 as a potential longer-term entry. Always pair price action with risk controls, such as stop-loss levels and position sizing, to ensure you remain aligned with your overall plan. Swastika's Sarthi AI stock assistant can help crystallize these rules into actionable steps for your portfolio.

Open your trading and demat account here

Reference :

1 : Economictimes

Latest Articles

Syrma SGS Stock Price Outlook: HSBC Buy Rating, Rs 1,750 Target And India EMS Growth

Key Takeaways

- HSBC initiates Syrma SGS with a Buy rating and a Rs 1,750 target, signaling upside from Rs 1,370 close.

- The Street's average target sits at Rs 1,310.86, implying about 4.1% downside to consensus.

- HSBC projects EPS growth of about 34% over the next three years, with Sales CAGR 32%, EBITDA 33%, and Net Profit 35%.

- India EMS growth is robust, with a 27% CAGR 2024-2029 and Syrma SGS positioned to capture a significant portion of a $320B incremental global opportunity, aided by policy incentives.

Investors tracking syrma sgs stock price will notice a fresh catalyst shaping Syrma SGS Technology Ltd.'s growth narrative. HSBC has initiated coverage with a Buy rating and aRs 1,750 target, signaling a potential re-rating as the stock price and the company’s earnings trajectory align with a broader push in domestic electronics manufacturing. The implied upside from the July 8 close of Rs 1,370 is about 27%, a figure that cements Syrma SGS as a stock to watch for those following the India EMS story. While the Street’s consensus target sits around Rs 1,310.86, implying roughly a 4.1% downside to that average, HSBC’s thesis pivots on a higher-quality growth path that could outpace peers over the coming years.

In this analysis, we unpack what the HSBC initiation means for retail investors, how the growth assumptions stack up against the industry backdrop, and what conclusions you can draw for your own portfolios. We explore the drivers HSBC highlights, the structural tailwinds in India’s EMS landscape, and the risks that could temper optimism. The goal is to translate a broker note into actionable takeaways for a retail audience that relies on disciplined thinking and scenario planning. For deeper number-crunching and scenario modeling, you can use Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Syrma SGS Stock Price Outlook After HSBC Buy Rating

HSBC describes Syrma SGS as one of India’s leading EMS companies with a diversified customer base and deep Original Design Manufacturing (ODM) capabilities. The bank emphasizes a strategic transition–from simply assembling PCBs for IT and consumer electronics to manufacturing the boards themselves–reflecting a shift toward higher-value, integrated electronics manufacturing. The Rs 1,750 target price implies about 27% upside from the July 8 closing price of Rs 1,370, with the note suggesting the target sits near the upper end of Street expectations. In practical terms, this implies a re-rating on earnings visibility and a stronger growth profile rather than a mere multiple expansion.

From a valuation perspective, the Rs 1,750 target translates into a two-year forward P/E of roughly 53x and a PEG of about 1.5x. HSBC projects earnings per share (EPS) to compound at around 34% over the next three years, supported by a sales CAGR of 32%, EBITDA CAGR of 33%, and net profit CAGR of 35% (FY26–FY29). The growth is pegged to multiple catalysts: robust demand in autos and industrials, a higher export mix, strong engineering capabilities, favorable product mix, and vertical integration that enhances value capture. Taken together, these elements form the backbone of the growth thesis behind Syrma SGS stock price under HSBC’s framework.

Beyond the company-specific drivers, policy and macro tailwinds are embedded in HSBC’s thesis. India’s EMS space is forecast to grow at about 27% CAGR from 2024 to 2029, a rate that aligns with the broader push toward domestic manufacturing and supply-chain localization. The opportunity in EMS is substantial: the sector could capture around 32% of a $320 billion incremental global opportunity during 2024–2029. Government incentives for manufacturing and the proposed India Semiconductor Mission 2.0–potentially supported by a $13 billion allocation–could further accelerate capacity expansion and technology adoption. In this context, Syrma SGS’s value proposition–complex board manufacturing, engineering depth, and a diversified customer base–appears well-positioned to leverage these macro trends.

From an investor’s lens, the valuation narrative hinges on execution as much as growth potential. HSBC’s emphasis on a sharp expansion in earnings power means investors should watch for evidence of margin stabilization and scale in capacity. The company’s existing trajectory suggests delivering above-market growth, but the degree to which capacity additions translate into higher utilization and pricing power will determine how closely Syrma SGS stock price tracks the Rs 1,750 pathway. A practical takeaway for readers is to track quarterly order flow and plant ramp timelines as real-world signals of the pace at which the growth thesis could unfold.

India EMS Industry Growth And Syrma SGS's Position

In HSBC’s framing, Syrma SGS sits among India’s leading EMS players with a diversified client base and a strong emphasis on engineering-driven manufacturing. This position is important because it underpins the company’s ability to win complex, high-value contracts that can withstand price competition in lower-margin assembly work. The move from PCB assembly toward full board manufacturing aligns with global value-chain shifts where OEMs seek closer, more integrated suppliers in regionalized markets. The context is critical: India currently imports roughly 90% of its PCB demand, creating a substantial domestic opportunity for EMS players that can scale and deliver reliable supply chains.

Growth drivers highlighted by HSBC include sustained demand from autos and industrials, a high export mix, and strong engineering competencies. Product mix improvements and vertical integration are expected to lift value capture, supporting stronger margins and earnings resilience amid cyclical demand. The broader EMS industry in India is expected to grow at a 27% CAGR from 2024 to 2029, a backdrop that enhances Syrma SGS’s ability to capture incremental demand within the domestic market. These dynamics dovetail with the global opportunity: EMS is projected to capture about 32% of the $320 billion incremental global opportunity during 2024–2029, a figure that underscores the scale of potential upside for players like Syrma SGS if execution matches the thesis.

On the policy side, manufacturing incentives and the India Semiconductor Mission 2.0 proposal–with a potential $13 billion allocation–could catalyze investment in local electronics manufacturing capacity. For Syrma SGS, this means more domestic demand, faster scale-up, and greater competition for high-margin projects. The synergy between policy support and a domestic EMS capability is a critical variable that could influence the stock’s trajectory, particularly if Syrma SGS demonstrates disciplined capex management and timely plant commissioning. Investors should monitor policy announcements and the pace of subsidy disbursements as part of their scenario planning for Syrma SGS stock price.

Another facet of the EMS opportunity is the structural transition toward vertical integration. By moving beyond PCB assembly into more complete board manufacturing and contributing to the design process, Syrma SGS can differentiate itself from peers that remain in lower-margin assembly work. That differentiation matters for valuation, because it expands addressable margin and strengthens pricing power with customers who seek integrated suppliers. For retail investors, the lesson is to consider where Syrma SGS stands on the value ladder: does the company’s product and service stack align with higher-margin, longer-tenure contracts that can sustain earnings growth through cyclical downturns?

Valuation And What The Rs 1,750 Target Means For Syrma SGS Stock Price

The Rs 1,750 target is a clear signal of HSBC’s confidence in Syrma SGS’s ability to convert growth into earnings power. The target implies a strong re-rating potential, anchored by a two-year forward P/E of roughly 53x and a PEG near 1.5x. HSBC projects that earnings per share will compound at about 34% over the next three years, supported by a 32% sales CAGR, 33% EBITDA CAGR, and 35% net profit CAGR between FY26 and FY29. These are ambitious figures, but they are anchored in a favorable mix shift toward higher-margin, high-automation electronics manufacturing and a growing domestic market that favors localized suppliers.

In parallel, the Street’s average target of Rs 1,310.86 paints a more conservative view, implying roughly a 4.1% downside to consensus. The divergence between HSBC’s 1,750 target and the broader Street average highlights the differing views on execution risk, margin trajectory, and the pace of capacity expansion. For retail investors, this means it’s prudent to view Syrma SGS stock price through a spectrum of scenarios rather than relying on a single forecast. A robust framework would contrast upside cases driven by accelerated capacity ramp and favorable product mix with downside scenarios where plant commissioning faces delays or macro demand softens.

The valuation snapshot also suggests a balance between earnings growth and multiple expansion. If Syrma SGS can deliver sustained top-line growth and translate it into resilient margins, the higher multiple could be justified. However, if utilization remains below plan or if competitive intensity grows in MSAs (manufacturing services agreements), the stock could face multiple contraction even as earnings grow. In either case, the key is to anchor decisions in tangible milestones–order intake, plant commissioning progress, and profitability trends–rather than relying solely on consensus targets or headlines.

Risks To Syrma SGS Stock Price: What Could Stop The Rally?

Every growth narrative has its risks. For Syrma SGS, one primary risk is competition in low-margin assembly. If price competition intensifies or if customers migrate to other suppliers with lower cost structures, margins in the core assembly business could come under pressure. Geopolitical factors that affect exports–such as tariffs, trade restrictions, or disruptions in key markets–could also weigh on the pace of revenue growth and the ability to sustain a favorable export mix. Additionally, delays in commissioning new plants could constrain capacity expansion and cap the upside by creating a mismatch between demand and supply. These factors can lead to volatility in Syrma SGS stock price as investors reassess the timeline for achieving the envisioned scale and profitability.

Other risks to monitor include the pace of policy implementation around manufacturing incentives and semiconductor missions. While these policies provide tailwinds, the actual disbursement of subsidies and the speed at which domestic capacity comes online can influence the feasibility of the growth plan. If subsidies lag or if supply chain constraints persist, Syrma SGS could encounter headwinds that affect both top-line growth and margin expansion. In short, the story remains conditional on execution, policy implementation, and external macro dynamics that influence demand in autos and industrials across India and export markets.

Practical Takeaways For Retail Investors: A Simple Mental Model

The growth thesis combines several favorable pieces: a rising EMS demand in India, a push toward domestic manufacturing, and Syrma SGS’s movement up the value chain. A practical mental model for evaluating Syrma SGS stock price is to view it as a function of three linked variables: demand expansion, capacity expansion, and earnings visibility. If demand from autos and industrials remains robust, and the company can meaningfully increase utilization through timely plant commissioning, earnings growth should translate into a higher-quality multiple rather than a purely multiple-driven rally. This is where policy tailwinds and the shift to domestically manufactured components come into play, potentially supporting a more favorable earnings trajectory than the market currently prices in.

Frequently Asked Questions

What is the HSBC target price for Syrma SGS Stock Price?

HSBC initiated coverage with a Buy rating and a Rs 1,750 target price.

What is the implied upside from the July 8 closing price for Syrma SGS?

About 27% upside from Rs 1,370 close.

What are HSBC's growth projections for Syrma SGS from FY26 to FY29?

Sales CAGR 32%, EBITDA CAGR 33%, and net profit CAGR 35%.

What are the key risks for Syrma SGS stock price raised by the note?

Competition in low-margin assembly; geopolitical factors affecting exports; delays in commissioning new plants.

What is the Indian EMS market outlook and Syrma SGS's potential share of global opportunity?

The EMS industry is projected to grow 27% CAGR from 2024 to 2029, with EMS potentially capturing about 32% of a $320 billion incremental global opportunity.

What incentives support Syrma SGS's growth trajectory?

Manufacturing incentives and a proposed $13 billion allocation for India Semiconductor Mission 2.0.

Conclusion

In the near term, the HSBC Buy rating and Rs 1,750 target establish a growth-driven framework for Syrma SGS stock price that aligns with India’s EMS expansion and the company’s strategic move up the value chain. The combination of strong earnings growth potential and favorable policy tailwinds creates a compelling backdrop for investors who emphasize growth quality and execution risk management. The key is to translate this narrative into a disciplined investment plan that accounts for capacity ramp timelines, utilization levels, and the volatility that can accompany rapid expansion.

Open your trading and demat account here

Reference :

1 : Ndtvprofit

Eternal Share Price Outlook: Motilal Oswal's Rs 380 Target And Multi-Business Growth

Key Takeaways

- Motilal Oswal's Rs 380 target on Eternal hinges on a SOTP view for Food Delivery and a DCF for Blinkit.

- eternal food delivery, eternal quick commerce, and District form the three growth pillars driving the upside.

- FD accelerates for the third straight quarter, aided by curated affordable meals under INR 250; GOV growth is robust and EBITDA margins improve.

- The target implies roughly 34% upside to the current eternal share price as the execution improves.

eternal share price sits at a pivotal moment as three growth engines–eternal food delivery, eternal quick commerce, and District–move in tandem with a rapidly evolving Indian consumer. A broker note places Eternal on a Buy, with a target price of Rs 380, supported by a hybrid valuation: Food Delivery is valued on a 35x FY28E EV/EBITDA multiple while Blinkit is priced through a discounted cash flow (DCF) model. This is not a single-story stock; it is a composite bet on a market where convenience, delivery efficiency, and dining choices are reshaping everyday consumer behavior. For retail investors, the message is clear: the eternal share price could re-rate as momentum builds across all three segments over the next 12–24 months.

The Rs 380 target implies roughly a 34% upside from the current level, according to the broker's framework that values a Food Delivery business at 35x FY28E EV/EBITDA and uses a DCF approach for Blinkit. The note identifies three core pillars–eternal food delivery, eternal quick commerce, and District–and argues that each can contribute to volume and margin expansion. It also notes that eternal food delivery is seen as a stable duopoly, while the quick commerce unit continues to scale despite intensifying competition. District, though nascent, is highlighted as a potential long-run growth trigger as the company experiments with experiences that blend dining, social interaction, and convenience.

From a growth perspective, the three-business framework matters because it diversifies risk and creates multiple catalysts. The FD segment (eternal food delivery) is reported to have accelerated for the third consecutive quarter, supported by targeted activation of budget-conscious customers and curated affordable meals–meals under INR 250–that broaden the addressable market. NAOV has moderated, but higher order frequency and new customer additions are driving volume growth. In short, the core food-delivery engine is showing resilience even as the competitive intensity in the sector remains high. The quick commerce arm (eternal quick commerce) is scaling and expanding reach, while District remains a nascent but potential upside lever as the company tests formats that could convert casual diners into repeat patrons.

Motilal Oswal's growth outlook also rests on explicit financials: they expect GOV growth of 21.5% YoY in 1QFY27E and an EBITDA margin of 5.0% for that period. The emphasis on a steady margin profile acknowledges that the FD business, while growth-heavy, still operates in a low-to-moderate margin environment, particularly as customer acquisition and delivery costs evolve. For investors tracking the eternal stock, these margins are as important as the top-line trajectory because they underpin the quality of earnings and the resilience of free cash flow–critical inputs for valuation models that hinge on future cash flows and multiple expansion. When you scan the operator's three-pillars framework, the question isn't whether each business can grow, but whether the aggregate effect translates into a durable earnings trajectory that justifies the Rs 380 price target.

For those evaluating the investment narrative, a practical takeaway is to view Eternal not as a single product company, but as a triad of growth levers that can potentially compensate for cyclicality in any one segment. The valuation framework–SOTP for Food Delivery and a DCF for Blinkit–helps explain how the broker arrives at a target that may imply meaningful upside from current Eternal share price levels. Investors should also consider the speed at which Blinkit stock price and other market variables respond to the evolving regulatory, competitive, and consumer-dynamics landscape in India. The brokerage note’s framework suggests continued emphasis on unit economics and user growth, rather than a rapid jump in margins–at least in the near term–which aligns with the steps Eternal is taking to broaden its affordable meal offerings and to optimize its delivery network for efficiency.

As a retail investor, you should balance the upside catalysts with execution risk, competitive intensity, and the precise timing of market re-rating. To help you dig deeper, consider Swastika's Sarthi AI stock assistant for a structured, institution-grade view of Eternal's three-business model and the associated valuation drivers. Swastika's Sarthi AI stock assistant is designed to provide independent analysis across multiple scenarios and alternative assumptions, helping you stress-test the Rs 380 target under different growth paths.

Eternal Share Price Outlook: Motilal Oswal's Rs 380 Target Across Three Growth Pillars

In the broker’s frame, Eternal is a multi-segment platform that blends a robust food-delivery core with a fast-growing quick-commerce extension and a nascent District initiative. The target price of Rs 380 is anchored by a SOTP approach for Food Delivery, which assigns a high multiple to the segment on the basis of its scale, density of demand, and the potential for loyalty-driven repeat purchases. Blinkit, by contrast, is valued via a discounted cash flow model that captures long-horizon cash generation from a high-frequency, convenience-focused platform that complements the FD business. Taken together, the sum of these values supports upside potential to the Eternal share price if execution remains on track and if the market continues to reward scalable, cash-generative growth across consumer services.

The three growth pillars–eternal food delivery, eternal quick commerce, and District–are not identical in risk or maturity, but each contributes to the overall earnings trajectory. The FD segment provides near-term revenue visibility and operating leverage, helped by the company’s focus on meals under INR 250 and targeted marketing that converts budget-conscious diners into repeat customers. The quick-commerce unit adds a second growth vector by expanding assortment breadth and reducing delivery times, while the District initiative represents a longer-term bet on out-of-home experiences that could become new monetization channels as consumer dining patterns evolve.

Three Growth Engines Behind Eternal: Eternal Food Delivery, Eternal Quick Commerce, And District

eternal food delivery, as a core operation, has shown resilience amid competitive pressure. The brokerage note emphasizes the potential for sustainable 18–20% growth in the FD business over the medium term, a projection grounded in volume expansion, customer retention, and improved unit economics as delivery logistics mature. This growth is pivotal because it strengthens the top-line contribution of the FD engine while also supporting margin expansion in the longer run as the network scales. For a stock like Eternal, where the FD business is the anchor, this growth cadence matters because it shapes how aggressively investors value the rest of the portfolio.

eternal quick commerce continues to scale despite intensifying competition. The note highlights that Blinkit’s growth trajectory remains favorable, supported by higher order frequency and a steady influx of new customers. The presence of a wide delivery radius, faster delivery times, and curated product assortments are essential to maintaining this momentum as consumer expectations for speed and convenience rise. District, the nascent going-out venture, is described as a potential upside lever: while early-stage, the concept could unlock cross-sell opportunities and experiential formats that drive incremental visits and higher ticket sizes over time. Taken together, the three engines offer a diversified growth path that can adapt to shifting consumer preferences and regulatory dynamics.

FD Momentum And Budget Meals Under INR 250

The FD momentum is a central theme in the Eternal growth narrative. The third consecutive quarterly acceleration signals that targeted activations of budget-conscious customers and curated meals under INR 250 are resonating with price-sensitive households. This strategy expands the addressable market and helps stabilize the volume trajectory even if overall consumer spending faces macro headwinds. The result is a more consistent revenue stream that, when coupled with improving unit economics, can contribute to healthier margins over time. In the broker's framework, this translates into a durable cash-flow generator for the FD business, reinforcing the thesis that the food-delivery core can sustain long-term growth even as new business lines mature.

Moreover, the note underscores that the FD business is a stable duopoly within its competitive space, a factor that reduces price-driven volatility and supports a more predictable growth path. The emphasis on affordability–particularly meals under INR 250–also suggests a defensible market position that can withstand price competition and shifting consumer preferences. For investors, these trends imply that Eternal’s cash-earnings power from the core FD operation could serve as a bedrock for the stock’s longer-term valuation, even if Blinkit and District encounter higher volatility in their early phases.

Valuation Framework: SOTP For Food Delivery And DCF For Blinkit - A 34% Upside

The broker's valuation framework blends a sum-of-the-parts approach with a discounting technique that is sensitive to growth trajectories and cash conversion. Food Delivery is valued on the basis of a 35x FY28E EV/EBITDA multiple, reflecting the scalability of a mass-market delivery platform with a proven unit-economics profile and strong network effects. Blinkit, the quick-commerce platform, is valued via a DCF to capture its long-horizon cash-generation potential in a high-frequency, time-sensitive market. The combined framework yields a target price of Rs 380, signaling about a 34% upside from the prevailing Eternal share price if growth drivers play out as expected and if the company can sustain the margin trajectory assumed in the model.

Two milestones embedded in the thesis deserve attention. First, a stable, rising gross order volume supported by higher order frequency and new customer additions enhances the quality of the FD franchise, potentially supporting higher near-term profitability and a more favorable multiple on the business. Second, Blinkit’s DCF valuation depends on the platform achieving sustained favorable unit economics and continued user growth, aided by logistic improvements and a broader product mix. If either pillar weakens or if competitive pressures accelerate, the target price could face revision. This is the essence of a growth investment: upside is tied to execution and market dynamics, with downside risk defined by the same variables in a more uncertain environment.

Market Context, Risks, And Strategic Takeaways For Investors

Investors should regard Eternal within the broader context of Indian consumer services and e-commerce. The FD and quick-commerce segments are both benefiting from rising digital adoption, urbanization, and a growing preference for convenient, affordable meals. Yet the competitive landscape in quick commerce remains intense, and price competition could compress near-term margins for Blinkit and other peers. The District venture is inherently riskier due to its early-stage nature, but it also offers the most meaningful potential for cross-sell opportunities as the platform tests new formats and partnerships in the out-of-home dining space. For the Eternal share price to move higher, execution across these three engines must be coherent and timely, with the FD business acting as a stabilizing anchor while the other two segments compound growth over time.

From a financial perspective, the projected GOV growth of 21.5% YoY in 1QFY27E and a 5.0% EBITDA margin set a framework for evaluating near-term profitability. The ability to translate top-line gains into cash flow will be a critical driver of the multiple expansion the market has priced into the stock. In practice, investors should monitor how the company accelerates the pace of customer acquisition while preserving or improving per-order margins, especially in the context of higher fixed costs tied to rapid delivery expansion and the continued investment needed for Blinkit’s DCF-based valuation to hold up. The interplay between revenue growth, cost discipline, and the pace of new customer additions will be decisive for whether the Eternal share price can realize the upside implied by Rs 380.

Investment Takeaways For Retail Investors

Takeaways for a retail investor come down to a few essential questions: Can the FD business maintain its acceleration while keeping cost of delivery under control? Will the eternal quick commerce unit sustain its growth trajectory amid intensifying competition and potential regulatory changes? Does District unlock meaningful cross-sell opportunities that can support incremental revenue at reasonable economics? If the answers trend positive, the composite risk-reward remains favorable, with the Rs 380 target offering a visible upside over the medium term. The multi-business approach reduces idiosyncratic risk associated with a single segment and provides multiple catalysts that can drive valuation revisions if the underlying metrics stay on track.

Frequently Asked Questions

What is Motilal Oswal's target price for Eternal?

Motilal Oswal's research note assigns a Buy rating on Eternal with a target price of Rs 380.

What are Eternal's three core business pillars analyzed in the note?

The note analyzes eternal food delivery, eternal quick commerce, and District (going-out) as the three core businesses.

What growth rate is expected for Eternal's Food Delivery in the medium term?

The note expects the Food Delivery business to grow around 18-20% in the medium term.

What is the 1QFY27E GOV growth projection mentioned in the note?

GOV growth is expected to be 21.5% year-on-year in 1QFY27E.

How is Blinkit valued in Eternal's overall valuation framework?

Blinkit is valued using a discounted cash flow (DCF) framework as part of the SOTP valuation for Food Delivery.

Conclusion

In the end, the eternal share price reflects not just a single quarter but the probability-weighted outcome of a set of opportunities in Indian consumer services. If the three engines continue to align, the upside could be durable and compelling; if execution falters, the same framework helps you re-calibrate with clarity. The choice is yours: build a position that aligns with your risk profile and use robust analytical tools to monitor the three growth engines as they evolve, one quarter at a time.

Open your trading and demat account here

Reference :

1 : Moneycontrol

Epfo Interest Rate For FY26: What It Means For Your Provident Fund And The New CITES 2.01 System

Key Takeaways

- epfo interest rate for FY26 stands at 8.25% for EPF accumulations.

- 34 crore EPF accounts will receive auto-processed credits under the new system.

- Credits targeted to be visible by July 15, 2026.

- Auto-settlement limit for fully KYC-compliant advance claims raised to ₹5 lakh.

When the epfo interest rate for FY26 is set at 8.25%, nearly 34 crore EPF accounts face a quiet but meaningful shift in how their retirement savings accrue and are credited. The annual interest credit is estimated at over ₹1.44 lakh crore, and the process is being auto-processed under a new centralized system after field offices verify each account. Credits are targeted to be visible by July 15, 2026. A new Centralised IT Enabled Services (CITES) platform, specifically CITES 2.01, will support the process and provide a unified view of member records and services.

Epfo Interest Rate For FY26: What It Means For Your Provident Fund

For individuals, the epfo interest rate for FY26 is set at 8.25% and is more than a number–it is a promise to keep retirement funds growing while a technology-driven process makes credits faster and more transparent. The annual interest credit is estimated at over ₹1.44 lakh crore and will involve approximately 34 crore EPF accounts. Credits will be auto-processed under the new system and are being verified by field offices before credit to member accounts. This acceleration is part of a broader push to make EPFO transactions more transparent, while reducing the time between rate announcements and actual credits.

In practice, this means your Provident Fund balance can start earning the official rate earlier in the cycle. The new system calculates interest up to the date of payment authorisation for final PF settlements, helping ensure you are credited for the exact period your funds were due. The migration from a decentralized to a single national database means officers anywhere in the country can verify member records and settle claims more quickly. This is not just about a number; it is about speed, accuracy, and a noticeably smoother experience for members and their families as they plan for retirement.

The Centralised CITES 2.01 Platform And The Shift To A Unified EPFO Database

The Centralised IT Enabled Services (CITES) platform, in its 2.01 iteration, is the backbone of today’s EPFO workflow. It provides a unified view of membership details, provident fund balances, claim status, pensionable service records, and benefits. Under a centralized payment architecture, claims are settled with funds credited directly into bank accounts on the day of settlement. The migration moves EPFO from a decentralized to a single national database, enabling member records to be processed from any authorized EPFO office. Field verification will be completed before credit to member accounts to ensure no account receives incorrect interest. This centralization is designed to improve transparency and make every member’s service history easier to audit and reference.

With CITES 2.01, EPFO members gain a single, coherent view of their records and status, and employers benefit from a streamlined interface for compliance and reporting. The platform is designed to work with auto-settlement features for fully KYC-compliant advance claims and ensures that all payments are traceable and timely, reinforcing trust in the system.

Timeline And Credit Process: When The Epfo Interest Rate Credits Will Be Visible

The credits for FY26 are targeted to be visible/credited by July 15, 2026, as the new system cycles into operation. The auto-processed credits will be verified by field offices before they are credited to member accounts, ensuring no account receives incorrect interest. Under the revised system, interest on final PF settlements will be calculated up to the date of payment authorisation. Previously, interest credit used to reflect in accounts in October or November after rates were announced. The combination of CITES migration and centralized processing is expected to accelerate settlement and improve transparency for all EPFO members.

Auto-Settlement Limits And Fully KYC-Compliant Claims: What Changes For You

Under the new framework, the auto-settlement limit for fully KYC-compliant advance claims has been raised to ₹5 lakh from ₹1 lakh. This change means eligible claimants can get faster early access to funds without manual verification steps, subject to compliance. As with all auto-settlements, the system requires that the claim be fully KYC-compliant and verified by the system before funds are credited. This is part of the accelerated settlement mechanism designed to bring relief to those who rely on timely access to PF funds for urgent needs.

UAN Transfers, Pension Payments, And The Centralised Pension Payment System

UAN-based provident fund accounts will be automatically transferred when employees change jobs, along with service history. This ensures continuity in service records and avoids gaps in PF accruals. Pension payments will be credited nationwide to bank accounts under a Centralised Pension Payment System, ensuring a unified and consistent approach to monthly retirement benefits. The transformation of the pension disbursement process aligns with the broader centralization strategy and reduces friction in pension delivery for retirees.

Additionally, the new portal will offer a unified view of membership details, provident fund balances, claim status, pensionable service records, and benefits; claims will be settled via a centralized payment architecture with funds credited directly into bank accounts on the day of settlement. These enhancements are designed to simplify the experience for workers and for employers who manage PF contributions as part of payroll.

State Readiness On Labour Codes: Kerala's Stand And West Bengal's Position

Mandaviya briefed reporters that almost all states have agreed to implement the new labour codes, with Kerala the notable exception. West Bengal is among those that have agreed to implement them, indicating significant momentum toward nationwide alignment. In practical terms, this state-by-state readiness can affect payroll integration, tax treatment, and the delivery speed of EPFO services in different regions. As the nationwide system matures, employees who switch jobs may appreciate smoother UAN transfers and more predictable pension payments across state lines.

Frequently Asked Questions

What is the epfo interest rate for FY26 and who approved it?

The epfo interest rate is 8.25% for FY26, recommended by the CBT and ratified by the government.

When will EPFO credit interest to member accounts?

Credits are targeted to be visible by July 15, 2026; auto-processing under the new CITES 2.01 platform will be verified by field offices before credit.

What is CITES 2.01 and how does it affect EPFO transactions?

CITES 2.01 is the Centralised IT Enabled Services platform that provides a unified view of member records and services, enabling centralized payment and faster, more transparent settlement.

What is the auto-settlement limit for fully KYC-compliant claims?

The auto-settlement limit has been raised to ₹5 lakh from ₹1 lakh.

How do UAN transfers and pension payments work under the new system?

UAN-based provident fund accounts will be automatically transferred when employees change jobs, along with service history. Pension payments will be credited nationwide under a Centralised Pension Payment System.

Which states have implemented the new labour codes?

Kerala is the only state yet to come on board; West Bengal is among those that have agreed to implement them.

Conclusion

The FY26 EPFO interest rate of 8.25% signals a faster, more transparent, and centrally managed credit process that could improve the reliability of your provident fund. The new CITES 2.01 platform and centralized architecture aim to deliver timely credits, better tracking, and unified service experiences across the EPFO ecosystem.

Open your trading and demat account here

Reference :

1 : Thehindu

Exide Industries Stock Price Outlook As India's Electronics Duty Push Accelerates Battery Makers

Key Takeaways

- Customs duty exemptions on electronics inputs are extended to March 31, 2029.

- Inputs include display cells, backlight units, FPCA, frames, and ACF for display modules.

- Concessions cover wireless charging parts such as NFC components and NdFeB magnets.

- The expanded 85-category battery equipment list aims to cut imports and spur domestic manufacturing.

India's drive to make electronics manufacturing cheaper and more self-reliant just got a major cost lever. The government has extended customs duty exemptions on key inputs used in display modules, wireless charging assemblies, and battery manufacturing, with effect immediate and lasting until March 31, 2029. For retail investors, this matters because the policy could tilt margins and investment prospects across sectors, and it could influence the exide industries stock price in the near term. The broad aim is to reduce dependence on imports and deepen local value addition, particularly in lithium-ion battery production and other high-end electronics manufacturing.

Exide Industries Stock Price Trajectory As Electronics Duty Exemptions Roll Out

The immediate effect is a potential easing of input costs for domestic players across electronics segments. The exemptions cover inputs like display cells, backlight units, flexible printed circuit assemblies (FPCAs), frames and anisotropic conductive film (ACF) used in manufacturing display modules for automotive, medical, and industrial equipment. Since the exemptions are effective now and run through March 31, 2029, manufacturers can plan longer horizons, and the exide industries stock price could react to the shift in margins and earnings expectations. While a single policy rarely determines stock moves, the market will now watch for how battery makers and their suppliers adjust pricing, procurement and capacity plans.

Inputs Exempted Under The Duty Concessions: Display Cells, Backlight Units And More

The exemptions extend to inputs such as display cells, backlight units, FPCA, frames and anisotropic conductive film (ACF) used in display modules. The CBIC has issued technical definitions for these components to ensure uniform implementation across the sector, reducing ambiguity for manufacturers importing these parts. The exemptions apply immediately, enhancing the cost-structure upside for domestic production while the display assemblies themselves for mobile phones, televisions, smartwatches, smart meters or interactive flat-panel displays remain outside the relief.

| Input Category | Exemption Status |

|---|---|

| Display cells | Exempt |

| Backlight units | Exempt |

| Flexible printed circuit assemblies (FPCA) | Exempt |

| Frames | Exempt |

| Anisotropic conductive film (ACF) | Exempt |

| Display assemblies for mobiles/TVs | Not Exempt |

Battery Manufacturing Upshot: 85 Categories Of Equipment Eligible For Concessional Duties

The revised notification now covers 85 categories of equipment spanning nearly the entire lithium-ion battery production process–from material mixing and coating to welding, testing, inspection and packaging. Supporting systems such as solvent recovery, heat recovery, dust collection and effluent treatment equipment have also been included. This broad coverage signals a strategic push to reduce import dependence and bolster domestic capacity for high-end battery manufacturing, a sector closely watched by investors for its role in electric mobility and energy storage. Investors will also track how the policy affects the stock price of Vedanta, stock price of Wipro, Tata Motors stock price, Infosys stock price, TVS Motors stock price and Amara Raja Batteries stock price for any early signals.

Wireless Charging Modules And NFC: NdFeB Magnets And Related Parts In The Relief

In wireless charging, concessions extend to NFC components and other parts used in charging modules. The broader list includes nano-crystalline assemblies, E-shields, PET liners, PC shims, coils and neodymium iron boron (NdFeB) magnets that appear in modern charging circuits. The inclusion of these inputs aligns with the government's aim to reduce the cost of advanced electronics manufacturing and strengthen domestic supply chains for critical components.

Uniform Implementation And Immediate Effect: CBIC Definitions For Clear Rules

The Central Board of Indirect Taxes and Customs (CBIC) has issued technical definitions for these components to ensure uniform implementation, preventing misclassification and ensuring the tax relief reaches intended users. The exemptions are already in effect, and a broad set of equipment for lithium-ion battery manufacturing has been included under the concessional duty regime.

Broader Market And Retail Investor Implications: Sector Signals For Exide Industries And Peers

Beyond batteries, the policy touches sectors linked to electric mobility, consumer electronics and advanced manufacturing. The cost relief can influence profit margins and cash flow for multiple players, including those involved in display modules and essential battery components. The reaction in Exide Industries stock price and peers may unfold over weeks as companies adjust procurement, capex plans and pricing strategies. Investors should monitor related stock price signals such as stock price of Vedanta, stock price of Wipro, Tata Motors stock price, Infosys stock price, TVS Motors stock price and Amara Raja Batteries stock price for early cues.

Frequently Asked Questions

How long will customs duty exemptions on electronics inputs be in effect?

The exemptions will remain in force until March 31, 2029.

Which inputs are covered by the exemptions?

Inputs include display cells, backlight units, flexible printed circuit assemblies (FPCAs), frames and anisotropic conductive film (ACF) used in display modules.

Are display assemblies for mobiles or TVs exempted?

No. Display assemblies meant for mobile phones, televisions, smartwatches, smart meters or interactive flat-panel displays are not covered by the relief.

How many categories of equipment are now eligible for concessional duties in battery manufacturing?

The revised notification covers 85 categories of equipment across the battery production process, including material mixing, coating, welding, testing, inspection and packaging, plus supporting systems like solvent recovery, heat recovery, dust collection and effluent treatment.

What is the broader goal of these exemptions for India's manufacturing landscape?

The measures aim to reduce dependence on imported finished products by making it cheaper to manufacture sophisticated electronics in India and to strengthen domestic supply chains, especially in electric mobility, consumer electronics and advanced manufacturing.

Could Exide Industries stock price respond to these changes?

Stock price responses depend on multiple factors, but improved input-cost dynamics could support margins for battery and electronics players, with Exide Industries stock price among the potential beneficiaries in the near to medium term.

Conclusion

Retail investors should view this as a meaningful step toward lower imported input costs and a more resilient domestic electronics ecosystem. The direct impact on Exide Industries stock price will depend on company-specific execution and broader market sentiment, but the trend points to a friendlier operating environment for battery and display-module suppliers in the medium term. The smart move is to build a watchlist focusing on battery, EV, and display-related players and apply a disciplined valuation lens as the reforms play out.

For deeper stock research and timely insights, consider Swastika's Sarthi AI stock assistant.

Open your trading and demat account here

Reference :

1 : Ndtv

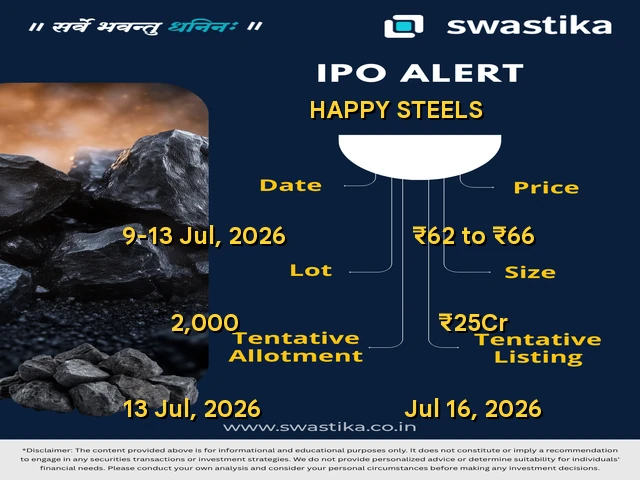

Happy Steels Limited IPO: Should You Apply, Wait, or Watchlist?

Key Takeaways

- Happy Steels Limited IPO is a NSE SME bookbuilt issue of 37,88,000 shares priced ₹62-₹66 with 2,000-share lots.

- GMP data is not available yet, so there is no clear listing gain signal.

- Major risks include missing financials and several key details (Registrar, Lead Manager, OFS) yet to be announced.

- Decision: watchlist for now, or apply only if you have a high risk tolerance and a post-listing plan.

Happy Steels Limited IPO Background: Company Overview

The IPO is described as an SME issue of 37,88,000 equity shares with a ₹10 face value, aggregating up to ₹25 crore. The price band is ₹62-₹66 per share, with a minimum order quantity of 2,000 shares. Open date is 9 July 2026 and close date is 13 July 2026. Listing is planned on 16 July 2026 on NSE SME. The registrar is Bigshare Services Pvt. Ltd., and the lead manager has not been announced yet. The sale type is Fresh capital only, with 35,98,000 shares (₹24 crore) under fresh issue. OFS, if any, will be announced later. GMP data is not available yet.

Happy Steels Limited IPO Details: Price Band, Size, Dates, And Listing

| Parameter | Details |

|---|---|

| Price Band | ₹62 to ₹66 |

| Lot Size | 2,000 shares |

| Issue Size | 37,88,000 shares (up to ₹25 Cr) |

| Open Date | 9 July 2026 |

| Close Date | 13 July 2026 |

| Listing Date | Thu, 16 July 2026 |

| Exchange | NSE SME |

| Issue Type | Bookbuilding IPO |

| Fresh Issue | 35,98,000 shares (₹24 Cr) |

| Fresh Capital | ₹24 Cr |

| OFS | To be announced |

| GMP | Not available yet |

| QIB Quota | 7,22,000 |

| NII Quota | 1,80,000 |

| Retail Quota | 12,60,000 |

| Registrar | Bigshare Services Pvt. Ltd. |

| Lead Manager | To be announced |

| Business | SME IPO of 37,88,000 equity shares of ₹10 each aggregating up to ₹25 Cr. The issue is priced at ₹62-₹66. Minimum order quantity is 2,000 shares. The registrar for the IPO is Bigshare Services Pvt. Ltd. The lead manager is yet to be announced. The shares are proposed to be listed on NSE SME. |

GMP Analysis: What Does No GMP Signal Mean For Investors?

Grey Market Premium (GMP) data is not available yet for this IPO. In general, a positive GMP can hint at listing gains, while a negative or zero GMP suggests modest expectations. The absence of GMP means you have no early price signal and must rely on the disclosed fundamentals and market conditions. For an SME issue with limited disclosures, this amplifies the uncertainty and is a caution flag for value-based investors.

Should You Apply? Pros And Cons For Retail Investors

Pros: The issue is priced within a moderate band for an SME, and the 2,000-share lot makes it accessible to many retail investors with ₹1.24–₹1.32 lakh ready to deploy (at the band endpoints). The NSE SME listing can offer liquidity if demand is strong and the SME story resonates with niche buyers.

Cons: There are no financials or profit metrics provided in the source material, so evaluating earnings potential is not possible. The lack of a confirmed registrar, lead manager, and OFS details adds execution risk. With GMP unavailable and a relatively small size, demand signals can swing quickly and heat listing day unpredictability.

How To Apply Via UPI/ASBA For This IPO

Applications for SME IPOs typically follow the standard ASBA process with a bank-blocked amount and, increasingly, UPI-based bidding options via your broker. Since the registrar and lead manager are not announced yet, confirm the exact steps on Swastika's platform or with your broker. In general, to bid via UPI/ASBA:

- Log in to your broker’s IPO bidding page and select Happy Steels Limited IPO.

- Enter the bid quantity (minimum 2,000 shares) and choose a price within the ₹62-₹66 band (for bookbuilt issues).

- Authorize the bid using UPI for payment or link your ASBA-blocked bank account as required by your broker.

- Submit the bid and ensure funds are blocked until the allotment is completed. If you use ASBA, funds are blocked and released if not allotted.

- Monitor the allotment status and listing details–these may be announced by the registrar once confirmed.

Once you decide to bid, you can consult Swastika's Sarthi AI stock assistant for help evaluating the IPO and tracking live signals through listing day.

IPO Listing And Allotment Timeline: What To Watch

The open date is 9 July 2026 and the close date is 13 July 2026. Listing is planned for 16 July 2026 on NSE SME. Allotment dates are not provided in the source material, and the registrar/lead manager are currently to be announced. Watch for updates from Bigshare Services Pvt. Ltd. and official exchange notices as the window closes and the listing day approaches.

Frequently Asked Questions

Is Happy Steels Limited IPO worth applying for at ₹62-₹66?

Given the lack of disclosed financials and other key details (registrar, lead manager, OFS), it’s challenging to justify value. The SME size and ₹25 Cr aggregate offer are small, and there’s no GMP signal yet. Only risk-tolerant investors with capital to spare and a post-listing plan should consider applying.

Is there GMP for Happy Steels Limited IPO?

GMP data is not available yet. There is no early listing-gain signal to rely on at this time.

What are the allotment odds for retail investors?

Retail quota is 12,60,000 shares within a 37,88,000-share issue. While this yields a theoretical 33.3% share of the issue to retail investors, actual allotment depends on oversubscription and the number of retail applicants.

When will the funds be blocked and when is listing expected?

Open on 9 July 2026, close on 13 July 2026, listing on 16 July 2026. Funds are blocked at bid time via ASBA or UPI-based submission, depending on your broker’s process.

How should I apply using UPI/ASBA for this IPO?

Use your broker’s IPO bidding platform to submit a bid at the desired price within the ₹62-₹66 band, enabling UPI-based payment authorization or ASBA-backed bank blocking. Confirm all details with your broker and registrar once finalized. If you need help, check Swastika’s resources or the Sarthi AI stock assistant for step-by-step guidance.

Conclusion

Happy Steels Limited presents a small-ticket SME IPO with a bounded price band and limited disclosure. The absence of financials, GMP signals, and confirmed registrar/lead manager details lowers transparency and increases risk for retail investors with tight budgets or limited risk tolerance. It’s a wait-and-watch scenario for most, with a cautious approach recommended until more information emerges. Watchlist – because additional disclosures (GMP, financials, registrar/lead manager) and a clearer demand picture are essential to judge reward vs risk.

Laser Power & Infra IPO: Apply, Watch, or Skip?

Key Takeaways

- Laser Power & Infra Limited IPO: price band ₹203-₹214, lot size 70 shares, total issue size 3,46,72,896 shares (up to ₹742 crore) with Fresh ₹542 crore and OFS ₹200 crore.

- GMP data not available yet; no clear listing gain signal at this stage.

- Key risk: no disclosed revenue or profit numbers in the source; valuation cannot be judged yet.

- Action: given data gaps, consider watching the listing or applying only if you have risk tolerance and capital around ₹14k per lot.

Laser Power &Amp Infra IPO Background: What The Company Does And Who Backs It

Laser Power & Infra Limited is launching a main-board IPO to raise up to ₹742 crore through a mix of Fresh capital and an Offer for Sale (OFS). The issue comprises a Fresh Issue of 2,53,27,102 equity shares (up to ₹542 crore) and an OFS of 93,45,794 shares (up to ₹200 crore). The IPO is priced in a band of ₹203 to ₹214 per share with a lot size of 70 shares. The listing will occur on both BSE and NSE on Thursday, 16 July 2026. While the name suggests activity in laser power and infrastructure segments, the source data does not provide a detailed business description or promoter background. This means the current read focuses on capital structure, timing, and market-access signals rather than a fundamental, revenue-based thesis.

Key numbers at a glance include the total issue size (3,46,72,896 shares), the split between Fresh Issue and OFS, and the price band. The exchange, open/close dates, and listing date offer a clear timetable for investors to plan around. The Registrar and Lead Manager status are listed as To be announced in the data, though the Business section notes MUFG Intime India Pvt. Ltd as registrar. Retail quota sits at 13% of net offer, with QIB quota capped at not more than 50% of net offer and NII quota not less than 15% of net offer. These allocations give a sense of the competitive landscape for bids and the potential for demand patterns to emerge once marketing begins.

Laser Power &Amp Infra IPO Details: Price Band, Lot Size, Issue Size, Dates

| Parameter | Details |

|---|---|

| Company | Laser Power & Infra Limited |

| Open Date | 9 Jul, 2026 |

| Close Date | 13 Jul, 2026 |

| Listing Date | Thu, 16 Jul 2026 |

| Price Band | ₹203 to ₹214 |

| Lot Size | 70 shares |

| Issue Size | 3,46,72,896 shares (up to ₹742 crore) |

| Fresh Issue | 2,53,27,102 shares (up to ₹542 crore) |

| OFS | 93,45,794 shares (up to ₹200 crore) |

| Exchange | BSE, NSE |

| Issue Type | Bookbuilding IPO |

| Registrar | To be announced |

| Lead Manager | To be announced |

| QIB Quota | Not more than 50% of Net Offer |

| NII Quota | Not less than 15% of Net Offer |

| Retail Quota | 13% of Net Offer |

Other operational details include a face value of ₹5 per share and a finish of 70 shares per lot. The Registrar and Lead Manager are not fully disclosed in the dataset, though MUFG Intime India Pvt. Ltd. appears as registrar in the business description. The lack of a disclosed Min Investment indicator is notable; investors should be prepared for the possibility that the minimum investment will correspond to one lot (i.e., 70 shares) at the lower end of the price band, which would be around ₹14,210 at ₹203 per share or about ₹14,980 at ₹214 per share. The GMP and subscription trends remain the primary external signals to watch as the open date approaches.

GMP Analysis And Subscription Signals: What We Know And What We Don’t

GMP status for Laser Power & Infra IPO is listed as Not available yet. That means there is no publicly verifiable market signal about potential listing gains or demand strength associated with the issue at this moment. There is also no live subscription data included in the source; the final outcome will hinge on investor appetite once the issue opens. In such scenarios, GMP typically acts as a rough proxy for expected listing performance; absence of GMP data keeps the decision-making anchored to the lack of disclosed financials and to the book-building dynamics rather than a clear premium or discount signal.

Laser Power &Amp Infra IPO Valuation: Is ₹203-₹214 Band Justified?

valuation assessment is hampered by the absence of any revenue or profitability numbers in the source material. The IPO is a large, ₹742 crore bookbuilt offer with a hefty fresh issue tranche (₹542 crore) and an OFS (₹200 crore). Without financials, peers, or earnings visibility, a traditional P/E or EV/EBITDA comparison isn’t possible here. The price band sits around ₹203-₹214, which translates to roughly ₹14k per lot at the lower end–this is a non-trivial outlay for retail investors without a disclosed earnings trajectory. Given these gaps, the risk-return equation remains uncertain, and the valuation’s credibility will largely ride on future disclosures and how demand evolves during the book-building window.

Should Investors Apply For Laser Power &Amp Infra IPO? Pros And Cons

Pros

- Large-capital raise of up to ₹742 crore gives the company room to fund growth and expansion plans (as per the data).

- Dual listing on BSE and NSE provides liquidity avenues for post-listing trading.

- Retail quota exists (13%), which helps distribute allocation opportunities beyond institutions, though exact allotment odds aren’t specified.

Cons

- No revenue or profitability data provided in the source, making fundamental valuation difficult.

- GMP data is not available yet, offering no early signal about potential listing gains or demand strength.

- Registrar and Lead Manager details are listed as To be announced in the data; operational clarity and investor protection depend on official confirmations.

Given the data gaps, this IPO reads as a risk-tocused play rather than a straightforward growth bet. Retail investors with a high risk tolerance and appetite for capital at roughly ₹14k per lot could consider a small exposure, but only with a clear post-listing plan and strict risk controls. If you are risk-averse or need earnings visibility before investing, this is a strong candidate to watch rather than buy now. For deeper stock insights, you may also consult Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

How To Apply For Laser Power &Amp Infra IPO Via ASBA/UPI

Laser Power & Infra’s IPO is a book-building issue, and retail investors typically apply through ASBA (Application Supported by Blocked Amount) via their bank’s IPO facility or via their stockbroker’s platform. While the source data does not outline bank-specific steps, the general process is:

- Open or use your existing trading and demat account with a broker who offers IPO subscriptions.

- Choose Laser Power & Infra IPO in the IPO tab and enter your bid details (price band, number of shares). If your broker supports ASBA, select ASBA as the payment method; your bank will block the application money until allotment.

- If your broker supports UPI-based bids, you can submit bids using your UPI ID as per the broker’s instructions.

- Submit the bid within the open window (9 Jul 2026 to 13 Jul 2026). Monitor confirmation and later the alloted shares and refund status post-allotment.

- Funds are released or debited depending on allotment; in case of partial/allocation, the unallotted amount is released.

Allotment Odds, Listing Timeline, And What To Watch

Allotment odds for retail investors are not disclosed in the source data. The retail quota is set at 13% of net offer, while QIB quota is not more than 50% and NII quota is not less than 15% of net offer, which hints at a balanced book but does not guarantee allocation outcomes. Key dates to watch are:

- Open: 9 Jul 2026

- Close: 13 Jul 2026

- Listing: 16 Jul 2026

Watch the GMP signal (once available) and subscribe to any official updates. Given the lack of disclosed financials, the primary risk remains the uncertainty around profitability and sustainable earnings. If you do decide to participate, have a clear post-listing plan and limit exposure to fit your risk tolerance and capital allocation.

Frequently Asked Questions

Is Laser Power & Infra IPO worth applying for at ₹203-₹214?

There is no revenue or profitability data in the source, so fundamental valuation cannot be assessed. The absence of GMP data adds to the uncertainty. Treat this as data-light and high-risk, and decide based on your risk tolerance and capability to absorb potential losses.

When does the Laser Power & Infra IPO open, close, and listing date?

Open on 9 July 2026 and close on 13 July 2026. Listing is scheduled for 16 July 2026 on BSE and NSE.

What is the lot size and approximate minimum investment for this IPO?

Lot size is 70 shares. Approximate minimum investment ranges from ₹14,210 to ₹14,980 depending on whether the bid is at ₹203 or ₹214. The official min investment figure is listed as To be announced in the source.

What is the GMP status and listing gain expectation for Laser Power & Infra IPO?

GMP data is not available yet, so there is no GMP-based listing gain signal to rely on at this moment.

How do I apply for Laser Power & Infra IPO via ASBA or UPI?

Apply through ASBA via your bank or broker's platform; funds are blocked until allotment. Some brokers support UPI-based bids. Use your broker’s exact steps and monitor allotment status after the window closes. For additional guidance, you can consult Swastika's Sarthi AI stock assistant:Swastika's Sarthi AI stock assistant.

Conclusion

The Laser Power & Infra IPO sits at the intersection of a substantial ₹742 crore capital raise and a conspicuously data-light investment thesis. The absence of any disclosed revenue or profitability metrics, coupled with no GMP signal yet, makes this a high-uncertainty listing rather than a straightforward growth bet. Retail investors should treat this as a watchlist opportunity until more financial clarity and official confirmations (Registrar/Lead Manager) are available. If you must act, restrict exposure to a small, well-planned amount and align with a post-listing strategy that minimizes downside risk. Watchlist – because there is insufficient data to justify a confident buy today.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App