Sanctum Wealth Portfolio: NRIs’ Three-Wallet Strategy for India Growth

Key Takeaways

- The sanctum wealth portfolio allocates 45% to equities and 28–30% to cash/debt/arbitrage for NRIs.

- A three-wallet approach–global, residence-market, and India wallets–limits currency risk and aligns with goals.

- Gold at 10–12%, private-market alternatives at 10%, and REITs/InvITs at 5% build diversification.

- Long-run earnings growth matters more than short-term currency moves; SIP flows and mutual funds are rising in India.

In a rapidly transforming India, long-run wealth creation for NRIs hinges on a disciplined, currency-smart approach that accommodates multiple needs. The sanctum wealth portfolio framework–articulated by Shiv Gupta of Sanctum Wealth–advocates a 45% allocation to equities, complemented by a 28–30% slice for cash, debt and arbitrage, 10–12% in gold, 10% in private-market alternatives, and 5% in REITs and InvITs. This multi-asset mix is designed to capture India's structural growth while managing currency risk and liquidity across time horizons.

Beyond asset allocation, the model introduces the three-wallet concept: global wallet, residence-market wallet, and India wallet. The India wallet serves a distinct purpose and should complement, not duplicate, the others. The right size for each wallet depends on goals, liabilities and long-term plans. Currency matters, but long-run earnings growth matters more when measuring returns in the investor's reference currency.

What Is The Sanctum Wealth Portfolio Allocation For NRIs?

The recommended mix includes 45% in equities, 28–30% in cash, debt and arbitrage, 10–12% in gold, 10% in private-market alternatives, and 5% in REITs and InvITs. This allocation is designed to balance growth with liquidity and risk, while letting the India wallet capture domestic opportunities without duplicating global exposure.

| Asset Class | Allocation | Notes |

|---|---|---|

| Equities | 45% | Domestic exposure with a focus on manufacturing and digitalisation themes |

| Cash, Debt & Arbitrage | 28-30% | Liquidity + hedging and risk management |

| Gold | 10-12% | Diversification & inflation hedge |

| Private-Market Alternatives | 10% | Private credit, private equity, venture capital |

| REITs & InvITs | 5% | Real estate exposure with liquidity |

If an NRI were building a fresh ₹50 crore India portfolio today, allocation would be broadly as follows: 45% in equities, 28–30% in cash, debt and arbitrage, 10–12% gold, 10% private-market alternatives, and 5% in REITs and InvITs. The same framework applies, with customization based on liabilities, time horizon and risk tolerance.

Three Wallet Strategy: Global Wallet, Residence-Market Wallet, And India Wallet

The three-wallet concept helps segregate exposures by currency and jurisdiction. The global wallet captures opportunities outside India, the residence-market wallet aligns with where you live and manage daily finance, and the India wallet targets domestic growth and savings channels. Importantly, the India wallet should complement, not duplicate, the other two wallets, and the right size for each depends on goals, liabilities and long-term plans.

Why Currency Movements Matter Less Than Long-Term Earnings Growth

While currency movements affect final returns, the long-run earnings growth of Indian assets matters more when measured in the investor's reference currency. The rupee depreciation has genuinely reduced final returns, having weakened historically in stages, averaging roughly 3–4% a year over the long run. Short-term exchange rates matter far less than the sustained earnings trajectory of Indian equities and financial assets.

India's Growth Themes And The Sanctum Wealth Portfolio

Five structural themes are central to the sanctum wealth portfolio: manufacturing, digitalisation, financialization, infrastructure and consumption. Of these, financialization and manufacturing stand out as key drivers of long-term value creation for Indian markets. Domestic consumption, household savings and local capital markets do far more of the work than they did in the past, underscoring the importance of exposure to domestic growth alongside global opportunities.

Practical Implications For A Fresh ₹50 Crore India Portfolio

Applying the same allocation is a practical approach for a fresh ₹50 crore India portfolio today. The split would be 45% in equities, 28–30% in cash, debt and arbitrage, 10–12% in gold, 10% in private-market alternatives, and 5% in REITs and InvITs. The India wallet should be sized to capture domestic opportunities without duplicating global or residence-market exposures, and currency considerations should guide how you measure returns.

Common NRI Mistakes And How To Avoid Them

Some frequent missteps include comparing returns over short periods and extrapolating currency movements, failing to update residential status with banks and intermediaries after becoming an NRI, using the wrong account (NRE vs NRO) leading to repatriation and tax frictions, and neglecting foreign tax credits which can lead to double taxation. For larger estates, succession planning across multiple jurisdictions is often omitted. Addressing these issues early can save costs and preserve wealth over generations.

Within this framework, you can bridge opportunities across wallets and currencies, ensuring a disciplined, purpose-built approach to investing in India. Swastika offers Sarthi – an AI stock assistant that gives institutional-level research on any stock or index to retail investors – to help you analyze potential ideas within the sanctum wealth portfolio framework. This can be a natural bridge between what you learned and what you might do next.

Frequently Asked Questions

What is the Sanctum Wealth Portfolio allocation for NRIs?

The suggested mix includes 45% in equities, 28-30% in cash, debt and arbitrage, 10-12% in gold, 10% in private-market alternatives, and 5% in REITs and InvITs. The India wallet should complement other wallets and the exact weights depend on goals and liabilities.

How does the three-wallet strategy work for NRIs?

It uses a global wallet for exposures outside India, a residence-market wallet for the country of residence, and an India wallet for domestic opportunities. Each wallet serves a distinct purpose and should not duplicate the others; the size of each wallet depends on goals, liabilities, and long-term plans.

Why do currency movements matter in the sanctum wealth portfolio?

Currency movements affect final returns, but long-run earnings growth matters more when measured in the investor's reference currency. The rupee depreciation has historically weakened about 3-4% a year over the long run.

What are the growth themes behind the sanctum wealth portfolio?

Five structural themes—manufacturing, digitalisation, financialization, infrastructure and consumption—are important; financialization and manufacturing stand out as particularly influential.

What common mistakes should NRIs avoid when building this portfolio?

Don’t chase short-term returns or extrapolate currency moves; ensure residential status is updated with banks, use the correct NRE vs NRO account, claim foreign tax credits, and plan cross-jurisdiction succession for larger estates.

Conclusion

The sanctum wealth portfolio approach for NRIs is built to balance growth with liquidity, by design. By separating capital into three wallets and sticking to a disciplined allocation, you can capture India’s structural drivers–while protecting against currency volatility–and align investments with long-term goals.

Latest Articles

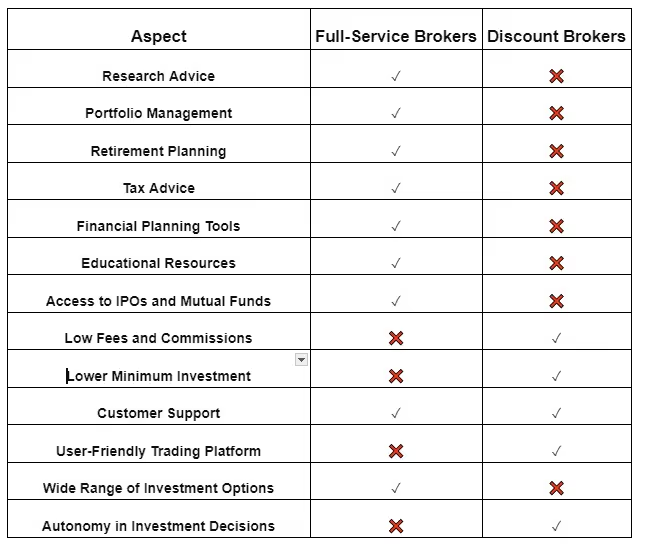

Understanding the Different Types of Brokers in the Stock Market

Stock market investing can be a great way to grow your wealth, but it can also seem complicated, especially for beginners. One of the first decisions you'll need to make is who will help you navigate this exciting world: a full-service broker or a discount broker? Today, we'll be exploring the types of brokers you can choose when entering the exciting world of stock trading.

What is a Stock Broker?

Before we dive into the different types of stockbrokers, let's first understand what a stock broker actually does. A stockbroker is a professional who helps in the buying and selling of stocks and other securities on behalf of investors. They act as intermediaries between buyers and sellers in the stock market. Share market investment advisors and registered representatives (RRs) are other names for stockbrokers.

Types of Stock Brokers:

- Full-Service Brokers: Picture them as your financial advisors, offering complete services to guide you through the complex world of investing. Here's what you can expect:

- Personalized Advice: Full-service brokers provide customized investment advice based on your financial goals, risk tolerance, and market conditions.

- Diverse Investment Options: Full-service brokers provides a wide range of investment options, including stocks, bonds, mutual funds, and more.

- Research Reports: They offer in-depth research reports and market analysis to help you make better investment and stock trading decisions.

- Portfolio Management: Many full-service brokers offer portfolio management services, where they actively manage your investments on your behalf.

- Complete Financial Planning: Beyond just buying stocks, full-service brokers offers complete financial planning services, covering areas like retirement planning, tax optimization, and estate planning.

- Additional Services: From retirement planning to tax advice, full-service brokers go the extra mile to meet all your financial needs.

- Examples of full-service brokers in India include Swastika Investmart, ICICI Direct, HDFC Securities, and Kotak Securities.

- Discount Brokers: A discount broker or online stockbrokers would typically just buy and sell on behalf of their clients.

- Cost-Effective Trading: Discount brokers take lower fees and commissions compared to their full-service brokers, making them an attractive option for investors for more affordable trading.

- User-Friendly Trading Platforms: Discount brokers provide simple and user-friendly trading platforms with features for executing trades efficiently.

- Independent Investing: With a discount broker, you have full control over your investment decisions. Whether you're buying stocks, ETFs, or options, you have the complete independence to execute trades according to your investment strategy and market analysis.

- Minimal Account Maintenance Requirements: Discount brokers often have lower minimum account balance requirements, making them affordable to a broader range of investors.

- Limited Customer Support: While discount brokers may offer basic customer support services, they generally provide less personalized assistance compared to full-service brokers. Examples of discount brokers in India include Tradingo, Zerodha, Upstox, and 5paisa.

Comparison of Different Types of Brokers: Let's compare the key features of full-service, discount, and online brokers in the table below:

Conclusion:

Choosing the right type of broker is an important decision for any investor. Whether you prefer personalized advice and portfolio management or are comfortable making your own investment decisions, there's a broker out there to suit your needs. We hope this guide has helped understand the types of stock market brokers.

Learn more about Stock Market!

Put Call Ratio (PCR): Definition, Formula, and Significance

Introduction to Put Call Ratio (PCR)

Among the many tools and indicators used by investors and traders, one of the indicators to understand is the Put Call Ratio (PCR). The Put-Call Ratio (PCR) is a popular tool to know the market sentiment!

Understanding PCR

Let’s understand this in the simplest way possible. Think of the stock market as a tug-of-war between investors who think prices will go up (bullish) and those who think the prices will go down (bearish). Stock options, which give you the right to buy (call) or sell (put) a stock at a predetermined price at a predetermined date, can reveal these beliefs. The PCR uses options to understand which side is pulling harder!

Before diving into the Put Call Ratio itself, it's essential to understand the basics of call and put options, and Market sentiment?

Call options give the holder the right, but not the obligation, to buy an asset at a specified price within a predetermined time frame. On the other hand, put options give the holder the right, but not the obligation, to sell an asset at a specified price within a predetermined time frame.

Market sentiment is the feeling of most investors at a particular time. It indicates whether they're feeling positive (bullish) or negative (bearish) about the market in general or a specific stock.

- Bullish Sentiment: Investors are feeling confident and expect prices to rise.

- Bearish Sentiment: Investors are feeling cautious and expect prices to fall.

So The Put Call Ratio (PCR) is a measure of market sentiment derived from the ratio of the trading volume of put options to call options.

Formula for Calculating PCR

The PCR is calculated using a simple formula:

PCR = Put Volume / Call Volume

Put Volume and Call Volume refer to the number of put and call option contracts traded in a day.

Example: Let's say on a particular day, 100 put contracts and 50 call contracts are traded for a stock. Here's how to find the PCR:

PCR = 100 (Put Volume) / 50 (Call Volume) = 2

A PCR of 2 suggests a bearish sentiment as more investors are buying puts, indicating a price drop.

Significance of PCR

The Put Call Ratio plays a significant role in market sentiment analysis. A high PCR value suggests that investors are bearish, indicating a potential downtrend in the market. While a low PCR value suggests that investors are bullish, indicating a potential uptrend. Ideal PCR is between 0.80-1.20.

In more simple language, A PCR value greater than 1 indicates a bearish sentiment, as there are more put options being traded in comparison to call options. A PCR value less than 1 indicates a bullish sentiment, as there are more call options being traded in comparison to put options.

Understanding PCR and its relation with market sentiment Practical Examples

Positive PCR (Bearish Sentiment):

Imagine a scenario where investors are feeling nervous about a stock, say ABC Ltd. They anticipate the price to go down. Here's how PCR reflects this:

Example:

- Put Volume: 200 contracts (Investors are actively buying puts)

- Call Volume: 100 contracts (Investors are hesitant to buy calls)

- PCR = Put Volume / Call Volume = 200 / 100 = 2

A PCR of 2 indicates a negative PCR, meaning there are more puts than calls. This suggests a bearish sentiment. Investors are betting on the price to fall by buying more put options.

Negative PCR (Bullish Sentiment):

Now, let's imagine a different scenario where investors are optimistic about XYZ Ltd. They expect the price to increase. Here's how PCR reflects this:

Example:

- Put Volume: 50 contracts (Investors are less interested in puts)

- Call Volume: 150 contracts (Investors are actively buying calls)

- PCR = Put Volume / Call Volume = 50 / 150 = (1 / 3)

A PCR of (1 / 3) is a positive PCR, meaning there are more calls than puts. This suggests a bullish sentiment. Investors are looking to profit from a price rise by buying more call options.

Neutral PCR:

Sometimes, investors might be unsure about the direction of the stock price. This creates a balanced market sentiment.

Example:

Put Volume: 75 contracts

Call Volume: 75 contracts

PCR = Put Volume / Call Volume = 75 / 75 = 1

A PCR of 1 is considered neutral. Put and call volumes are equal, indicating a balanced market sentiment where investors are neither overly bullish nor bearish.

Where to Find PCR Data:

Many financial websites and trading platforms offer live and historical PCR data. You can also find specific PCRs like the Nifty 50 PCR (for the top 50 Indian stocks) or the Bank Nifty PCR (for banking stocks). Additionally, some platforms provide PCR data for individual stocks.

Conclusion:

The Put-Call Ratio (PCR) is a valuable tool to understand investor sentiment in the stock market. By analyzing the PCR along with other factors, you can gain insights into market psychology.

Learn more about financial terminologies with Swastika!

What is Brokerage? | Meaning, Types, & More

The Indian stock market is a big marketplace where people buy and sell shares of ownership in companies, similar to a stock market anywhere else in the world. Here's a quick breakdown:

- Companies Sell Shares: Companies can raise money by selling small pieces of ownership, called shares or stocks, to the public. This is a way for them to get funding for growth.

- Investors Buy Shares: People who buy these shares become part-owners of the company. They hope that the company will do well, and the value of their shares will increase. They can then sell their shares at a profit later.

- The Stock Exchange: This is where the buying and selling of shares takes place electronically. The Bombay Stock Exchange (BSE) and the National Stock Exchange of India (NSE) are the two main stock exchanges in India.

- Brokers Help You Trade: You can't directly buy and sell shares on the stock exchange. You need a brokerage firm, like a middleman, to handle the transactions for you.

What is a Brokerage in the Stock Market?

A brokerage in the stock market is like a middleman that helps you buy and sell stocks. They are companies or individuals authorized to buy and sell stocks on behalf of investors. The stock brokerage company that facilitates your share purchases and sales levies a fee for its services. The term "brokerage" refers to this charge.

Example of a Brokerage:

Let's say you want to buy shares of a company like TCS. You don't go directly to the stock exchange to buy them yourself. Instead, you open an demat account with a brokerage firm like Swastika Investmart. Through their online platform or app, you place an order to buy TCS shares. The brokerage then carries out the transaction for you, and the shares are added to your account.

There are currently four methods available to stock brokers in India for charging brokerage fees. Let's examine each of them individually.

- Flat fee for every trade: As the name implies, there is a flat price associated with each deal you make in this mode. As a result, the brokerage you must pay is the same regardless of the transacted value. But there's a catch: the investor will only be charged the lower sum if the percentage brokerage is lower.

- Brokerage as a percentage of the traded value: A portion of the entire trade value is charged as brokerage by stock brokers. Put simply, a trade's worth will determine how much the brokerage is going to be, and vice versa.

- Monthly trading plans: A few stock brokers now provide monthly trading plans that let you make an infinite amount of trades in a given month, regardless of how much each trade is worth. They also demand a monthly or annual subscription fee in exchange.

- Zero brokerage: Numerous discount broking businesses do not charge a brokerage fee for the transactions.

How to Choose the Perfect Broker in India

The Indian stock market offers exciting opportunities, but choosing the right brokerage firm can feel difficult.

- Reputation and Reviews: Trust is key! Look for firms with a strong track record and satisfied customers.

- Reviews: User reviews on financial websites and forums offer valuable insights from real people. Read both positive and negative comments to get a well-rounded picture.

- Registrations: Ensure the firm is registered with SEBI (Securities and Exchange Board of India), the regulatory body. Their website should display membership codes for stock exchanges like NSE (National Stock Exchange) or BSE (Bombay Stock Exchange).

- Reputation: Established firms with a long history and satisfied clients are often a safe bet.

- Services: Consider your investment style and experience level when choosing between service models:

- Full-service brokers: Ideal for beginners. They offer personalized advice, research reports, and educational resources, but charge higher fees. (commissions).

- Discount brokers: Perfect for experienced investors who prioritize low costs. They focus on trade execution with minimal fees.

- Fees (Brokerage Charges): Understand fee structures, including commissions, account minimums, and any hidden charges. Full-service brokers might offer bundled services at a higher cost, while discount brokers have lower fees but fewer services.

- Trading Platform: Check the user-friendliness and features of the platform. Look for ease of navigation, real-time market data, and charting tools to support your investment decisions.

- Customer Support:

- Multiple Channels: Check whether they offer phone, email, and live chat options for assistance.

- Prompt Response: Look for firms known for resolving issues.

- Transparency is Key: No Hidden Costs.

Before opening an account, have a detailed discussion with the brokerage representatives. Ensure a clear understanding of all charges involved in the transaction

By understanding these costs upfront, you can avoid surprises and make better decisions about your investment.

Conclusion

Brokerage plays a crucial role in the stock market by facilitating the buying and selling of shares for investors. It serves as a middleman and charges fees for its services, which can be structured as flat fees, percentage-based commissions, monthly trading plans, or zero brokerage models. Choosing the right broker requires evaluating reputation, SEBI registration, fees, trading platforms, and customer support. By understanding these factors, investors can select a brokerage that aligns with their needs, ensuring a seamless and cost-effective trading experience.

Start Investing Today!

.avif)

What is the Securities Transaction Tax (STT)?

Introduction:

The world of finance can be confusing, especially when it comes to terms like Securities Transaction Tax (STT). But don't worry! This blog will make STT simple. Let's explore what it is, how it works, why it's there, and what it means for you as an investor.

What is STT?

STT is a tax imposed by the government on the buying and selling of securities like stocks, derivatives, and certain mutual funds. Whenever you make a transaction in the stock market, a small percentage of the transaction value is collected as STT. The tax is levied at a predetermined rate, expressed as a percentage of the transaction value, and is applicable to both the buyer and the seller.

How Does STT Work?

STT operates as a transaction-based tax, meaning it is triggered with every buy or sell order executed in the market. The tax rate varies based on the type of security being traded and the nature of the transaction—whether it involves delivery (holding securities beyond a specified period) or intraday trading (buying and selling within the same trading day). For instance, equity delivery trades typically attract a different STT rate compared to intraday trades. In other words STT is calculated based on the type of security you're trading and whether it's a buy or sell transaction. The rates may vary, but the idea remains the same: a little slice of your transaction goes to the government.

Why Does STT Exist?

The primary goal of STT is twofold. Firstly, it's a way for the government to collect revenue. Secondly, it acts as a measure to regulate the stock market. By imposing a tax on transactions, especially on short-term trades, it aims to discourage excessive speculation and promote more stable, long-term investments.

The introduction of STT serves several purposes, primarily driven by governmental and regulatory objectives:

- Revenue Generation: STT serves as a crucial source of revenue for the government. By taxing transactions within the securities market, the government can accumulate funds to support various developmental initiatives, infrastructure projects, and welfare programs.

- Regulatory Measure: Beyond revenue generation, STT acts as a regulatory tool aimed at shaping market behavior and fostering stability. By imposing a tax on transactions, particularly on short-term trades, STT discourages speculative activities and promotes a more disciplined, long-term approach to investing.

Impact on Investors:

For investors, STT adds a small cost to each transaction. While it may seem like pennies at a time, it can add up, especially for frequent traders. However, it's also a transparent tax, clearly stated on your transaction records, making it easy to keep track of.

For investors participating in the securities market, STT carries both direct and indirect implications:

- Cost Consideration: STT adds to the overall cost of trading for investors. While the tax rates are relatively modest, even small percentages can accumulate, especially for frequent traders engaged in high-volume transactions.

- Transparency: Unlike some other charges and fees associated with stock market transactions, STT offers transparency. It is explicitly disclosed in transaction statements provided by brokerage firms, allowing investors to accurately track and account for their tax liabilities.

- Behavioral Influence: STT plays a pivotal role in shaping investor behavior. By making short-term trades comparatively more expensive, STT incentivizes investors to adopt a more strategic, long-term perspective. This shift towards long-term investing not only aligns with wealth accumulation goals but also contributes to market stability and resilience.

Conclusion:

STT may sound intimidating at first, but it's simply a tax on stock market transactions. It serves the dual purpose of revenue generation for the government and regulating market behavior. So, the next time you see STT mentioned, just remember: it's a small fee for playing in the stock market sandbox.

Learn More about financial terminologies with Swastika !

What is Rollover in Stock Market

Introduction:

In the world of finance, there are many terms that can sound intimidating to beginners. "Rollover" is one such term that might seem confusing at first glance. However, once you understand what it means, it's actually quite simple. In this blog post, we'll break down the concept of rollover in the stock market.

What is Rollover?

Rollover in the stock market refers to the process of extending the expiration date of an investment position. This typically applies to futures contracts, options, and certain other derivative instruments. Let's delve into each of these to understand rollover better:

Futures Contracts:

In futures trading, investors agree to buy or sell a particular asset at a predetermined price on a specified future date. However, not all investors intend to take physical delivery of the underlying asset. Instead, they may choose to close out their position before the contract expires by offsetting their initial position with an opposite position (buying back what they sold or selling what they bought).

Rollover occurs when an investor extends the expiration date of their futures contract by closing out their current position and simultaneously opening a new position with a later expiration date. This allows investors to maintain exposure to the underlying asset without actually taking delivery.

Options:

Options contracts give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) within a specified period. Like futures contracts, options contracts have expiration dates.

When an options holder decides to extend the expiration date of their contract, they can engage in a rollover. This involves closing out their existing position and opening a new position with a later expiration date.

Why Rollover?

Investors might choose to rollover their positions for several reasons:

- Time Horizon: If an investor's outlook on the underlying asset hasn't changed but they want to extend their investment horizon, rollover allows them to do so without exiting the position entirely.

- Avoiding Delivery: In futures trading, rollover helps investors avoid taking physical delivery of the underlying asset, which may not be practical or desirable for various reasons, such as storage costs or logistical constraints.

- Adapting to Market Conditions: Rollover can also be a strategic move in response to changing market conditions. For example, if an investor expects volatility to increase in the near future, they may roll over their position to a later expiration date to give their investment more time to play out.

Conclusion:

Rollover is a common practice in the stock market, particularly in futures and options trading. It allows investors to extend the expiration date of their positions, providing flexibility and strategic options. By understanding the concept of rollover, investors can better manage their investments and adapt to evolving market conditions.

Learn more about Stock Market!

One Time Mandate (OTM) for Mutual Funds

Are you interested in growing your wealth but find traditional investment methods difficult? If so, then a mutual fund might be the perfect solution for you.

What are Mutual Funds?

A mutual fund is a type of investment that pools money from many investors and invests it in a variety of assets, like stocks and bonds. A professional manager, then uses that money to buy different investments on behalf of all the contributors (investors) like you. This approach allows you to gain exposure to a diversified portfolio of investments without having to pick individual stocks or bonds yourself.

What is OTM in Mutual Fund?

OTM stands for One Time Mandate in mutual funds. It's a one-time registration process where you allow your bank to deduct a certain amount from your savings account for investing in a specific mutual fund scheme.

One Time Mandate (OTM) in mutual funds covers the following transactions:

- Fresh Lump-Sum Investments:

You can use your bank account to make payments for lump-sum investments. The amount will be debited based on the fixed limit set in your OTM form.

- New Systematic Investment Plans (SIPs):

You can start new SIPs through the OTM service. There's no need to provide bank details or a canceled cheque again.

Duration of OTM: You can set up an OTM for a specific period, like five years, or keep it active until you decide to cancel it.

Overall, OTM is a convenient way to invest in mutual funds regularly and grow your money over time.

How Does OTM Work?

Once you set up an OTM, your bank will deduct the specified amount from your account based on requests from the mutual fund company. These requests come from investors like you who want to invest in the mutual fund scheme. This eliminates the need for manual payments every time you want to invest.

To register for a One Time Mandate (OTM), the process is straightforward. Follow these steps:

- Complete OTM Form: Fill out the OTM form with your personal and financial information.

- Bank Account Details: Provide details such as your bank's name, branch, account number, type, and IFSC code. Remember, only one bank account can be used for OTM registration.

- Personal Information: Include your name, date of birth, PAN number, address, phone number, and email ID. If the bank account is joint, provide details for other account holders too.

- Set Mandate Limit: Specify the maximum amount that can be debited. Transactions exceeding this limit will be rejected.

- Investment Preferences: Share your folio number and choose between fixed or maximum debit options. Decide the frequency of debits – monthly, quarterly, half-yearly, or as needed.

- Signature: All account holders must sign the OTM form. Ensure the signatures match those on file with the bank.

After submitting the form, the bank will process your request. Once approved, you can start using the OTM facility for mutual fund investments.

Benefits of OTM:

- Convenience: OTM makes investing in mutual funds easy and hassle-free. You don't need to attach a cheque or go through a payment gateway each time you invest.

- Paperless and Electronic: It's a digital process, so you don't have to deal with paper forms or documents.

- Automatic Investing: OTM automates your investments, helping you build wealth over time without having to remember to invest manually.

FAQs

How do I register for OTM?

Contact your bank. They will provide you with an OTM form to fill out. The form will ask for your personal information, bank details, and investment preferences.

Is OTM safe?

OTM is a secure process because it involves your bank and a registered mutual fund company.

Can I cancel OTM once I register?

Yes, you can cancel OTM at any time by contacting your bank.

What if I forget my folio number?

Your folio number is your unique identification number for your mutual fund investment. You can find it in your account statements or by contacting the mutual fund company.

Conclusion

OTM simplifies mutual fund investing by automating transactions, making it a hassle-free and paperless process. It ensures disciplined investing without the need for repeated manual payments, ultimately helping investors build wealth efficiently over time.

Learn more about financial terminologies with Swastika!

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App