NTPC Share Price Insights: Fifth Straight Session Eases And Market Context

Key Takeaways

- NTPC share price eased for the fifth straight session, around Rs 346.75 on NSE.

- NTPC stock price rose 1.55% in the last year, while NIFTY declined 5.14% and Nifty Energy rose 6.91%.

- July futures stood at Rs 347.85, signaling near-term price alignment with the spot.

- NTPC PE is 14.6x based on TTM earnings to March 26.

NTPC share price eased for the fifth straight session, quoted at Rs 346.75 on the NSE as of 13:19 IST. This move frames a session where the benchmark NIFTY is around 24,052.3, up 0.71%, while the Sensex sits near 77,018.87, higher by about 0.67% for the day. The year-to-date view remains mixed: NTPC has gained 1.55% over the last 12 months as NIFTY slides 5.14% and the Nifty Energy index climbs 6.91%. Volume in NTPC today stood at 101.69 lakh shares, versus the 1-month average of 134.92 lakh. The July futures contract for NTPC sits at Rs 347.85, down 0.33%, signaling near-term alignment with the cash price. The stock carries a price-earnings ratio of 14.6x on TTM earnings to March 26.

NTPC Share Price Momentum After Five Straight Sessions

NTPC share price has shown a pause after five successive sessions of declines, with the current quote at Rs 346.75 on the NSE as of 13:19 IST. The intraday movement placed NTPC down 0.56% on the day, underscoring a risk-off tone that often accompanies short-term consolidation. In the broader market, NIFTY trades around 24,052.3, up roughly 0.71%, while the Sensex hovers near 77,018.87, up about 0.67%. The energy complex continues to be a source of relative strength in the market context, with the Nifty Energy index showing resilience. Over the past year, NTPC has risen 1.55%, compared with a 5.14% decline in the NIFTY and a 6.91% rise in the Nifty Energy index. On the volume front, today’s turnover was 101.69 lakh shares, below the 1-month average of 134.92 lakh. A close look at the chart suggests potential support near the Rs 340–345 zone, with resistance near Rs 350–355, depending on energy sector momentum. If momentum shifts above Rs 350, bulls could revisit a test of the Rs 355–360 area in coming sessions.

Market Context: Nifty And Energy Sector Movements

The present market context shows the NIFTY up around 0.71% on the day to about 24,052.3, while the Sensex is near 77,018.87, up about 0.67%. NTPC sits in a sector that has been relatively resilient; the Nifty Energy index is up about 0.69% on the day and has posted a 0.04% increase over the last month. NTPC’s daily volume stood at 101.69 lakh shares today, below the 1-month average of 134.92 lakh, underscoring a day of cautious participation. Such dynamics imply that energy names, including NTPC, may still attract steady interest even as the broader market exhibits mixed momentum.

Trading Signals: Futures And Short-Term Indicators

The July futures contract for NTPC is priced at Rs 347.85, down 0.33% on the day, indicating near-term alignment with the cash price. With a P/E ratio of about 14.6x based on trailing twelve months earnings to March 26, the stock sits at a moderate valuation relative to the sector. For traders, the Rs 347–350 zone will be critical in the near term; a break above could invite fresh buyers, while a break below Rs 340 could put pressure on the stock. The path for NTPC will likely mirror the energy sector’s broader rhythm and macroeconomic cues like interest rates and risk appetite.

NTPC Share Price History And Chart Perspective

Looking at the ntpc share price history, NTPC has gained 1.55% over the last year, while the NIFTY has fallen 5.14% and the Nifty Energy index has advanced 6.91%. The ntpc share price history shows a mild up-and-down trajectory that suggests consolidation rather than a robust breakout. The last month has seen NTPC ease by about 1.39%, indicating a temporary pause in the upward drift, even as energy stocks display selective strength. A chart view would emphasize watching the supports near Rs 340 and resistance around Rs 355–360, with the longer-term trend dependent on broader market and energy-specific catalysts.

NTPC Earnings And Valuation Considerations

NTPC’s earnings framework remains anchored by a moderate valuation, with a trailing P/E of approximately 14.6x based on earnings to March 26. This indicates a valuation that reflects stable earnings and a defensively positioned utility play within India’s power sector. Investors should monitor the evolution of fuel costs, base tariffs, and hydropower dynamics, as these variables can influence earnings stability in the coming quarters. While near-term price action may oscillate with energy-sector sentiment, the longer-term case for NTPC hinges on steady project execution and policy clarity, which keep the valuation in a reasonable band for a utility stock.

Frequently Asked Questions

What is NTPC share price today?

As of 13:19 IST on the NSE, NTPC share price is Rs 346.75, with the stock easing for the fifth straight session.

How did NTPC perform in the last year compared to the NIFTY?

NTPC stock price jumped 1.55% in the last year, while the NIFTY declined 5.14% and the Nifty Energy index rose 6.91%.

What is the July futures price for NTPC?

The July futures price for NTPC is Rs 347.85, down 0.33% on the day.

What is NTPC's price-to-earnings ratio based on TTM earnings?

NTPC's price-to-earnings ratio is 14.6x based on trailing twelve months earnings to March 26.

Where can I access AI stock research for NTPC?

You can access institution-level stock research via Swastika's Sarthi AI stock assistant.

Conclusion

For the retail investor, the NTPC share price action indicates a pause rather than a definitive reversal. With the stock around Rs 346–347 and a 14.6x trailing PE, the setup favors a wait-and-watch approach in the near term, particularly as the July futures hover near Rs 347. A test of support near Rs 340 or a break above Rs 350 could provide more clarity on the next directional move. The practical takeaway is to couple price action with broader energy-sector momentum and to manage risk through clear stop levels and position sizing.

For deeper, institution-level stock research that blends experience, analysis, and trusted data, consider Swastika Investmart’s Swastika's Sarthi AI stock assistant. This tool helps retail investors navigate NTPC and other sector names with AI-powered insights and research that complement traditional analysis.

Open your trading and demat account here

Reference :

Latest Articles

.jpg)

Kusumgar IPO: Should You Apply or Not? IPO Details, GMP, Subscription Status & Complete Review

The Kusumgar IPO has attracted significant investor attention due to its strong Grey Market Premium (GMP), healthy Day 1 subscription numbers, and the company's niche presence in India's defence and aerospace manufacturing sector. However, while the listing sentiment appears positive, long-term investors should look beyond the GMP and understand the company's financial performance, business fundamentals, valuation, and key risks before investing.

Kusumgar Limited is not a traditional textile manufacturer. It specialises in engineered technical fabrics used across defence, aerospace, automotive, industrial, and outdoor applications. Its products include military parachutes, camouflage netting, cold-weather clothing fabrics, and coated textiles designed for high-performance use.

If you're wondering whether the Kusumgar IPO is worth applying for, what the latest GMP indicates, or whether the company has long-term growth potential, this guide covers everything you need to know.

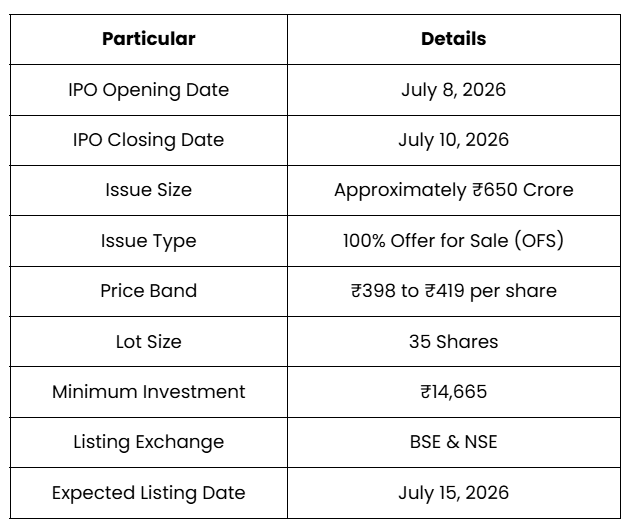

Kusumgar IPO Highlights

Before evaluating the company's investment potential, let's look at the key details of the public issue.

The Kusumgar IPO is entirely an Offer for Sale, meaning the company will not receive any funds from the issue. Instead, existing shareholders are selling part of their holdings. Investors should understand that unlike a fresh issue, the IPO proceeds will not be used for expansion, debt repayment, or business growth.

What Does Kusumgar Limited Do?

A primary question on many investors' minds is whether Kusumgar Limited qualifies as a defence enterprise.

Partially, yes. Kusumgar Limited manufactures engineered technical fabrics that are widely used in defence and aerospace applications. At the same time, it also serves industrial, automotive, and outdoor lifestyle markets.

Its product portfolio includes:

- Military parachute fabrics

- Stealth camouflage netting

- Extreme weather military clothing fabrics

- Industrial coated textiles

- Automotive fabrics

- Outdoor performance fabrics

Unlike conventional textile manufacturers, Kusumgar focuses on specialised products that require advanced technical expertise and lengthy customer approval processes. This specialisation creates higher entry barriers compared to regular textile businesses.

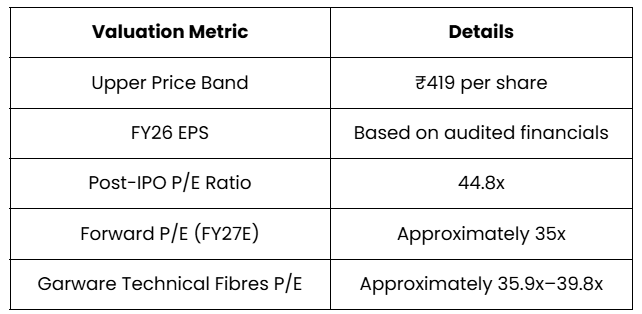

How is the Kusumgar IPO Valued?

One of the first questions investors ask before applying for an IPO is whether the company is fairly valued. The Price-to-Earnings (P/E) ratio helps compare the IPO's pricing with its earnings and listed peers.

The table below highlights Kusumgar's valuation at the upper end of the price band and compares it with its closest listed competitor.

At the upper price band, Kusumgar is valued at 44.8 times its FY26 earnings, which appears slightly higher than its closest listed peer, Garware Technical Fibres. However, some analysts believe the valuation becomes more reasonable at around 35x forward FY27 earnings, assuming the company delivers the expected earnings growth. Investors should therefore evaluate whether Kusumgar can sustain its growth trajectory and justify the premium valuation over the long term.

Why is the Kusumgar IPO Attracting Investor Interest?

Several factors have contributed to the strong interest in the IPO.

First, the company operates in India's growing defence manufacturing ecosystem, which continues to receive policy support under initiatives such as Make in India and increased defence spending.

Second, the IPO received backing from well-known institutional investors during the anchor allocation. Finally, the Grey Market Premium (GMP) and strong retail participation have boosted investor sentiment ahead of the listing.

While these factors have generated excitement, investors should remember that IPO decisions should be based on business fundamentals rather than market sentiment alone.

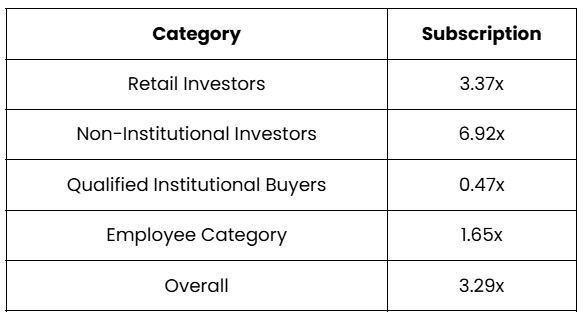

Kusumgar IPO Subscription Status

Subscription numbers indicate how much demand exists across different investor categories. The following table shows the Day 1 subscription status.

This indicates that retail and HNI investors showed strong interest on the opening day. The relatively lower QIB subscription should not be viewed negatively, as institutional investors typically place most of their bids on the final day of the issue.

Kusumgar IPO Subscription Status (Day 1)

One of the strongest indicators of investor interest in an IPO is the subscription status. It shows how different investor categories are responding to the public issue during the bidding period.

The table below presents the updated subscription status as of 4:15 PM on July 8, 2026.

The Kusumgar IPO witnessed strong demand on the very first day, driven primarily by Non-Institutional Investors (HNIs), whose category was subscribed 6.92 times. Retail investors also showed healthy participation with 3.37 times subscription, indicating positive sentiment among individual investors. Meanwhile, the QIB portion stood at 0.47 times, which is not unusual, as institutional investors often place the majority of their bids on the final day of the issue. With the IPO remaining open until July 10, 2026, subscription levels may increase further before the issue closes.

Kusumgar IPO GMP: What Does It Suggest?

A frequent inquiry among investors is whether Kusumgar Limited operates as a defence corporation.

According to market reports, the Grey Market Premium (GMP) stood at approximately ₹168 on July 8, 2026. Based on the upper price band of ₹419, this indicates an estimated listing price of around ₹587, suggesting a potential listing premium of about 40%.

However, investors should remember that GMP is an unofficial market indicator. It reflects current market sentiment but does not guarantee listing gains or future share price performance. Investment decisions should never be based solely on GMP.

Who Invested Before the IPO?

Anchor investors often provide confidence to the market because they are typically large domestic and international institutions. Kusumgar raised nearly ₹193.9 crore from anchor investors before the IPO opened.

Some of the notable investors include:

- BlackRock Global Funds

- Goldman Sachs

- Kotak Mahindra Life Insurance

- SBI Mutual Fund

- ICICI Prudential ELSS Tax Saver Fund

Strong institutional participation indicates confidence in the company's long-term business prospects, although it should not be the only factor influencing an investment decision.

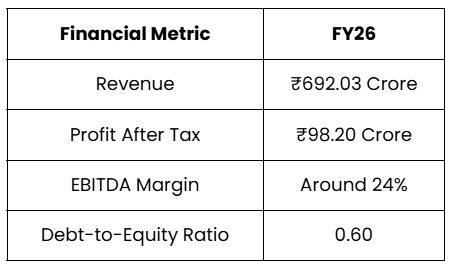

How has Kusumgar Performed Financially?

Financial performance is one of the most important factors investors should evaluate before applying for any IPO. The table below summarises the company's latest financial performance.

At first glance, the business appears profitable. However, investors should note that both revenue and net profit declined during FY26 compared to FY25. The decline was mainly driven by lower execution of large defence contracts rather than weakness across the company's entire business.

Meanwhile, industrial and outdoor fabric segments continued to grow strongly. This highlights an important point. The company's revenue can fluctuate significantly because defence orders are often project-based rather than recurring.

What makes Kusumgar Different from Other Textile Companies?

Kusumgar's biggest strength lies in its specialised manufacturing capabilities. Unlike ordinary textile companies, Kusumgar operates in highly regulated industries where product approvals can take several years. Some of its competitive advantages include:

Long Customer Approval Cycles

Products used in defence and aerospace require extensive testing before approval. Once approved, customers rarely switch suppliers.

Technical Expertise

The company possesses specialised knowledge in manufacturing engineered fabrics using advanced synthetic fibres and coatings.

Integrated Manufacturing

Kusumgar handles multiple manufacturing processes under one roof, including weaving, coating, lamination, and fabrication.

Diverse Product Portfolio

The company manufactures over 1,000 fabric variants for different industrial applications. These factors create meaningful entry barriers for new competitors.

What are the Biggest Risks in the Kusumgar IPO?

Every IPO carries risks, and Kusumgar is no exception. Here are some important concerns investors should understand.

Dependence on Large Defence Orders

The company's revenue depends on a relatively small number of high-value defence contracts. Delays or postponements can significantly impact financial performance.

Underutilised Capacity

Although Kusumgar has expanded its manufacturing capacity considerably, utilisation dropped to around 50%. This means the company must increase demand to improve operational efficiency.

Rising Working Capital

Trade receivables increased sharply during FY26, indicating that cash collections have become slower. This may temporarily affect cash flow.

Raw Material Price Volatility

The company uses petrochemical-based raw materials. Fluctuations in crude oil prices could impact profitability.

No Fresh Capital

Since the IPO is entirely an Offer for Sale, the company will not receive any funds to support expansion or strengthen its balance sheet.

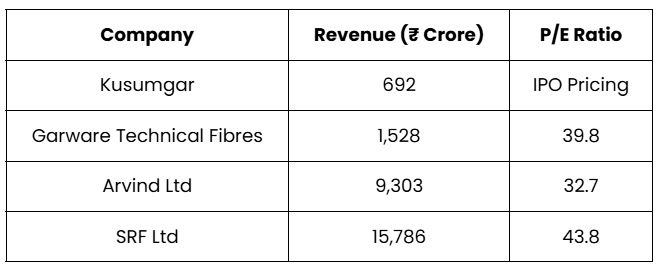

How does Kusumgar Compare with Listed Peers?

Investors often compare IPO valuations with existing listed companies before making a decision. The following comparison provides useful context.

Compared to these companies, Kusumgar operates on a much smaller scale. However, it focuses on a highly specialised niche with relatively fewer direct competitors.

Should You Apply for the Kusumgar IPO?

The answer depends on your investment objective. If you're looking for listing gains, the healthy GMP, strong retail participation, and reputed anchor investors indicate positive market sentiment.

From a valuation perspective, the IPO is priced at a post-issue P/E of 44.8x FY26 earnings, which is higher than some listed peers. Investors should assess whether the company's niche positioning, technical expertise, and expected earnings growth justify this premium valuation before subscribing.

However, if you're investing for the long term, it's equally important to consider the company's declining revenue, dependence on large defence orders, underutilised manufacturing capacity, and the fact that the IPO does not raise fresh capital for the business.

Investors should evaluate the company's long-term growth prospects alongside its current financial performance before making a decision.

Expert View

According to the research team at Swastika Investmart, Kusumgar operates in a niche segment with strong technical capabilities and high entry barriers, particularly in defence and aerospace fabrics. While the robust GMP, healthy subscription, and marquee anchor investors reflect positive market sentiment, investors should carefully assess the company's revenue concentration, capacity utilisation, and valuation before applying for the IPO.

Frequently Asked Questions (FAQs)

Should you apply for the Kusumgar IPO?

The answer depends on your investment objective. Investors looking for potential listing gains may find the IPO attractive due to the strong Grey Market Premium (GMP), healthy subscription, and participation from marquee anchor investors. However, long-term investors should evaluate the company's financial performance, valuation, revenue visibility, and business risks before making an investment decision.

Is Kusumgar IPO good for listing gains?

Current market sentiment suggests the possibility of positive listing gains. The IPO has witnessed a healthy Grey Market Premium and strong demand from retail and HNI investors. However, GMP is an unofficial indicator and can change before listing, so it should not be the sole basis for investing.

Is Kusumgar a defence company?

Kusumgar is a technical textile manufacturer with a strong presence in the defence and aerospace sector. It manufactures engineered fabrics used in military parachutes, camouflage netting, protective clothing, and other specialised defence applications. The company also serves industrial, automotive, and outdoor lifestyle segments.

Why is the Kusumgar IPO a 100% Offer for Sale?

The IPO is entirely an Offer for Sale (OFS), meaning existing shareholders are selling their shares. The company will not receive any funds from the public issue. As a result, the IPO proceeds will not be used for expansion, debt repayment, or business operations.

What are the biggest strengths of Kusumgar Limited?

Kusumgar's biggest strengths include its niche product portfolio, technical expertise, and high entry barriers. Long qualification cycles in the defence and aerospace sectors make it difficult for new competitors to enter the market. The company also has an integrated manufacturing setup and a diversified portfolio of engineered fabrics.

What are the major risks investors should consider?

The company's dependence on large defence orders, underutilised manufacturing capacity, rising receivables, and exposure to raw material price fluctuations are some of the key risks. Investors should also note that since the IPO is a pure OFS, the company will not receive fresh capital to support future growth initiatives.

How can investors check the Kusumgar IPO allotment status?

Investors can check the allotment status through the registrar, Bigshare Services Private Limited. Once the basis of allotment is finalised, applicants can use their PAN, application number, or DP Client ID to verify whether shares have been allotted.

What should investors track after the IPO?

Beyond the listing, investors should monitor order inflows from the defence and aerospace sectors, capacity utilisation, revenue growth, operating margins, working capital management, and the company's ability to improve cash flows. These factors will provide a better indication of Kusumgar's long-term growth potential than listing-day performance alone.

Conclusion

The Kusumgar IPO offers investors an opportunity to invest in a company operating in the niche technical textiles segment with a strong presence in defence and aerospace applications. While the healthy Grey Market Premium (GMP) and robust subscription reflect positive market sentiment, investors should focus on the company's business fundamentals, financial performance, valuation, and long-term growth potential rather than short-term listing expectations. Before investing, ensure the IPO aligns with your financial goals, investment horizon, and risk appetite instead of relying solely on GMP or market buzz.

For the latest IPO updates, expert reviews, and research-backed investment insights, follow Swastika Investmart and stay informed to make well-informed investment decisions.

Nps Withdrawal Rules And Global Pension Capital: The ASCEND Panel And NPS Growth

Key Takeaways

- PFRDA's ASCEND panel aims to attract global pension capital into India's NPS ecosystem.

- Dinesh Khara chairs ASCEND; panel includes Narayan Ramachandran, Ananth Narayan, Ashvin Parekh, Arvind Gupta, and Suparna Tandon.

- As of June 2026, nps assets under management are about ₹17.5 trillion ( $185 billion) for nearly 10 crore subscribers.

- The move could channel stable capital to infrastructure and support better long-term returns, with Sarthi for stock insights.

Nps Withdrawal Rules: What Retail Investors Should Know In 2026

nps withdrawal rules are drawing more attention as India's pension landscape shifts toward patient, global capital. A newly formed panel named ASCEND–Accelerated Scaling of Global Capital Ecosystem and NPS Development–has been appointed to explore how Indian pension funds can co-invest with leading international funds. Chaired by Dinesh Khara, it will also consider innovative investment structures and partnerships designed to channel durable capital into infrastructure and nation-building projects. The move aims to diversify risk and improve long‑term outcomes for NPS subscribers, who benefit as nps assets under management grow to ₹17.5 trillion (roughly $185 billion) for nearly 10 crore subscribers.

ASCEND Panel Composition, Mandate, And The Road Ahead

ASCEND stands for Accelerated Scaling of Global Capital Ecosystem and NPS Development, a panel appointed by the Pension Fund Regulatory and Development Authority (PFRDA) to attract global pension capital into India's retirement savings framework. The regulator described the panel's role as laying the foundation for a globally competitive pension ecosystem that supports long-term infrastructure financing needs. The panel's core mandate includes enabling Indian pension funds to collaborate with leading global pension funds through co-investment platforms, strategic partnerships, and innovative investment structures.

The committee is chaired by Dinesh Khara, who also serves as the chairman of the NPS Trust. The other members are Narayan Ramachandran (Chairman of TeamLease Services Ltd), Ananth Narayan (former whole-time member of Sebi), Ashvin Parekh (Managing Partner at Ashvin Parekh Advisory Services), Arvind Gupta (Trustee of NPS Trust), and Suparna Tandon (CEO of NPS Trust, who will serve as member secretary). These appointments signaled a deliberate blend of public policy, regulatory oversight, and private-sector investment expertise.

Nps Assets Under Management And Subscriber Growth: The Scale Behind The Reform

As of June 2026, nps assets under management stood at ₹17.5 trillion (about $185 billion), underscoring the scale of India's long-term savings platform. The NPS serves nearly 10 crore subscribers, and in parallel estimates indicate that pension funds under the NPS manage assets worth about $185 billion (₹17.5 trillion)–equivalent to around 5% of India's GDP. This sizable pool provides both opportunities and responsibilities: to channel durable, patient capital into infrastructure and nation-building assets while offering diversification and better long-term risk-adjusted returns to NPS subscribers.

How Global Pension Capital Could Change Your Nps Experience

The ASCEND initiative aims to create co-investment platforms and strategic partnerships that widen the set of investment opportunities available to Indian pension funds. For retail investors, this could translate into more robust, long-horizon capital flows that stabilize funding for essential infrastructure and public goods. While the regulatory and policy framework evolves, subscribers may see improved risk-adjusted returns and greater resilience against macro shocks–benefits that can compound over decades. Importantly, these moves complement existing rules and structures around withdrawal and retirement income planning, rather than replacing them.

Practical Steps For Investors: Navigating The Nps And Pension Capital Theme

Retail investors should monitor updates from PFRDA and the ASCEND panel as they unfold. If you're exposed to the NPS or related pension products, consider how broader capital connectivity could influence fund performance and volatility. Diversification remains key: maintain exposure across asset classes and ensure your retirement plan aligns with your time horizon. For stock-level research and deeper insights, explore Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What is ASCEND and what does it stand for?

ASCEND stands for Accelerated Scaling of Global Capital Ecosystem and NPS Development. It is a Pension Fund Regulatory and Development Authority (PFRDA) panel appointed to attract global pension capital and develop the National Pension System (NPS).

Who is leading the ASCEND panel?

Dinesh Khara, the chairman of NPS Trust, will head the ASCEND panel.

What is the main objective of ASCEND?

ASCEND aims to enable Indian pension funds to collaborate with leading global pension funds through co-investment platforms, strategic partnerships, and innovative investment structures, while channeling stable, patient capital into infrastructure and nation-building assets to improve long-term risk-adjusted returns for NPS subscribers.

How large is the NPS as of June 2026?

NPS manages assets of over ₹17.5 trillion (about $185 billion) for nearly 10 crore subscribers. Pension funds under the NPS currently manage assets worth about $185 billion (₹17.5 trillion) for nearly 100 million subscribers.

When did the NPS start and who oversees it?

NPS was launched on 1 January 2004 for new central government employees (except armed forces) and opened to all Indian citizens in May 2009, with NRIs and OCIs later. It is overseen by the Pension Fund Regulatory and Development Authority (PFRDA) under the PFRDA Act, 2013.

Conclusion

For the retail investor, the ASCEND panel signals a potential shift toward more stable, long-term capital flows into India's infrastructure and growth story. The combination of a larger nps assets under management base and global partnerships could improve diversification and long-term risk-adjusted returns for NPS subscribers, while increasing the attractiveness of Indian pension assets to international investors. Next, assess how these macro shifts affect your retirement plan: update your expectations for liquidity, risk, and horizon, and consider integrating thoughtful, long-term stock and bond exposure with the help of a trusted advisor.

Open your trading and demat account here

Reference :

1 : Livemint

SBI Funds Management IPO: Reserved SBI Shareholder Portion, OFS Details, And Retail Outlook

Key Takeaways

- IPO size is Rs 11,693 crore and is entirely an offer for sale with no funds to the company.

- Reserved SBI shareholder portion is up to 1.3 crore shares for SBI's over 38 lakh holders, valued at nearly Rs 750 crore.

- Retail allocation is 35%; QIBs 50%; OFS size over 20 crore shares; SBI selling up to 12.83 crore; Amundi selling up to 7.54 crore (3.7% paid-up); Employee reservation worth Rs 170 crore with Rs 54 per share discount.

- Grey market premium ahead of listing is more than 13% (GMP Rs 649); IPO price Rs 574; Price band Rs 545-574; Listing July 21, 2026; Proceeds to company: None.

Retail investors and SBI shareholders watch as the sbi funds management ipo unfolds in July 2026, a high-stakes move that ties a trusted SBI-backed investment arm to a large exit. The offering is the largest public issue of 2026 so far, with an IPO size of Rs 11,693 crore and a structure that is entirely an offer for sale. No fresh funds go to the company, but the deal reshapes the ownership profile of SBI Funds Management, the investment manager of SBI Mutual Fund. The reserved SBI shareholder portion is up to 1.3 crore shares, valued at nearly Rs 750 crore, reserved for over 38 lakh SBI shareholders who hold valid PAN and an updated PAN in SBI’s register and a demat account. The numbers speak to a targeted, veteran investor base that has long-term ties to SBI's ecosystem.

In this guide, we unpack what this IPO means for retail investors, how allocations are split, and what the GMP signals could imply for a potential listing pop. We also highlight eligibility criteria, timelines, and what to watch for on listing day. For those seeking deeper, stock-specific insights, Swastika offers Swastika's Sarthi AI stock assistant, a resourceful tool for institutional-grade research in retail terms: Swastika's Sarthi AI stock assistant.

Now, let’s dive into the structure and implications of the SBI Funds Management IPO, from who can participate to how the allocations are likely to play out in practice.

What Is The SBI Funds Management IPO And Why It Matters For SBI Shareholders

The sbi funds management ipo represents a strategic exit by Amundi India Holding, with the objective of a partial exit while SBI’s stake remains a meaningful presence in the management of SBI Mutual Fund. The offering is not dilutive to the company’s own balance sheet, since it is entirely an offer for sale. The primary figures you need to track are: a Rs 11,693 crore IPO size; no proceeds to the company; and a reserved SBI shareholder portion up to 1.3 crore shares valued at about Rs 750 crore. Among the SBI ecosystem, more than 38 lakh shareholders are eligible to participate, provided they hold valid PAN and have updated PAN details with SBI’s register and a demat account. The SBI share of paid-up equity capital stands at 6.3%, illustrating SBI’s continued influence even as the exit unfolds.

The listing would mark a major milestone for 2026’s IPO calendar, with the largest public issue so far this year. The IPO structure includes allocations for multiple investor classes: 50% to QIBs, 35% to retail, 10% to Big HNIs, and 5% to Small HNIs. The employee reservation is worth Rs 170 crore, with a discount of Rs 54 per share. The purpose, explicitly stated, is partial exit for Amundi India Holding, while SBI maintains a strategic link through its stake in SBI Funds Management. The overall offering is structured as an exit event rather than a capital-raising exercise, reinforcing investor focus on the quality and liquidity of SBI-related assets.

For retail participants, the key takeaway is the combination of an attractive price band and a strong grey market signal ahead of listing. The price band is Rs 545-574 per share, with the IPO price set at Rs 574 per share. The grey market premium ahead of listing is reported to be more than 13%, with GMP around Rs 649 per share. While GMP is not a guarantee of listing performance, it often reflects market expectations of demand dynamics and post-listing momentum.

In practice, this means retail investors should evaluate both the price band and their own risk tolerance against the backdrop of a premium market for pre-listing trading activity.

For a more structured decision path, consider using Swastika’s Sarthi AI stock assistant to analyze stock-by-stock fundamentals, market sentiment, and risk profiles. Swastika's Sarthi AI stock assistant can provide additional, data-driven context to your subscribe-or-don’t decision.

Key Dates, Price Band, And Allocation For Investors In The SBI Funds Management IPO

The IPO timeline is central to planning. Opening for subscription is set for July 14, 2026, with the closing on July 16. The alloting date is July 17, and the listing date is July 21, 2026. The price band runs from Rs 545 to Rs 574 per share, and the base offer price is Rs 574 per share. The offering constitutes an OFS (offer for sale) up to more than 20 crore shares, with SBI itself selling up to 12.83 crore shares during the process. The allocation scheme prioritizes retail participants (35%), followed by Small HNIs (5%), Big HNIs (10%), and QIBs (50%).

The reserved SBI shareholder portion comprises up to 1.3 crore shares, with an approximate value near Rs 750 crore, allocated to SBI shareholders with 38 lakh eligible holders. The SBI family’s exposure remains notable, accounting for 6.3% of the paid-up equity capital, while Amundi India Holding’s selling offers up to 7.54 crore shares, representing 3.7% of paid-up capital. The employee reservation adds another Rs 170 crore, with a Rs 54 per-share discount, adding an interesting dynamic for eligible employees.

From a practical investor’s perspective, the combination of a robust QIB allocation (50%), strong retail allocation (35%), and a meaningful reserved SBI block creates a layered demand profile that could influence the listing day liquidity and subsequent performance. The GMP signal – Rs 649 – adds color to expectations, but actual listing performance will hinge on broader market conditions and post-listing demand for fund-management exposure tied to SBI, a well-known household brand in India.

For those unfamiliar with the mechanics of OFS, think of the sbi ofs as the instrument used to transfer ownership of existing shares from the selling shareholders to buyers on the exchange, rather than raising fresh capital for the issuer. This nuance matters: the IPO’s proceeds go to the selling shareholders, not to the company, which aligns with the stated objective of a partial exit for Amundi India Holding.

The Red Herring Prospectus date is July 8, 2026, and the eligibility conditions emphasize the need for a valid PAN and PAN updates with SBI’s register, along with a functional demat account. This is a standard compliance framework that ensures alignment of investors with the shareholding ecosystem of a financially stable SBI-linked asset.

Allocation Mechanics, Holdings, And What It Means For Different Investor Classes

Retail investors hold 35% of the allocation in this IPO, a significant share that reflects the broad retail base of SBI Mutual Funds and related financial products. QIBs command the largest slice at 50%, which is a common structure for large public issues and indicates confidence from institution-led demand. The remainder is carved into Small HNIs (5%) and Big HNIs (10%). The presence of Amundi India Holding as a seller adds another dynamic, with up to 7.54 crore shares offering liquidity to the market and a 3.7% stake in paid-up capital. The SBI share of paid-up capital is 6.3%, reinforcing SBI’s ongoing role in the governance of SBI Funds Management.

From the perspective of an individual investor, the key questions include: Will the reserved SBI portion set a benchmark for SBI shareholders who wish to participate, and how will the OFS sizing impact post-listing liquidity? The employee reservation, worth Rs 170 crore, with a discount of Rs 54 per share, is a smaller but meaningful incentive for eligible employees. The prospects for listing-day performance appear supportive, given the GMP signals and the strong appetite for public issues tied to well-known financial services brands.

The sbi funds management listing could become a talking point in the weeks after listing, with market participants watching how the stock behaves in its early days. While GMP provides one lens into pre-listing sentiment, actual trading dynamics will depend on investor demand for SBI’s fiduciary management of mutual funds and the broader market environment. For retail investors looking to participate, ensure you meet PAN and demat requirements and verify PAN updates on SBI’s register to avoid any subscription issues.

How The Reserved SBI Shareholder Portion In The SBI Funds Management IPO Works

The reserved portion for SBI shareholders is capped at 1.3 crore shares, a chunk designed to recognize the longstanding relationship between SBI and the SBI Funds Management arm. With over 38 lakh SBI shareholders eligible for reservation, the value attached to these shares is around Rs 750 crore, assuming the upper-end price band around Rs 574. This reserved pool creates a predictable anchor for SBI stakeholders who want exposure, without the need to participate in the entire public book. Importantly, the reserved portion is subject to PAN verification and demat qualifications, so investors should confirm their PAN status with SBI and ensure demat readiness before applying.

The broader allocation also includes the remaining shares that will be sold to the market through OFS and public allocations, with 50% reserved for QIBs and 35% for retail participants. The inclusion of Amundi India Holding as the selling shareholder adds pressure on the supply side, potentially influencing post-listing liquidity for SBI Funds Management shares. The interplay between reserved SBI shares and outside demand will shape the early-price discovery and the first few days of trading, making this a case study in how large, trust-backed financial brands perform post-listing.

In terms of listing dynamics, the phrase sbi funds management listing has become a talking point among market watchers, as investors weigh the combined influence of a trusted brand, a high-quality asset manager, and the OFS-driven supply. The overall signal remains positive given the GMP premium and the sizable demand seen in similar, large financial services listings in recent memory.

Before subscribing, ensure you have met all eligibility criteria: valid PAN, PAN updated in SBI’s register, and a functioning demat account. The Reserve Bank of India’s capital-market environment for large, asset-backed financial services names also factors into risk considerations–investors should evaluate their own tolerance for volatility around listing and the potential for post-listing volatility in such a high-profile IPO.

What Retail Investors Should Do Now: A Practical Roadmap For The SBI Funds Management IPO

Allotment is scheduled for July 17, with listing on July 21. For retail investors, the core steps are straightforward: verify PAN details with SBI and ensure your PAN is updated; confirm you have a valid demat account; and decide whether the retail allocation aligns with your risk and liquidity needs. Given the GMP dynamics and the fact that the IPO is an offer for sale (with no fresh funds to the company), the decision to subscribe should be guided by expectations of listing-day liquidity and the long-term prospects of the SBI ecosystem that underpins the asset manager.

Additionally, keep a close eye on Amundi India Holding’s selling tranche, which runs up to 7.54 crore shares (3.7% of paid-up capital), and SBI’s own selling cap of 12.83 crore shares in the OFS. These factors influence the immediate post-listing price action and the stock’s ability to sustain gains beyond day one. Retail investors should also consider their risk-reward profile relative to the price band (Rs 545-574) and the base price (Rs 574). Remember, the GMP is a leading indicator of demand expectations, but the actual listing outcome can diverge due to market sentiment, macro conditions, and sectoral rotation.

Related Reads

Frequently Asked Questions

What is the total size and structure of the SBI Funds Management IPO?

The IPO size is Rs 11,693 crore and is entirely an offer for sale, with no fresh funds raised for the company.

How many SBI shareholders are eligible and what is the reserved portion for SBI holders?

Eligible SBI shareholders number over 38 lakh; the reserved SBI shareholder portion is up to 1.3 crore shares, valued at nearly Rs 750 crore.

What are the allocation targets for different investor classes in the SBI Funds Management IPO?

Allocations are 50% to QIBs, 35% to retail investors, 10% to Big HNIs, and 5% to Small HNIs.

What are the key dates and price details for this IPO?

Opening date is July 14, 2026; closing on July 16; allotment on July 17; listing on July 21. Price band is Rs 545-574 with IPO price Rs 574.

What is the grey market signal for the SBI Funds Management IPO?

Grey market premium ahead of listing is more than 13%, with GMP around Rs 649 per share.

What are the eligibility conditions to participate in the SBI Funds Management IPO?

Participants must have a valid PAN and a PAN updated with SBI’s register, and must have a valid demat account.

Conclusion

The SBI Funds Management IPO represents not just a large, sale-based listing but a nuanced alignment of a trusted SBI ecosystem with a global asset manager’s strategic exit. For SBI shareholders and retail investors alike, the reserved portion for SBI’s 38 lakh shareholders, the sizable OFS, and the retail-friendly 35% allocation create a complex but potentially rewarding entry point. With a price band of Rs 545-574 and a listing date set for July 21, 2026, investors should weigh the premium GMP signal against the fact that the proceeds from this IPO go to selling shareholders, not the company. The event could serve as a meaningful read on how high-profile financial services listings behave when anchored by a strong brand and a well-known asset-management platform.

Open your trading and demat account here

Reference :

1 : Economictimes

Tata Motors Share Price Insights From 13 Fallen Giants In Nifty 500

Key Takeaways

- Nifty slid around 10% from its 52-week high, while the broader Nifty 500 declined about 5%.

- 13 Nifty 500 stocks plunged more than 50% from their 52-week highs, with current prices ranging from Rs 25 to Rs 3,211.

- The detailed table below shows each stock's current price, its 52-week high, and the date of that high.

- Retail investors should consider risk management and can explore Swastika's Sarthi AI stock assistant for deeper analysis.

Market moves rarely present clear-cut stories. When 13 Nifty 500 stocks plunge more than 50% from their 52-week highs, the story isn't just about the drop–it's about what lies beneath the price, and what a retail investor should do next.

Data Source: ACE Equity shows that the benchmark Nifty slid around 10% from its 52-week high, while the broader Nifty 500 declined a relatively modest 5% in the same period. Among the declines, 13 names stand out for their sharp reversals. In this piece, we dissect the price action, the context for tata motors share price, and what the numbers imply for risk and opportunity.

Tata Motors Share Price And The 13 Fallen Giants In Nifty 500

As investors monitor tata motors share price and other signals, a pattern emerges: some names, even in a broad market downturn, screen as potential bargains while others reflect fundamental challenges. The 52-week highs set in 2025 show how far some have fallen within 12 months. The current price readings and 52-week highs below provide a reference map for what has moved, what hasn’t, and why.

Reliance Power is trading at Rs 25, down 63% from its 52-week high of Rs 67. The 52-week high was touched on 16-Jul-2025. Cohance Lifesciences is at Rs 431, down 62% from Rs 1,121; its 52-week high was on 17-Jul-2025. Newgen Software Technologies is at Rs 466, down 59% from Rs 1,137; high on 09-Jul-2025. Kaynes Technology India is at Rs 3,211, down 58% from Rs 7,705; high on 07-Oct-2025. KPIT Technologies at Rs 555, down 58% from Rs 1,328; high on 18-Sep-2025. Tata Motors Passenger Vehicles at Rs 332, down 55% from Rs 740; high on 03-Oct-2025. Inox Wind at Rs 83, down 53% from Rs 178; high on 10-Jul-2025. CE Info Systems at Rs 931, down 53% from Rs 1,998; high on 14-Oct-2025. Brainbees Solutions at Rs 207, down 53% from Rs 439; high on 08-Sep-2025. Sapphire Foods India at Rs 184, down 50% from Rs 368; high on 18-Jul-2025. Pine Labs at Rs 142, down 50% from Rs 284; high on 14-Nov-2025. Clean Science at Rs 768, down 48% from Rs 1,490; high on 15-Jul-2025. Zensar Technologies at Rs 451, down 48% from Rs 869; high on 18-Sep-2025.

| Stock | Current Price (Rs) | 52-Week High (Rs) | 52-Week High Date | Drop From 52-Week High |

|---|---|---|---|---|

| Reliance Power | 25 | 67 | 16-Jul-2025 | 63% |

| Cohance Lifesciences | 431 | 1121 | 17-Jul-2025 | 62% |

| Newgen Software Technologies | 466 | 1137 | 09-Jul-2025 | 59% |

| Kaynes Technology India | 3,211 | 7,705 | 07-Oct-2025 | 58% |

| KPIT Technologies | 555 | 1,328 | 18-Sep-2025 | 58% |

| Tata Motors Passenger Vehicles | 332 | 740 | 03-Oct-2025 | 55% |

| Inox Wind | 83 | 178 | 10-Jul-2025 | 53% |

| CE Info Systems | 931 | 1,998 | 14-Oct-2025 | 53% |

| Brainbees Solutions | 207 | 439 | 08-Sep-2025 | 53% |

| Sapphire Foods India | 184 | 368 | 18-Jul-2025 | 50% |

| Pine Labs | 142 | 284 | 14-Nov-2025 | 50% |

| Clean Science | 768 | 1490 | 15-Jul-2025 | 48% |

| Zensar Technologies | 451 | 869 | 18-Sep-2025 | 48% |

All price data reflect last tick in the dataset; Data Source: ACE Equity. The numbers illustrate how quickly price can move relative to a 52-week high, underscoring the importance of valuation discipline and risk management in stock selection.

Despite the declines, some of these stocks belong to businesses with potential in their respective sectors. Kaynes Technology India and Newgen Software Technologies, for instance, show enduring growth opportunities in their domains. The price action should be interpreted with care: for some names, the decline may reflect cyclical pressures rather than a fundamental erosion of value.

Investors seeking deeper insight should consider the Swastika Sarthi AI stock assistant to view fundamentals, price action, and scenario planning for any stock or index, click here: Swastika's Sarthi AI stock assistant.

Broader Market Context: Why The Nifty And Nifty 500 Fell From Their 52-Week Highs

The broader market backdrop matters. The Nifty's ~10% decline from its 52-week high contrasts with a ~5% drop in the Nifty 500, signaling a market where mega-cap leadership and sector rotations influence performance. The price action across the fallen giants reveals that investors are re-pricing risk across segments, with cyclicals and tech-driven names showing the most volatility. For the retail investor, understanding this context helps separate stock-specific drama from macro-driven moves, enabling more informed decisions about entries, exits, and position sizing.

Deep Dive: Price, Drop, And The 52-Week High Dates Of Each Stock

Below is a consolidated view of the 13 stocks in the list, tying together current prices, 52-week highs, dates, and declines. This arrangement makes it easier to spot which names are trading closest to their highs and which have drifted the farthest from them. The table supplements narrative commentary with precise numbers from ACE Equity, presenting a consistent snapshot of market discipline at work.

The 52-week highs date range across the list runs from July 2025 to October 2025, illustrating a window where investor sentiment pinned highs for different reasons. The current prices span from Rs 25 to Rs 3,211, reflecting the wide dispersion in market capitalization and sector exposure within the Nifty 500.

For the record, the data presented above references ACE Equity as the source and the publication date is July 9, 2026. The numbers reflect price action up to that date and are intended to illustrate how the interplay of momentum and fundamentals can reshape investment outcomes over a cycle.

What Retail Investors Can Learn From The Fallen Giants

The central takeaway is not merely the magnitude of declines but how such moves inform your investment process. This set of 13 cases demonstrates that price alone is not a verdict on quality. The challenge for investors is to separate those with durable moats and growth prospects from those facing structural headwinds. A disciplined approach–clear valuation checks, risk controls, diversified exposure, and a defined investment horizon–helps you navigate such environments and avoid overreaction to volatility.

Ultimately, a systematic framework for monitoring price action, fundamental signals, and macro backdrop will help retail investors convert information into decision-ready insights. The fallen giants may highlight aggressive re-pricings or temporary mispricings, but the strategic response should be anchored in your long-term goals and risk tolerance.

Frequently Asked Questions

How many Nifty 500 stocks plunged over 50% from their 52-week highs?

13 stocks are listed in the article: Reliance Power, Cohance Lifesciences, Newgen Software Technologies, Kaynes Technology India, KPIT Technologies, Tata Motors Passenger Vehicles, Inox Wind, CE Info Systems, Brainbees Solutions, Sapphire Foods India, Pine Labs, Clean Science, and Zensar Technologies.

What is the current price of Reliance Power, and how far is it from its 52-week high?

Current price Rs 25; down 63% from its 52-week high of Rs 67; 52-week high touched on 16-Jul-2025.

Which stock had the highest drop from its 52-week high in the list?

Reliance Power is the stock with the highest drop, down 63% from its 52-week high.

When was the 52-week high reached for Kaynes Technology India?

The 52-week high for Kaynes Technology India was reached on 07-Oct-2025.

What market context does the article provide for the Nifty and Nifty 500 declines?

The Nifty declined around 10% from its 52-week high, while the Nifty 500 fell about 5% in the same period.

Conclusion

If you want to stay updated with a structured approach to market signals, remember that the numbers here come from ACE Equity as of the publication date, and real-world prices can vary. The key is to keep a method – the price you see today is a data point in a larger process of valuation, risk assessment, and portfolio construction.

Open your trading and demat account here

Reference :

1 : Economictimes

SBI Share Price Outlook After Banks Q1 Preview: Deposits Rise, Margins Pressure

Key Takeaways

- System-wide deposits grew 12% YoY while credit growth surged to 17.7% as of June 15.

- Motilal Oswal forecasts sbi credit growth to moderate to about 14% by FY27 end.

- NIMs are expected to stay muted with flat PSB margins and 3–8 bps QoQ compression for larger private banks.

- Deposit growth trails loan growth, increasing reliance on wholesale deposits and intensifying low-cost deposit competition.

Can a credit boom outrun shrinking margins for the sbi share price? The Banks Q1 Preview shows deposits up 12% YoY and credit growth accelerating to 17.7% as of June 15, underscoring robust loan demand even as margin pressures creep in for larger lenders. This tension between strong lending and tighter funding costs could shape how retail investors price the sector in the coming quarters.

SBI Share Price And Q1 Preview: What It Signals For Retail Investors

The sbi results preview highlights system-wide deposits growing 12% YoY while sbi credit growth climbs to 17.7% by mid-June. The drivers are clear: higher working capital requirements amid rising input costs, and a surge in corporate borrowings as bond yields rose in Q1FY27. Regulators have shifted focus from the simple credit-deposit ratio toward liquidity metrics such as the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR), which can affect funding costs and, by extension, margins. Motilal Oswal projects sbi credit growth moderating to around 14% by FY27 end, while sbi deposits remain robust, suggesting a more sustainable growth trajectory for the sector.

Analysts note that, despite robust growth, deposit growth continues to trail loan growth, increasing reliance on wholesale deposits. The 0.5% to 5.1% sequential deposit growth range underscores how banks are juggling the challenge of mobilising low-cost funds amidst competition. As a result, the sbi nim (net interest margin) is likely to stay under pressure for larger private banks and remain muted for many lenders in the near term. Axis Securities notes that with the full impact of repo rate cuts already absorbed, NIMs will reflect shifts in product mix while funding costs stay sticky. They expect PSBs to deliver flat NIMs QoQ and larger private banks to see 3–8 bps QoQ compression, a pattern that suggests margins could be steadier for some state-owned lenders.

While the West Asia conflict has not yet translated into an immediate hit to loan books, market participants will watch for early signals in sectors like commercial vehicles and SMEs. This backdrop means retail investors should weigh credit growth momentum against margin resilience when evaluating bank stocks in the sbi share price context.

For more granular stock ideas, Swastika's Sarthi AI stock assistant can help you build a focused watchlist. Swastika's Sarthi AI stock assistant.

Deposits Versus Credit Growth: The 12% Sbi Deposits Story

Across the system, deposit momentum remains robust at about 12% YoY, but loan growth is outpacing deposits, creating a funding gap that banks must finance with wholesale sources. The sbi deposits story matters because it influences funding costs and margins in the Q1 period. The 12% deposits growth is anchored by strong credit expansion, indicating that the system's money multiplier is supporting the lending boom. The deposit-growth gap is a key reason why margins may compress, even as credit growth remains healthy.

Retail investors should watch how banks manage this funding mix; those with stronger retail deposit franchises and steadier NIMs might outperform in a rising rate environment. This dynamic aligns with the sbi nim theme and the broader NIM narrative for the sector.

NIM Outlook: Margin Trends Across PSBs And Private Banks

Industry voices expect margins to stay muted and decline QoQ across most lenders. PSBs may exhibit flat NIMs QoQ, while larger private banks could face 3–8 bps QoQ compression as they shift toward higher-yield lending and costlier funding. This environment suggests the sbi nim trajectory will depend on the ability to balance asset yields with funding costs and capital constraints. The key is to observe how corporate lending, working capital finance, and retail lending mix influence margins in the near term.

Keep an eye on the regulatory environment and the evolving pricing power across loan segments; a disciplined approach to deposit mobilisation and asset quality will be essential to preserving earnings and, by extension, the sbi share price over the longer horizon.

West Asia Conflict And The Banking Sector: Risk Or Not?

Market participants will monitor how events in the West Asia corridor influence loan demand for commercial vehicles and SMEs. While banks have stated no immediate impact on their loan books, any shift in demand patterns or input costs could alter credit metrics and put pressure on margins, affecting valuations of bank stocks including sbi share price. Retail investors should maintain a diversified exposure, focusing on banks with robust deposit franchises and prudent risk management.

What Retail Investors Should Watch In The Coming Months

Key metrics to watch include sbi deposits growth, sbi credit growth momentum, and sbi nim trajectories across lenders, along with the regulatory environment affecting liquidity. The Q1 preview suggests the sector remains in a phase of healthy credit expansion, but margin discipline will be central to sustaining earnings and valuations. Watch for the money multiplier’s strength, changes in wholesale funding costs, and any shifts in corporate borrowings that could influence sbi share price movements.

Related Reads

Frequently Asked Questions

What did the Banks Q1 Preview reveal about system-wide deposits and credit growth?

System-wide deposits grew 12% YoY, while credit growth accelerated to 17.7% as of June 15.

What is Motilal Oswal's projection for sbi credit growth by FY27 end?

Motilal Oswal forecasts sbi credit growth to moderate to around 14% by FY27 end.

How are NIMs expected to move across lenders in the Q1 cycle?

Margins are expected to remain muted and decline QoQ across most lenders; PSBs may have flat NIMs QoQ while larger private banks could see 3-8 bps QoQ compression.

Is there an immediate impact from the West Asia conflict on banks' loan books?

Banks say there is no immediate impact, but market participants will monitor segments like commercial vehicles and SMEs for signs.

What should investors watch regarding the sbi share price after the Q1 preview?

Watch the balance between sbi deposits growth, sbi credit growth, and sbi nim trends, along with regulatory liquidity metrics that affect funding costs and valuation.

Conclusion

As always, stay disciplined, validate assumptions with a diversified set of data points, and align your portfolio with your risk tolerance and time horizon.

Open your trading and demat account here

Reference :

1 : Ndtvprofit

Infosys Share Price And Crisil Q1FY27 Revenue Outlook

Key Takeaways

- India Inc's Q1FY27 revenue growth is estimated at 11–11.5% YoY, the fastest pace in eight quarters and the highest in two years.

- Pricing gains drive revenue growth across sectors, with margins contracting 75–100 bps YoY as airlines and tyres face cost pressures.

- Aluminium revenue grows 51–53% YoY; Automobiles 22–24%; Power 8–10%; Telecom 10–11%; FMCG 6–7%; Pharma ~12%; IT ~5%; Cement 6–8%; Construction 1–3%.

- Three drivers will shape the trajectory: price pass-through, volume protection, and normalisation of fuel, freight, feedstock, and packaging, with monsoon dynamics influencing rural demand.

Infosys share price has long served as a quick signal of IT sector health, and Crisil Intelligence's fresh Q1FY27 data show a broader narrative for Indian Inc across 400+ companies and 47 sectors. Revenue growth is estimated at 11–11.5% YoY, the fastest pace in eight quarters and the highest in two years, supported by pricing gains and resilient domestic demand. For investors watching IT leadership, the infosys share price remains a handy proxy to gauge sector sentiment as Crisil Intelligence maps profits, pricing trends, and demand across the economy.

Crisil Intelligence Q1FY27 Revenue Growth Across Indian Sectors: An 11–11.5% Rise

Crisil Intelligence covers more than 400 companies across 47 sectors, excluding banking, financial services and oil & gas, representing nearly half of India’s listed market capitalization. The revenue growth estimate for Q1FY27 (quarter ended June 30, 2026) sits at 11–11.5% year-on-year, the fastest pace in eight quarters and the highest in two years. While uncertainties around crude oil and gas affected fuel, freight, packaging and feedstock costs, domestic demand held up reasonably well, allowing many companies to pass higher costs on to end-consumers.

According to Sehul Bhatt of Crisil Intelligence, For much of the past two years, revenue growth was powered largely by volume.

Reference :

1 : Economictimes

Pricing emerged as the primary driver this time, contributing more to revenue growth than volume in sectors such as aluminium, steel, cement, airlines, fertilisers and gems and jewellery. Aluminium producers benefited from supply disruptions and firmer global prices, with primary aluminium revenue estimated to have surged 51–53% YoY, supported by lower import availability, higher regional premiums and capacity additions. Other sector gains include Automobiles at 22–24%, Power generation at 8–10%, and Telecom services at 10–11%; FMCG rose 6–7%, Pharmaceuticals around 12%, IT services about 5%, Construction 1–3%, and Cement 6–8%.

Despite the revenue surge, aggregate EBITDA margins contracted by 75–100 basis points YoY in the June quarter. Airlines faced an aviation turbine fuel-led cost escalation, resulting in an estimated ~1,000 basis points decline in EBITDA margin; Tyre makers experienced a 200–300 basis point squeeze owing to higher costs for natural rubber, carbon black and synthetic rubber. The evolving macro environment–ranging from energy prices in West Asia to domestic demand drivers–will continue to be a key variable for Indian corporates in the quarters ahead.

Pricing-Led Revenue Growth Across Key Sectors In Q1FY27

The pricing impulse was broad-based, helping sectors navigate higher input costs. In particular, aluminium, steel, cement, airlines, fertilisers and gems and jewellery benefited from price gains that helped offset cost pressures. The Crisil Intelligence dataset highlights significant sectoral variance in growth dynamics, reinforcing the view that where price pass-through is effective, revenue growth can be sustained even as input costs remain volatile. The southwest monsoon’s progress will also influence rural demand and food inflation, which in turn affects consumption-led sectors such as FMCG and pharmaceuticals.

From a stock-specific lens, investors often monitor Infosys share price to gauge IT sector momentum. The IT services segment grew about 5% in Q1FY27, buoyed by favourable currency movements. In practice, the price environment for IT stocks, including infosys stock price nse and infosys stock price history, can amplify or dampen the broader earnings narrative depending on currency trends and client spend patterns. The infosys share price target is one of several indicators analysts use to calibrate near‑term momentum, while Infosys quarterly results typically drive short‑term price action. For investors seeking deeper, institutional-grade insights, Swastika offers Swastika's Sarthi AI stock assistant as a decision-support tool.

Margin Contraction In The Face Of Revenue Growth: EBITDA And Sectoral Pain Points

Margin dynamics reflect the pressure from higher costs even as revenues rise. Aggregate EBITDA margins contracted 75–100 basis points YoY in Q1FY27, underscoring that revenue growth alone does not guarantee profitability. Airlines faced an especially sharp margin decline due to aviation turbine fuel costs, while tyre makers saw a squeez e of 200–300 basis points on elevated synthetic and natural rubber costs. These sectoral disparities emphasise the need for disciplined pricing, operational efficiency, and targeted cost management as input costs normalise over time. The net effect is a more complex profitability landscape where pass-through potential and cost control determine the trajectory of margins across industries.

Three Key Drivers Shaping The Trajectory For Indian Corporates

The Crisil Intelligence forecast points to three critical levers that will shape corporate performance in the coming quarters: 1) The extent of further price increases and their impact on demand; 2) The ability of companies to protect volumes while recovering higher costs; 3) The pace at which pressures in fuel, freight, feedstock and packaging begin to normalise. The interaction of these factors will determine how quickly margins recover to pre-shock levels and how sustainable revenue growth remains across cycles. Higher-cost inventory already in the system could keep replacement costs elevated and trigger another round of margin pressure before profitability begins to fully normalise.

Southwest Monsoon, Rural Demand, And Food Inflation: The Hidden Force Behind Consumption-Led Sectors

The evolution of the southwest monsoon will be a critical driver of rural demand and food inflation, shaping consumption-led sectors such as FMCG, consumer durables, and even some pharma segments. In periods of strong monsoons, rural households tend to increase expenditure, supporting demand for everyday essentials; a weak monsoon can suppress rural consumption and raise price pressures. Geopolitical developments in West Asia remain a key variable for Indian corporates as energy prices react to regional tensions, influencing input costs and global supply chains.

Infosys Share Price Context In The IT Sector: Currency Benefits And Price Pass-Through

The IT services revenue growth of around 5% YoY benefits from currency movements, which can influence relative stock performance. For investors tracking technology names, the infosys stock price nse and the infosys stock price history provide quick read-throughs on momentum in the IT space. The infosys share price target among analysts varies, reflecting differing near-term currency and order-book expectations; Infosys quarterly results have historically driven price movements, while the infosys dividend policy can affect returns for IT investors. For deeper stock insights, consider Swastika's Sarthi AI stock assistant.

Related Reads

- Infosys share price: A Retail Investor's Guide to Navigating the Indian Market

- Infosys Share Price Signals In July 2026: IT Sector Pulse And Market Liquidity

- Infosys Share Price And The Indian Growth Reboot: Large-Cap Leaders In Focus

Frequently Asked Questions

What is Crisil Intelligence's estimate for Q1FY27 revenue growth in Indian Inc?

11–11.5% year-on-year, the fastest pace in eight quarters and the highest in two years.

How many companies and sectors does Crisil Intelligence cover and what does it represent?

More than 400 companies across 47 sectors, excluding BFSI and oil & gas; representing nearly half of India’s listed market capitalization.

Which sectors recorded the strongest revenue growth in Q1FY27 and by how much?

Aluminium 51–53%; Automobiles 22–24%; Power generation 8–10%; Telecom services 10–11%; FMCG 6–7%; Pharmaceuticals around 12%; IT services around 5%; Cement 6–8%; Construction 1–3%.

What margins trend did Crisil Intelligence observe in Q1FY27?

Aggregate EBITDA margins contracted 75–100 basis points year-on-year; airlines faced about a 1000 basis points decline; tyre makers experienced a 200–300 basis point squeeze.

What are the three key drivers that will shape corporate performance going forward?

The extent of further price increases and their impact on demand; the ability to protect volumes while recovering higher costs; and the pace at which pressures in fuel, freight, feedstock and packaging normalise, with monsoon dynamics also playing a role.

Conclusion

This article was published without a generated conclusion. Please review and add a conclusion before publishing.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App