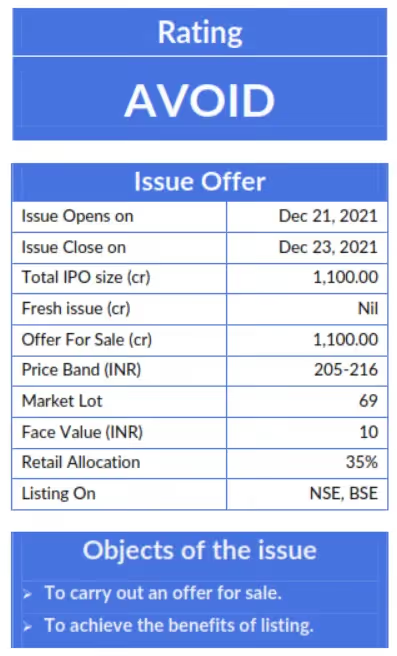

IPO Review

CMS Info Systems Limited IPO : Outlook & Valuation

.webp)

In December, CMS Info Systems Limited IPO was listed. Incorporated in 2008, CMS Info Systems Limited is India's largest cash management company in terms of the number of ATM points and retail pick-up points as of March 31, 2021.

The company is engaged in installing, maintaining, and managing assets and technology solutions on an end-to-end outsourced basis for banks, financial institutions, organized retail as well as e-commerce companies in India.

CMS Info Systems Limited Business Operates in 3 Segments:

- Cash management services.

- Managed services i.e. banking automation product sales, common control systems, and software solutions, etc.

- Others i.e. financial cards issuance for banks and card personalization services.

In the first place, CMS integrated business platform is supported by customized technology and process controls.

In addition CMS enables it to offer its customers a wide range of tailored cash management and managed services solution.

The Company caters to a broad set of outsourcing requirements for banks, financial institutions, organized retail as well as e-commerce companies in India.

firstly, the demand for cash and cash related services in India has increased, banks and other participants in India are increasingly outsourcing their ATM operations and management.

Secondly, As of August 31, 2021, it has a network of 3,965 cash vans , 238 branches , offices to cover all of India's states , union territories and covering 97.04% of India’s 742 districts, 14,949, or 77.46%, Indian postal codes.

At last the revenue of the cash management market in India grew from approximately ₹10.0 billion in the Fiscal Year 2010 to approximately ₹27.7 billion in the Fiscal Year 2021, a CAGR of 10.88%

Outlook & Valuation:

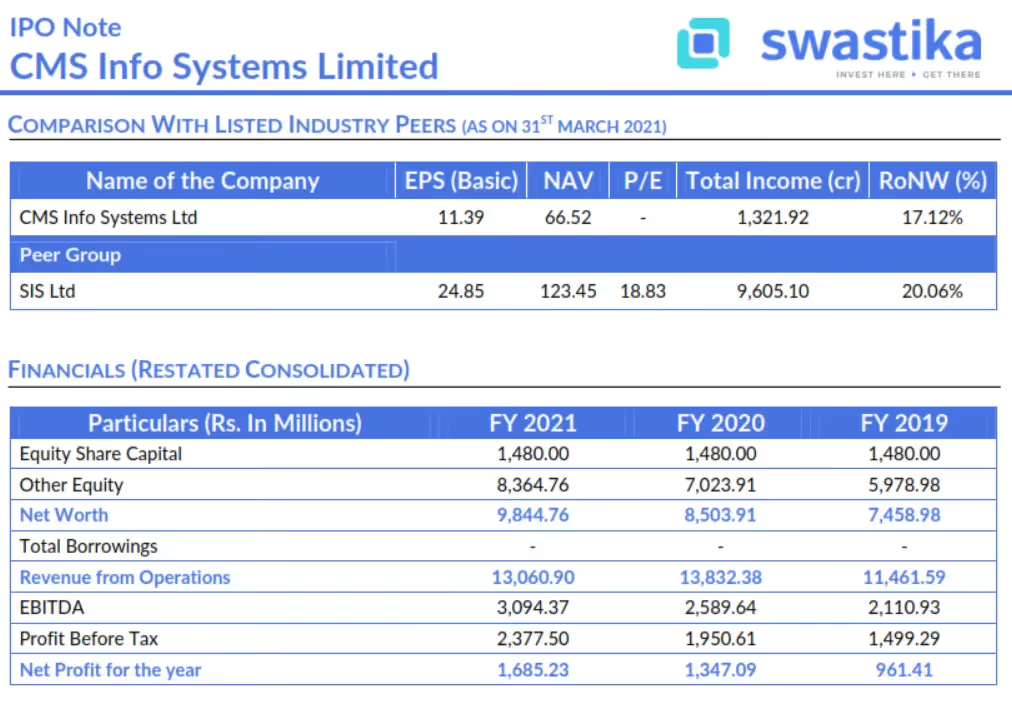

Despite consistent growth in revenues, we saw a decline in FY21 which can be attributed to COVID-19. According to the company, the revenue in FY20 was Rs. 1388.29 Crores and fell to Rs 1321.92 crore in FY21.

However, the company has improved its net profit from Rs. 134.7 crore in FY 20 to Rs. 168.52 crore in FY 2021. Also the company has stable financial performance and increasing margins.

In the first place, the risk of market volatility needs to be considered right now on the back of rising cases from the omicron variant.

As the government focuses on digital payments, a further decrease in the use and availability of cash can have an adverse effect on business activities.

The IPO is priced at a PE of 19x to its FY21 EPS of Rs 11.09 and a P/BV of 3.24x on the NAV of Rs 66.52, which is in line with its listed peers. Thus we assign an "Avoid" rating to the IPO.

KEY MANAGERIAL PERSONNEL

- Shyamala Gopinath is the Chairperson and an Independent Director of the Company. She has been associated with the Company since November 13, 2017. In the past, she has served as the Deputy Governor of the RBI

- Rajiv Kaul is the Executive Vice Chairman, Whole Time Director and CEO of the Company. He is currently heading the Company and is responsible for the overall management of the Company. He has over 24 years of experience across technology, private equity and cash management industry.

- Pankaj Khandelwal is the President and Chief Financial Officer of the Company. He is currently responsible for the finance, legal as well as secretarial functions of the Company. He is a qualified chartered accountant from ICAI with over 27 years of experience.

- Praveen Soni is the Company Secretary and Compliance Officer of the Company. He has been associated with the Company since July 1, 2009. He has over 16 years of experience in secretarial as well as legal practices.

- Manjunath Rao Pare Parmeshwar is the President- Managed Services Business. He has been associated with the Company since July 6, 2012. He has over 34 years of experience in sales and marketing across sectors.

- Anush Raghavan is the President- Cash Management Business of the Company. He has over 14 years of experience in business management and business development.

- Sanjay Singh is the Chief Human Resources Officer of the Company. He has been associated with the Company since July 26, 2021

- Rohit Kilam is the Chief Technology Officer of the Company. He has over 20 years of experience in IT across sectors.

COMPETITIVE STRENGTHS

- Leading player in a consolidating market with strong fundamentals.

- Pan-India footprint with deep penetration in growing markets.

- Longstanding customer relationships with increased business opportunities.

- Integrated business platform offering a broad range of services and products.

- Track record of strong productivity and operational excellence.

- Experienced and highly qualified management team.

KEY STRATEGIES

- Drive operational efficiencies and increase profitability.

- Expand into business areas that create synergies with the current business.

- Enhancing the organizational capabilities.

KEY CONCERNS

- Company entire IPO proceeds (Rs 1,100 Crores) is Offer for Sale.

- India has moved to digitization post demonetization.

- The company business is highly dependent on the banking sector in India.

- Company business has affected by covid-19 pandemic and it can affect in future too.

- The company derives a substantial portion of its revenue from the limited number of customers.

Data Patterns (INDIA) Limited IPO

RatingSUSBCRIBE Issue OfferIssue Opens onDec 14, 2021Issue Close onDec 16, 2021Total IPO size (cr)588.22Fresh issue (cr)240.00Offer For Sale (cr)348.22Price Band (INR)555-585Market Lot25Face Value (INR)2Retail Allocation35%Listing OnNSE, BSEObjects of the issue ⮚ For Repayment of borrowings ⮚ For Funding working capital requirementIssue Break-up (%)QIB Portion 50NIB Portion 15Retail Portion ⮚ 35Shareholding (No. of Shares)Pre Issue 47,784,086Post Issue 51,886,650Indicative TimetableFinalisation of Basis of Allotment 21-12-2021Refunds/Unblocking ASBA Fund 22-12-2021Credit of equity shares to DP A/c 23-12-2021Trading commences 24-12-2021

Established in 1985, Data Patterns is a defence and aerospace electronics solutions provider specializing in indigenously designed defence equipment. The firm provides equipment for all types of defence and aerospace systems, including space, air, land, and sea.

Electronic hardware design and development, software and firmware design and development, mechanical design and development, product prototype design and development, functional testing and validation, environment testing and verification, and engineering services opportunities are among the company's core competencies.

⮚ It was one of the fastest-growing firms in terms of revenues among significant Indian defence and aerospace companies between Fiscal 2019 and Fiscal 2021, according to the Company Commissioned F&S Report, with a revenue increase of 71%.

⮚ The company's strengths throughout the gamut of defence and aerospace electronics solutions from design to delivery give it a considerable competitive edge in terms of overall development time and cost, as well as competitive pricing when bidding on defence and aerospace contracts.

⮚ The company has design capabilities across the entire spectrum of strategic defence and aerospace electronics solutions including processors, power, radio frequencies (“RF”) and microwave, embedded software and firmware and mechanical engineering.

⮚ The company is upgrading and expanding its facility, with a proposed doubling of available floor area and manufacturing capacity, as well as the addition of large and heavy equipment handling capability, large radar and mobile electronic warfare system integration, and a satellite integration facility. Its testing capabilities are also proposed to be further strengthened.

Outlook & Valuation:

In the last 3 years, the company has shown strong growth in revenue where it grew at a CAGR of 19% from Rs 132.50 cr to Rs 226.55 cr over the period of FY19 to FY21, during the same period profit has grown at a CAGR of 97% from Rs 7.70 cr in FY19 to Rs 54.6 cr in FY21. The margins of the company are also expanding.

As part of the 'Make in India' initiative, the company will bid on bigger, more challenging contracts. Data Patterns increased its net profitability by approximately 158% between FY20 and FY21.

We believe that the company has enormous potential to grow rapidly thanks to the government's focus on Defense and Aerospace. The IPO is priced at a 49x PE and 13x P/BV to its FY21 earnings at an upper price band of Rs 585. Attractiveness in the defence sector is likely to boost sentiment for the IPO.

IPO Note

DATA PATTERNS (INDIA) LIMITED

KEY MANAGERIAL PERSONNEL

⮚ Srinivasagopalan Rangarajan is the Chairman and Managing Director of the Company. He has been associated with the Company since its incorporation. He holds a Bachelor’s Degree of Technology in Chemical Engineering and he has over three decades of experience in business development, corporate affairs, finance and marketing.

⮚ Venkata Subramanian Venkatachalam is the Chief Financial Officer of the Company. He is a fellow member of the Institute of the Chartered Accountants of India. He has over two decades of experience in the finance sector.

⮚ Manvi Bhasin is the Company Secretary and Compliance Officer of the Company. She is an associate of the Institute of the Company Secretaries of India. She has three years of experience in legal and secretarial matters.

⮚ Vijay Ananth K is the Chief Operating Officer and Chief Information Security Officer of the Company. He has more than two decades of experience in software engineering and product management.

⮚ Desinguraja Parthasarathy is the Chief Technical Officer of the Company. He has 32 years of experience in Product Development.

⮚ Thomas Mathuram Susikaran is the Senior Vice President-Business Development. He holds a bachelor’s degree in engineering. He has over 21 years of experience in business development and marketing.

⮚ Nandaki Devi Ramachandracharya is the Deputy General Manager and Management Representative Quality Management System. She has 22 years of experience in test engineering.

COMPETITIVE STRENGTHS

⮚ Integrated and strategic defence and aerospace electronics solutions provider based in India, well-positioned to profit from the Make in India initiative.

⮚ Innovation focused business model.

⮚ Sound order book with orders from several prestigious customers in the Indian defence ecosystem. ⮚ The modern certified manufacturing facility of international standards.

⮚ Track record of profitable growth.

⮚ The experienced management team and skilled workforce.

KEY STRATEGIES

⮚ Continue expansion of product portfolio with complex technology-based products.

⮚ Focus on repeat large volume production orders.

⮚ Improving manufacturing infrastructure and enhancing design and development capabilities

⮚ Augmenting the design and development capabilities and expanding manufacturing infrastructure

⮚ Focus on increasing revenues by leveraging core competencies and growing the services business

⮚ Focus on increasing export business

KEY CONCERNS

⮚ The company depends on a limited number of customers for major business.

⮚ Subject to strict quality requirements, customer inspections and audits, and any failure to comply with quality standards may lead to cancellation of existing and future orders

⮚ Failure to qualify for or win bids could have an adverse effect on its business.

⮚ If it does not maintain its technical information and processes discreet, it may lose its competitive advantage.

⮚ The company has significant working capital requirements.

IPO Note

DATA PATTERNS (INDIA) LIMITED

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2021)

Name of the Company EPS (Basic) NAV P/E Operational Rev (cr) RoNW Data Patterns (India) Ltd 11.89 44.38 49 223.95 26.79% Peer Group MTAR Technologies Ltd 16.99 154.99 83.56 246.43 9.66%Astra Microwave Products Ltd 3.33 64.51 51.28 640.91 5.16%Centum Electronics Ltd 13.31 173.14 34.90 817.43 5.40%Bharat Electronics Ltd 8.62 45.39 23.49 14,108.69 18.99%

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Millions) FY 2021 FY 2020 FY 2019Equity Share Capital 17.00 17.00 17.00Other Equity 2060.70 1517.95 1311.93Net Worth 2077.70 1534.95 1328.93Total Borrowings 332.21 605.66 601.33Revenue from Operations 2239.50 1560.98 1310.63EBITDA 945.88 472.50 269.93Profit Before Tax 745.34 284.29 103.59Net Profit for the year 555.71 210.48 77.02

HP Adhesives IPO : Outlook & Valuation

Issue Offer

Issue Opens on Dec 15, 2021Issue Close on Dec 17, 2021 Total IPO size (cr)125.96 Fresh issue (cr) 113.44 Offer For Sale (cr) 12.53 Price Band (INR) 262-274 Market Lot 50 Face Value (INR)10 Retail Allocation 10% Listing On NSE, BSE

Objects of the issue

⮚ For funding the working capital.

⮚ Capital expenditure for expansion.

Issue Break-up (%)

QIB Portion 75 NIB Portion 15 Retail Portion 10

⮚ Shareholding (No. of Shares)

Pre Issue1,42,34,947Post Issue1,83,74,947

Indicative Timetable

Finalization of Basis of Allotment 22-12-2021 Refunds/Unblocking ASBA Fund 23-12-2021 The credit of equity shares to DP A/c 24-12-2021 Trading commences 27-12-2021

Registered in 2019, HP Adhesives Limited is an adhesives and sealants company. The company manufactures a wide range of consumer adhesives and sealants such as PVC, cPVC, and uPVC solvent cement, synthetic rubber adhesive, PVA adhesives, silicone sealant, acrylic sealant, gasket shellac, other sealants, and PVC pipe lubricants.

These adhesives and sealant products have applications in multiple industries such as plumbing and sanitary, drainage and water distribution, general-purpose building/ construction, and interior operations as well as for glazing operations, woodwork, footwear, automotive, foam-furnishing, and other varied industries.

⮚ Apart from the above products, the company also sells ancillary products like ball valves, thread seals, and other tapes and FRP products for drainage and architectural solutions.

⮚ The company has grown from a single product to a multi-product adhesives company with sales across India (through a pan-India distribution network) and also in international markets.

⮚ Over the years, Company’s brands “HP” and “Strong Weld” in the PVC adhesives product category have gained increasing acceptance on account of high product quality and efficient pricing.

⮚ The company has a solid business model that focuses on consistently expanding its product portfolio by introducing new product categories and SKUs to cater to a wide range of end-use applications and selling them through its distribution network across India.

⮚ As of September 30, 2021, its distribution network comprised of 4 depots situated in Delhi, Kolkata, Bengaluru, and Indore and more than 750 distributors who cater to more than 50,000 dealers in India

⮚ The company wants to expand its manufacturing capacity at Village Narangi, Raigad, Maharashtra to cater to the growing demand for several product categories.

Outlook & Valuation:

In the last 3 years, the company has shown stable growth in revenue where it grew from Rs 87.97 cr to Rs 123.87 cr over the period of FY19 to FY21, during the same period profit has grown from Rs 4 cr in FY19 to Rs 10.05 cr in FY21, but the company faced a huge loss of Rs. (4.67) cr in FY20 on the back of exceptional item.

The industry is expected to grow at a CAGR of 6-8% while the company is in a growth phase and is expanding installed capacities for its product lines and is also expanding its portfolio.

The IPO is valued at a PE of 35x and P/BV of 28x to its FY21 earnings. However, if we annualized FY22 earnings PE and P/BV work out to be 81x and 10.38x which is in line with the peer. Due to its small size, the SME-IPO is going to be listed in the T2T segment.

We have an "AVOID" rating for the IPO.

For additional information & risk factors please refer to the Red Herring Prospectus

IPO Note

HP ADHESIVES LIMITED

KEY MANAGERIAL PERSONNEL

⮚ Anjana Haresh Motwani, with over 40 years of experience in the adhesive industry, is currently designated as the Executive Director and Chairperson of the Company.

⮚ Karan Haresh Motwani currently holds the position of Managing Director of the Company. He was admitted to the partnership M/s. HP International in 2007.

⮚ Mr Mihir Shah, is the chief financial officer of the Company. He has been associated with the Company since May 2021. He has an overall experience of nearly 15 years in investment banking.

⮚ Ms Jyoti Nikunj Chawda is the Company Secretary & Compliance Officer of the Company. She is a commerce and law graduate from the University of Mumbai and holds an overall experience of nearly 7 years in secretarial and compliance functions.

⮚ Ms Nidhi Haresh Motwani is the Vice President – Operations of the Company, She has been associated with the Company since February 2016. She has an overall experience of 10 years in the fields of branding, marketing, and sales.

⮚ Mr Saurabhraj Bhatt is the Vice President – Sales and Marketing, of the Company. He has an overall experience of about 22 years. He handles the product promotion, branding, sales, and marketing functions of the Company.

⮚ Mr. K. P. Unnikrishnan is the Assistant Vice President – New Product Development of the Company. He has a multi-functional experience of 36 years

⮚ Mr. Sabrinath Gopalkrishnan Nair is the Senior Manager – Purchase of the Company. He has experience of over 28 years in accounts, inventory control and logistics operations.

COMPETITIVE STRENGTHS

⮚ Consistently growing company with established brand presence

⮚ Wide Product Portfolio and Multiple SKUs

⮚ Focusing on multiple end-user industries

⮚ Extensive distribution network across India catering to customers.

⮚ Efficient manufacturing set-up with scope for expansion

⮚ Effective quality checks

⮚ R&D set up for constant product improvement and new product development

KEY STRATEGIES

⮚ Further, strengthen brand image

⮚ Expansion of manufacturing facility

⮚ Further expansion of distribution network across India and globally

KEY CONCERNS

⮚ The impact of the COVID-19 pandemic on business and operations is uncertain.

⮚ The company does not have any long-term arrangements with its distributors.

⮚ Restrictions on the import of raw materials may adversely impact the business.

⮚ Prices of the principal raw materials are subject to changes in the prices of crude oil.

⮚ The company has incurred losses in the recent past.

IPO Note

HP ADHESIVES LIMITED

COMPARISON WITH LISTED INDUSTRY PEERS (AS OF 31ST MARCH 2021)

Name of the Company EPS (Basic) NAV P/E Total Income (Mn) RoNW (%)HP Adhesives Limited 7.74 9.74 35 118.16 79%Peer GroupPidilite Industries Limited 22.26 114.78 81.28 7293.00 114.78

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Lakh) FY 2021 FY 2020 FY 2019Equity Share Capital 1,300.00 1,300.00 1,300.00Other Equity (34.12) (1,051.56) 166.23Net Worth 1,265.88 248.44 1,466.23Total Borrowings 3,138.52 3,405.98 2,358.33Revenue from Operations 11,816.16 9,547.93 8,741.75EBITDA 1,768.67 691.95 870.09Profit Before Tax 1,323.02 (536.06) 405.91Net Profit for the year 1,005.96 (467.05) 400.07

Medplus Health Services Limited IPO

Rating SUBSCRIBE Issue Offer Issue Opens on Dec 13, 2021Issue Close on Dec 15, 2021Total IPO size (cr) 1,398.30Fresh issue (cr) 600.00Offer For Sale (cr) 798.30Price Band (INR) 780-796Market Lot 18Face Value (INR) 2Retail Allocation 35%Listing On NSE, BSE

Objects of the issue

⮚ For funding working capital requirement of the subsidiary.

⮚ For general corporate purposes. Issue Break-up (%)QIB Portion 50NIB Portion 15Retail Portion

⮚ Shareholding (No. of Shares)Pre Issue 111,761,165Post Issue 119,305,676

Indicative Timetable

Finalisation of Basis of Allotment 20-12-2021Refunds/Unblocking ASBA Fund 21-12-2021Credit of equity shares to DP A/c 22-12-2021Trading commences 23-12-2021

Incorporated in 2006, Medplus Health Services is India's second-largest pharmacy retailer in terms of the number of stores and revenue.

The company offers pharmaceutical and wellness products i.e. medicines, vitamins, medical devices, test kits, and fast-moving consumer goods i.e. home and personal care products, baby care products, sanitisers, soaps, and detergents, etc.

It is also the first pharmacy retailer in India to offer an omnichannel platform wherein customers can purchase products through stores, place orders over the telephone, online orders, and a Click and Pick facility.

⮚ According to the Technopak Report, it is India's first pharmaceutical retailer to offer an omnichannel platform. This approach aims to broaden and expand the Company's client base while also enhancing "convenience" as a primary customer value proposition and retaining customers inside its ecosystem.

⮚ As of September 30, 2021, we operated 546 stores in Karnataka, 475 stores in Tamil Nadu, 474 stores in Telangana, 297 stores in Andhra Pradesh, 224 stores in West Bengal, 221 stores in Maharashtra and 89 stores in Odisha.

⮚ The company has an established track record of delivering strong financial performance. Between the financial year 2019 and financial year 2021, total revenue from operations grew at a compound annual growth rate (“CAGR”) of 16.21% from ₹22,727.37 million to ₹30,692.69 million.

⮚ The company’s business operations across the entire value chain are backward integrated and are wholly managed and operated by itself. The company's operations are supported by its technology-driven supply chain and distribution infrastructure, which is arranged in a hub-and-spoke model and gives it a strong foundation and substantial power to continue to grow.

Outlook & Valuation:

Over the period of FY19 to FY21, company revenue increased from Rs 2,284.94 crore to Rs 3,090.81 crore, while profits grew from Rs 11.92 crore in FY19 to Rs 63.11 crore in FY21 with only a slight dip in FY20.

Margins of the company are increasing slowly.

The company is the second-largest pharmacy retailer in India which offers an omnichannel platform. After a dismal performance for FY20, the company posted super earnings recently.

The company has low margins, but it is expanding. We believe that there are growth opportunities in the industry and might perform better over the period. There are no listed peers and IPO is arriving at a PE of 71x to its annualized FY22 earnings.

Prima-facie the valuation looks expensive but over the period of time, we believe the company's growth may justify its valuation.

IPO Note

MEDPLUS HEALTH SERVICES LIMITED

KEY MANAGERIAL PERSONNEL

⮚ Ganga Madhukar Reddy is the Managing Director and Chief Executive Officer of the Company. He is one of the Promoters of the Company and has been a Director of the Company since its incorporation on November 30, 2006. He holds a bachelor’s degree in medicine and surgery and a master’s degree in business administration.

⮚ Cherukupalli Bhaskar Reddy is the Chief Operating Officer – outlet operations of the company. He joined the company on March 1, 2007. He has over 14 years of experience in the pharmaceutical industry.

⮚ Surendranath Mantena is the Chief Operating Officer – MedPlus Mart of the company. He joined the company on October 1, 2010.

⮚ Hemanth Kundavaram is the CFO of the company. He joined the company on January 2, 2021. He has over 15 years of experience in corporate finance and accounting in various industries.

⮚ Parag Jain is the company secretary and compliance officer of the company. He joined the company on March 10, 2014. He has 14 years of experience as a company secretary.

⮚ Atul Gupta is the Non-Executive Director of the company. He has over 13 years of experience in the investment industry.

⮚ Murali Sivaraman is the Non-Executive Independent Director of the company. He was previously associated with Philips Lighting.

COMPETITIVE STRENGTHS

⮚ India’s Second Largest Pharmacy retailer Company.

⮚ Strong brand name and customer value proposition.

⮚ Successful Track Record of Expansion Using a Distinct Cluster-based and Replicable Store Unit Expansion Approach

⮚ High-Density Store Network Enhancing Omni-channel Proposition

⮚ Lean Cost Structure and Technology-Driven Operations

⮚ Well Qualified, Experienced and Entrepreneurial Board and Senior Management Team

⮚ Strong promoter background and an experienced and entrepreneurial management team

BUSINESS STRATEGIES

⮚ Strengthen the Market Position by Increasing Store Penetration in Existing Clusters and Developing New Cluster

⮚ Further Develop the Omni-channel Platform with a Hyper-local Delivery Model

⮚ Increase the Share of Private Labels and Enhance the Stock Keeping Unit (“SKU”) Mix

⮚ Continue to Increase Operating Efficiency and Enhance Supply Chain Management to Drive Profitability

⮚ Enhance Revenue and Increase Customer Wallet Share.

KEY CONCERNS

⮚ Changes in prescription medicine prices and commercial terms may have a negative impact on their business.

⮚ Their company, subsidiaries, promoters, and directors are involved in ongoing legal procedures.

⮚ Privacy and security rules govern the use and sharing of personally sensitive information, especially personal health information.

⮚ Their financial success may be harmed if they will not effectively manage inventory and forecast demand.

⮚ Any negative news or occurrence related to the Indian pharma industry may have a negative impact on their business.

IPO Note

MEDPLUS HEALTH SERVICES LIMITED

COMPARISON WITH LISTED INDUSTRY PEERS

There are no listed companies in India that engage in a business similar to that of the Company. Accordingly, it is not possible to provide an industry comparison in relation to the Company

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Millions) FY 2021 FY 2020 FY 2019 Equity Share Capital 4.48 1.94 1.94Other Equity 7,301.05 5,276.08 2,911.43 Net Worth 7,305.53 5,278.02 2,913.37 Total Borrowings 1,352.35 1,050.51 1,044.02 Revenue from Operations 30,692.69 28,706.03 22,727.37 EBITDA 2,382.13 1,509.62 1,313.47 Profit Before Tax 950.98 293.59 227.51 Net Profit for the year 631.11 17.94 119.22

C.E Info Systems Limited IPO

Rating SUSBCRIBE Issue Offer Issue Opens on Dec 09, 2021Issue Close on Dec 13, 2021 Total IPO size (cr) 1,039.61Fresh issue Nil Offer For Sale (cr) 1,039.61Price Band (INR) 1,000-1,003 Market Lot 14 Face Value (INR) 2Retail Allocation 35%Listing On NSE, BSE

Objects of the Issue

⮚ For achieving the benefits of listing on the stock exchanges.

Issue Break-up (%)QIB Portion 50NIB Portion 15Retail Portion 35

C.E. Info systems limited (MapmyIndia) is a leading provider of advanced digital maps, geospatial software, and location-based IoT technologies in India. The company is a data and technology products and platforms company, offering proprietary digital maps as a service (MaaS), software as a service (SaaS), and platform as a service (PaaS). The company provides products, platforms, application programming interfaces (APIs), and solutions across a range of digital map data, software, and IoT for the Indian market under the (MapmyIndia) brand, and for the international market under the (Mappls) brand.

⮚ Company provide 2D and 3D visual and voice-based navigation platforms that are interactive, capable of outdoor and indoor map rendering, location search, geocoding and reverse geocoding, as well as traffic and turn-by-turn route planning optimization.

⮚ Its geo-analytics services assist customers in a variety of industries in analyzing their markets and developing prediction models using geographical patterns offered by them. These services also give consumers with near-real-time dashboarding and monitoring capabilities.

⮚ Company’s IoT platform, ‘InTouch’, enables connectivity with real world sensors, phones and IoT devices. It provides a wide range of applications for near real-time vehicle and asset tracking, geo fencing alerts, historical movement and driver behavior analysis, predictive vehicle health alerts, as well as fleet, transport and logistics management

⮚ The company's digital maps comprehensively cover India; approximately its digital maps cover 6.29 million kilometers of roads in India, representing 98.50% of India’s road network.

Outlook & Valuation:

Shareholding (No. of Shares)Pre Issue 53,242,967Post Issue 53,242,967

Indicative Timetable

Finalisation of Basis of Allotment 16-12-2021Refunds/Unblocking ASBA Fund 17-12-2021Credit of equity shares to DP A/c 20-12-2021Trading commences 21-12-2021

The company has shown stable growth in revenue, where it grew from Rs 163.35 cr to Rs 192.27 cr over the period of FY19 to FY21, over the same period profit, has grown from Rs 33.56 cr in FY19 to Rs 59.43 cr in FY21 with a minor dip in FY20. MapmyIndia is the leader in digital mapping in India and has an early mover advantage. We believe that new edge technology including SaaS, PaaS, and MaaS platform providers has a sparkling future for the next few years. The company serves various industries and sectors which is also a positive. The company saw stable revenue growth in the last few years where the margins have improved too also there are no listed peers currently. The IPO is arriving at a PE of 93x and P/BV of 15x on FY21 earnings, being the first mover the company is seeking higher valuation.

IPO Note

C.E. INFO SYSTEMS LIMITED

KEY MANAGERIAL PERSONNEL

⮚ Rakesh Kumar Verma is the Chairman and Managing Director of the Company. He co-founded this Company along with Rashmi Verma in 1995 and has significant experience as an entrepreneur in the field of digital maps and geospatial information technologies.

⮚ Rohan Verma is the Whole-time Director and the CEO of the Company. He joined this Company in 2007 and worked in various capacities and was appointed as CEO of the Company with effect from April 1, 2019.

⮚ Anuj Kumar Jain is the Chief Financial Officer of the company and has been associated with the company since May 2011. He has significant experience in the field of finance, taxation, and accounting.

⮚ Saurabh Surendra Somani is the Company Secretary and Compliance Officer of the company with effect from July 27, 2021. He has significant experience in the fields of legal, secretarial and listing compliance.

⮚ Rashmi Verma is the co-founder and chief technology officer of the company. Prior to founding the company, she worked in the U.S.A., including with the IBM Corporation till 1988. She has significant experience as an entrepreneur in the fields of information technology, management, and the geospatial industry, and digital mapping in India.

⮚ Shishir Verma is the senior vice-president, human resources and corporate affairs, and had joined the company on January 17, 2014. He has to look after corporate and legal affairs of the company.

COMPETITIVE STRENGTHS

⮚ Pioneers of digital mapping in India having an early mover advantage.

⮚ Leading the B2B and B2B2C market for digital maps and location intelligence in India.

⮚ Market position built around proprietary technology and network effect resulting in strong entry barriers.

⮚ Independent, global geospatial products and platforms company with strong data governance. ⮚ Prestigious customers across sectors with strong relationships.

⮚ Profitable business model with consistent financial track record, high operating leverage and strong cash flows.

KEY BUSINESS STRATEGIES

⮚ Continue to scale and expand the customer reach leveraging market presence in India.

⮚ Augment company products, platforms and the technology lead.

⮚ Drive expansion in international markets and geospatial sector

⮚ Pursue selective strategic acquisitions and investments to grow their business

KEY CONCERNS

⮚ The entire proceeds of the IPO is Offer for Sale. Means, the IPO proceeds would go to selling shareholders and company would not get anything except for listing gains.

⮚ Part of the business is dependent on the performance of the auto sector in India. Any adverse changes in the conditions affecting this sector can impact the business.

⮚ Company’s inability to maintain or update its map database or errors in its map database could harm the reputation of the company.

⮚ Company depends on a limited number of customers for a significant portion of its revenues.

⮚ Company is dependent on trends in the sectors where enterprise customer operates.

IPO Note

C.E. INFO SYSTEMS LIMITED

COMPARISON WITH LISTED INDUSTRY PEERS

There are no listed companies in India that engage in a business similar to that of the Company. Accordingly, it is not possible to provide an industry comparison in relation to the Company

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Millions) FY 2021 FY 2020 FY 2019Equity Share Capital 38.33 38.33 38.33Convertible Preference Shares 1,289.64 1,289.64 1,289.64Other Equity 2,252.01 1,649.43 1,524.03Net Worth 3,579.97 2,977.39 2,851.99Total Borrowings 5.90 8.80 0.00Revenue from Operations 1,524.63 1,486.29 1,352.55EBITDA 543.24 371.87 404.60Profit Before Tax 787.66 315.96 418.02Net Profit for the year 594.33 231.95 335.66

Metro Brands Limited IPO

Rating

SUSBCRIBE (Only Long-Term Investors)Issue Offer

Issue Opens on Dec 10, 2021Issue Close on Dec 14, 2021Total IPO size (cr) 1,367.51Fresh issue 295.00Offer For Sale (cr) 1072.51Price Band (INR) 485-500Market Lot 30Face Value (INR) 5Retail Allocation 35%Listing On NSE, BSE

Objects of the issue

⮚ For meeting Capex requirements.

⮚ For general corporate purposes.Issue Break-up (%)QIB Portion 50NIB Portion 15Retail Portion 35

Established in 1955, Metro Brands Limited is one of the largest Indian footwear speciality retailers. Customers' footwear demands are met by a diverse assortment of branded products of Company for men, women, unisex, and children, as well as for various events. The company targets the mid and premium segments in the footwear market which have a higher presence of organized players and growth in the overall footwear industry. Metro, Mochi, Walkway, Da Vinchi, and J. Fontini, as well as Crocs, Skechers, Clarks, Florsheim, and Fitflop, are among the company's well-known brands. The company follows the "company owned and company operated" (COCO) model of retailing through their own Multi Brand Outlets (MBOs) and Exclusive Brand Outlets (EBOs), to manage their stores.

⮚ The company’s total store count has grown from 504 in 116 cities as of March 31, 2019, to 586 stores across 134 cities as of March 31, 2021, and to 598 stores across 136 cities as of September 30, 2021, also Company had the third-highest number of exclusive retail outlets in India, in Fiscal 2021

⮚ The company also offers accessories such as belts, bags, socks, masks and wallets, at its stores. It also offers foot care and shoe care products at stores through its joint venture, M.V. Shoe Care Private Limited, making it a ‘one-stop-shop’ for all footwear and related accessories for customers.

⮚ In Fiscal 2021, In-Store Product Sales, Online Product Sales, and Omni-Channel Product Sales represented 91.93%, 6.15%, and 1.09%, of the Company’s revenue from operations, respectively.

⮚ The company’s retail operations are carried out through stores and distributors as well as through online channels. It primarily follows the ‚company owned and company operated‛ (COCO) model of retailing through its own Multi Brand Outlets (MBOs) and Exclusive Brand Outlets (EBOs), to better manage customer experience at stores.

Outlook & Valuation:

The company's revenue dropped by 33% in the

Shareholding (No. of Shares)

Pre Issue 265,607,426Post Issue 271,507,426

Indicative Timetable

Finalisation of Basis of Allotment 17-12-2021Refunds/Unblocking ASBA Fund 20-12-2021Credit of equity shares to DP A/c 21-12-2021Trading commences 22-12-2021

Year FY21 to Rs 878 cr from Rs 1311 cr in FY20 on the back of the Covid-19 pandemic. Similarly, profit also declined from Rs. 160.5 cr in the year FY20 to Rs. 64.61 cr in the FY21. The margin of the company was flat in FY19 and FY20 while it dropped since COVID. Metro Brands Limited has demonstrated its growth, profitability, and financial discipline in the past as one of India's leading pan-India footwear retailers. The sector is mostly under-rated and may see a re-rating. The majority of their revenue is from third parties and the company has an asset-light business model however we believe that the IPO is priced aggressively. The IPO is arriving at PE of 205x and P/BV of 16x while if we annualized the FY22 earnings PE works out to be 157x.

SME-IPO Note

METRO BRANDS LIMITED

KEY MANAGERIAL PERSONNEL

⮚ Rafique A. Malik is the Chairman of the Company’s Board. He has been associated with this Company as a director since January 19, 1977. He has over 50 years of experience in the field of footwear retail.

⮚ Farah Malik Bhanji is the Managing Director of the Company. She has been associated with the Company as a director since December 5, 2000. She has over 20 years of experience in the field of footwear retail.

⮚ Mohammed Iqbal Hasanally Dossani is the Whole-time Director of the Company. He holds a bachelor’s degree in commerce, Financial Accounting and Auditing.

⮚ Utpal Hemendra Sheth is the Non-Executive Director of the Company. He holds a bachelor’s degree in commerce. He was first appointed as an alternate director in the Company on March 14, 2007.

⮚ Manoj Kumar Maheshwari is the Independent Director of the Company. He has been associated with the Company as an Independent Director since July 24, 2009.

⮚ Aruna Bhagwan Advani is the Independent Director of the Company. She has been associated with the Company as an Independent Director since July 27, 2010.

⮚ Arvind Kumar Singhal is the Independent Director of the Company. He has been associated with the Company as an Independent Director since August 12, 2016.

⮚ Vikas Vijaykumar Khemani is the Independent Director of the Company. He has been associated with the Company as an Independent Director since March 12, 2019. He is an associate of the Institute of Chartered Accountants of India

⮚ Tina Srikanth Velamakanni is the Independent Director of the Company. He has been associated with the Company as an Independent Director since March 25, 2021.

COMPETITIVE STRENGTHS

⮚ One of India's largest footwear retailers brands.

⮚ Wide range of brands and products catering to all occasions across age groups and market segments

⮚ Efficient operating model through deep vendor engagements and TOC based supply chain.

⮚ Asset light business with an efficient operating model leading to sustained profitable growth

⮚ Presence across multiple formats and channel

⮚ Strong track record of growth and profitability and financial discipline

⮚ Strong promoter background and an experienced and entrepreneurial management team

KEY STRATEGIES

⮚ Expand the store network in existing and new Indian cities.

⮚ Increase the contribution of e-commerce and omnichannel sales as a proportion of the sales.

⮚ Expand the portfolio of accessories and grow other allied businesses

KEY CONCERNS

⮚ The ongoing COVID-19 epidemic has had a substantial impact on their business.

⮚ All of their stores and warehouses are leased spaces.

⮚ For the production of all the items they sell, they rely on third parties.

⮚ They may not be effective in maintaining and increasing brand visibility.

⮚ The selling of third party brands accounts for a major amount of their revenues.

For additional information & risk factors please refer to the Red Herring Prospectus

IPO NoteMETRO BRANDS LIMITEDCOMPARISON WITH LISTED INDUSTRY PEERS (AS OF 31ST MARCH 2021)Name of the Company EPS (Basic) NAV P/E Total Income (Mn) RoNW (%)Metro Brands Limited 2.43 31.17 205 8,785.38 8.24Peer GroupBata India Limited (6.95) 136.79 - 18,025.65 (5.08)Relaxo Footwears Limited 11.74 63.29 118 23,819.20 18.54FINANCIALS (RESTATED CONSOLIDATED)Particulars (Rs. In Millions) FY 2021 FY 2020 FY 2019Equity Share Capital 1,327.67 1,327.67 1,327.67Other Equity 6,948.03 6,745.22 5,170.99Net Worth 8,275.70 8,072.89 6,498.66Total Borrowings 14.06 115.23 98.56Revenue from Operations 8,000.57 12,851.62 12,170.65EBITDA 1709.3 3535.1 3373.3Profit Before Tax 845.05 2,184.17 2,281.28Net Profit for the year 646.19 1,605.75 1,527.30

Shriram Properties Limited IPO

RatingSUSBCRIBE (Only Aggressive Investors)Issue OfferIssue Opens on Dec 08, 2021Issue Close on Dec 10, 2021Total IPO size (cr) 600Fresh issue 250Offer For Sale (cr) 350Price Band (INR) 113-118Market Lot 125Face Value (INR) 10Retail Allocation 10%Listing On NSE, BSEObjects of the issue ⮚ For repayment of borrowings. ⮚ For general corporate purposes.Issue Break-up (%)QIB Portion 75NIB Portion 15Retail Portion 10⮚ Shareholding (No. of Shares)Pre Issue 148,411,448Post Issue 169,597,889Indicative TimetableFinalisation of Basis of Allotment 15-12-2021Refunds/Unblocking ASBA Fund 16-12-2021Credit of equity shares to DP A/c 17-12-2021Trading commences 20-12-2021

- Incorporated in 2000, Shriram Properties is a part of the Shriram Group and is one of the leading residential real estate development companies in South India.

- The company primarily focuses on the mid-market and affordable housing segments. The company is also present in the mid-market premium and luxury housing categories as well as commercial and office space categories.

- Bengaluru and Chennai are the key markets for the company. The company also has operations in Coimbatore, Visakhapatnam, and Kolkata. It is among the top five residential real estate companies in South India in terms of the number of units launched between the calendar years 2012 and the third quarter of 2021 across Tier 1 cities of South India including Bengaluru, Chennai and Hyderabad.

- It is a part of the Shriram Group, which is a prominent business group with four decades of operating history in India and a well-recognized brand in the retail financial services sector and several other industries.

- The company has been focused on the mid-market and affordable housing categories as its target segment within the residential housing market. The mid-market and affordable housing categories have accounted for a significant share of overall market absorption in India in recent years. According to the JLL Report, these housing categories accounted for 75.00%, 72.00% and 74.00% of overall residential unit absorption during calendar years 2018, 2019 and 2020, respectively.

- As of September 30, 2021, it has a total portfolio of 35 projects in Ongoing Projects, Projects under Development and Forthcoming Projects aggregating to 46.72 million square feet of estimated Saleable Area.

Outlook & Company Valuation:

The company's financials have been on a weaker note where revenues of the company are declining while the company turned loss-making since FY20. The company's revenues in FY19 were Rs. 723 cr, which fell to Rs 501 cr in FY21, while it made a profit of Rs 48 cr in FY19 and a loss of Rs 67 cr in FY21.

Despite strong brand recognition, the company has suffered losses during the COVID, when real estate and housing were booming. Being a loss-making company retail portion is 10%.

The SME IPO is arriving at a P/BV of 2.09x while the industry average is 3.69x which might attract minor listing gain. However, we believe that there are many reputable listed companies such as Sobha, Brigade, Prestige, etc., and only "AGGRESSIVE INVESTORS" should apply for the IPO.

IPO Note

SHRIRAM PROPERTIES LIMITED

KEY MANAGERIAL PERSONNEL

⮚ M. Murali is the Chairman and Managing Director and individual Promoter of the Company. He has over 17 years of work experience with this Company and was first appointed as a Director on March 30, 2003.

⮚ S. Natarajan is a Non-Executive Director of the Company.

He is a member of the Institute of Chartered Accountants of India since 1975. He has been associated with the Shriram group for over 17 years and has been a Director of the Company since March 30, 2003.

⮚ Raphael Dawson is a Non-Executive Nominee Director of the Company. He has more than 15 years of work experience.

⮚ Gautham Radhakrishnan is a Non-Executive Nominee Director of the Company. His career has been exclusively in private equity and corporate finance.

⮚ T.S. Vijayan is an Independent Director of the Company. He has many years of experience in the insurance sector and was formerly the Chairman of the Life Insurance Corporation of India.

⮚ K.G. Krishnamurthy is an Independent Director of the Company. He has over 38 years of experience in the real estate sector.

⮚ Anita Kapur is an Independent Director of the Company. She has been a director of the Company since November 14, 2018.

⮚ Professor R. Vaidyanathan is an Independent Director of the Company. He has been a director of the Company since December 13, 2018.

COMPETITIVE STRENGTHS

⮚ Part of the Shriram Group and Backed by Marquee Investors.

⮚ One of the Leading Residential Real Estate Development Companies in South India with a Focus on Mid-market and Affordable Housing Categories.

⮚ Demonstrated Capabilities in Project Identification and Strong Execution Track Record

⮚ Established Strategic Relationships

⮚ Scalable and Asset Light Business Model supported by our Strong Financial Position

⮚ Well Positioned to Benefit from Regulatory and Industry Developments

⮚ Experienced and Professional Management Team

⮚ The company has strong, proven capabilities in the identification and execution of projects.

KEY CONCERNS

⮚ Their business is capital intensive and is significantly dependent on the availability of real estate financing in India.

⮚ Shortages or disruption in the supply of labor and key building materials could affect the estimated construction cost and timelines.

⮚ They depend on landowners or developers for obtaining certain regulatory approvals for the development management business any failure in that may adversely affect the business.

⮚ The Indian real estate sector is heavily regulated. Changing laws, rules and regulations and legal uncertainties.

⮚ An increase in competition in the Indian real estate sector may adversely affect profitability.

⮚ The company has a significant amount of debt which could affect its ability to obtain future financing or pursue its growth strategy.

IPO Note

SHRIRAM PROPERTIES LIMITED

COMPARISON WITH LISTED INDUSTRY PEERS

Name of the Company EPS (Basic) NAV P/E P/BV Total Income (mn)c Shriram Properties Limited (4.60) 56.44 - 2.09 5,013.08 Peer Group Sobha Limited 6.57 255.97 133.13 3.32 21,904.00Prestige Estates Projects Limited 36.32 166.52 12.86 2.68 75,018.00Brigade Enterprises Limited (2.24) 111.32 - 4.08 20,103.90Godrej Properties Limited (7.48) 299.32 - 6.70 13,330.90Oberoi Realty Limited 20.33 257.68 45.29 3.24 20,905.87Sunteck Realty Limited 2.98 19.75 160.64 2.28 6,308.42

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Millions) FY 2021 FY 2020 FY 2019Equity Share Capital 1,481.10 1,481.10 1,481.10Other Equity 6,791.78 7,459.82 8,215.10 Net Worth 8,272.88 8,940.92 9,696.20Total Borrowings 7,271.69 7,372.47 8,456.65 Revenue from Operations 5,013.08 6, 318.43 7,237.80 EBITDA 1,210.53 904.14 799.30Profit Before Tax (452.00) (816.58) 829.21 Net Profit for the year (674.80) (864.25) 480.62

Aditya Birla Sun Life AMC IPO

IPO Note

Aditya Birla Sun Life AMC Limited

- Incorporated in 1994, Aditya Birla Sun Life AMC is set up as a joint venture between ABCL and Sun Life AMC. The company managed a total AUM of ₹2,736.42 billion under mutual funds (excluding our domestic FoFs), portfolio management services, offshore and real estate offerings, as of June 30, 2021.

- The company has automated and digitized several aspects of its operations including in relation to customer onboarding, online payments and other transactions, fund management, dealing, accounting, customer service, data analytics, and other functions.

- The company is the largest non-bank affiliated Asset Management Company (AMC) in India by quarterly average assets under management (QAAUM) since 31 March 2018 and is among the four largest AMCs in India by QAAUM since 30 September 2011.

- Geographically diversified pan-India distribution presence covering 284 locations spread over 27 states and six union territories. The company’s distribution network is extensive and multi-channelled with a significant physical as well as digital presence, and included over 66,000 KYD-compliant MFDs, over 240 national distributors and over 100 banks/financial intermediaries, as of June 30, 2021.

- The company managed 118 schemes comprising 37 equity schemes (including, among others, diversified, tax saving, hybrid and sector schemes), 68 debt schemes (including, among others, ultra-short- duration, short-duration and fixed-maturity schemes), two liquid schemes, five ETFs and six domestic FoFs, as of June 30, 2021.

- Total QAAUM (excluding our domestic FoFs) has grown over the years and was ₹2,654.54 billion, ₹2,672.68 billion, ₹2,465.22 billion and ₹2,464.80 billion as of June 30, 2021, and March 31, 2021, 2020 and 2019, respectively.

KEY MANAGERIAL PERSONNEL

- A Balasubramanian is the Managing Director and Chief Executive Officer of the Company and has been associated as an employee in the Company since 1994.

- Mahesh Patil is the Chief Investment Officer who holds a bachelor’s degree in engineering from the University of Bombay and a master’s degree in management studies from the University of Bombay and has been associated with the company since 2005.

- Bhavdeep Bhatt is the Head - Retail Sales and holds a bachelor’s degree in commerce from Bhavnagar University and a master’s degree in business administration from Bhavnagar University and has been associated with the company since 2008.

- Anil Shyam is the Head - Alternate Business and holds a bachelor’s in commerce and master’s in finance & control from Himachal Pradesh University, Shimla and has been associated with the company since 2007.

- Parag Joglekar is the Chief Financial Officer and holds a bachelor’s degree in commerce from the University of Bombay. He is a member of the Institute of Chartered Accountants of India and is a member of the Institute of Cost and Works Accountants of India and has been associated with the company since 2006.

- Keerti Gupta is the Chief Operations Officer and holds a bachelor’s degree in science (home science) from Rajasthan Agriculture University, Bikaner, and a master’s degree in business administration from Maharishi Dayanand Saraswati University, Ajmer and has been associated with the company for the last 25 years.

- Vikas Mathur is the Head - Institutional Sales and holds a bachelor’s degree in electronics and communication engineering from the University of Madras, a postgraduate diploma in business entrepreneurship and management from the Indian Institute of Planning and Management and a master’s degree in business administration from the International Management Institute and has been associated with the company since 2008.

COMPETITIVE STRENGTHS

- Largest Non-bank Affiliated Asset Manager in India.

- Well-Recognized Brand with Experienced Promoters.

- Growing Individual Investor Customer Base Driven By Strong Systematic Flows and B-30 Penetration.

- Diverse Product Portfolio with Fund Performance supported by Research Driven Investment Philosophy.

- Geographically diversified pan-India distribution presence that is not only extensive but multi-channeled, with a significant physical as well as a digital presence.

- Franchise Led By Experienced and Stable Management and Investment Teams.

- Long-term Track Record of Innovation in and Use of Technology.

KEY CONCERNS

- The COVID-19 pandemic has had, and we expect it to continue to have, a material adverse effect on business.

- Revenue and Profit are largely dependent on the value and composition of the AUM of the schemes managed by us and any adverse change in our AUM may result in a decline in our revenue and profit.

The SME-IPO is purely OFS based where the company will not get anything from proceeding.

- Their market share might be eroded by competition from existing and future market competitors offering investment products.

- They rely heavily on the strength of their brand and reputation to succeed.

- The regulatory environment in which we operate is subject to change.

COMPARISON WITH LISTED INDUSTRY PEERS (As of 31st March 2021)

Name of the CompanyEPS (Basic)NAVP/EP/BRoNW (%)Aditya Birla Sun Life AMC Limited18.2759.1938.912.0230.87Peer GroupHDFC Asset Management Company Limited62.16224.2850.914.227.76Nippon Life India Asset Management Limited11.0450.2938.48.621.94UTI Asset Management Company Limited38.97255.3130.14.315.27

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Millions)FY 2021FY 2020FY 2019Equity Share Capital180.00180.00180.00Other Equity16,866.1312,988.7312,025.65Net Worth17,046.1313,168.7312,205.65Revenue from Operations11,910.2812,338.3514,060.67EBITDA7,388.877,026.926,839.03Profit Before Tax6,958.886,607.296,457.67Net Profit for the year5,262.804,944.024,467.99

Outlook & Company Valuation

The AMC industry has grown tremendously in recent years on the back of strong flows by the individuals as the AMC companies are increasing penetration across geographies. Also, the tech easiness is helping the millennials to get access to AMC easily.

- At the upper price band of Rs 712, the PE works out to be 33x based on annualized FY22 earnings which are slightly lower than peers. So there is room for minor listing gain also the IPO is purely OFS based.

- Thus, we assign a “SUBSCRIBE” rating to the IPO for the long-term investors. We believe that going forward the company will get benefit as the millennials are keen into the stock market and we have seen tremendous account opening which will lead to flow in AMC too.

Exxaro Tiles IPO

Exxaro Tiles is a company that specializes in the marketing and production of vitrified tiles. It was founded in 2008. Exxaro Tiles has a product range that includes over 1000 distinct tile designs in six sizes.

The firm's well-known products include the Galaxy Series, Topaz Series, and High Gloss Series. The firm produces glazed vitrified tiles composed of ceramic elements such as quartz, clay, and feldspar, as well as double charge vitrified tiles (double layer pigment).

Large infrastructure projects, such as educational, hotels, educational institutions, government, and hospitals, are also served by the firm.

About the IPO

A pre-IPO placement of up to 22 lakh shares may potentially be considered by the firm.

According to the DRHP, the SME IPO would be for up to 1.34 crore shares, with a fresh issuance of 1.12 crore shares and a Dixit kumar Patel offer for the sale of up to 22.38 lakh shares.

The fresh issue's net proceeds would be used to repay debt, finance working capital requirements, and for general company reasons.

Objectives

- To repay or prepay secured borrowings that the firm has taken out.

- To satisfy the needs for working capital.

- Meeting the needs of the company as a whole.

Strength:

- The company has one of India's largest glazed vitrified tile production facilities.

- The company offers a wide range of vitrified tile designs in various sizes.

- Across India, one company has a substantial presence in 27 states.

- With over 2,000 registered dealers, it boasts a huge dealer network.

- It exports to more than 13 nations across the world.

Allocation:

Up to 50% of the shares will be allocated for qualified institutional purchasers, while 15% will be designated for non-institutional investors; the remaining 35% will be reserved for retail investors.

Employees will be entitled to a part of the offer.

Risks to be aware of:

- Supply and pricing fluctuation in raw materials, stores, and spares may have a negative impact on the company's business, financial condition, and results of operations.

- The company's failure to satisfy its working capital requirements might have a negative impact on its financial results.

- The company's failure to develop or manage its distribution network for commercial purposes, or the loss of any key dealer, might have a negative impact on its business and financial performance.

- Failure to satisfy its debt financing commitments might have a negative impact on the company's business, results of operations, and cash flow.

Strategies

- Enhance the brand's value.

- Increase sales through upgrading manufacturing capacity.

- Purchasing materials on an outsourced basis.

- Expanding dealer networks in existing markets and increasing export presence.

- Continue to increase operating efficiencies by implementing new technologies and opening your own gas station.

IPO Details

Subscription Dates4 – 6 August 2021 Price Band INR 118 – 120 per share Fresh issue 11,186,000 shares Offer For Sale 2,238,000 shares Total IPO size 13,424,000 shares Minimum bid (lot size) 125 shares Face Value INR10 per share Retail Allocation 35% Listing On NSE, BSE

Recommendation

In the fiscal year ending March 2021, the company's top five customers contributed 36.34 per cent of revenue, while the top ten customers accounted for 40.76 per cent of the top line. The Group continues to work to improve its position in the business world by establishing successful verticals.

Through its more than 2,000 registered dealers, it generates over 86 per cent of its income from the domestic retail and institutional market.

The remaining 13.88 per cent of total income comes from exports, the firm has no long-term commitments with any of its institutional clients, resulting in a hazy picture of its order book in the future.

The firm requires a significant quantity of operating capital to continue expanding.

The company's failure to manage its working capital requirements might have a detrimental impact.

We advocate investing in the Stock IPO for the reasons stated above.

Devyani International Ltd IPO

About Devyani International Ltd:

Devyani International Ltd is the largest Yum Brands franchisee in India and one of the country's leading operators of chain quick-service restaurants (QSR).

As of March 31, 2021, the company had 655 outlets in 155 cities across India. Yum! Brands Inc. owns and runs KFC, Pizza Hut, and Taco Bell restaurants around the world, with over 50,000 locations in more than 150 countries.

About the IPO:

Devyani International IPO subscriptions will begin on August 4th and end on August 6th, 2021. The additional offering of up to Rs. 1,838 crores in the Initial Public Offering of Equity Shares.

The new issuance was reported as raising up to Rs 440 crore and offering up to 155,333,330 equity shares for sale.

The offer's price range has been set at Rs 86–90 per share.

The IPO constitutes an offer for sale of up to 155.33 million shares by the existing shareholders and promoters as well as an Rs440 crore fresh issue.

Objectives of the IPO:

The objectives of the Devyani International IPO are:(i) Repayment of all borrowings(ii) General corporate purposes

RJ Corp Ltd owns the company are up to 90 million. While Dunearn Investments Mauritius Pte is owned the company up to 65.34 million shares, The proceeds of the offering will then be used to repay some or all of the firm's debts.

The total outstanding borrowings of its Company (on a consolidated level) were 541.59 Crores as of June 2021. Devyani is India's largest quick-service restaurant (QSR) company to be listed on Swiggy and Zomato in 2019-2020

Investment bankers that are been appointed for the Issue are as follows :

- Kotak Mahindra Capital Company Ltd,

- Motilal Oswal Investment Advisors Ltd,

- CLSA India Pvt Ltd,

- Edelweiss Financial Services Ltd.

Devyani International IPO details Subscription Dates 4 – 6 August 2021Price BandINR86 – 90 per share Fresh issueINR440 crore Offer For Sale155,333,330 shares (INR1,335.87 – 1,398 crore)Total IPO sizeINR1,775.87 – 1,838 crore Minimum bid (lot size)165 shares Face Value INR1 per share Retail Allocation 10% Listing On NSE, BSE

Strength

- The product portfolio of reputed QSR brands financial discipline, a competitive advantage.

- Yum Brands' is the largest franchisee in India.

- Cross-brand synergies provide you with more operating leverage.

- Significant emphasis on cash flow management.

Risks

- Revenues falling from Rs 542 crore in FY20 to Rs 284 crore in FY21.

- The company's auditors had expressed concern about audited financial statements.

- The majority of the stores are located on leased sites because of which renting costs are incurred

- The company had 297 Pizza Hut locations, 264 KFC locations, and 44 Costa Coffee Locations as of March 31, 2021, in India.

- The core brand stores grew from 469 to 605 outlets between March 2019 and March 2021 which is about 13.58 percent.

Company Strategies

- Core Brands Business's shop network should be strategically expanded

- Invest in technology and place a strong emphasis on digital capabilities

- Continue to increase performance

- Focus on Core Brands' delivery channel

IPO Issue Allocation:

- For QIB the issue allocation is not More than 50% of the offer

- For NII the issue allocation is not less than 15% of the offer

- For Retail, the issue allocation is not less than 35% of the offer

Recommendation:

The company is a major QSR player with well-known international brands. However, the company has experienced a net loss in recent years as a result of high advertising costs, license fees, and commissions.

With the current euphoria in the stock market and IPO listings, one can subscribe to the IPO. Despite the epidemic, it has continued to develop its shop network, opening 109 outlets in the last six months across its core brand business.

KFC and Pizza Hut were among the first to provide contactless delivery in May 2020 and June 2020, respectively.

It is expected that considerable interest will be seen through this IPO. It also provides listing gains. With an increasing number of individuals ordering food or visiting restaurants, future growth appears to be optimistic.

Krsnaa Diagnostics IPO Ltd

Krsnaa Diagnostics Ltd provides a comprehensive variety of technology-enabled diagnostic services to public and private hospitals, medical institutions, and community health centres across India, including imaging (including radiology), pathology/clinical laboratory, and teleradiology. Across many divisions, the company delivers high-quality, all-inclusive diagnostic services at reasonable prices. Krsnaa Diagnostics Ltd's Initial Public Offering (IPO) will commence for bidding on August 4, 2021, and end on August 6, 2021. A new offering of Rs 400 crore will be part of the company's IPO. It also includes an offer by the company's existing promoters and shareholders to sell up to 8.53 million or 85.30 lakh shares. PHI Capital Growth Fund will sell 1.6 million or 16 lakh shares, Kitara PIIN 1104 will sell up to 3.34 million or 33.4 lakh shares, Somerset Indus Healthcare Fund I Ltd will sell up to 3.56 million or 35.6 lakh shares, and Lotus Management Solutions will sell up to 21,380 shares in the Offer for Sale (OFS).

About the IPO

Krsnaa Diagnostics plans to raise Rs 1,213.33 crore through its first public offering. The issue is made up of a new issue of Rs 400 crore and an offer for sale (OFS) for Rs 813.33 crore, comprising 8,525,520 equity trading shares having a face value of Rs 5 each. On August 3, a day before the IPO opens for subscription, all anchor reservations will take place. The issue price range was Rs 933 to Rs 954 per equity share, with a face value of Rs 5 per share. It's an IPO with a book-built issue. The offering has a grey market premium of Rs 400, implying that the shares are trading on the unlisted market at a premium of Rs 1,333 to Rs 1,354 per share. The minimum lot size for the Krsnaa Diagnostics IPO is 15 shares, with an associated application fee of Rs 14,310. On the top end of the lot, there are 195 shares with a Rs 186,030 application amount. Retail investors can apply for up to 13 lots at the higher end of the lot size for this issue.

Strength

For starters, it is one of India's most well-known diagnostic chains. The company's financial picture. It also provides a broad and diversified variety of diagnostic services because of its complicated network and presence in 13 locations, it has a large market footprint. In addition, the firm has a solid financial track record.

Objectives

- A proposal to funding the establishment of diagnostics centres in Punjab, Karnataka, Himachal Pradesh, and Maharashtra.

- Repayment/prepayment, in whole or in part, of our Company's borrowings from banks and other financial institutions.

- General business objectives

Strategies:

- Continually grow our footprint in India

- Expand diagnostic services with an emphasis on specialist diagnostics

- Increase your digital footprint

- Maintain a high level of social impact

- Continue to increase profit and efficiency

- Opportunistic purchases expand business and geography.

Investment allocation:

When it comes to investment allocations, the retail part is only 10%. The SME IPO has a 75 percent reservation for qualified institutional buyers (QIBs) and a 15% reservation for non-institutional investors (NIIs).

Financial Highlights:

The firm was able to sustain a high level of performance. For the fiscal year ending March 31, 2020, the film earned Rs 271.38 crore in total revenue. This was increased from Rs 214.31 crore the previous year. The company's net losses increased to Rs 111.95 crore in FY20, up from Rs 58.05 crore the previous year. Krsnaa Diagnostics, on the other hand, had a significant decrease in spending and an increase in income.For the nine-month period ending December 31, 2020, the net profit and sales were Rs 195.93 crore and Rs 562.7 crore, respectively. This trend was caused by increased income from operations as a result of the pandemic's outbreak.

Recommendation: The business model is scalable, and in the present climate, where post-COVID health consciousness is at an all-time high, this industry is only going to grow in the next years. This represents a big market for the firm as well as significant potential.The firm intends to use the proceeds of the offering to pay down debt, which is usually valued accretive for service-oriented enterprises. ) The IPO price for Krsnaa Diagnostics discounts the most recent year's profits at roughly 21X, which is lower than the comparable group. We recommend you to subscribe(Aggressive Investors).

Glenmark Life Sciences IPO Date, Price, GMP and more.

Introduction:

Glenmark Life Sciences is a wholly-owned subsidiary of Glenmark Pharmaceuticals Ltd. Incorporated in 2011 and is situated in Maharashtra, India. Glenmark Life Sciences IPO is in news these days because it is open for a subscription (Initial Public Offering) from 27th July 2021 till 30th July 2021.

About the company:

The company is responsible for manufacturing and supplying high-quality APIs for gastrointestinal disorders, cardiovascular disease, pain management, and diabetes, anti-infectives, central nervous system disease and other therapeutic areas. The revenues it has generated in India in the last two years have grown at 71.62%. While revenues generated internationally since 2019 have grown at 25.61%.The major competitors of the Glenmark Life sciences IPO within the API market contain Laurus Labs, Divis Labs, Shilpa Medicare, Aarti Drugs, and Solara Active Pharma Sciences.

What are its objectives for raising an IPO?

- Paying off outstanding purchase considerations

- For funding capital expenditures

- Geographic expansion

- Growth in API and CDMO business

Financial highlights:

- Sales that are the total revenues stands at Rs 1885.98 crore for FY21

- PAT of FY21 is Rs 351.58 crore

- Net margin dropped to 18.64% from 20%. in FY21

- The debt to equity ratio is 1.27 times.

- Return on net worth is 46.71% for 2021.

- Net cash generated from operations was for FY 21 is Rs 388.11crore, for FY20 is Rs 195.01 crore, and FY19 is Rs 10.35 crore.

- Earnings Per Share is around Rs.32.61

- The price/earnings ratio is about 21.31 – 22.08

- Net Asset Value stands at Rs.69.82 per share

Fresh equity shares up to a total of Rs 1,060 crore will be issued. Under this public issue, the issue particularly includes an offer for the sale of 63 lakh equity shares by Glenmark Pharma. In this way, a total of Rs 1,513.6 crore will be available at the upper level of the price range under the SME IPO. The company had planned to issue fresh equity for Rs. 1160 cr but then the issue size got reduced to Rs. 1060 cr. Even to the astonishment of investors, the shareholder quota was totally skipped. It then was termed as investor unfriendly move as it sent wrong signals in the primary market. The equity trading of the corporate is going to be listed on BSE and NSE. Glenmark shares are available at a premium of ₹300 within the grey market, that's from the difficulty price of ₹695 to ₹720 about 40 per cent higher. GMP is very volatile because the Glenmark shares were available within the grey market at a premium of ₹200 to ₹205. So, the share market trading is predicted to reply strongly to the public issue.

Strengths:

- Strong growth in top-line, bottom-line expansion

- Strong margins

- It has a great financial performance track record and it provides return ratios

- It holds leadership in APIs and has a strong relationship with global generic companies.

- High-quality product manufacturing.

IPO Details:

- Glenmark Life Sciences IPO details

- Subscription Dates:27 – 29 July 2021

- Price Band: INR695 – 720 per share

- Fresh issue: INR1,060 crore

- Offer For Sale: 63,00,000 shares (INR437.85 – 453.60 crore)

- Total IPO size: INR1,497.85 – 1,513.6 crore

- Minimum bid (lot size): 20 shares

- Face Value: INR2 per share

- Retail Allocation: 35%

- Listing On: NSE, BSE

Whom to Invest and How Much to Invest

The reservation was kept in the following manner half of the total issue is for qualified institutional buyers, 35 per cent is kept for retail investors, and the remaining 15 per cent is for non-institutional investors. Glenmark Life Sciences has reduced its IPO size as compared to earlier. Also, if you want to invest in it, then at least 14 to 15 thousand will have to be spent. The company has made a lot of 20 shares. A person can buy at most 13 lots. The company will pay its expenses and borrow from the money earned from this IPO.

Conclusion:

Grey market observers are attracted by Glenmark shares. API business is expected to reach USD 306 bn by the year 2027 due to the coronavirus. The second reason being we are becoming independent as of now in China so we don’t plan to export drugs from China. The issue when compared to its peers is reasonably priced in terms of price to its earnings ratio. Hence, we recommend subscribing to the IPO.

Macrotech Developers Limited IPO (Lodha Developers IPO)

Incorporated in 1995, Macrotech Developers [Formerly known as Lodha Developers] is the largest real estate developer in India. The company is primarily engaged in affordable residential real estate developments and in 2019, it entered into the development of logistics and industrial parks and also developed commercial real estate.

The company’s large ongoing portfolio of affordable and mid-income housing projects include Palava (Navi Mumbai, Dombivali Region), Upper Thane (Thane outskirts), Amara (Thane), Lodha Sterling (Thane), LodhaLuxuria (Thane), Crown Thane (Thane), Bel Air (Jogeshwari), LodhaBelmondo (Pune), Lodha Splendora (Thane) and Casa Maxima (Mira Road).

The affordable and mid-income housing developments accounted for Sales of Rs.3055 crores during the financial year 2020 and constituted 57.77% of our total residential sales.

Company Business:

- The Company develops Real estate across the residential and commercial sectors in the Mumbai Metropolitan Region, Pune, and London.

- In the Residential Portfolio, the price of the Flat they sell is in the range of 35 Lacs to 59 Cr.

- In the commercial portfolio, they develop office and retail projects as income-generating assets on the lease model and sale models, with an increasing focus on the former.

- The company has a good track record of completing projects from acquisition to launch to completion thereby improving Return on investment.

Strength of the Company

- Largest residential real estate developer in India.

- Strong sales distribution network across India as well as NRI markets

- Brand equity and premium pricing.

- Strong project execution capabilities.

- Experienced Management Team.

RISKS RELATING TO BUSINESS:

- There are material outstanding legal proceedings involving Company, Subsidiaries, Associates, Directors, Promoters, and Group Companies

- The company may not be able to successfully identify and acquire suitable land or development rights, which may affect business and growth.

- The company’s business and results of operations could be adversely affected by the incidence and rate of property taxes and stamp duties.

- Compliance with, and changes in, environmental, health and safety, and labor laws and regulations could adversely affect the development of projects and financial conditions.

IPO Details:

IPO DateApr 7, 2021to Apr 9, 2021Issue TypeBook Built Issue IPOIssue Size51,440,328 Eq Shares of ₹10(aggregating up to ₹2,500.00 Cr)Fresh Issue5,14,40,329Eq SharesOffer for SaleNILFace ValueRs.10 per equity shareIPO PriceRs.483 to Rs.486 equity shareMin Order Quantity30Listing AtBSE, NSE

IPO Objective:

- Reduce the aggregate outstanding borrowings of the company on a consolidated basis.

- To acquire land or land development rights.

- To meet general corporate purposes.

Financial Performance:

FY2018FY2019FY20209M FY2021Revenue13,726.611,979.912,561.03,160.5Expenses11,017.09,490.011,560.23,218.8Comprehensive income1,767.91,641.6732.5-264Margin (%)12.913.75.8-8.2

Tentative Time Table:

- IPO Opens on: Apr 7, 2021

- IPO Closes on Apr 9, 2021

- Basis of Allotment Date: Apr 16, 2021

- Initiation of Refunds: Apr 19, 2021

- The credit of Shares to Demat Account: Apr 20, 2021

- IPO Listing Date: Apr 22, 2021

Outlook:

Lodha Group has been involved in the real estate business since 1995. Further, the Company is led by Abhishek M. Lodha, Managing Director and Chief Executive Officer. The company has a leadership team of experienced professionals with relevant functional expertise across different industries who are instrumental in implementing the business strategies.

The company commenced operations in Mumbai, developing affordable housing projects in the suburbs of Mumbai, and later diversified into other segments and regions in the MMR and Pune. In addition to the ongoing and planned projects, as of 31 December 2020, the company has land reserves of approximately 3,803 acres for future development in the MMR, with the potential to develop approximately 322 million square feet of Developable Area.

The company has clocked sales of approximately INR 6,569 crores with gross collections of approximately INR 8,189 crores for FY 19-20. The company reported a total income of ₹3,160.49 crores for the period ended December compared with ₹9,357.35 crores a year ago. The net loss stood at ₹264.30 crores compared to a profit of ₹503.08 crores.

Their residential and commercial spaces are aimed at every segment, right from super luxury to budget, thereby enabling every aspiring consumer to fulfill their dream. The company’s brands include “Lodha”, “CASA by Lodha” and “Crown – Lodha Quality Homes” for our affordable and mid-income housing projects. The “Lodha” and “Lodha Luxury” brands for premium and luxury housing projects, and the “iThink”, “LodhaExcelus” and “LodhaSupremus” brands for office spaces.

The company’s in-house sales team is supported by a distribution network of multiple channels across India as well as key non-resident Indian (“NRI”) markets, such as the Gulf Cooperation Council, United Kingdom, Singapore, and the United States.

The real estate market in India has grown at a CAGR of approximately 10 percent from $ 50 billion in 2008 to $120 billion in 2017 and is expected to further grow at a CAGR of 17.7% to reach $1 trillion by 2030. The real estate market contributed approximately 6 percent to India’s GDP in 2017 and is likely to contribute approximately 13% to India’s GDP by 2025.

Valuation of Macrotech Developers (as of FY2020)

Earnings Per Share (EPS): INR18.46Price/Earnings (PE ratio): 26Return of Net Worth (RONW): 17.8%Net Asset Value (NAV): INR103.86 per share

Macrotech Developers has a strong reputation in the Mumbai region with delivery of close to 10,000 homes annually. Has the ability to price at a premium which results in higher margins.