Tech Mahindra Share Price Outlook: Q1 Preview, AI Strategy, And Margin Trajectory

Key Takeaways

- Tech Mahindra's Q1 preview suggests about 1% constant currency revenue growth QoQ.

- Margins are expected to rise by 30–50 basis points, with FY27 EBIT around 15%.

- Large deals in telecom and BFSI, plus a broad range of TCV expectations, could steer momentum.

- Monitor margin pace, demand trends across verticals, and the AI/telecom roadmap for clarity.

For investors tracking tech mahindra share price today, the June quarter preview could set the tone for the IT sector's next leg. The Q1 preview hints at modest revenue growth led by telecom, with margins likely to improve on ongoing cost-optimisation and efficiency measures. As the company eyes large deals, BFSI momentum, and progress toward the FY27 margin target, the path to profitability and AI-driven growth remains a focus for retail investors.

Tech Mahindra Share Price Outlook After Q1 Preview

Analysts broadly expect the June-quarter revenue to grow in constant currency by about 1% QoQ. The dispersion across brokerages ranges from 1.0% to 1.2% CC, with Nuvama indicating 1.2% CC growth (0.8% in US dollar terms) and Nomura, Motilal Oswal, and Kotak Institutional Equities all anchoring around 1% CC. Systematix sits slightly higher at 1.1% CC. These forecasts imply a continuation of a steady, telecom-led push rather than a material acceleration in discretionary segments.

On the margin front, there is a consensus that profitability should creep higher as cost optimisation and productivity initiatives take hold. Nuvama and Nomura expect margins to improve by about 30 basis points QoQ; Systematix also projects roughly 30 basis points of expansion. Motilal Oswal is a touch more optimistic, predicting a margin rise of about 50 basis points to around 14.3%. Kotak, while seeing a similar uplift, notes an approximate 40 basis-point expansion offset by an initial 20 basis-point drag from compensation realignment tied to labour-code changes. Taken together, the Street is leaning toward a modest margin uplift rather than a swing to a new profitability regime in the near term.

Regarding the longer horizon, most analysts appear inclined to reiterate a FY27 EBIT margin target near 15%. This keeps Tech Mahindra in the category of peers guiding toward mid-teens profitability while balancing investments in AI and strategic hires with ongoing efficiency measures.

The large-deal picture is a critical hinge for the stock. Nomura surveys roughly $800 million in new deal wins as a potential accelerant. Systematix cites a total contract value (TCV) between $800 million and $1 billion, underscoring appetite for meaningful contract wins. Kotak adds a view of new deal wins in the $900 million to $1 billion band. These magnitudes matter, given how deal momentum can translate into revenue visibility and improved operating leverage in subsequent quarters.

From a sectoral viewpoint, telecom is expected to remain a growth pillar in the near term, with BFSI showing healthy demand against a backdrop of persistent macro uncertainty. Manufacturing is anticipated to stay steady, though US automotive weakness remains a balancing factor. The high-tech vertical may remain soft due to softer discretionary spend, underscoring the role of efficiency gains and anchor client relationships to sustain growth.

Beyond the numbers, investors are seeking a sharper AI narrative and a clearer long-range telecom outlook. Kotak’s view that Tech Mahindra’s AI story has been less prominent than peers highlights an important gap: clarity on AI initiatives, use cases, and client deployment timelines. In a market where AI becomes a larger portion of growth storytelling, the absence of a crisp AI play can constrain multiple expansion, even if near-term fundamentals look steady.

As the earnings preview unfolds, investors should monitor a few key questions: Is the pace of margin expansion sustainable, or will it flatten as the year progresses? Are demand trends broad-based across verticals or concentrated in telecom and BFSI? And will management strike the right balance between profitability improvements and reinvestment to accelerate revenue growth? These dynamics will shape the stock's near-term trajectory and long-run value.

For deeper stock-specific analysis and to contextualize these numbers within a broader trading framework, consider Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Modest June Quarter Revenue Growth By Vertical: Telecom And BFSI In Focus

The telecom vertical is expected to anchor growth as telecom operators continue to modernise networks, roll out 5G-related services, and pursue efficiency-led IT partnerships. In BFSI, demand remains resilient–payments modernization, risk analytics, and core systems refreshes continue to drive deal sizes and renewal rates. Manufacturing remains a stabilising factor, with steady outsourcing needs supporting ongoing digital transformation efforts. However, US automotive weakness and macro headwinds could cap upside from discretionary tech spend, especially in the high-tech segment where budgets can swing with enterprise capex cycles.

In this mix, Tech Mahindra's relative exposure to telecom and BFSI could provide a degree of earnings visibility, potentially offsetting slower demand in other segments. The question for investors is whether this vertical mix translates into durable free cash flow and improving margins as pricing, automation, and offshore delivery benefits materialise. A disciplined approach to pricing and project-management discipline will be essential to translate topline recovery into meaningful margin gains over the medium term.

Margin Trajectory And FY27 EBIT Guidance

The margin trajectory remains a focal point for the stock. With consensus pointing toward a 30–40 basis-point QoQ improvement for several analysts, the range of expectations extends a little wider for Motilal Oswal’s more optimistic 50-basis-point uplift to approximately 14.3% EBIT margin in the current trajectory. This pathway aligns with the broader objective of achieving roughly a 15% EBIT margin by FY27, a target that would require continued efficiency gains, selective reinvestment, and a measured approach to wage and cost realignment initiatives.

From a management perspective, sustaining margin expansion will hinge on balancing profitability with revenue growth. If large deals accelerate, there could be a modest near-term dilution of margins due to ramp costs, followed by a more meaningful uplift as volumes scale and utilisation improves. Conversely, a softening revenue environment could compress margins if fixed-cost absorption deteriorates. Investors should watch the cadence of margin expansion and any forward-looking commentary around re-investment plans, especially in AI and automation initiatives, to gauge the likely path toward the FY27 margins target.

AI Strategy And Large Deals: Key Catalysts For Tech Mahindra

Analysts are watching how Tech Mahindra articulates its AI strategy as a differentiator. In a market where peers have highlighted AI-led offerings and platform-scale initiatives, a clearer narrative around AI use cases, vertical deployment, and client traction could help support a higher multiple. The large-deal pipeline is a crucial guardrail for earnings visibility, with Nomura’s ~"$800 million" expectation and Systematix’s $800 million to $1 billion TCV suggesting a meaningful contribution if closed in the current cycle. Kotak’s $900 million to $1 billion band adds to the sense that the next few quarters could hinge on success in large, multi-year engagements rather than a string of smaller contracts.

Investors should watch how AI initiatives translate from pilots to production, the breadth of AI-led value across BFSI and telecom, and whether AI-enabled automation begins to meaningfully improve delivery efficiency. A transparent update on AI offerings, customer adoption, and the scalability of these initiatives could be a material re-rating factor for Tech Mahindra share price, particularly if the company can demonstrate quantifiable AI-enabled outcomes in client portfolios.

Monitorables: Margin Pace, Demand Trends, And Profitability Path

Beyond the headline estimates, several monitorables can help investors triangulate the company’s true near-term trajectory. The pace of margin expansion will be a critical signal, especially when juxtaposed with ongoing demand trends across verticals. Management commentary on whether profitability improvements take priority over reinvestment could signal the sustainability of the current earnings trajectory. Demand trends across telecom, BFSI, manufacturing, and high-tech will together paint a picture of stability versus acceleration. Finally, the development of a clearer AI and automation roadmap will likely influence long-term investor confidence and the stock’s valuation multiple.

As you weigh these factors, remember that large deals can alter the trajectory in meaningful ways. A strong queue of large wins could compress ramp-up costs and eventually translate into higher margins and more consistent earnings power. Conversely, if large deals slow down, the near-term earnings resilience will depend on efficiency gains and a steadier flow of medium-sized contracts.

Frequently Asked Questions

What is the expected June-quarter revenue growth for Tech Mahindra in constant currency (CC)?

Analysts expect about 1% CC revenue growth QoQ, with brokerages showing a range from 1.0% to 1.2% CC. Nuvama projects 1.2% CC growth (0.8% in USD terms), while Nomura, Motilal Oswal, Systematix, and Kotak Institutional Equities are around 1% CC, with Systematix at 1.1%.

What are the expected margin improvements for Tech Mahindra in the Q1 preview?

Margin improvements are expected to range from about 30 basis points to 50 basis points QoQ. Nuvama and Nomura foresee ~30 bps, Motilal Oswal eyes ~50 bps to around 14.3%, Systematix ~30 bps, and Kotak ~40 bps after an estimated 20 bps drag from compensation realignment related to labour-code changes.

What is the FY27 EBIT margin guidance for Tech Mahindra according to most analysts?

Most analysts expect Tech Mahindra to reiterate a FY27 EBIT margin guidance of about 15%.

Which large deals or project pipelines are highlighted as catalysts in the Q1 preview?

Analysts point to about $800 million in new deal wins per Nomura, a total contract value between $800 million and $1 billion per Systematix, and $900 million to $1 billion in new deal wins per Kotak. These figures point to meaningful revenue visibility if closed.

Which verticals are expected to drive growth and which might underperform?

Telecom is expected to drive growth, with BFSI showing healthy demand. Manufacturing is anticipated to remain stable, while US automotive weakness could temper growth, and the high-tech vertical may remain soft due to reduced discretionary spending.

Conclusion

In the near term, Tech Mahindra share price appears to be navigating a balanced path: modest revenue growth underpinned by telecom-led demand, with a margin uplift that mirrors ongoing cost optimization. The breadth and scale of large deals remain a pivotal swing factor that could unlock a more confident revenue trajectory and stronger profitability through the remainder of the year and into FY27. For retail investors, the prudent approach is to watch the pace of margin expansion, the durability of demand across verticals, and the clarity of the AI and telecom strategic roadmap. The next few quarters will reveal whether the current expectations translate into sustained earnings power or whether the company must accelerate profitability through selective reinvestment and disciplined execution.

Open your trading and demat account here

Reference :

1 : Economictimes

Latest Articles

.avif)

A Wintry night of plight for Credit Suisse

Those who don’t learn from history, are doomed to repeat it.

However, the financial crisis of 2008-09 is a history you would want to avoid at all costs. And that is exactly why those who are aware of the gloom, that the Infamous crisis bestowed upon us (ahem), are keeping a close eye on the ongoing turmoil, that ‘Credit Suisse’ finds itself to be in.

With $22 Billion of Revenue, $1.5 Trillion of ‘Assets under Management’ and currently operating in 50+ Countries, the Swiss Mammoth is a systematically important financial institution. And given the scales, it's a no-brainer why its collapse can herald another calamity, with multi-fold consequences, just like what happened in 2008, when 'Lehman Brothers’ an organization that was deemed ‘Too big to fail’, went under and triggered worldwide mayhem. Flashes of those times still send a chill down the spine of Economists all over the globe alike.

But before we draw the parallels between the two companies and their predicament, let us understand a few terms.

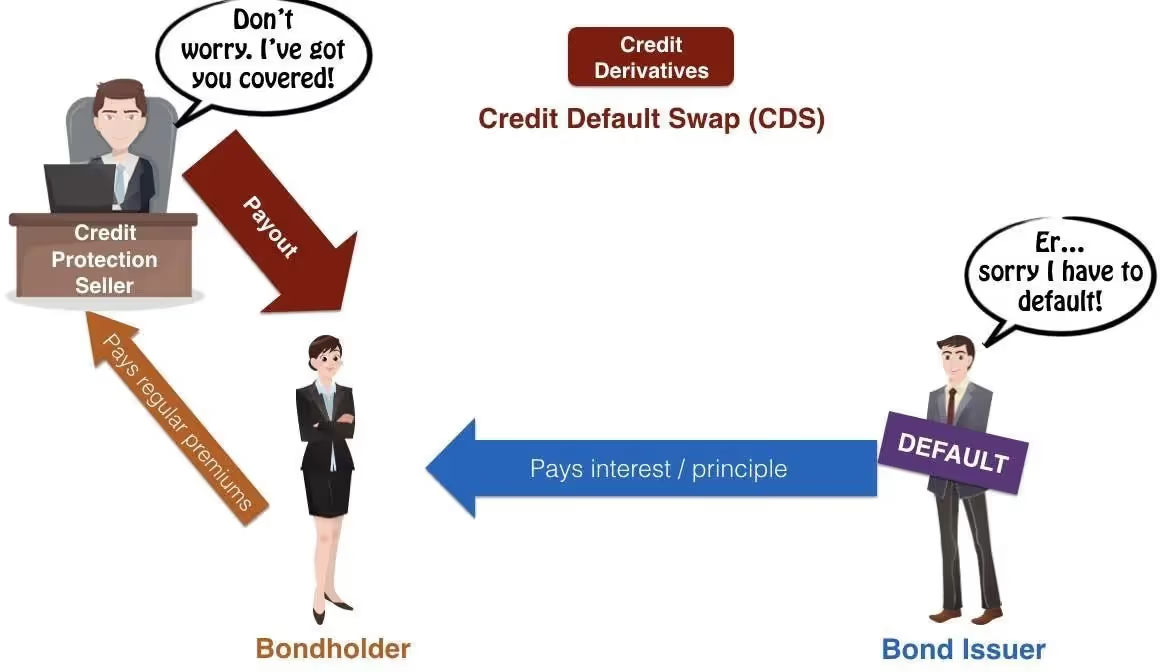

First is Credit Default Swap (CDS)-

In lehman oops.. laymen’s terms, it's an insurance instrument, in which the insuring party charges an upfront fee for the promise of reimbursing them any losses due to the default by the borrowers. Here, the borrowers are usually companies that issue Bonds. In essence, the parties agree to swap the risk of Credit default.

(https://prepnuggets.com/glossary/credit-default-swap)

The fees charged by the party assuming the risk of default is called 'Credit Default Swap Spread' or CDS Spread. Higher the risk, the higher the CDS Spread that will be charged. Conversely, the higher the spread on a particular security, the higher the chances of it defaulting on its repayment commitments.

With this out of the way, let's wipe the dust off of our time machine, and travel back to 2007-08, when American Real Estate Sector was on an unprecedented boom, and Banks were churning out House Loans against Mortgage- Backed Securities, at a rapid pace. Thus, every Tom, Dick, and Harry were granted loans and bought homes, irrespective of their financial capabilities and credit history. Banks then hedged themselves by signing Credit default swaps with Institutions like AIG and..... (drumrolls please) Lehman Brothers. This activity spearheaded the ill-famed ‘Housing bubble’.

But like every other bubble that ever graced this planet, this one too, sooner or later, had to burst. And as they say, when it rains, it pours.

Due to the influx of so many houses in the market and people failing to honor their commitments, the housing sector collapsed like a bunch of legos. With piling defaults, Banks turned to the Institutions that issued Credit Default swaps, to get the payment. But those institutions weren't any Cash Printing Genie who could summon such humongous amounts at such short notice.

Subsequently, due to abnormally high default claims, they were left with no cash to honor the swaps and were looking at possible Bankruptcy. Although Institutions like Citi Banks and AIG were bailed out by the government, Lehman Brothers found themselves beyond salvation. They ultimately collapsed and declared bankruptcy on 15th September 2008. Their downfall and the aftermath of this crisis ushered an era of disastrous financial ramifications for the global economy.

Coming back to 2022, Macro-Economic factors don't instill a lot of confidence in the European Economy. With the ongoing Russia-Ukraine War, Energy prices rising by 175%, rapid depreciation of the Pound, and Europe still recovering from Covid-19's implications, it won't be an understatement to say that things are looking a bit iffy.

Further, after incurring losses in the last 5 out of 7 quarters, and laying off 500+ employees, Credit Suisse has watched 66% of its market cap getting eroded, since the beginning of 2022.

Along with that, the CDS spread on Credit Suisse's bond (which, as discussed earlier, indicates the risk on the security) stands at an all-time high of 4.4%, with the same metric for its Industrial counterparts standing at appx. 0.6%-0.8%. And with rising chances of defaults on loans due to severe economic shortcomings, investors are afraid that a fate like Lehman Brothers, might await Credit Suisse.

However, when we compare the position of Lehman Brothers at the time of bankruptcy, and Credit Suisse as of now, one might feel that the talks of Credit Suisse going down, is getting blown way out of the proportions.

Let us have a look at the factors given below.

Factor Lehman Brothers Credit Suisse Cash in Hand$19548 Mil$159752 Mil(Cash in Hand as % of assets)3.10%21.30%% of Assets in form of Securities 88.20%30.33% Leverage Ratio 24.34 Times15.9 Times

Also, Credit Suisse has a CET-1 Ratio of 13.5 % and a liquidity ratio of 191%. As one can see, it is in a significantly better position in almost all of the metrics. Further, The company is in process of raising $4 Billion from its existing investors and has onboarded a new CEO, who is faced with two impending tasks, i.e., to cut costs by $1 Billion p.a. and restructure the IB Department. Considering all of these, one can assume that the company is committed to getting back on track, as soon as possible.

But that does not undermine the gravity of the bedlam looming over it’s head. The risk is too damn high, but not all hope is lost. Whether Credit Suisse will go tumbling down or will it steer away from the danger unscathed, only time will tell. But one thing is for sure, a very cold winter awaits the Swiss Giant.

However, before departing, I'm going to leave you with an interesting trivia. The last name of the newly appointed Chairman of Credit Suisse is...wait for it...

Lehmann. Take that as you may, and I'll see you pretty soon.

सकारात्मक दायरे में कीमती धातुओं के भाव

न्यू ईयर और क्रिसमस के चलते कीमती धातुओं में कारोबार सिमित रहा, हालांकि कीमती धातुओं के भाव मजबूती के साथ सिमित दायरे में बने हुए है। भारत में पिछले एक साल में सोने और चांदी की कीमतों में अच्छी बढ़त दर्ज की गई है जबकि फेड और अन्य प्रमुख केंद्रीय बैंको द्वारा मई 2022 के बाद लगातार की गई ब्याज दर वद्धि के कारण कॉमेक्स वायदा में सोने और चांदी की कीमतों में मामूली बढ़त देखि गई है। हालांकि, लगातार ब्याज दर वृद्धि के कारण मुद्रास्फीति में कुछ कमी देखने को मिली, लेकिन फेड द्वारा ब्याज दर वृद्धि में नरमी से सोने और चांदी के भाव में चमक लौट आई है। नए साल के लिए कोवीड वापसी की चिंता और आर्थिक मंदी की आशंका, कीमती धातुओं के भाव के लिए ट्रिगर रहेगा। डॉलर, जो सोने के विपरीत दिशा में चलता है, में गिरावट से कीमती धातुओं के भाव को सपोर्ट रह सकता है। साल 2022 में क्रिप्टो करेंसी में जबरदस्त बिकवाली और बिटकॉइन जिसको सोने के विकल्प के रूप में देखा जा रहा था, अपने उच्चतम स्तर से 76 प्रतिशत टूट चुका है जिससे निवेशकों का भरोसा सोने पर बना हुआ है। फेड द्वारा ब्याज दरे उम्मीद से ज्यादा बढ़ा दी गई है, और अधिक ब्याज दरों में बढ़ोतरी ग्लोबल अर्थव्यवस्था पर प्रतिकूल प्रभाव डाल सकती है जबकि फेड के बाद यूरोपियन सेंट्रल बैंक भी लगातार ब्याज दर बढ़ाने के संकेत दिए है। ग्लोबल शेयर बाज़ारो से मिले-जुले संकेत, निवेशकों को सेफ हैवन की तरफ आकर्षित कर सकता है। इस सप्ताह ओपेक - नॉन ओपेक देशो की बैठक, फेड बैठक के मिनट्स और अमेरिकी पैरोल के आंकड़े कीमती धातुओं के लिए महत्वपूर्ण रहेंगे।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं में तेज़ी रहने की सम्भावना है। सोने में सपोर्ट 54400 रुपये पर है और रेजिस्टेंस 55500 रुपये पर है। चांदी में सपोर्ट 68000 रुपये पर है और रेजिस्टेंस 70500 रुपये पर है।

.avif)

भारत में इस साल 13 प्रतिशत तेज़ हुए सोने के भाव

यूएस फेड की अति-उच्च ब्याज दर मौद्रिक नीति ने 2022 में सोने और चांदी की कीमतों को दबाव में रखा। हालांकि, फेड द्वारा दरों में बढ़ोतरी की श्रृंखला के बावजूद, मुद्रास्फीति 40 साल के उच्च स्तर के करीब बनी रही, जबकि उभरते बाजार की मुद्रा में भारी अवमूल्य, निवेशकों को सोने और चांदी की तरफ आकर्षित करते रहे। बैंक ऑफ जापान, यूरोपीय सेंट्रल बैंक और यूएस फेड की कठोर मौद्रिक नीति, वैश्विक विकास दर को क्षति पहुंचने की सम्भावना से अनिश्चितता बढ़ रही है। अगले साल भी अगर ब्याज दरे बढ़ती रही तो ग्लोबल अर्थव्यवस्था को नुकसान हो सकता है जिससे हेवन मांग 2023 में बने रहने का अनुमान है। चीन में बढ़ते कोवीड मामले, दुनिया के लिए एक बार फिर चिंताओं को बढ़ाने लगे है जिससे कीमती धातुओं के भाव घरेलु बाजार में अपने उच्चतम स्तरों के करीब पहुंच गए है। हालांकि, लगातार ब्याज दरों में बढ़ोतरी होने के बावजूद, अमेरिका के आर्थिक आकड़ो में सुधार और चीन में कोवीड प्रतिबंधों में ढील से कीमती धातुओं की तेज़ी सीमित रही है। भारत में पिछले साल की तुलना में इस साल सोने का आयात 35 प्रतिशत ज्यादा रहने का अनुमान है। पिछले एक साल में डॉलर ने 11 प्रतिशत बढ़त दर्ज की है और 83 रुपये के उच्चतम स्तरों पर पहुंच गया है। बढ़ती ब्याज दरों के कारण भारत जैसी उभरती अर्थव्यवस्था से फण्ड ऑउटफ्लो बढ़ा है जिससे चालू खाते में बढ़ोतरी हुई है और कीमती धातुओं के भाव को सपोर्ट रहा है। घरेलु वायदा बाजार में सोने ने साल-दर-साल 13 प्रतिशत और चांदी ने 11 प्रतिशत का रिटर्न दिया है, जबकि कॉमेक्स में सोने और चांदी के भाव फ्लैट रहे है। दुनिया में फैली महामारी के बीच कठोर मौद्रिक निति, कीमती धातुओं में सुरक्षित निवेश की मांग बढ़ा सकता है।

तकनिकी विश्लेषण:

इस सप्ताह कीमती धातुएँ सकारात्मक दायरे में रहने की सम्भावना है। सोने में सपोर्ट 53700 रुपये पर है और रेजिस्टेंस 55200 रुपये पर है। चांदी में सपोर्ट 67700 रुपये पर है और रेजिस्टेंस 71500 रुपये पर है।

फेड की हॉकिश टिपण्णी से बिगड़े सोने-चांदी में तेज़ी के सेंटीमेंट

पिछले सप्ताह कीमती धातुओं की तेज़ी, अमेरिकी फेड के हॉकिश टिप्पणी से थमती दिखी। घरेलु वायदा बाजार एमसीएक्स में सोने के भाव 9 महीने के उच्च स्तरों से पीछे हट गए जबकि चांदी में भी गिरावट दर्ज की गई है। कॉमेक्स वायदा में सोने की कीमते 1800 डॉलर के ऊपर नही टिक रही है। ज्यादातर प्रमुख केंद्रीय बैंको का कहना है की ब्याज दरों का उच्चतम स्तर अभी दूर है जिसके कारण आर्थिक मंदी का डर फिर से बढ़ने लगा है और कीमती धातुओं के साथ दुनिया भर के शेयर बाज़ारो में बिकवाली का दबाव देखने को मिला है। पिछले सप्ताह अमेरिकी फेड के बाद यूरोपियन सेंट्रल बैंक द्वारा भी लगातार ब्याज दरे बढ़ाने की बात कही है क्योकि मुद्रास्फीति अभी टारगेट से ऊपर चल रही है।

अमेरिका, चीन और यूरो ज़ोन के आर्थिक आंकड़ों से यह स्पष्ट होता है की यह प्रमुख अर्थव्यवस्थाएं उच्च मुद्रास्फीति और बढ़ती ब्याज दरों के दबाव से जूझ रही हैं। इस साल लगातार हो रही ब्याज़ दर वृद्धि के कारण सोने के स्थान पर निवेशकों ने डॉलर को चुना है और केंद्रीय बैंको का मोद्रिकनीति पर कठोर रुख अमेरिकी डॉलर इंडेक्स में तेज़ी का ट्रेंड फिर से शुरू कर सकता है। लेकिन, चीन में कोवीड प्रतिबंधों में ढील के बाद कोरोना मामलों में बढ़ोतरी और ग्लोबल अनिश्चितताओं के चलते कीमती धातुओं में निचले स्तरों पर सपोर्ट देखने को मिलेगा। पिछले सप्ताह फेड की बैठक के बाद सोना सप्ताह के उच्च स्तरों से 900 रुपये फिसल कर 54200 रुपये प्रति दस ग्राम के स्तरों पर पहुंच गया। जबकि चांदी के भाव भी सप्ताह के उच्च स्तरों से 2500 रुपये टूट कर 67000 रुपये प्रति किलो पर रहे।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं में क्रिसमस हॉलिडे के चलते सीमित दायरे में कारोबार रहने की सम्भावना है। सोने में सपोर्ट 53300 रुपये पर है और रेजिस्टेंस 55000 रुपये पर है। चांदी में सपोर्ट 65000 रुपये पर है और रेजिस्टेंस 69000 रुपये पर है।

Top Dividend Payer Vedanta Dividends Since 2021

Vedanta to Pay a Third Interim dividend at Rs 17.5 per Equity Share

One of the largest mining and metals companies in the world, Vedanta Limited, managed by billionaire Anil Agarwal, has interests in iron ore, steel, copper, zinc-lead-silver, aluminum, power, oil, and gas in India, South Africa, and Namibia.

The Mumbai-based business paid its shareholders the first interim dividend for FY23, which was 31.5 rupees per equity share, in May 2022. In July 2022, it paid eligible shareholders the second interim dividend, which was 19.5 rupees per share.

The company had declared a third interim dividend of Rs 17.50 per equity share, or 1750% of the face value of Re 1 per share, for the Financial Year 2022–23, totaling Rs 6,505 crore, by a resolution voted by circulation on Tuesday, November 22, 2022.

Vedanta Dividend Ex-Date 2022

The ex-dividend date for Vedanta stocks will be before the record date. A stock often trades ex-date prior to the record date. Vedanta ex-dividend will be on November 29.

Vedanta Dividend Record Date 2022

Vedanta has set the record date for determining whether shareholders are eligible to receive a dividend payment of Rs 17.50. The record date for the dividend's payment, according to the firm, is November 30. This indicates that Vedanta would pay shareholders who have shares of the company in their Demat accounts.

Dividend History

The business raised its total pay-out in two rounds of dividends announced so far in FY23 to Rs 18,960 crore in July when it announced a second interim dividend of Rs 19.5 per equity share.

The company announced its first interim dividend of Rs 31 per share in April, which resulted in an outflow of Rs 11,710 crore.

The Vedanta Resources dividend announcements coincide with the company's efforts to deleverage its balance sheet, since Vedanta Resources controls 69.7% of Vedanta.

Vedanta was the top dividend-paying company in FY22, and it was followed in the top 20 list by businesses like Tata Consultancy Services, Oil and Natural Gas Corporation, HCL Technologies, Indian Oil Corporation, Hindustan Unilever, Hindustan Zinc, Indian Tobacco Company, State Bank of India, and Reliance Industries.

VEDANTA's Peers

The stocks in this group to be on the lookout for are NMDC, HINDUSTAN ZINC, and COAL INDIA.

Year Ended Dividend Payout Per Share (Rs)Dividend Payout Ratio (%)Dividend Yield EOY (%) COAL INDIA March 2022 17.060.3% 9.3% HINDUSTAN ZINC March 2022 18.0 79.0% 5.8% NMDC March 2022 14.74 6.0% 9.1%

Why Vedanta is giving Dividends

The company's extremely explicit capital allocation policy is one of the factors contributing to the aggressive and large dividend payments. It has specified exactly how much of the company's income would go toward inorganic growth, dividend policy, and capital expenditures. This policy states that shareholders shall receive a minimum of 30% of the company's attributable sustainable profit after tax (excluding HZL profits).

The Company has established a great track record of generating cash flows due to consistent increase in sales volume and balanced capital expenditure for ongoing operations.

Vedanta Financials

Prior to extraordinary and one-time tax credits, Vedanta's profit for the fiscal year 2021–2022 increased by 95% to 24,299 crores, while its sales increased by 51% to 1.3 lakh crore. The company's total debt was Rs 53,109 crore, while its EBITDA increased by 66% to Rs 45,319 crore. On July 28, 2022, the corporation will release its Q1 FY23 financial results.

According to the corporation, the company will maintain an adequate leverage ratio at the consolidated level. "Vedanta Limited's consolidated leverage ratio on December 21 was 0.7x, ranking among the best in its peer group. The company would maintain the consolidated ratio below 1.5x throughout typical business cycles, according to the organization.

Archean Chemical Industries Limited IPO

About the Company

Archean Chemical Industries Limited, a renowned specialty marine chemical manufacturer produces and exports Bromine, industrial salt, and sulfate of potash as the main products. In Fiscal 2021, the firm was the leading exporter of industrial salt and bromine, and both products were among the products that have the lowest manufacturing costs in the world.

Archean Chemical Industries IPO

The specialty chemical manufacturer Archean Chemical Industries' initial public offering (IPO) is set to open on November 9 and end on November 11. The IPO's price range was set at Rs. 386 to Rs. 407 per share. In addition to an offer for the sale of 657 crores by the promoters and current shareholders, Archean Chemical Industries intends to raise 805 crore through a fresh issue of shares through the IPO.

According to the firm, 75 percent of the issue is set aside for qualified institutional investors, 15 percent is allocated to non-institutional investors, and the remaining 10 percent is allocated to retail investors.

Purpose of the IPO

The objective of the Offer for Sale (OFS) is to enable the selling shareholders to sell up to 1,61,50,000 equity shares, with the selling shareholders receiving the net proceeds.

- The company would use the net proceeds from the new issuance to redeem or redeem earlier, in full or in part, the NCDs it has issued totaling up to Rs 644 crore.

- Corporate general objectives.

Archean Chemical IPO – Details

IPO Opening Date 09 November 2022 IPO Closing Date 11 November 2022 Issue Type Book Built Issue IPO Issue Size ₹1462.31 Crore Face Value ₹2 per equity share IPO Price₹386 – ₹407 Market Lot 36 Shares Min Order 36 Shares Listing At BSE NSERegisterLink Intime India Private Limited QIB Shares Offered 75% Retail Shares Offered 10% NII (HNI) Shares Offered 15%

Strengths of the Company

The company has a competitive advantage since the industry in which it works has substantial entry barriers.

In Fiscal 2021, the company was India's top exporter of industrial salt and bromine.

- The company has a skilled management team, promoters, financial investors, and stakeholders

- The company has built integrated manufacturing sites that have shown to be cost-effective for the company.

Risk and Concerns

- unfavorable government laws and regulations

- a delay in capacity growth

- failure in a bromine derivative venture

- client revenue concentration risk

- unfavorable sales-mix and sales realization

- Unfavorable changes in exchange rates and competition.

Financials in Brief

Its revenue increased by 36% and 78% during the course of FY20-22, while its EBITDA margin increased from 24.3% to 41.3%. The company recorded FY22 revenue of Rs11.3 billion, up 53% YoY, and FY22 EBITDA of Rs4.8 billion, up 78% YoY. In comparison to FY21's PAT of Rs666mn and FY20's net loss of Rs362mn, FY22's PAT was Rs1.9bn. From 92% in FY21 to 72% in FY22, ROE has decreased. The business reported 2QFY23 sales of Rs 4 billion, up 99% YoY, EBITDA of Rs 1.6 billion (margin of 40.2%), and PAT of Rs 844 million, up 4.5 times YoY. In FY22, the company's Net Debt/Equity ratio dropped from 11.4x in FY21 to 3x.

GMP, Listing & Allotment Date

Market observers report that the Grey Market Premium (GMP) for the Archean Chemicals IPO is now 70 per equity share. The shares will be allocated on November 16, 2022. On November 21, 2022, the Archean Chemical IPO is most likely to list on both NSE and BSE

Outlook & Valuation

In the calendar year 2021, the Indian chemicals industry was valued at US$178 billion, representing approximately 3- 4% of the value of the global chemicals industry, and with rapid industrialization, this market is expected to grow even more. Archean Chemical Industries Ltd. is a formidable player in the bromine, industrial salt, and sulphate potash industry. It has witnessed a significant improvement in its top-line and bottom-line performance in the last three years. Nevertheless, the high debt-to-equity ratio (3.25 based on March, FY 22 consolidated numbers), high product as well as key customer concentration, and restructuring of loans during FY 17-18 make us averse to the issue. Additionally, the 3 years of data is limited for concluding the sustainability of high growth and margins. In short, considering all the shortcomings, investors should consider this issue for listing gains only due to the company’s reasonable valuations and presence in the specialty chemical industry.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App