Swastika News

Outperformance of Pharma Sector During COVID-19

.webp)

On March 13th, 2020 the Pharma index on National Stock Exchange made a low of 6242.85 since from that day the pharmaceutical stock has given a tremendous return. The pharma index made a high of 14282.90 an up move of 8040.05 points with almost 40% returns in 1 year and it has been assumed that the future outlook of the Indian Pharmaceutical industry will have a 3 times growth from till next decade. Indian domestic market is estimated to grow around US$ 41 billion by 2021 and may reach US$ 65 billion by 2024.These growth figures indicate that in long term the pharma sector can be a game-changer for the investors along with a great contribution to the countries economy. We are the major suppliers of generic medicines & drugs across the globe and with new PLI schemes and government intervention for 100% FDI the pharmaceutical industry will witness new growth ahead in the future. The contribution of around 1.72 % to the GDP of the country, makes a significant mark. Earlier it was only 1% in last decade. Lots of research& development programs, FDI inflow opens new avenues for the industry to grow further. The flow of $ 16.5 billion by FDI in April 2000-June 2020, due to 100% FDI is approval in greenfield projects via automatic route & 74 % FDI for brownfield projects. The efforts made by pharmaceutical companies to overcome the current Covid-19 crisis with the help of the Indian government show the robustness itself. We are the largest manufacturer of vaccines across the globe, and the fight against COVID-19 will not be successful without Indian vaccine manufacturers. We were the first to produce the vaccination for Covid-19.With this outperformance, many companies turned out to be multi-baggers for the investors.

Orchid Pharma Ltd

The company manufactures a wide range of APIs for oral cephalosporins, beta-lactams formulation, Special nutraceuticals, etc. The company is also engaged in formulation development for various segments like anti-oxidants, oral anti-diabetics. The return given by the company is 25,770.64% in one year with 52 weekly low of Rs.17.15 & made a high of Rs.2654.25

Bafna Pharmaceuticals Ltd.

The company engaged in the manufacturing of pharmaceutical formulations of Betalactum and Non-Betalactum productsThe return given by the company is 567.32% in one year with 52 weekly low of Rs.20.35 & made a high of Rs.233.55

Kopran Ltd

The company engaged in the manufacturing and supplying of International Quality Formulations and Active Pharmaceutical Ingredients worldwide. The return given by the company is 562.09% in one year with 52 weekly low of Rs.27.05 & made a high of Rs.234

Beta Drugs Ltd

The company manufactures & markets drugs for domestic & international customers, Primarily engaged in the manufacturing of oncology products It includes anti-cancer tablets, Injections & lyophilized injections.The return given by the company is 520.00% in one year with 52 week low of Rs.47. & made a high of Rs.350.20

Laurus Lab Ltd.

The company offers an integrated portfolio of API which includes intermediate, generic finished dosage forms and carries out contract research services. The return given by the company is 476.39% in one year with 52 weekly low of Rs.92.80. & made a high of Rs.544.95

Wanbury Ltd

The company engaged in the business of manufacturing of formulations Active Pharmaceutical Ingredient(API) and Contract Research and Manufacturing Services.The return given by the company is 425% in one year with 52 weekly low of Rs.19.05 & made a high of Rs.114.00

Neuland Laboratories Ltd

The Company is a leading manufacturer of active pharmaceutical ingredients & an end-to-end solution provider for the pharmaceutical industry.The return given by the company is 423.19% in one year with 52 weekly low of Rs.387.75 & made a high of Rs.2844.40

Solara Active Pharma Science Ltd.

The company is pure play for API & engaged in the manufacturing & development of API. It also offers Contract Manufacturing & development services for foreign companies.The return given by the company is 215.97% in one year with 52 week low of Rs.516.35 & made a high of Rs. 1859.95

Aarti Drugs Ltd

The company is one of the major pharmaceutical manufacturers in the country. It is engaged in the manufacturing of pharmaceuticals. It also operates in anti-diarrhoea, anti-inflammatory, and anti-biotic therapeutic segments.The return given by the company is 201.72% in one year with a 52 week low of Rs.227.75 & made a high of Rs. 1026.95

CURRENT SCENARIO IN OIL COMPLEX

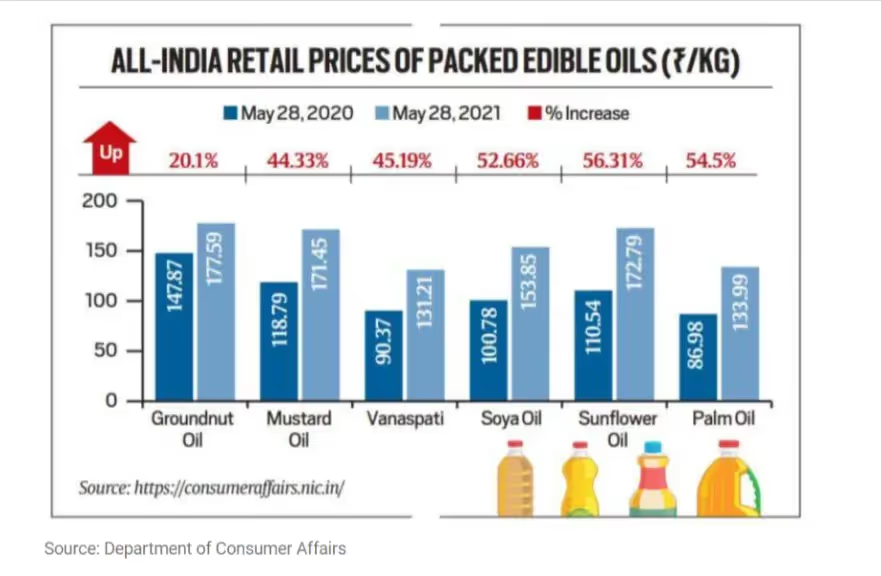

India is the biggest consumer of refined soybean oil and is one of the major importers of oil and oil complexes, contributing around 70% of which palm oil contributes around 80%. India is the third largest export destination for Malaysian palm oil. Over the months we have seen a huge surge in the prices of edible oil, and as per the government data, the retail prices of edible oil have risen over 62% in over a year adding woes to the consumers who are already suffering from the economic crisis induced by the COVID-19 pandemic.

MALAYSIAN CRUDE PALM OIL (CPO)

Palm oil is edible oil which is extracted from the pulp of the fruit of oil palms. Commonly, it is combined or mixed with coconut oil to make highly saturated vegetable fat, which is also used for cooking purposes. Indonesia, Malaysia, Nigeria, and Columbia are the largest producers of CPO and even the major exporter of palm oil where as India is the net importer of CPO. Looking at the recent price changes in the CPO huge volatility has been noticed leading to the surge in its price and the reason for the same has been quoted as the bad weather in its producing countries because of that the output has also been lowered and also the shifting of edible oil from food to fuel basket. Adding to this, the continuous buying from China and export duties on CPO in Indonesia and Malaysia are also the key triggers for the rise in its price.

REFINED SOY OIL

It is a vegetable oil extracted from the seeds of the soybean and is one of the most widely consumed cooking oil and the second most consumed vegetable oil. As per the Department of Consumer Affairs, there has been a rise in the price of edible oil between 20%-56% at all India levels within the last year. In fact, the monthly average retail prices of all six edible oils soared to an almost 11-year high on May 21 where already household incomes have been hit due to this pandemic. India meets 56% of its domestic demand through imports where the increase in domestic price of edible oil is just a reflection of international prices, which have jumped sharply in recent months due to various factors. Even the Food and Agriculture Organization (FAO) price index for vegetable oils, an indicator of movement of edible oil prices in the international market, soared to 162 in April 21, as compared to 81 in April 20.

After the huge surge in edible oil prices now we can see some cool-off as it is expected that China may reduce palm oil exports in 2021-22 which may result in reduced prices of palm oil as it is focusing on self-reliance on vegetable oil. On the other hand, we are expecting our government to lower import duties so that some drop can be seen in the prices of edible oil. Technically, we have seen some profit booking among most of the agricultural commodities on NCDEX as making the top such as Soybean, Rmseed and Refined Soy Oil. In the coming days refined soy oil may test the levels of 1330-1340 where as in soybean selling can be seen below 6800 as being the important support level.

Know Why is the Price of Gold Rising Amid Inflation and Second Wave of Pandemic in India

Gold, a precious metal, has been an integral part of ancient India. For years, Gold has been considered a symbol of wealth, status and an important part of many Indian rituals. Thanks to the metal’s affluence and its usage, gold has shown a great shielding effect against uncertain market conditions i.e. pandemic.As the 2021 quarter comes to an end, gold hasn’t made a great hit. The precious metal has tumbled 19% from its last August and is back where it was in February last year before the pandemic hit the developed world. However, as the quarter-end and the pandemic began, the price of gold has subsequently increased. Gold’s price has suddenly increased and it touched an over a three-month peak on Tuesday as the investors have shown a great interest in the yellow metal. Another important cause behind the sudden rise of gold prices is the second wave of the pandemic, rising inflation, and a weekend US dollar that marks investors to make Gold a hedge option. Also, recently, it has been seen that the gold prices are rising with a decent amount and due to the occasion of Akshay Tritiya, the prices are further increased. The second wave of pandemic gold prices had faced a slight drop but post-Akshay Tritiya occasion, it is again in the spotlight. That means, the prices have recovered and experts say that it will cross the mark of 50000 in July 2021.Even though businesses are suffering and the economy is struggling to come to its normal pace, many people are perplexed as to why gold prices are rising during the weak condition of the economy. Below are the factors that influence gold prices to a greater extent: A lot of things has been said about the factors that influence financial markets, many investors are unaware of the rising prices of gold:

Demand and Supply

The demand and supply of gold play a crucial role in rising gold’s price. The inadequate availability of gold increases the demand for gold and hence the prices rise as well as the supply is limited.

Rate of Interest

Gold prices and interest rates are inversely proportional to each other. As interest rates decline, people don’t get good returns. Hence, people are required to split their deposits and buy gold which in turn increases the demand and the price.

Reserves Held by the Government

RBI plays an important role in affecting gold prices. Indian’s government maintains gold reserves. By doing this, the Indian government can buy and sell gold through the Reserve bank of India. If they purchase or sell more gold, the prices would affect the gold.

The market for Indian Jewellery

Many people buy gold jewellery in India and hence the gold price rises during festivals and wedding seasons.

Import Taxes

India’s contribution to global output is observed as less than 1%. Although the country is the second-largest consumer of gold, to meet its metal demand, India also imports a lot of gold from other countries.

Market For Indian Jewelry

The demand for gold rises during the festive and wedding seasons in India as many people wear gold jewelry on occasions. Such things increase the demand for gold which will eventually rise in its prices.

Why are gold prices rising? Key things to know:

The sudden rise in gold prices makes many investors worried. They fail to recognize the real reasons for rising gold prices. Why are gold prices rising? At what time does the gold price rise? Can they invest in gold now or they have to wait for some months?

Investors now, seeking the safest instrument to invest:

Since March 2020, many countries have adopted nationwide lockdown to prevent the spread of Covid 19 infections. It has helped several countries to minimize the spread of coronavirus among people, however, it also caused a lot of economic damage as all the production was closed and imports and exports were cancelled. To get rid of the tough times of the pandemic, people are finding gold as the safest instrument to invest.

Understanding the relation between lockdown and gold price:

When the lockdown had ended in June 2020, many people would think that the businesses would grow faster and the economy would soon recover. Hence, a large number of investors had started investing in high-quality stocks. However, as the myths of economic recovery have faded, people have started to invest in safer options. As a result, gold prices are rising day by day as the people see it as a natural shield or safeguard against inflation and economic instability.

Should You Invest in Gold Now?

Although increasing demand for gold prices indicates strong demand for gold jewelry, experts believe that the gold prices will reach up to 65000 per 10 gram in the upcoming years. The reason behind the rising demand for gold depends on a lot of factors such as low interest rates, liquidity and availability. Is it a good time to invest in gold? Well, the answer heavily depends on how you see the market. If you think that the economy will take a long time to recover and the interest rates will remain low for a long duration; investing in gold is considered a good option. However, if you think the economy will soon recover and the industries will receive a heavy boom, then you need to look for other investment options i.e. stocks.

The Bottom Line

As the gold prices are rising day by day, it catches investors' attention. As a result, many investors have started to invest in gold considering it as the safest instrument. However, it is also crucial to think of all the other investment options before making any decision. Hence, before jumping on board, please make sure that your investments flow parallelly with your portfolio, investment strategy and risk tolerance.

ईरानी तेल के बाजार में आने की उम्मीद से कच्चे तेल की कीमतों में गिरावट आई है

पिछले सप्ताह ब्रेंट कच्चे तेल के भाव अमेरिका-ईरान के बीच हो रही परमाणु डील की वार्ता के दौरान 70 डॉलर प्रति बैरल के स्तरों से टूट कर 65 डॉलर तक फिसल गए। घरेलु वायदा कच्चे तेल के भाव सप्ताह में 5 प्रतिशत तक टूट कर 4550 रुपये प्रति बैरल पर रहे। तेल की कीमतें मार्च के बाद से अपने सबसे बड़े साप्ताहिक गिरावट को दर्ज करने की कगार पर है। अमेरिका और ईरान 2015 के परमाणु समझौते को पुनर्जीवित करने के करीब हैं, जो ईरान के तेल, बैंकिंग और शिपिंग क्षेत्रों पर प्रतिबंध हटा सकता है, और इस प्रकार ईरानी कच्चे तेल की आपूर्ति को बढ़ावा दे सकता है।

उधर, ओपेक समूह ने इस महीने उत्पादन में 350,000 बैरल प्रति दिन की कटौती को कम करना शुरू कर दिया है। ओपेक सामूहिक तेल उत्पादन मई और जून दोनों में 350,000 बैरल प्रति दिन और जुलाई में 400,000 बैरल प्रति दिन से अधिक बढ़ाने के लिए तैयार है। इसके अतिरिक्त, सऊदी अरब भी अगले कुछ महीनों के दौरान धीरे-धीरे १० लाख बैरल प्रतिदिन की अतिरिक्त एकतरफा कटौती को कम करेगा, जिसकी शुरुआत मई और जून दोनों में मासिक उत्पादन में 250,000 बैरल प्रतिदिन की वृद्धि के साथ होगी। कुल मिलाकर, ओपेक के जुलाई तक बाजार में 21 लाख बैरल प्रतिदिन तक लौटने की उम्मीद है।

तकनीकी विश्लेषण

इस सप्ताह कच्चे तेल के भाव में मंदी रहने की संभावना है। ब्रेंट क्रूड ऑयल में 60 डॉलर पर सपोर्ट है और 71 डॉलर पर प्रतिरोध है। घरेलू वायदा क्रूड ऑइल में 4450 रुपये पर सपोर्ट है और 4900 रुपये पर प्रतिरोध है।

Weekly Stock Recommendation

1. Glenmark Pharmaceuticals:- CMP 591.5 SL 570 TGT 640

Sector: Pharmaceuticals Industry: Pharmaceuticals - Indian - Bulk Drugs & Formulation

Business Area:

The company is engaged in the development of new chemical entities & new biological entities. Speciality Business: Drug Discovery, Primarily focused in the areas of inflammation, metabolic disorders, and pain. Speciality Business: Formulation Business, The formulation business focuses on therapeutic areas viz. Dermatology, anti-infective, respiratory, cardiac, diabetes, gynecology, CNS & oncology.

Technical Setup:

- Stocks are trading above short, medium & long-term moving averages

- MACD crossover above the signal line

- Price Strength indicated by RSI

Fundamental Setup:

- Company with high TTM EPS growth

- The company has reduced debt

- Growth in net profit with an increasing profit margin

2. Lux Industries:- CMP 1980 SL 1900 TGT 2150

Sector: Textiles Industry: Textiles

Business Area:

The company is primarily engaged in the manufacturing and sales of knitwear. The company has an enduring brand image in the hosiery market. With the rapid growth that the company has been experiencing, in both sales and profits, constantly expanding and innovating products and production techniques while manufacturing an uncompromising stance on comfort.The company has operations in India & caters to both domestic and international markets.

Technical Setup:

- Strong price momentum with volume

- Double bottom price formation on daily charts indicating a strong move above CMP1980

- Stocks trading above its all-important moving averages

Fundamental Setup:

- FII & FPI or institution increasing their shareholding

- The company has delivered good profit growth of 22.81% CAGR over the last 5 years

- The company has a good return on equity (ROE) track record: 3 Years ROE 27.66%

3. Carborundum Universal: CMP 571 SL 535 TGT 620

Sector: Capital Goods-Non Electrical Equipment Industry: Abrasives and Grinding Wheels

Business Area:

The company pioneered the manufacture of Coated Abrasives & bonded abrasives in India in addition to the manufacture of Super Refractories, Electro Minerals, Industrial Ceramics & ceramic fibers. The Company's range of varieties of Abrasives, Ceramics, Refractory products & electro-minerals is manufactured across several locations in & outside the country.

Technical Setup:

- Stock Formed Inverted Head & Shoulder kind of price pattern

- Increase in volume with the high delivery percentage in last few trading sessions

Fundamental Setup:

- The company has been maintaining a healthy dividend payout of 20.04%

- Company with reduced debt.

- FII & FPI or institution increasing their shareholding

- ROE & ROA is improving for last 2 years

Investment Pick

4. Gujarat Narmada Valley Fertilizers: CMP 367 TGT 485

Sector: Chemicals Industry: Fertilizers

Business Area:

Gujarat Narmada Valley Fertilizer& Chemical is one of India's Leading entities engaged in the manufacturing & selling of fertilizers, Industrial chemical products & providing IT services.

Products & Services:

GNFC Fertilizers GNFC Chemical

5. Information Technology ( For IT related products & services)

Fundamental Setup :

- Stocks are trading at 1.05 times its book value

- The company has delivered good profit growth of 25.77% CAGR over the last 5 years

- Stock is trading at 0.99 times its book value

- Over the last 5 years, the Debt to equity ratio has been 34.23% V/S industry average of 107.62%

- Growth in Net Profit with increasing Profit Margin (QoQ)

- Increasing Revenue every quarter for past 2 quarters

बुलियन रिपोर्ट: मुद्रास्फीति में बढ़ोतरी से सोने में मजबूती।

दो सप्ताह से सीमित दायरे में चल रही कीमती धातुओं में अक्षय तृतीया पर कीमतों में सपोर्ट देखने को मिला है। सोने की कीमतों में पिछले सप्ताह निचले स्तरों से 300 रुपये प्रति दस ग्राम सुधर कर 47600 और चाँदी की कीमते 600 रुपये प्रति किलो सुधर कर 70700 पर रही है। अमेरिका और यूरोप में घटते कोवीड मामले के कारण अर्थव्यवस्था मे सुधार हो रहा है जिसके कारण मुद्रास्फीति में बढ़ोतरी देखि गई है। गुरुवार को जारी अमेरिकी वार्षिक कंस्यूमर प्राइस इंडेक्स के आंकड़े 2.6 प्रतिशत से बढ़कर 4.2 प्रतिशत पर पहुंच गए, जिससे सोने के भाव को सपोर्ट मिला है।मुद्रास्फीति में बढ़त के कारण डॉलर इंडेक्स में उछाल देखने को मिला लेकिन अमेरिकी फ़ेडरल रिज़र्व की तरफ से ब्याज दरों में समय से पहले कोई बदलाव नहीं करने के बयान पर डॉलर में दबाव बना रहा। तेज़ी से होते टीकाकरण और बड़े राहत पैकेज से अमेरिकी आर्थिक आकड़ो मे मजबूती देखि गई है। अमेरिकी फ़ेडरल रिज़र्व के अधिकारिओ द्वारा मुद्रास्फीति में बढ़ोतरी को अस्थाई बताया है और अर्थव्यवस्था मे वर्ष के अंत तक अच्छी मजबूती आने की सम्भावना व्यक्त की है।हालाँकि आर्थिक विकास आने वाले वर्षो मे सामान्य गति से ही बढ़ने के संकेत भी दिए है। बढ़ती मुद्रास्फीति पर फेड का शांत बने रहना कीमती धातुओं के भाव को सपोर्ट कर रहा है। लंदन मेटल एक्सचेंज में औद्योगिक धातुओं के भाव में अप्रत्याशित बढ़ोतरी होने के कारण अतिरिक्त मार्जिन लगाने से औद्योगिक धातुओं में गिरावट रही जिसके चलते चाँदी की कीमतों में भी दबाव रहा।

तकनीकी विश्लेषण

घरेलु वायदा बाजार में सोने के भाव 47000 रुपये के ऊपर बने रहने में कामयाब हुए है जिससे इसमें तेज़ी बने रहने की सम्भावना है। सोने में 46400 पर सपोर्ट है तथा 48000 रुपये पर प्रतिरोध है। चाँदी में भी तेज़ी रहने की सम्भावना है। इसमें 69000 रुपये पर सपोर्ट है और 73000 रुपये पर प्रतिरोध है।

SEBI to Fix The Principles for The Listing of New Businesses

The Ministry of Company Affairs (MCA) has asked market controller SEBI to fix the principles for the listing of new businesses. It has requested SEBI to pull out some of the concessions given in the listing to new companies.

SEBI has proposed to diminish this cutoff from 70% to 40 per cent. However, if the startup is not making a profit, it can also be listed on the mainboard, provided the institutional investors hold a 75 per cent stake in the company. However, many startups have been seeking relief in the institutional investors' stake of 75 percent.

However, the MCA became more lenient and made the limit to be up to 50 per cent, to which SEBI agreed. There was no reaction to messages shipped off SEBI and MCA in regards to this matter.

SEBI HAS DECIDED TO FORCE ASSET ALLOCATION BY CONSIDERING EMPLOYEES 20% SALARY AS FUND UNITS

What is a Mutual Fund Scheme?

If you invest 20 thousand rupees in a scheme of a mutual fund. Its NAV is 200 rupees. In this case, you will get 100 units.

How 20,000 divided by 200 gives you 100. these units are a result of investing in the scheme. Now suppose that in a year the NAV rises from Rs 200 to Rs 300 and you decide to sell it. Now you will get 30,000 rupees.

What has SEBI decided?

MMC i.e. Asset Management Companies (mutual fund houses that run schemes) will now have to pay 20% of their fund managers' salaries in units of the same scheme.

Of which he is the fund manager. In such a situation, the funds of the fund managers would also be invested in those schemes. So the performance of the schemes can be improved. The salary of all the employees of the fund house will be paid similarly.

These units will be secured for a base time of three years and workers would not have the option to redeem such units. On account of infringement of a set of principles, misrepresentation, and gross carelessness, the units will be mauled back, and the redeemed sum will be credited to the plan.

What Role Does the Fund Manager Play In It?

The fund manager ensures that the investors keep getting good returns from the fund. The fund manager is also responsible for making the wrong decisions.

The fund manager trying to get higher returns by breaking the benchmark of its fund Suppose last year you got a return of 10 per cent, then the next year there is an attempt of 13 per cent. Also, the returns of the benchmark index i.e. Sensex-Nifty, Midcap, and Small-cap are compared with the returns of the fund.

Why has SEBI made this Decision?

SEBI has taken this choice. On the off chance that in a fiduciary business when senior staff has their investments it makes them oversee cash all the more capably. If something has turned out badly, it solidly falls on the shoulders of these folks so the fund managers who have the cash ought to oversee it with the full obligation.

In such a situation, the expectation of getting more investors will increase.

Positives

- Results in benefit for the investors.

- Transparency in the investing field as directors would now contribute more.

- The interest of key supervisors and unitholders of Mutual Fund plans will be on a similar balance.

- There will be an increase in the confidence of the Mutual fund investors in the AMCs and thus help raise the securities market.

- Fund managers will work efficiently after taking money from investors in the way of expense as they will now have ownership to the fund managers.

Negatives

- Forcing individuals is never a smart thought. The subtleties are prohibitive on somebody's personal asset allocation and personal savings.it is up to individuals and their different risk appetites as to what is their portfolio.

- It depends on the sum that people are saving. It depends on CTC thus it is not a small percentage of bonus. It is not a percentage of investments.

- There is No connection between employees and performance. Making managers perpetual insiders is certainly not a smart thought. it will not guarantee performance.

- Lastly, it resembles convincing corporate administration to purchase just their organization stock.

डॉलर में गिरावट से मजबूत हुए सोना -चाँदी।

कीमती धातुओं के भाव मुनाफा वसूली के बाद फिर तेज़ हुए है। कॉमेक्स में सोना 1820 डॉलर प्रति औंस के ऊपर निकल चुका है। कॉमेक्स वायदा चांदी भी 2745 सेंट के स्तरों पर पहुंच गई है। पिछले सप्ताह घरेलु वायदा सोना 2 प्रतिशत तक तेज़ हुआ और इसके भाव 46800 रुपय प्रति दस ग्राम के स्तरों पर रहे। चाँदी के भाव भी सप्ताह मे 5 प्रतिशत तेज़ हो कर 71600 रुपये प्रति किलो पर रहे। कोरोना के बढ़ते मामलो के कारण प्रमुख अर्थव्यवस्थाओं से जारी राहत पैकेज से मुद्रास्फीति बढ़ने का अनुमान है। बढ़ती मुद्रास्फीति के कारण सुरक्षित निवेश की मांग बढ़ी है।

भारत में बढ़ते कोविड मामलों के कारण वैश्विक अर्थव्यवस्था चिंता में है जिससे डॉलर में गिरावट देखि गई है। डॉलर एक सप्ताह के निचले स्तर पर आ गया है और अमेरिकी 10-वर्षीय ट्रेजरी की उपज, सकारात्मक आर्थिक आंकड़ों होने से दो सप्ताह के निचले स्तर के करीब पहुंच गई है। अमेरिका द्वारा गुरुवार को जारी किए गए बेरोज़गारी आकड़ों के मुताबिक पिछले सप्ताह की तुलना में 498,000 प्रारंभिक बेरोजगार दावे दर्ज किए गए है, जो मार्च 2020 के बाद से सबसे कम संख्या है। अमेरिकी पैरोल के आंकड़े अनुमान से कमजोर दर्ज किये गए जिससे कीमती धातुओं के भाव ऊपरी स्तरों पर बने रहने में कामयाब हुए है।

आगामी सम्भावना

इस सप्ताह कीमती धातुओं में तेज़ी रह सकती है। सोने मे 48500 रुपये पर प्रतिरोध है और 47500 रुपये पर सपोर्ट है। चाँदी में 73800 रुपये पर प्रतिरोध है तथा 70500 रुपये पर सपोर्ट है।

Impact of Second Wave of COVID 19 On Indian Stocks

The second wave of coronavirus seems to be very dangerous as it has badly hit the Indian economy. With new cases rising every day, state governments immediately came into action and imposed strict restrictions to curb the resurgence.

Although the curb is weaker than last year's pandemic, it somehow has started to affect several business activities.

Like last, the second wave of COVID 19 would heavily impact India’s Gross Domestic Product (GDP) growth in the coming months.

If we talk about business activities and the economy then the Indian stock market is also not untouched by this.

However, pessimism hasn't come up with the equity trading market so far. If you look at the last two month’s data, you will get to know that the NIFTY50 gets down by only 7% from its all-time high of 15,431.75.

Then what's the reason behind the market afloat?

Despite the critical situation across the country, analysts point towards the two factors that still maintain complacency in the stock market.

Several traders and expert analysts said that the global peers are doing well and that's the reason the Indian stock market trading is also performing well.

In other words, Global equity markets in the US have been in a good condition which is the main reason behind the drifts of the Indian stock market, The S&P 500, Dow Jones index touched an up of 4,195 and 34,200, this month.

It clearly shows that global equity markets are performing outstanding well and that makes a positive rub off on Indian equity markets as well.

As of now, we have not experienced a major decline in Indian equities despite having one of the highest infection rates in India - said Mr Sanjay Mookim, Research Head, JP Morgan Chase.

Besides, the hindsight of Indian investors makes the equity market more stable than before. The second wave reminds them of the mistakes they made in last year’s pandemic.

Therefore, they clearly say, even if the index goes down, they also go up. Also, last year, many fund managers made a huge mistake by selling a majority of stocks, this year they wouldn't.

Also, we have seen the equity market has bounced back from its position and hence the aggressive selling has not been done by many people, this time, Majoom said.

Naveen Kulkarni, CEO at Axis Securities Ltd, stated that “Prior experience shows how the stock market made a massive comeback post last year’s pandemic and therefore we don’t expect investors to offload equities hugely this year. This is because as the vaccination picks up the pace, the curve will flatten.

When a nationwide lockdown was announced in March 2020, the Nify50 went down by 13%. After 1 year, shares have grown up by double or sometimes even thrice. A recent analysis done by Mint report, in Nifty500 index, the stocks have shown the growth of more than 50% than last year and 247 stock’s price goes up by more than 100%, which is unbelievable and beyond the expectations of Indian investors.

Besides, the positive factors by global markets, RBI also put its eye on the Indian stock market. The monetary policy members of RBI still get worried about the economic growth. They are not in a favor of complete lockdown in the country.

Experiencing the rising cases of Covid positive, FIIs have sold equities worth $934 million so far this month.

What Should You Do?

Analysts suggest that your portfolio along with asset allocation tells your gain and loss. If you put loads of equity stocks in your portfolio, then it can also be quite risky as the stock market is seeing a bit of a downward trend. Therefore, it is suggested to add some growth stocks to your portfolio as it will minimize your risks.

Earnings Outlook

While the second wave of COVID poses challenges to the ongoing economic recovery, consumers and businesses have adapted to the new normal, and lockdowns are likely to be localised; hence, we do not expect this wave to derail the economy. Therefore, we don't expect any significant impact on aggregate earnings.

Amidst this second wave of the pandemic, some stocks are still performing exceptionally well. Here is a list of stocks to Bet Upon:

6 Economy-Related Stocks to Bet On

1. Divis Laboratories

Divis Laboratories is considered one of the leading manufacturers of Active Pharmaceutical ingredients (API) in the world. As per the reports, the company’s growth looks promising due to the diversification from China into other countries including India.

As many global players try to minimize the dependencies on China and prefer In dia, companies like Divis Laboratories remained well placed to capitalise on such opportunities.

Also, the company announced the construction of the Divis Unit-III Facility at Kakinada, East Godavari District, Andhra Pradesh.

2. CDSL

CDSL stands for Central Depository Service Limited. The company facilitates the transaction and holdings of securities in Demat form and settlement of trade which are executed on a stock exchange.

Other services include KYC services in respect of investors to capital market intermediaries, holding insurance policies in electronic form and other online services such as e-Locker, e-voting etc.

If we talk about the market share of CDSL, it has witnessed a massive growth from 14% in FY14 to 51% in FY2020 in the market share.

3. Dr. Reddy’s Laboratories

We can't ignore the performance of Dr Reddy’s Laboratories. Amidst the pandemic, the company has managed to generate revenue of Rs 4,930 Cr in FY21 which is up by 12%.

4. HDFC Bank

The bank’s strong fundamentals with good quarter to quarter growth makes HDFC one of the best choices among Indian retail investors. The company’s operating profit goes up by 22.83 per cent. Good revenues (up 29.10 %) and the approaching summer seasons are the good factors of this stock.

5. Havells India

The company gave a strong performance, with its operating profit going up by 22.83% whereas the revenues (29.10%) and profit (22.35%) also showed a positive side.

6. Voltas

Volta's growth in FY21 is also fascinating. Its operating profit (53.44% up), revenue (22.14% Up), gross profit (up 22.35%) and a reduction of interest expense make this stock is one of the highest-value stocks in the Indian stock market.

Mid Cap Rally in Indian Stock Market May Take a Breather Soon

Last year we faced a pandemic that was very difficult to comprehend not just for individuals, but also for the overall economy.

Now, even if the second wave of a pandemic is still on the rise, the S&P BSE Midcap Index has outperformed the benchmark S&P BSE Sensex Index in the last five months since the end of 2019.

If we compare the performance of mid-cap stocks to last year, we will get to know that these companies had suffered a lot in 2019 but today, we don't see a major change in these stock’s prices.

In fact, the outperformance of India’s mid-cap stocks over their larger peers may take a deep breather, as per the new investors. In the fiscal year 2021, the BSE midcap index rose 91% as India’s market capitalization rose up to Rs91 trillion in a year and hence we can predict that the BSE Sensex Index has outperformed the Sensex post end of the pandemic; according to Bloomberg data.

Even the smaller stock of mid-cap companies has gained approximately 33% in a short period, which is more than double according to the set benchmark.

Mid Cap Stocks May Stop Growing Upwards: Rising Cases

As the mid-cap stocks outperformed the large-cap stocks in 2020, this year the experts predict that these stocks may hit a pause because of the second surge of COVID 19 infections across the country.

Due to the sudden pandemic, many investors are seeking large-cap stocks, especially in Bank stocks. In the current situation, everyone wants to play safe and therefore, investors find large-cap stocks (primarily bank stocks) are the safest options to invest in.

Mid-cap stocks may take a pause for some time but the performance depends a lot on the pace of vaccination. Last week, the Indian government announced that the vaccines will be available for everyone ranging over the age of 18, applicable from May 1.

As of now, India has vaccinated over 13 crore vaccinated doses and by doing this, the country becomes one of the fastest nations to vaccinate many people within a short span of time.

Earlier, investors used to be attracted towards mid-cap stocks as these stocks were relatively cheaper than other stocks, but that’s not the condition anymore. Nowadays, large companies are better equipped to handle crises and therefore these stocks are becoming the top priority of investors.

How Midcaps Fared Thus Far (Change)

Mid-cap companies in India are those who have a market capitalization of Rs 5k Crore and less than Rs 20k Crore. These companies come under the top 100 companies that are listed on the stock exchanges (BSE and NSE). If we compare mid-cap stocks with the small caps, you will find out that the mid-cap stocks come with a moderate risk as compared to small-cap stocks. The risks of these stocks are comparatively higher than large-cap stocks.

Another advantage of applying for mid-cap stocks is that these stocks offer an opportunity for growth and in future, these stocks perform well with outstanding returns than large-cap stocks.

Mid-cap stocks are mainly responsible for boosting up the market share and profitability.

According to the present situation, the markets are in rallied mode, and when such things happen, investors are generally inclined towards large-caps, however, after the crash of 2020, investors have started to channelize their portfolio into mid-cap and small-cap stocks.

The primary factor that worked in the favor of mid-cap stocks is its low-interest regime that has been controlled by the Reserve Bank of India. Because of the low-interest rates, the capacity of taking risk appetite increases, which makes investors invest more in mid-cap stocks than other stocks.

Experts see a strong connection between the midcap index and repo rates. High liquidity and moderate risks are the major factors that contribute to the mid-cap rally.

A brokerage house says, whenever there is a disturbance, it has been followed by outperformance in mid-cap and small-cap indices. The same trend has been noticed in 2009, 2016, and 2017. This year: in March 2021, the Midcap Index outperformed both the Nifty Small-Cap and Nifty 50 indices.

If we see the performance of the Nifty Midcap index over the others, then last year, the Nifty mid-cap index bounced back by over 70 percent post-pandemic. However, Smallcap indices gained 19% in 2020.

Correction Phase

As the second wave of infections is still on the rise, the major indices of India Sensex and Nifty have seen some contraction this month. On April 20, Sensex fell 10 percent, after maintaining an all-time high of 52k levels in February. The Nifty has also gone down by 6% to 14,296 levels on April 20, after witnessing a peak of 15k levels.

Looking at the current scenario, investors are moving towards large-cap stocks considering it as the safest option to invest at this time.

However, the movement of investors toward large-cap stocks is temporary, they are doing this only because of market volatility. Once the market returns to its original pace, investors will prefer mid-cap stocks over long-term stocks.

Market Move in the Next Months

The ease of availability of vaccines, and economic recovery are some of the factors that may decide the market way; which way the stock market will move in the future.

According to the credit rating agency, Moody, the second wave will definitely hurt the economy which may affect the country’s future growth, however, the agency has also stated that the economy will grow in the double digits after a few months.

Conclusion

If the second wave curbs quickly and the economic resurgence gets started then mid-cap stocks will become the investor’s first choice over large-cap stocks. In 2020, when the stock market fell, the market saw a big bull which extended up to 2021.

Due to the unpredictability of the stock market, mid-cap stocks too had an unbeaten run. Although the mid-cap market sees a slower pace in the market, they will rise once the market regains and all things come at a normal pace.

India’s Economic Growth Won't be Derailed by Second Wave of COVID 19: RBI Governor Shaktikant Das

Two months ago, no one could have predicted that April would be the worst month of 2021 with an increasing number of COVID 19 infections among patients. The second wave of Covid 19 seems to be very fierce as it has already started slowing down the economic growth of the country while the inflation rate remains high.

Amid this uncertainty, Reserve Bank of India governor Shaktikanta Das on Thursday gave a positive statement regarding the economic activities held in the country.

He confidently said that the new wave of COVID 19 would not derail the economic journey. He maintained the RBI’s recent 10.5 percent growth forecast for the upcoming fiscal year (FY 2022). In other words, RBI Governor Shaktikanta Das has come up with an exclusive idea of keeping liquidity sufficient enough to rein in yield, preventing the currency from appreciating and inflation from going upside.

The governor’s assurance assumes significance amid apprehension about surging new COVID cases and resultant lockdown being clamped in many cities.

Many states along with the COVID hotspot state of India - Maharashtra that has marked a huge number of cases more than 50,000; are seeing a massive surge in pandemic infections, irritating the equity and bond market.

The worry is that most of these infections are caused by the strain that came this year but not the initial COVID 19 that killed over 1.5 lakh people in the country.

It may be noted that the RBI governor has given a 10.5% growth for FY 22 and the governor firmly believes that never sees a downward revision in 10.5% growth. He also does not believe that the complete lockdown will be held this year which the country witnessed last year.

When the developed markets are unleashing large fiscal stimuli, U.S. treasury yields are rising and commodity prices are going down.

The inflation rate for the Feb month was around 5 %, however, the core inflation rate in January was at 6%. Now, some economists say, there is a chance that the inflation rate could oscillate between 5.5% to 6%.

Fortunately, some helpful base effects are expected to hold down food prices.

Growth: A New Concern

The Indian economy somehow returned to its original track i.e. growth in the last quarter of the year 2020 and is expected to surge again by the end of March. However, with the rising Covid 19 infections, the sequential growth may drop thereafter.

As the cases are rising with strict state-wise restrictions, the country expects soft, steady growth in Q1 FY 22, financial experts said in one of her reports.

RBI clearly monitors the growth factor of the Indian economy, keeping the inflation rate in mind. According to Madhavi Arora, an economist at Emkay Global, RBI leaves no stone unturned in maintaining FY 22 growth.

Rising Inflation Can't Be Ignored

Rising Covid infections lead to high inflation that even MPC will not be able to ignore the inflation effect. Retail inflation rose to 5.03% which is a three month high in February as food prices saw a modern bounce back. According to the MPC said in its last meeting, fundamental requirements such as food, fuel all have risen.

Maintaining retail inflation at 4% with a margin of 2% is a quite challenging task, especially in the current circumstances, said Govinda Rao, chief economic advisor at Brickwork ratings.

As the inflation rate is still moving upward, excess liquidity and volatility in crude oil prices could lead to upward risk, Rao further said. Once the current output gap narrows, surplus liquidity conditions could put pressure on prices, and the RBI will have to be vigilant.

Liquidity: Excesses to Continue

At the last of the last MPC, RBI had decided to restore CRR (cash reserve ratio) in two phases. However, Governor Shaktikanta Das had assured to maintain the market liquidity despite restoring a huge amount of CRR. Also, he mentioned that a reversal of CRR cut will be given to central bank space to conduct larger bond purchases.

Rao further said, the RBI may likely drain excess liquidity. But given the higher government borrowings, which may put pressure on bond yields, the RBI may go slow in reversing its liquidity measures.

The RBI also all set to announce its first monetary policy in the first week of April. Also, high government borrowings at record high leads to soaring yields. Shaktikanta Das said, there is no fight between the central bank and the bond market.

The governor further assured, the RBI will ensure the bond purchases are of equal quantum. The RBI’s foreign exchange reserves are all its requirements.

The government took a new decision to privatize the state-run bank, he said the central bank is in continuous discussions with the RBI on the same. The centre always took into consideration the viewpoint of the regulator on such issues, he said.

Also, RBI is working on a central bank digital currency (CBDC). RBI’s stance on cryptocurrency has revealed that it will bring a new bill on cryptocurrencies.

It has been noticed that there are few practical operationalizations of CBDC which makes RBI more responsible while launching a safe and robust model. RBI further said that the UPI can act as the best medium for providing the best yet fast services for cross border payments.

Adding to this, Shaktikanta Das, further said the day is not too far when we (India) will experience cheaper, safer and faster cross border remittances, adding Rupay card which in future, will make a mark in the global financial landscape.

Bottom Line

Needless to say, the second wave of infections badly threatens the economy which in turn increases inflation to a greater extent. Growth is clearly losing its momentum as many sectors fail to generate revenue in the upcoming months.

At this point in time where the second wave of COVID ruins almost everything, many investors are trying to save their money for future perspective. Therefore, many investors are seeking the best stock broking company which help them to grow business financially.

कच्चे तेल का उत्पादन बढ़ने से कीमतों पर दबाव पड़ने की संभावना है

शुक्रवार को हुई ओपेक और नॉन ओपेक देशो की बैठक के कारण कच्चे तेल के भाव मे उठापटक देखि गई। ओपेक देशो के आश्वासनों से पहले क्रूड की कीमतें गुरुवार से अस्थिर रही, क्योंकि मांग बढ़ोतरी मे संदेह के बावजूद, मई से वैश्विक तेल उत्पादन बढ़ने की सहमति हुई है।

ओपेक और नॉन ओपेक देशो के सदस्य, दो-दिवसीय कॉन्फरेंस के माध्यम से बैठक करते हुए, मई और जून में प्रति दिन 350,000 बैरल और जुलाई में 400,000 बैरल प्रतिदिन उत्पादन बढ़ाने पर सहमत हुए है।

सऊदी अरब को कटौती के प्रति दिन 250,000 बैरल मई और जून में घटाने पर विचार करना था, ताकि बाजार को निरंतर समर्थन प्रदान किया जा सके। लेकिन इसने उस विचार को अन्य उत्पादकों के साथ आम सहमति पर पहुंचने के बाद समाप्त कर दिया कि उत्पादन मे बढ़ोतरी तेल मांग मे बढ़ोतरी के अनुरूप है। लगभग 2.5 मिलियन बैरल प्रति दिन, कई सप्ताह तक रुके रहने के बाद, अमेरिकी कच्चे तेल का निर्यात पिछले हफ्ते बढ़कर 3.2 लाख बैरल प्रति दिन हो गया है।

अमेरिकी तेल उत्पादन भी पिछले सप्ताह बढ़कर 11.1 लाख बैरल प्रतिदिन हो गया है। पिछले कुछ महीनों में संयुक्त राज्य अमेरिका के लिए 11 मिलियन बैरल या उससे कम का दैनिक उत्पादन मानक बना हुआ था। कॉमेक्स मे कच्चे तेल के भाव सप्ताह मे मामूली बढ़त के साथ 61 डॉलर तथा ब्रेंट कच्चा तेल 64.7 डॉलर और घरेलु कच्चे तेल की कीमते 4516 रुपये प्रति बैरल पर रही।

तकनिकी विश्लेषण

कच्चे तेल की कीमतों मे ऊपरी स्तरों पर दबाव रहने की सम्भावना है। इसमें 4670 रुपये पर प्रतिरोध तथा 4300 रुपय पर सपोर्ट है।

डॉलर इंडेक्स में मजबूती से दबाव में कीमती धातुएँ।

मार्च के शुरुवाती महीने में निचले स्तरों से उछाल होने के बाद कीमती धातुओं के भाव मे दबाव बढ़ने लगा है। सोने में पिछले दो सप्ताह तक कीमते सकारात्मक रहने के बाद पिछले सप्ताह ऊपरी स्तरों पर दबाव बना और घरेलु वायदा सोने मे 500 रुपय प्रति दस ग्राम की मंदी देखि गई और कीमते 44500 रुपय के स्तरों पर रही। चांदी के भाव में ऊपरी स्तरों से 4900 रुपय प्रति किलो तक की साप्ताहिक मंदी देखि गई, लेकिन इसमें निचले स्तरों से सुधार भी आया और चांदी के भाव सप्ताह मे 2500 रुपय की मंदी रहने के साथ 65000 रुपय प्रति किलो के करीब कारोबार किया।

डॉलर इंडेक्स अपने निचले स्तरों से ऊपर बढ़ने की कोशिश मे दिखाई पड़ता है। जो सोने की कीमतों को आगे भी दबाव मे रख सकता है। बढ़ती हुई ट्रेज़री उपज ने भी सोने की कीमतों पर दबाव बनाया है। पिछले सप्ताह अमेरिका से जारी होने वाले बेरोज़गारी के दावे एक साल के निचले स्तरों पर पहुंच गए है। अमेरिकी तिमाही जीडीपी मे भी बढ़त दर्ज की गई है।

अर्थव्यवस्था मे सुधार से ट्रेज़री उपज में बढ़त होने से निवेशकों का रुझान बॉन्ड निवेश मे बढ़ा है जो डॉलर को सपोर्ट कर रहा है। उभरती अर्थव्यवस्थाओं की मुद्राओं मे रुपया डॉलर की अपेक्षा मजबूत हुआ है और एक साल की उचाई पर पहुंच गया है। सोने मे कस्टम ड्यूटी घटने के बाद, रुपये मे मजबूती आयात को सस्ता बना रहा है जिससे सोने की कीमतों मे दबाव है। सोने मे वर्तमान निचले स्तरों पर ज्वेलर्स की मांग बढ़ने की सम्भावना है।

आगामी सम्भावना

इस सप्ताह सोने के भाव में दबाव बना रह सकता और अप्रैल वायदा सोने मे 43700 रुपये पर सपोर्ट है और 45200 रुपये पर प्रतिरोध है। चांदी में 63500 रुपये पर सपोर्ट तथा 68500 रुपये पर प्रतिरोध है।

LAXMI ORGANIC | Laxmi Organic Industries Ltd IPO

Laxmi Organic is a leading manufacturer of Acetyl Intermediates and Specialty Intermediates with almost three decades of experience in the large scale manufacturing of chemicals. Since its inception in 1989, it has been on a journey of transformation.

It initially started manufacturing acetaldehyde and acetic acid in 1992, and soon thereafter moved on to manufacturing ethyl acetate in 1996. It is currently among the largest manufacturers of ethyl acetate in India with a market share of approximately 30% of the Indian ethyl acetate market.

Laxmi Organic is the only manufacturer of diketene derivatives in India with a market share of approximately 55 % of the Indian diketene derivatives market in terms of revenue in Fiscal 2020 and one of the largest portfolios of diketene products. Its products are currently divided into two broad categories, namely the Acetyl Intermediates and Specialty Intermediates.

Alembic Pharmaceuticals Limited, Laurus Labs Limited, Granules India Limited, Hetero Labs Limited, Heubach Colour Private Limited, Hubergroup India Private Limited, Huhtamaki India Limited, Macleods Pharmaceuticals Private Limited, Suven Pharmaceuticals Limited, Colourtex Industries Private Limited, and UPL Limited are some of its customers.

The company has a global footprint with customers in 30 countries including but not restricted to China, Russia, Singapore, UAE, UK, USA, Netherland, etc. Currently, it has 2 manufacturing facilities in Mahad, Maharashtra for the manufacturing of AI and SI products. It is also proposing to set-up a new manufacturing facility at Lote Parshuram, Maharashtra to manufacture four speciality chemicals.

Product Portfolio:

The products currently manufactured by us are divided into two categories, namely the Acetyl Intermediates and Specialty Intermediates.

Acetyl Intermediates:

The Acetyl Intermediates find application in inter alia the pharmaceuticals, agrochemicals, inks and paints, coatings, printing, packaging, and adhesives industries. Ethyl acetate is used in multiple industries as a solvent.

Speciality Intermediates:

Specialty Intermediates comprise more than 34 products which include ketene, diketene derivatives namely esters, acetic anhydride, amides, arylides and other chemicals. Speciality Intermediates find application in inter alia the pharmaceuticals, agrochemicals, dyes and pigments.

Strength of the Company

- Leading manufacturer of ethyl acetate in India.

- The largest manufacturer of diketene derivative products.

- Diversified customer base across industries.

- Strategically located manufacturing facilities.

- Consistent financial performance.

RISKS RELATING TO BUSINESS

- Any failure to commercialize new products may adversely impact a company’s business.

- Any shortfall in the supply of our raw materials has an adverse effect on business

- The company is exposed to foreign currency exchange risks which may adversely impact the results of operations

- Any significant fall in global prices of products may have an adverse effect on business

- Disruptions of logistics could adversely affect our business and the results of operations.

IPO DetailsIPO DateMarch 15th, 2021 to March 17th, 2021Issue TypeBook Built Issue IPOIssue Size45,15,38,46 Equity Shares of ₹2 (aggregating up to ₹600.00 Cr)Fresh Issue23,07,69,23 Equity Shares of ₹2 (aggregating up to ₹300.00 Cr)Offer for Sale23,07,69,23 Equity Shares of ₹2 (aggregating up to ₹300.00 Cr)Face ValueRs.2 per equity shareIPO Price RangeRs.129 to Rs.130 per equity shareMinimum Order Quantity115 sharesListing AtBSE, NSE

IPO Objective:

The company purposes to utilize funds towards the following objectives:

- Investment in Yellowstone Fine Chemicals Private Limited (“YFCPL”)for funding its working capital requirements

- Funding capital expenditure requirements for expansion of its SI Manufacturing Facility

- Funding working capital requirements of the Company

- Purchase of plant and machinery for augmenting infrastructure development at its SI Manufacturing Facility

- Prepayment or repayment of all or a portion of certain outstanding borrowings availed by the Company & its wholly-owned Subsidiary, Viva Lifesciences Private Limited

Financial Performance:

Laxmi Organic’s financial performance (in INR crore)Financial YearFY2018FY2019FY2020H1 FY2021Revenue1,396.11,574.31,538.6814.4Expenses1,282.81,476.31,483.5758.2Net income76.072.369.745.6Net margin: (%)5.44.64.55.6

Tentative Time Table:

- IPO Opens on 15 March 2021

- IPO Closes on 17 March 2021

- Basis of Allotment Date: Mar 22, 2021

- Initiation of Refunds: Mar 23, 2021

- A credit of Shares to Demat Account: Mar 24, 2021

- IPO Listing Date: Mar 25, 2021

Outlook:

Incorporated in 1989, Laxmi Organic Industries Ltd is a specialty chemical manufacturer that operates in 2 business segments; Acetyl Intermediates (AI) and Specialty Intermediates (SI)

According to the Frost & Sullivan Report, given its expertise in the Acetyl Intermediates and the Specialty Intermediates segments, its entry into the fluorochemicals space will put it in a differentiated position from other chemical manufacturers.

Laxmi Organic has been the largest exporter of ethyl acetate from India in the six months ended September 30, 2020, and Fiscals 2020, 2019, and 2018 and one of the largest exporters of ethyl acetate to Europe from India since 2012.

For the six months ended September 30, 2020, and the Fiscals 2020, 2019, and 2018, its Company’s revenue from exports of manufactured products contributed 23.17%, 24.24%, 27.80%, and 22.18%, respectively, of its revenue from operations on a standalone basis.

The company has had stable revenue growth over the last three years though the company has not grown significantly over the same period, while we can see a decline in net profits too. The margins of the company have been stable varying between 4%-6%.

At the upper price band of Rs. 130 and EPS of Rs. 2.86, the PE works out to be 37.68 which is higher than the industry average of 21.70. However, their entry into a high margin business of specialty fluorochemicals though the IPO justifies the higher PE.

Eyeing the growth of the intermediaries industry and its growth globally we may expect the company to do well in the upcoming years. Laxmi Organic was the largest exporter of ethyl acetate from India in the six months ending September 2020. We may expect the company to do much better with the new acquisition.

Kalyan Jeweller’s India Limited IPO

Kalyan Jewellers is one of the largest jewellery companies in India based on revenue as of March 31, 2020. It started its jewellery business in 1993 with a single showroom in Thrissur, Kerala.

The key business activities of the company are to design, manufacture, and sell a variety of gold, studded and other jewellery products for various occasions i.e. wedding, festivals, etc.

Initially, the company was started with a single showroom in Kerala, and over the years, it has expanded its presence with 107 showrooms located across 21 states and union territories in India.

It not just serves the domestic market but also serves overseas customers with 30 showrooms located in the Middle East. The company generates a significant portion of revenues from gold jewellery, accounted for 74.77% in fiscal 2020 followed by studded (diamond and precious stone) and other jewellery segments.

Kalyan Jewellers designs manufacture and sells a wide range of gold, studded and other jewellery products across various price points ranging from jewellery for special occasions, such as weddings, which is its highest-selling product category, to daily-wear jewellery.

Product Portfolio:

The company design, manufacture and sell a wide range of jewellery products at varying price points for uses ranging from jewellery for special occasions such as weddings, which is our highest sold product category, to daily-wear jewellery.

Product Category:

- gold jewellery,

- studded jewellery (including diamond) and

- other jewellery (including platinum jewellery and silver jewellery)

Strength of the Company

- One of India's largest jewellery companies.

- Trusted Jewelry brand.

- Strong network distribution with global outreach.

- Wide range of jewellery product offerings.

- Experienced promoters and managers.

RISKS RELATING TO BUSINESS:

- Changes or a downturn in economic conditions may affect consumer spending, including on a company’s products.

- The company may be unable to expand our product offerings and distribution channels

- The company’s income and sales are subject to seasonal fluctuations which may have a disproportionate effect on the results of operations.

- Company’s business depends on promoters and senior management and their ability to attract and retain sales personnel

IPO Details:

IPO Date March 16th, 2021 to March 18th, 2021Issue Type Book Built Issue IPO Issue Size135057471 Eq Shares of ₹10(aggregating up to ₹1,175.00 Cr)Fresh Issue91954023 Eq Shares of ₹10(aggregating up to ₹800.00 Cr)Offer for Sale43103448 Eq Shares of ₹10(aggregating up to ₹375.00 Cr)Face ValueRs.10 per equity share IPO PriceRs.86 to Rs.87 equity share Min Order Quantity 172 Listing At BSE, NSE

IPO Objective:

The company purposes to utilize funds towards the following objectives:

- To finance business working capital requirements.

- To meet general corporate purposes.

Financial Performance:

Kalyan Jewellers’ financial performance (in INR crore)FY2018FY2019FY20209M FY2021Revenue10,580.29,814.010,181.05,549.8Expenses10,366.49,793.19,960.15,608.9Net income140.9-4.8142.2-79.9Margin (%)1.30.01.4-1.4

Tentative Time Table:

IPO Opens on 16 March 2021

IPO Closes on 18 March 2021

Basis of Allotment Date: Mar 24, 2021

Initiation of Refunds: Mar 2021

Credit of Shares to Demat Account: Mar 2021

IPO Listing Date: Mar 26, 2021

Outlook:

Kalyan Jeweller is one of India’s largest jewellery companies with a pan-India presence. The hyperlocal strategy enables the company to cater to a wide range of geographies and customer segments.

In Fiscal 2020, 78.19% of its revenue was from India and 21.81% was from the Middle East. Over the same period, 74.77% of its revenue from operations was from the sale of gold jewellery, 23.36% was from the sale of studded jewellery (which includes diamonds and precious stones), and 1.87% was from the sale of other jewellery.

In fact, in Fiscal 2019, the revenue earned fell by over 9%. This was attributed due to an experimental strategy that the company adopted in that year. The questionable strategy was withdrawn after that year, and the revenue again increased by 3.58%. As the revenue from operations declined in FY 2019, this is also reflected by the net profit earned by the profit.

Another factor that can contribute to the dismal performance in FY 2019 is the severe floods that hit the southern part of India during this time. Owing to this, the demand for gold jewellery was affected.

The total assets owned by the company has shown a CAGR of 5.02% between 2017 and 2020. One positive fact to note here is that the long-term debt of Kalyan Jewellers has shown a consistent decline over the years.

As for India, expenditure on jewellery is one of the top constituents of retail consumption. In 2020, the amount spent on jewellery amounted to Rs. 449 thousand crores. This is expected to grow to Rs. 633 thousand crores by 2025 which will surely benefit the company in the long run.

Craftsman Automation Ltd IPO

Incorporated in 1986, Craftsman Automation Ltd is a leading engineering organization that is engaged in manufacturing precision components. The company designs, develops and manufactures a range of engineering products. It is one of the leading players in the machining of cylinder blocks for the tractor segment.

The business operates 3 key segments namely Automotive-Powertrain and others, Automotive-Aluminium Products, and Industrial and Engineering division that is engaged in manufacturing material handling equipment i.e. hoists, industrial gears, marine engines, crane kits, gearboxes, locomotive equipment, storage solutions, etc.

The company owns 12 state-of-the-art manufacturing facilities across 7 cities of India. Its customer base includes Tata Motors, Daimler India, Tata Cummins, Mahindra & Mahindra, Royal Enfield, Siemens, Escorts, Ashok Leyland, VE Commercial Vehicles, TAFE Motors & Tractors, etc.

Furthermore, it has two wholly-owned overseas subsidiaries, namely Craftsman Marine B.V. and Craftsman Automation Singapore Pte Limited. Craftsman Marine B.V. is engaged in the marketing, sales, and servicing of marine engines, engineering products and accessories for propulsion, manoeuvring and steering parts, storage, electronic instruments, deck equipment and spare parts for all the engines and other equipment used in yachts.

These products are manufactured and assembled by us in India and sold under the name “Craftsman Marine” by our subsidiary. Craftsman Automation Singapore Pte Limited, also set up in 2008 in Singapore, is its strategic sourcing centre for overseas procurement, primarily for procurement of aluminum ingots, which is one of its key raw materials.

Product Portfolio:

The company has three business segments :

Automotive – Powertrain and Others

Automotive – Powertrain and Others segment include engine parts such as cylinder block and cylinder head, camshafts, transmission parts, gear box housings, turbo charges and bearing caps.

Automotive – Aluminium Products

The Aluminium Products segment include crank case and cylinder blocks for two-wheelers, engine and structural parts for passenger vehicles and gearbox housing for a heavy commercial vehicle.

Industrial & Engineering Segment

This segment can be divided into two sub-segments, namely, High-End Sub-Assembly, Contract Manufacturing & Others and Storage Solution & Material Handling.

Strength of the Company

- Leading engineering product manufacturer.

- Strategically located and vertically integrated manufacturing facilities.

- Strong product design capabilities.

- Robust financial performance.

RISKS RELATING TO BUSINESS

- Company’s Inability to meet obligations under debt financing arrangements could adversely affect business.

- Group Companies have incurred losses in the last three Fiscals.

- The company do not have long term contracts with any of our supplier which could adversely affect their business.

- The company is subject to risks arising from interest rate fluctuations, which could adversely affect its results.

- The company has been unable to locate certain of its corporate records.

IPO Details:

IPO DateMarch 15th, 2021 to March 17th, 2021Issue TypeBook Built Issue IPO Issue Size5528161 Eq Shares of ₹5(aggregating up to ₹823.70 Cr)Fresh Issue1,006,711 Eq Shares of ₹5(aggregating up to ₹150.00 Cr)Offer for Sale4,521,450 Eq Shares of ₹5(aggregating up to ₹673.70 Cr)Face ValueRs.5 per equity shareIPO PriceRs.1488 to Rs.1490 equity shareMin Order Quantity10Listing AtBSE, NSE

IPO Objective:

The company purposes to utilize funds towards the following objectives;

- To make repayment/pre-payment of company's borrowing fully or partially.

- To meet general corporate purposes.

Financial Performance:

Craftsman Automation’s financial performance (in INR crore)FY2018FY2019FY2020H1 FY2021Revenue1,522.91,831.61,501.1536.5Expenses1,479.61,692.11,437.9526.1Net income25.687.841.75.6Net margin: (%)1.74.82.81.0

Tentative Time Table:

- IPO Opens on 15 March 2021

- IPO Closes on 17 March 2021

- Basis of Allotment Date: Mar 22, 2021

- Initiation of Refunds: Mar 23, 2021

- The credit of Shares to Demat Account: Mar 24, 2021

- IPO Listing Date: Mar 25, 2021

Outlook:

Craftsman Automation commenced its operations in 1986 in Coimbatore, in the State of Tamil Nadu, India. It is a diversified engineering company with vertically integrated manufacturing capabilities.

It is the largest player involved in the machining of cylinder blocks and cylinder heads in the medium and heavy commercial vehicles category. Craftsman owns and operates 11 strategically located manufacturing facilities across seven cities in India, with a total built-up area of over 1.5 million sq. ft.

The revenues of the company have been in a declining mode over the last three years. However, the key point to note is that over the last five years the auto sector has not done pretty well and we are seeing a turnaround in the industry after the lockdown and Craftsman automation is doing well since then.

Craftsman is the top 3-4 component manufacturers with respect to cylinder block matching in the case of the tractor industry, which is a very positive thing for the company and we expect things to do better form year.

At the upper price band of Rs. 1490 and 3 years average EPS of Rs. 28.95 the PE works out to be 51x as while current the PE of the industry is 60.7x. The valuations of the company look attractive at the current level and as the auto industry is expected to do well in the near future we may expect that company should do well too.

Anupam Rasayan India Limited IPO

Anupam Rasayan India Limited is one of the leading companies engaged in the custom synthesis and manufacturing of specialty chemicals in India. The company started business as a partnership firm in 1984 as a manufacturer of conventional products.

Their business verticals are (i) life science-related specialty chemicals comprising products related to agrochemicals, personal care and pharmaceuticals, and (ii) other specialty chemicals, comprising specialty pigment and dyes, and polymer additives, company’s focus is to manufacture products with sustainability using our continuous process technology through flow chemistry and photochemistry, greater R&D and engineering capabilities to deliver values for customers for their complex and multi-step synthesis projects.

Green manufacturing and green growth have always been at the top of the agenda, they have developed new eco-friendly, safer and novel routes for many products. Most of these products have been introduced on an exclusive basis for their customers.

Certain of their facilities are ISO 9001:2015 and ISO 14001:2015 certified companies with sound technology, environment consciousness, rich history of innovation through research, and a total commitment to excellence towards quality and sustainability.

There are six manufacturing sites that are located in the state of Gujarat: 4 sites are in Sachin, Surat and 2 state of art sites are in Jhagadia, Gujarat.

Product Portfolio:

The company’s products and services are organized primarily in the following segments:

- The company manufactures agro intermediates and agro active ingredients for the agrochemicals industry which are used in the manufacture of insecticides, fungicides and herbicides.

- For the personal care industry, companies provide anti-bacterial and ultraviolet protection intermediates and ingredients

- In the pharmaceutical segment, companies focus on developing intermediates and ‘key starting materials’ for active pharmaceutical ingredients, and may also be used in material sciences and surface chemistry.

Strengths of the Company

- Strong and long-term relationships with diversified customers across geographies with significant entry barriers

- The core focus on process innovation through consistent R&D, value engineering and complex chemistries

- Diversified and customized product portfolio with a strong supply chain

- Automated manufacturing facilities with a strong focus on the environment, sustainability, health, and safety measure

- Consistent track record of financial performance

- Experienced promoters and a strong management team.

RISKS RELATING TO BUSINESS

- Any unplanned or prolonged disruption of our manufacturing operations could materially and adversely affect business

- The shortfall in the availability or quality of raw materials could have an adverse effect on business and the results of operations

- Any failure to raise additional financing could have an adverse effect on business

- Any failure to comply with quality standards may adversely affect business

- Reduction in demand for products could adversely affect our business, results of operations, financial condition, and cash flows

IPO Details:

IPO Date March 12th, 2021 to March 16th, 2021 Issue Type Book Built Issue IPO Issue Size Rs 760 Cr Fresh Issue 13693693 Equity Shares aggregating to Rs 760 Cr Offer for Sale NIL Face Value Rs.10 per equity share IPO Price Rs.553 to Rs.555 equity share Min Order Quantity 27 Listing At BSE, NSE

IPO Objective:

The net proceeds of the Issue, i.e. Gross proceeds of the Issue less the Issue expenses (“Net Proceeds”) are proposed to be utilized in the following manner:

- Repayment/prepayment of certain indebtedness availed by our Company (including accrued interest)

- General corporate purposes

Financial Performance:

FY2018FY2019FY20209M FY2021Revenue349.2521.0539.4563.2Expenses299.4455.2468.0496.4Net income40.149.351.247.1Net margin: (%)11.59.59.58.4

Tentative Time Table:

- Price Band announced 8 March 2021

- IPO Opens on 12 March 2021

- IPO Closes on 16 March 2021

- IPO Allotment on 19 March 2021

- Unblocking ASBA 22 March 2021

- Credit to Demat Accounts 23 March 2021

- IPO Listing on 24 March 2021

Outlook:

Anupam Rasayan commenced operations in 1984 as a partnership firm with conventional products and now it makes specialty chemicals that involve multi-step synthesis and complex chemistries.

The company’s R&D team has successfully carried out the multi-step synthesis and scale-up for several new molecules in the area of life sciences related specialty chemicals and other specialty chemicals, and as a result, expanded its commercialized product portfolio from 25 products in Fiscal 2018 to 34 products in Fiscal 2020 and 36 products in the six months September 30, 2020

The company’s total revenue has increased at a CAGR of 24.29% from Rs 3,49.1 Cr in FY18 to Rs 5,39.3 Cr in FY20 and was Rs 2,37.5 Cr and Rs 3,73.5Cr in the six months ended September 30, 2019, and 2020, respectively.

EBITDA for the year 2018, 2019, 2020 and the six months ended September 30, 2019 and 2020 was Rs 74.5 Cr, Rs 92.1 Cr, Rs 1,34.8Cr, Rs 57.5 Cr, Rs 77.4 Cr, respectively while its EBITDA margin was 21.82%, 18.38%, 25.51%, 24.55% and 21.79%, respectively, for similar periods.

Its profit after tax and share of profit of associates was Rs 41.3 Cr, Rs 49.2Cr, Rs 52.9 Cr, Rs 21.7 Cr and Rs 26.4 Cr for Fiscals 2018, 2019, 2020 and the six months ended September 30, 2019, and 2020, respectively, while it's PAT margin was 11.83%, 9.45%, 9.82%, 9.15% and 7.09%.

The company’s revenue and PAT have increased over the year but the margins have declined. At an upper price band of Rs 555 and EPS of 6.94, the PE comes out to be 79.97 which is higher than the PE of peers which is at 42.81.

Eyeing the growth of specialty chemical business we may expect to see a boost in revenue and profit. However, companies might have to work on the margin front. The company would be paying off debt by raising money from the IPO which will help in gaining the margins going further.

MTAR Technologies Limited IPO

Incorporated in 1999, MTAR Technologies is a leading national player in the precision engineering industry. The company is primarily engaged in the manufacturing of mission-critical precision components with close tolerance and in critical assemblies through its precision machining, assembly, specialized fabrication, testing, and quality control processes.

Since its inception, MTAR Technologies has significantly expanded its product portfolio including critical assemblies i.e. Liquid propulsion engines to GSLV Mark III, Base Shroud Assembly & Airframes for Agni Programs, Actuators for LCA, power units for fuel cells, Fuel machining head, Bridge & Column, Drive Mechanisms, Thimble Package, etc. A wide range of complex product portfolios meets the varied requirements of the Indian nuclear, Defense, and Space sector. ISRO, NPCIL, DRDO, Bloom Energy, Rafael, Elbit, etc. are some of the esteem clients.

Currently, the firm has 7 state-of-the-art manufacturing facilities in Hyderabad, Telangana that undertake precision machining, assembly, specialized fabrication, brazing and heat treatment, testing and quality control, and other specialized processes.

Product Portfolio:

Nuclear sector

- Fuel machining head: Used for loading and unloading of fuel bundles in nuclear reactors

- Bridge and column

- Grid plate

- Sealing plug, shielding plug, liner tubes and end fittings

- Drive Mechanisms

Customer Sector

- Ball screws and water-lubricated bearings

- Base shroud assembly and airframes

- Various missile parts

- Valves

- Cryogenic engines (turbopumps, booster pumps, gas generators and injector heads for such engines)

- Ball screws and water-lubricated bearings

Strength of the company:

- Wide range of product portfolio.

- 7 Modern technology manufacturing units.

- Diversified supplier base.

- Strong financial track record.

- Experienced and qualified management.

Risks Relating to Industry

- Company depend on a limited number of customers for a significant portion of their revenue. The loss of one or more of their significant customers or a significant reduction in demand for their products from such significant customers.

- The company depend significantly on orders from the NPCIL, ISRO and DRDO. A decline or re-prioritization of funding in the Indian budget towards the respective departments of the Government of India under which these customers operate or delays in the budget process could adversely affect their ability to grow or maintain our sales, earnings, and cash flow.

- The company primarily rely on purchase orders to govern the volume and other terms of the sales of their products. The company do not have long-term supply agreements with its customers.

- The company are subject to strict quality standards. Any failure to comply with such quality standards may lead to the cancellation of existing and future orders which may adversely affect their reputation, financial conditions, cash flows and results of operations.

- The company could make investments and acquisitions in the future that involve considerable integration costs. The company may be unable to sustain, manage or realize the expected benefits of such growth or may not be able to fund that growth.

- Company may face claims and incur additional rectification costs for delays and/or defects in respect of their precision components and equipment

IPO Details:

IPO Date Mar 3, 2021 to Mar 5, 2021Issue Type Book Built Issue IPO Issue Size Equity Shares of Rs.10 totaling up to Rs. 596.41 Crore Fresh Issue Equity Shares of Rs.10 totaling up to Rs. 123.52croreOffer for Sale Equity Shares of Rs.10 totaling up to Rs.472.89 crore Face Value Rs.10 per equity share IPO Price Per Equity Share: Rs. 574-575 Min Order Quantity 26 Listing At BSE, NSE

IPO Objective :

The company proposes to utilize the Net Proceeds from the Fresh Issue towards funding the following objects:

- Repayment/prepayment in full or in part, of borrowings availed by our Company

- Funding working capital requirements; and

- General Corporate Purposes

Financial Performance:

Particulars For the year/period ended (₹ in million)31-Dec-2031-Mar-2031-Mar-1931-Mar-18 Total Assets3,819.143,462.713,051.582,810.32Total Revenue1,779.912,181.421,859.101,605.45Profit After Tax280.69313.18391.9954.23

Tentative Time Table:

IPO Opening Date: 3rd March 2021IPO Closing Date: 5th March 2021Finalisation of Basis of Allotment: 10th March 2021Initiation of refunds: 12th March 2021Transfer of shares to Demat account: 15th March 2021Listing Date: 16th March 2021

Outlook:

Hyderabad-based MTAR Technologies is a leading player in the precision-engineering industry develops and manufactures equipment for the defense, aerospace, clean energy, and nuclear energy sectors.

The company has long-standing relationships of over three to four decades with customers such as the Indian Space Research Organization (“ISRO”) and the Defense Research and Development Organization (“DRDO”), and have been able to supply specialized products to the Indian space programmes and the Indian missile programme, respectively.

The company’s aggregate Order Book as of November 30, 2020, was Rs.356 crores, comprising Order Book in the nuclear, space and defence, and clean energy sectors of Rs.93 crores, Rs.172 crores and Rs.86 crores respectively. These numbers signify the strength of the company. When it comes to Clean energy which is a boom these days, accounts for 64.34% of its revenues in FY2020 which also depicts its strong hold in the Clean energy sector.

The company is also focusing on its expansion plans and for the same, it is establishing an additional manufacturing facility at Adibatlaand in Hyderabad which is expected to become operational in Fiscal 2022.MTAR Technologies owns a large range of equipment, resulting in increased fixed costs.

When it comes to the financial performance of MTAR Technologies over the last three years highlights significant growth. The total revenue of the company showed a 3-year CAGR growth of 16.57%. Further, between 2018 and 2020, the profit after tax grew at a staggering CAGR of 14.39%. Also, the company’s total assets grew at a CAGR of 11%. The company’s Earnings Per Share is 11.11 and the Price to Earnings ratio stands at 51.75. As a niche player, the company is expected to gain fancy after the listing as it will be the first company to list in this segment.

Effect on Stock Market After Rising COVID 19 Cases: Government Moves and Vaccine Rollout

As the COVID 19 cases had marked a considerable decline in the past few months, the active cases have been on the rise again and with Feb 21, registering new cases of 14,199. However, the cases had seen a sudden decline on Feb 16 with 9,121.

The spectacular fall in the COVID 19 cases for nearly five months, in the states that has shown a resurgence now, had led to a belief that the infection levels in the country had probably reached a new level where the effects of herd immunity had started to play out.

On Monday, the ministry reported 83 deaths with a total tally of over 1.56 lakh. This accounts for 1.42% of more than 1.1 crore coronavirus cases detected in India. Some states including Maharashtra, Kerala have been advised by the centre to increase the proportion of RT-PCR tests and regularly monitor mutant strains.