TCS Share Price Outlook: Q1FY27 Preview, AI Momentum, And Growth Signals

Key Takeaways

- Brokerages forecast 13% year-on-year revenue growth and 4% year-on-year profit growth for Q1FY27, with almost flat sequential growth.

- Margins are expected to fall 100–160 basis points sequentially due to wage revisions and macro headwinds.

- AI-led services momentum and acquisitions like Coastal Cloud and ListEngage could support mid-term growth, even as near-term margins face pressure.

- Investors should monitor US demand, BFSI growth, discretionary technology spending, pricing pressure, and AI strategy for signs of demand recovery.

tcs share price has zigzagged through a choppy year as the IT bellwether braces for Q1FY27. The consensus foresees 13% year-on-year revenue growth and 4% year-on-year profit growth, with almost flat sequential growth. In context, the stock price of tcs has corrected about 35% year-to-date, while the Sensex has fallen roughly 9% over the same period. Peer context shows Wipro and HCLTech underperforming, while Infosys stock price is viewed as less unfavorable on risk-reward. Against this backdrop, investors are parsing AI bets, deal momentum, and margin trajectories to gauge the next move for the stock.

TCS Q1FY27 Revenue Forecast And The Implications For TCS Share Price

Brokerages’ consensus, based on an average of estimates from six brokerages, points to 13% year-on-year revenue growth and 4% year-on-year profit growth for Q1FY27, with almost flat sequential growth. The QoQ picture is mixed: Nuvama expects 0.1% constant-currency revenue growth, Systematix 0.3%, and Nomura, Motilal Oswal, and Kotak Equities all forecasting revenue broadly flat. This range implies a muted near-term upgrade path for the stock price of tcs, even as the longer-term AI and outsourcing demand narrative remains intact. The narrative is also framed by macro headwinds and delayed discretionary spending, which could keep the growth trajectory modest in the near term.

Contextual price dynamics add another layer: the stock price of tcs has corrected about 35% year-to-date while the Sensex is down around 9% YTD. Management commentary will be critical in gauging how US demand, BFSI growth, and discretionary technology spending could translate into earnings in the coming quarters. Pricing pressure remains a theme, and AI strategy is now a central talking point as clients seek higher productivity and new service lines from technology providers. As investors weigh these factors, the ability of TCS to defend margins amid wage revisions and currency movements will be a key determinant of the near-term tcs share price trajectory.

Growth drivers and headwinds converge here: macro headwinds and delayed discretionary spend point to a cautious near-term environment, but productivity pass-throughs in large renewals and AI-enabled offerings could unlock upside in the medium term. The external backdrop–the Middle East conflict and softening in select verticals–adds to the uncertainty. Yet, the AI context is clear: clients are seeking productivity gains, and firms investing in AI capabilities hope to build new service lines that eventually translate into revenue and margin resilience. Investors should watch how management frames US demand recovery, BFSI growth, and the expected timeline to close the growth gap with peers.

AI Impact On TCS Margins: Near-Term Pressure And Long-Term Potential

The AI narrative has become a core driver of sector debate, and TCS is balancing new AI-enabled service lines with a cost base that faces wage revisions. Margins are expected to fall sharply on a sequential basis due to wage revisions from April. Specifically, Nuvama and Kotak Equities peg the EBIT margin decline at about 160 basis points quarter-on-quarter, while Motilal Oswal projects a 140-basis-point fall to around 23.9%. Nomura and Systematix estimate a ~100-basis-point drop. These figures reflect wage adjustments, a potentially softer rupee, and the offsetting effect of productivity gains. Investors should treat these as near-term headwinds rather than long-run outcomes, as AI-led pricing power and efficiency gains could alter the trajectory over the next several quarters.

The long-term angle remains nuanced: AI-driven productivity could lift utilization and enable new revenue streams, potentially expanding margins once the cost structure stabilizes. The pace at which AI-enabled offerings translate into actual client spend is the critical variable, and frontier AI labs’ model releases will be read as potential inflection points for AI deflation assumptions. Management commentary on AI strategy, data-center investments, and pricing discipline will be under the microscope to assess how well TCS can defend margins while pursuing growth in AI-enabled services.

Deal Wins, Acquisitions, And Growth Visibility For TCS

Deal momentum is central to growth visibility. Systematix contends that healthy deal total contract value (TCV) could be around $10 billion, while Kotak projects a more conservative $8–9 billion. The caveat on both sides is that pricing compression YoY and normal seasonality temper the upside. In terms of strategic moves, acquisitions Coastal Cloud and ListEngage are highlighted as potential levers for growth, especially in cloud and marketing-tech services. The real test will be how these acquisitions translate into revenue contribution and client cross-sell opportunities, particularly in an environment where AI-led services momentum is seen by some brokers as a mid-term growth catalyst.

Growth visibility depends on the integration of these acquisitions and their ability to unlock larger deal wins in overlapping client cohorts. Investors will be watching for concrete evidence that acquisitions are improving top-line contributions and profit margins, rather than merely broadening the portfolio. This is where AI-driven services momentum, highlighted by several brokerages, could become a meaningful signal for the medium term–provided integration milestones and client wins align with expectations.

Management Focus And Sector Context: What Investors Should Watch

Management commentary is expected to focus on several high-signal areas: US demand, BFSI growth, discretionary technology spending, pricing pressure, and the AI strategy’s execution timeline. AI-related strategy notes–particularly frontiers and data center investments–will be scrutinized for signs of margin protection amid pricing pressure. The broader sector narrative suggests stable execution but no immediate growth rebound; a sharp correction in the stock has already tempered expectations. For retail investors, the key question is whether management can deliver a credible path to closing the growth gap with peers, even as macro headwinds persist.

In this environment, investors also weigh relative performance among peers. Infosys stock price is viewed by some as relatively better on risk-reward, while stock price of wipro and hcltech stock price have faced more pronounced headwinds. The context of a 9% fall in the Sensex YTD provides a backdrop for how much macro risk the IT pack is discounting. The crucial test remains: can management translate AI investments into tangible revenue and margin improvements in a timeframe that matters to investors?

Peer Performance Context: How TCS Compares With Infosys, Wipro And HCLTech

In peer comparisons, the stock price of tcs sits against a mixed backdrop: infosys stock price tends to be viewed as less risky on a risk-reward basis, while stock price of wipro and hcltech stock price have underperformed. The broader market environment has contributed to a broader IT sector drawdown, with the Sensex down about 9% YTD and the stock price of tcs down roughly 35% YTD. While Infosys stock price has faced its own pressures, some investors consider it a relatively steadier proxy for the sector’s rebound potential. This dynamic shapes how retail investors calibrate exposure across the IT landscape, particularly when AI strategy and margin management are front and center.

From a valuation perspective, TCS’s growth trajectory remains anchored in stable execution rather than a rapid post-pandemic rebound. The information from brokerages suggests a cautious stance for the near term, with room for a more constructive view if AI-enabled service lines translate into durable top-line growth and margin resilience over the next few quarters.

Investment Takeaways For Retail Investors: What To Do Now

The core takeaways for a retail investor are to monitor whether AI investments translate into sustainable revenue and whether the company can bridge the growth gap relative to peers. The Q1FY27 forecast suggests a steady, if modest, revenue trajectory, with near-term margin headwinds. The market's focus on US demand and BFSI growth will determine whether the stock price of tcs can rally from current levels. Acquisitions, and AI-led services momentum, could provide a path to improved revenue visibility over the medium term, but immediate upside requires concrete signs of demand recovery and resilient pricing power.

As a practical next step, investors might consider using Swastika's Sarthi AI stock assistant to access deeper, institutional-grade research on TCS and other indices; it can help frame trade ideas and risk controls. The AI-powered insights can be a valuable complement to your own analysis as you navigate this evolving IT landscape.

Related Reads

- TCS share price Outlook: Brokerages Cut Targets On Tata Consultancy Services And The IT Sector

- TCS Share Price Crash Signals Deep IT Sector Repricing And Opportunities

Frequently Asked Questions

What is the Q1FY27 revenue growth forecast for TCS according to brokerages?

Brokerages estimate 13% year-on-year revenue growth for Q1FY27, with 4% year-on-year profit growth.

What do brokerages expect for Q1FY27 quarter-on-quarter revenue change?

Consensus ranges from 0.1% QoQ constant-currency growth (Nuvama) to 0.3% (Systematix), with Nomura, Motilal Oswal, and Kotak Equities forecasting broadly flat revenue QoQ.

How are margins expected to move in Q1FY27 for TCS?

EBIT margins are expected to decline by about 100–160 basis points QoQ; Motilal Oswal projects a 140-bps decline to around 23.9%, while Nomura and Systematix expect about 100 bps of decline; Nuvama and Kotak expect a 160 bps drop.

What deal-wins scenarios are discussed for TCS?

Systematix expects a healthy deal total contract value around $10 billion, while Kotak projects $8–9 billion; there is a caveat of pricing compression and normal seasonality.

Which acquisitions were mentioned and what is their potential impact?

Coastal Cloud and ListEngage were mentioned as acquisitions; investors will be watching whether these acquisitions improve growth visibility and revenue contribution, especially in AI-enabled services.

How does TCS compare with peers like Infosys, Wipro, and HCLTech in this context?

Infosys stock price is viewed as less unfavorable on risk-reward; stock price of wipro and hcltech stock price have underperformed; the stock price of tcs has declined about 35% YTD, while the Sensex is down about 9% YTD.

Conclusion

The retail investor’s take from TCS’s Q1FY27 preview is that steady execution meets near-term margin headwinds, with AI investments and deal momentum shaping the mid-term path. The tcs share price may remain sensitive to signs of demand recovery and the pace at which AI-enabled revenue contributions translate into earnings. A clear management narrative on US demand, BFSI growth, pricing discipline, and acquisition integration will be the decisive factors for re-rating in the coming quarters.

One practical mental model is to separate AI-driven margin resilience from near-term top-line growth and to wait for tangible deal wins and integration milestones before adjusting exposure. You can further calibrate your view by leveraging Swastika's Sarthi AI stock assistant for deeper, institutional-grade research on TCS and its IT peers. This approach helps a retail investor stay disciplined amid a shifting AI-led growth narrative while keeping focus on the fundamentals that really move the tcs share price over time.

Open your trading and demat account here

Reference :

1 : Economictimes

Latest Articles

Mutual Fund Rules that Come into Effect from 2021

We have noticed many regulatory changes in the mutual fund industry in the upcoming year, which is about to end soon. In an attempt to make mutual funds more transparent for traders and investors, SEBI came up with some changes which will remain applicable in the new year 2021.

Here is a list of changes that will come into effect in Jan 2021.

1. Changes in portfolio allocation rules for multi-cap funds:

SEBI announced portfolio allocation rules for multi-cap mutual fund schemes. As per the new rules made by SEBI, a mutual fund scheme will have to invest at least 75% in equities and equity-related investments. In addition to this, the schemes will have to invest in a minimum of 25% each in small-cap, mid-cap and large-cap stocks. At present, there is no such restriction allocation and therefore fund managers are allowed to invest in the mid-cap as per their own choice.

All mutual fund houses were given time till 31 January 2021, to comply with the fresh rules, within the one month from the date of publishing the next lists of stocks by AMFI. Following concern in the industry, the SEBI later introduced a new mutual fund category called flex cap fund, which is required to invest at 65% of the corpus in equity without any restrictions on investing in small-cap, mid-cap or large-cap funds. Some AMCs have already reclassified their multi-cap schemes as Flexi cap category to avoid any portfolio changes.

2. Changes in NAV Calculation

From January 1, 2021, mutual fund investors will get the purchase NAV of the day, when investors’ money reaches the AMC, irrespective of the size of investments. This NAV rule will be applicable only for those funds which are available for utilization irrespective of the name and size of the application.

Under the prevailing rules, the NAV of the date of purchase is considered for the purchase of less than Rs 2 lakh, even if the money does not reach the AMC, but the order is placed within the cut off time.

3. Inter Scheme Transfer of Securities

According to the sources, inter scheme transfer (IST) of debt papers can only be done within 3 business days of the allotment of the schemes’ units and after three business days, such transfer will not be allowed. Under prevailing rules, SEBI only requires that such IST be done at the market prices.

From January 1, 2021, inter scheme transfer in closed-ended funds can be done within 3 business days as the scheme transfers involve shifting of debt papers from one mutual fund scheme to another.

Moreover, SEBI also specified that such ISTs be done only at the market places and no ISTs shall be allowed if there is any negative market news or rumours in the mainstream media.

4. Renaming the dividend option

From April 1, 2021, mutual fund schemes comprising all the dividend schemes will be renamed as income distribution cum capital withdrawal options.

5.New Riskometer Tool

SEBI introduces a new category of mutual fund schemes on its riskometer tool for investors to make better decisions with high-risk mutual funds. Earlier, the model was simply based on the risk of the category without considering its actual portfolio. The new riskometer shall be evaluated every month and all schemes will be labelled for risks and funds.

Additional Measures Under Consideration

SEBI is considering additional measures which are expected to be implemented with the mutual fund industry. Here are some of them:

- It is mandatory to maintain a minimum 10% exposure in liquid assets such as government securities, treasury bills, and cash in hand.

- Gating of redemption during extreme events to prevent any pressure on the fund.

- Do assessment whether the side pocket creation norms need to be revised.

- Stress testing for all open-ended debt oriented mutual fund schemes will raise early warning signs and enable AMCs to take necessary actions.

- Encourage repo in corporate bonds to raise liquidity in the secondary market and to enable greater issuance of paper rated below AAA.

Intraday Trading Strategies - Golden Rules For Picking Stocks When Intraday Trading

Intraday trading is considered as quite riskier than other trading strategies as it involves buying and selling of stocks on the very same day. This is because, in intraday trading, a large number of stocks are bought and sold with the intention of booking profit. Here, the objective is plain and simple: to buy and sell shares within the same day. Before we begin, let's understand what exactly is Intraday trading and what are the strategies investors need to apply while intraday trading.

Strategies for Intraday Trading

Needless to say, intraday trading means purchasing and selling of stocks on the very same day. However, with intraday trading, traders can short sell their shares and then buy back during the rolling settlement period. Experienced traders always recommend selecting the shares which are highly liquid.

Find Entry and Target Price

It is important to determine the entry-level and target price before placing the buy order. It’s quite understandable for a person’s psychology to change post buying of shares. Hence, many traders may sell shares even if the price experiences high growth. As a result, they may lose the best chance of achieving gains because the price goes upward.

Utilizing Stop Loss for Lower Impact

Stop loss is defined as an advanced order placed with the assistance of a broker to buy or sell a specific stock once it reaches a price point. It is generally used to restrict the loss or gain in a trade. This is beneficial in limiting the potential loss for investors due to downfall in a stock.

Stop-loss also works great in short selling. Investors who short sell their shares, stop loss acts a boon by minimizing the losses if the price goes up beyond their expectations.

Book Your Profits Once You Achieve Your Target

There is a famous quote saying “ As long as greed is stronger than compassion, there will always be suffering”. Many investors suffer from greed or fear in terms of high earning. With the help of stop-loss, investors not only minimize their losses but also book their profits once the target is achieved.

Research Your Wish List Frequently

Successful traders advised to include 10-12 shares in their wish-list and research all the stocks in depth. For instance, do fundamental analysis and technical analysis of stock and try to understand the trend such as the history of a stock, merger, present return and more.

Don't Move Against the Market

Experienced professionals fail to predict the exact market movement. There are many times when all the technical indicators depict a bull market; there is still a decline. However, these factors do not provide any guarantee. If the market does not move according to your expectation, then it is important to exit your position to avoid huge losses.

.avif)

SOYBEAN ONE OF THE MOST TRADEABLE AGRI-COMMODITY

Soybean (Glycine max) is termed Golden Bean. The plant is classed as associate seed and is a vital international crop. The processed soybean is the largest supply of supermolecule feed and second-largest supply of edible fat within the world. The foremost portion of the worldwide and domestic crop is solvent-extracted with alkane to yield soy oil and procure Soymeal, which is widely employed in the animal feed trade.

Soybean has a very important place in the world's seed cultivation state of affairs, because of its high productivity, profitability and important contribution towards maintaining soil fertility. The crop additionally features an outstanding place as the world's most vital seed legume, that contributes 25% to the worldwide edible fat production, about 2/3rd of the world's protein concentrate for livestock feeding, and is a valuable ingredient in formulated feeds for poultry and fish.

About 85% of the world's soybeans are processed annually into soybean meal and oil. Of the oil fraction, 95% is consumed as edible oil; the rest is used for industrial products such as fatty acids, soaps and biodiesel.

Soybean seed is processed for Soymeal and Soy oil, both of these products are consumed throughout the country. A previously substantial part of Soymeal production gets exported but in the last two years exports reduced and domestic consumption increased.

India produces around 10 Mn tones of Soybean, while global production is around 340Mn tones. Among which the major producing countries are the USA, Brazil and Argentina whereas the major producing states are MP, Maharashtra and Rajasthan.

USES OF SOYBEAN:

- Processed Soybean is the largest source of protein feed and second-largest source of vegetable oil in the world. Soybean seed is processed for Soymeal and Soy oil, both of this product are consumed throughout the country.

- Soybean seed is processed for Soymeal and Soy oil, both of these products are consumed throughout the country.

- There are many other products which are manufactured from Soybean like Soy nutrila, Soy flour, Soy yogurt, Soy sauce, Soy milk, tofu etc

- Soybean oil is also used for industrial purposes in products like paints, plastics and cleaners and also used as biodiesel fuel for diesel engines that are being produced from the soybean oil by a simple process called transesterification.

FACTORS AFFECTING THE PRICE OF SOYBEAN:

- Weather condition especially during sowing and pod bearing condition.

- Demand for Soybean from Soybean processing industry.

- The demand of Soymeal from the poultry feed industry.

- Government policies: MSP, Import duty, stock limit, import and export duty on its derivatives.

- Demand-Supply and price scenario of other competitive oils i.e. palm oil.

- Price movement of Soybean in international exchange CBOT.

- International production of Soybean and also International prices of Soymeal and Soy oil.

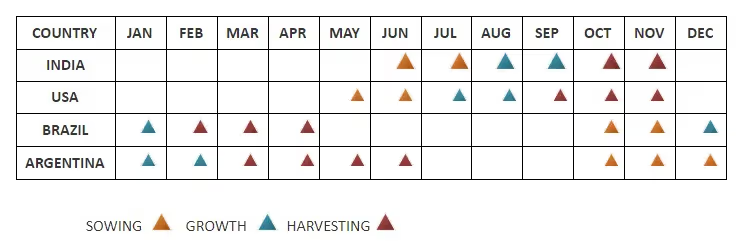

SEASONALITY:

BENEFITS OF NCDEX SOYBEAN FUTURES:

- It acts as a benchmark for the futures contract of soybean.

- It helps in a robust delivery mechanism.

- It connects the entire value chain.

- Hedging and price risk management tool for the value chain.

- Efficient and transparent price discovery.

CONTRACT SPECIFICATIONS:

- Ticker symbol - SYBEANIDR

- Trading Unit - 5 MT

- Delivery Unit - 5 MT

- Maximum Order Size - 500 MT

- Tick Size - Re.2 (per QUINTAL)

- Hours of Trading- Mondays through Fridays: 9:00 A.M. to 5:00 P.M.

- Quantity Variation - +/- 2%

- Delivery Center - Indore, Akola, Latur (Maharashtra), Mandsaur (MP), Kota (Rajasthan)

- Delivery Logic - Compulsory Delivery

- Delivery Specification - Upon expiry of the contracts all the outstanding open positions shall result in compulsory delivery.

- Due date/ Expiry Date 20th day of the delivery month - If 20th happens to be a holiday, a Saturday, or a Sunday, then the expiry date (or due date) shall be the immediately preceding trading day of the Exchange, which is other than a Saturday.

उत्पादन कटौती को कम करने से दबाव मे कच्चे तेल के भाव।

रॉयटर्स सर्वे के मुताबिक, ओपेक के कच्चे तेल के उत्पादन में जनवरी महीने में प्रति दिन 160,000 बैरल प्रति दिन की वृद्धि हुई है क्योंकि ओपेक और गठबंधन 2021 के पहले महीने में उत्पादन में कटौती को कम कर रहा है। ओपेक के स्रोतों के अनुसार ओपेक का उत्पादन जनवरी में औसत 25.75 मिलियन बैरल प्रति दिन रहा, दिसंबर से 160,000 बैरल प्रति दिन और लगातार सातवें महीने में कार्टेल ने अपना उत्पादन बढ़ाया है।

जबकि उत्पादन में बढ़त पिछले महीने में अधिकांश लीबिया से है, जिसे ओपेक गठबंधन मे कटौती से छूट दी गई है। जनवरी में उत्पादन में वृद्धि आश्चर्यजनक नहीं है क्योकि ओपेक गठबंधन ने जनवरी में उत्पादन में 500,000 बैरल प्रति दिन जोड़ने का फैसला किया था।

पूरे समूह के लिए 500,000 बैरल प्रति दिन के कोटे में से, ओपेक की बढ़ी हुई उत्पादन की हिस्सेदारी लगभग 300,000 बैरल प्रति दिन है। इसलिए, जनवरी में उत्पादन की सबसे बड़ी वृद्धि क्रमशः ओपेक के नंबर एक और नंबर दो उत्पादकों, सऊदी अरब और इराक से हुई है, क्योंकि उनका उत्पादन मे हिस्सा अधिक है।

जनवरी में ओपेक के उत्पादन में तीसरा सबसे बड़ा इज़ाफा ईरान से आया है, जो लीबिया की तरह ओपेक गठबंधन की कटौती से मुक्त है। कच्चे तेल की कीमतों मे मांग कम होने की सम्भावना और उत्पादन अधिक होने से ऊपरी स्तरों पर दबाव है और नए कोवीड-19 वायरस महामारी को लंबे समय तक जारी रख सकता है, जिससे मांग घट सकती है।

तकनीकी विश्लेषण:

इस सप्ताह फ़रवरी वायदा कच्चे तेल की कीमतों मे ऊपरी स्तरों पर दबाव रहने की सम्भावना है। इसमें 4025 रुपय के ऊपरी स्तरों पर प्रतिरोध एवं 3650 रुपय के निचले स्तरों पर सपोर्ट है।

Understanding the Types and Features of Bonds

Introduction:

Bonds are one of the most essential financial instruments available to investors. They are popular for their stability and predictable returns, making them a key component in a balanced investment portfolio..

1. What Are Bonds?

Bonds are debt securities issued by various entities such as governments, municipalities, and corporations to raise capital. When you purchase a bond, you're essentially lending money to the issuer. In return, the issuer promises to pay you periodic interest (known as the coupon) and return the bond’s face value (or principal) when it matures.

Did you know The concept of bonds dates back to ancient Mesopotamia, where they were used to record debts and obligations. Fast forward to today, and bonds remain a cornerstone of modern finance!

2. Types of Bonds

Let's dive into the various types of bonds available in the market, with examples relevant to Indian investors:

a. Government Bonds

Government bonds are issued by national governments and are considered one of the safest investments. In India, these are known as Government Securities (G-Secs). They are backed by the government’s ability to tax its citizens, which minimizes the risk of default.

Example: The 10-year Government of India Bond is a common benchmark bond that many investors in India consider for long-term stability.

Did you know Did you know that India’s first-ever bond issue dates back to 1811? It was issued by the East India Company to fund its operations in the country.

b. Corporate Bonds

Corporate bonds are issued by companies to fund their operations or expansion. These bonds typically offer higher interest rates than government bonds due to the increased risk associated with the issuer's financial health.

Example: HDFC, a leading financial services company in India, frequently issues corporate bonds that offer attractive returns compared to government bonds.

c. Municipal Bonds

Municipal bonds are issued by state governments, cities, or other local government entities. In India, these bonds are not as prevalent as in some other countries, but they do exist. The interest from these bonds is often exempt from certain taxes, making them appealing to investors in higher tax brackets.

Example: Some Indian states have issued municipal bonds to fund infrastructure projects like the development of smart cities.

d. Zero-Coupon Bonds

Zero-coupon bonds do not pay periodic interest. Instead, they are issued at a discount to their face value, and the investor receives the full face value at maturity. This type of bond can be useful for long-term financial goals.

Example: The Reserve Bank of India has issued zero-coupon bonds in the past, which are sold at a deep discount and redeemed at face value upon maturity.

e. Convertible Bonds

Convertible bonds are hybrid securities that can be converted into a predetermined number of the issuing company’s shares. These bonds offer the potential for equity-like returns while providing the safety of a bond.

Example: Tata Motors has issued convertible bonds that can be converted into equity shares, offering investors both stability and potential for growth.

f. High-Yield Bonds (Junk Bonds)

High-yield bonds, also known as junk bonds, are bonds with a lower credit rating, which means they carry a higher risk of default. To compensate for this risk, they offer higher interest rates.

Example: Some smaller Indian companies, particularly in the infrastructure and real estate sectors, may issue high-yield bonds to attract investors willing to take on more risk for higher returns.

3. Key Features of Bonds

Understanding the key features of bonds is crucial for making informed investment decisions. Here are some important aspects to consider:

a. Face Value (Par Value)

The face value, or par value, is the amount the bondholder receives when the bond matures. In India, corporate bonds typically have a face value of ₹1,000.

b. Coupon Rate

The coupon rate is the interest rate the bond pays, usually expressed as an annual percentage of the face value. In India, interest payments on bonds are often made semi-annually.

Example: A corporate bond from Infosys might offer a coupon rate of 8%, meaning the investor would receive ₹80 per ₹1,000 bond each year.

c. Maturity Date

The maturity date is when the bond’s principal amount is repaid to the bondholder. Bonds can have short-term, medium-term, or long-term maturities, depending on the issuer's needs and the investor's preferences.

Example: A 5-year bond issued by Reliance Industries would return the principal amount after five years, along with the final interest payment.

Did you know The longest-maturity bond ever issued was a 100-year bond, sometimes referred to as a "century bond." In 2020, India’s largest steelmaker, Tata Steel, issued such a bond!

d. Yield

Yield represents the bond’s return on investment. It can vary based on factors like the bond’s price, coupon rate, and remaining time to maturity. Yield is an important measure for comparing the potential returns of different bonds.

e. Credit Rating

Bonds are rated by agencies like CRISIL, ICRA, and CARE in India, which assess the issuer’s creditworthiness. Higher ratings (like AAA) indicate lower risk, while lower ratings (like BB or lower) suggest higher risk.

Example: A bond issued by the State Bank of India (SBI) might have a AAA rating, indicating a very low risk of default.

Did you know India’s bond market was largely developed after the 1991 economic reforms, and today it’s one of the fastest-growing bond markets in Asia!

f. Callable Bonds

Callable bonds can be redeemed by the issuer before the maturity date, usually at a premium. This feature benefits the issuer if interest rates drop, allowing them to refinance at a lower cost.

Example: Some bonds issued by Indian corporations like ICICI Bank are callable, giving the issuer flexibility to manage their debt efficiently.

Conclusion

Bonds are a versatile investment option that can offer varying degrees of risk and return. By understanding the different types and features of bonds, Indian investors can make informed decisions that align with their financial goals, whether they're seeking safety, income, or growth potential.

Stove Kraft IPO

Stove Kraft was originally incorporated in 1999. They are primarily involved in the manufacture of kitchen appliances, equipment and utensils. Stove Kraft is a kitchen solution and an emerging home solutions brand. Further, it is one of the leading brands for kitchen appliances in India and is one of the dominant players for pressure cookers and a market leader in the sale of free-standing hobs and cooktops.

Stove Kraft is engaged in the manufacture and retail of a wide and diverse suite of kitchen solutions under its Pigeon and Gilma brands and proposes to commence manufacturing of kitchen solutions under the BLACK + DECKER brand, covering the entire range of value, semi-premium and premium kitchen solutions, respectively.

Its kitchen solutions comprise of cookware and cooking appliances across its brands, and its home solutions comprise various household utilities, including consumer lighting, which not only enables it to be a one-stop-shop for kitchen and home solutions but also offer products at different pricing points to meet diverse customer requirements and aspirations.

The company has a strong distribution network as under the "Pigeon" brand, it has 651 distributors in 27 states and 5 union territories and 12 distributors for exports and under the "Gilima" brand, it has 65 stores across 4 states and 28 cities.

It not just distribute its products in the Indian market but also exports them to countries like the USA, Mexico, Kenya, Qatar, Sri Lanka, Fiji, Bahrain, Kuwait, etc. Stove Kraft has manufacturing facilities at Bengaluru (Karnataka) and Baddi (Himachal Pradesh).

All Pigeon and Gilima branded appliances are manufactured at its Bengaluru unit and the Baddi facility focuses on the Oil Company Business (OCB) to manufacture products like LPG stoves, inner lid cookers, etc.

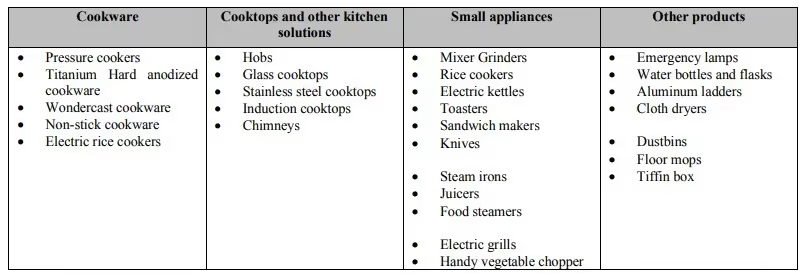

Products and Brands:

Stove Krafts products are sold under three brands, viz. Pigeon, Gilma and BLACK + DECKER to cater to the value, semi-premium and premium customer segments, respectively. Set out below is a brief overview of the class of products retailed under each of the brands:

Pigeon:

Pigeon, which is value for money brand, offers a wide array of products under various sub-categories. Set out below is an overview of the products currently offered by us under the Pigeon brand:

Some of the marquee innovative products, such as the Super Cooker, Infinity glass cooktops and Super Storm Advanced mixer grinder, are sold under the Pigeon brand. The Pigeon ‘super cooker’ is an innovative offering which provides the functionalities of straining, serving, induction cooking compatibility and non-stick, energy-efficient cooking in a single product.

Gilma:

Gilma brand, which focuses on the semi-premium customer segment, is sold exclusively through Gilma branded stores which are designed to offer the customer a modular kitchen experience. Currently, the Gilma portfolio comprises of chimneys, hobs and cooktops across price ranges and design offerings. We believe that our Gilma products combine premium design with effective performance, offered at a competitive price. While Gilma chimneys come built with higher suction power and a lifetime warranty, the hobs offer features such as anti-rust stainless steel body, energy efficiency and one-touch auto-ignition. Similarly, Gilma LPG stoves are designed keeping in mind thermal efficiency, durability and portability. Gilma LPG stoves use toughened glass and brass burners and come with a two-year warranty.

BLACK + DECKER

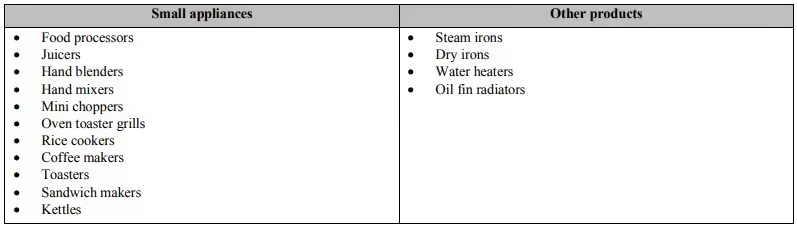

BLACK + DECKER is a renowned name internationally in the field of, inter alia, kitchen appliances. Presently, we offer the following products under the BLACK + DECKER brand, aimed at the premium segment of customers:

IPO Details:

Subscription Dates25 – 28 January 2021Price BandINR 384 – INR 385Fresh issueINR 95 croresOffer For SaleINR 317.63 croresTotal IPO sizeINR 412.63Minimum bid (lot size)38 SharesFace Value INR 10 per shareRetail Allocation10%Listing OnNSE, BSE

Strengths of the Company:

- A one-stop-shop for a well-recognized, award-winning portfolio of kitchen solutions brands with a diverse range of products across consumer preference

- Widespread, well-connected distribution network with a presence across multiple retail channels and a dedicated after-sales network

- Strong manufacturing capability with efficient backward integration;

- Consistent focus on quality and innovation

- Professional management with a successful track record and extensive experience in the kitchen solutions industry, and a young and dynamic workforce

- Strong track record and financial stability

IPO Objective:

- To make the repayment or prepayment payment of the company's borrowings fully or partially

- To meet general corporate purposes.

Financial Performance:

Financial performance (in INR crore)FY2018FY2019FY2020H1 FY2021Revenue534.6642.6672.9329.5Expenses547.1641.4669.4300.7Net income-11.70.92.930.1Margin (%)-2.20.10.49.1

IPO Tentative Time Table

21 Jan 2020: Price Band announced

22 Jan 2020: Anchor List

25 Jan 2021: Offer Opens

28 Jan 2021: Offer Closes

3 Feb 2021: Finalization of Basis of Allotment

3 Feb 2021: Unblocking of ASBA“

4 Dec 2020: Credit to Demat Accounts

5 Feb 2021: Listing on NSE & BSE

Risks:

- Expenses on raw materials increase or the cost of production rises for any other reason, the company will not be able to break even.

- There are unresolved legal issues with regard to certain land parcels which fall inside the factory space.

- There are several outstanding cases — both criminal and civil — against the company and the Stove Kraft Limited owner, Rajendra Gandhi.

Outlook:

Eyeing the brand reorganization and their focus on the innovation of products to meet the needs of the customer we expect that the fundamental of the company will boost up. The company's revenue from operations stood at Rs 328.8 crore in the April-September 2020 period, up from 4.2 percent from the year earlier. Its net profit jumped to Rs 28.8 crore in the same period, against Rs 4.4 crore a year ago. Stove Kraft IPO is priced at 34.5x PE on a trailing basis while the PE of the industry is 46x. We assign a "Subscribe" rating only for listing gain.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App