Record Foreign Flows Into Indian Sovereign Bonds Push RBI 10 Year Bond Yield Outlook Higher After Tax Relief

Key Takeaways

- Foreign funds bought ₹41,800 crore of Indian sovereign debt under FAR last month, a new record.

- This inflow nearly doubles the prior August 2024 record of ₹23,900 crore.

- June 5 tax relief on capital gains and bond interest lifted appetite for rbi government bonds among global funds.

- The rbi 10 year bond yield fell 25 basis points in June, and the rupee rose over 2% from May lows.

Record foreign buying of Indian sovereign bonds surged last month, driven by a government decision on June 5 to cut taxes on capital gains and interest income on bonds. This policy shift, paired with the addition of more securities to the fully accessible route (FAR) category, sent Indian debt attractively higher on the radar of global buyers. In June, foreign funds bought ₹41,800 crore of debt under FAR, a mark that not only set a new monthly record but also underscored a dramatic re-pricing of risk in India’s sovereign market. This inflow level is almost double the previous monthly record of ₹23,900 crore set in August 2024 and signals a broader pivot toward Indian assets. The surge came as part of a broader trend of rising overseas participation in India’s bond market, with the rupee gaining ground in parallel to equity results that were among the best in the region.

Tax relief on capital gains and bond interest income on debt instruments removes one of the final barriers for global funds to allocate to India’s sovereign debt. The addition of new securities to the FAR category further boosted the debt’s attractiveness, creating a more liquid and diverse lineup for foreign buyers. As flows accumulate, the government could see easing financing costs, while a stronger external bid supports the rupee even as external dollar strength poses ongoing considerations for exporters and importers alike.

The breadth of the move is clear from commentary by market economists. Dhiraj Nim, economist at Australia & New Zealand Banking Group, notes that a confluence of steps – including tax cuts, currency stability, delayed hike expectations, and receding fiscal risks – may have given foreign investors good reason to purchase Indian bonds. “The number of steps – tax cuts, currency stability, delayed hike expectations and receding fiscal risks – may have all given a good reason for foreign investors to purchase Indian bonds.”

For the bond market, a sustained inflow would help cushion equity pullbacks and support a more stable financing environment for the government, which in turn can influence the broader macro trajectory. As inflows continue to aggregate, many observers are watching the rbi 10 year bond yield and the currency’s trajectory closely. The rupee has already risen more than 2% since its May low, a sign of improving sentiment around India’s macro fundamentals. The June data were further supported by the reclassification of existing holdings into the FAR eligible category, a technical shift that inflated the reported monthly inflows. Analysts caution that inflows may moderate in the coming months if global financial conditions tighten or US rates rise again, but the direction remains supportive for India’s debt markets in the near term.

As investors recalibrate their exposure in a post-relief backdrop, the bond market’s sensitivity to policy shifts remains pronounced. The rbi 10 year bond yield functionally acts as a barometer for the external financing cost curve, the path of monetary policy expectations, and the currency’s relative strength. The broader narrative of rising overseas participation is visible in inflation and growth backdrop improvements, currency stabilisation, and receding fiscal risks that together help explain why more global funds are considering India’s debt as a core allocation. The inflows could also have implications for index inclusion discussions, which some analysts cite as a natural outcome of sustained cross-border demand for Indian debt. In the meantime, the market will continue to weigh the pace of global rate normalization against India’s domestic policy trajectory and fiscal trajectory, a balance that will shape the near-term resonance of the rbi 10 year bond yield and the rupee.

For retail investors, navigating this evolving landscape requires a clear framework. The Sarthi AI stock assistant can help tailor fixed income exposures and identify bond funds or laddered strategies aligned with risk tolerance and time horizon. Swastika's Sarthi AI stock assistant can be a useful companion to sift through fund options and validate assumptions in a fast-moving market.

Why Foreign Buying Of Indian Sovereign Bonds Reached A Record After Tax Relief

The June 5 policy move to cut taxes on capital gains and interest income on bonds removed a traditional hurdle for foreign funds that seek predictable, tax-efficient returns from sovereign debt. The policy, combined with the ongoing expansion of FAR eligibility, expanded the universe of eligible securities and liquidity for global investors, making Indian debt more attractive relative to other emerging markets. In short, tax relief plus more bonds eligible under FAR created a dual tailwind: higher potential returns after tax and greater ease of entry for foreign buyers. The result is a historically elevated level of foreign participation in rbi government bonds, which helps anchor the debt market and improve overall liquidity for all market participants.

How The June 5 Tax Relief For Bond Income Attracted Global Flows

The June tax relief on capital gains and interest income was designed to reduce the after-tax cost of holding Indian sovereign debt for foreign funds. In practical terms, the relief translates into stronger after-tax yields for offshore buyers and more predictable cash flows, enhancing the relative attractiveness of rbi government bonds for global portfolios. The tax relief, paired with the addition of new bonds to the FAR category, increased instrument diversification and improved the overall risk-adjusted return proposition of India’s sovereign debt in the eyes of global asset managers. In a climate of global rate adjustments and currency volatility, these structural steps are particularly meaningful for long-horizon allocations and for passive inflows that may be driven by index and tracker funds seeking eligible Indian debt exposure.

Impact On The Rbi 10 Year Bond Yield And The Rupee From Record Inflows

The influx of foreign capital has implications for the rbi 10 year bond yield and the rupee. In June, the 10-year yield fell by 25 basis points–the largest drop in six years–signalling a decisive reaction to the stronger external demand for Indian debt and the improved financing environment. The rupee appreciated more than 2% from its May lows, reflecting the supportive spillovers of higher foreign participation into India’s bond market. The path of the yield and currency will continue to be influenced by how sustainably inflows are maintained and how global rate expectations evolve in the coming months.

According to Danny Suwanapruti of Goldman Sachs, "a question of timing rather than direction" applies to India’s eventual inclusion in the Bloomberg Global Aggregate Index.

Goldman analysts suggest that the trajectory toward inclusion is a matter of timing rather than momentum, with potential passive inflows of around $15 billion over the phase-in period if conditions align. This framing underscores the broader test facing India’s debt market: sustained inflows versus episodic bursts tied to policy shifts and reclassifications. The near-term market dynamics must be read in the context of both policy-driven demand and the evolving global rate environment, which can be a source of both resilience and volatility for rbi government bonds.

What The FAR Category Changes Mean For Foreign Investors

The June data were boosted by the addition of more securities to the FAR category, and by the reclassification of existing foreign holdings in those bonds into the eligible bucket. This technical adjustment inflated the reported inflows for the month, creating a potentially modest headline if the effect fades in the coming months. Still, the structural upgrade–the expansion of bond eligibility under FAR–improves the market’s depth and liquidity, inviting a longer horizon of foreign participation. For investors, this means more robust price discovery and potentially tighter spreads across the debt curve, all else equal. However, analysts caution that inflows can moderate if global financial conditions tighten or if US rates rise, which would place added emphasis on the RBI’s policy stance and the currency’s stability.

Analysts Forecast And The Prospects For Bloomberg Global Aggregate Index Inclusion

Analysts see potential for significant passive inflows should India secure continued eligibility in major global indices. A note from Goldman analysts led by Danny Suwanapruti highlights the likelihood that inclusion is a matter of timing rather than direction. They estimate around $15 billion of passive inflows over the phase-in period, assuming conditions remain supportive. Such flows would further amplify the demand for Indian debt and could reinforce the benefits of tax relief and expanded FAR eligibility. This perspective aligns with a broader trend of rising overseas participation and suggests that India’s debt market could experience incremental upgrades in index status in the medium term, further anchoring foreign demand for rbi government bonds.

Risks To The Rally If Global Conditions Tighten

Despite the upbeat tone, there are meaningful risks to the sustained rally in Indian debt. If global financial conditions tighten and US rates rise, flows could moderate. The inflows observed in June may reflect a confluence of policy relief, additional eligible securities, and currency stabilisation; a reversal in any of these factors could temper investor appetite. The market will be watching for shifts in the US rate trajectory, as higher global rates can reprice EM debt and alter relative yields. In such an environment, the risk-reward for holding long-duration rbi government bonds may shift, underscoring the importance of diversification and risk management in any fixed-income strategy.

What This Means For Retail Investors And Bond Portfolios

For retail investors, the immediate takeaway is to recalibrate expectations for fixed-income performance in light of rising foreign participation and policy-driven supply dynamics. The record inflows can improve liquidity and offer potential price stability in the near term, but the risk of volatility remains, especially if global rates move higher or if the policy path changes. A practical approach is to build a bond ladder across maturities, balancing duration risk with credit risk and currency considerations. Retail investors might also consider bond funds or ETFs that track Indian debt indices with transparent fee structures, or direct investment in rbi government bonds where suitable in a well-structured portfolio. For deeper, more tailored insights, consider leveraging Swastika's Sarthi AI stock assistant to explore bond exposure options and related research reports. Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What Triggered The Record Foreign Buying Of Indian Sovereign Bonds?

The June 5 tax relief on capital gains and interest income on bonds, plus the addition of more securities to the FAR category, boosted the attractiveness of rbi government bonds for global funds.

How Much Inflows Were Recorded Under FAR Last Month?

Foreign funds bought ₹41,800 crore ($4.4 billion) of debt under FAR last month, according to data from Clearing Corp. of India Ltd.

What Was The Previous Monthly FAR Inflow Record?

The previous monthly record was ₹23,900 crore, set in August 2024.

How Did The rbi 10 Year Bond Yield Respond In June?

The 10-year yield fell by 25 basis points in June, the largest drop in six years.

Will The Inflows Sustain As Global Conditions Evolve?

Analysts say inflows could be sustained if global financial conditions stay supportive and US rates stay favorable, but they may moderate if global conditions tighten.

Conclusion

The record foreign flows into Indian sovereign debt after the June tax relief signify a meaningful shift in international appetite for rbi government bonds and highlight the important link between policy, liquidity, and macro stability. For retail investors, this environment offers a clearer picture of how policy incentives can alter yield dynamics and currency moves in the short term, while underscoring the need for a disciplined, risk-managed approach to fixed income. The evolution of the rbi 10 year bond yield will continue to reflect not only domestic policy but also global rate expectations, and today’s flows could translate into tomorrow’s yield curve adjustments as investors reassess risk and return in India’s debt markets.

The next step is to adopt a mental model that blends policy impact with market structure. A practical approach is to treat tax relief as a catalyst for a multi-quarter re-pricing rather than a one-off event, and to evaluate exposure in fixed income through a laddered, duration-aware strategy. Keep monitoring the RBI’s policy stance and US rate trajectories to gauge the durability of inflows, and consider using Swastika's Sarthi AI stock assistant to navigate fixed-income ideas and research that align with your risk tolerance and time horizon. The evolving debt landscape offers opportunities, but success will hinge on disciplined position sizing, ongoing risk assessment, and timely reassessment as global conditions shift.

Latest Articles

How Do Election Results Impact the Indian Stock Market?

Elections are crucial events in any democracy, and India is no exception. The outcomes of elections can have significant impacts on the stock market. This blog explores how election results influence the Indian stock market and what the potential impacts of Prime Minister Narendra Modi’s third term could be.

Political Factors Affecting the Stock Market

Market Sentiment and Stability:

- Market Sentiment: Elections often bring a sense of uncertainty. Investors generally prefer stability, and election outcomes can either boost or reduce their confidence. If the results are in favor of a party or leader perceived to be business-friendly and stable, the market reacts positively.

- Policy Predictability: Stable governments are often able to implement policies more predictably. Investors like predictability as it reduces the risks associated with sudden policy changes.

Economic Policies:

- Pro-Growth Policies: If the elected government has a track record or a plan focusing on economic growth, infrastructure development, and business-friendly regulations, the stock market usually reacts positively.

- Reform Initiatives: Governments promising and delivering structural reforms (like tax reforms, deregulation, and infrastructure spending) can boost investor confidence and drive market rallies.

Fiscal Management:

- Budget and Spending: Election outcomes can impact fiscal policies. Governments that promise sensible fiscal management and reduced deficits tend to be favored by the markets.

- Spending Programs: Conversely, if a new government is expected to increase public spending significantly without a clear plan for managing the budget, it may cause concern among investors about inflation and fiscal health, potentially leading to market volatility.

Global Perception:

- Foreign Investments: Global investors closely watch Indian elections. A government perceived as stable and reform-oriented can attract more Foreign Direct Investment (FDI) and Foreign Institutional Investment (FII), positively influencing the stock market.

- Geopolitical Stability: Election results that contribute to regional stability or enhance diplomatic relations can positively impact the stock market.

Narendra Modi’s Potential Third Term and Its Impact

Prime Minister Narendra Modi, known for his strong leadership and decisive economic policies, could significantly impact the stock market if he secures a third term. Here’s how:

Continuation of Economic Reforms:

Modi’s government has been known for several landmark economic reforms such as the Goods and Services Tax (GST), Insolvency and Bankruptcy Code (IBC), and digitalization initiatives. A third term could mean the continuation and deepening of these reforms, providing a stable and predictable policy environment that is likely to be welcomed by investors.

Infrastructure and Development Projects:

Modi’s focus on infrastructure development, including projects like smart cities, improved transportation networks, and digital infrastructure, could continue. These initiatives can stimulate economic growth, create jobs, and increase demand in various sectors, positively influencing the stock market.

Foreign Investment and Economic Relations:

Under Modi’s leadership, India has improved its ease of doing business rankings and attracted significant foreign investments. A third term could further strengthen India’s global economic relations, encouraging more foreign investments and boosting market confidence.

Political Stability:

A third term for Modi could imply political stability, which is generally favorable for the stock market. Stability reduces uncertainty and helps in long-term planning for both domestic and foreign investors.

Focus on Technology and Innovation:

Modi’s government has also emphasized technology and innovation through initiatives like Digital India and Make in India. Continued focus in these areas could foster a more robust tech ecosystem, providing growth opportunities for tech stocks and start-ups.

Potential Risks:

Implementation Risks: While Modi’s policies are generally market-friendly, the actual implementation of large-scale reforms can sometimes face hurdles, leading to temporary market fluctuations.

Global Economic Conditions: The global economic environment can also impact the effectiveness of Modi’s policies. Trade wars, global slowdowns, or geopolitical tensions can affect market performance regardless of domestic policies.

Conclusion

Election results have a deep impact on the Indian stock market, primarily due to changes in market sentiment, policy direction, and fiscal management. A potential third term for Prime Minister Narendra Modi is expected to bring continued economic reforms, infrastructure development, and political stability, all of which are likely to positively influence the stock market. However, investors should remain mindful of implementation challenges and global economic conditions that can also affect market dynamics. As always, a balanced and insightful approach to investing is crucial in navigating the impacts of election results on the stock market.

Learn more about stock market with Swastika!

What is Prospectus?

A prospectus is a formal document that gives information about an investment offering to the public and is required by the Securities and Exchange Commission (SEC) to be filed. Bonds, mutual funds, and stock offers need the filing of a prospectus. Because it includes a wealth of pertinent information about the investment or security, the prospectus can assist investors in making better-informed investing decisions.

- Preliminary Prospectus

This is the initial offering document provided by the company. It contains most details about the business and the transaction. However, it doesn't include the number of shares or the price.

- Final Prospectus

This document provides all the details of the investment offering to the public. It includes background information, the number of shares or certificates to be issued, and the offering price.

Prospectus Example

In mutual funds, the prospectus covers objectives, investment strategies, risks, and performance, fees, and fund management details.

Requirements for Issuing a Prospectus

To issue a prospectus, a company must:

- File it with local regulatory bodies like SEBI and stock exchanges.

- It must be dated and signed.

- Include all necessary information outlined in the Companies Act 2013.

- Avoid providing misleading information.

Why Read a Prospectus? Here's Why It Matters:

An SEC-mandated prospectus gives investors crucial information regarding an offering of securities.

It disseminates risk information to the public and compiles important details about the investment and the business being invested in.

Investors should take into account the type and degree of risk involved, which is why those facts are usually included early in the prospectus and in more depth later on.

Investors want to know that the firm they are investing in is financially stable enough to fulfill its obligations, therefore the financial standing of the business is also crucial.

Types of Prospectuses

- Red Herring Prospectus: Filed with the registrar before offering shares. Usually lacks details like quantity or price.

- Abridged Prospectus: A brief summary with essential offer details. Must include all documents needed for purchasing the security.

- Deemed Prospectus: Considered deemed if it details the company’s investment offer to the public.

- Shelf Prospectus: Distributed by banks or financial institutions, containing details of multiple investment types.

Details Included in a Prospectus

A prospectus contains the following details:

- Company Information: Name, registered office address, objectives, and background.

- Offer Details: Number of shares or certificates to be issued, offering price, and any minimum subscription amount.

- Financial Information: Audited financial reports, including profit and loss statements, balance sheets, and cash flow statements.

- Management Details: Information about the company's directors, management team, and key personnel.

- Risk Factors: An overview of the risks associated with the investment, including market risks, regulatory risks, and operational risks.

- Legal and Regulatory Information: Details of any legal proceedings, regulatory compliance, and agreements relevant to the offering.

- Use of Proceeds: How the funds raised from the offering will be used by the company.

- Fees and Expenses: Details of any fees, expenses, or charges associated with the investment, including management fees and transaction costs.

- Offering Structure: Any special terms or conditions of the offering, such as underwriting arrangements or distribution channels.

- Other Relevant Information: Any additional information deemed relevant to investors, such as industry trends, competitive landscape, and future growth prospects.

Conclusion

By reading the prospectus carefully, you can:

- Compare different investment options.

- Spot any potential risks.

- See if the investment aligns with your goals and risk tolerance

What is a Covered Call? Overview of a Covered Call Strategy

As an investor, navigating the stock market can often involve balancing potential profits with risks. One strategy that stands out for its is the Covered Call Strategy. This approach allows you to generate income from your stock holdings Let's dive into what a covered call is and how this strategy can benefit you as an investor.

Understanding a Covered Call Strategy

Imagine you own shares of a company. You believe the stock may rise in the long run but don't expect gains in the near term. However, you still want to earn some income from these shares in the meantime. This is where a covered call strategy comes in

In a covered call strategy, an investor sells a call option on a stock they already own. This nets them a premium from the sale of the option. the call option is sold as an Out of The Money (OTM) call, meaning the option's strike price is higher than the current stock price. The call option would not get exercised unless the stock price increases above the strike price. Until then, the investor retains the premium as income, making this strategy attractive for those who are neutral to moderately bullish about their stock.

How a Covered Call Strategy Works

To use a covered call option strategy, you must first own the stock of a company. Let's assume you already hold the stock, showing a bullish movement. Over time, you become unsure about the stock's short-term upside potential and don't expect a significant price increase. Here's what you can do:

- Sell a Call Option: You sell a call option contract at a strike price higher than your stock's purchase price. The buyer of the call option pays you a premium for this contract.

- Collect the Premium: Regardless of whether the option is exercised, you keep the premium. This becomes your immediate income from the stock.

- Outcome Scenarios: After executing a covered call strategy, one of three scenarios can occur:some text

- Stock Price Remains Stable or Falls: The call option expires worthless, and you keep both the premium and your shares.

- Stock Price Rises Slightly: The stock price increases but remains below the strike price. The call option still expires worthless, allowing you to keep the premium and benefit from the stock's appreciation.

- Stock Price Rises Significantly: The stock price rises above the strike price. The call option is exercised, and you must sell your shares at the strike price. You keep the premium and receive the strike price for your shares, potentially missing out on further gains beyond the strike price.

When to Use a Covered Call

The covered call strategy works particularly well in the following situations:

Generating Income

The primary use of the covered call strategy is to generate income. If you own assets like stocks or ETFs that you're willing to sell at a certain price, selling a covered call can help generate additional income.

Neutral or Slightly Bullish Market

The covered call strategy is effective in a neutral or slightly bullish market. If you expect the price of an asset to remain relatively stable or increase slightly, selling a covered call can allow you to generate income while still owning the asset and benefiting from modest price increases.

Reducing Risk/Hedging

By selling a call option, you can theoretically limit downside risk if the price of the underlying stock falls. If the stock price drops below the strike price of the call option, the option will expire worthless, and you'll still own the underlying stock, which you can sell or hold for potential future gains.

When to Avoid a Covered Call

A covered call should be avoided in the following situations:

Expecting a Stock Price Rise

If you expect the stock to rise significantly in the near future, selling a covered call may limit your potential upside. It's better to hold onto the stock and let it appreciate.

Facing Serious Downside

If the stock looks like it's going to drop significantly, using a covered call to get extra cash might not be wise. In such cases, it’s probably best to sell the stock or consider short selling to profit from its decline.

Advantages of a Covered Call Strategy

- Generates Income: Covered calls generate income from holdings that wouldn't otherwise provide a cash flow stream.

- Adds to Returns: Investors periodically sell covered call options to enhance a position's return.

- Acts as a Hedge: A covered call offers some protection by reducing the breakeven price due to the premium.

- Low-Risk Strategy: Selling covered calls is easy and low-risk because the stock position "covers" the short call.

Conclusion

In summary, covered calls can be a strategy for investors looking for risk management and income generation. By merging stock ownership with the sale of call options, investors can increase their potential returns in a moderate appreciation of stock price. This strategy provides a balance between earning additional income and managing risks, making it a valuable tool for an investor.

Learn more about financial terminologies with Swastika!

How to Use Open Interest for Intraday Trading

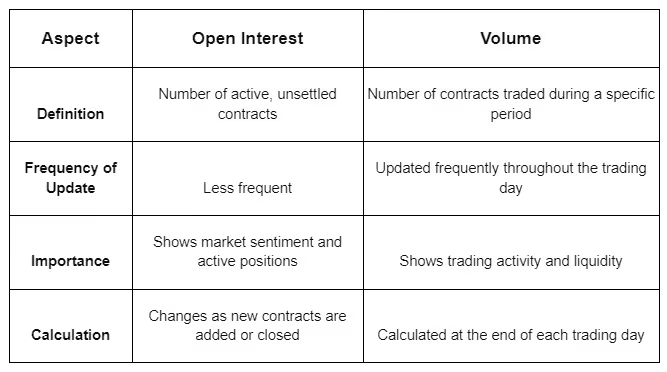

What is Open Interest?

Open interest refers to the total number of outstanding options and futures contracts that have not been settled, closed out, or exercised. In simple terms, it's the number of active positions in options and futures contracts. For example, if a buyer and a seller enter into a new call option contract, open interest increases by one. Conversely, if the same buyer and seller close their contract by taking an opposite position, open interest decreases by one. If the buyer sells their contract to another buyer, the open interest remains unchanged, as there is no net change in open positions.

How to Use Open Interest for Intraday Trading

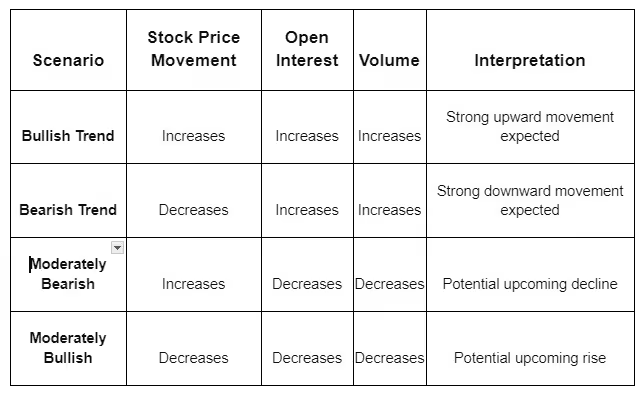

- Bullish Trend: If the stock price rises along with an increase in open interest and volume, it shows a bullish trend.

- Bearish Trend: If the stock price falls along with an increase in open interest and volume, it shows a bearish trend.

- Moderately Bearish: If the stock price rises but open interest and volume decrease, it shows a moderately bearish trend.

- Moderately Bullish: If the stock price falls but open interest and volume decrease, it shows a moderately bullish trend.

Open Interest vs. Volume

Importance of Open Interest

Monitoring open interest provides valuable insights for making decisions in financial markets. Here are some key points:

- Market Sentiment Indicator: Changes in open interest shows bullish or bearish sentiment of the market.

- Price Trend Confirmation: Rising open interest signal uptrends, while falling open interest may signal downtrends.

- Reversal Indication: Sudden changes in open interest can hint at trend reversals.

- Liquidity and Trading Activity: High open interest shows increased market liquidity and trading activity.

- Options Expiry Consideration: Important in options trading, helps in influencing decisions around expiry dates.

- Contrarian Indicator: Analyses extreme open interest situations for potential contrarian trading opportunities.

Example in INR

Suppose an investor is tracking a stock with the following details:

- Current Stock Price: ₹500

- Open Interest: 10,000 contracts

- Volume: 5,000 contracts

Conclusion

By analyzing open interest along with volume and price action, you can identify market trends. Once you've identified the trend, you can take appropriate positions. To get specific open interest data for an asset, use an open interest calculator, which is often available online for free.

Stock Market Vs Commodity Market

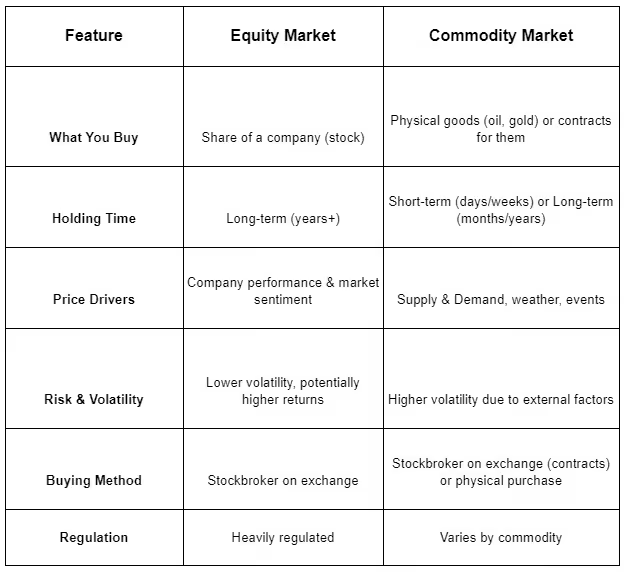

What is the Equity Market?

The equity market, commonly known as the stock market or share market, is a platform where people buy and sell shares of companies. In India, these shares are traded on stock exchanges or directly between individuals. To trade shares online in India, you need a "demat account" and a "trading account." These accounts function like digital wallets for your shares.

What is the Commodity Market?

Commodities are important resources that can be traded for other commodities of the same type. They are divided into two categories: hard commodities like gold and oil, and soft commodities like agricultural products and cattle. The commodity market is a place where these commodities are bought and sold, either physically or virtually. Investments in commodities can be made directly or through commodity futures contracts.

Key Differences: Equity Market vs. Commodity Market

Knowing the differences between these two markets can help you decide which one suits your investment goals better. Here are some key differences:

Performance Comparison

The stock market and commodity market can perform differently:

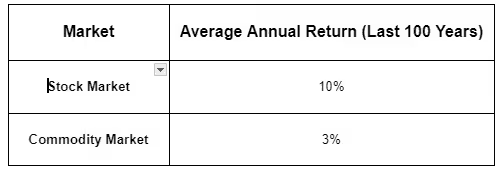

- Stock Market: Historically, the stock market has provided higher returns, with an average annual return of around 10% over the last 100 years.

- Commodity Market: The commodity market has averaged around 3% annual returns.

Factors influencing these markets differ as well. Stock market performance is driven by company earnings, economic growth, interest rates, and geopolitical events. Meanwhile, the commodity market is influenced by supply and demand factors like weather conditions, production levels, and geopolitical events.

Which Market Should You Choose?

Choosing between the stock market and the commodity market depends on your investment goals, risk tolerance, and investment horizon:

- Long-Term Growth: The stock market may be better for long-term growth and capital appreciation.

- Short-Term Speculation: The commodity market may be suitable for short-term speculation and hedging against inflation.

Both markets carry risks. The stock market is subject to market volatility and company-specific risks, while the commodity market is influenced by supply and demand factors and geopolitical risks. It's essential to conduct thorough research and consult with a financial advisor before making any investment decisions.

Example: Comparing Returns in INR

For instance, if you invested ₹1,00,000 in the stock market, you could expect an average return of ₹10,000 annually. In contrast, the same investment in the commodity market would yield around ₹3,000 annually.

Conclusion

Both the equity and commodity markets offer unique opportunities and risks. Understanding these differences and how each market works can help you make informed investment decisions. Whether you're looking for long-term growth in the stock market or short-term gains in the commodity market, it's crucial to align your investments with your financial goals and risk tolerance.

Understanding Commodity Transaction Tax (CTT): A Comprehensive Guide

In the realm of financial markets, various taxes and fees play a crucial role in regulating transactions and generating revenue for the government. One such tax that impacts commodity trading in India is the Commodity Transaction Tax (CTT). In this comprehensive guide, we will delve into the details of CTT, exploring its purpose, impact, and implications for traders and investors.

What is Commodity Transaction Tax (CTT)?

Commodity Transaction Tax (CTT) is a tax imposed by the Indian government on transactions executed on commodity exchanges. Introduced in the Finance Act, 2013, CTT is similar to the Securities Transaction Tax (STT) imposed on equity transactions. The primary objective of CTT is to generate revenue for the government and discourage speculative trading in commodity markets.

How Does CTT Work?

- CTT is imposed on the value of taxable commodities transactions conducted on recognized commodity exchanges in India. The tax rate varies depending on the type of commodity and the nature of the transaction. As of the latest guidelines, the following rates apply:

- CTT tax is 0.01% for non-agricultural commodities futures contracts and 0.05% for non-agricultural commodities options contracts. While agricultural commodities are exempt.

- CTT is typically collected by the commodity exchange at the time of the transaction and passed on to the government. It is applied to both buy and sell transactions, thereby impacting both buyers and sellers in the commodities market.

Purpose and Objectives of CTT

The imposition of CTT serves several purposes and objectives, including:

- Revenue Generation: CTT serves as a source of revenue for the government, contributing to the overall tax collection and fiscal management.

- Discouraging Speculative Trading: By imposing a tax on commodities transactions, especially in non-agricultural commodities, CTT aims to discourage speculative trading and promote more stable and orderly commodity markets.

- Level Playing Field: CTT helps create a level playing field between different asset classes by subjecting commodity trading to similar taxation as equity trading, where STT is applicable.

- Regulatory Oversight: CTT also serves as a regulatory tool, enabling authorities to monitor and regulate commodities transactions more effectively.

Impact of CTT on Traders and Investors

The imposition of CTT has several implications for traders and investors active in commodity markets:

- Cost of Transactions: CTT adds to the overall cost of trading in commodities, as traders are required to pay the tax on every transaction executed on the exchange.

- Impact on Trading Volumes: The introduction of CTT may have an impact on trading volumes in commodity markets, as it could discourage high-frequency traders and speculators from participating in the market.

- Risk Management: Traders and investors need to factor in the impact of CTT when creating their trading strategies and risk management plans. The tax can influence decision-making regarding position sizing, trading frequency, and holding periods.

- Market Liquidity: CTT may affect market liquidity in commodity markets, as it could lead to reduced trading activity and narrower bid-ask spreads.

- Compliance Requirements: Market participants need to ensure compliance with CTT regulations and reporting requirements to avoid penalties and legal repercussions.

Challenges and Criticisms of CTT

While CTT serves certain objectives, it has also faced criticism and challenges:

- Impact on Market Efficiency: Critics argue that CTT may hamper market efficiency by reducing liquidity and increasing transaction costs, especially for small investors and hedgers.

- Competitive Disadvantage: Some stakeholders believe that the imposition of CTT puts Indian commodity exchanges at a competitive disadvantage compared to global counterparts where similar taxes are not levied.

- Need for Review: There have been calls for a review of CTT rates and structures to ensure that they strike the right balance between revenue generation and market development.

Conclusion

In conclusion, Commodity Transaction Tax (CTT) is a tax levied on transactions conducted on commodity exchanges in India. It serves various purposes, including revenue generation, discouraging speculative trading, and promoting regulatory oversight. While CTT has implications for traders and investors in commodity markets, it also faces challenges and criticisms regarding its impact on market efficiency and competitiveness. As the commodities market continues to evolve, it remains essential for policymakers to review and adapt CTT regulations to ensure a balance between revenue objectives and market development goals.

Start Investing Today!

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App