Adani vs. Vedanta — The JAL Insolvency Battle and What It Means for Market Investors

Quick Summary

- Jaypee Associates Limited (JAL) is one of the largest ongoing insolvency cases under the Insolvency and Bankruptcy Code (IBC), involving massive debt and multiple creditors.

- Adani Group and Vedanta have emerged as key contenders bidding for assets under the Corporate Insolvency Resolution Process (CIRP).

- The outcome could reshape ownership of cement plants, power assets, and real estate holdings worth thousands of crores.

- Homebuyers, financial creditors, and operational creditors are all stakeholders with competing interests before the NCLT.

- For investors, the resolution process signals how large conglomerates use stressed asset acquisition as a growth lever in India's distressed debt market.

There is a certain drama that plays out every time two of India's biggest conglomerates go head to head for a prize asset. The courtrooms of the National Company Law Tribunal (NCLT) rarely make front-page news in the way a Sensex rally does. But the ongoing tussle over Jaypee Associates Limited — better known as JAL — is the kind of story that quietly shapes the financial landscape for years to come.

This is not just a legal dispute. It is a window into how India's insolvency ecosystem actually works, who benefits, who takes a haircut, and why companies like Adani Group and Vedanta see opportunity where others see risk.

The JAL Story: How Did We Get Here?

The Jaypee Group was once one of India's most diversified conglomerates. From the Yamuna Expressway to cement plants to hydro power projects, the group had its fingerprints on some of the country's most ambitious infrastructure. But aggressive expansion, mounting debt, and execution challenges eventually caught up with it.

By the time JAL was admitted into insolvency proceedings under the IBC, its debt had ballooned to a figure that few resolution applicants could comfortably absorb. The admitted financial debt alone runs into tens of thousands of crores, with a large chunk owed to banks like ICICI Bank, IDBI Bank, and other institutional lenders.

What Is JAL?

Jaypee Associates Limited is the flagship holding entity of the Jaypee Group, promoted by Manoj Gaur. It holds stakes in various subsidiaries involved in cement manufacturing, power generation, real estate development, and infrastructure construction. The insolvency case before the NCLT has been one of the most watched resolutions under India's IBC framework due to the sheer scale of assets and the complexity of stakeholder interests involved.

What makes JAL particularly complex is the layered nature of its corporate structure. Several subsidiaries are separately listed or undergoing their own resolution proceedings, which means any bidder for JAL effectively needs a clear roadmap for how they intend to deal with those interdependencies. That is no small task.

Why Adani and Vedanta Want a Piece of This

It is worth asking why two of India's most acquisitive conglomerates would wade into such complexity. The answer lies in the quality of the underlying assets beneath the debt overhang.

The Cement Angle

JAL's cement plants, particularly the ones in Madhya Pradesh and Himachal Pradesh, are operationally functional and strategically located. Adani, which has been aggressively scaling its cement business following the acquisition of Holcim India's assets (now Ambuja Cements and ACC), would see JAL's cement capacity as a meaningful bolt-on. Adding capacity through a stressed asset purchase is almost always cheaper than greenfield construction, and it allows immediate market share gains in central and northern India.

The Power Play

Vedanta's interest, on the other hand, is believed to be tilted toward the power and energy assets within JAL's portfolio. Anil Agarwal's group has historically viewed energy as a core vertical, and acquiring operational hydro power capacity at a discount to replacement cost fits neatly into that strategy.

"In distressed asset acquisitions, you are essentially buying time — time the original promoter ran out of but time the acquirer believes it can monetize effectively."

Both bids, in their own way, reflect a calculated bet. The bidders are not just paying for current cash flows. They are paying for strategic positioning, and they are doing so at prices that only become available when a company goes through the insolvency wringer.

The IBC Process: A Quick Primer for Investors

India's Insolvency and Bankruptcy Code, enacted in 2016, was designed to resolve corporate distress in a time-bound manner and improve creditor recovery rates. Before IBC, bank NPAs often lingered for a decade in litigation. The code set a 180-day resolution window (extendable to 270 days) and created a clear hierarchy of creditors.

- CIRP Initiation: A financial creditor, operational creditor, or the company itself files before the NCLT. An Insolvency Resolution Professional (IRP) is appointed.

- Moratorium Period: All legal proceedings against the company are paused. This gives the IRP time to assess assets and liabilities.

- Committee of Creditors (CoC): Financial creditors form a CoC that evaluates resolution plans submitted by bidders.

- Resolution Plan: Bidders submit plans detailing how they will restructure debt, manage operations, and protect stakeholder interests.

- NCLT Approval: The accepted plan goes to the NCLT for approval. Any aggrieved party can appeal to the NCLAT and then to the Supreme Court.

In JAL's case, the process has taken considerably longer than the statutory timeline owing to multiple legal challenges, appeals, and the sheer complexity of the asset base. This is actually quite common in large-ticket cases — the resolution of Essar Steel, for instance, took close to three years before ArcelorMittal's plan was approved.

The Homebuyer Factor: A Stakeholder Often Overlooked

One aspect of the JAL case that sets it apart from a typical industrial insolvency is the large number of homebuyers caught in the crossfire. Thousands of families had booked homes in Jaypee Group's various real estate projects — many of them in the Noida and Greater Noida region — and paid substantial sums toward properties that remain incomplete.

The Supreme Court of India has been particularly vocal about the rights of homebuyers in insolvency proceedings. In landmark judgments, the court recognized homebuyers as financial creditors under IBC, giving them a seat at the table in the Committee of Creditors. Any resolution plan that does not adequately address the delivery of homes or refund of amounts paid is likely to face judicial scrutiny.

This adds another layer of complexity for Adani, Vedanta, or any other bidder. Winning the bid is only the beginning. The acquirer also inherits the moral and contractual obligation to address the homebuyer problem in some form, whether through project completion or a structured refund mechanism.

What the Market Is Watching

From a markets perspective, the JAL resolution has several ripple effects worth tracking.

Cement Sector Consolidation

If Adani secures JAL's cement assets, the competitive dynamics in the cement industry will shift further. The market is already navigating a duopoly-ish structure with Adani and UltraTech holding commanding positions. Additional capacity in JAL's hands would reinforce that trajectory and could have implications for pricing power and margins across the sector.

Distressed Asset Valuations

The resolution price — whatever it eventually turns out to be — will set a reference point for how stressed assets in the cement and power space are valued. SEBI-registered analysts and institutional research desks will use it to benchmark ongoing valuations, especially for companies with similar leverage profiles.

Bank NPA Recovery Rates

For the banking sector, JAL's resolution is a data point in the long story of NPA cleanup. How much of the admitted debt the lenders actually recover will reflect on the headline recovery rates under IBC, which hover between 25% and 45% on average according to recent IBBI data. A higher recovery in JAL could slightly improve sector-wide sentiment around NPA provisioning.

The Regulatory and Legal Landscape

The NCLT Allahabad bench has been handling the JAL case, and given the size and sensitivity of the matter, it has attracted interventions from multiple parties. The Insolvency and Bankruptcy Board of India (IBBI) periodically updates its regulations around the resolution process, and any procedural gaps in the JAL case have the potential to trigger appeals that drag the timeline further.

For investors who follow such cases closely, the IBBI Annual Reports and NCLT order databases are invaluable resources. They offer transparency into the resolution timelines, haircut percentages, and the industry breakdown of stressed assets — all of which feed into sector-level analysis.

Lessons for Individual Investors

You do not need to be a legal expert to draw useful insights from how a case like JAL unfolds. Here are a few practical takeaways.

First, when a company is under CIRP, its listed group entities often experience significant stock price volatility. Investors sometimes confuse the existence of a resolution process with a sign of imminent recovery, when in reality the outcome is deeply uncertain. Do not anchor on pre-insolvency price levels.

Second, the acquirer's stock is worth watching. When Adani announced its acquisition of Holcim India's assets, the market eventually re-rated the cement segment's earnings potential upward. A similar dynamic could play out if JAL's cement assets land in Adani's lap and are successfully integrated.

Third, the banking sector exposure matters. Banks with heavy exposure to JAL on their books will see some relief once a resolution plan is approved and proceeds are distributed. Tracking NPA recovery for specific lenders can give you a sense of incremental clean-up in their balance sheets.

Frequently Asked Questions

What exactly is the JAL insolvency case about?

JAL or Jaypee Associates Limited is the holding company of the Jaypee Group, which accumulated large amounts of debt through infrastructure and real estate projects. After failing to service this debt, the company was admitted into the Corporate Insolvency Resolution Process (CIRP) under India's Insolvency and Bankruptcy Code. The case is being heard by the NCLT and involves financial creditors, operational creditors, and thousands of homebuyers as stakeholders.

Why are Adani and Vedanta interested in JAL?

Both groups see strategic value in JAL's underlying assets. Adani is reportedly interested in the cement manufacturing capacity, which would complement its rapidly growing cement business. Vedanta is believed to be attracted to the power and energy assets. Acquiring through insolvency allows them to buy operational assets at a discount compared to building from scratch or buying from a healthy seller.

How does the JAL case affect ordinary investors?

Investors in listed entities linked to the Jaypee Group, the acquiring companies, or the lender banks should pay attention. The resolution outcome could impact stock valuations in the cement sector, affect the NPA provisioning levels of lending banks, and signal broader trends in India's distressed debt market. It also demonstrates how India's IBC framework is being tested on complex, multi-stakeholder cases.

What happens to homebuyers if a resolution plan is approved?

Following Supreme Court rulings that recognised homebuyers as financial creditors, any approved resolution plan must address their claims. Typically this means either committing to complete the housing projects or offering a structured refund mechanism. However, the exact treatment depends on the resolution plan submitted by the successful bidder and approved by the NCLT.

What is the role of SEBI in insolvency-related market activity?

SEBI's primary role here is to ensure that listed group companies comply with disclosure norms throughout the insolvency process. Any material development, such as a resolution plan being submitted or approved, must be disclosed to stock exchanges promptly. SEBI also monitors for any insider trading or market manipulation that might occur around such sensitive corporate events.

The Bigger Picture

The Adani versus Vedanta contest for JAL is more than a corporate legal battle. It is a test of whether India's insolvency architecture can deliver on its original promise of faster resolution, better creditor recovery, and a second life for stressed assets under new ownership.

For the Indian capital markets, every large IBC resolution that concludes cleanly adds a layer of credibility to the system. It reassures foreign institutional investors that India has functional legal recourse for distressed debt. It signals to domestic banks that writing off an NPA does not mean writing off the asset forever. And it gives conglomerates with strong balance sheets and appetite for growth a legitimate, regulated route to acquire capacity at a point in the business cycle when valuations are compressed.

Watch this space. The JAL case has a long way to go before a gavel falls and a winning bidder walks away with the keys. But the contours of the resolution, when they become clear, will tell us something important about the direction of India's corporate landscape in the years ahead.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

.avif)

Types of Orders

What Is an Order?

An order is an instruction given to a broker or brokerage firm to buy or sell a security for an investor. It's the basic way to trade in the stock market. Orders can be placed by phone, online, or through automated systems and algorithms. Once an order is placed, it goes through a process to be completed.

There are different types of orders, allowing investors to set conditions like the price at which they want the trade to happen or how long the order should stay active. These conditions can also determine whether an order is triggered or cancelled based on another order.

Types of Orders

Market Order

A market order is an instruction to buy or sell a stock at the current price available in the market. With a market order, the investor doesn't control the exact price they pay or receive—the market decides the price. In a fast-moving market, the price can change quickly, so you might end up paying more or receiving less than expected.

For example, if an investor wants to buy 100 shares of a stock, they will get those 100 shares at whatever the current asking price is at that moment. If the price is ₹500 per share, they’ll buy 100 shares for ₹500 each. However, if the price changes before the order is executed, they might pay a different amount.

Limit Order

A limit order is an instruction to buy or sell a stock at a specific price or better. This allows investors to avoid buying or selling at a price they don't want. If the market price doesn't match the price set in the limit order, the trade won't happen. There are two types of limit orders: a buy limit order and a sell limit order.

Buy Limit Order:

A buy limit order is placed by a buyer, specifying the maximum price they are willing to pay. For example, if a stock is currently priced at ₹900, and an investor sets a buy limit order for ₹850, the order will only go through if the stock price drops to ₹850 or low

Sell Limit Order:

A sell limit order is placed by a seller, specifying the minimum price they are willing to accept. For example, if a stock is currently priced at ₹900, and an investor sets a sell limit order for ₹950, the order will only go through if the stock price rises to ₹950 or higher.

Stop Order

A stop order, also known as a stop-loss order, is a trade order that helps protect an investor from losing too much money on a stock. It automatically sells the stock when its price drops to a certain level. While stop orders are commonly used to protect a long position (where the investor owns the stock), they can also be used with a short position (where the investor has sold a stock they don't own yet). In that case, the stock would be bought if its price rises above a certain level.

Example for a Long Position:

Imagine an investor owns a stock currently priced at ₹1,000. They're worried the price might drop, so they place a stop order at ₹800. If the stock price falls to ₹800, the stop order will trigger, and the stock will be sold. However, the stock might not sell exactly at ₹800—it could be sold for less if the price is dropping quickly.

Example for a Short Position:

If an investor has shorted a stock at ₹1,000 and doesn't want to lose too much if the price rises, they might set a stop order at ₹1,200. If the price goes up to ₹1,200, the stop order will trigger, and the investor will buy the stock at that price (or higher if the price is rising quickly) to cover their short position.

To avoid selling at a much lower price than expected, investors can use a stop-limit order, which sets both a stop price and a minimum price at which the order can be executed.

Stop-limit order

A stop-limit order is a trade order that combines features of both a stop order and a limit order. It involves setting two prices: the stop price and the limit price. When the stock reaches the stop price, the order becomes a limit order. This means the stock will only be sold if it can meet or exceed the limit price, giving the investor more control over the selling price.

Example:

Let's say an investor owns a stock currently priced at ₹2,500. They want to sell the stock if the price drops below ₹2,000, but they don't want to sell it for less than ₹1,900. To do this, the investor sets a stop-limit order with a stop price of ₹2,000 and a limit price of ₹1,900.

If the stock price falls to ₹2,000, the stop order triggers, but the stock will only be sold if it can get at least ₹1,900 per share. If the price drops too quickly and falls below ₹1,900 before the order can be executed, the stock won’t be sold until it reaches ₹1,900 or higher.

In contrast, a regular stop order would sell the stock as soon as it hits ₹2,000, even if the price continues to fall rapidly and ends up selling for less. The stop-limit order gives the investor more control over the price, but there’s a chance the stock won’t sell if the limit price isn’t met.

Trailing stop order

A trailing stop order is a type of stop order that adjusts automatically based on the stock's price movement. Instead of setting a specific price, the trailing stop is based on a percentage change from the stock's highest price. This helps protect profits while allowing the stock to rise in value. If the stock's price falls by the set percentage, the order is triggered and the stock is sold.

Example for a Long Position:

Imagine an investor buys a stock at ₹1,000 and sets a trailing stop order with a 20% trail. If the stock price goes up to ₹1,200, the trailing stop will automatically move up to ₹960 (20% below ₹1,200). If the stock price then drops to ₹960 or lower, the trailing stop order will trigger, and the stock will be sold.

Example for a Short Position:

If an investor has shorted a stock at ₹1,000 and sets a trailing stop of 10%, the stop price would move down as the stock price falls. If the stock price rises by 10% from its lowest point, the trailing stop order will trigger, and the stock will be bought to cover the short position.

The trailing stop order allows the investor to lock in gains as the stock price moves favorably, while still providing protection if the market turns.

Immediate or Cancel (IOC) order

An Immediate or Cancel (IOC) order is a type of stock order that must be executed immediately. If the full order cannot be filled right away, whatever portion can be filled will be completed, and the rest will be canceled. If no part of the order can be executed immediately, the entire order is canceled.

Example:

Suppose an investor places an IOC order to buy 500 shares of a stock at ₹1,000 per share. If only 300 shares are available at ₹1,000 right away, the IOC order will purchase those 300 shares, and the remaining 200 shares will be canceled. If no shares are available at ₹1,000 immediately, the entire order will be canceled.

Good Till Cancelled (GTC) order

A Good Till Cancelled (GTC) order is a type of stock order that stays active until you choose to cancel it. Unlike other orders that expire at the end of the trading day, a GTC order remains open until you either cancel it or it gets executed. However, most brokerages set a limit on how long you can keep a GTC order open, usually up to 90 days.

Example:

Let's say an investor wants to buy a stock at ₹500, but the current price is ₹600. They place a GTC order to buy 100 shares at ₹500. This order will stay active until the stock price drops to ₹500 and the order is filled, or until the investor cancels the order. If the price never drops to ₹500 and the investor doesn't cancel the order, it will automatically expire after 90 days (or whatever time limit the brokerage sets).

Good 'Till Triggered (GTT) order

A Good 'Till Triggered (GTT) order is similar to a Good 'Til Canceled (GTC) order but with a key difference: a GTT order only becomes active when a specified trigger condition is met. Once the trigger price is reached, the order is placed in the market. If the trigger price is not reached, the order stays inactive.

Example:

Imagine an investor wants to buy a stock currently priced at ₹600, but only if it drops to ₹550. They set a GTT order with a trigger price of ₹550. If the stock price falls to ₹550, the order is activated and placed in the market. If the price never drops to ₹550, the order remains inactive until it reaches the trigger price or the investor cancels it.

GTT orders can also have a time limit, so if the trigger price isn’t reached within a certain period, the order will expire.

Conclusion

In the stock market, an order is a fundamental instruction to buy or sell a security, tailored to an investor's strategy and market conditions. The various types of orders—such as market, limit, stop, stop-limit, trailing stop, IOC, GTC, and GTT—offer flexibility to manage price, timing, and risk. Understanding these order types empowers investors to execute trades more effectively, ensuring alignment with their financial goals and risk tolerance.

Learn how to optimize your trades and manage risk with Swastika!

Understanding Long Strangles

The stock market can be unpredictable, and sometimes you might have a feeling that a stock's price will move significantly, but you're unsure if it will go up or down. This is where the long strangle strategy comes in.

The long strangle can be a valuable strategy for options traders who anticipate high volatility but are unsure of the price direction. However, it's important to understand the risks involved, including limited profit potential and the possibility of losing your entire investment.

What is a Long Strangle?

A long strangle is an options trading strategy that helps investors make money when they expect a big price move in a stock but aren't sure which direction it will go. This strategy involves buying two options: a call option and a put option with different strike prices. Both options are out-of-the-money, meaning they are not yet profitable at the current stock price.

Both call and put options are out-of-the-money (OTM), meaning their strike prices are above (for calls) or below (for puts) the current market price of the underlying asset.

Why Use a Long Strangle?

- Profit from Volatility: This strategy aims to benefit from a large price movement in the underlying asset, regardless of the direction (up or down).

- Lower Cost: Compared to a straddle, long strangles are generally less expensive because OTM options cost less than at-the-money (ATM) options used in straddles.

Example (using INR):

Imagine Nifty is at 10,400 and you expect an important price swing but are unsure of the direction. You can create a long strangle by:

- Buying a Nifty call option with a strike price of ₹10,600 (OTM call).

- Buying a Nifty put option with a strike price of ₹10,200 (OTM put).

Key Points:

- The net cost you pay for both options is your maximum loss.

- You'll potentially make a profit if the Nifty price moves above ₹10,600 (call strike + premium) or below ₹10,200 (put strike - premium).

Here's a table summarizing the profit and loss potential:

Break-even Points:

A long strangle has two break-even points:

- Lower Break-even Point: Strike price of Put - Net Premium

- Upper Break-even Point: Strike price of Call + Net Premium

The stock price needs to move beyond these break-even points for you to start making a profit.

Risks to Consider:

- Limited Profit Potential: a long strangle has a limited profit potential capped by the strike prices and volatility.

- Losing Your Investment: If the stock price ends up between the strike prices at expiration, you lose your entire investment (net debit).

When to Use a Long Strangle:

- High Volatility Expected: This strategy is suitable when you predict significant price changes in the underlying asset due to events like elections, policy changes, or earnings announcements.

Steps to Execute a Long Strangle:

- Choose the Underlying Asset: Select a stock or index where you expect an important price movements but are unsure of the direction.

- Pick OTM Strike Prices: Choose strike prices for both call and put options that are OTM but allow for enough price movement in either direction.

- Calculate Total Cost: Determine the combined cost of buying both options, including fees and commissions.

- Place Your Orders: Place buy orders for the chosen call and put options with specific expiration dates and strike prices. Make sure that you have sufficient funds in your brokerage account.

Conclusion:

The long strangle can be a valuable strategy for options traders who predict high volatility but are unsure of the price direction. However, it's crucial to understand the risks involved, including limited profit potential and the possibility of losing your entire investment.

Learn more about financial terminologies with Swastika!

What is a Bear Put Spread?

Options trading offers various strategies to maximize returns and minimize risks. One common strategy is the bear put spread, which helps investors profit from a gradual decline in a stock’s price. This blog will explain the bear put spread in simple terms with easy examples.

Goal of the Bear Put Spread

The primary goal of a bear put spread is to profit from a gradual decrease in the price of the underlying stock.

Understanding the Bear Put Spread

A bear put spread involves two steps:

- Buy a Put Option (Long Put): This gives you the right to sell a stock at a higher price.

- Sell a Put Option (Short Put): This obligates you to buy the same stock at a lower price if exercised.

Both options have the same stock and expiration date. You set up this strategy for a net cost (or net debit) and profit when the stock's price falls.

How to Set Up a Bear Put Spread

- Buy an ATM Put Option: An at-the-money (ATM) put option has a strike price close to the current market price.

- Sell an OTM Put Option: An out-of-the-money (OTM) put option has a strike price lower than the current market price.

- Ensure Both Options Have the Same Expiry Date

Example of a Bear Put Spread

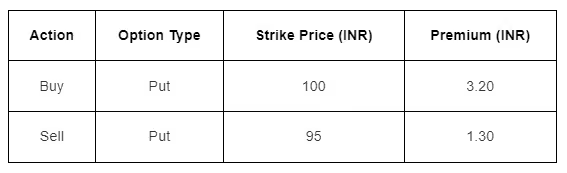

Let's use stock XYZ as an example:

- Total Cost: 3.20 - 1.30 = 1.90 INR

How You Make Money

- Maximum Profit: The most you can earn is the difference between the two strike prices minus the net cost.

In this example:

- Difference between strike prices: 100 - 95 = 5.00 INR

- Net cost: 1.90 INR

- Maximum profit: 5.00 - 1.90 = 3.10 INR

You achieve this maximum profit if the stock price is below the lower strike price (95 INR) at expiration.

- Maximum Loss: The most you can lose is the net cost you paid.

In this example:

- Maximum loss: 1.90 INR

This loss happens if the stock price is above the higher strike price (100 INR) at expiration.

- Breakeven Price: The stock price at which you neither make nor lose money.

In this example:

- Breakeven: 100 - 1.90 = 98.10 INR

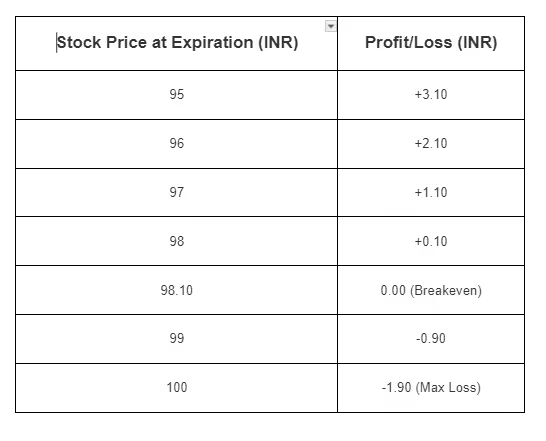

Profit/Loss Table

Advantages and Disadvantages of a Bear Put Spread

Pros

- Less Risky than Short-Selling: Limits your losses to the net amount paid.

- Profitable in Modestly Declining Markets: Effective when expecting moderate price declines.

Cons

- Risk of Early Assignment: The buyer of your short put can exercise it early if the stock price falls sharply. This would force you to buy the stock at a potentially unfavorable price.

- Limited Profit: Profits are capped at the difference between strike prices minus the net cost.

- Risk if Stock Price Rises: If the stock price rises significantly, the strategy results in a loss.

When to Use the Bear Put Spread

This strategy is ideal when you expect a moderate decline in stock prices and want to limit your risk. It works best in low volatility markets, as increased volatility after you enter the trade can amplify profits.

What Does the Bear Put Spread Result In?

The bear put spread results in a net debit, calculated as the difference between the higher and lower strike prices. The maximum loss is the net debit paid.

Closing a Bear Put Spread

It's usually a good idea to close a bear put spread before it expires if it's profitable. This helps you capture the maximum gain and avoid the risk of early assignment on the short put. If the short put is exercised, it creates a long stock position, which can be closed by selling the stock or exercising the long put. These actions may incur additional fees, so closing a profitable position early is often wise.

Summary

The bear put spread is a useful strategy for options traders expecting a moderate decline in stock prices. It offers a balanced approach by limiting both potential profits and losses, making it a safer alternative to other bearish strategies.

Learn more about financial terminologies with Swastika!

The 12 Stock Market Movies You Must Watch

The stock market is a fascinating world filled with drama, mystery, and high stakes. It’s no wonder that Hollywood has produced some incredible movies centered around the financial world. Whether you're a seasoned investor or just curious about the stock market, these movies offer valuable insights and a dose of entertainment. Here are 12 must-watch stock market movies that provide a thrilling look into the highs and lows of trading, investing, and the world of finance.

1. Wall Street (1987)

- Director: Oliver Stone

- Synopsis: This classic movie follows the story of Bud Fox, a young and ambitious stockbroker, who becomes entangled with the ruthless corporate raider Gordon Gekko. Gekko's famous mantra, "Greed is good," captures the essence of the 1980s financial world.

- Why Watch: "Wall Street" is a compelling tale of ambition, greed, and the moral dilemmas faced by those in the high-stakes world of finance. Michael Douglas’s portrayal of Gordon Gekko won him an Academy Award.

2. The Wolf of Wall Street (2013)

- Director: Martin Scorsese

- Synopsis: Based on the true story of Jordan Belfort, this film narrates his rise and fall as a stockbroker who engages in corruption and fraud on Wall Street. It’s a wild ride through the excesses and indulgence of the financial world.

- Why Watch: With Leonardo DiCaprio’s electrifying performance and Scorsese’s masterful direction, this film offers an steadfast look at the darker side of Wall Street. It's both hilarious and horrifying.

3. Margin Call (2011)

- Director: J.C. Chandor

- Synopsis: Set during the early stages of the 2008 financial crisis, "Margin Call" follows key employees at an investment bank over a 24-hour period as they realize the impending disaster.

- Why Watch: This movie provides a gripping and realistic portrayal of the decisions and panic that led to the financial meltdown. The ensemble cast, including Kevin Spacey and Jeremy Irons, delivers powerful performances.

4. The Big Short (2015)

- Director: Adam McKay

- Synopsis: Based on Michael Lewis’s book, "The Big Short" tells the story of a group of investors who predicted the 2008 financial crisis and bet against the housing market, making a fortune in the process.

- Why Watch: This film explains complex financial concepts in an accessible and entertaining way. With a star-studded cast including Christian Bale, Steve Carell, and Ryan Gosling, it’s both educational and highly engaging.

5. Guru (2007)

- Director: Mani Ratnam

- Synopsis: Inspired by the life of businessman Dhirubhai Ambani, "Guru" follows the journey of Gurukant Desai, a village boy who rises to become a powerful tycoon. The film explores his ambition, ethics, and the challenges he faces in building his business empire.

- Why Watch: "Guru" offers a compelling narrative about entrepreneurship, ambition, and the complexities of business ethics. Abhishek Bachchan's portrayal of Gurukant Desai and Aishwarya Rai's performance as his supportive wife add depth to the story.

6. Scam 1992: The Harshad Mehta Story (2020, Web Series)

- Director: Hansal Mehta

- Synopsis: Based on the true story of Harshad Mehta, a stockbroker who was involved in India's largest financial scam in the 1990s. The series chronicles his rise and fall, exploring the complexities of the stock market and the allure of wealth.

- Why Watch: "Scam 1992" is a critically acclaimed series that provides a detailed and nuanced portrayal of the stock market boom and subsequent crash. Pratik Gandhi's performance as Harshad Mehta received widespread praise for its depth and authenticity.

7. The Big Bull (2021)

- Director: Kookie Gulati

- Synopsis: Loosely based on the life of Harshad Mehta, "The Big Bull" portrays the journey of a small-time stockbroker who becomes a financial wizard. The film explores his meteoric rise, manipulation of the stock market, and eventual downfall.

- Why Watch: "The Big Bull" offers a dramatized account of the events surrounding Harshad Mehta's life, providing insights into the stock market's workings and the ethical dilemmas faced by traders. Abhishek Bachchan's performance as the protagonist is captivating.

8. Trading Places (1983)

- Director: John Landis

- Synopsis: This comedy classic tells the story of a snobbish investor and a street hustler whose lives are swapped as part of a bet by two wealthy brothers. The film explores themes of social class and the mechanics of the commodities market.

- Why Watch: "Trading Places" is a hilarious yet insightful look at the financial world. Eddie Murphy and Dan Aykroyd deliver memorable performances in this timeless comedy.

9. Boiler Room (2000)

- Director: Ben Younger

- Synopsis: A college dropout gets a job at a suburban investment firm, where he discovers the firm’s questionable business practices. He quickly rises through the ranks, only to face moral and legal dilemmas.

- Why Watch: "Boiler Room" offers a look at the high-pressure world of stock brokerage firms and the ethical challenges faced by brokers. It’s a thrilling and thought-provoking film.

10. Glengarry Glen Ross (1992)

- Director: James Foley

- Synopsis: Based on David Mamet’s play, this film follows a group of real estate salesmen who are under intense pressure to close deals. The story delves into their desperation and unethical tactics.

- Why Watch: With a stellar cast including Al Pacino, Jack Lemmon, and Alec Baldwin, "Glengarry Glen Ross" is a powerful exploration of the cutthroat nature of sales and the impact of capitalism on individuals.

11. Rogue Trader (1999)

- Director: James Dearden

- Synopsis: This film is based on the true story of Nick Leeson, a derivatives broker who caused the collapse of Barings Bank through unauthorized and risky trades.

- Why Watch: "Rogue Trader" provides a real-world cautionary tale about the dangers of unchecked trading and the consequences of financial recklessness. Ewan McGregor’s portrayal of Leeson is compelling.

12. Equity (2016)

- Director: Meera Menon

- Synopsis: This film centers around a senior investment banker who is navigating the world of IPOs while facing pressures from both her personal and professional life.

- Why Watch: "Equity" is one of the few films that focus on women in finance. It offers a unique perspective on the challenges faced by women in a male-dominated industry and is a gripping drama.

Conclusion

These 12 movies provide a captivating glimpse into the world of finance, each from a unique angle. From comedies to intense dramas and real-life stories, they explore the motivations, challenges, and ethical dilemmas faced by those in the stock market. Whether you’re an aspiring trader, an experienced investor, or simply someone interested in the financial world, these films are both entertaining and educational. They highlight the high stakes, the allure of wealth, and the potential pitfalls of the financial industry. So, grab some popcorn and get ready to dive into the fascinating world of stock market cinema!

How Does Monsoon Impact the Economy and Stock Market?

Monsoon season, with its heavy rains and thunderstorms, is a crucial period for many countries, especially those heavily reliant on agriculture like India. This season significantly impacts the economy and stock market. Let's break down how this happens in simple terms.

1. Impact on Agriculture

a. Crop Production:

Monsoons are essential for watering crops. A good monsoon means enough water for rice, wheat, sugarcane, and other important crops.

When there is enough rain, crops grow well, leading to a good harvest. This means farmers have more produce to sell, which boosts their income.

Conversely, if the monsoon is weak (less rain) or too strong (flooding), crops can be damaged, leading to a poor harvest. This can reduce farmers' incomes and increase food prices.

b. Rural Economy:

A large portion of the population in countries like India lives in rural areas and depends on agriculture for their livelihood.

A good monsoon improves rural incomes, leading to higher spending on goods and services. This increased spending supports local businesses and stimulates economic growth.

2. Impact on Industry

a. Raw Material Supply:

Industries that rely on agricultural products, such as food processing, textiles, and beverages, are directly affected by monsoon performance.

A good harvest ensures a steady supply of raw materials at stable prices, which benefits these industries. Poor monsoons can disrupt supply chains and increase costs.

b. Consumer Goods:

Higher rural incomes from a good monsoon increase the demand for consumer goods, such as electronics, clothing, and household items.

Companies manufacturing these goods see higher sales and profits, positively affecting their stock prices.

3. Impact on Inflation

Inflation is the rate at which prices for goods and services rise. Food prices are a major component of inflation.

A good monsoon keeps food production high and prices low, controlling inflation.

Poor monsoon leads to lower food production, higher prices, and increased inflation, which can affect the entire economy.

4. Impact on Government Finances

The government often has to step in to support farmers during bad monsoon years through subsidies and relief packages.

This additional spending can strain the government's budget and increase public debt.

5. Impact on Stock Market

a. Agricultural Stocks:

Companies directly related to agriculture, like those producing fertilizers, pesticides, and tractors, benefit from a good monsoon. Their stock prices tend to rise as investors anticipate higher sales.

Conversely, a poor monsoon can lead to lower demand for these products, causing stock prices to fall.

b. Consumer Goods Companies:

Companies producing consumer goods see increased sales in rural areas during a good monsoon, leading to higher stock prices.

If the monsoon is poor, reduced rural spending can negatively impact their sales and stock prices.

c. Overall Market Sentiment:

The stock market is influenced by investor sentiment. A good monsoon boosts investor confidence, leading to higher stock prices across various sectors.

A poor monsoon can create uncertainty and lower investor confidence, leading to market volatility and lower stock prices.

6. Impact on Interest Rates

Central banks monitor inflation closely. A good monsoon can lead to lower inflation, allowing central banks to keep interest rates low.

Low-interest rates make borrowing cheaper for businesses and individuals, stimulating economic activity.

High inflation from a poor monsoon might force central banks to raise interest rates to control prices, making borrowing more expensive and potentially slowing down economic growth.

Conclusion

The monsoon season plays a pivotal role in shaping the economy and stock market, particularly in agrarian countries. Good monsoons lead to increased agricultural output, stable inflation, and positive investor sentiment, benefiting the overall economy and stock market. Conversely, poor monsoons can disrupt economic stability, increase inflation, and cause market volatility. Understanding these dynamics helps investors, policymakers, and businesses make smart decisions during the monsoon season.

How to Start Investing in Stock Market in 2024

Whether you’re new to the investing world or have some experience under your belt, understanding the stock market can be a difficult task. With so many options, strategies, and risks involved, it’s important to have a clear understanding of how to invest wisely. In this blog post, we’ll break down the basics of investing in the Indian stock market for beginners, providing you with the knowledge and tools you need to get started.

Understanding the Stock Market

Before diving into stock investing, it’s important to understand what the stock market is and how it works. Simply put, the stock market is a place where you can buy and sell shares of publicly traded companies. It plays a vital role in the global economy by allowing companies to raise capital and enabling investors to own a piece of these companies and potentially profit from their success.

In India, the major stock exchanges facilitating these transactions are the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE). These exchanges provide a platform for trading shares, making it easier for investors to participate and for companies to secure funding.

Why Invest in Stocks?

Step 1. Set Your Investment Goals

Before you start investing, it’s important to define your investment goals. Are you looking to build long-term wealth, save for retirement, or generate passive income? By setting clear goals, you can develop a strategy that aligns with your objectives and risk tolerance.

Step 2.Determine How Much You Can Afford to Invest in Stocks

Before you start investing in stocks, it's important to figure out how much money you can comfortably set aside. First, look at your monthly income and expenses to see how much you have left over. Then, decide on an amount that won’t affect your day-to-day finances or other financial goals. Only invest money you won't need soon, as the market can be unpredictable. This careful planning helps you invest without risking your financial stability.

Step 3. Determine Your Investing Style

Your investing style shapes how you approach the market. Consider your preference: do you enjoy researching stocks and market trends, or do you prefer a more hands-off strategy?

There are three main investing styles:

- Active Investing: You actively manage your portfolio, choosing and trading stocks, bonds, and other assets using advanced brokerage tools. Pros include potential for higher returns and full control, but it's time-consuming and requires extensive research.

- Passive Investing: You invest in index funds, ETFs, or mutual funds through low-cost brokerage accounts. Pros include less time commitment, lower fees, and diversification, though potential returns may be lower compared to active trading.

- Professional Guidance: Working with a financial advisor offers personalized advice and expert management of your investments. Pros include tailored guidance, but cons include advisory fees and less direct control over investment decisions. Choose the style that best fits your goals and comfort level with risk and involvement.

Step 4: Choose the Right Investment Accounts

Selecting the right type of investment account is crucial for maximizing your returns and achieving your financial goals.

Types of Investment Accounts

- Demat Account: A Demat account holds your shares electronically instead of physical certificates. It's necessary for trading in the Indian stock market, providing convenience and security. However, there may be maintenance charges associated with maintaining this account.

- Trading Account: A trading account is used specifically for buying and selling securities in the stock market. It's essential for executing trades and managing your investments effectively. However, brokerage charges may apply for each transaction made through this account.

These accounts serve different purposes and cater to varying financial goals. Choosing the right one depends on your investment horizon, risk tolerance, and financial objectives.

5: Choose Your Investments

- Stocks: Stocks are pieces of ownership in individual companies. They can give you high returns, but they come with higher risk and you need to do your homework to choose wisely.

- Bonds: Bonds are like loans you give to companies or the government. They are safer than stocks and give you steady income, but the returns are usually lower.

- Mutual Funds: Mutual funds collect money from many people to invest in a variety of stocks and bonds. They spread out the risk and are managed by professionals, making them easier for beginners. However, you have to pay management fees and have less say in what gets bought or sold.

- Exchange-Traded Funds (ETFs): ETFs are funds that you can buy and sell on the stock exchange, just like stocks. They offer a mix of investments, usually at lower fees. However, they can have trading costs and can be a bit tricky to understand at first.

6: Tax Implications on Different Account Types

Consider the Tax Implications: Different accounts have different tax rules:

- Taxable Accounts: You pay taxes on any profits you make from selling investments, but you can add or take out money whenever you want.

- Tax-Deferred Accounts: Contributions to traditional IRAs and 401(k) s lower your taxable income now. You pay taxes on the money later when you take it out.

- Tax-Free Accounts: Roth IRAs and Roth 401(k) s are funded with money you've already paid taxes on. Your money grows tax-free, and you won't owe taxes when you take it out in retirement.

Choosing the right investment account depends on your financial goals, how much risk you're comfortable with, and the tax implications you prefer. Each account type has its own benefits and considerations that can impact your investment strategy and long-term financial plans.

Open a Brokerage Account

To begin investing, opening a brokerage account is essential. A brokerage account allows you to buy and sell stocks, bonds, ETFs, and mutual funds through a platform provided by the brokerage firm.

Swastika Investmart offers a range of investment options and personalized services, making it suitable for investors seeking customized solutions and local market expertise. However, its platform may be perceived as less technologically advanced compared to other brokerages listed. Choosing the right brokerage account depends on your specific needs and preferences, whether you prioritize low fees, advanced tools, or specialized customer support.

7: Build a Diversified Portfolio

Diversification helps manage risk by spreading investments across various asset classes.

How to Diversify

- By Asset Class:

- Stocks: Invest in a mix of different sectors and industries.

- Bonds: Include a variety of corporate, government, and municipal bonds.

- Other Assets: Consider real estate, commodities, and alternative investments.

- By Geography:

- Domestic: Invest in companies within your own country.

- International: Include investments in foreign market.

8: Monitor and Rebalance Your Portfolio

Regularly monitoring and rebalancing your portfolio ensures it stays aligned with your goals.

- Monitoring Your Portfolio

- Performance Review: Check the performance of your investments periodically.

- News and Updates: Stay informed about market trends and news affecting your investments.

- Rebalancing

- Frequency: Review and rebalance your portfolio annually or semi-annually.

- Adjustments: Sell over performing assets and buy underperforming ones to maintain your target allocation.

9. Stay Updated &Educate Yourself

One of the most important steps in investing is educating yourself about the basics of investing, different investment options, and the risks involved. There are plenty of resources available online, such as blogs, books, and investment websites like Investopedia, where you can learn more about investing.

Finally, it’s important to stay informed about the stock market and economic trends that may impact your investments. Read financial news, follow market updates, and stay up-to-date on company earnings reports to make informed investment decisions. By staying informed, you can make smarter investment choices and take advantage of profitable opportunities.

Conclusion

Starting to invest in stocks in 2024 requires a clear understanding of the basics, a determination of how much you can afford to invest, an assessment of your risk tolerance, and a defined investing style. By choosing the right investment accounts, selecting diversified investments, and continuously educating yourself, you can build a robust investment portfolio that helps you achieve your financial goals. Remember to regularly monitor and rebalance your portfolio to ensure it stays aligned with your objectives.

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App