The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

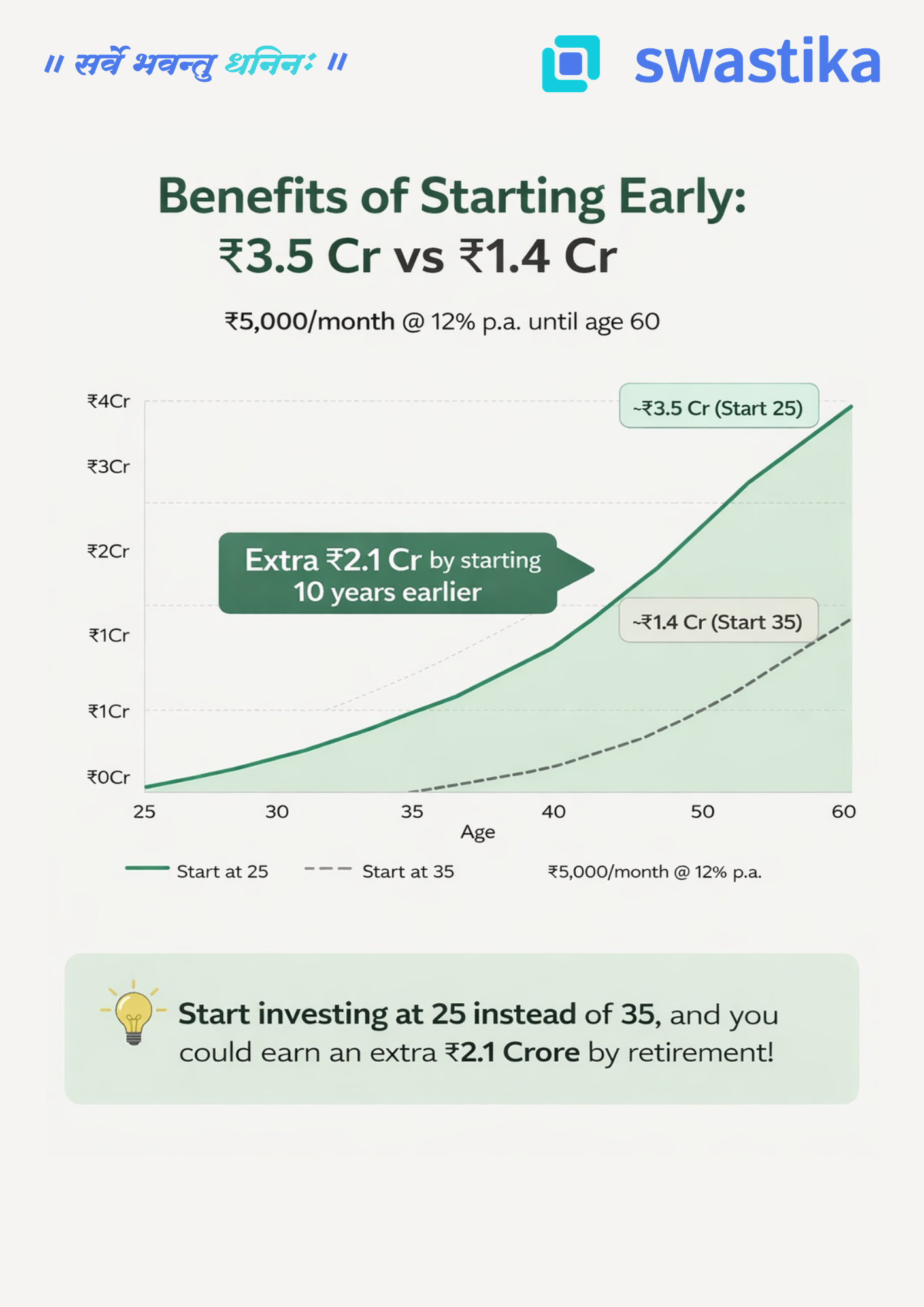

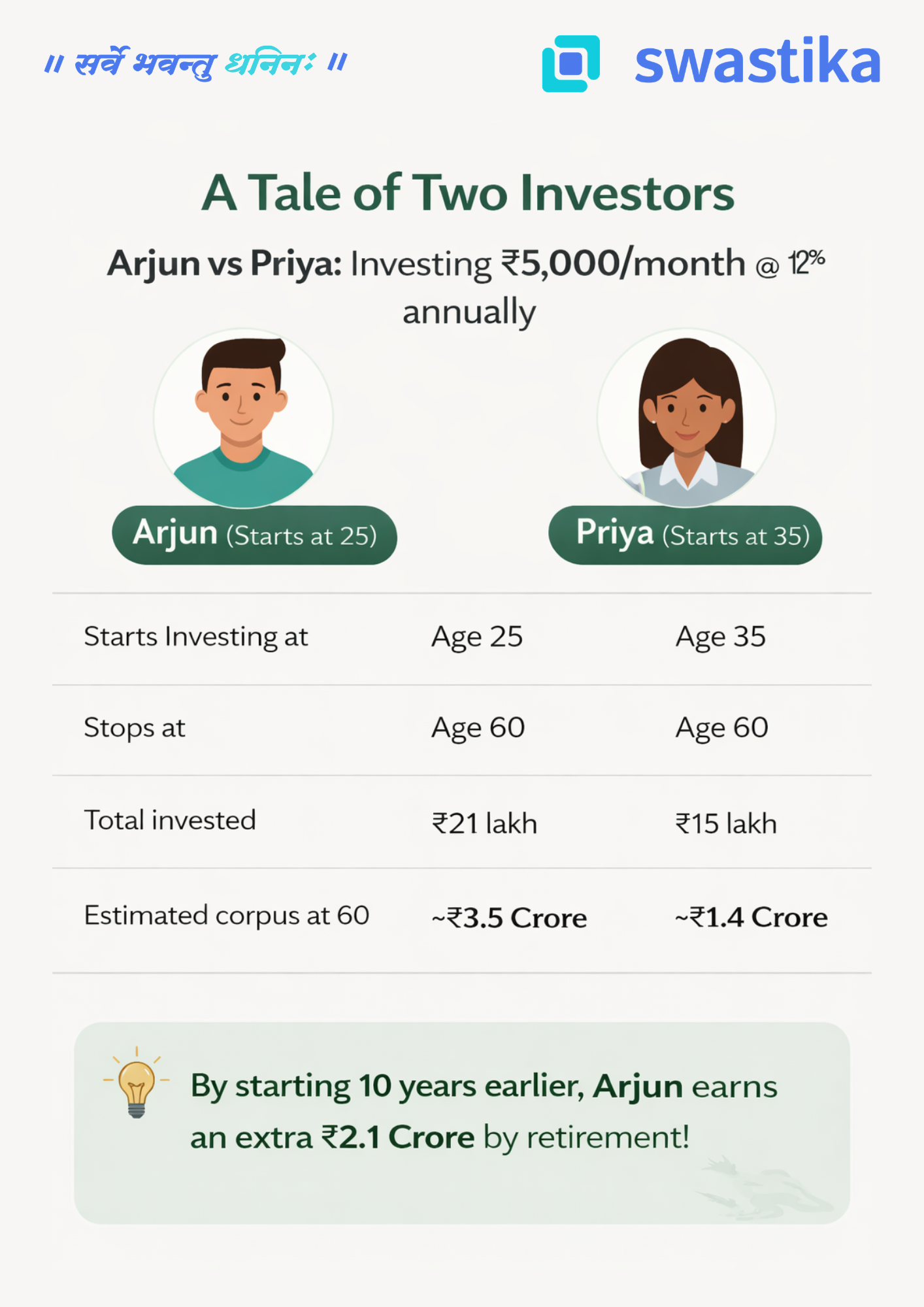

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

Start Up Funding & Indian Government Rules and Schemes for Sources of Funding

1. What is Startup Funding?

Startup Funding is an essential part of building a successful new business. It provides the necessary capital to develop and grow the business and can help turn a great idea into a profitable and sustainable company.

Startup funding is typically used to cover expenses such as product development, marketing, hiring, and office space. Depending on the stage of the business, the amount of funding needed can vary significantly.

2. Why Funding is required by Startups?

Startups require funding to turn their ideas into reality, attract and retain talent, market and sell their products, expand their business, cover operational costs, and compete with established players in their industry.

Funding is required by startups for several reasons:

- Product development: Startups often need funding to develop their product or service. This includes research and development, prototyping, testing, and manufacturing.

- Hiring: Startups need talented individuals to bring their ideas to life. Funding can be used to attract and hire the right people for the job.

- Marketing and sales: Once a product or service is developed, startups need to get the word out to potential customers. Funding can be used to launch marketing and advertising campaigns and to hire sales teams.

- Expansion: Startups that are successful need to expand in order to reach more customers and grow their business. This includes opening new locations, launching new products, and hiring more staff.

- Operations: Funding expenses such as rent, utilities, and supplies can be utilised to pay for ongoing operational costs.

- Competing with established players: Startups often face competition from established players in their industry. Funding can be used to develop a competitive advantage, such as building proprietary technology or developing a unique business model.

3. Stages of Startups and Source of Funding

Here are the common stages of startups and the corresponding sources of funding:

- Idea stage: This is the earliest stage of a startup, where the idea is still being developed and validated. At this stage, the founders typically rely on their own resources to fund the startup, such as savings or personal loans.

- Seed stage: This is the stage where the startup has a validated idea and is ready to build a prototype or minimum viable product (MVP). At this stage, the founders may seek seed funding from individual investors, angel investors, or seed-stage venture capital firms.

- Early stage: This is the stage where the startup has developed a product or service and is ready to launch and acquire customers. At this stage, the founders may seek funding from venture capital firms or early-stage investors.

- Growth stage: This is the stage where the startup has achieved product-market fit and is ready to scale. At this stage, the founders may seek funding from venture capital firms or growth-stage investors.

- Later stage: This is the stage where the startup has become a mature company with a proven business model and revenue streams. At this stage, the founders may seek funding from private equity firms, strategic investors, or even public markets through an initial public offering (IPO).

In addition to the sources of funding mentioned earlier, startups can also explore other financing options such as debt financing, lines of credit, and revenue-based financing. It's important for startups to choose the right source of funding that aligns with their growth stage and long-term goals.

Here are the steps to obtain startup funding in India:

- Develop a business plan: The first step is to develop a comprehensive business plan that outlines your startup's goals, products or services, target market, and financial projections. This will help you determine the amount of funding you need and the type of investors you should approach.

- Identify potential investors: There are several sources of startup funding in India, including angel investors, venture capitalists, incubators and accelerators, and government grants. Research and identify potential investors that align with your startup's industry and growth stage. For all the potential investors out there, we are here to provide you with a complete investment banking solution to satisfy all your needs.

- Prepare a pitch deck: A pitch deck is a presentation that outlines your startup's value proposition, market opportunity, and financial projections. It's important to prepare a well-crafted pitch deck that highlights your startup's strengths and potential for growth.

- Approach investors: Once you have identified potential investors and prepared a pitch deck, you can start approaching them with your funding proposal. This could involve networking events, pitch competitions, or direct outreach.

- Negotiate terms: If an investor is interested in your startup, you will need to negotiate the terms of the funding. This could include the amount of funding, equity stake, and any other conditions or requirements.

- Complete due diligence: Before finalizing the funding, the investor will conduct due diligence to verify your startup's claims and financial projections. It's important to be transparent and provide accurate information during this process.

- Finalize the funding: Once due diligence is complete and both parties agree on the terms, you can finalize the funding and receive the funds for your startup.

4. What do investors look for in startups?

Investors typically look for certain key factors when considering investing in startups. Here are some of the main things that investors look for:

- A strong and experienced management team with a clear vision for the company

- A unique business idea or technology with the potential for significant growth

- A large and growing market opportunity

- Evidence of market demand and customer traction, such as a proven customer base, sales, or partnerships

- A scalable business model that can generate significant revenue and profits

- A competitive advantage or barrier to entry that can protect the company's market position

- A clear path to profitability and a well-defined plan for achieving it

- Intellectual property protection, such as patents or trademarks, that can prevent competitors from copying the technology or idea

- A strong and well-developed business plan that includes financial projections, milestones, and goals

- A solid understanding of the regulatory environment and potential risks and challenges facing the company.

5. Why do investors invest in startups?

Here are some key points on why investors invest in startups:

- High potential for return on investment (ROI)

- Opportunity to get in on the ground floor of a promising new business

- Potential for significant company valuation increase

- Ability to secure a larger stake in the company at a lower valuation

- Chance to support innovation and entrepreneurship

- Opportunity to diversify the investment portfolio

- Access to new technologies and markets

- Chance to be part of a growing network of entrepreneurs and investors

- Possibility of participating in the growth and success of the company.

6. Government schemes for startups

There are several government schemes available for startups in India in 2023. Some of the well-known schemes are listed below:

1. Startup India: The Startup India scheme was started in 2016 with the aim of encouraging innovation and entrepreneurship in the country. It provides funding, mentorship, and other resources to startups to help in the growth of their businesses.

2. Atal Innovation Mission: The Atal Innovation Mission was started in 2016 with the goal of encouraging innovation and entrepreneurship among young people in India. Young entrepreneurs can find funding, mentorship, and other resources from that.

3. Pradhan Mantri Mudra Yojana: Pradhan Mantri Mudra Yojana was launched in 2015 to provide funding to small and micro enterprises in the country. It offers loans of up to Rs. 10 lakhs to support the establishment and growth of businesses.

4. MSME Sambandh Portal: The Ministry of Micro, Small, and Medium Enterprises has launched an online portal called MSME Sambandh, which aims to provide easy access to information about government schemes and services for MSMEs.

5. Credit Guarantee Fund Scheme for Micro and Small Enterprises: This scheme aims to provide collateral-free credit to MSMEs by guaranteeing loans provided by banks and financial institutions.

6. National Small Industries Corporation Subsidy: The National Small Industries Corporation provides various subsidies and schemes to MSMEs, including a marketing assistance scheme, a credit support scheme, and a raw material assistance scheme.

7. Technology Upgradation Fund Scheme: This scheme provides financial assistance to MSMEs for upgrading their technology and machinery.

10. National Manufacturing Competitiveness Programme: This programme aims to enhance the competitiveness of Indian manufacturing industries by providing funding and support for various activities, such as quality improvement, technology upgradation, and marketing.

11. Digital India: The Digital India initiative aims to transform India into a digitally empowered society and knowledge economy. It provides various schemes and initiatives to promote digital literacy, e-governance, and digital infrastructure development.

These are just a few of the government schemes available for startups in India. You can visit the Startup India website or speak to a business advisor to learn more about these schemes and how to apply for them.

7. Government startup rules

Government startup rules vary by country, but here are some common examples of regulations and policies that governments may implement to support and regulate startups:

- Business registration: Governments typically require startups to register their businesses and obtain necessary licenses and permits before operating. This ensures that startups comply with local laws and regulations.

- Tax incentives: Governments may offer tax incentives to encourage entrepreneurs to start businesses. This could include tax credits or deductions for research and development, hiring employees, or investing in certain industries. For more information, you can visit the income tax website.

- Access to funding: Governments may provide funding or support for startups through grants, loans, or venture capital programs. These programs may be targeted towards specific industries or technologies that the government wants to promote.

- Intellectual property protection: Governments may have laws and regulations to protect the intellectual property of startups, such as patents, trademarks, and copyrights. This can help startups protect their innovations and gain a competitive advantage in the market.

- Regulatory framework: Governments may establish regulations and standards to ensure the safety and quality of products and services offered by startups. This can help build consumer confidence and promote growth in the startup ecosystem.

- Public procurement: Governments may provide opportunities for startups to compete for government contracts and procurement opportunities. This can provide startups with a stable source of revenue and help them build their reputation and credibility in the market.

HOW TO CLAIM FOR GENERAL INSURANCE

Process of Claim Settlement

General insurance is a type of insurance that provides coverage for various risks and uncertainties that may occur in everyday life. It can include coverage for health, home, motor, travel, and other types of insurance policies. In the event of an unfortunate incident, it is important to know how to claim your insurance to get the coverage you deserve. In this blog, we will discuss the steps you need to follow to claim your general insurance policy.

Step 1: Intimation of Claim

The first step to claim your general insurance policy is to inform your insurance company about the incident immediately. This process is known as the intimation of a claim. You can do this by calling the toll-free number provided by the insurance company, sending an email, or visiting their website. Make sure you provide accurate details about the incident and your policy number. The insurance company will assign a claim number and a claims representative to assist you in the process.

Step 2: Documentation

Once you have informed the insurance company about the incident, you will need to submit the necessary documents to support your claim. The documents required may vary depending on the type of insurance policy you have and the incident you are claiming for. Below are the standard documents that may be required:

- Policy documents.

- Proof of incident, such as a police report, medical certificate, or accident report.

- Identity proof.

- KYC documents.

- Bills and receipts related to the incident.

- Any other documents that the insurance company may require.

- Make sure you submit all the necessary documents in a timely manner to avoid any delays in the claim process.

Step 3: Survey and Assessment

After receiving the claim intimation and necessary documents, the insurance company will assign a surveyor to assess the damage or loss. The surveyor will visit the location of the incident, examine the damage, and prepare a report. The surveyor's report is an important document as it helps the insurance company determine the extent of the damage and the compensation that needs to be paid.

Step 4: Settlement

Based on the surveyor's report and the documents submitted, the insurance company will process your claim and settle the amount due. The settlement may be made in the form of cashless settlement or reimbursement, depending on the terms and conditions of your policy.

Cashless Settlement:

In a cashless settlement, the insurance company directly pays the hospital or service provider for the expenses incurred by the policyholder. This option is available for health insurance policies and motor insurance policies.

Reimbursement:

In a reimbursement settlement, the policyholder pays the expenses incurred and then submits the bills and receipts to the insurance company for reimbursement. This option is available for most general insurance policies.

Step 5: Follow up

After submitting your claim, make sure to follow up with the insurance company regularly to get updates on the status of your claim. You can also check the status of your claim online through the insurance company's website. In case of any discrepancies or delays, you can contact the claims representative assigned to you for assistance.

Say hello to a new way of comparing insurance policies from various insurers across India! Compare and buy insurance products like Term Insurance, Health Insurance, General Insurance, and Investment Plans which are best for you with Hello Policy – Powered by Swastika Insurance Broking Services Limited (SIBSL), an IRDA-registered subsidiary company of Swastika Group.

बैंकिंग संकट के बढ़ते दबाव से सोने की कीमतों में तेजी

पिछले सप्ताह मौद्रिक नीति पर फेड के कम आक्रामक रहने से सोने की कीमतों में तेजी आई। ब्याज दर बढ़ोतरी की सीमित गुंजाइश की प्रत्याशा में, अमेरिका और यूरोप में हाल के बैंकिंग संकट ने कीमती धातुओं की मांग को बढ़ा दिया है, और डॉलर इंडेक्स को सात सप्ताह के निचले स्तर पर खींच लिया। फेड ने संकेत दिया कि वह आगे की आर्थिक प्रतिकूलताओं को रोकने के लिए अपनी तंग मौद्रिक नीति में नरमी पर विचार कर सकता है।

जबकि फेड ने उम्मीद के मुताबिक ब्याज दरों में बढ़ोतरी की और कहा कि यह मुद्रास्फीति को रोकने के लिए प्रतिबद्ध है, फेड की भाषा में बदलाव से बाजार को उम्मीद है की ब्याज दर बढ़ोतरी का पीक निकट है। डॉलर इंडेक्स में गिरावट रहने से सोने -चांदी के साथ अन्य कमोडिटी के भाव को भी फायदा मिल रहा है। फेड ने पिछले सप्ताह उम्मीद मुताबिक 0.25 प्रतिशत ब्याज दरें बढ़ाई है और अर्थव्यवस्था को नुकसान से बचाने के लिए लिए मौद्रिक नीति में नरमी रखने के संकेत दिए है। फेड ने अभी ब्याज दर कटौती से इंकार किया है। लगातार ब्याज दर वृद्धि होने के कारण अमेरिका के कुछ बैंक दिवालिया हो गए है और कई बैंको की वित्तीय हालत ख़राब होने से आगे ब्याज दरों में बढ़ोतरी बैंकिंग संकट को बढ़ा सकता है। वित्तीय संकट की सम्भावना के चलते निवेशकों में निवेश के लिए सुरक्षित आश्रय की मांग बढ़ी है जिससे सोने और चांदी की चमक लगातार बढ़ती दिख रही है। फेड के अतिरिक्त यूरोपियन सेंट्रल बैंक ने 0.5 प्रतिशत और बैंक ऑफ़ इंग्लैंड ने 0.25 प्रतिशत ब्याज दरों में बढ़ोतरी की है। हालांकि, पिछले सप्ताह प्रमुख बैंको की मौद्रिक नीति रहने के चलते सोने के भाव में उठा-पटक देखि गई और सप्ताह में सोना मामूली बढ़त दर्ज करते हुए 59500 रुपये प्रति दस ग्राम पर रहा, जबकि चांदी के भाव में 3 प्रतिशत की साप्ताहिक बढ़त दर्ज की गई है और इसके भाव 70400 रुपये प्रति किलो के स्तरों पर पहुंच गए है।

तकनिकी विश्लेषण:

इस सप्ताह कीमती धातुओं में तेज़ी रहने की सम्भावना है। सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 60000 रुपये पर है। चांदी में सपोर्ट 68000 रुपये पर है और रेजिस्टेंस 72000 रुपये पर है।

Understanding the Different Types of Investors in the Stock Market

Types of Investors in the Stock Market

Investing in the stock market can be a great way to grow your wealth and secure your financial future. But before you start investing, it's important to understand the different types of investors in the stock market. Knowing the different types of investors can help you make better investment decisions and achieve your financial goals.

Retail Investor:

Retail investors are individual investors who invest in the stock market. These investors typically invest smaller amounts of money Retail investors may invest through online trading platforms or through a dealer with a broker.

Institutional Investors:

Institutional investors are large organizations that invest in the stock market. These organizations include mutual funds, pension funds, insurance companies, pension funds etc. Institutional investors typically invest large sums of money and have professional investment managers who make investment decisions on behalf of the organization.

Hedge Fund Investors:

Hedge funds are pool funds of investors. These funds are managed by professional fund managers and they use risky management strategy for buying and selling securities. Investors who invest in hedge funds are called hedge fund investors.

Day Traders:

Day traders are investors who buy and sell stocks within the same trading day. Day traders typically use technical analysis and charting tools to identify short-term price movements in the market. Day traders may invest through online trading platforms or through a dealer with a stock broker.

Swing Traders:

Swing traders are investors who hold onto stocks for a few days to a few weeks. Swing traders typically use a combination of technical analysis and fundamental analysis to identify stocks with short-term price momentum. Swing traders may invest through online trading platforms or through a dealer with a stockbroker.

Index Fund Investors:

Index fund investors are investors who invest in index funds. Index funds are mutual funds or exchange-traded funds (ETFs) that track a specific market index, such as the S&P 500. Index fund investors typically invest in index funds to achieve diversification and to minimize their investment costs.

ESG Investors:

ESG investors are investors who invest in companies that prioritize environmental, social, and governance (ESG) factors. ESG investors typically use a combination of financial analysis and non-financial analysis to identify companies that are socially responsible and have a positive impact on the environment and society.

High Net Worth Individuals (HNIs):

High Net Worth Individuals (HNIs) are individuals with a significant amount of wealth, widely defined in India investible surplus of more than Rs.5 crores. HNIs are an important segment of investors in the financial market, and their investment decisions can have a significant impact on the market. HNIs have a wide range of investment options available to them, including stocks, bonds, real estate, alternative investments, and private equity.

Domestic Institutional Investors (DII):

Domestic Institutional Investors (DIIs) are institutional investors that operate within a country's borders and are involved in investing in financial markets. DIIs include entities such as mutual funds, insurance companies, pension funds, and banks. DIIs are important players in the Indian stock market and contribute significantly to the liquidity of the market. They are subject to regulations and guidelines set by regulatory bodies such as the Securities and Exchange Board of India (SEBI). DIIs play a vital role in providing stability to the market and creating a balance in the demand and supply of securities.

Foreign Institutional Investors (FIIs) or Foreign Portfolio Investors (FPI):

Foreign Institutional Investors (FIIs) or Foreign Portfolio Investors (FPI) are institutional investors from outside a country that invest in financial markets within that country. FIIs/FPIs include hedge funds, pension funds, sovereign wealth funds, and other institutional investors. They bring in foreign capital to the domestic market, which helps in boosting liquidity and improving the overall performance of the market. FIIs/FPIs are subject to regulatory guidelines set by the regulatory authorities of the country where they are investing. They play a crucial role in the growth and development of the domestic market by bringing in foreign investment and expertise.

Types of Investors Grouped by Investment Category

The first way to categorize investors is based on their investment category. There are three main categories of investors:

Equity Investors:

Equity investors buy shares in companies in the hope of earning a return on their investment through dividends or capital gains. They invest in stocks, which can be highly volatile but also have the potential for high returns over the long term.

Fixed Income Investors:

Fixed-income investors invest in debt securities such as bonds, which provide a steady income stream in the form of interest payments. Bonds are generally considered less risky than stocks, but they also offer lower returns.

Alternative Investors:

Alternative investors invest in assets that are not traditional stocks or bonds, such as real estate, commodities, or hedge funds. These investments can be highly specialized and often require a high degree of expertise to understand and evaluate. Alternative investments can offer diversification benefits and potentially higher returns, but they are also typically riskier than traditional investments.

Types of Investors Grouped on Basis of Their Investment Styles

Investors can also be grouped based on their investment style. There are three main investment styles:

Value Investors:

Value investors look for undervalued stocks that are trading below their intrinsic value. They seek out companies with strong fundamentals and a margin of safety, and they aim to buy stocks at a discount to their true value. Value investors tend to have a long-term investment horizon and are willing to hold stocks for years or even decades.

Growth Investors:

Growth investors focus on companies that are growing quickly and have high earnings potential. They seek out companies with strong growth prospects and are willing to pay a premium for these stocks. Growth investors tend to have a shorter investment horizon than value investors and are more focused on short-term earnings growth.

Passive Investors:

Passive investors take a more hands-off approach to investing and seek to match the performance of a broad market index, such as the S&P 500. They achieve this by investing in index funds or exchange-traded funds (ETFs) that track the performance of the index. Passive investors tend to have a lower risk tolerance and a longer investment horizon than active investors.

Types of Investors Based on Their Risk Appetite

Finally, investors can also be grouped based on their risk appetite. There are three main types of investors based on their risk tolerance:

Conservative Investors:

Conservative investors prioritize capital preservation over high returns. They are willing to accept lower returns in exchange for lower risk and are more likely to invest in fixed-income securities such as bonds. Conservative investors tend to have a shorter investment horizon and are more concerned with avoiding losses than maximizing gains.

Moderate Investors:

Moderate investors seek a balance between risk and return. They are willing to accept some degree of risk in exchange for the potential for higher returns, but they also prioritize capital preservation. Moderate investors tend to have a longer investment horizon than conservative investors and are more focused on building wealth over the long term.

Aggressive Investors:

Aggressive investors prioritize high returns over capital preservation. They are willing to take on higher levels of risk in exchange for the potential for higher returns and are more likely to invest in equities or alternative investments. Aggressive investors tend to have a longer investment horizon than moderate or conservative investors and are more focused on achieving their financial goals than on avoiding losses.

Conclusion:

There are many different types of investors in the stock market, each with their own investment strategies and goals. Whether you are a retail investor or an institutional investor, it's important to understand the different types of investors and to choose an investment strategy that aligns with your financial goals and risk tolerance.

ग्लोबल बैंकिंग संकट की आशंका से बढ़ी सेफ हैवन मांग

सोने और चांदी की कीमतों में पछले सप्ताह ग्लोबल बैंको में संकट बढ़ने के कारण, हैवन डिमांड देखि गई। एमसीएक्स में सोना पिछले सप्ताह 3.8 प्रतिशत तेज़ हो कर 58250 रुपये प्रति दस ग्राम के स्तरों पर रहा, जबकि चांदी वायदा सप्ताह में 7 प्रतिशत तेज़ हो कर 67200 रुपये प्रति किलो पर रहा। बैंकिंग संकट की आशंकाओं और मौद्रिक नीति पर अनिश्चितता ने कीमती धातुओं की सुरक्षित आश्रय अपील को बढ़ाया है। अमेरिका सिलिकॉन वैली बैंक दिवालिया होने के बाद स्विस बैंक क्रेडिट सुइस भी वित्तीय संकट का सामना कर रही है। हालांकि, क्रेडिट सुइस को मदद मिलने, और यूरोपियन सेंट्रल बैंक द्वारा ब्याज दरों में 0.5 प्रतिशत की बढ़ोतरी से कीमती धातुओं में पिछले सप्ताह के अंत मे मुनाफा वसूली रही। बैंकिंग संकट के चलते निवेशकों को उम्मीद है की फेड मौद्रिक नीति पर नरमी रखेगा। फेड के दर-वृद्धि चक्र में किसी भी रुकावट से सोने को फायदा होगा और डॉलर के मुकाबले सोने की मांग बढ़ेगी, और गैर-उपज वाली संपत्ति रखने की अवसर लागत भी कम रहेगी। बैंकिंग संकट और ब्याज दर बढ़ोतरी पर अनिश्चितता कीमती धातुओं को सपोर्ट कर रही है। हालांकि, मुद्रास्फीति स्थिर रहने के कारण फेड मौद्रिक नीति पर कठोर रह सकता है। मार्च में होने वाली फेड की बैठक पर निवेशकों की नज़रे रहेंगी जिसमे ब्याज दर बढ़ोतरी कितनी होगी, यह स्पष्ट नहीं हुआ है।

इस सप्ताह के आर्थिक आंकड़े कीमती धातुओं के लिए महत्वपूर्ण रहेंगे जिसमे फेड की बैठक, ब्रिटैन की मॉनेटरी पॉलिसी और यूरोप के मैन्युफैक्चरिंग आंकड़े शामिल है।

तकनिकी विश्लेषण:

इस सप्ताह कीमती धातुओं के भाव में अस्थिरता रहने की सम्भावना है। सोने में सपोर्ट 57000 रुपये पर है और रेजिस्टेंस 59000 रुपये पर है। चांदी में सपोर्ट 65400 रुपये पर है और रेजिस्टेंस 69000 रुपये पर है।

बुलियन, कमोडिटी, बेस मेटल्स, एग्रीकल्चरल कमोडिटीज से जुडी हुई एक्सपर्ट रेकमेंडेशन्स के लिए आज ही अपना फ्री डीमैट अकाउंट खोले

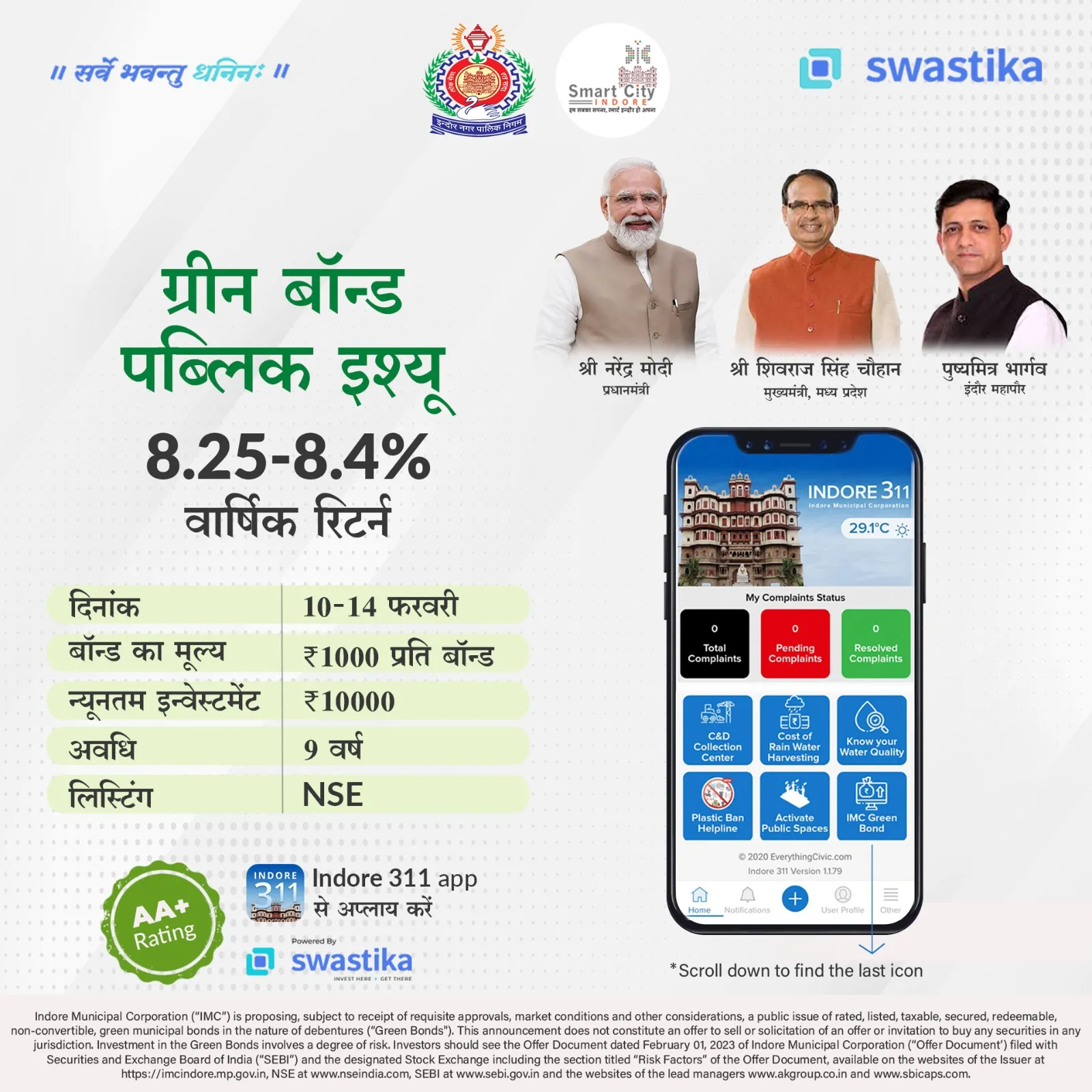

IMC Green Bond -All details here

The Indore Municipal Corporation (IMC) in Madhya Pradesh will issue green bonds as a public issue on February 10 to raise funds for building a solar power plant. This will be a first of its kind in India.

The green bond issue will open on February 10 and close on February 14. the bond is expected to list on the National Stock Exchange after February 22.

What is a Green Bond?

A green bond is a type of debt security that a company issues to finance or refinance projects that have a beneficial impact on the environment and the climate. A climate bond is another name for a green bond.

About IMC

The chief municipal corporation for the city of Indore is the Indore Municipal Corporation (IMC). The Commissioner (Nagar Aayukt) of the Issuer is Smt. Pratibha Pal, an IAS, and the Mayor are Shri Pushyamitra Bhargav. IMC is secured under the AMRUT Scheme of the Indian Government. Additionally, Indore Municipal Corporation owns 50% of Indore Smart City Development Limited (ISCDL), a Special Purpose Vehicle established under the Companies Act of 2013 to carry out Indore Municipal Corporation's Smart City Mission plan to build a smart city (SCM). ISCDL has contributed to the successful execution of a number of projects.

IMC Green Bond Details

According to DRHP, the corporation would issue four individually transferable and redeemable principal parts non-convertible debentures (NCDs) with a face value of Rs 1,000 each (STRPP). Each NCD of Rs 1,000 will include one STRPP A, one STRPP B, one STRPP C, and one STRPP D, each with a face value of Rs 250. The duration of STRPP A is 3 years, STRPP B is 5, STRPP C is 7, and STRPP D is 9 years.

The green bond issue would need a minimum application size of Rs 10,000 (or 10 NCDs), with subsequent applications coming in multiples of Rs 1,000.

India Ratings & Research gave the proposed green bonds an AA+ rating with a stable outlook. Care Ratings has given the issue an AA rating with a stable outlook, nonetheless.

According to the Income Tax Act of 1961, NCD holders are not entitled to any special tax benefits. If the NCD is held for less than 12 months the holder must pay short-term capital gains on interest income or for more than 12 months, the holder must pay long-term capital gains on interest income.

The book-running lead managers for the issue are AK Capital Services Limited, SBI Capital Markets Limited, and Vistra ITCL (India) Limited, while KFin Technologies is the registrar.

Objective

According to the source, the civic corporation of the nation's cleanest city hopes to raise at least Rs 245 crore through green bonds that will be utilized to build a 60 MW solar power at the villages of Samraj and Ashukhedi in the Madhya Pradesh district of Khargone and the electricity from it will be used to pump water to Indore from the Narmada river in Jalud village, which is located in the nearby Khargone district and is around 80 km distant.

The official projected that Rs 300 crore will be needed to build up the solar power facility.

A solar power plant building tender has already been announced, and once it is approved, construction will take two years, the municipality will save Rs 25 crore per month after the projected solar power facility at Jaludis constructed.

Financials of IMC Bond

The corporation's revenue income for the financial year 2021–2022 was Rs 1,739.95 crore as compared to Rs 1,508.10 crore in the same time the previous year.

While the corporation expenditure was Rs 1,107.88 crore in FY22, excluding interest and depreciation.

The total debt in 2021–22 was Rs 579.43 crore, down from Rs 648.45 crore in the same time the previous year.

Return & Ratings

The Green Bonds Issue offers an effective return of 8.42% annually and a coupon rate of 8.25% p.a. payable every six months. the NCDs are intended to be listed on both NSE and BSE. CARE Ratings Limited and India Ratings & Research Private Limited have rated the Green Bonds as "CARE AA: Stable" and "IND AA+/Stable," respectively.

To Invest in IMC green Bond Issue with the Swastika app or visit the link or apply through the Indore 311 App.

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App