Inside the IPO Filing Process from DRHP to Listing Day

An IPO is often perceived as a single event. In reality, it is a tightly regulated capital markets transaction that tests a company’s governance, financial maturity and disclosure standards. Long before the stock lists, months of preparation go into drafting, verification, regulatory review and investor positioning.

Why the Filing Process Matters

The offer document is the backbone of the IPO. For SEBI, it is a legal disclosure document. For investors, it is the primary source of truth.For the company, it becomes a permanent public record. Gaps in statutory disclosures or inconsistencies in financial reporting may result in approval delays and affect investor confidence.

Phase I: Pre IPO Preparation

The IPO process begins well before drafting the prospectus. At this stage, the company prepares itself to operate as a listed entity. Key actions include finalising the issue structure, converting into a public limited company, updating constitutional documents, strengthening board and committee structures, appointing key managerial personnel and dematerialising shareholding.

Phase II: Due Diligence and DRHP Preparation

This is the most intensive stage of the IPO journey. The Merchant Banker conducts detailed financial, legal and business due diligence, followed by preparation of the Draft Red Herring Prospectus covering company profile, industry overview, risks, financials and utilisation of proceeds.

Phase III: SEBI and Stock Exchange Review

SEBI, along with the stock exchanges, reviews the DRHP to ensurefull and fair disclosures, eligibility, and governance compliance. All queries and observations are addressed before final In-Principal approval.

Phase IV: Issue Management and Investor Outreach

Post regulatory clearances, the Red Herring Prospectus is finalised and the issue pricing is decided. Merchant Bankers, working closely with syndication and underwriting teams, drive investor outreach and roadshows, while market makersplay a role in supporting orderly trading and liquidity (in case of SME-IPO), in line with applicable issue regulations.

Phase V: Post Issue Formalities and Listing

After the issue closes, the basis of allotment is finalised, funds are reconciled by the banker to the issue, and shares are credited to investors’ demat accounts. In cases of oversubscription, allotment is carried out as per category-wise allocation norms, with proportionate or lottery-based distribution and refunds/unblock of excess application amounts. The company then lists on the stock exchanges and enters the post-listing compliance framework. Syndication and underwriting teams continue to support investor engagement, while issuer-led marketing and investor interactions remain ongoing. Anchor investors participate up to one working day prior to the issue opening, helping establish early demand visibility and confidence in the offering.

Role of the Merchant Banker

The Merchant Banker anchors the IPO end-to-end, beginning with comprehensive due diligence and preparation of offer documentation. They act as the primary interface with SEBI and Stock Exchanges, provide valuation and structuring advice, and lead investor marketing efforts. In coordination with syndication and underwriting teams, the merchant banker supports book building, demand aggregation, and risk underwriting. Post listing, they also facilitate market-making arrangements and ensure regulatory and compliance requirements are met, enabling a smooth transition from a privately held company to the public markets.

Closing Thoughts

The IPO process shows how ready a company is to operate in public markets. With the right Merchant Banker guiding the company at every stage, the journey becomes well-planned and manageable, helping the business move smoothly into the listed space and build long-term, sustainable growth.

👉 To Connect with us today, please click here.

Latest Articles

Brpl Share Price And Delhi Power Discom Audit: What The ₹38,500 Crore RA Means For Investors

Key Takeaways

- Delhi government directs a CAG audit of BRPL, BYPL, and TPDDL over ₹38,500 crore in pending regulatory assets.

- The RA composition is BRPL ₹19,174 crore, BYPL ₹12,333 crore, TPDDL ₹7,046 crore, totaling ₹38,553 crore.

- The audit will examine why tariffs stayed unchanged for more than a decade and who benefited.

- The outcome could influence the brpl share price and consumer tariffs while enhancing transparency.

Delhi's power-discom audit might seem like a bureaucratic story, but it has direct consequences for retail investors who watch the brpl share price. The Delhi government has directed the Comptroller and Auditor General (CAG) to audit three private distribution companies – BRPL, BYPL, and TPDDL – to investigate why nearly ₹38,500 crore in regulatory assets remain unrecovered. The aim is to determine how these regulatory assets accumulated and, crucially, who benefited from tariff decisions that left revenue gaps unaddressed for more than a decade. The audit's outcome could influence both policy and investor sentiment as regulators reassess recovery mechanisms and tariff design.

As a starting point, consider how the regulatory assets (RAs) are recovered. They are embedded in electricity bills as a surcharge designed to bridge gaps between the cost of supply and revenue recovered, a mechanism that has long supported the balance sheets of the private discoms but has also kept tariffs steady for years. The questions the CAG audit will address include: when did these RAs accumulate at the pace seen in BRPL, BYPL, and TPDDL, and what governance gaps allowed the increases to persist without timely recovery? The answers could influence not only policy formulations but also how investors price risk around these distributors. For deeper, stock-level insights on BRPL and the sector, explore Swastika's Sarthi AI stock assistant.

Brpl Share Price Context In Delhi Power Sector Audit

The investigation centers on how regulatory decisions translated into cost structures and consumer charges in Delhi’s energy market. Retail investors are watching whether the audit triggers policy tweaks that could alter the risk-reward calculus for BRPL, BYPL, and TPDDL. A transparent review of RA accruals may influence market sentiment around the brpl share price and related assets. The audit’s framework, aligned with a Supreme Court ruling and subsequent regulatory actions, signals a pivot toward stricter governance in tariff recovery and asset management. The net effect on brpl share price will hinge on how quickly recovered amounts affect future tariffs and cash flows for the discoms.

₹38,500 Crore Regulatory Asset: Composition And Implications

Discoms submitted RA figures to APTEL: BRPL ₹19,174 crore, BYPL ₹12,333 crore, TPDDL ₹7,046 crore. The total cum RA is ₹38,553 crore, described as around ₹38,500 crore in reporting. This composition matters because it frames what regulators might seek to recover through tariffs and surcharges, and how that recovery translates into future bill impacts. Tariffs remaining unchanged for more than a decade created the backdrop for this RA accumulation, underscoring the tension between keeping tariffs stable for consumers and ensuring full cost recovery for the utilities. Investors should note that the recovery mechanism–an RA surcharge embedded in electricity bills–directly feeds the discoms’ ability to cover past and future costs, which will influence earnings visibility and capital allocation decisions in the sector.

Timeline Of The CAG Audit: From January To June 2026

The audit process has a structured timeline. On January 20 (this year), the CAG granted in-principle approval to audit the accounts of BRPL, BYPL, and TPDDL, subject to authorization by the Lieutenant Governor under Section 20(1) of the CAG Act. June 6 saw notices issued to the discoms under Section 20(3) of the Act. Earlier in the year, APTEL dismissed DERC’s request for a CAG audit and directed liquidation of pending RAs within three weeks. On June 22, the Delhi High Court declined to interfere with the government’s CAG audit plan, deeming the petition premature. On June 29, the Delhi Cabinet approved a public-interest recommendation for a strict and intensive CAG audit, with the Power Department’s order receiving the Lieutenant Governor’s approval. The path was also shaped by a Supreme Court ruling on August 6, 2025, calling for a strict and comprehensive audit into how RA accumulation occurred without recovery. These steps collectively signal a deliberate, phased approach to scoping and authorizing the audit, which will influence governance and investor expectations around the sector’s regulatory risk profile.

Tariffs, Recovery Mechanism And Consumer Impact

Regulatory assets are recovered via a surcharge included in electricity bills, a mechanism that creates a direct link between past costs and current consumer charges. Tariffs remaining unchanged for more than a decade provided the space for RA build-up, and the audit now scrutinizes whether this approach balanced consumer protection with the utilities’ financial health. If the CAG identifies governance gaps or outdated accounting, policy implications could include revisiting the RA recovery framework, tariff revisions, or more stringent oversight. For retail investors, this means monitoring how regulators, policymakers, and discoms negotiate the balance between stable tariffs and timely cost recovery, which can alter earnings visibility and risk pricing in BRPL and its peers.

What The Delhi Cabinet, LG, And Supreme Court Rulings Mean For Investors

The sequence of regulatory and judicial steps provides a backdrop to the audit’s trajectory. The Supreme Court’s August 6, 2025 ruling called for a strict and comprehensive audit into how RA assets accumulated without proper recovery. APTEL’s April directive to liquidate pending RAs within three weeks, the Delhi High Court’s June 22 decision validating the audit plan, and the Cabinet’s June 29 approval–together with the Lieutenant Governor’s sign-off on the Power Department’s order–mark a strong administrative embrace of rigorous scrutiny. For investors, these steps translate into heightened clarity on governance and potential timing for any tariff or recovery decisions, which could influence market pricing of BRPL and related assets.

Historical And Legal Context: Privatization Since 2002 And The 2025 Supreme Court Ruling

Delhi’s discom landscape has been shaped by privatization since 2002, and this audit is the first CAG exercise of the privatized entities. An AAP-era attempt to audit in 2015 was blocked by the Delhi High Court, making the current sequence a notable shift toward accountability. The Supreme Court ruling in 2025, combined with the 2026 APTEL directive and the subsequent cabinet and LG approvals, reflects a broader move toward transparency and governance reforms in the power sector. For investors, this historical arc helps interpret how regulatory decisions translate into risk and rewards in BRPL and related securities in Delhi’s energy market.

Frequently Asked Questions

What is the total regulatory asset (RA) pending for BRPL, BYPL, and TPDDL?

Total RA is around ₹38,500 crore, with BRPL ₹19,174 crore, BYPL ₹12,333 crore, and TPDDL ₹7,046 crore, summing to ₹38,553 crore.

Which discoms are named in the CAG audit plan?

BRPL, BYPL, and TPDDL.

What is the purpose of the CAG audit?

To examine why BRPL, BYPL, and TPDDL have continued to carry regulatory assets without recovery.

When is the audit expected to be completed?

Ideally within three months of communication, with extensions possible depending on scope and complexity.

How are regulatory assets recovered?

RA are recovered via a regulatory assets surcharge included in electricity bills.

What precedents shaped the audit process?

The Supreme Court ruling of August 6, 2025 calling for a strict and comprehensive audit; APTEL's April directive to liquidate pending RAs within three weeks; Delhi High Court's June 22 decision; January 20, 2026 CAG in-principle approval; June 6 notices; June 29 Cabinet approval.

Conclusion

The Delhi CAG audit is more than a numbers exercise; it represents a governance moment that could reshape tariff recovery, regulatory risk, and investor confidence in Delhi’s power sector. The clarity around ₹38,500 crore of RA accumulation and the recovery path will influence policy discussions, tariff trajectories, and the way investors price risk for BRPL and other discoms. In the near term, the brpl share price will react primarily to how quickly the audit’s scope is defined, how swiftly recovery decisions are acted upon, and whether accompanying policy moves emerge to rebalance tariffs with cost recovery. Retail investors should stay attuned to official updates and the evolving regulatory narrative, as these signals often precede tangible shifts in risk premiums and stock performance.

Epfo Scheme Changes: A Retail Investor's Guide To Rs 1,800 Cap And Voluntary Top-Ups

Key Takeaways

- epfo scheme changes set a Rs 1,800 monthly cap on the statutory employee PF contribution.

- Contributions above the cap can be made voluntarily through the Voluntary Provident Fund (VPF).

- The change adds flexibility but requires planning to optimize your retirement corpus.

- For stock ideas aligned with these changes, explore Swastika's Sarthi AI stock assistant.

Retail investors across India should watch epfo scheme changes closely as the Rs 1,800 cap on the statutory provident fund contribution reshapes how your retirement corpus grows. In this guide, we break down what this means for your salary, your savings rate, and your overall financial plan.

Under the latest epfo scheme changes, the monthly employee contribution towards the Provident Fund is capped at Rs 1,800. Any amount you wish to save beyond this cap can be contributed voluntarily through the Voluntary Provident Fund (VPF) facility, subject to the prevailing EPFO rules. This dual-structure aims to protect lower-income savers while giving higher earners an optional lever to accelerate their retirement savings.

The change introduces a flexible framework that attempts to balance universal savings with individual capability. You may still owe a fixed statutory portion each month, but the slope of your savings for retirement can be steeper for those who can contribute more through VPF. The practical effect is that your PF corpus can reflect your personal discipline and cash flow more accurately than before.

The Rs 1,800 cap is the central element of epfo scheme changes. It defines the line between mandatory PF contributions and voluntary savings. In simple terms, you will see the mandatory employee contribution capped at Rs 1,800 per month. If you wish to save more into your PF, you can do so on a voluntary basis through the Voluntary Provident Fund (VPF). The VPF lets you increase your retirement corpus while maintaining the policy's risk controls and tax advantages, subject to your employer's payroll process and EPFO rules.

The government intends this structure to preserve universal savings while allowing higher earners to tailor their retirement contributions. For retail investors, this means your overall retirement savings mix can be shaped by your cash flow and long-term goals rather than being strictly bound by a fixed statutory rate.

Epfo Scheme Changes And The Rs 1,800 Cap: A Quick Primer

The Rs 1,800 cap forms the cornerstone of the new epfo scheme changes. It defines the line between mandatory PF contributions and voluntary savings. In simple terms, the mandatory employee contribution is capped at Rs 1,800 per month. If you wish to save more into your PF, you can do so on a voluntary basis through the Voluntary Provident Fund (VPF). The VPF lets you increase your retirement corpus while maintaining the policy's risk controls and tax advantages, subject to your employer's payroll process and EPFO rules.

The government intends this structure to preserve universal savings while allowing higher earners to tailor their retirement contributions. For retail investors, this means your overall retirement savings mix can be shaped by your cash flow and long-term goals rather than being strictly bound by a fixed statutory rate.

How The Rs 1,800 Cap Changes Your PF Strategy: Practical Implications

From an investment strategy perspective, epfo scheme changes offer a new dimension: the ability to top up beyond the cap via VPF. If your monthly cash flow allows, you can allocate additional savings toward VPF up to the allowed limit, which earns interest at the EPFO rate along with the regular PF. The incremental contributions compound over time, potentially boosting your retirement corpus. However, remember that EPFO's interest rate can vary; thus, the returns from VPF are not guaranteed in the same way as fixed-income products. Diversification remains essential: rely on PF for stable, risk-free accumulation and complement it with market-accessible savings or investments in mutual funds, index funds, and other tax-advantaged avenues where appropriate.

As you consider this, one practical move is to automate the process. Your payroll can usually handle automatic VPF contributions, ensuring you don't forget to top up each month. If you're aiming for a larger PF corpus, you might also pair VPF with additional tax-advantaged savings outside EPFO, such as mutual funds or PPF, depending on your tax planning. Always coordinate with your HR/payroll and tax adviser to ensure you stay compliant and optimize your net take-home pay.

Practical Steps To Align Your Finances With Epfo Scheme Changes

Here are concrete steps to adopt the epfo scheme changes in your financial plan:

- Assess your monthly cash flow and determine how much you can comfortably allocate to VPF beyond the Rs 1,800 cap.

- Consult your employer on how to set up automatic VPF contributions so you don’t forget to top up each month.

- Review your overall retirement strategy and diversify beyond EPF to include other suitable options like tax-saving mutual funds or direct equity exposure via a broad, low-cost index approach.

- Factor in tax considerations. While EPF contributions are tax-advantaged, the tax treatment for VPF contributions varies with regime changes over time, so consult a tax professional for current guidance.

- Use a structured mental model to compare the stability of EPF against the growth potential of other assets. For instance, view EPF as the anchor with the best-guaranteed returns in your portfolio, and other assets as growth engines to complement that anchor.

To refine your plan, you can rely on strategic tools and data-driven insights. Swastika's Sarthi AI stock assistant can help you evaluate stock-based opportunities that complement your PF strategy and ensure you stay within a disciplined risk framework. Swastika's Sarthi AI stock assistant is designed to provide institution-level research to retail investors, enabling you to align your equity choices with your savings goals.

Tax Considerations Under Epfo Scheme Changes

Tax implications surrounding EPF and VPF contributions are shaped by prevailing tax laws. In general, EPF contributions enjoy tax-advantaged treatment within the framework of Indian tax policy, and voluntary top-ups through VPF are often considered part of your overall Section 80C planning. However, the exact deduction limits and eligibility depend on the current tax regime and other 80C investments. Always consult a tax advisor to tailor this to your circumstances and to ensure you maximize after-tax savings.

Frequently Asked Questions

What are epfo scheme changes?

The latest EPFO guidelines introduce an Rs 1,800 monthly cap on the statutory employee PF contribution. Amounts beyond this cap can be contributed voluntarily through the Voluntary Provident Fund (VPF), subject to EPFO rules.

What is the Rs 1,800 cap on EPF contributions?

Under the updated rules, the statutory portion of the employee's PF contribution is capped at Rs 1,800 per month.

Can I contribute more than Rs 1,800 to EPF?

Yes. You can make voluntary top-ups through the Voluntary Provident Fund (VPF) mechanism.

How does this change affect retirement planning?

You gain flexibility: keep the statutory cap while increasing your retirement savings via VPF if you can afford it. It may improve your corpus, but returns will depend on the EPFO's interest rate and market performance.

Where can I get personalized investment insights?

For tailored stock ideas and financial planning, you can use Swastika's Sarthi AI stock assistant.

Conclusion

The epfo scheme changes set a new balance between mandatory savings and voluntary top-ups, offering a safety net for lower-income savers and a growth option for those who can contribute more. As a retail investor, treat EPF as the anchor of your retirement strategy–reliable and low risk–while actively building growth through diversified assets that fit your risk tolerance. Use this framework to design a savings plan that stays aligned with your cash flow and long-term goals.

Dollar To Rupee Exchange Rate Signals Rupee Strength As Softer Dollar Boosts Sentiment

Key Takeaways

- Rupee Opens At 95.21 Per U.S. Dollar, Up 18 Paise From Previous Close.

- Dollar Index Dips Below 101, Supporting The Rupee And EM Currencies.

- Firex Forecasts A 94.80–95.50 Range With A 95.00 Test In Play.

- Exporters May Cover July Dollars; Importers Could Use Any Easing To Meet Needs.

The dollar to rupee exchange rate has shifted in India's favor this morning as the rupee opened stronger against the U.S. dollar, marking an 18-paise gain from the previous close of 95.39. The currency opened at 95.21 per U.S. dollar, and broad weakness in the greenback supported this move. The soft U.S. labour data cooled expectations of aggressive tightening, lifting sentiment across emerging markets and giving the domestic market a fresh impetus to test higher levels after a three-session slide.

For Indian traders, this opening signals a potential shift in the near-term momentum. The dollar index dipped below the 101 mark, a pointer to softer dollar strength that can provide technical relief to the currency pair and the dollar to rupee exchange rate. As the session unfolds, market participants will watch whether the pair can sustain gains beyond the opening level and whether exporters who had delayed selling their dollar holdings begin covering positions for July, while importers could utilize any easing in the exchange rate to meet their dollar requirements. In this evolving backdrop, investors should balance currency cues with stock-specific risk and macro data to navigate the day.

Dollar To Rupee Exchange Rate Shifts As U.S. Dollar Weakens

The daily dynamic in the dollar to rupee exchange rate is driven by how aggressively the U.S. dollar is sought after and how much risk appetite the global market can tolerate. Softer U.S. labour data reduced expectations of near-term tightening by the Federal Reserve, a factor that supported Indian assets and helped the rupee find footing after weakness in the prior three trading sessions. In practical terms, the dollar to rupee exchange rate this morning suggests a potential shift in near-term momentum for local traders and for hedgers who cover currency exposures.

Traders will monitor the dollar to rupee exchange rate through the session for confirmation of a sustained move beyond the opening level, or a pullback if demand for the U.S. dollar strengthens again. The broader macro setup remains supportive of a softer dollar, with the dollar index hanging below the 101 mark, a sign that global liquidity conditions may support EM currencies including the rupee. Markets will also react to future U.S. data releases and external factors that can reassert dollar strength, potentially capping gains in the near term.

Rupee Opens At 95.21 Per U.S. Dollar And Gains 18 Paise

The rupee opened at 95.21 per U.S. dollar, an 18-paise improvement from the previous close of 95.39, marking a positive start after a softer session. The movement comes after the rupee's decline over the previous three trading sessions, as broad-based U.S. dollar weakness aided EM currencies. The intra-day range remains something to watch as the currency pair could trade within the 94.80–95.50 corridor, with a possible test of 95.00 if demand for the greenback remains contained.

Exporters who had delayed selling their dollar holdings may begin covering positions for July, and importers could utilize any easing in the exchange rate to meet their dollar requirements. The rupee's direction will likely stay linked to dollar demand, overseas capital flows and broader global sentiment through the trading session. This dynamic environment means an acknowledgement that a short-term dollar to rupee exchange rate move can be a catalyst for corporate hedges and dynamic trade decisions by domestic buyers and sellers. Traders are also watching how movements in major domestic stocks translate into broader market sentiment.

Exporters And Importers React To July Dollar Movements And Range Bound Outlook

With the 94.80–95.50 range in sight and the possibility of testing the 95.00 level, exporters who hold USD liabilities may cover; importers will watch the arrival of dollars to meet their obligations. The macro backdrop also has implications for corporate finance decisions, including capital management and hedging strategies. Retail investors may want to track the price action in major domestic equities as a pulse of risk appetite. The list includes reliance industries limited stock price, tata motors share price, state bank of india stock price, infosys stock price, hdfc bank stock price, and icici bank stock. While currency dynamics have a direct line to the currency pair, stock responses are often driven by sector catalysts, earnings, and macro data. Keeping an eye on these stock prices can provide insight into market breadth and risk sentiment as the rupee to dollar moves unfold, while Swastika's Sarthi AI stock assistant helps synthesize insights across stocks and indices in one place. Swastika's Sarthi AI stock assistant.

Asian Currencies Move In Mixed Direction As U.S. Data Eases Pressure On The Dollar

Among Asian currencies, the Malaysian ringgit led gains with an appreciation of 0.270%, while the Philippine peso advanced 0.202% and the Thai baht rose 0.178%. The Chinese renminbi, Singapore dollar and Taiwan dollar also posted modest gains during early trade. By contrast, the South Korean won declined 0.383%, marking the sharpest fall in the region, and the Indonesian rupiah slipped 0.239%. The Japanese yen edged 0.074% lower against the U.S. dollar. These moves illustrate the broad-based effect of a softer dollar on regional peers and highlight how global cross-currency flows can influence Indian markets and the dollar to rupee exchange rate path in the near term.

For India, the interplay between global dollar strength and local capital flows remains a central determinant of the dollar to rupee exchange rate path, especially as markets monitor upcoming U.S. economic data and the Fed policy trajectory. Traders often frame this as a balance between global liquidity and domestic fundamentals–a dynamic that can widen or compress trading ranges through July and into the monsoon season. The currency landscape remains sensitive to external shocks and domestic policy signals, meaning a disciplined approach to hedging and risk assessment is essential for investors who balance currency exposure with equity allocations.

Frequently Asked Questions

What is the opening rate for the rupee against the dollar today?

The rupee opened at 95.21 per U.S. dollar, up 18 paise from the previous close of 95.39.

What range does Firex expect for the currency pair today?

Firex expects the pair to trade in the 94.80 to 95.50 range, with a test around the 95.00 level if dollar demand remains contained.

Which Asian currencies moved with the rupee and by how much?

The Malaysian ringgit rose 0.270%, the Philippine peso advanced 0.202%, and the Thai baht rose 0.178%. The renminbi, Singapore dollar, and Taiwan dollar posted modest gains, while the South Korean won fell 0.383%, the Indonesian rupiah slipped 0.239%, and the Japanese yen dropped 0.074% against the U.S. dollar.

What actions might exporters and importers take in July?

Exporters who had delayed selling their dollar holdings may begin covering positions for July, while importers could use any easing in the exchange rate to meet their dollar needs.

What should retail investors watch regarding the dollar to rupee exchange rate?

Retail investors should monitor dollar demand, overseas capital flows, and broader global sentiment, as these influence the dollar to rupee exchange rate and the rupee's near-term trajectory.

Conclusion

The rupee's reaction to the softer U.S. dollar data underlines the central pivot in the currency story: the dollar to rupee exchange rate is a barometer of India's macro momentum, global liquidity conditions, and domestic capital flows. The opening rate of 95.21 per U.S. dollar and an 18-paise gain against the prior close of 95.39 signals a potential near-term shift in momentum, though the future path will remain contingent on U.S. data releases and overseas capital dynamics. For retail investors, the near-term takeaway is simple: monitor the 95.00 level and the 94.80-95.50 corridor, maintain awareness of USD demand, and consider hedging exposures if risk tolerance or portfolio composition warrants it. The broader message is that a measured approach–balancing currency signals with stock-specific analysis–can help you navigate volatility and capture opportunities as markets respond to evolving macro cues.

Visl Share Price Rally: What The Post-Listing Move Means For Retail Investors

Key Takeaways

- visl share price surged about 93.9% from ₹20 listing price to ₹38.78 on NSE, with the stock locking in the 10% upper circuit.

- The rally followed Vedanta's demerger of four entities, and VISL said there was no undisclosed material information behind the move.

- visl stock is an integrated iron ore mining, processing and steel manufacturing business with operations in India and Africa, including a Bokaro plant with 1.5 MTPA capacity.

- Regulators sought clarifications after market hours on June 30, 2026, and VISL affirmed compliance with SEBI rules and disclosures.

From ₹20 on 15 June 2026 to an intraday high of ₹38.78 on 1 July 2026, visl share price drew attention from retail investors. The visl share price momentum reflects more than headlines; it hints at the evolving post-demerger strategy for VISL as a standalone steel and mining player operating in India and Africa. This article unpacks the drivers behind the movement, the core business, and practical takeaways for investors navigating this dynamic sector.

Visl Share Price Momentum: What Drove The 93.9% Rally Since Listing

The visl share price momentum from ₹20 at listing (June 15, 2026) to ₹38.78 at the intraday high on July 1, 2026 represents a gain of about 93.9% based on the listing price. On that same date, the stock was locked in the 10% upper circuit on NSE, underscoring the strength and volatility of the early post-listing phase. The demerger into four Vedanta entities, including Vedanta Iron and Steel, contributed to a window of trading interest as investors priced future prospects around standalone VISL operations rather than the collectively diversified Vedanta group.

Visl Stock Dynamics: Understanding The Business Behind The Rally

visl stock operates as an integrated iron ore mining, processing and steel manufacturing company with operations across India and Africa. Its Bokaro plant in Jharkhand state (a greenfield project) has a capacity of 1.5 MTPA via ESL Steel Ltd. The Bokaro facility, established in 2006 and later acquired by Vedanta in 2018, sits at the heart of VISL's production capacity. The product portfolio spans steel, wire rods, TMT bars, pig iron, ductile iron pipes, ferro-silicon, cement and metallurgical coke, illustrating a diversified line-up that can cushion some volatility in steel prices. The VISL narrative is anchored in Vedanta's broader strategy to create standalone steel and metals assets that can be optimally leveraged in India and selected African markets.

Demerger Context And Regulatory Disclosures: How It Impacts Valuation

As part of the Vedanta demerger, four entities–Vedanta Power, Vedanta Aluminium, Vedanta Oil and Gas, and Vedanta Iron and Steel–completed a mandatory 10-day Trade-to-Trade (T2T) settlement period and exited the relevant segment on 30 June 2026. After market hours on that same date, regulatory authorities issued clarification requests on the significant price movement. VISL subsequently stated that it had made all disclosures required under the SEBI Listing Obligations and Disclosure Requirements Regulations, 2015 and that it was not aware of any material information that would explain the rally.

Historical Milestones And Certifications: Why ISO 14001 Matters

visl stock's legacy runs deep in Indian iron ore mining and steel production. The mining lineage dates back to 1954 in Goa, with expansions into Karnataka and Odisha and diversification into pig iron and metallurgical coke in the early 1990s. In 1997, VISL achieved ISO 14001 environmental management certification, becoming the first iron ore mining company in India to obtain this standard. The Bokaro plant, together with ESL Steel's integrated network, reinforces VISL's capacity to produce a broad steel product mix across multiple geographies.

What Retail Investors Should Watch Next: Risks, Disclosures, And Decision Guidelines

Even as the visl share price has surged, retail investors should anchor their decisions on fundamentals. The company has emphasized compliance disclosures and indicated an absence of undisclosed material information driving the rally. It is essential to monitor quarterly production data, capex plans for Bokaro and other mining sites, and regulatory filings for any new material disclosures. Given the nature of demerger-driven price action, a disciplined approach–factoring in valuation benchmarks, balance-sheet strength, and commodity cycles–helps avoid overpaying in the chase for momentum. For deeper insights, you can consult Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What caused the visl share price surge after listing?

The visl share price rose from ₹20 at listing on June 15, 2026, to ₹38.78 on NSE by July 1, 2026, a gain of about 93.9%, with the stock locking in the 10% upper circuit.

What is VISL's business and where does it operate?

VISL is an integrated iron ore mining, processing and steel manufacturing company with operations in India and Africa, including a Bokaro plant with 1.5 MTPA capacity.

What was the demerger context for VISL?

As part of Vedanta's demerger, four entities—Vedanta Power, Vedanta Aluminium, Vedanta Oil and Gas, and Vedanta Iron and Steel—completed a mandatory 10-day Trade-to-Trade settlement and exited the segment on 30 June 2026.

Has VISL disclosed any undisclosed material information related to the rally?

VISL stated that there was no undisclosed material information behind the price movement and that it has complied with SEBI Listing Obligations and Disclosure Requirements Regulations, 2015.

What are VISL's milestones and certifications?

Mining operations date back to 1954 in Goa; VISL expanded to Karnataka and Odisha, diversified into pig iron and metallurgical coke in the early 1990s, and achieved ISO 14001 environmental management certification in 1997.

Where can I get more in-depth stock analysis for VISL?

For deeper insights, you can use Swastika's Sarthi AI stock assistant: https://www.swastika.co.in/sarthi

Conclusion

The VISL story shows how a post-listing event paired with a company-specific expansion path can create rapid price action. For retail investors, the prudent response is to balance momentum with a sober assessment of VISL's long-term capacity and regulatory posture, focusing on production metrics, asset utilization, and cost structure rather than headlines alone.

.jpg)

Coca-Cola IPO is Coming? What Investors Need to Know

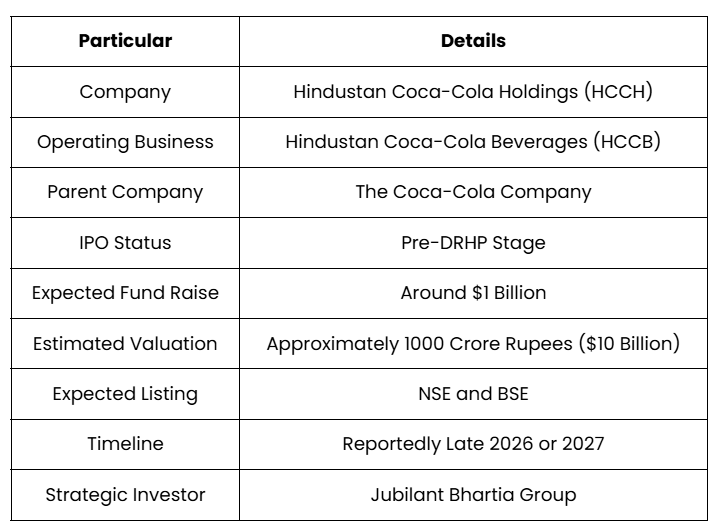

If you've ever wanted to invest in Coca-Cola's India business, you may soon have that opportunity. Reports suggest that Hindustan Coca-Cola Holdings (HCCH), the parent company of Hindustan Coca-Cola Beverages (HCCB), is preparing for a public listing that could raise around $1 billion (approximately ₹9,000 to ₹9,500 crore).

However, here's the most important point investors should know. The IPO has not yet been officially announced. HCCB is still in the pre-DRHP stage, which means the company is yet to file its Draft Red Herring Prospectus (DRHP) with the Securities and Exchange Board of India (SEBI). Until then, the issue size, valuation, timeline, and price band remain subject to change.

Despite this, the proposed IPO has generated significant interest because it could become one of India's largest consumer sector listings and provide investors with exposure to Coca-Cola's Indian bottling business for the first time.

This guide answers the questions investors are actively searching for, explains how HCCB operates, analyses why Coca-Cola is considering the IPO, discusses the opportunities and risks, and highlights the factors investors should monitor before making an investment decision.

HCCB IPO Highlights at a Glance

Before exploring the business in detail, here's a quick overview of what is currently known about the proposed IPO.

The above details are based on publicly available reports and may change once the company files its DRHP.

Can You Invest in Coca-Cola India Right Now?

No. Retail investors cannot invest in HCCB yet because the company is still unlisted. Although reports indicate that Coca-Cola is preparing to list its Indian bottling business, the IPO process has not officially begun. Investors will only be able to apply once the company files its DRHP, receives regulatory approvals, and announces the IPO dates.

Until then, investors should treat the current information as preliminary and continue tracking official announcements.

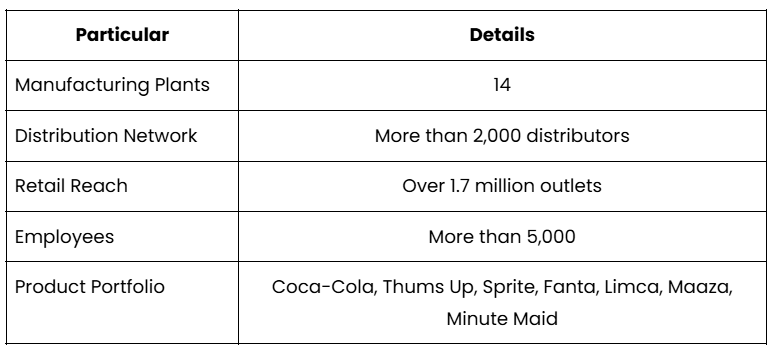

What is HCCB?

HCCB is Coca-Cola's principal bottling and distribution company in India. While most consumers associate Coca-Cola with brands such as Coca-Cola, Thums Up, Sprite, Fanta, Limca, Maaza, and Minute Maid, HCCB is the company responsible for manufacturing, bottling, and delivering many of these beverages to retailers across India.

Unlike The Coca-Cola Company, which owns the global brands and develops beverage concentrates, HCCB operates the manufacturing plants, manages logistics, and supplies products to millions of retail outlets.

The following table provides an overview of HCCB's operational scale. The scale of these operations makes HCCB one of India's largest beverage bottling companies.

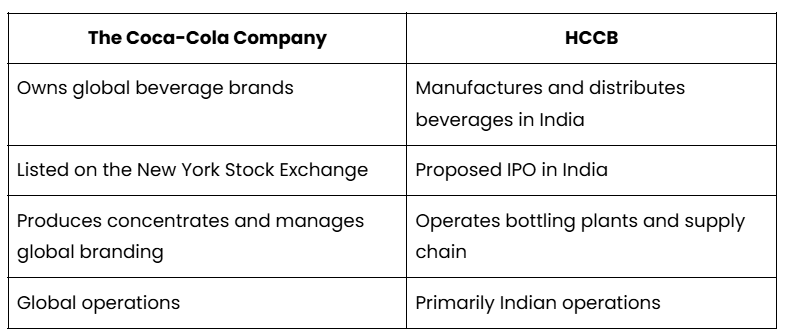

Is HCCB the Same as The Coca-Cola Company?

No. HCCB and The Coca-Cola Company are two different businesses with different roles. Many investors assume they would be investing directly in Coca-Cola's global business. That is not the case. The following comparison explains the difference.

This distinction is important because HCCB's financial performance depends on manufacturing efficiency, distribution strength, and domestic beverage demand rather than Coca-Cola's worldwide earnings.

Does HCCB's IPO Affect Coca-Cola Share Price?

No, the proposed HCCB IPO is unlikely to directly impact the Coca-Cola share price in the United States. The Coca-Cola share price reflects the financial performance of The Coca-Cola Company, which owns the global beverage brands and operates in multiple countries.

The proposed HCCB listing represents only the Indian bottling business. Although a successful listing may highlight the strength of Coca-Cola's operations in India, the global stock price will continue to be influenced by worldwide revenue, profitability, and broader market conditions.

What is Coca-Cola's Market Cap and Why Does It Matter?

The Coca-Cola Company has a market capitalisation of approximately $350 billion, making it one of the world's largest publicly listed beverage companies. Market capitalisation, or market cap, represents the total market value of a company's outstanding shares and is often used by investors to assess its size and overall market value.

However, investors should understand that the Coca-Cola market cap represents the global parent company listed in the United States and should not be confused with the proposed valuation of HCCB in India.

Media reports suggest the Indian bottling business could be valued at approximately $10 billion, which is significantly smaller than the market capitalisation of The Coca-Cola Company.

Why is Coca-Cola Planning This IPO?

The proposed IPO is part of Coca-Cola's long-term global strategy to become a more asset-light business. Over the years, Coca-Cola has shifted away from directly owning manufacturing facilities. Instead, it has focused on brand building, marketing, product innovation, and concentrate production while allowing bottling businesses to operate independently.

India is now following the same strategy. The transformation has taken place in three major stages.

First, Jubilant Bhartia Group acquired a 40% stake in HCCH in 2025.

Second, Coca-Cola transferred several manufacturing plants to franchise bottlers across different states.

Finally, the company is preparing to list its Indian bottling business on the stock market.

This strategy allows Coca-Cola to unlock value while reducing the capital required to operate manufacturing facilities.

Why is This IPO Important for Investors?

The proposed HCCB IPO could provide investors with direct exposure to India's growing beverage consumption story. India remains one of Coca-Cola's fastest-growing markets, supported by increasing disposable incomes, urbanisation, organised retail expansion, and rising demand for branded beverages.

If listed, HCCB would become one of the country's largest beverage manufacturing companies available for public investment. For investors seeking exposure to India's consumer sector, the IPO could become an attractive opportunity, subject to valuation and financial performance.

How Strong is HCCB's Business?

HCCB operates one of India's largest beverage manufacturing and distribution networks. Its extensive retail presence, diversified beverage portfolio, and established supply chain provide significant operational advantages.

At the same time, the company benefits from globally recognised brands that enjoy strong consumer demand across urban and rural markets. These factors contribute to stable business fundamentals, although profitability will depend on execution, cost management, and competitive intensity.

According to Shyam Bhartia and Hari Bhartia, Chairman and Co-Chairman of the Jubilant Bhartia Group, the acquisition of a 40% stake in Hindustan Coca-Cola Holdings (HCCH) aligns with their long-term value creation strategy. They expressed enthusiasm about the partnership, stating that the move would help "reap the benefits of the public listing to create value for all shareholders," reflecting their confidence in the company's growth prospects and the potential value that a future IPO could unlock.

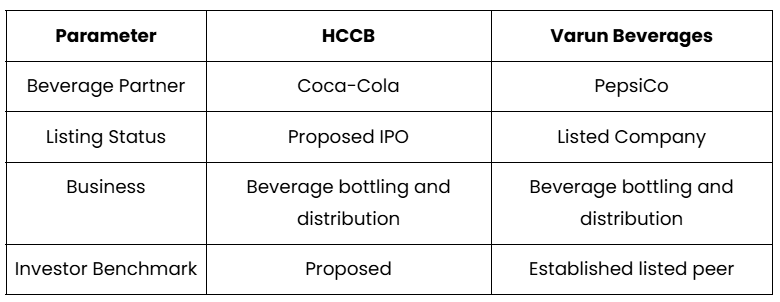

Can HCCB Become the Next Varun Beverages?

Possibly, but investors should compare financial performance rather than brand names. Whenever HCCB enters the stock market, comparisons with Varun Beverages Limited (VBL) are inevitable.

Just as Varun Beverages bottles PepsiCo products in India and several international markets, HCCB manages Coca-Cola's bottling operations across a significant part of India. The following comparison provides a broad overview.

Investors are likely to compare revenue growth, EBITDA margins, return ratios, debt levels, and valuation before deciding whether HCCB deserves a premium valuation.

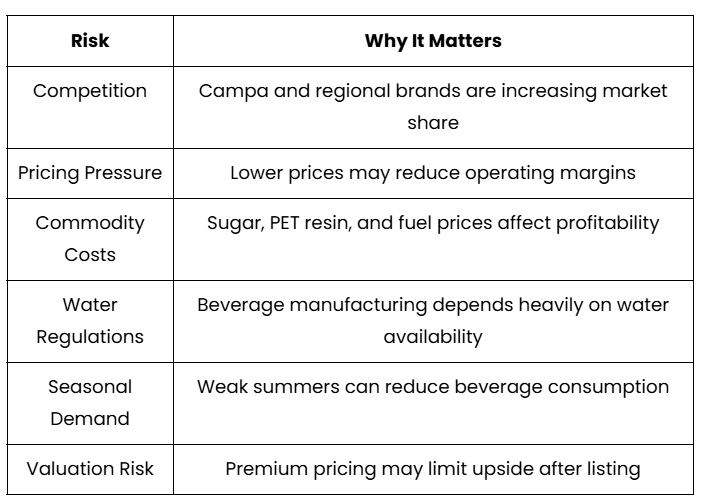

What Risks Should Investors Consider?

Strong brands alone do not eliminate business risks. Although HCCB benefits from Coca-Cola's global brand portfolio, investors should evaluate the challenges that could affect future performance. The following table summarises the major risks.

Understanding these risks is essential because they can influence long-term earnings and shareholder returns.

What Should Investors Watch Before the IPO Opens?

The DRHP will be the most important document for evaluating HCCB. Before making any investment decision, investors should focus on the following disclosures once the company files its DRHP.

- Revenue and profit growth

- EBITDA margins

- Return on Equity and Return on Capital Employed

- Debt levels

- Capital expenditure plans

- Objects of the issue

- Valuation

- Promoter shareholding

- Risk factors

- Dividend policy

These details will provide a much clearer picture of the company's financial strength and growth potential.

Should You Track the HCCB IPO?

Yes, but invest based on fundamentals rather than the Coca-Cola brand name. The proposed HCCB IPO has the potential to become one of India's largest consumer sector listings. The company benefits from a strong distribution network, an established portfolio of leading beverage brands, and long-term demand driven by India's growing consumption economy.

However, investors should avoid making investment decisions solely because of the Coca-Cola brand. The final investment case will depend on financial performance, profitability, competitive positioning, IPO valuation, and management's future growth strategy.

Once the DRHP is released, investors will have sufficient information to evaluate whether the IPO offers attractive long-term investment potential.

For the latest IPO updates, detailed company analysis, and expert insights, stay connected with Swastika Investmart to make informed investment decisions.

Frequently Asked Questions (FAQs)

Can I invest in Coca-Cola India right now?

No. HCCB is not yet listed on Indian stock exchanges. Investors will only be able to apply after the company files its DRHP with SEBI and officially launches the IPO.

Is HCCB the same as The Coca-Cola Company?

No. HCCB is Coca-Cola's Indian bottling and distribution business, while The Coca-Cola Company owns the global beverage brands and is listed on the New York Stock Exchange.

Why is Coca-Cola bringing HCCB to the stock market?

The proposed IPO is part of Coca-Cola's asset-light strategy. Listing the bottling business allows the company to unlock value while focusing on brand development and concentrate production.

When is the HCCB IPO expected?

Media reports suggest the IPO could be launched in late 2026 or 2027. However, no official timeline has been announced because the company has not yet filed its DRHP.

Is HCCB a good investment?

It is too early to determine. Investors should wait for the DRHP to review the company's financial performance, valuation, business risks, and use of IPO proceeds before making an investment decision.

Who are HCCB's biggest competitors?

Varun Beverages, Campa, and several regional beverage brands are among HCCB's major competitors. Competition in India's beverage market has increased significantly in recent years.

What makes HCCB different from Varun Beverages?

Both companies operate beverage bottling businesses, but they partner with different global brands. HCCB bottles Coca-Cola products, while Varun Beverages bottles PepsiCo products.

What is the biggest factor investors should watch?

The DRHP is the single most important document to monitor. It will disclose financial statements, valuation, risk factors, IPO structure, and the intended use of funds, helping investors make an informed decision.

Are Coca-Cola Shares Available in India?

No, Coca-Cola shares listed on Indian stock exchanges are not available at present. While many investors search for Coca-Cola shares or the Coca-Cola share price, these refer to The Coca-Cola Company, which is listed on the New York Stock Exchange (NYSE) under the ticker symbol KO.

Asian Paints Share Price Signals A Sector Turnaround For Retail Investors

Key Takeaways

- Paint stocks have tumbled up to 48% from their peaks, driven by margin pressure and raw-material costs.

- Asian Paints share price remains the sector bellwether, down about 10% from its 52-week high of Rs 2,985 (current around Rs 2,715).

- ICICI Securities expects FY27 Q1 revenue growth above 15%, with margins under pressure but improving in Q2.

- Price cuts are likely only after a commodity downcycle, with 3-4 months lag and selective marketing spend to protect margins.

Asian Paints Share Price And Sector Margin Dynamics In FY27

The paint sector faced a tough year as margins contracted under the weight of higher raw-material costs, currency headwinds and supply disruptions from geopolitical tensions. Asian Paints, the sector’s largest listed company by market value, has seen its price correct about 10% from its 52‑week high of Rs 2,985, touched in December 2025; the current price sits near Rs 2,715. The market value for Asian Paints is around Rs 2.60 lakh crore, highlighting its dominance even as the broader sector retrenches.

Shalimar Paints, by contrast, has plummeted nearly 48% from its peak, and its market capitalisation is around Rs 440 crore. Berger Paints, the second-largest listed player by market value, is down about 15% from its annual high. Indigo Paints, Kansai Nerolac, and JSW Dulux have corrected roughly 20% from their respective peaks.

The sector has been navigating a complex mix of headwinds. Paint manufacturers raised prices by 14–16% between March and June 2026 after a sharp surge in crude-linked raw material costs, depreciation in the Indian rupee, and supply disruptions triggered by the Middle East conflict. Since the de-escalation of geopolitical tensions, crude oil prices have corrected sharply–from nearly $120 per barrel in May to below $75 per barrel in June. At the same time, the rupee has strengthened.

How will prices move going forward? ICICI Securities notes that history suggests paint companies pass on a portion of lower input costs to consumers–but not immediately. Three trends persist from previous commodity downcycles: price cuts tend to occur 3–4 months after commodity prices decline, companies pass on less than half of the earlier hikes, and instead channel savings into dealer incentives, influencer marketing, and trade schemes to defend market share. The brokerage expects a similar pattern in FY27, with meaningful price cuts likely after the Diwali season and extra emphasis on trade spend in the July–September quarter.

Margins may improve before price cuts kick in, with sector revenue growth anticipated to be healthy. ICICI Securities expects Q1FY27 revenue growth to exceed 15%, though margins could stay under pressure because raw-material costs stayed elevated for much of the quarter and price hikes were implemented gradually. In Q2FY27, revenue growth could outpace margin expansion as the benefits of higher prices and lower input costs start to flow through; in the second half of FY27, gradual price reductions could weigh on realizations and margins. Dealers are expected to reduce inventory ahead of any potential price reductions.

Brokerage house consensus remains bullish: Asian Paints with a target price of Rs 3,050; Berger Paints with a target price of Rs 550; Kansai Nerolac with a target price of Rs 230; JSW Dulux with a target price of Rs 3,350; Indigo Paints with a Buy rating and a target of Rs 1,200.

For deeper stock-level insights, explore Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Raw Material Costs And Currency Movements: How They Shape The Paint Realisations

The March–June 2026 period saw price hikes in the range of 14–16% as input costs rose sharply on crude-linked materials, rupee depreciation, and Middle East disruptions, forcing producers to tweak production schedules and trim trade discounts. The consequence was a temporary improvement in product realisations across the sector, even as margins remained under pressure due to the time-lag before input-cost relief fully translated into lower prices for end-consumers.

With crude slipping from around $120/bbl to sub-$75/bbl and the rupee strengthening, the industry is watching to see how quickly input costs recede and how aggressively companies pass on any savings. In practice, history shows that price cuts arrive after a lag and that the market will favor selective price adjustments supported by promotional activity and dealer incentives to defend market share.

Price Cuts On The Horizon: Timing And The Industry Playbook

Analysts expect paint companies to delay meaningful price reductions until after the Diwali season, mirroring patterns observed in past commodity downcycles. The emphasis is likely to shift toward trade promotions, dealer incentives, and marketing spend rather than aggressive price cuts in the near term. In the meantime, companies may use the savings to bolster distribution strength and expand their share of shelf space, even as realisations are gradually helped by lower raw-material costs.

Stock-Specific Trajectories: Berger Paints Stock Price, Shalimar Paints Stock Price, Asian Paints Stock Price, Kansai Nerolac Stock, Indigo Paints Stock

Among the big names, Shalimar paints stock price has seen a sharper correction–about 48% from its peak–reflecting the challenges faced by smaller players. Berger paints stock price has declined around 15% from its annual high, while Indigo paints stock has corrected roughly 20% from their peaks. Kansai Nerolac stock has also corrected around 20%, and Asian paints stock price has eased about 10% from its 52-week high of Rs 2,985 (December 2025), now trading near Rs 2,715. The overall sector remains sensitive to raw-material costs, currency swings, and supply-chain dynamics, which directly impact pricing, margins, and market share.

Frequently Asked Questions

What caused the paint sector to tumble in 2026?

Rising crude-linked raw material costs, depreciation in the Indian rupee, and supply disruptions from geopolitical tensions pressured margins, while price hikes in 14–16% during March–June 2026 supported realizations.

How has Asian Paints share price moved relative to its 52-week high?

Asian Paints is down about 10% from its 52-week high of Rs 2,985, reached in December 2025; the current price is around Rs 2,715.

When are paint companies likely to implement price cuts?

Historically, price cuts occur about 3–4 months after commodity prices decline, and companies tend to pass on less than half of earlier hikes, while using savings for promotions and dealer incentives.

What is the expected revenue growth for Q1FY27 in the paint sector?

ICICI Securities expects sector revenue growth of over 15% in Q1FY27, with margins likely under pressure but set to improve in Q2FY27.

Which stocks had notable price declines, and by how much?

Shalimar paints stock price fell about 48% from its peak; Berger paints stock price declined around 15%; Indigo paints stock and Kansai Nerolac stock have fallen about 20% from their peaks; Asian paints stock price fell about 10% from its 52-week high.

What are the broker target prices for major paint stocks?

Targets include Asian Paints at Rs 3,050, Berger at Rs 550, Kansai Nerolac at Rs 230, JSW Dulux at Rs 3,350, and Indigo Paints at Rs 1,200.

Conclusion

What this means for the retail investor is to focus on timing and price trajectory rather than just absolute stock moves. The paint sector is likely to see a gradual margin upturn and a more favorable realisation cycle as input costs ease, but price cuts will come with a lag and will be focused on sustaining market share. Your next step could be to monitor the asian paints share price alongside macro signals, and consider a staged entry strategy aligned to the expected Diwali-season price adjustments.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App