Gold Price Today Across Indian Markets: City-Wise Trends And Practical Investor Takeaways

Key Takeaways

- Gold price today shows volatility with 24K rates around 14,300 per gram in Bengaluru on July 16.

- June lows near 12,860 per gram for 22K; a tentative bounce near 13,000 in early July.

- City-wide 24K quotes cluster around 14,329–14,346 per gram, with Delhi, Mumbai, and Chennai near the top.

- Silver price per kilogram hovered around 2,35,000 after peaking around 2,90,000 and sliding through June.

Gold Price Today Across Indian Markets: July 2026 Snapshot

Gold price today in India is oscillating within a narrow corridor as global rate narratives and regional tensions influence demand. The June US inflation print came in cooler than expected, which typically supports gold, but persistent geopolitical tensions and higher rate expectations kept gains cautious. The price journey since mid-June shows a sharp move: on June 15, the 22-karat jewelry gold price per gram hovered around Rs 14,000. By June 25, it slipped to Rs 12,860 per gram, followed by a cautious rebound in early July. This week opened with a dip and a mixed pace through Wednesday, before a fresh decline today. On July 16, Bengaluru’s market data show 24-karat pure gold at Rs 14,329 per gram, 22-karat at Rs 13,135, and 18-karat at Rs 10,747 per gram. Mangalore mirrored 24K and 22K levels at Rs 14,329 and Rs 13,135, with 18K around Rs 10,747 as well.

To ground the narrative in the latest numbers, yesterday’s move shows the 22-karat price per gram slipping Rs 25 to Rs 13,135, while a ten-gram block moved down to Rs 131,350. This pattern–modest daily deltas within a broad range–reflects the market’s sensitivity to global liquidity signals, currency movements, and local demand pockets. The takeaway for a retail investor is clarity: do not rely on a single datapoint; instead, track a short-range trend and consider staged exposure when you expect a longer plateau.

Chennai Gold Price Today: City-Wide 24K And 22K Rates Across Major Cities

Morning trade confirms a tight cluster in 24-karat rates and a stable band for 22-karat variants across Indian metros. Here are the city-wise quotes captured in the latest morning trade across the ten major markets:

- Delhi: 24K Rs 14,344; 22K Rs 13,150

- Mumbai: 24K Rs 14,329; 22K Rs 13,135

- Ahmedabad: 24K Rs 14,334; 22K Rs 13,140

- Chennai: 24K Rs 14,346; 22K Rs 13,150

- Kolkata: 24K Rs 14,329; 22K Rs 13,135

- Hyderabad: 24K Rs 14,329; 22K Rs 13,135

- Jaipur: 24K Rs 14,344; 22K Rs 13,150

- Chandigarh: 24K Rs 14,344; 22K Rs 13,150

- Lucknow: 24K Rs 14,344; 22K Rs 13,150

- Kochi: 24K Rs 14,329; 22K Rs 13,135

- Mangalore: 24K Rs 14,329; 22K Rs 13,135

Chennai gold price today sits near the top end of the spectrum in the 24K category, consistent with a broader trend where the 24K line hovers above Rs 14,300 and the 22K line sits around Rs 13,1xx across major markets. For investors, this city-wise snapshot highlights where local supply and demand dynamics can tilt the buying experience, even when the underlying pure gold value remains relatively steady.

To deepen your understanding of how these city quotes impact purchases or hedging, see Swastika’s Sarthi AI stock assistant, which can help you connect precious metals market signals to stock market decisions: Swastika's Sarthi AI stock assistant.

24 Karat Gold Price And 22 Karat Price Trends: July 2026 Moves And What They Signal

The 24-karat gold price today, as observed in Bengaluru on July 16, shows Rs 14,329 per gram (down Rs 28 from the previous day), while 22-karat jewelry gold is Rs 13,135 per gram (down Rs 25). The 18-karat variant trades around Rs 10,747. The same morning in Mangalore confirms the trend with 24K Rs 14,329 and 22K Rs 13,135, underscored by the same 18K rate around Rs 10,747.

This data suggests a converging price path where the pure metal remains at the Rs 14.3k level, while jewelry-specific variants maintain a small premium over the 24K price, adjusted for alloy content, making Rs 13.1k for typical 22K jewelry a practical benchmark for buyers. The spread between 24K and 22K remains around Rs 1,000 to Rs 1,200 per gram in most markets, a factor that jewelry buyers monitor when negotiating gains or discounts with local dealers.

Silver Price Stability And Intercity Variations: What It Means For Your Portfolio

Silver’s price path has been comparatively steadier in recent weeks, though it also moves with commodity markets and currency shifts. In May, silver price per kilogram peaked near Rs 2,90,000, then eased to about Rs 2,80,000, and declined further to Rs 2,40,000 in June. By early July, silver hovered around Rs 2,50,000 per kilogram, with last week’s readings settling near Rs 2,35,000 and then stabilizing. For a retail investor, silver offers diversification potential but comes with higher volatility on a per-gram basis than gold, and storage and liquidity considerations can affect convenience and cost of ownership.

City-wise, the silver price today mirrors the same trend observed in gold: fluctuations in demand, local liquidity, and currency movements contribute to small variations across metros. Investors should view silver as a complement to gold for hedging, rather than a direct substitute, especially in times of currency stress or rising inflation expectations.

Morning Trade Snapshot: City-Wise 1 Gram Gold Price Across India

Here is a consolidated look at the 1-gram price levels in the morning trade for key cities, highlighting both the 24K and 22K variants. The values reflect the latest morning quotes and show how city-specific pricing aligns with the national trend:

| City | 24K Price (Rs/gram) | 22K Price (Rs/gram) |

|---|---|---|

| Delhi | Rs 14,344 | Rs 13,150 |

| Mumbai | Rs 14,329 | Rs 13,135 |

| Ahmedabad | Rs 14,334 | Rs 13,140 |

| Chennai | Rs 14,346 | Rs 13,150 |

| Kolkata | Rs 14,329 | Rs 13,135 |

| Hyderabad | Rs 14,329 | Rs 13,135 |

| Jaipur | Rs 14,344 | Rs 13,150 |

| Chandigarh | Rs 14,344 | Rs 13,150 |

| Lucknow | Rs 14,344 | Rs 13,150 |

| Kochi | Rs 14,329 | Rs 13,135 |

| Mangalore | Rs 14,329 | Rs 13,135 |

Understanding 24K, 22K And 18K Price Differentials: Practical Investor Insights

Grasping the difference between 24K, 22K, and 18K gold prices is essential for deciding when to buy or sell jewelry versus raw gold. The 24-karat price reflects the value of pure gold, while 22-karat and 18-karat prices incorporate alloy content that makes up the jewelry and affects making charges. The July 16 data shows 24K at Rs 14,329 per gram and 22K at Rs 13,135, with 18K at Rs 10,747 in Bengaluru and Mangalore. A small delta between 24K and 22K in many cities points to relatively stable alloy premiums in the current environment, though regional pricing can deviate due to dealer policies and local demand. Understanding this differential helps you budget jewelry purchases, plan for investment-grade metal, and estimate the relative cost of converting jewelry into pure gold when needed.

For a retail investor, the practical takeaway is clear: track the ratio of 24K to 22K prices over several weeks to identify whether the premium is widening or narrowing. A widening gap can indicate stronger jewelry demand or supply constraints, while a narrowing gap suggests a move toward a more uniform raw-gold price across markets. A disciplined approach–buying in increments, setting price alerts, and using a hedging mindset–can help you navigate the current price environment more effectively.

Actionable Takeaways For Retail Investors: How To Use The Gold Price Today Data

Given the data, a few practical steps can help you navigate gold investments in this environment. First, consider a staged purchase or diversifying across 24K and one or two widely traded jewelry-focused variants to manage liquidity and price risk. Second, use city-wise variations to time small entry opportunities where your preferred dealer offers a favorable 22K to 24K delta or where local demand indicators suggest a short-term move. Third, complement your gold exposure with a portion of silver if your portfolio requires diversification against inflation and currency risk, while being mindful of the higher volatility in silver compared with gold.

Frequently Asked Questions

What is the current gold price today in Bengaluru and other major markets?

As of July 16, 2026, Bengaluru shows 24K gold at Rs 14,329 per gram, 22K at Rs 13,135 per gram, and 18K at Rs 10,747 per gram. Other major markets reflect similar patterns: Delhi 24K Rs 14,344; Mumbai 24K Rs 14,329; Chennai 24K Rs 14,346.

How does the 24 karat gold price today compare with the 22 karat price today in major cities?

Across major cities, 24K prices hover around Rs 14,329 to Rs 14,346 per gram, while 22K jewelry prices range from Rs 13,135 to Rs 13,150 per gram. For example, Delhi 24K Rs 14,344 vs 22K Rs 13,150; Mumbai 24K Rs 14,329 vs 22K Rs 13,135; Chennai 24K Rs 14,346 vs 22K Rs 13,150.

What has been the trend for gold price today since mid-June 2026?

From June 15 to June 25, the 22-karat price per gram moved from around Rs 14,000 to Rs 12,860, then rebounded toward Rs 13,000 in early July. On July 16, the 24K price in Bengaluru was Rs 14,329 per gram, with 22K at Rs 13,135 and 18K at Rs 10,747, indicating a cautious, range-bound movement despite global volatility.

What is the silver price per kilogram and how has it moved recently?

Silver price per kilogram moved from around Rs 2,90,000 in May to Rs 2,80,000, then Rs 2,40,000 in June, rising to about Rs 2,50,000 in early July, and last week around Rs 2,35,000, with some stabilization since. This trajectory suggests silver is tracking broader commodity dynamics with notable volatility.

Where can I track the gold price today data in real-time and get AI-assisted insights?

Real-time price data can be tracked on credible market platforms. For deeper, AI-assisted insights that connect precious metals moves to stock market decisions, you can use Swastika's Sarthi AI stock assistant:Swastika's Sarthi AI stock assistant.

Conclusion

This article was published without a generated conclusion. Please review and add a conclusion before publishing.

Open your trading and demat account here

Reference :

1 : Varthabharati

Latest Articles

.jpg)

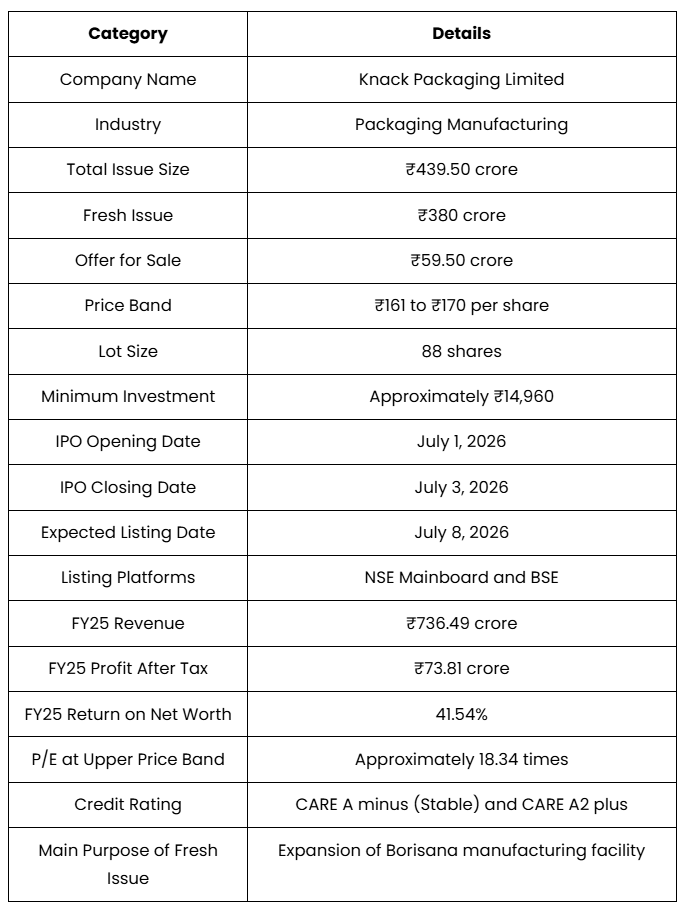

Knack Packaging IPO: Complete Guide for Investors Before Applying

The Indian packaging industry has witnessed steady growth over the past few years, supported by increasing demand from sectors such as agriculture, food processing, chemicals, construction, and industrial manufacturing. Within this growing market, Knack Packaging Limited has established itself as one of the prominent manufacturers of Printed and Laminated Woven Polypropylene (PP) bulk bags.

The Gujarat-based company is now preparing to launch its Initial Public Offering (IPO) on the NSE and BSE Mainboard. The IPO includes a fresh issue of shares to raise capital for business expansion along with an Offer for Sale (OFS), where existing shareholders will sell a portion of their holdings.

With an issue size of ₹439.50 crore and a price band of ₹161 to ₹170 per share, the Knack Packaging IPO provides investors an opportunity to participate in a company that has shown strong financial growth, expanded its global presence, and is investing heavily in increasing its manufacturing capacity.

This detailed IPO guide covers all important aspects of the issue, including the company background, business model, financial performance, valuation, growth plans, strengths, risks, and key factors investors should evaluate before making an investment decision.

Knack Packaging IPO Quick Summary

For investors looking for a quick overview of the IPO, the following table summarises the key details of the issue, financial performance, valuation, and growth plans.

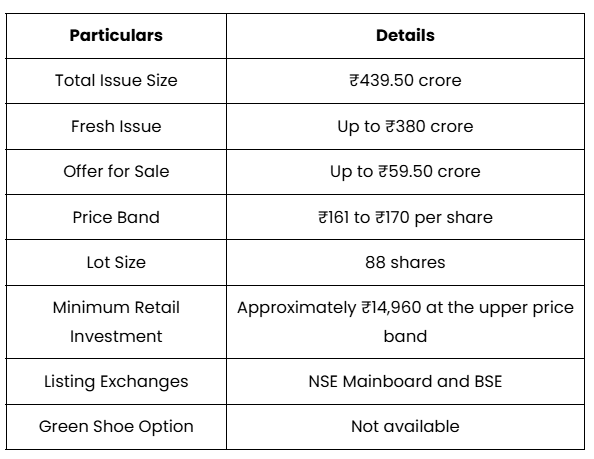

Knack Packaging IPO Overview

The Knack Packaging IPO consists of a fresh issue and an Offer for Sale component. The fresh issue will bring additional capital into the company, which will primarily be used for expansion activities, while the OFS will allow existing shareholders to sell part of their stake.

The following table provides a quick summary of the IPO structure and important issue related details.

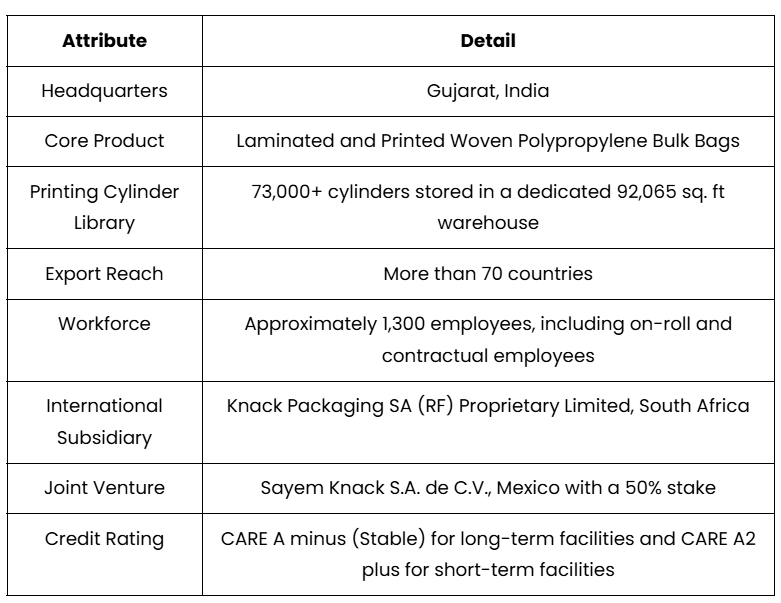

Knack Packaging - Company Overview

Knack Packaging Limited is engaged in manufacturing flexible bulk packaging solutions, mainly printed and Laminated Woven Polypropylene (PLWPP) bags. These bags are widely used by industries that require durable and lightweight packaging solutions for transporting and storing bulk materials.

The company's products are supplied to sectors including agriculture, chemicals, food grains, cement, fertilisers, and other industrial applications. Due to their strength, moisture resistance, and customisation options, woven PP bags have become an important packaging solution for businesses handling large quantities of materials.

One of the key strengths of Knack Packaging is its ability to provide customised packaging solutions at scale. The company has developed a large library of more than 73,000 printing cylinders, allowing it to meet specific design and branding requirements of customers across different industries.

Apart from its domestic presence, the company has built a strong export network and supplies its products to more than 70 countries. This international presence helps the company diversify its revenue base and reduce dependence on a single market.

The following table provides an overview of the company's important business details, including its headquarters, product portfolio, international presence, and operational strengths.

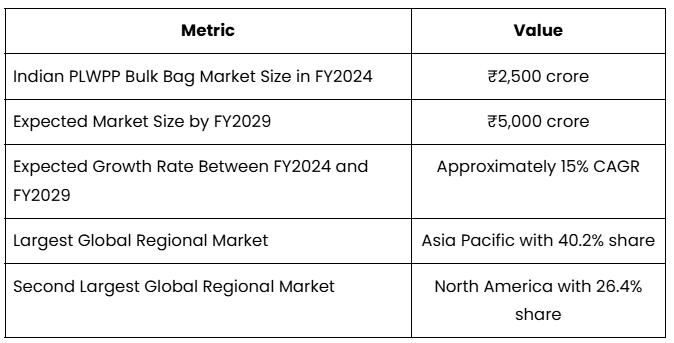

Market Position and Industry Opportunity

The packaging industry in India has been expanding due to rising industrial production, increasing exports, and growing demand for efficient transportation packaging. Bulk packaging solutions are becoming increasingly important as companies look for cost-effective and reliable ways to handle large volume goods.

Knack Packaging currently holds an estimated 10.1% share of the Indian PLWPP bulk bag market as of FY2025. The company operates in a market that is expected to witness strong growth in the coming years.

The following table highlights the size and expected growth opportunity of the PLWPP bulk bag industry. It helps investors understand the broader market environment in which Knack Packaging operates.

The company's growth strategy is focused on increasing manufacturing capacity, strengthening international operations, and improving operational efficiency. Its upcoming expansion project at Borisana, Gujarat, is expected to play an important role in supporting future growth.

However, investors should also evaluate factors such as execution capability, raw material dependency, market competition, and industry cycles before considering the IPO.

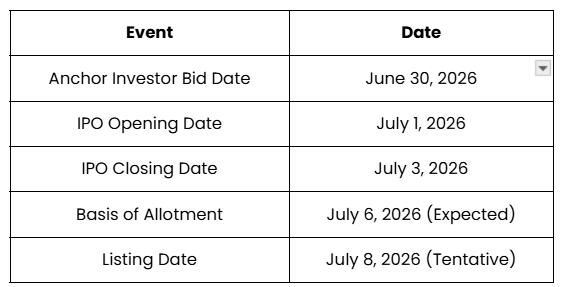

Knack Packaging IPO - Important Dates

Understanding the IPO timeline is important for investors as it helps them plan their application process, track allotment status, and prepare for the expected listing date.

The IPO process includes multiple stages, starting from anchor investor bidding, followed by the opening and closing of the issue for public subscription. After the issue closes, the company completes the allotment process before the shares are listed on the stock exchanges.

The table below highlights the key dates associated with the Knack Packaging IPO.

Investors should note that allotment and listing dates mentioned above are indicative and may change depending on regulatory approvals and the IPO process timeline.

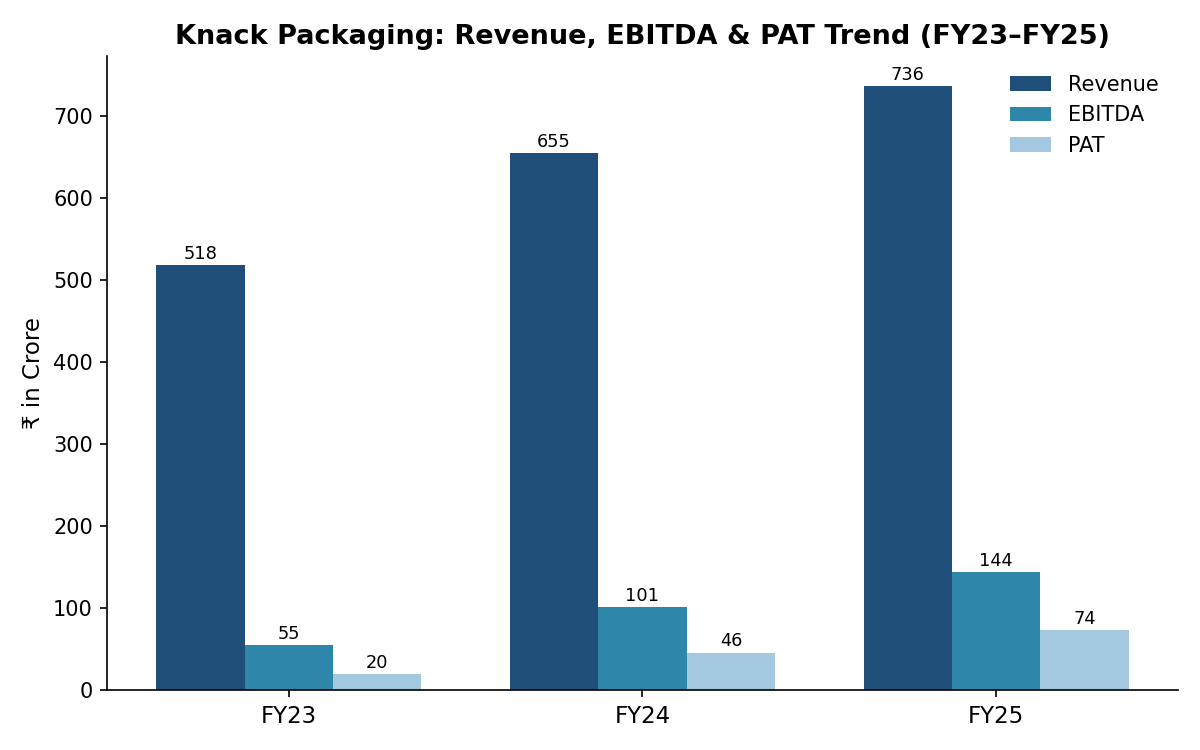

Knack Packaging Financial Performance Analysis

Financial performance is one of the most important factors investors evaluate before investing in an IPO. A company's revenue growth, profitability, margins, and return ratios provide insights into its business stability and future growth potential.

Knack Packaging has reported consistent improvement in its financial performance over the last three financial years. The company has recorded growth in revenue, EBITDA, and profit after tax, supported by higher production capacity, increasing exports, and operational efficiency.

The following image presents the company's key financial performance indicators for FY23, FY24, and FY25.

The company has shown strong improvement in profitability during the period. Profit after tax increased significantly from ₹198.70 million in FY23 to ₹738.10 million in FY25, indicating improved operational efficiency and better utilisation of resources.

The improvement in EBITDA also highlights the company's ability to maintain healthy operating margins despite operating in a competitive manufacturing segment.

Knack Packaging - Growth Highlights

The following points highlight the company's financial growth over recent years:

- Profit after tax increased at a CAGR of 50.30% between FY22 and FY24.

- EBITDA increased at a CAGR of 36.50% during the same period.

- Debt-to-equity ratio improved to 0.7 times in FY25 compared to 1.1 times in FY24 and 1.2 times in FY22.

- Return on Net Worth improved from 23.40% in FY23 to 41.54% in FY25.

A consistently improving return ratio indicates that the company has been generating better returns from shareholder capital. However, investors should also consider whether these growth rates can be maintained after the IPO and during the company's expansion phase.

According to Swastika Investmart's research team, as quoted by Mint, Knack Packaging IPO offers an attractive short-term investment opportunity backed by healthy financial growth, improving profitability, strong return ratios, and robust operating margins. The research team believes the IPO is reasonably valued at a pre-issue P/E of around 18.3x FY26 earnings, while highlighting the company's fully integrated manufacturing operations, extensive portfolio of over 13,000 SKUs, and a library of more than 73,000 customised printing cylinders as key competitive strengths. However, the team also advises investors to consider risks such as customer concentration, the absence of long-term supplier contracts, and execution risks associated with the proposed manufacturing facility, recommending long-term investors reassess the company after its post-listing performance.

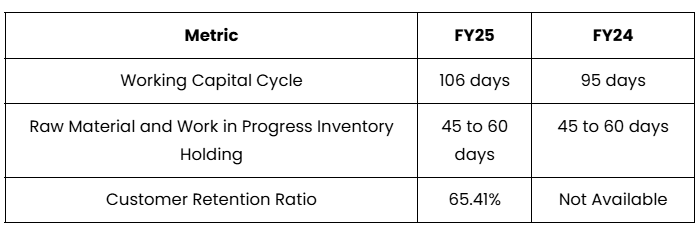

Working Capital and Operational Efficiency of Knack Packaging

For manufacturing companies, working capital management plays an important role because businesses need to maintain inventory, manage supplier payments, and provide credit periods to customers.

The following table highlights important operational metrics that reflect the company's working capital cycle and customer relationships.

The increase in the working capital cycle from 95 days in FY24 to 106 days in FY25 indicates that more capital is being blocked in daily operations. While this is common during expansion phases, investors should monitor whether the company can improve working capital efficiency in the future.

The company has also maintained long-term relationships with several customers. Clients such as KRBL Limited and Repi Soap and Detergent PLC have been associated with Knack Packaging since 2013, highlighting customer trust and repeat business potential.

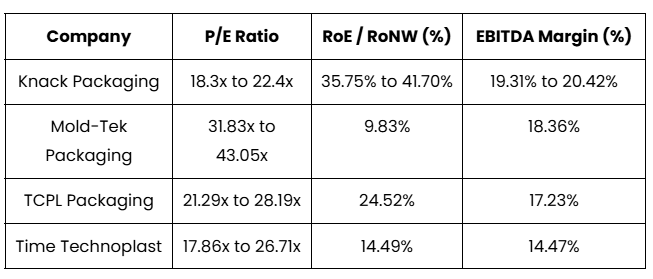

Knack Packaging IPO Valuation and Peer Comparison

Valuation analysis helps investors understand whether an IPO is reasonably priced compared to similar listed companies operating in the same industry.

Knack Packaging is being valued at a price-to-earnings ratio of approximately 18.34 times at the upper price band of ₹170 per share based on the company's reported earnings. Investors generally compare this valuation with industry peers to understand the attractiveness of the issue.

The following table compares Knack Packaging with selected listed packaging companies based on important valuation and profitability parameters.

The comparison indicates that Knack Packaging is available at a relatively competitive valuation compared with many peers. The company also reports stronger return ratios and EBITDA margins compared with the selected companies.

However, investors should remember that valuation should not be considered in isolation. Factors such as company size, industry competition, expansion execution, and future earnings visibility are equally important while evaluating an IPO.

According to CARE Ratings, Knack Packaging’s credit profile is supported by sustained business growth, healthy profitability, a comfortable financial position, and experienced promoters. The company has been assigned CARE A-minus with Stable outlook for long-term facilities and CARE A2 plus for short-term facilities. The rating agency also highlights risks related to volatile raw material prices and foreign exchange fluctuations.

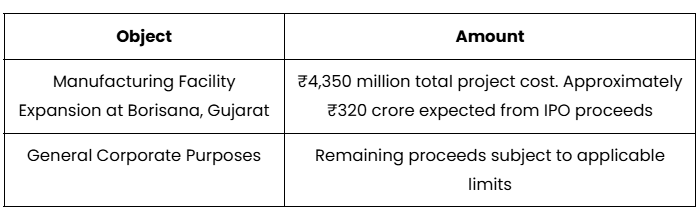

Objects of the Knack Packaging IPO Issue

The purpose of raising funds through an IPO provides investors with insight into how the company plans to use the capital received.

In the case of Knack Packaging, the majority of the fresh issue proceeds will be utilised towards expanding manufacturing capacity through a new facility at Borisana, Mehsana, Gujarat. This expansion is expected to support future production growth and help the company cater to increasing demand.

The table below explains how the company plans to utilise the proceeds raised through the IPO.

The Offer for Sale component of ₹59.50 crore will be received by the selling shareholders and will not directly contribute to the company's growth capital.

From an investor perspective, the IPO proceeds are primarily growth-focused. The success of this investment will depend on how efficiently the company completes the expansion project and converts additional capacity into revenue growth.

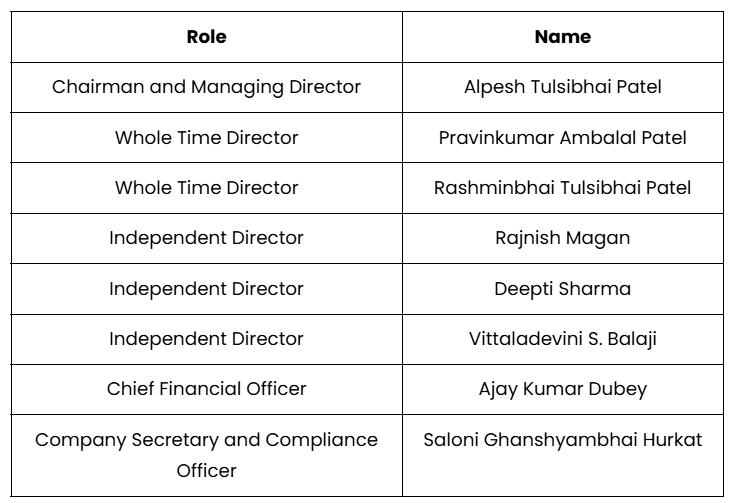

Promoters, Management and Shareholding Structure

The strength of a company is often closely linked with the experience of its management team and the vision of its promoters. In a manufacturing business, where long-term customer relationships, operational execution, and capacity expansion play a crucial role, experienced leadership becomes an important factor for sustainable growth.

Knack Packaging is promoted and managed by professionals with experience in the packaging industry. The management team has been involved in expanding manufacturing capabilities, developing export markets, and building relationships with customers across multiple industries.

The following table provides details about the key members of the company's management team.

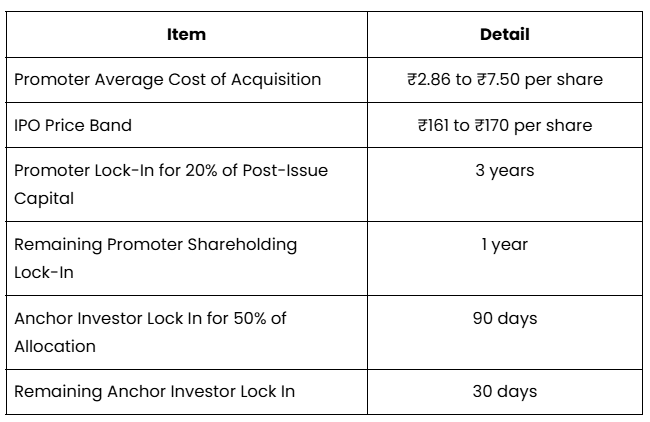

Promoter Holding and Lock-In Details

Promoter holding and lock-in periods provide investors with an understanding of promoter commitment after the IPO. A longer lock-in period generally indicates that promoters continue to have a long-term interest in the growth of the company.

The following table explains important promoter and investor lock-in details related to the IPO.

A key point investors should evaluate is that some important company properties, including the registered office and the upcoming Borisana project site, are leased from promoter-related entities. While such arrangements are common in promoter-driven businesses, investors should carefully review the terms, duration, and renewal conditions mentioned in the Red Herring Prospectus.

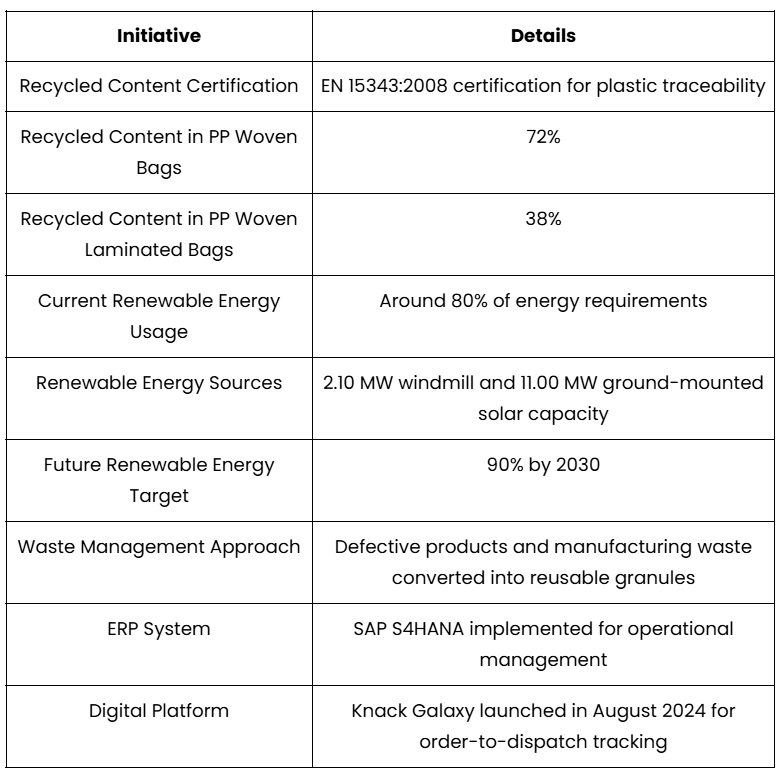

Sustainability Initiatives and Technology Advantage

The packaging industry is undergoing significant changes as customers increasingly focus on sustainability, recycling, and efficient manufacturing processes. Companies that can provide environmentally responsible packaging solutions may have better opportunities to attract global customers.

Knack Packaging has focused on sustainability initiatives by increasing the use of recycled materials, adopting renewable energy sources, and implementing technology-driven systems to improve operational visibility.

The following table highlights the company's major sustainability and technology initiatives.

These initiatives can help the company improve operational efficiency, reduce dependency on conventional energy sources, and strengthen its position among customers that prioritise sustainable packaging solutions.

However, investors should also consider that sustainability initiatives require continuous investment and their financial benefits depend on effective implementation and customer acceptance.

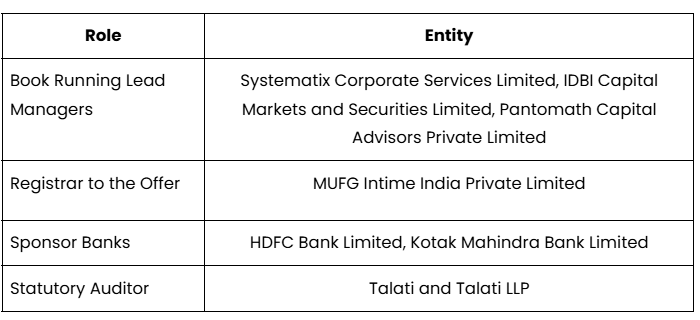

Key Intermediaries Involved in Knack Packaging IPO

An IPO involves several financial institutions and professional agencies responsible for managing different aspects of the issue process. These intermediaries ensure regulatory compliance, investor servicing, and smooth execution of the public offering.

The following table provides details of the major intermediaries associated with the Knack Packaging IPO.

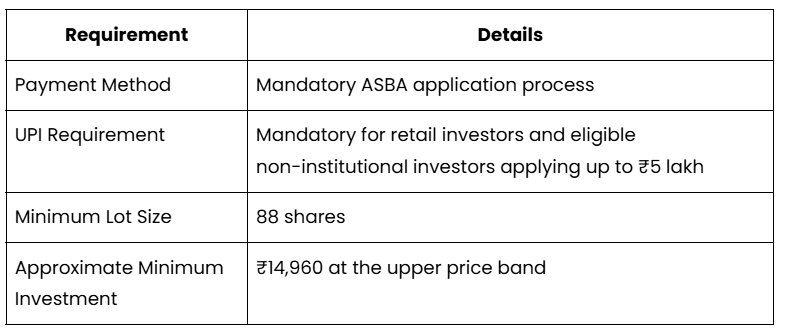

How to Apply for Knack Packaging IPO

Applying for an IPO has become simpler with digital banking facilities and online application platforms. Retail investors can participate through the ASBA process, where the application amount remains blocked in the bank account until the allotment process is completed.

The following table explains the important application requirements for investors.

Investors should ensure that their PAN details, bank account information, and UPI details are correctly updated before applying. Any mismatch in details may lead to rejection of the application.

Key Strengths of Knack Packaging IPO

Before investing in an IPO, investors should evaluate the factors that can support the company's long-term growth. Knack Packaging has several business strengths that differentiate it within the packaging industry.

Strong Product Customisation Capability

The company's large library of more than 73,000 printing cylinders provides it with an advantage in serving customers requiring customised packaging solutions. This capability can help improve customer retention as businesses often prefer suppliers who can efficiently manage specific design requirements.

According to Nidhi Thakur of Swastika Investmart, Knack Packaging IPO offers a balanced growth opportunity backed by its premium packaging segment. The company’s 73,000+ printing cylinder library creates a strong competitive advantage. While valuation is supported by robust profitability, investors should consider moderated growth and the delayed impact of the Borisana facility before subscribing.

Established Export Presence

With exports reaching more than 70 countries, Knack Packaging has developed a diversified customer base across international markets. A global presence can provide additional growth opportunities and reduce dependency on domestic demand.

Healthy Financial Performance

The company has reported great improvement in revenue, profitability, and return ratios. Rising RoNW and improving debt levels indicate better capital efficiency and financial discipline.

Competitive Valuation Compared With Peers

At the upper price band, the company's valuation appears reasonable compared with several listed packaging companies. The combination of healthy margins and return ratios makes valuation an important factor for investors evaluating the IPO.

Long-Term Customer Relationships

The company's association with customers for several years indicates business stability and repeat order potential. Strong customer relationships are particularly valuable in the B2B packaging industry.

Focus on Sustainability

Higher usage of recycled materials and renewable energy adoption can support the company's positioning among customers looking for sustainable packaging solutions.

International Expansion Opportunities

The company's presence through its South African subsidiary and Mexican joint venture provides opportunities to expand its global footprint, especially in emerging markets.

Key Risk Factors Investors Should Consider

While Knack Packaging has demonstrated strong financial growth and has several business advantages, every investment opportunity comes with certain risks. Understanding these risks is important before making an IPO investment decision.

Investors should evaluate both the growth potential and possible challenges that may impact the company's future performance.

Expansion Project Execution Risk

A significant portion of the fresh issue proceeds will be utilised towards the company's new manufacturing facility at Borisana, Gujarat. The success of this expansion will depend on timely completion, effective utilisation of the new capacity, and the company's ability to generate sufficient demand.

Any delay in project completion, increase in project cost, or slower than expected capacity utilisation could impact future growth expectations.

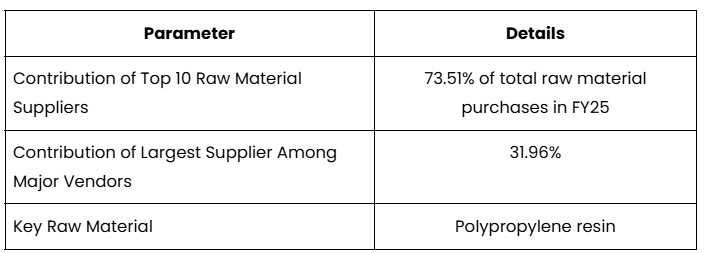

Dependence on Raw Material Prices

The company's primary raw material is polypropylene, whose prices are linked to crude oil movements and global market conditions. Any significant increase in raw material costs without a corresponding increase in selling prices could affect profit margins.

Additionally, the company has some dependence on key suppliers, which creates concentration risk in procurement.

The following table highlights the company's raw material supplier concentration.

Currency Fluctuation Risk

Since Knack Packaging exports its products to more than 70 countries, changes in foreign currency exchange rates can impact revenue and profitability.

A stronger Indian rupee against major global currencies may reduce export competitiveness, while adverse currency movements can affect margins if not effectively managed.

Employee Retention Challenges

Manufacturing businesses require skilled employees for production operations, quality control, and technical processes.

The company's employee attrition rate increased from 9.43% in FY23 to 21.39% in FY25. A continued increase in employee turnover could create challenges related to recruitment, training costs, and operational efficiency.

Related Party Lease Arrangements

Certain important properties, including the registered office and the upcoming project location, are leased from promoter-related entities.

While such arrangements are common among promoter-driven companies, investors should review the lease agreements carefully to understand rental terms, renewal conditions, and any potential dependency on related parties.

Increasing Working Capital Requirement

The working capital cycle increased from 95 days in FY24 to 106 days in FY25. A longer working capital cycle means more funds remain blocked in inventory and receivables.

If the company continues expanding rapidly, efficient management of working capital will become increasingly important to maintain healthy cash flows.

Restated Financial Statement Considerations

The financial statements included in the IPO documents have been prepared specifically for the public issue process. Investors should review the restated financial statements and auditor observations provided in the Red Herring Prospectus before making an investment decision.

Legal and Regulatory Matters

The company is involved in certain legal matters, including recovery cases related to dishonoured cheques and a pending direct tax dispute.

While the financial impact of these matters appears limited based on available information, investors should consider all disclosed legal proceedings before investing.

Final Thoughts on Knack Packaging IPO

Knack Packaging enters the IPO market with a combination of strong financial growth, an established manufacturing base, international customer presence, and expansion plans aimed at increasing future capacity.

The company's strengths include healthy profitability, improving return ratios, a wide export network, long-standing customer relationships, and a differentiated position through customised packaging capabilities.

The valuation also appears competitive when compared with several listed peers, especially considering the company's profitability metrics and operating margins. The planned capacity expansion could provide the next phase of growth if executed successfully.

However, investors should also consider the associated risks, including dependence on raw material prices, working capital requirements, supplier concentration, export-related currency exposure, and execution challenges related to the new manufacturing facility.

Overall, the Knack Packaging IPO represents an opportunity in a growing industrial packaging segment, but investors should evaluate the company's growth potential, valuation comfort, and risk factors based on their individual investment objectives and risk appetite.

Before investing, investors are advised to carefully read the Red Herring Prospectus and consider consultation with a registered financial advisor.

For detailed IPO analysis, market insights, and expert guidance on IPO investments, investors can connect with Swastika Investmart, a trusted financial services provider helping investors make informed market decisions.

Nhai Share Price Outlook: Delhi Dwarka Tunnel And Kanpur Highway Projects

Key Takeaways

- Two Cabinet-approved road projects total Rs 14,115 crore, including the Delhi Dwarka tunnel and Kanpur–Kabrai highway.

- The Delhi tunnel is 8.1 km long with a Rs 6,969.67 crore budget, featuring a 3.14 km tunnel, 0.98 km approaches, a 0.554 km reinforced earth wall, a 2.556 km elevated corridor, and a 0.87 km at-grade road.

- The Kanpur–Kabrai highway is four-lane with a budget of Rs 7,145 crore.

- Direct and indirect employment is significant: every lane-km yields 264 direct and 55 indirect person-days, with the Delhi tunnel alone projected to generate about 7.54 lakh direct and 9.8 lakh indirect person-days.

nhai share price is more than a number; it's a signal of how India's infrastructure push translates into market expectations. The government approved two major road projects on Wednesday, totaling Rs 14,115 crore, including a six-lane tunnel connecting the Dwarka Expressway with Vasant Kunj in Delhi and a four-lane access-controlled highway between Kanpur and Kabrai in Uttar Pradesh. The Delhi project alone carries a cost of Rs 6,969.67 crore and will be developed under the Hybrid Annuity Mode as part of the National Highways (Original) scheme. This post unpacks what these approvals mean for traffic, employment, and the investment landscape, and how it relates tonhai share price in the near term.

Nhai Share Price Outlook For Indian Infrastructure Plays

The approvals signal a robust public works pipeline that can influence sentiment around nhai share price and related infrastructure stocks. The two projects – Delhi Dwarka tunnel (NH-148AE) and Kanpur–Kabrai highway in Uttar Pradesh – total Rs 14,115 crore, with the Delhi tunnel portion valued at Rs 6,969.67 crore. The Kanpur–Kabrai four-lane highway carries a separate budget of Rs 7,145 crore. Both projects are designed to improve regional connectivity, shorten travel times, and relieve congestion across critical corridors linking West, South, and East Delhi as well as Ghaziabad and Noida.

| Delhi Tunnel Project (NH-148AE) Components | Length / Cost |

|---|---|

| Total Length | 8.1 km |

| Tunnel Length | 3.14 km |

| Tunnel Approaches | 0.98 km |

| Reinforced Earth Wall Approaches | 0.554 km |

| Elevated Corridor | 2.556 km |

| At-Grade Road | 0.87 km |

| Under Forest Ridge | 1.98 km |

| Nelson Mandela Marg Elevated | 1.8 km |

| Alignment | Shiv Murti Interchange to Nelson Mandela Marg/Mahipalpur-Chhatarpur Road |

| Development Model | Hybrid Annuity Mode (HAM) as part of National Highways (Original) scheme |

| Estimated Cost | Rs 6,969.67 crore |

| Planned Integrations | AIIMS–Mahipalpur elevated corridor; Barapullah linked corridor |

The project is designed to integrate with the proposed elevated corridor between AIIMS and Mahipalpur. The link will eventually connect with the Barapullah elevated corridor, enhancing connectivity across West, South, and East Delhi, and extending to Ghaziabad and Noida.

The tunnel will pass beneath the environmentally sensitive Southern Delhi Ridge using TBM technology to minimise surface disruption while ensuring structural safety for the surrounding eco-system. In addition to the tunnel, the package includes a 1.8-km elevated U-turn facility and an elevated road along Nelson Mandela Marg to improve traffic flow and accessibility toward Chhatarpur and Mahipalpur.

Kanpur To Kabrai Highway: Cost, Length, And Connectivity Benefits

The other announced project is a four-lane, access-controlled highway between Kanpur and Kabrai in Uttar Pradesh, with an estimated cost of Rs 7,145 crore. This second project complements the Delhi tunnel by connecting major industrial and agricultural hubs in the region, reducing travel times and easing congestion along the Kanpur corridor.

Together, the two projects represent a total investment of Rs 14,115 crore and aim to unlock faster regional connectivity, improve freight and passenger movement, and stimulate economic activity around the corridor. The reforms reflect a broader strategy to modernise national highways and improve multi-modal connectivity across the National Capital Region and the northern plains.

Employment Impact And Economic Multiplier Of The Two Projects

As a rule of thumb, the government estimates that every lane-km of national highway construction generates around 264 person-days of direct employment and 55 indirect employment days. Based on this logic, the Delhi tunnel project alone is expected to create nearly 7.54 lakh person-days of direct employment and 9.8 lakh indirect employment days, besides generating additional economic activity in the surrounding areas. This implies sizable local and regional benefits beyond the construction phase and can influence the consumption dynamics in nearby communities.

Hybrid Annuity Mode And What It Means For Investors

The Delhi tunnel project will be developed under the Hybrid Annuity Mode (HAM) as part of the National Highways (Original) scheme. HAM is designed to combine public funding with private capital and project execution efficiency, potentially reducing toll risk and accelerating project delivery timelines. For investors, HAM-backed projects often offer a mixed risk-reward profile: steady revenue streams backed by government payments coupled with the potential for long-term asset value creation as the corridor integrates with existing networks.

With two major road infrastructure projects moving forward, there is a clear signal that the pipeline for public works remains robust. While stock-specific calls should be grounded in company fundamentals and broader market conditions, the macro visibility from such projects tends to support a constructive stance on infrastructure beneficiaries. As a practical consideration, retail investors can monitor the project milestones, bid awards, and private partner disclosures that often foreshadow value creation in related stock segments.

For a deeper, institution-grade search on any stock or index, Swastika's Sarthi AI stock assistant provides research insights and scenario analysis that can help you align infrastructure exposure with your risk tolerance and time horizon. Swastika's Sarthi AI stock assistant.

What The Delhi Projects Mean For The Nhai Share Price: Investor Takeaways

From an investor perspective, the two Cabinet-approved road projects signal a continued commitment to expanding road connectivity and reducing travel times across key corridors. While project approvals do not immediately translate into earnings statements for listed peers, the ramp-up in project execution can influence sentiment around infrastructure stocks and the broader nhai share price trajectory. Investors should watch for tender awards, concession opportunities under HAM, and the pace at which the National Highways Authority of India (NHAI) monetises or refinances project cash flows as part of the asset-light growth narrative that many market participants favour in the sector.

Frequently Asked Questions

Which two highway projects were approved and what are their costs?

The Cabinet Committee on Economic Affairs approved two road projects: the Delhi Dwarka tunnel on NH-148AE with a cost of Rs 6,969.67 crore, and the Kanpur–Kabrai four-lane highway in Uttar Pradesh with a cost of Rs 7,145 crore, for a combined investment of Rs 14,115 crore.

What are the key features of the Delhi Dwarka tunnel project?

The Delhi Dwarka tunnel project is 8.1 km in total length, comprising 3.14 km of tunnel, 0.98 km of tunnel approaches, 0.554 km of reinforced earth wall approaches, 2.556 km of elevated corridor, and 0.87 km of at-grade road. It includes a 1.8 km elevated segment along Nelson Mandela Marg and a 1.98 km section under environmentally sensitive forest ridge, and begins at Shiv Murti Interchange, terminating before Nelson Mandela Marg and Mahipalpur-Chhatarpur Road. It will integrate with AIIMS–Mahipalpur elevated corridor and Barapullah corridor, and is developed under Hybrid Annuity Mode (HAM).

What is HAM financing and which scheme does this project use?

The Delhi tunnel project is developed under the Hybrid Annuity Mode (HAM) as part of the National Highways (Original) scheme, combining public funding with private capital to support project execution.

What is the employment impact of these road projects?

The government estimates that every lane-km of national highway construction generates around 264 direct employment days and 55 indirect employment days. Based on this logic, the Delhi tunnel project alone is expected to create about 7.54 lakh direct and 9.8 lakh indirect employment days, contributing to local economic activity.

What is the overall investment and connectivity impact of the two projects?

Together, the two projects involve Rs 14,115 crore in investment, aimed at improving regional connectivity and reducing travel times and congestion. The Delhi tunnel links Dwarka Expressway, Vasant Kunj, and other West-South Delhi corridors, while the Kanpur–Kabrai highway enhances north-central Uttar Pradesh connectivity.

Conclusion

The Delhi Dwarka tunnel and Kanpur–Kabrai highway approvals are a reminder of how public infrastructure spend is a leading indicator for the financial performance and market perception of infrastructure stocks. For retail investors, the key takeaway is to monitor the project milestones, HAM financing progress, and regional connectivity gains as a way to gauge potential shifts in nhai share price over the coming quarters. Consider applying a simple mental model: treat the project pipeline as a forward-looking indicator of sector momentum, and align your holdings with those stocks and sectors most likely to benefit from faster, more reliable transport corridors.

Geojit BNP Paribas Share Price Context In The Indian Market Outlook

Key Takeaways

- Crude price near $70-75 per barrel relieves earnings, forex and fiscal headwinds.

- FII selling eases; domestic money leads the rally.

- Private banks, consumption, and telecom offer attractive opportunities as earnings visibility improves.

- Premium valuations persist, but large-cap stocks now offer better value than mid/small caps.

Investors watching geojit bnp paribas share price may sense a turning point for Indian equities as crude eases and FII selling cools. A brighter backdrop is emerging: crude oil has slipped toward the $70-75 per barrel band, which has positive implications for earnings, forex, interest rates, and the government's fiscal position. In this environment, domestic flows have room to sustain momentum, with private banks, consumption, and telecom sectors offering attractive opportunities. While near-term results may reflect temporary disruptions, the earnings outlook is improving, with some sectors showing resilience even as others recalibrate.

Geojit BNP Paribas Share Price Context In The Indian Market Outlook

Investors following geojit bnp paribas share price can glean insights into the sentiment that informs cross-border brokerage and local market flows. The market's fundamentals are now more important than headlines; with crude trending lower, FII selling easing, valuations modestly more attractive, and earnings visibility improving, the tone has shifted toward earnings-driven returns. Domestic investors, too, are recalibrating risk, focusing on sectors that can sustain growth as temporary headwinds fade.

The broader narrative remains earnings-driven rather than dependent on large foreign inflows. The improvement in crude pricing is a big relief for corporate earnings and macro stability, while valuations across sectors have become slightly more attractive as earnings visibility strengthens.

Lower Crude Oil And Easing FII Selling: Implications For Market Outlook

A major driver is crude oil falling to the $70-75 per barrel range, one of the biggest positives for the Indian economy. The fall has positive implications for earnings, forex, interest rates and the government's fiscal position. The reasons for FII selling have reduced, valuations have become slightly more attractive and the earnings outlook is improving.

According to Kunal Vora of BNP Paribas India, "Compared to where we were two months back, the market construct is looking better. Crude at $70-75 is a big relief. It has positive implications for earnings, forex, interest rates and the government's fiscal position. The reasons for FII selling have reduced, valuations have become slightly more attractive and the earnings outlook is improving," he said.

In the near term, earnings may reflect the temporary impact of crude-related disruptions, but the medium-term trajectory remains constructive for the broader market.

Private Banks Earnings Growth Outlook For FY27

After a subdued FY26, the forecast is earnings growth of 15-18% for leading private lenders during FY27. Attractive valuations across price-to-earnings and price-to-book metrics further strengthen the investment case. Heavy FII selling has weighed on the sector, but if that pressure eases, banks should benefit from improving flows.

According to Kunal Vora of BNP Paribas India, "After a subdued FY26, he expects earnings growth of 15-18% for leading private lenders during FY27. Attractive valuations across price-to-earnings and price-to-book metrics further strengthen the investment case."

Private banks, by virtue of their earnings resilience and balance-sheet strength, are positioned to lead the rally as external headwinds ease and domestic flows stabilize.

Domestic Money Can Carry The Market When FII Flows Subside

India does not really need FPI money to come back in a big way. What we need is a lack of selling. If incremental FII selling eases, domestic money can continue doing the heavy lifting and help the market grind higher even in the absence of a strong FPI inflow. This premise underpins a broader strategy for retail investors who focus on earnings growth and sustainable cash generation.

As a result, consumer-facing names, particularly within consumer staples and telecom, remain attractive on demand recovery hopes and pricing power. The picture for equities remains more balanced between growth and value as earnings visibility broadens.

Consumption And Telecom Stocks Offer Attractive Opportunities In The Coming Quarters

Besides financials, Vora remains constructive on consumption stocks, especially consumer staples, following the recent GST rate cut. He believes improving demand and pricing power could support earnings after the temporary crude-related impact fades. Telecom is another sector he favours because of its consistent pricing power and the possibility of another tariff hike over the coming quarters.

According to Kunal Vora of BNP Paribas India, "Besides financials, Vora remains constructive on consumption stocks, especially consumer staples, following the recent GST rate cut. He believes improving demand and pricing power could support earnings after the temporary crude-related impact fades. Telecom is another sector he favours because of its consistent pricing power and the possibility of another tariff hike over the coming quarters."

The stance underscores a balanced view: look for earnings growth in sectors with durable pricing power, while remaining selective in IT given AI-driven uncertainties.

IT Sector Valuations And Structural Questions In The AI Era

IT valuations have corrected meaningfully and dividend yields have become increasingly attractive, yet the sector continues to grapple with long-term uncertainty stemming from artificial intelligence. While the risk of widespread degrowth is unlikely, terminal growth assumptions have changed because of AI, making this a more value-oriented call, with an eye on eventual stabilization of growth. The broader implications of an IT hiring slowdown remain, given the sector remains one of India's largest employers and a significant contributor to wage growth.

According to Kunal Vora of BNP Paribas India, "We do not expect the sector to start degrowing, but terminal growth assumptions have changed because of AI. This has become more of a value call and a hope that growth eventually bottoms out."

The IT sector remains a key barometer for corporate demand but requires a nuanced view of long-term growth prospects in an AI-influenced world.

Premium Valuations Are A Structural Feature

Indian valuations across sectors are higher than global peers. That is a structural feature of our market and not unique to IT. I do not expect that premium to disappear. This makes a focus on earnings quality and balance sheets essential for stock selection in a high-valuation environment.

According to Kunal Vora of BNP Paribas India, "Indian valuations across sectors are higher than global peers. That is a structural feature of our market and not unique to IT. I do not expect that premium to disappear."

Investors should emphasize earnings durability, revenue visibility and robust balance sheets to navigate premium prices.

Large Caps Offer Better Value Than Mid And Small Caps

Although mid- and small-cap stocks have delivered exceptional returns, valuations have stretched after sustained domestic inflows and relatively lower FII ownership. Midcaps and smallcaps have become much more expensive relative to largecaps. We currently see better value in the large-cap space, while some froth remains in the broader market.

According to Kunal Vora of BNP Paribas India, "Midcaps and smallcaps have become much more expensive relative to largecaps. We currently see better value in the large-cap space, while some froth remains in the broader market."

For long-term investors, this suggests focusing on quality large-cap franchises with sustainable earnings growth and strong capital allocation at reasonable valuations.

Focus On Earnings Growth Rather Than Foreign Flows

Looking ahead, Vora expects market returns to broadly track corporate earnings rather than be driven by large foreign inflows. He believes India can continue delivering respectable returns if earnings growth remains in the low-to-mid teens and foreign selling gradually subsides. "We are banking on domestic money to drive the market, not FIIs. If earnings grow in the mid-teens and FII selling eases, returns should broadly follow earnings even without large foreign inflows," he said.

For stock-level decisions, this translates to a disciplined focus on companies with visible earnings trajectories, stable margins and strong balance sheets. Retail investors can complement this with AI-assisted insights from Swastika’s research tools and stock assistant to validate ideas before taking positions.

To explore stock ideas with AI-driven insights, explore Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What is the current market outlook with crude prices easing and FII selling cooling?

Crude easing and easing FII selling brighten the market outlook; earnings visibility is improving, and domestic money can sustain momentum even if foreign flows stay cautious.

Which sectors are highlighted as opportunities in this market environment?

Private banks, consumption, and telecom offer attractive opportunities, while IT remains a sector with premium valuations and structural questions due to AI.

What earnings growth is expected for private banks in FY27?

Leading private lenders are expected to grow earnings by about 15-18% in FY27, with valuations remaining supportive.

Why are valuations in Indian markets described as premium and structural?

Valuations across sectors in India are higher than global peers as a structural feature of the market, and this premium is not expected to disappear quickly.

What role does domestic money play if FIIs retreat?

Domestic money can carry the market if incremental FII selling subsides, reducing reliance on foreign inflows.

How are IT sector valuations and AI influencing growth assumptions?

IT valuations remain premium with AI introducing structural questions; growth may bottom out but not degrow, making it a cautious but value-oriented call.

Conclusion

For the retail investor today, the question is not whether FIIs will return in full force, but whether earnings growth can sustain a mid-to-high-teens trajectory as crude headwinds fade. With crude near $70-75 per barrel, earnings visibility improves, and valuations in large caps remain attractive relative to mid/small caps, the case for stock picking is clear: focus on sectors with pricing power and durable earnings. A disciplined, earnings-driven approach can help you navigate the current environment and participate in a potential rally driven by domestic money while keeping risk under check.

Zomato Share Price Sparks Market Momentum: A Retail Investor's Guide

Key Takeaways

- Sensex gained 444 points to 76,922.64 and Nifty 50 rose to 24,005.85.

- India VIX fell over 3% to 13.19, signaling cooled fear and improved risk appetite.

- 1,852 stocks advanced, 1,473 declined, and 100 were unchanged.

- Zomato share price led gains amid a broad rally in consumer staples and select defensive names.

Markets opened with a sharp question: can today’s breadth carry the rally? Sensex gained around 444 points to close at 76,922.64, and Nifty 50 rose over 140 points to end at 24,005.85. The zomato share price drew attention, rising around 6% to lead gains as several consumer staples joined the upmove, including hindustan unilever limited stock price moving around 3-4% higher, nestle india stock price also improving, and dabur stock price climbing roughly 5%.

Beyond the headline moves, breadth mattered. About 1,852 stocks advanced on the session, while 1,473 declined and 100 remained unchanged. The total market capitalization of all listed companies rose by more than Rs 2 lakh crore, lifting the aggregate to around Rs 476 lakh crore. Global cues provided supportive backdrop: Dow Jones finished at 52,319.20 and Nasdaq gained about 1.52%, reinforcing the mood in risk assets. Brent crude futures hovered near $72 per barrel, with WTI trading around $69 per barrel, underscoring a more comfortable supply backdrop compared with earlier spikes. On the monsoon front, June ended with a 40% rain deficit, and IMD projected July rainfall at roughly 90% of the long-term average, a factor investors will monitor for sector rotation and inflation dynamics.

From a sector lens, Nifty FMCG rose about 2% while Nifty Realty added roughly 4%. Nifty IT slipped more than 2%, reflecting profit-taking in some technology names. The leadership came from a mix of consumer staples and select defensives as the market breadth widened. Zomato stock price, nestle india stock price, hindustan unilever limited stock price, and other names delivered gains that helped offset pockets of weakness in heavyweight IT names. In single-session terms, the day’s movers painted a picture of breadth supporting a cautious but constructive risk stance for retail portfolios.

Zomato Share Price Movements And Market Implications

The zomato share price move highlighted the day’s breadth and the appetite for growth names alongside staples. The stock’s approximately 6% rise acted as a bellwether for a broader momentum across consumer-focused equities. While some investors focus on mega-cap indices, this session underscored how mid- and small-cap themes can accompany the carryover in large-cap sentiment, enabling a wider allocation spectrum for retail portfolios. The name’s movement must be interpreted in the context of a broader market that saw 1,852 advancers versus 1,473 decliners and 100 unchanged.

For traders and investors, the implications are twofold. First, simultaneous gains in consumer staples and select defensive names suggest a shift from purely cyclical bets to more resilient themes amid uncertain monsoon signals. Second, the strong breadth hints at accumulation in pockets of the market beyond the usual large-cap leaders, potentially offering fresh ideas for stock-picking within a diversified framework. To navigate this, consider balancing growth opportunities with defensive ballast to manage potential volatility from IT sector adjustments and global macro shifts.

According to VK Vijayakumar of Geojit Investments, “Investors may fine tune portfolios to discount the potential negative fallout of poor monsoon. Partial portfolio adjustment in favour of fixed income may be considered. Also churning of portfolios in favour of monsoon-proof sectors like health care, pharmaceuticals, power and select fairly valued defence stocks is advisable.”

Sensex And Nifty Rally: Key Levels And Sector Performance

The Sensex’s 444-point gain and the Nifty’s move above 24,000 levels marked another day of resilience for Indian equities. The closing print of 76,922.64 on the Sensex and 24,005.85 for the Nifty 50 translated into a broad-market footprint, with the breadth data showing 1,852 advances, 1,473 declines, and 100 unchanged stocks. In terms of sector effects, the Nifty FMCG index rose around 2% while the Nifty Realty index logged a 4% uptick. By contrast, the Nifty IT index declined by more than 2%, underscoring intra-sector rotation rather than a one-way chase in equities.

Key stock-specific moves underscored the day’s theme. The zomato share price was among the morning’s top movers, while the asian paints stock price improved by roughly 3%, and the hindustan unilever limited stock price rose in the 3–4% band. The nestle india stock price also contributed to the risk-on mood, with gains in the same range, and dabur stock price climbing around 5%. These participants helped create a more balanced risk-reward dynamic for investors weighing consumer staples against cyclical bets.

On the technical side, the market held above key supports as traders eyed the next leg higher. The short-term bias remained constructive as long as the Nifty stayed above a rough 23,800 support, with potential targets around 24,200 and beyond if momentum sustains. In this context, market participants should watch the interplay between pervasive breadth and sector-specific dynamics to identify pockets of value that align with a monsoon-adjusted macro outlook.

According to Rupak De of LKP Securities, “The short-term trend remains positive, with the index showing resilience throughout the session. However, momentum continues to be subdued. Going forward, the bullish bias is likely to remain intact as long as the Nifty holds above the 23,800 support level. On the higher side, the index may continue its slow but steady upward trajectory, with the potential to move towards 24,200 and higher over the near term.”

Market Breadth, Volume And Global Cues

Market breadth on the day was favorable to the bulls, with 1,852 advances versus 1,473 declines and 100 unchanged stocks. The broader market mood aligned with a steady global backdrop: the Dow Jones Industrial Average closed at 52,319.20 and the Nasdaq Composite rose by about 1.52%. Commodities also traded with calm: Brent crude futures hovered around $72 per barrel while WTI traded near $69 per barrel, signaling a softer energy backdrop relative to the earlier spikes visible during mid-year volatility.

These dynamics are particularly meaningful for retail investors, as they translate into opportunities for diversification across sectors and market caps. High-frequency traders and longer-term investors alike should consider how the breadth expansion interacts with sector rotations–especially when monsoon uncertainty weighs on agricultural and consumer demand dynamics. The calendar’s near-term risk factors also include the monsoon’s trajectory, with June’s 40% rainfall deficit and IMD’s July forecast of roughly 90% of long-term average rainfall. Investors may want to factor these into sector tilts toward staples, pharma, power, and defense as part of a calibrated defensive stance.

Stock And Sector Movers: Zomato, Nestle India, Dabur, Asian Paints, Hindustan Unilever, And More

Beyond the headline indices, a handful of individual names carried the day. The zomato share price remained in focus as a standout performer in a day of broad gains. Others showing strength included asian paints stock price (about 3%), hindustan unilever limited stock price (around 3–4%), nestle india stock price (roughly 3–4%), and dabur stock price (approximately 5%). In contrast, several IT names, including Tech Mahindra, TCS, and HCL Technologies, slipped around 3% apiece, illustrating the ongoing rotation within the market. The indices meanwhile reflected a mixed image with Nifty IT down more than 2% while realty and consumer staples lifted the broader market mood.

From a position-management perspective, the gains in consumer staples and defensives suggest that investors may be recalibrating expectations in light of the monsoon risk and macro uncertainties. This environment supports a disciplined approach: blend selective growth exposures with defensive quality stock picks and maintain readiness to reallocate based on evolving rainfall signals and earnings trajectory. A practical way to stay disciplined is to anchor decisions around a few core holdings while allowing for small, targeted bets in outperforming sectors when risk-reward looks favorable.

Monsoon Outlook And Defensive Positioning For Retail Investors

The monsoon context remains a tailwind and a watchful eye for equity markets. A 40% rainfall deficit in June raises concerns about agricultural incomes and rural demand, potentially affecting consumer sectors differently across states. With IMD projecting July rainfall near 90% of the long-term average, investors might find merit in defensive exposures–pharma, power, health care, and carefully valued defense stocks–while maintaining exposure to high-quality growth names that can weather near-term volatility. The nuanced takeaway is not to shy away from equities, but to tilt toward sectors with resilient earnings and enough pricing power to weather uneven monsoon seasons.

To navigate these uncertainties, portfolio tilts toward fixed income and cash-like instruments can provide ballast when equities wobble. The goal is not to avoid risk, but to manage it intelligently by creating a structure that can adapt to a shifting rainfall and macro narrative. In this context, Swastika’s research tools, including the Swastika's Sarthi AI stock assistant, can help retail investors drill into stock-specific theses and monitor evolving monsoon-linked dynamics. Swastika's Sarthi AI stock assistant can be a practical companion as you refine portfolio ideas and risk controls.

How To Use This Session Data In Your Portfolio

Given the day’s breadth and the sectoral splits, a practical approach for a retail investor is to build a framework that balances resilience with selective upside capture. Start by evaluating core holdings in consumer staples and defensives, alongside tactical allocations in growth-oriented names that show durable earnings and robust cash generation. Use the 23,800 Nifty support as a mental anchor for risk management: if prices pull back, it could be an opportunity to add quality names with improving earnings visibility and favorable competitive dynamics.

Frequently Asked Questions

How did Sensex and Nifty perform in the latest session?

Sensex gained around 444 points to 76,922.64, and Nifty 50 rose over 140 points to 24,005.85.

What happened to India VIX in today’s session?

India VIX dropped over 3% to 13.19, signaling a softer fear gauge and relatively steadier risk appetite.

Which sectors led gains and which were weaker in this session?

Nifty FMCG gained about 2% and Nifty Realty rose around 4%, while Nifty IT fell by more than 2%.

Which stock movers stood out today, including the zomato share price and others?

Zomato share price rose around 6%, with other noteworthy movers including asian paints stock price (~3%), hindustan unilever limited stock price (~3–4%), nestle india stock price (~3–4%), and dabur stock price (~5%). Tech Mahindra, TCS, and HCL Technologies fell about 3% each.

What should retail investors consider given monsoon uncertainty and global cues?

Investors may consider a portfolio mix that combines fixed income with defensive sectors like health care and power, while staying open to selective growth opportunities. Monitoring rainfall forecasts (monsoon) and global cues (Dow/Nasdaq, crude prices) is important, and tools like Swastika's Sarthi AI stock assistant can help refine ideas and risk controls.

Conclusion

Today’s session illustrates that a broad market rally can coexist with selective sector rotation, especially when monsoon and macro signals create mixed narratives. For the retail investor, the takeaway is to stay nimble, blend defensive ballast with selective growth bets, and rely on disciplined risk controls to weather volatility. As you respond to the zomato share price and other movers, focus on quality earnings, price discipline, and diversification across sectors that historically demonstrate resilience in uncertain monsoon years.

Kajaria Ceramics Buyback: Key Details For Retail Investors

Key Takeaways

- The kajaria ceramics buyback is worth Rs 297 crore and opens on July 3, offering up to 21.50 lakh shares at Rs 1,380 per share.

- It represents 1.35% of equity and carries a premium of over 14% to the last close of Rs 1,210.40.

- Tender forms must be submitted by July 9, with registrar verification by July 13 and final acceptance by July 15; unaccepted shares are returned by July 16.

- The stock price hovered around Rs 1,198.80 on NSE, with a YTD gain of over 25% in 2026 and mixed performance across 1-, 3-, and 5-year horizons.

The kajaria ceramics buyback kicks off on July 3, 2026, with a Rs 297 crore offer to repurchase up to 21.50 lakh shares at Rs 1,380 each, representing roughly 1.35% of the company’s equity. This tender route provides eligible shareholders with a liquidity option while allowing the company to adjust its capital structure. The buyback price marks a premium of more than 14% over the stock’s last close of Rs 1,210.40, setting a clear value proposition for participating shareholders. The combination of size, price, and timing signals a notable event for investors watching how buybacks influence liquidity and price action. The details below reflect the official update and should be interpreted in the context of market dynamics and the company’s broader strategy.

Kajaria Ceramics Buyback: What It Entails For Retail Investors

The buyback value stands at Rs 297 crore, with the total tender size capped at 21.50 lakh shares, representing 1.35% of the company’s equity. The offer is structured on a fixed price basis at Rs 1,380 per share, which is a premium of over 14% to the stock’s prior closing price of Rs 1,210.40. Eligible shareholders can participate only through tenders submitted via stock brokers registered with BSE or NSE. This setup implies that retail investors who hold Kajaria Ceramics shares will need to decide whether to tender a portion or all of their holdings within the tender window to realize the stated price, while other investors may choose to hold and ride on secondary market movements.

Buyback Size, Price, And The 1.35% Stake: What The Offer Covers

In concrete terms, the buyback seeks to acquire up to 21.50 lakh shares, equal to about 1.35% of the company’s outstanding equity. At Rs 1,380 per share, the total payoff to participating shareholders depends on the number of shares tendered and accepted. The 1.35% scope is modest relative to total equity but meaningful for float adjustment and liquidity. The premium versus the last close (Rs 1,210.40) reinforces the offer’s attractiveness from a price perspective, even as market dynamics and liquidity conditions can influence actual post-buyback price behavior. Investors should weigh the impact on their cost of capital and the potential for short-term price movement as the buyback progresses.

Tender Timeline, Dates You Must Track, And The Process To Tender

The tender window runs from July 3 to July 9, 2026. The record date for eligibility to participate is June 29. Tender forms must be submitted by July 9, and registrar verification is scheduled for July 13. Final acceptance or rejection of tendered shares will be communicated to stock exchanges by July 15, with unaccepted shares to be returned to shareholders by July 16. Eligible participants are reminded that the tender route is the prescribed method for acceptance, and all activities must be coordinated through registered stockbrokers with BSE or NSE. The sequence of dates creates a structured path for investors to work through, from decision to execution to settlement.

Market Context: Kajaria Ceramics Stock Price And Performance Trends

On NSE, the kajaria ceramics stock price was around Rs 1,198.80 per share on Wednesday afternoon, reflecting a slight decline of about 1% during that trading session. Over the past week, the stock has posted marginal losses, while it recorded a roughly 10% gain over the last month. Year-to-date performance stands out, with a rise of more than 25% in 2026 so far. Looking back at longer horizons: the stock gained over 12% in the last year, fell 4% over three years, and delivered about 22% returns over the last five years. These figures provide a multi-period context for evaluating the buyback against the stock’s broader price trajectories and volatility. Investors should consider how the buyback interacts with the existing trend line and whether any near-term price strength or consolidation could accompany the tender window.

What Retail Investors Should Do Next

Retail investors should start by aligning the buyback offer with their cost basis, liquidity needs, and view on Kajaria Ceramics’ longer-term business trajectory. If you already hold a stake and prefer to realize part of your gains at Rs 1,380 per share, the tender route offers a clear exit mechanism. Conversely, if you anticipate continued upside in the business fundamentals or believe the stock’s market price could extend the premium, you may opt to hold. It’s important to consider the buyback’s potential impact on share count, earnings per share, and liquidity. For deeper analysis and stock-specific research, you can explore Swastika's Sarthi AI stock assistant: Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What is the size and value of Kajaria Ceramics' buyback?

The buyback is worth Rs 297 crore and covers up to 21.50 lakh shares, representing 1.35% of the company's equity.

What is the buyback price and premium versus the last close?

The buyback price is Rs 1,380 per share, which is a premium of more than 14% to the last close of Rs 1,210.40.

What are the tender dates and key milestones for the Kajaria Ceramics buyback?

Tender window opens July 3 and closes July 9. Record date is June 29. Registrar verification is by July 13. Final acceptance or rejection will be communicated to stock exchanges by July 15, and unaccepted shares will be returned by July 16.

How can investors participate in the buyback?

Eligible shareholders must tender via stock brokers registered with BSE or NSE. The offer is through the tender route.

What recent price and performance context surrounds Kajaria Ceramics stock price during the buyback period?

The kajaria ceramics stock price on NSE was around Rs 1,198.80 per share on Wednesday afternoon, with the stock showing marginal losses over the past week but a 10% gain in the last month. Year-to-date performance is over 25% in 2026; the 1-year return is over 12%, the 3-year return is -4%, and the 5-year return is +22%.

Conclusion

In practical terms, the kajaria ceramics buyback represents a calculated cross-section of liquidity provision and equity strategy. It offers a defined exit at Rs 1,380 per share for participating shareholders, within a Rs 297 crore framework, and the tender window runs July 3–9 with related milestones through mid-July. Retail investors should weigh this immediate liquidity option against potential longer-term upside and the stock’s price behavior in a moving market environment.

Axis Bank Share Price Outlook: Fundraising Signals And Market Crosswinds

Key Takeaways

- Axis Bank raised $500m AT1 and $300m Senior Notes under its Global Medium Term Note Programme, signaling strong access to capital.

- Ayana Renewable Power won a 193 MW wind project at a tariff of ₹4.17 per unit, highlighting renewable capacity expansion.

- RailTel secured a ₹107.60 crore MPLS VPN order for 60 months, indicating steady recurring revenue potential.

- Max Healthcare expanded in Pune by acquiring Yerawada Properties Pvt Ltd to build a 450-bed hospital, signaling regional growth.

In an era of rising capital needs for Indian banks and infrastructure players, Axis Bank's latest overseas fund-raising isn't merely a debt story–it's a signal about liquidity, growth opportunities, and risk management that could influence the axis bank share price. Retail investors should watch how the bank deploys these funds alongside parallel moves from Ayana Renewable Power's wind project, RailTel's VPN contract, and Max Healthcare's Pune expansion to gauge the likely path of returns and risk in the sector. This analysis uses the latest corporate moves across sectors to map potential outcomes for your portfolio. For deeper, AI-driven stock insights, Swastika's Sarthi AI stock assistant is available here: Swastika's Sarthi AI stock assistant.

TLDR

- Axis Bank raised $500m AT1 and $300m Senior Notes under its Global Medium Term Note Programme, signaling strong access to capital.

- Ayana Renewable Power won a 193 MW wind project with a tariff of ₹4.17 per unit, underscoring renewable expansion dynamics.

- RailTel secured a ₹107.60 crore MPLS VPN order for 60 months, indicating revenue visibility in public IT networks.

- Max Healthcare expanded in Pune by acquiring Yerawada Properties Pvt Ltd to build a 450-bed hospital, signaling regional growth and scale.

| Company / Event | Key Detail | Value / Scope |

|---|---|---|

| Axis Bank | Overseas note fundraising | $500m AT1; $300m Senior Notes |

| Ayana Renewable Power (NTPC Green Energy subsidiary) | 193 MW wind project win | Tariff ₹4.17 per unit |

| RailTel | MPLS VPN order from Mahanadi Coalfields | ₹107.60 crore; 60 months |

| Max Healthcare | Pune expansion via Yerawada Properties | 450-bed hospital plan |

| Muthoot Microfin | Non-convertible debentures | Up to ₹3,000 crore private; up to ₹1,000 crore public (FY27) |

| Rane (Madras) | Friction business acquisition | Enterprise value ₹370 crore |

| Power Finance Corporation | Transfer of SPV | ₹20.51 crore; Kakinada green H2 & ammonia transmission |

| Newgen Software Technologies | Retail loan origination LOA | $1.71 million |

| DCM Shriram | Industrial salt companies acquisition | Four units |

| H.G. Infra Engineering | Acquisition of WR ER Part C Power Transmission | 100% equity |

| IPO Listings | Waterways Leisure Tourism & Advit Jewels | Listing scheduled |

Beyond the numbers, some names to watch include_ntpc share price_ trajectory as India continues to push for renewable capacity and grid stability. The bank of maharashtra share price narrative may hinge on how efficiently the ₹7,500 crore fund raise is deployed to grow high-margin revenue and improve asset quality. For investors who track infrastructure and IT-enabled services, the railtel stock story offers a window into public-sector project execution, while the max healthcare stock narrative captures the scaling of private healthcare facilities in tier-1 cities. Each of these pieces feeds into a broader market view: capital is moving toward assets with durable cash flows, regulatory clarity, and scale advantages. Axis Bank's share price, while still influenced by macro factors, will likely respond to the quality of deployment of these funds and the evolving risk profile in the financial sector.

Upcoming catalysts to track: Axis Bank's use of these notes, NAV improvement from renewable projects like the Ayana wind project, and the margin trajectory in RailTel's MPLS VPN work will shape the axis bank share price and peers' trajectories over the next 6–12 months. The Muthoot Microfin debenture programme and DCM Shriram's salt-manufacturing expansion are reminders that non-banking financials and commodities players can offer diversified risk/return profiles in a volatile macro backdrop. In the period ahead, keep a close watch on the execution milestones of the Pune hospital project by Max Healthcare and the Kakinada transmission initiative by Power Grid to gauge potential cross-sector contagion in equity markets.

Frequently Asked Questions

What fundraising instruments did Axis Bank use to raise funds, and what were the amounts?

Axis Bank issued $500 million of 6.875% Additional Tier-1 Notes and $300 million of 5.348% Senior Notes under its $5 billion Global Medium Term Note Programme.

Which wind project did Ayana Renewable Power win and what is the tariff per unit?