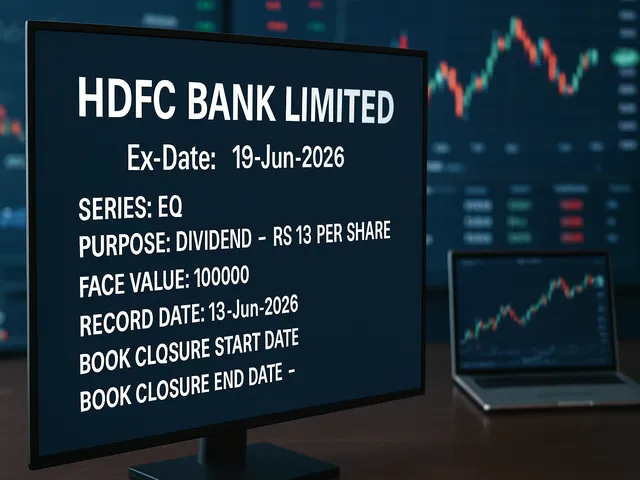

HDFC Bank Limited - Ex-Date: 19-Jun-2026

Quick Takeaways

• HDFC Bank announces a Rs 13 per share dividend for the EQ series with ex-date and record date on 19-Jun-2026.

• Ex-date explains eligibility: ownership before 19-Jun-2026 qualifies for the payout.

• Dividend yield depends on the stock price and may affect short-term price movements around the ex-date.

• Book closure dates aren’t specified in the notice; verify timings through official filings and exchanges.

HDFC Bank Dividend Alert: Rs 13 Per Share Ex-Date 19-Jun-2026

Overview of the announcement

HDFC Bank has announced a dividend on its equity shares for the series EQ, with a payout of Rs 13 per share. The ex-date and the record date are both set for 19 June 2026. The notice lists the face value as Rs 100,000 per share, a nominal value used in regulatory filings. No book-closure dates are specified in the notice, so investors should verify the final dates with the exchange or the bank's investor relations portal. This dividend reflects the bank's ongoing practice of returning capital to shareholders at regular intervals, a common feature among large Indian lenders.

What ex-date means and why it matters

Ex-date is the key cutoff for eligibility. If you buy shares on or after the ex-date, you will not receive the declared dividend for this cycle. Those who hold shares before the ex-date qualify for the payout, subject to being registered as a shareholder on the record date. On or around the ex-date, the stock price often adjusts downward to reflect the impending dividend, though market moves can overshadow this adjustment. The record date confirms who is entitled to receive the dividend, and in this case it is 19 June 2026. For investors, understanding these dates helps avoid missing out on expected income and ensures correct settlement timing across brokers and exchanges.

Dividend yield and portfolio impact

The Rs 13 per-share dividend provides a clear income component, but the realized benefit depends on the share price at the ex-date. Yield is calculated as annual dividend divided by the market price, so higher prices reduce the percentage yield and lower prices increase it, all else equal. Remember that total return includes price movement and taxes, not just the dividend amount. This means a stock could deliver a modest dividend but strong price appreciation, or vice versa, influencing overall performance. For those comparing dividend opportunities, it helps to look at historical payout consistency and the longer-term trend in the stock's returns rather than a single payout event.

Yield calculation basics

As a simple illustration, if a share trades around Rs 6,000 and pays Rs 13 in annualized dividend, the nominal yield from this payout is about 0.22% before tax and after price effects are considered. That figure would change with the actual trading price on the ex-date. In practice, many investors weigh such dividends against alternative income options and volatility risk, while also considering how the dividend aligns with their investment horizon and risk profile.

Practical steps for investors

To qualify for the Rs 13 dividend, you should hold HDFC Bank shares before the ex-date of 19 June 2026 and remain registered on the record date. If you acquire shares on or after the ex-date, you would typically miss this payout. Since the notice does not provide book closure dates, it is wise to confirm the exact timeline from official filings or the exchange. Aligning trading plans with corporate actions helps ensure you receive expected income without disrupting other parts of your strategy.

For retail investors, platforms like Swastika Investmart provide research snippets and market updates that help track corporate actions such as dividends. These resources can simplify understanding of when payouts are expected and how to position your portfolio accordingly. By staying informed, investors can avoid missing out on eligible dividends due to timing issues.

It is also worth noting the tax implications of cash dividends. In India, dividend incomes are generally taxable as part of total income, and tax treatment can vary across regimes and years. Investors should consult a tax advisor to understand how the Rs 13 per share payout fits into their personal tax situation and overall investment plan.

Tax considerations and corporate actions

Dividend payments are a form of shareholder value distribution and are distinct from capital gains. Regulatory filings and exchange notices remain the most reliable source for payout timing and any related corporate actions, including changes in capital structure or shareholder registers. Keeping an eye on these sources can help investors adjust expectations and avoid surprises around payout timing or eligibility.

Conclusion

The Rs 13 per share dividend for HDFC Bank, with ex-date and record date lined up for 19 June 2026, provides a defined income event for shareholders. While the headline amount is straightforward, the real takeaways include understanding eligibility, the interaction with stock price on the ex-date, and how this payout fits into a broader investment plan. Staying informed through official channels and reliable market updates supports a disciplined approach to dividend investing.

Frequently Asked Questions

What is the ex-date for HDFC Bank's dividend?

The ex-date is 19 June 2026, which determines who qualifies to receive the Rs 13 per share dividend.

How much dividend is being paid per share?

Rs 13 per equity share for the series EQ.

Why is the record date important?

The record date identifies shareholders who are eligible to receive the dividend; you must be registered as a holder by the record date.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

Infosys Shares in Focus After 10% ADR Surge: What to Expect in Indian Markets

Key Takeaways at a Glance

- Infosys ADR surged nearly 10% in US trading, boosting investor sentiment

- ADR movements often influence early trade cues for Indian IT stocks

- Positive global cues could support Infosys shares in Indian markets

- Fundamentals, guidance, and global tech spending remain key drivers

- Long-term investors should focus on earnings visibility, not just ADR moves

Infosys Shares in Focus After 10% ADR Surge: What to Expect in Indian Markets

Infosys shares are back in the spotlight after the company’s American Depository Receipts surged nearly 10% in US trading. Such sharp moves in ADRs often grab investor attention, especially when domestic markets are closed. For Indian investors, the big question is whether this rally will translate into momentum for Infosys shares on Dalal Street.

ADR movements can influence sentiment, but they are not the sole factor shaping stock performance. Understanding the reasons behind the surge and its likely impact on Indian markets is crucial for making informed investment decisions.

What Triggered the Surge in Infosys ADR?

Infosys ADRs trade on US exchanges and typically reflect how global investors perceive the company. A sharp rise usually points to improved sentiment, triggered by factors such as earnings expectations, sectoral tailwinds, or broader market rallies.

In this case, optimism around global technology stocks, easing concerns over US interest rates, and renewed confidence in IT spending cycles have played a role. Large-cap IT companies like Infosys often benefit when global funds rotate back into technology after periods of caution.

ADR gains also reflect expectations of stable revenue visibility and margin resilience, especially at a time when global enterprises are selectively increasing digital transformation spends.

How ADR Movements Affect Infosys Shares in India

ADR prices act as an overnight indicator for Indian markets. While they do not guarantee identical price movement, they often influence opening sentiment.

Early trade cues

A strong ADR performance usually leads to positive cues during pre-market sessions in India. Traders and short-term participants closely track ADR premiums or discounts to anticipate opening gaps.

Currency and valuation impact

ADR prices are dollar-denominated, while Infosys shares trade in rupees. Exchange rate movements can amplify or moderate the impact of ADR gains on domestic prices.

Not a standalone trigger

It is important to note that ADR rallies do not override domestic fundamentals. Indian market participants eventually align stock prices with earnings, guidance, and management commentary.

Current Market Context for Indian IT Stocks

The Indian IT sector has seen mixed sentiment over the past year. While long-term digital demand remains intact, short-term challenges such as delayed client spending, pricing pressure, and cautious global outlook have weighed on valuations.

However, recent signs suggest stabilisation.

- US inflation data has shown signs of cooling, supporting risk appetite

- Global technology indices have regained momentum

- Large IT companies continue to report strong deal pipelines

Infosys, being one of India’s top IT exporters, is closely linked to global economic trends. A positive ADR move reflects improved confidence in these broader conditions.

What Investors Should Watch Going Forward

Earnings consistency

Infosys has maintained disciplined execution despite global uncertainty. Investors should track quarterly revenue growth, deal wins, and margin trends rather than short-term price spikes.

Management guidance

Forward-looking commentary often matters more than historical numbers. Any improvement in demand outlook or discretionary spending can support sustained upside.

Regulatory and compliance environment

As a SEBI-compliant listed entity, Infosys operates under strict disclosure norms. Transparent communication and governance standards continue to strengthen investor trust, especially among foreign institutional investors.

Broader IT sector movement

Infosys rarely moves in isolation. If peers also see buying interest, it signals sector-wide optimism rather than stock-specific speculation.

Short-Term Trading vs Long-Term Investing

For traders, ADR surges can offer short-term opportunities driven by momentum and sentiment. However, such trades carry higher volatility risk.

Long-term investors should view ADR rallies as confirmation of improving sentiment rather than a reason to chase prices. Sustainable wealth creation in IT stocks depends on earnings growth, return ratios, and competitive positioning.

This distinction is crucial, especially for retail investors navigating fast-moving headlines.

How Swastika Investmart Supports Smarter Decisions

Interpreting global cues like ADR movements requires context and clarity. Swastika Investmart, a SEBI-registered broking and research firm, empowers investors with in-depth analysis, sector insights, and timely market updates.

With strong research tools, technology-driven platforms, responsive customer support, and a focus on investor education, Swastika Investmart helps clients cut through market noise and focus on fundamentals that matter.

Frequently Asked Questions

Why do Infosys ADR movements matter to Indian investors?

ADR prices provide overnight cues on global investor sentiment and can influence early trading in Indian markets.

Does a 10% ADR surge guarantee a similar rise in Infosys shares in India?

No. While sentiment may turn positive, domestic prices ultimately depend on fundamentals, currency movement, and overall market conditions.

Are ADR-based trades suitable for long-term investors?

ADR movements are better suited for short-term sentiment tracking. Long-term investors should focus on earnings and growth visibility.

Is the IT sector entering a recovery phase?

Signs of stabilisation are visible, but a full recovery depends on global economic growth and technology spending trends.

Final Takeaway

The sharp rise in Infosys ADRs has brought the stock back into focus and improved near-term sentiment. While this could support Infosys shares in Indian markets, investors should avoid making decisions based solely on overnight cues.

A balanced approach that considers fundamentals, global trends, and long-term strategy remains key.

If you want expert insights, research-backed recommendations, and a reliable trading platform, consider opening your account with Swastika Investmart today.

India’s Labour Code Reform: Short-Term Pain, Long-Term Gain for IT Sector?

Key Takeaways at a Glance

- India’s labour code reform could raise near-term costs for IT companies due to compliance and benefits alignment

- Large IT firms may absorb the impact better than mid-sized players

- Over time, flexibility in hiring and workforce management could improve productivity

- The reforms may enhance India’s global competitiveness in IT services

- Investors should focus on long-term fundamentals rather than short-term margin pressure

India’s long-awaited labour code reforms are finally inching closer to full implementation. While the intent is to simplify and modernise India’s complex labour framework, the immediate impact on corporate India is mixed. For the IT sector, one of India’s largest employers and foreign exchange earners, the reforms raise an important question. Will labour code reform disrupt margins in the short term, or will it strengthen the sector’s global standing over time?

To answer this, investors need to look beyond headline costs and understand how structural reforms reshape long-term value creation.

Understanding India’s Labour Code Reform

India has consolidated 29 central labour laws into four labour codes. These include the Code on Wages, Industrial Relations Code, Social Security Code, and Occupational Safety, Health and Working Conditions Code.

The objective is clear. Simplify compliance, standardise definitions, improve worker protection, and give employers greater flexibility in workforce management. However, implementation across states remains staggered, adding an element of uncertainty for businesses.

For the IT sector, which employs millions across delivery centres in multiple states, alignment with these codes is not just a legal change but an operational shift.

Why the IT Sector Feels the Immediate Heat

Unlike manufacturing, IT firms already operate in a largely formalised environment. Yet the labour code reform introduces new cost and compliance elements that can impact margins.

Higher social security obligations

The revised definition of wages expands the base on which provident fund and gratuity contributions are calculated. Variable pay, allowances, and incentives may now fall under wage limits.

For large IT firms with thousands of employees, even a small increase in contribution percentages translates into significant absolute costs.

Compliance recalibration across states

IT companies operate delivery centres in Bengaluru, Hyderabad, Pune, Chennai, and Gurugram. Since states are rolling out labour codes at different speeds, firms must manage multiple compliance frameworks simultaneously.

This adds administrative burden and increases legal and HR costs in the short term.

Impact on operating margins

In a sector already facing pricing pressure from global clients, currency volatility, and higher attrition costs, labour reforms add another layer of near-term margin pressure.

Recent quarterly results from leading IT firms have already highlighted rising employee costs as a key concern.

Why Large IT Firms Are Better Positioned

The impact of labour code reform will not be uniform across the sector.

Scale matters

Large-cap IT companies have stronger balance sheets, diversified revenue streams, and established HR systems. They can absorb higher costs without significant disruption to profitability.

Mid-sized IT firms, on the other hand, may face tighter margins, especially those operating on lower billing rates or niche contracts.

Automation as a buffer

India’s top IT companies have already invested heavily in automation, AI, and digital delivery models. Over time, higher labour costs could accelerate this transition, improving productivity per employee.

This shift may initially impact hiring sentiment but strengthens long-term efficiency.

Long-Term Gains That Investors Should Not Ignore

While the short-term pain is real, labour code reform offers several structural benefits for the IT sector.

Workforce flexibility

Simplified rules around hiring, termination, and contract labour can help IT companies align workforce size with project demand. This is particularly important in a sector driven by global business cycles.

Improved formalisation

Standardised wage definitions and social security coverage enhance employee trust and retention. Over time, this can reduce attrition costs, a persistent challenge for Indian IT firms.

Global competitiveness

Multinational clients increasingly focus on ESG compliance, labour standards, and workforce welfare. A modernised labour framework improves India’s credibility as a responsible outsourcing destination.

This strengthens India’s position against competing IT hubs in Eastern Europe and Southeast Asia.

Market Impact and Investor Perspective

From a market standpoint, labour code reform is unlikely to trigger sharp valuation re-rating in the near term. Instead, it acts as a slow-burn structural change.

Short-term stock reactions may reflect margin concerns, especially during result seasons. However, long-term investors should track how efficiently companies adapt their cost structures and leverage productivity gains.

This is where informed research becomes crucial. Understanding which IT firms can convert regulatory change into operational advantage makes a meaningful difference to portfolio outcomes.

Regulatory Context and Policy Direction

The labour code reform aligns with broader policy initiatives such as Make in India, Digital India, and ease of doing business reforms. While IT is not a traditional manufacturing sector, its employment intensity makes it a key stakeholder.

SEBI-regulated research firms and market participants are closely tracking how these reforms influence earnings visibility and capital allocation decisions within the IT space.

How Swastika Investmart Helps Investors Navigate This Shift

Navigating policy-driven sectoral changes requires more than surface-level analysis. Swastika Investmart, a SEBI-registered research and broking firm, provides investors with data-backed insights, sectoral deep dives, and long-term investment frameworks.

With robust research tools, responsive customer support, and a strong focus on investor education, Swastika Investmart helps investors look beyond short-term noise and focus on sustainable value creation.

Frequently Asked Questions

Will labour code reform significantly hurt IT company profits?

The impact is expected to be moderate and front-loaded. Large IT firms can absorb higher costs, while long-term benefits may offset short-term pressure.

Which IT companies are most vulnerable to these reforms?

Mid-sized IT firms with thinner margins and limited automation capabilities may face higher relative pressure.

Does labour reform improve India’s attractiveness for global IT clients?

Yes. Better labour standards and compliance improve India’s ESG profile, which matters to global enterprises.

Is this reform positive for IT employees?

In the long run, expanded social security coverage and standardised wage structures enhance employee benefits and stability.

Final Thoughts

India’s labour code reform is a classic case of structural change. The IT sector may experience near-term discomfort as costs rise and compliance evolves. However, the long-term gains in flexibility, productivity, and global credibility cannot be ignored.

For investors, the key is to stay informed, patient, and selective.

If you want expert insights on how regulatory shifts impact Indian sectors and stocks, consider opening your trading and investment account with Swastika Investmart today.

%20(7)%20(6).avif)

ICICI Lombard Q3 FY26: Profit Slips 9% as Rising Claims Push Combined Ratio Above 105%.

Key Takeaways at a Glance

- ICICI Lombard reported a 9 percent year-on-year decline in profit for Q3 FY26

- Rising claims, especially in motor and health insurance, impacted underwriting performance

- Combined ratio crossed the 105 percent mark, indicating margin pressure

- Long-term growth drivers remain intact despite near-term profitability concerns

ICICI Lombard Q3 FY26: Profit Slips 9% as Rising Claims Push Combined Ratio Above 105%

The ICICI Lombard Q3 FY26 results reflect a challenging quarter for India’s largest private-sector general insurer. While premium growth remained steady, profitability came under pressure as higher claims weighed on margins. Net profit declined by around 9 percent year on year, and the combined ratio moved above the critical 105 percent level, raising concerns among investors about near-term earnings visibility.

For market participants tracking the insurance space, these numbers highlight the fine balance insurers must maintain between growth and underwriting discipline, especially in a competitive environment.

Understanding ICICI Lombard’s Q3 FY26 Performance

Profit Decline Explained

The drop in profit during the quarter was largely driven by an increase in claims across key segments. Motor insurance witnessed higher claim frequencies, while health insurance continued to see elevated medical costs. These trends pushed up the loss ratio, directly impacting underwriting margins.

Although investment income provided some support, it was not enough to fully offset the pressure from rising claims. As a result, overall profitability declined despite stable operating income.

Combined Ratio Crosses 105 Percent

The combined ratio is a crucial metric for general insurers, as it measures underwriting performance by combining claims and expense ratios. A ratio above 100 percent indicates that the insurer is paying out more in claims and expenses than it earns in premiums.

In Q3 FY26, ICICI Lombard’s combined ratio crossed 105 percent, signaling stress on underwriting margins. While this level is not unprecedented during periods of high claims, it does raise questions about pricing discipline and cost control in the short term.

Segment-Wise Trends and Market Context

Motor and Health Insurance Pressures

Motor insurance has seen a gradual increase in claim severity, driven by higher repair costs and rising spare part prices. Health insurance, on the other hand, continues to face inflationary pressures due to increased hospital charges and more frequent claims.

These trends are not unique to ICICI Lombard. The broader general insurance industry in India has been grappling with similar challenges, making underwriting discipline more important than ever.

Competitive Intensity in the Industry

India’s general insurance market remains highly competitive, with private players focusing on growth through pricing and product innovation. While this supports premium expansion, it can also compress margins if claims experience worsens.

ICICI Lombard’s scale and diversified portfolio provide some resilience, but maintaining profitability in such an environment requires careful risk assessment and pricing adjustments.

Regulatory and Industry Factors at Play

IRDAI Oversight and Pricing Discipline

The Insurance Regulatory and Development Authority of India plays a key role in shaping industry practices. Regulatory focus on transparency, solvency, and fair pricing encourages insurers to strengthen their underwriting frameworks.

In recent years, regulatory measures have aimed to promote sustainable growth rather than aggressive price-led expansion. Over time, this could help stabilise combined ratios across the industry.

Long-Term Insurance Penetration Story

Despite short-term volatility, India’s insurance penetration remains relatively low compared to global standards. Rising awareness, increased vehicle ownership, and growing healthcare needs continue to support long-term demand for general insurance products.

For established players like ICICI Lombard, this structural growth offers a strong foundation, even if quarterly earnings fluctuate.

What This Means for Investors

Short-Term Volatility vs Long-Term Fundamentals

From an investor’s perspective, the ICICI Lombard Q3 FY26 results may prompt near-term caution. Elevated combined ratios and profit pressure could weigh on sentiment in the short run.

However, long-term investors often look beyond a single quarter. ICICI Lombard’s strong brand, wide distribution network, and disciplined balance sheet position it well to benefit from industry growth over time.

Importance of Tracking Key Metrics

For insurance stocks, metrics such as combined ratio, loss ratio, and premium growth are as important as headline profit numbers. Investors should monitor whether pricing adjustments and cost controls help improve margins in coming quarters.

Access to structured research and timely insights can make a meaningful difference in such analysis.

Role of Research and Technology in Smarter Investing

Understanding sector-specific nuances requires more than just headline data. Platforms like Swastika Investmart, a SEBI-registered brokerage, support investors with in-depth research, market insights, and advanced trading tools.

With a focus on investor education, technology-enabled investing, and responsive customer support, Swastika Investmart helps investors make informed decisions across market cycles, including sectors like insurance where fundamentals matter more than short-term noise.

Frequently Asked Questions

Why did ICICI Lombard profit fall in Q3 FY26?

Profit declined mainly due to higher claims in motor and health insurance, which increased the combined ratio.

What does a combined ratio above 105 percent indicate?

It suggests that underwriting operations are under pressure, with claims and expenses exceeding premium income.

Is this issue specific to ICICI Lombard?

No, rising claims have affected the broader general insurance industry in India.

Does this impact ICICI Lombard’s long-term outlook?

While short-term profitability is impacted, long-term growth drivers such as low insurance penetration remain intact.

What should investors track going forward?

Investors should watch combined ratio trends, premium growth, and management commentary on pricing and claims control.

Final Takeaway

The ICICI Lombard Q3 FY26 results underline the challenges facing general insurers amid rising claims and competitive pressures. While the combined ratio crossing 105 percent is a concern in the near term, the company’s strong market position and long-term industry tailwinds provide comfort to patient investors.

Staying informed and data-driven is key when evaluating such developments. With its research-backed approach, technology-driven platforms, and strong investor support, Swastika Investmart enables investors to navigate earnings seasons with greater clarity.

If you are looking to track market opportunities more effectively, take the next step today.

Tata Punch 2026 Facelift: Can the New Turbo Engine Redefine the Entry SUV Segment?

Key Takeaways at a Glance

- Tata Punch 2026 Facelift is expected to bring a refreshed design and a new turbo petrol engine

- The upgrade could strengthen Tata Motors’ leadership in the entry-level SUV segment

- Improved performance and features aim to attract younger urban buyers

- Strong product momentum may support Tata Motors’ passenger vehicle growth story

Tata Punch 2026 Facelift: Can the New Turbo Engine Redefine the Entry SUV Segment?

The Tata Punch has been one of the most successful stories in India’s compact SUV space. Since its launch, it has consistently featured among the top-selling cars in the country, appealing to first-time buyers, small families, and urban commuters alike. Now, market buzz around the Tata Punch 2026 Facelift suggests that Tata Motors is preparing to raise the bar once again.

At the heart of this update could be a new turbo petrol engine, a move that may change how buyers view entry-level SUVs. The big question is whether this upgrade is just a cosmetic refresh or a strategic step that could reshape the segment and strengthen Tata Motors’ position in the Indian auto market.

Why the Tata Punch Facelift Matters

A Strong Base to Build On

The current Tata Punch has already proven its appeal with a strong safety rating, practical design, and competitive pricing. It struck a chord with buyers who wanted the SUV look without stretching their budget.

However, customer preferences are evolving. Buyers now expect more power, better technology, and refined driving experiences even in smaller cars. The upcoming facelift is Tata Motors’ opportunity to meet these expectations head-on.

Turbo Engine as a Game Changer

If reports hold true, the Tata Punch 2026 Facelift may feature a turbocharged petrol engine similar to what Tata Motors already offers in other models. For everyday users, this could mean smoother highway drives, quicker overtakes, and a more confident feel behind the wheel.

For a buyer upgrading from a basic hatchback, this performance boost could be a decisive factor.

What to Expect from the Tata Punch 2026 Facelift

Design and Feature Upgrades

While Tata Motors is unlikely to alter the Punch’s core design language, subtle exterior tweaks are expected. These may include revised bumpers, updated lighting elements, and new alloy wheel designs.

Inside the cabin, buyers can expect improvements in infotainment, connected car technology, and comfort features. A larger touchscreen and enhanced driver assistance features could bring the Punch closer to premium offerings without losing its value positioning.

Improved Driving Experience

The introduction of a turbo engine could significantly enhance the driving dynamics. Urban commuters often struggle with underpowered engines during peak traffic or highway merges. A turbocharged option would address this pain point directly.

This aligns well with India’s changing driving patterns, where city dwellers increasingly take weekend highway trips and expect versatility from their vehicles.

Competitive Landscape and Market Impact

Standing Out in the Entry SUV Segment

The entry-level SUV category is one of the most competitive spaces in India. Buyers compare features, mileage, safety, and resale value closely before making a decision.

With the facelift, Tata Motors is likely aiming to create clear differentiation. A turbo engine combined with a strong safety reputation could position the Punch as a more complete package than many rivals.

Impact on Tata Motors Passenger Vehicle Business

From a market perspective, consistent success of models like the Punch strengthens Tata Motors’ passenger vehicle portfolio. This segment has been a key growth driver for the company in recent years, alongside electric vehicles.

A successful facelift could help Tata Motors maintain volumes, protect market share, and improve margins, factors that equity investors closely monitor.

Regulatory and Policy Context in India

Emissions and Safety Norms

Any new engine introduced in 2026 will comply with India’s prevailing emission standards, ensuring alignment with regulatory requirements. Tata Motors has already demonstrated its capability to adapt to stricter norms without compromising performance.

On the safety front, the Punch’s strong crash test credentials have been a major selling point. Maintaining or improving this standard will be critical, especially as safety awareness among Indian buyers continues to rise.

Push for Domestic Manufacturing

The Indian government’s emphasis on local manufacturing supports automakers with strong domestic supply chains. Tata Motors, with its established manufacturing base, is well positioned to benefit from this policy environment.

What This Means for Investors

Auto Sector Momentum

The Indian automobile sector has shown resilience despite economic cycles. Strong demand, improving rural sentiment, and premiumisation trends are shaping long-term growth.

Product upgrades like the Tata Punch 2026 Facelift signal management’s focus on innovation and consumer-centric design, which can positively influence investor confidence.

Tracking Tata Motors Through Research Tools

For investors following auto stocks, staying updated on product launches, sales data, and margin trends is essential. Platforms like Swastika Investmart, a SEBI-registered brokerage, support investors with research-driven insights, advanced trading tools, and dedicated customer support.

Such resources help investors connect product-level developments with broader financial performance.

Frequently Asked Questions

What is new in the Tata Punch 2026 Facelift?

The facelift is expected to bring design updates, enhanced features, and a possible turbo petrol engine.

Will the new Tata Punch be more powerful than the current model?

If a turbo engine is introduced, the Punch will likely offer better performance and improved drivability.

Is the Tata Punch suitable for first-time car buyers?

Yes, its compact size, safety focus, and expected feature upgrades make it appealing for new buyers.

How could the facelift impact Tata Motors stock?

Successful launches can support sales growth and strengthen investor sentiment, though stock performance depends on broader market factors.

Will the Tata Punch remain affordable after the facelift?

Tata Motors is expected to retain competitive pricing while offering added value through features and performance.

Final Thoughts

The Tata Punch 2026 Facelift appears more than just a routine update. With the possibility of a turbo engine and meaningful feature enhancements, it could redefine expectations in the entry SUV segment. For consumers, this means more choice and better performance. For investors, it highlights Tata Motors’ commitment to product-led growth.

If you want to stay ahead of such market-moving developments and explore investment opportunities with confidence, Swastika Investmart offers a robust platform backed by research, technology, and investor education.

Take the next step in your investing journey.

ONGC, Oil India Extend Rally on Rising Crude Prices — Can the Momentum Sustain?

Key Takeaways at a Glance

- ONGC and Oil India stocks are rising in sync with higher global crude oil prices

- Improved realizations and stable cost structures support near-term earnings visibility

- PSU oil explorers benefit directly from crude upcycles, unlike downstream peers

- Sustainability of the rally depends on crude price stability, policy clarity, and global demand trends

Shares of ONGC and Oil India have been on a steady upward move, tracking the recent rise in global crude oil prices. For investors watching India’s energy space, the rally has revived a familiar question. When oil prices move up, upstream PSU stocks tend to outperform. But can this momentum last, or is it another short-term trade driven by volatile commodities?

To answer that, it is important to look beyond daily price action and understand how crude prices, government policy, and global demand dynamics shape the earnings outlook for India’s oil exploration companies.

Why Are ONGC and Oil India Rising Now?

Crude Oil Prices Move Higher

The primary trigger behind the recent rally is the sharp uptick in global crude oil prices. Brent crude has been trading at elevated levels due to a mix of factors including supply discipline by OPEC+, geopolitical tensions in key producing regions, and signs of improving global demand.

For upstream companies like ONGC and Oil India, higher crude prices translate almost directly into better realizations. Unlike downstream oil marketing companies, they do not face price caps on petrol and diesel. This direct linkage often makes upstream stocks early beneficiaries in a crude upcycle.

Strong Link Between Crude and Earnings

Historically, ONGC and Oil India have shown a strong correlation between crude prices and profitability. Even a modest rise in average crude realization can significantly boost operating margins, especially when production costs remain stable.

For example, when crude prices recovered post pandemic, ONGC’s cash flows improved materially despite flat production volumes. Investors tend to anticipate this effect early, which partly explains the recent stock performance.

How Rising Crude Impacts ONGC and Oil India Financials

Revenue and Margin Expansion

Higher crude prices improve topline growth for upstream players without proportionately increasing costs. Exploration and production costs are largely fixed in the short term. This operating leverage works in favour of companies like ONGC and Oil India during an upcycle.

As a result, EBITDA margins typically expand, strengthening balance sheets and improving dividend-paying capacity.

Improved Cash Flows and Capex Visibility

Stronger cash flows allow oil PSUs to fund capital expenditure internally. This is crucial for long-term investors because sustained investment in exploration ensures reserve replacement and production stability.

Oil India, for instance, has been focusing on domestic exploration blocks and enhanced recovery techniques. A favourable crude environment supports these initiatives without stretching leverage.

Indian Market Context and Policy Landscape

Government Policies and Windfall Taxes

One key risk investors track closely is government intervention. India has, in the past, imposed windfall taxes on crude producers when prices surged sharply. While such levies help protect fiscal stability, they can cap upside for upstream companies.

However, recent policy actions suggest a more calibrated approach, with taxes adjusted periodically rather than abruptly. This has improved visibility and reduced regulatory shock for investors.

Strategic Importance of Domestic Oil Production

India imports a significant portion of its crude oil requirement. Domestic producers like ONGC and Oil India play a strategic role in reducing import dependence. This gives them long-term relevance, even if near-term production growth remains moderate.

From a regulatory standpoint, stable policies under the Ministry of Petroleum and Natural Gas continue to support domestic exploration and production activity.

Can the Rally Sustain From Here?

Factors Supporting the Momentum

- Continued firmness in global crude prices

- Stable production levels and cost discipline

- Healthy dividend yields attracting long-term investors

- PSU rerating theme driven by balance sheet improvement

For investors seeking exposure to commodities within the Indian equity market, upstream oil stocks offer a relatively direct play on crude prices compared to diversified energy companies.

Risks That Could Derail the Trend

Despite the positives, risks remain. A sharp correction in crude prices due to global slowdown fears or increased supply could impact sentiment quickly. Additionally, any unexpected increase in windfall taxes or policy changes may limit upside.

Market participants should also watch currency movements, as a stronger rupee can partially offset crude realization gains.

How Retail Investors Should Look at ONGC and Oil India

Trading vs Long-Term Investing

For short-term traders, ONGC and Oil India often work best as momentum plays aligned with crude price trends. For long-term investors, the appeal lies in consistent dividends, improving capital discipline, and strategic relevance.

A balanced approach is to track crude prices along with company-specific updates such as production guidance, capex plans, and policy developments.

Role of Research and Market Tools

Navigating commodity-linked stocks requires timely data and research. This is where platforms like Swastika Investmart add value through structured research, sector insights, and technology-driven investing tools. Being a SEBI-registered broker, Swastika Investmart focuses on informed decision-making rather than speculation.

Frequently Asked Questions

Why do ONGC and Oil India rise when crude prices increase?

Upstream oil companies earn more per barrel when crude prices rise, directly improving revenues and margins.

Are ONGC and Oil India affected by fuel price controls?

Unlike oil marketing companies, upstream players are not directly impacted by petrol and diesel price controls.

What is the biggest risk to these stocks?

A sharp fall in crude prices or higher windfall taxes imposed by the government can impact earnings.

Are these stocks suitable for long-term investors?

They can be suitable for income-focused investors due to dividends, but returns remain linked to commodity cycles.

How do global events impact Indian oil stocks?

Geopolitical tensions, OPEC decisions, and global demand trends directly influence crude prices and, in turn, oil stocks.

Conclusion

The rally in ONGC and Oil India reflects a familiar but powerful theme in Indian markets: rising crude prices boost upstream oil stocks. While the current momentum is supported by global supply dynamics and stable domestic policies, sustainability will depend on how crude prices behave over the coming quarters.

For investors, the key lies in staying informed, balancing risk, and using reliable research tools. With its strong research ecosystem, investor education initiatives, and tech-enabled platforms, Swastika Investmart helps investors navigate such sectoral trends with confidence.

Ready to take the next step in your investing journey?

.avif)

Tata Elxsi Q3 Results: Profit Slumps 45%, Brokerages Flag Downside Risk

Summary

- Tata Elxsi Q3 net profit declined sharply due to a one-time labour law impact

- Revenue and margins showed resilience despite uneven demand

- Brokerages remain divided, with some flagging downside risk due to rich valuations

- Long-term potential exists, but near-term visibility remains muted

Tata Elxsi Q3 Results: Profit Slumps 45%, Brokerages Flag Downside Risk

Tata Elxsi Q3 results have put the spotlight back on valuation concerns within India’s premium engineering and design services space. The Tata Group company reported a sharp year-on-year decline in net profit for the December 2025 quarter, triggering mixed reactions from brokerages and cautious sentiment among investors.

While the headline numbers appear weak, a deeper look reveals a combination of one-time regulatory impact, modest revenue growth, and selective strength across business verticals. For Indian equity investors, this raises an important question: Is Tata Elxsi facing a structural slowdown, or is this a temporary setback in an otherwise strong long-term story?

What Happened in Tata Elxsi Q3 FY26

Net Profit Impacted by One-Time Labour Law Charge

Tata Elxsi reported a year-on-year decline of over 45 percent in consolidated net profit for the third quarter. The primary reason was a one-time exceptional charge linked to the implementation of India’s revised labour codes.

The new labour regulations mandate changes in wage structures, impacting gratuity, provident fund, and employee benefit calculations. This led to a significant accounting adjustment during the quarter. Importantly, this charge is non-recurring and does not reflect a deterioration in core business demand.

However, from a market perspective, headline profit numbers often influence short-term stock sentiment, especially for high-valuation companies like Tata Elxsi.

Revenue Growth Remains Modest but Positive

Revenue from operations grew marginally on a year-on-year basis, reflecting a challenging demand environment for discretionary engineering spends. While growth was not strong, it remained positive, indicating stability rather than contraction.

Sequentially, certain segments showed better traction, suggesting early signs of normalisation after a muted first half of the financial year.

Margin Performance and Operational Trends

Margins Show Sequential Improvement

Despite the profit decline, operating margins improved sequentially. Better utilisation levels, delivery efficiencies, and cost optimisation measures helped support profitability at the EBITDA level.

This highlights Tata Elxsi’s ability to protect margins even during periods of slower revenue growth, a key strength acknowledged by most analysts.

Mixed Performance Across Business Segments

Tata Elxsi operates across transportation, media and communications, and healthcare and life sciences.

- The transportation vertical, especially software-defined vehicles and automotive engineering, showed relative resilience

- Media and communications faced delayed deal closures and cautious client spending

- Healthcare and life sciences remained soft, with recovery expected to be gradual rather than immediate

This uneven segmental performance explains why revenue growth remains muted despite strong long-term sector themes.

What Brokerages Are Saying About Tata Elxsi

Cautious on Valuations

Several brokerages flagged concerns around Tata Elxsi’s valuation. Even after the recent correction, the stock continues to trade at a premium multiple compared to peers in the engineering research and development space.

Some analysts have highlighted potential downside risk of over 20 percent based on current earnings visibility and near-term growth expectations. Their view is that premium valuations require strong and consistent growth, which is currently uneven.

Neutral to Long-Term Constructive Views

Other brokerages have adopted a more balanced stance. They acknowledge near-term headwinds but continue to see long-term opportunity in Tata Elxsi’s positioning across automotive technology, embedded systems, and digital engineering.

The consensus view is not bearish on the business model, but cautious on timing and entry valuations.

Market Context and Impact on Indian IT Stocks

Tata Elxsi’s results come at a time when Indian IT and ER&D stocks are under scrutiny. Global clients are prioritising cost optimisation, delaying large transformation deals, and taking a measured approach to discretionary spending.

In such an environment, companies with premium pricing and niche offerings tend to see slower deal ramp-ups. This has led investors to reassess expectations, especially for stocks that delivered outsized returns over the past few years.

From a broader Indian market perspective, Tata Elxsi’s performance reinforces the theme of selective stock picking rather than sector-wide rallies.

Is Tata Elxsi Still a Long-Term Story

Long-Term Positives Remain Intact

Despite short-term challenges, Tata Elxsi continues to benefit from structural trends such as vehicle electrification, connected devices, and digital healthcare solutions. Its strong parentage, clean balance sheet, and deep client relationships provide stability.

For long-term investors, the company remains a quality play in India’s ER&D ecosystem.

Near-Term Risks Cannot Be Ignored

At the same time, rich valuations, muted visibility in certain segments, and dependency on global discretionary spending create near-term risks. Investors with shorter time horizons may need to be cautious and patient.

How Swastika Investmart Helps Investors Navigate Such Results

Interpreting quarterly results goes beyond headline profit numbers. It requires understanding regulatory changes, sector cycles, and valuation dynamics.

As a SEBI registered brokerage, Swastika Investmart supports investors with in-depth equity research, advanced trading platforms, and dedicated customer support. Through tech-enabled investing tools and continuous investor education, Swastika Investmart helps clients evaluate opportunities objectively, even during volatile earnings seasons.

Frequently Asked Questions

Why did Tata Elxsi Q3 profit fall sharply?

The decline was mainly due to a one-time charge related to the implementation of India’s new labour laws.

Is the labour law impact recurring?

No, the charge is largely one-time and does not affect future quarters in the same manner.

What is the brokerage outlook on Tata Elxsi shares?

Brokerages remain divided, with some cautious due to valuations and others neutral on long-term potential.

Which segment is performing better for Tata Elxsi?

The transportation and automotive technology segment has shown relatively better resilience.

Is Tata Elxsi suitable for long-term investors?

It may suit investors with a long-term horizon and higher risk tolerance, given near-term volatility.

Conclusion: Balance Quality with Valuation Discipline

Tata Elxsi Q3 results underline an important investing lesson: even high-quality companies go through phases of muted growth and regulatory impact. While the long-term story remains intact, valuation discipline and time horizon are critical.

If you are looking to analyse such stocks with expert insights, reliable execution, and ongoing market support, consider investing through Swastika Investmart.

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App