The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

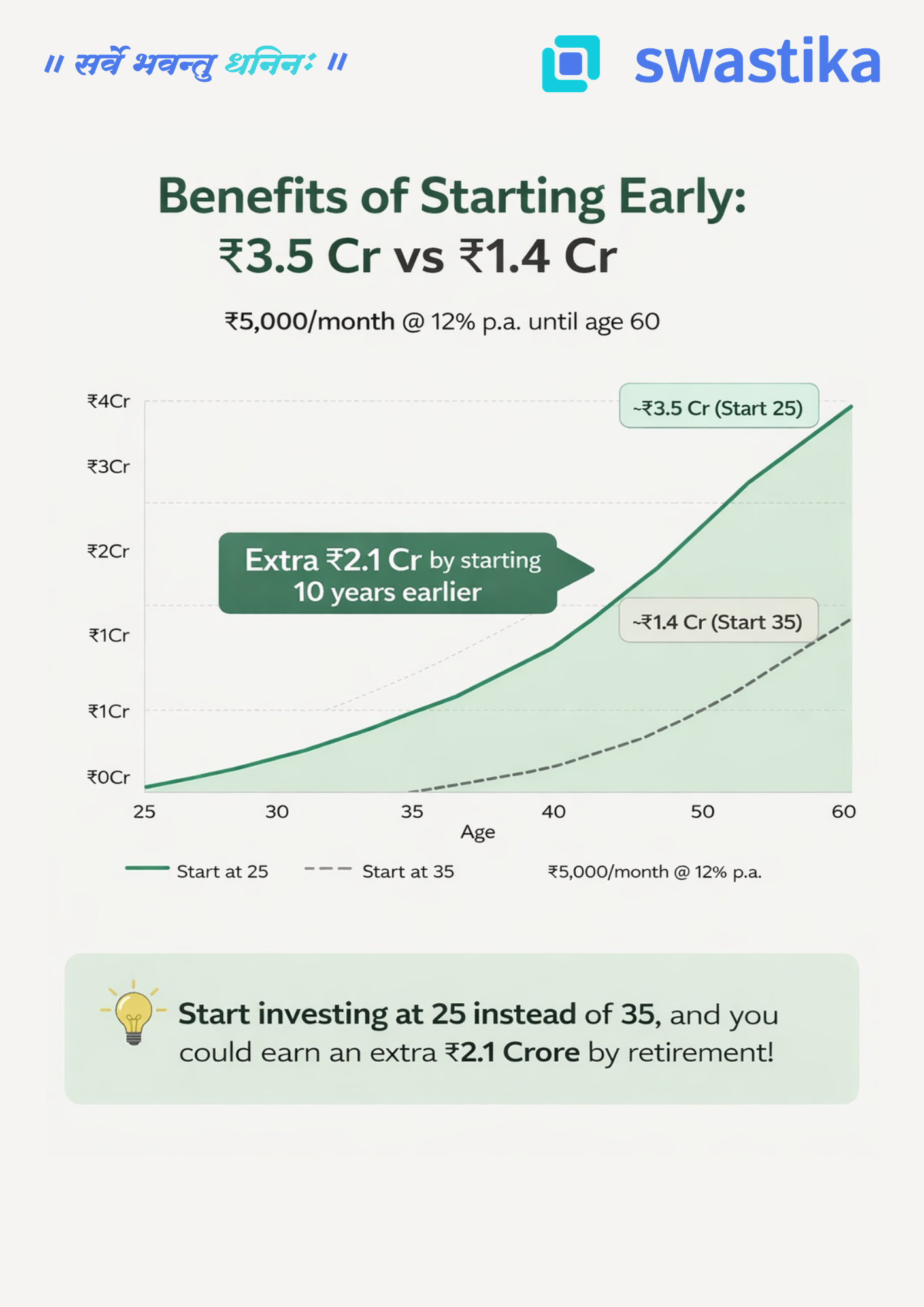

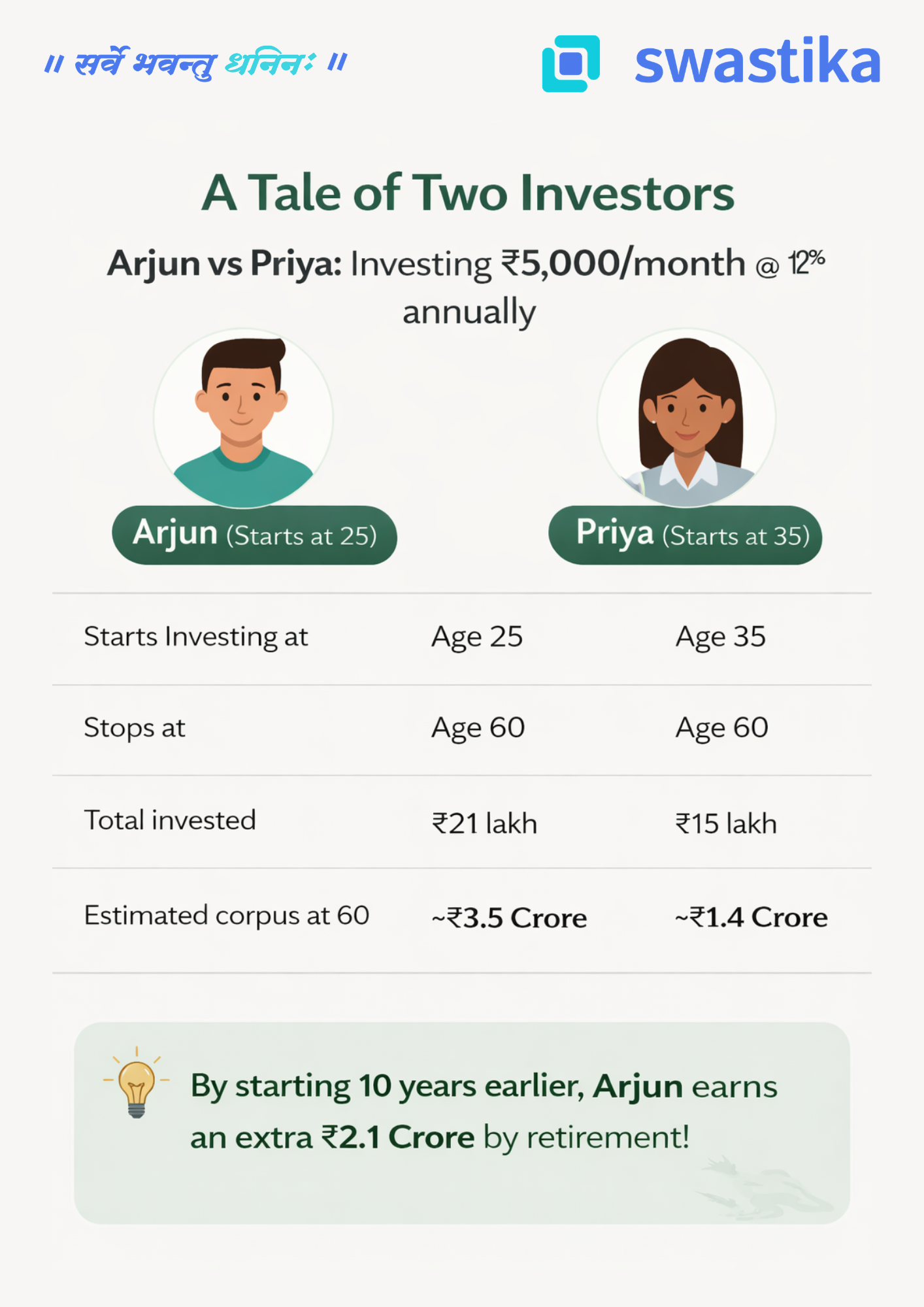

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

Updater Services IPO Date, Price, GMP, Review, Details

Updater Services Limited is an integrated business services platform in India offering integrated facilities management (“IFM”) services and business support services (“BSS”) to its customers, with a pan-India presence.

OBJECTS OF THE ISSUE

- Payment of certain borrowings.

- Funding the working capital requirements. Pursuing inorganic initiatives.

.webp)

Raghunandana Tangirala

Promoter, Chairman and Managing Director of the Company. He is one of the founding directors of the Company and has been on the board since its incorporation. In the Company, he focuses primarily on corporate governance, organizational development, capital allocation and strategic growth of the Company. He has approximately 30 years of experience.

C. R. Saravanan

Director of business operations of the Company. He has been associated with the Company since October 3, 2016. In the Company, he handles the pan India business operations.

Balaji Swaminathan

Chief Financial Officer of the Company. He has been associated with the Company since December 11, 2019. He handles finance & accounts and compliances of the Company. He holds a bachelor’s degree in commerce from University of Madras. He is an associate member of the Institute of Chartered Accountants in India.

Ravishankar B

Company Secretary of the Company. He has been associated with the Company since March 6, 2023. In the Company, he is responsible for secretarial compliances. He holds a bachelor degree in commerce from the University of Madras. He is an associate member of the Institute of Chartered Accountants of India and an associate member of the Institute of Company Secretaries in India.

COMPANY PROFILE

- Updater Services Limited commenced operations in 1990 as a housekeeping and catering services company situated in Chennai, Tamil Nadu.

- Over the years, it has evolved into an integrated business services platform with a pan-India presence serving customers across industries and business service lines.

- In IFM other service segments include Production Support Services, Soft Services, Engineering Services, Washroom and feminine hygiene, Warehouse management, General Staffing, and more. In the BSS segment, the company offers Audit and Assurance services, employee background verification check services, airport ground handling services, sales enablement services, and more through its subsidiaries.

- All these services are B2B services which are primarily in the nature of annuity-based services whereby the customer, once acquired, generates revenue over an extended period of time.

- It served 2,797 customers across various sectors, including certain marquee global and Indian customers.

COMPETITIVE STRENGTHS

- Leading integrated business services platform, operating across diverse segments. Longstanding relationship with customers across diverse sectors leading to recurring business. Track record of successful acquisition and integration of high-margin business segments.

- Pan India presence with a large and efficient workforce. Technology at the forefront of its current and future business.

- Highly experienced Management team with support from PE Investors.

KEY STRATEGIES

- Retain, strengthen, and grow customer base. Grow market share in key segments.

- Introduce new products and services catering to existing and new customer segments. Pursue inorganic growth through strategic acquisitions.

- Continue to improve operating margins.

KEY CONCERNS

- The Company employs a large workforce of 65,627 employees as of June 30, 2023, thus it faces significant employee-related regulatory risks.

- Operational risks, as it provides services in different business environments.

- It witnessed a reduction in its profit in the Financial Year ending March 31, 2023. Any delay or default in receiving payments for services rendered by the Company.

- The Company is exposed to service-related claims and losses or employee disruptions that could have an adverse effect on its business.

- The industries in which it operates are intensely competitive.

- Certain of the services that it offer to its customers are subject to seasonal variations.

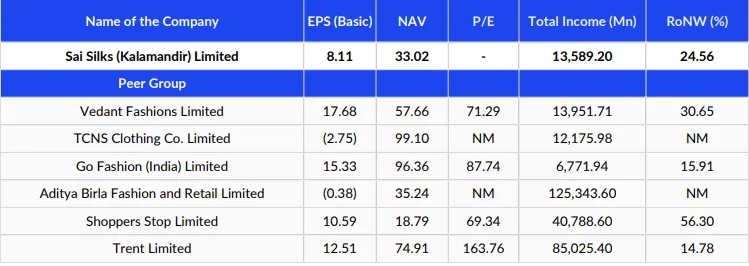

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

...webp)

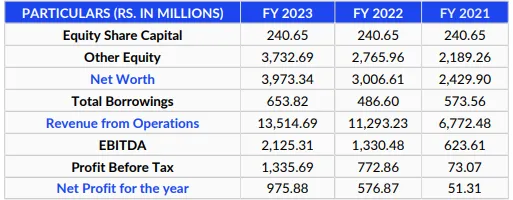

FINANCIALS (RESTATED CONSOLIDATED)

..webp)

OUTLOOK & VALUATION

Updater Services Ltd. (UDS) is a leading business services platform that offers a diverse range of services to customers (B2B) across diverse sectors. The company has a pan-India presence and a large workforce.

The financial performance of the company has been mixed, with growing revenue but declining profit. The company faces certain regulatory and operational risks due to the nature of its business. It is also exposed to service-related claims and losses.

Lastly, the issue is priced at a P/E of 44.3x, which is significantly higher than its listed peers. Thus, considering all the factors, we will avoid this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.in Phone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

उच्च ब्याज दरों से दबाव में सोना।

फेड बैठक के बाद सोने की कीमते सप्ताह के निचले स्तरों पर आ गई, हालांकि कीमतों में गिरावट सीमित रही जबकि चांदी में 2 प्रतिशत की तेज़ी के बाद भाव 73600 रुपये प्रति किलो पर पहुंच गए। पिछले सप्ताह की बैठक में फेडरल रिजर्व ने तब तक दरें बढ़ाने के संकेत दिए है जब तक कि मुद्रास्फीति अपने वार्षिक लक्ष्य 2 प्रतिशत पर वापस नहीं आ जाती। जिसके कारण एमसीएक्स में सोना 0.20 की साप्ताहिक गिरावट के बाद 58800 रुपये प्रति दस ग्राम के स्तरों पर कारोबार करता दिखा। मौद्रिक नीति पर फेड के कड़े रुख के कारण स्पॉट गोल्ड 1950 डॉलर के महत्वपूर्ण स्तरों को पार नहीं कर पाया है जबकि यह महत्वपूर्ण सपोर्ट 1900 डॉलर के ऊपर बना हुआ है। बेंचमार्क अमेरिकी 10-वर्षीय ट्रेज़री यील्ड 4.5 प्रतिशत के शिखर पर पहुंचने के बाद सोने में दबाव बढ़ गया है, जो 2007 के बाद से सबसे अधिक है, और यह बांड बाजार में भारी बिकवाली को दर्शा रहा है। इस बीच, डॉलर इंडेक्स छह महीने के उच्चतम स्तर पर पहुंच गया, जिससे अन्य मुद्राओं के धारकों द्वारा डॉलर में कारोबार करने वाली वस्तुओं की खरीदारी सीमित कर दी है। पिछले सप्ताह फेड की नीति बैठक में सितंबर के लिए दरों को अपरिवर्तित छोड़ने के बावजूद, फेड द्वारा इस साल के अंत तक ब्याज दरों में एक और 0.25 प्रतिशत वृद्धि का अनुमान लगाया है। ब्याज दरों में बढ़ोतरी रोकने के बाद भी उच्च दरें लम्बी अवधि तक बने रहने के संकेत दिए है, जिससे सोने की कीमतों में दबाव बना रह सकता है जब तक की उच्च ब्याज़ दरों के कारण आर्थिक मंदी हावी नहीं हो जाती है।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं के भाव सिमित दायरे में रहने की सम्भावना है। एमसीएक्स अक्टूबर वायदा सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 59500 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 71000 रुपये पर है और रेजिस्टेंस 75000 रुपये पर है।

Manoj Vaibhav Gems 'N' Jewellers Ltd. IPO details

Manoj Vaibhav Gems 'N' Jewellers Limited is a hyperlocal jewelry retail chain with a presence in the micro markets of Andhra Pradesh and Telangana with 13 showrooms (inclusive of two franchisee showrooms) across 8 towns and 2 cities. It has dedicated branded showrooms and has a strong rural market focus and a dedicated urban focus.

OBJECTS OF THE ISSUE

- To Finance the Establishment of the proposed 8 new showrooms.

- General corporate purposes.

Bharata Mallika Ratna Kumari Grandhi

Chairperson and Managing Director of the Company. She has 23 years of experience in jewellery industry, having been associated with the Company since 2001. Her knowledge of jewellery industry has contributed to the growth of the Company.

Currently, she looks after the overall operations and gives strategic directions furthering the growth of the Company.

Grandhi Sai Keerthana

Whole-time Director and CFO of the Company. She has been involved in the areas of marketing, operations and product development of the Company.

Currently, she is involved in managing the finances of the Company.

Mr. Gontla Rakhal

Chief Operating Officer of the Company and is responsible for the operations of the Company. He joined the Company on April 01, 2022. He has an overall experience of approximately 9 years. Prior to joining the Company. he worked as an Assistant Manager-Business Development in Vijay Engifab Private Limited.

Mr Raghunath Jonnavithula

General Manager – Marketing of the Company. General Manager –Marketing of the company. He has an overall experience of approximately 37 years. Prior to joining this Company, he has worked with Cipla Limited and Rexcel Pharmaceuticals Limited.

Mr. Bandari Shiva Krishna

Company Secretary and the Compliance Officer of the Company. He has been associated with the Company since 2014. His primary responsibility is to look after the overall secretarial matters of the Company. He has an overall experience of approximately 13 years.

COMPANY PROFILE

- Vaibhav Jewellers started its jewelry business as a proprietorship concern in the year 1994 from its first retail showroom in Visakhapatnam, Andhra Pradesh.

- It has a market share of ~4% of the overall Andhra Pradesh and Telangana jewelry market and ~10% of the organized market in these two states in FY2023.

- The Company has positioned itself as a retailer focused on ‘Relationships, by Design’ where it focuses on offering designs, high quality, transparency, and customer service to its customers.

- 77% of its retail showrooms are in Tier 2 and Tier 3 cities catering to the semi-urban and rural demand of Andhra Pradesh and Telangana.

- It has designed and developed a website for its online sales in addition to other online marketplaces.

- It procures jewelry on an outright basis from its list of suppliers as well as it supply bullion to job workers for creating varied designs of jewelleries as per its specifications.

COMPETITIVE STRENGTHS

- A key leading home-grown regional brand built on hyperlocal retail strategy. Early mover advantage in the state of Andhra Pradesh.

- Its focus of fortifying its business through Rural Market focus.

- Through its operating ethos of ‘Relationships, by Design’ it offer diverse product designs at varied price range.

- Its go-to-market strategy is its key business enabler thereby providing wider market reach. Experienced promoter and professional senior management team.

KEY STRATEGIES

- Expand in the untapped sections of the micro markets of Andhra Pradesh and Telangana. Focus on further strengthening its rural focus and improving its sales from existing showrooms. Deepen its customer relationships by enhancing focus on its Go-to-Market strategy.

- Focus on augmenting its Brand strength.

- Invest to enhance its product portfolio by offering a wider spectrum of designs.

KEY CONCERNS

- The Company is subject to fluctuations in prices or any unavailability of the raw materials that it uses in its products.

- It has significant working capital requirements.

- It operates in a competitive market and faces competition from other jewelry retailers. The business may be subject to fraud, theft, employee negligence, or similar incidents.

- The current geographic concentration of its operations exposes it to risks related to local economies, and regional downturns.

- The Company does not register its jewelry designs under the Designs Act, 2000 and it may fail to protect its jewelry designs.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

.webp)

FINANCIALS (RESTATED CONSOLIDATED)

.webp)

OUTLOOK & VALUATION

Vaibhav Jewellers is a South Indian-based jewelry retail chain. It has a focus on rural and urban markets, with 13 stores currently. It is also planning to expand with eight new stores. The company offers diverse product designs. and it has reported consistent financial performance.

However, this business is subject to price fluctuations for raw materials and requires high working capital as well.

Secondly, it operates in a very competitive market.

The issue is coming at a P/E valuation of 43.69x which seems fully priced. So considering all these factors and current market sentiments, we will avoid this IPO. One may consider other listed peers for better opportunities.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

Signatureglobal India IPO Date, Price, GMP, Review

Signatureglobal (India) Limited largest real estate development company in the National Capital Region of Delhi (“DelhiNCR”) in affordable and lower mid-segment housing. It has strategically focused on the Affordable Housing (“AH”) segment (below ₹ 4 million price category) and the Middle Income Housing (“MH”) segment (between ₹ 4 million to ₹2.5 million private-category) through GoI and state government policies.

OBJECTS OF THE ISSUE

- Payment of borrowings.

- Infusion of funds in certain of its Subsidiaries. Inorganic growth through land acquisitions.

Pradeep Kumar Aggarwal

Chairman and Whole time Director of the Company. He has over eight years of experience in real estate industry. He has been appointed as a director on the Board of the Company since November 2, 2017.

Lalit Kumar Aggarwal

Vice Chairman and Whole-time Director of the Company. He has an experience of over seven years in the real estate sector. He has been appointed as a director on the Board of the Company since February 15, 2022.

Ravi Aggarwal

Managing Direct of the Company. He is a fellow member of the Institute of Chartered Accountants of India. He has over nine years of experience in the real estate industry. He has been appointed as a director on the Board of the Company since November 5, 2015.

Meghraj Bothra

Company Secretary and Compliance Officer of the Company. He joined the Company on May 2, 2022.He has been admitted as a fellow at the Institute of Company Secretaries of India since November 13, 2011.

Manish Garg

Chief Financial Officer of the Company. He joined the Company on October 17, 2016. He holds a bachelor’s degree in commerce (honors) from the University of Delhi. He has been admitted as an associate member of the institute of chartered accountants of India.

Rajat Kathuria

Chief Executive Officer of the Company. He joined the Company on February 1, 2020. He holds a bachelor’s degree in commerce from the University of Delhi and has passed the final examination conducted by the institute of chartered accountants of India.

COMPANY PROFILE

- The Company commenced operations in 2014 through its Subsidiary, Signature Builders Private Limited, with the launch of its Solera project on 6.13 acres of land in Gurugram, Haryana.

- As of March 31, 2023, it had sold 27,965 residential and commercial units, all within the Delhi NCR region, with an aggregate Saleable Area of 18.90 million square feet.

- Most of its Completed Projects, Ongoing Projects, and Forthcoming Projects are located in Gurugram and Sohna in Haryana, with 88.49% of its Saleable Area located in this region as of March 31, 2023, and almost all of its projects have been, or are being, undertaken under the AHP or the DDJAY -APHP. It has adopted an integrated real estate development model, with in-house capabilities and resources to execute projects from inception to completion which enables it to offer its projects at competitive prices.

- The Company has an extensive distribution network focused on the customer segments it targets, with 593 channel partners and an in-house team of 41 employees engaged in direct sales and 100 employees for indirect sales, as of March 31, 2023.

COMPETITIVE STRENGTHS

- Largest affordable and lower-mid and mid-segment real estate developer in Delhi NCR.

- Well-established brand, strong distribution network, and digital marketing capabilities translate into faster sales.

- Fast growing with the ability to scale up rapidly.

- Ability to provide aspirational lifestyle and amenities at affordable pricing and strategic locations. Standardized product offerings, quick turnaround, and end-to-end in-house project execution expertise. Positive operating cash flows with low levels of debt.

KEY CONCERNS

- The Company has incurred a net loss and negative Net Worth in the past.

- Its business is significantly dependent on the performance of the real estate market in the Delhi- NCR region.

- Changes in government policies may adversely affect its business.

- Significant increases in prices or shortage of or delay or disruption in the supply of, construction materials, contract labor, and equipment could adversely affect its estimated construction cost. Competition from other renowned brands.

- The Company is required to obtain statutory and regulatory approvals and permits to operate its business. Any delay or failure in that may affect the business.

COMPARISON WITH LISTED INDUSTRYPEERS (AS ON 31ST MARCH 2023)

%252C.webp)

FINANCIALS (RESTATED CONSOLIDATED)

%252C.webp)

OUTLOOK & VALUATION

Signature Global is the largest real estate player in Delhi, NCR, operating in affordable and lower-mid-segment housing. It is a well-known brand with a strong distribution network. The company also has large projects on hand.

But it has been a loss-making business for the last few years. Secondly, its major business is focused on a limited region. Changing government policies may also impact its business adversely.

As it has been at a loss, we cannot define its P/E valuation; however, its discounted revenue multiple is 3.48x, which is lower than the industry average. However, due to its current financial condition and other risk factors, we will avoid this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

%2520LIMITED%2520IPO.webp)

SAI SILKS (KALAMANDIR) LIMITED IPO Details

Sai Silks (Kalamandir) Limited is amongst the top retailers of ethnic apparel, particularly sarees, in south India. Through its four store formats, i.e., Kalamandir, VaraMahalakshmi Silks, Mandir, and KLM Fashion Mall as well as through e-commerce channels. It offers its products to various segments of the market including premium ethnic fashion, ethnic fashion for middle income, and value-fashion, with a variety of products across different price points, thereby catering to customers across all market segments.

OBJECTS OF THE ISSUE

- Funding capital expenditure towards setting up 25 new stores and two warehouses.

- Funding the working capital requirements of the company. Payment of borrowings.

KEY MANAGERIAL PERSONNEL

Ravindra Vikram Mamidipudi

Chairman & Independent Director of the Company. He has been a Director of the Company since February 18, 2022. He is a fellow member of the Institute of Chartered Accountants of India. He has approximately four decades of experience in finance sector. He is a partner at M. Anandam & Co., Chartered Accountants since 1981.

Nagakanaka Durga Prasad Chalavadi

Managing Director of the Company. He is also one of the Promoters of the Company and has been associated with the Company since its incorporation. He has more than 16 years of experience in the retail sector and is responsible for the overall management, finance, internal controls and security systems of the Company.

Konduri Venkata Lakshmi Narasimha Sarma

Chief Financial Officer of the Company. He has been associated with the Company since March 1, 2022. He has been associated with the Company since March 1, 2022. He holds a bachelor’s degree in commerce from Osmania University. He is also a fellow member of the Institute of Cost Accountant of India. He has over 35 years of experience in Corporate Finance.

Matte Koti Bhaskara Teja

Company Secretary and Compliance Officer of the Company. He has been associated with the Company since November 5, 2018. He is also an associate member of the Institute of Company Secretaries of India. He has approximately 8 years of experience in secretarial work.

COMPANY PROFILE

- SSKL has a network of 54 stores as of July 31, 2023, in four south Indian states, i.e., Andhra Pradesh, Telangana, Karnataka, and Tamil Nadu.

- It offers a diverse range of products which includes various types of ultra-premium and premium sarees suitable for weddings, and party wear, as well as occasional and daily wear; lehengas, men’s ethnic wear, children’s ethnic wear, and value fashion products comprising fusion wear and western wear for women, men and children.

- It offers one of the widest portfolios of saree SKUs among women’s apparel brands in India with large retail outlets that provide customers with a wide variety of options in ethnic wear across various price points.

- The Company directly purchases the products from the master weavers, weavers, and vendors. It manages its inventory and logistics as well as its entire supply chain for all its channels from four of its warehouses in Karnataka, Andhra Pradesh, Telangana, and Tamil Nadu, and it

COMPETITIVE STRENGTHS

- Among the leading ethnic and value-fashion retail companies in South India.

- Scalable model, well positioned to leverage growth in the ethnic and value-fashion apparel industry in India.

- Strong presence in offline and online marketplace with an omni-channel network.

- Track record of growth, profitability, and unit economics with an efficient operating model. Experienced Promoter, management and in-house teams with proven execution capabilities.

KEY STRATEGIES

- High competition, pricing pressures, and fluctuating demand could hurt sales.

- The company relies heavily on sales in Southern India, which could be affected by adverse developments in the region.

- Maintaining sufficient inventory leads to high costs.

- The company operates in a fragmented market with unorganized competition.

- The company procures products from third-party vendors without long-term agreements. The growth of online retailers and discounting trends could hurt pricing ability.

- Sales are subject to seasonality.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

FINANCIALS (RESTATED CONSOLIDATED)

OUTLOOK & VALUATION

SSKL is the leading ethnic apparel retailer in the southern region of the country, with a network of 54 stores. The company has a strong presence in the offline and online markets with a track record of consistent growth and profitability. It is also strategizing to expand its footprint with a plan to set up 25 new stores.

However, concerns related to high competition, dependency on third-party vendors, regional concentration, and high cost are also there.

The issue is coming at a P/E valuation of around 27.3x, which seems fairly priced. Thus, after checking all the factors, this IPO could be considered for listing gain and long-term holding.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research

Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532

CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

घरेलु मांग बढ़ने के अनुमान से सुधरा सोना-चांदी।

भारत में आमतौर पर कीमती धातुओं की खरीद साल की दूसरी छह माहि में बढ़ती हुई दिखाई देती है। इस बीच, कच्चे तेल के भाव में बढ़त और सोने के इम्पोर्ट में बढ़ोतरी से भारत का ट्रेड बैलेंस -20.7 बिलियन बढ़कर -24 बिलियन हो गया है जिससे डॉलर मजबूत हो कर 83.20 रुपये पर पहुंच गया है। भारत में त्यौहार शुरू होने के पहले सोने का इम्पोर्ट इस साल अगस्त 2022 की तुलना में 40 प्रतिशत अधिक रहने का अनुमान है जिससे सोने और चांदी के भाव को घरेलु मांग का सपोर्ट भी मिल रहा है। जबकि इस साल मानसून कमजोर रहने के चलते मुद्रास्फीति को बल मिल सकता है जो सेफ हैवन मांग बढ़ा सकता है। कॉमेक्स वायदा में सोने और चांदी की कीमतों में दो हफ्तों से चल रहा दबाव फेड बैठक के पहले कम होता दिखाई दिया है। अमेरिकी कंस्यूमर और प्रोडूसर मुद्रास्फीति में हुई बढ़ोतरी मामूली रहने के चलते अनुमान लगाया जा रहा है की फेड इस सप्ताह होने वाली बैठक में ब्याज दरे नहीं बढ़ाएगा। हालांकि, बढ़ती मुद्रास्फीति पर नियंत्रण करने के लिए हॉकिश टिपण्णी, कीमती धातुओं के भाव में बढ़ोतरी की सम्भावना को सीमित कर सकती है। यूरोपियन सेंट्रल बैंक द्वारा पिछले सप्ताह मुद्रास्फीति को स्थिर करने के लिए डिपोसिट रेट में बढ़ोतरी की गई है जबकि चीन द्वारा अपनी अर्थव्यस्था को बढ़ाने और लोकल बैंक को सपोर्ट करने के लिए रिज़र्व आवश्यकता में कटौती की है, जो चांदी की ग्लोबल मांग के लिए अच्छा होगा। इस सप्ताह फेड की बैठक कीमती धातुओं के भाव को नै दिशा है।

तकनिकी विश्लेषण :

इस सप्ताह कीमती धातुओं के भाव में सुधार रहने की सम्भावना है। एमसीएक्स अक्टूबर वायदा सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 59700 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 70000 रुपये पर है और रेजिस्टेंस 74000 रुपये पर है।

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App