NHPC’s ₹26,070 Crore Hydroelectric Project: A Game-Changer for Growth?

Key Takeaways

- NHPC Ltd receives approval for a ₹26,070 crore hydroelectric project

- Project to be developed in partnership with the Arunachal Pradesh government

- Strengthens India’s renewable energy push and hydro capacity

- Long gestation period but strong long-term visibility

- Execution, funding, and timelines remain key factors

Introduction

India’s renewable energy ambitions are gaining momentum, and hydropower is once again coming into focus. In a significant move, NHPC Ltd has received approval for a ₹26,070 crore investment in the Kamala Hydroelectric Project.

This development not only strengthens NHPC’s project pipeline but also signals a broader policy push toward clean and sustainable energy. For investors, the key question is whether this project can truly act as a growth catalyst or if challenges around execution and timelines may limit its near-term impact.

Project Overview

The Kamala Hydroelectric Project will be implemented through a joint venture between NHPC and the Government of Arunachal Pradesh.

Key highlights

- Total investment: ₹26,070 crore

- Location: Arunachal Pradesh

- Structure: Joint venture model

- Objective: Expand hydroelectric capacity

Hydropower projects are capital-intensive and long-term in nature, often taking several years to become operational.

Strategic Importance of the Project

Strengthening Renewable Energy Portfolio

Hydropower plays a crucial role in balancing renewable energy sources like solar and wind. Unlike intermittent sources, hydro provides stable and flexible power.

For NHPC, this project enhances its position as a leading player in India’s renewable energy ecosystem.

Government Policy Support

India has been actively promoting renewable energy through policy initiatives and incentives. Large-scale hydro projects are now being recognized as an essential part of this transition.

Approvals from bodies like the Cabinet Committee on Economic Affairs reflect strong government backing for such investments.

Regional Development

Projects in the Northeast region contribute to:

- Infrastructure development

- Employment generation

- Improved connectivity

This aligns with the government’s broader focus on regional growth.

Impact on Indian Stock Market

Positive Signals for Investors

The project sends a strong message about NHPC’s growth ambitions.

- Expands long-term revenue visibility

- Reinforces leadership in hydro power

- Aligns with India’s clean energy goals

Such developments often improve investor sentiment, especially in PSU and energy stocks.

Sectoral Impact

The announcement may have a broader impact on:

- Renewable energy companies

- Power equipment manufacturers

- Infrastructure and EPC players

As hydro projects scale up, ancillary industries also benefit.

Financial Implications

High Capital Investment

A project of this scale requires significant funding.

- Potential increase in debt levels

- Long payback period

- Gradual revenue realization

Investors should be mindful that returns from such projects are not immediate.

Revenue Visibility

Once operational, hydro projects generate stable and predictable cash flows. This makes them attractive from a long-term perspective.

Risks to Consider

Execution Risk

Large infrastructure projects often face delays due to:

- Land acquisition challenges

- Environmental clearances

- Logistical constraints

Cost Overruns

Inflation in raw materials and delays can increase project costs, impacting profitability.

Regulatory and Environmental Factors

Hydropower projects require multiple approvals and are subject to environmental scrutiny, which can affect timelines.

Real-World Context

Globally, countries are increasingly investing in hydroelectric power as part of their renewable energy mix. In India, companies like NHPC are at the forefront of this transition.

With rising electricity demand and a push for clean energy, hydro projects are expected to play a key role in ensuring grid stability.

Investor Perspective

Short-Term View

- Limited immediate earnings impact

- Possible neutral to mild positive market reaction

Long-Term View

- Strong revenue visibility once operational

- Strategic alignment with energy transition

- Potential for steady cash flows

Investors with a long-term horizon may find such projects attractive.

Regulatory Framework

Projects of this scale operate under strict regulatory oversight. Institutions like the Securities and Exchange Board of India ensure transparency for listed companies, while government approvals add credibility to large investments.

What Should Investors Do?

Investors should take a balanced approach.

- Evaluate NHPC’s overall project pipeline

- Monitor funding strategy and execution progress

- Consider long-term potential rather than short-term gains

Hydropower investments are typically suited for patient investors.

FAQs

What is the size of NHPC’s new project?

The project involves an investment of ₹26,070 crore.

Where will the project be developed?

It will be developed in Arunachal Pradesh through a joint venture.

Is this project positive for NHPC stock?

It is positive from a long-term perspective but may not have an immediate impact on earnings.

What are the key risks?

Execution delays, cost overruns, and regulatory challenges are the main risks.

Should investors invest in NHPC now?

Investors should consider their risk appetite and investment horizon before making a decision.

Conclusion

NHPC’s ₹26,070 crore hydroelectric project reflects a strong commitment to India’s renewable energy future. While the scale of the investment is impressive, the benefits will unfold gradually over time.

For investors, this is not a short-term trigger but a long-term structural story. Tracking execution, funding, and policy developments will be key to understanding the real impact.

Navigating such opportunities requires the right guidance and tools. With SEBI registration, robust research capabilities, advanced technology, and a strong focus on investor education, Swastika Investmart empowers you to make informed investment decisions.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

%2520LIMITED%2520IPO.webp)

SAI SILKS (KALAMANDIR) LIMITED IPO Details

Sai Silks (Kalamandir) Limited is amongst the top retailers of ethnic apparel, particularly sarees, in south India. Through its four store formats, i.e., Kalamandir, VaraMahalakshmi Silks, Mandir, and KLM Fashion Mall as well as through e-commerce channels. It offers its products to various segments of the market including premium ethnic fashion, ethnic fashion for middle income, and value-fashion, with a variety of products across different price points, thereby catering to customers across all market segments.

OBJECTS OF THE ISSUE

- Funding capital expenditure towards setting up 25 new stores and two warehouses.

- Funding the working capital requirements of the company. Payment of borrowings.

KEY MANAGERIAL PERSONNEL

Ravindra Vikram Mamidipudi

Chairman & Independent Director of the Company. He has been a Director of the Company since February 18, 2022. He is a fellow member of the Institute of Chartered Accountants of India. He has approximately four decades of experience in finance sector. He is a partner at M. Anandam & Co., Chartered Accountants since 1981.

Nagakanaka Durga Prasad Chalavadi

Managing Director of the Company. He is also one of the Promoters of the Company and has been associated with the Company since its incorporation. He has more than 16 years of experience in the retail sector and is responsible for the overall management, finance, internal controls and security systems of the Company.

Konduri Venkata Lakshmi Narasimha Sarma

Chief Financial Officer of the Company. He has been associated with the Company since March 1, 2022. He has been associated with the Company since March 1, 2022. He holds a bachelor’s degree in commerce from Osmania University. He is also a fellow member of the Institute of Cost Accountant of India. He has over 35 years of experience in Corporate Finance.

Matte Koti Bhaskara Teja

Company Secretary and Compliance Officer of the Company. He has been associated with the Company since November 5, 2018. He is also an associate member of the Institute of Company Secretaries of India. He has approximately 8 years of experience in secretarial work.

COMPANY PROFILE

- SSKL has a network of 54 stores as of July 31, 2023, in four south Indian states, i.e., Andhra Pradesh, Telangana, Karnataka, and Tamil Nadu.

- It offers a diverse range of products which includes various types of ultra-premium and premium sarees suitable for weddings, and party wear, as well as occasional and daily wear; lehengas, men’s ethnic wear, children’s ethnic wear, and value fashion products comprising fusion wear and western wear for women, men and children.

- It offers one of the widest portfolios of saree SKUs among women’s apparel brands in India with large retail outlets that provide customers with a wide variety of options in ethnic wear across various price points.

- The Company directly purchases the products from the master weavers, weavers, and vendors. It manages its inventory and logistics as well as its entire supply chain for all its channels from four of its warehouses in Karnataka, Andhra Pradesh, Telangana, and Tamil Nadu, and it

COMPETITIVE STRENGTHS

- Among the leading ethnic and value-fashion retail companies in South India.

- Scalable model, well positioned to leverage growth in the ethnic and value-fashion apparel industry in India.

- Strong presence in offline and online marketplace with an omni-channel network.

- Track record of growth, profitability, and unit economics with an efficient operating model. Experienced Promoter, management and in-house teams with proven execution capabilities.

KEY STRATEGIES

- High competition, pricing pressures, and fluctuating demand could hurt sales.

- The company relies heavily on sales in Southern India, which could be affected by adverse developments in the region.

- Maintaining sufficient inventory leads to high costs.

- The company operates in a fragmented market with unorganized competition.

- The company procures products from third-party vendors without long-term agreements. The growth of online retailers and discounting trends could hurt pricing ability.

- Sales are subject to seasonality.

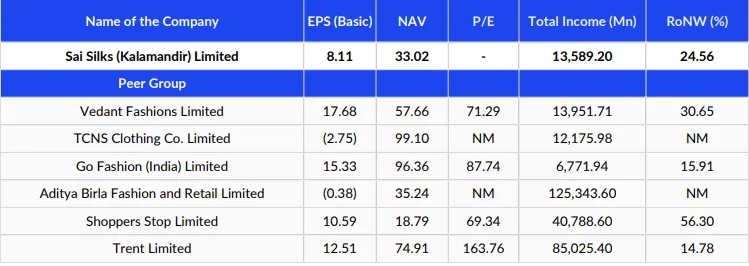

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

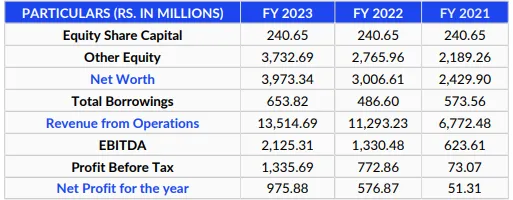

FINANCIALS (RESTATED CONSOLIDATED)

OUTLOOK & VALUATION

SSKL is the leading ethnic apparel retailer in the southern region of the country, with a network of 54 stores. The company has a strong presence in the offline and online markets with a track record of consistent growth and profitability. It is also strategizing to expand its footprint with a plan to set up 25 new stores.

However, concerns related to high competition, dependency on third-party vendors, regional concentration, and high cost are also there.

The issue is coming at a P/E valuation of around 27.3x, which seems fairly priced. Thus, after checking all the factors, this IPO could be considered for listing gain and long-term holding.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research

Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532

CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

घरेलु मांग बढ़ने के अनुमान से सुधरा सोना-चांदी।

भारत में आमतौर पर कीमती धातुओं की खरीद साल की दूसरी छह माहि में बढ़ती हुई दिखाई देती है। इस बीच, कच्चे तेल के भाव में बढ़त और सोने के इम्पोर्ट में बढ़ोतरी से भारत का ट्रेड बैलेंस -20.7 बिलियन बढ़कर -24 बिलियन हो गया है जिससे डॉलर मजबूत हो कर 83.20 रुपये पर पहुंच गया है। भारत में त्यौहार शुरू होने के पहले सोने का इम्पोर्ट इस साल अगस्त 2022 की तुलना में 40 प्रतिशत अधिक रहने का अनुमान है जिससे सोने और चांदी के भाव को घरेलु मांग का सपोर्ट भी मिल रहा है। जबकि इस साल मानसून कमजोर रहने के चलते मुद्रास्फीति को बल मिल सकता है जो सेफ हैवन मांग बढ़ा सकता है। कॉमेक्स वायदा में सोने और चांदी की कीमतों में दो हफ्तों से चल रहा दबाव फेड बैठक के पहले कम होता दिखाई दिया है। अमेरिकी कंस्यूमर और प्रोडूसर मुद्रास्फीति में हुई बढ़ोतरी मामूली रहने के चलते अनुमान लगाया जा रहा है की फेड इस सप्ताह होने वाली बैठक में ब्याज दरे नहीं बढ़ाएगा। हालांकि, बढ़ती मुद्रास्फीति पर नियंत्रण करने के लिए हॉकिश टिपण्णी, कीमती धातुओं के भाव में बढ़ोतरी की सम्भावना को सीमित कर सकती है। यूरोपियन सेंट्रल बैंक द्वारा पिछले सप्ताह मुद्रास्फीति को स्थिर करने के लिए डिपोसिट रेट में बढ़ोतरी की गई है जबकि चीन द्वारा अपनी अर्थव्यस्था को बढ़ाने और लोकल बैंक को सपोर्ट करने के लिए रिज़र्व आवश्यकता में कटौती की है, जो चांदी की ग्लोबल मांग के लिए अच्छा होगा। इस सप्ताह फेड की बैठक कीमती धातुओं के भाव को नै दिशा है।

तकनिकी विश्लेषण :

इस सप्ताह कीमती धातुओं के भाव में सुधार रहने की सम्भावना है। एमसीएक्स अक्टूबर वायदा सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 59700 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 70000 रुपये पर है और रेजिस्टेंस 74000 रुपये पर है।

Zaggle Prepaid Ocean Services IPO Details

Zaggle Prepaid Ocean Services Limited is a leading player in spend management with a diversified offering of fintech and SaaS products and services to corporates. Their SaaS platform is designed for (i) business spend management (including expense management and vendor management); (ii) rewards and incentives management for employees and channel partners; and (iii) gift card management for merchants, which they refer to as customer engagement management system (CEMS).

OBJECTS OF THE ISSUE

- Expenditure towards Customer acquisition and retention.

- Expenditure towards the development of technology and products.

- Payment of certain borrowings availed by the company.

...png)

Raj P Narayanam

Executive Chairman of the Company. He has been on the Board of the Company since April 30, 2012. He completed post graduate diploma in business management with specialisation in finance from the FORE School of Management, New Delhi. He has experience in the technology and fintech industry.

Hari Priya

Company Secretary and Compliance Officer of the Company. She joined the Company on January 18, 2022. Prior to joining this company, she worked with Axis Clinicals Limited as assistant general manager- company secretary, Gayatri Projects Limited as assistant company secretary and Spandana Sphoorty Financial Limited as deputy company secretary and manager– corporate affairs

Avinash Ramesh Godkhind

Managing Director and Chief Executive officer of the Company. He has been on the Board of the Company since May 7, 2012. He holds a bachelors’ degree in engineering from Bangalore University, and a masters’ degree in business administration from the University of Chicago. Prior to this, he worked as an Assistant Vice President at Citibank N.A., India.

Venkata Aditya Kumar Grandhi

Chief Financial Officer of the Company. He joined the Company as vice president-finance and accounts on May 9, 2022 and was promoted as the Chief Financial Officer on August 25, 2022. He is a member of the Institute of Chartered Accountants of India, New Delhi. Prior to joining this Company, he worked at Spandana Sphoorty Financial Limited.

COMPANY PROFILE

- Zaggle Prepaid Ocean Services is a leading player in spend management, with more than 50 million prepaid cards issued in partnership with banking partners and more than 2.27 million users served, as of March 31, 2023’.

- The Company’s network of corporate customers (“Customers”) covers the banking and finance, technology, healthcare, manufacturing, FMCG, infrastructure, and automobile industries, among others. The Company has relationships with brands such as TATA Steel, Persistent Systems, Vitech, Inox, Pitney Bowes, Wockhardt, MAZDA, PCBL (RP – Sanjiv Goenka Group), Hiranandani group, Cotiviti, and Greenply Industries.

- Its core product portfolio includes i) ‘Propel’ (a corporate SaaS platform for channel rewards and incentives, employee rewards and recognition), ii) ‘Save’ (a SaaS-based platform and a mobile application to offer expense management solution), iii) ‘CEMS’ (a customer engagement management system), iv) ‘Zaggle Payroll’ Card (a prepaid payroll card), and v) ‘Zoyer’ (an integrated data-driven, SaaS- based business spend management platform).

COMPETITIVE STRENGTHS

- Differentiated SaaS-based fintech platform, offering a combination of payment instruments, mobile applications, and API integrations.

- In-house developed technology and strong network effect.

- Business model with diverse sources of revenue and low customer acquisition and retention costs. Diversified customer relationships across sectors along with preferred banking and merchant partnerships.

- Seasoned management team with deep domain expertise supported by a professional workforce.

KEY STRATEGIES

- Continue to increase the Customer base of corporate accounts, SMB accounts, start-ups and merchants.

- Continue to scale and expand by increasing user penetration and cross-selling within the existing Customer base.

- Continue to innovate to introduce new products and use cases.

- Leverage strategic partnerships with financial institutions and merchants.

KEY CONCERNS

- The Company is dependent on their relationships with their banking partners, for a substantial portion of their revenue, which is derived from Program Fees generated from their arrangements with such banking partners.

- The Company is dependent on third-party Payment Networks, channel partners, and third-party providers for various aspects of its business and its growth.

- It may encounter challenges with the adoption and usage of the products if it is not able to successfully integrate with other software applications.

- The Company operates in a highly competitive industry.

- It experienced negative operating cash flows in Fiscal 2023 and negative net worth as of March 31, 2022, and March 31, 2021.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

There are no directly listed companies in India, or internationally, whose business portfolio is comparable with that of our business and comparable to Zaggle Prepaid Ocean Services Limited’s scale of operations. Hence, it is not possible to provide an industry comparison in relation to this Company.

FINANCIALS (RESTATED CONSOLIDATED)

...webp)

OUTLOOK & VALUATION

Zaggle Prepaid Ocean Services Limited is a uniquely positioned player in the fintech industry, offering a diversified suite of products and services. The company has a SaaS-based fintech platform and in- house-developed technology. Additionally, the company has diverse sources of revenue and a low-cost operation model.

However, there are some concerns about the company's financial performance. The company has a major dependency on third parties, and it has faced negative cash flow and a decline in its profitability in recent years. Additionally, the company operates in a highly competitive industry.

The IPO is coming at a P/E valuation of 66.6x, which is significantly higher than the valuations of its listed peers. The company's debt-to- equity ratio is also high.

Overall, we believe that the risks outweigh the potential rewards for this IPO. We would avoid investing in this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

SAMHI Hotels IPO: GMP, Details, Price, and More

SAMHI Hotels Limited is a branded hotel ownership and asset management platform in India. SAMHI Hotels has a portfolio of 4,801 keys across 31 operating hotels in 14 of India's key urban consumption centers, including Bengaluru, Hyderabad, National Capital Region (NCR), Pune, Chennai and Ahmedabad, as of March 31, 2023. The company also has 2 hotels under development with a total of 461 keys in Kolkata and Navi Mumbai.

OBJECTS OF THE ISSUE

- Payment of certain borrowings availed of by the company and the subsidiaries.

- General corporate purposes.

.png)

Ashish Jakhanwala

Chairman, Managing Director and Chief Executive Officer of the Company. He has been a member of the Board since December 28, 2010. He has experience in the field of hotel operations, design, consulting and investment

Gyana Das

Executive Vice President and Head of Investments of the company. He joined the Company on February 8, 2011.

Previously, he was associated with Inter Globe Hotels Private Limited.

Sanjay Jain

Senior Director - Corporate Affairs, Company Secretary and Compliance Officer of the Company. He is a member of the Institute of Company Secretaries of India and a member of the Institute of Cost and Works Accountants of India.

Rajat Mehra

Chief Financial Officer of the Company. He joined our Company on December 11, 2012. Previously, he was associated with Religare Corporate Services Limited as an executive vice president finance change management

Tanya Chakravarty

General Counsel of the Company. She joined the Company on May 2, 2017. Previously, she was associated with Phoenix Legal, Vaish Associates Advocates and Unitech Limited

COMPANY PROFILE

- The company has a branded hotel ownership and asset management platform in India, with the third- largest inventory of operational keys.

- Within 12 years of starting business operations, the Company built a portfolio of 3,839 keys across 25 operating hotels in 12 of India’s key urban consumption centers, including Bengaluru, Hyderabad, National Capital Region, Pune, Chennai, and Ahmedabad, as of March 31, 2023.

- Pursuant to the completion of the ACIC Acquisition on August 10, 2023, the company portfolio has further increased to 4,801 keys across 31 operating hotels.

- The company categorizes its hotel portfolio into three distinct hotel segments based on brand classification-Upper Upscale, Upper Mid-scale, and Mid-scale.

COMPETITIVE STRENGTHS

- Company’s ability to acquire dislocated hotels and demonstrated track record to re-rate hotel performance through renovation and/or rebranding.

- The company’s portfolio’s scale and diversification are further enhanced by sector tailwinds. The track record of managing hotels efficiently.

- It’s ability to create operating efficiencies and long-term performance using analytics tools. The company’s has strong governance and seasoned management team.

KEY STRATEGIES

- Its hotels are positioned to benefit from favorable demand trends in the hospitality industry and enhance operating efficiencies.

- Complete development of identified opportunities that are currently under development. Integrate the ACIC Portfolio to drive enhanced performance.

- Pursue growth opportunities via programmatic capital deployment, tactical mergers and acquisitions.

- Ensure disciplined capital allocation and reduction of debt.

KEY CONCERNS

- Business is subject to seasonal and cyclical variations that could result in fluctuations in results of operations.

- A significant portion of revenues are derived from a few hotels and from hotels concentrated in a few geographical regions.

- Company experienced restated losses and negative net worth in recent years.

- The hospitality industry is intensely competitive and company inability to compete effectively may adversely affect business, results of operations and financial condition.

- Company subject to extensive government regulation with respect to safety, health, environmental, real estate, excise and labor laws.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

.webp)

FINANCIALS (RESTATED CONSOLIDATED)

.webp)

OUTLOOK & VALUATION

SAMHI Hotels Limited is a branded hotel ownership and asset management platform in India. The company has a track record of successfully renovating or rebranding hotels to improve performance, and it actively pursues growth prospects through tactical mergers, acquisitions and programmatic capital investment.

SHL, is currently a loss-making hospitality company. The company's financial performance has been poor for the last three years, but it is making progress on cutting losses. But business is subject to seasonal and cyclical variations that could result in fluctuations in the results of operations.

The company is loss-making, so we do not have a P/E ratio. However, its sales multiple is 3.7X, which is below when compared to the industry average. However, as the company is in financial trouble, we won't apply for this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

अमेरिकी डॉलर इंडेक्स में मजबूती से दबाव में सोना-चांदी।

पिछले सप्ताह फेडरल रिजर्व की एक रिपोर्ट से स्पष्ट हुआ है कि जुलाई और अगस्त में श्रम बाजार में सुस्ती और धीमी मुद्रास्फीति के दबाव के बीच अमेरिकी आर्थिक विकास मामूली रहा है, जिससे उम्मीदों को बल मिला कि केंद्रीय बैंक ने ब्याज दरों में बढ़ोतरी या तो कर दी है, या इसके अंत के करीब है। फेड की बीइंग बुक के मुताबिक जुलाई-अगस्त में आर्थिक विकास माध्यम रहा है। टूरिस्म खर्चो में बढ़ोतरी हुई है, जबकि रिटेल स्पेंडिंग में लगातार गिरावट देखने को मिल रही है। मूल्य वृद्धि धीमी हुई है, लेकिन फेड सर्वे के अधिकतर जिलों ने संकेत दिया कि इनपुट कॉस्ट वृद्धि बिक्री मूल्य से कम धीमी है, क्योकि कम होती मांग के कारण व्यापार बढ़ी हुई लागत को बिक्री मूल्य में शामिल करने में असमर्थ है। लेकिन, कच्चे तेल की कीमतों में बढ़ोतरी से मुद्रास्फीति फिर से बढ़ने की सम्भावना है जिससे यह अनुमान है की फेड सितम्बर में होने वाली बैठक में अपना रुख हॉकिश रखेगा। हालांकि, अमेरिका के आर्थिक आंकड़े यह दर्शाते है की अर्थव्यवस्था की स्तिथि अभी बेहतर बनी हुई है और उम्मीद है की आर्थिक मंदी इस साल के लिए टल जाएगी जिससे सुरक्षित आश्रय की मांग कम हुई है। उधर, चीन की अर्थव्यवस्था में सुस्ती, इसके आर्थिक आकड़ो में देखि जा सकती है जिससे अमेरिकी डॉलर के विरुद्ध चीन की मुद्रा में गिरावट देखि जा रही जिससे एशिया की अन्य अर्थव्यवस्थाओं की मुद्रा भी गिरावट की चपेट में आ गई है। यूरोपियन यूनियन की मुद्रा यूरो में डॉलर की तुलना में गिरावट बनी हुई है जिससे छः प्रमुख मुद्राओ का मापक अमेरिकी डॉलर इंडेक्स, में तेज़ी देखने को मिल रही है और कीमती धातुओं के भाव में दबाव बना हुआ है। इस सप्ताह अमेरिका मुद्रास्फीति, रिटेल सेल्स, कंस्यूमर सेंटीमेंट और यूरोपियन सेंट्रल बैंक की मॉनेटरी पॉलिसी, कीमती धातुओं के भाव के लिए महत्वपूर्ण रहेंगी।

तकनिकी विश्लेषण :

इस सप्ताह कीमती धातुओं के भाव सीमित दायरे में रहने की सम्भावना है। एमसीएक्स अक्टूबर वायदा सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 60000 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 68000 रुपये पर है और रेजिस्टेंस 75000 रुपये पर है।

R R Kabel Limited IPO Detail

R R Kabel Limited is one of the leading companies in the Indian consumer electrical industry (comprising wires and cables and fast- moving electrical goods (“FMEG”)), with an operating history of over 20 years in India. They sell products across two broad segments - (i) wires and cables including house wires, industrial wires, power cables, and special cables; and (ii) FMEG including fans, lighting, switches, and appliances.

OBJECTS OF THE ISSUE

- Repayment or prepayment of borrowings availed by the company from banks and financial institutions.

- General corporate purposes.

Tribhuvanprasad Rameshwarlal Kabra

Executive Chairman of the Company. He has completed his secondary level school education from Hindi High School, Mumbai. He has extensive experience in the electrical industry. Previously, he was associated with Shramik Winding Wires Private Limited as a director. He was appointed to RR Kabel’s Board of Directors with effect from May 13, 1997.

Shreegopal Rameshwarlal Kabra

Managing Director of the Company. He has extensive experience in the electrical industry. Previously, he was associated with the International Copper Association as the chairman of wire and cable product council and the Indian Electrical and Electronics Manufacturers’ Association as the president.

Mahendrakumar Rameshwarlal Kabra

Joint Managing Director of the Company. He has extensive experience in the electrical industry. Previously, he was associated with MEW Electricals Limited as a director. He was appointed to the Board of Directors with effect from February 6, 1995.

Rajesh Babu Jain

Chief Financial Officer of the Company. He joined the Company on July 1, 2000 and is responsible for heading the financial functions of the Company including leading various initiatives in the organization of business excellence and operational efficiency of the Company.

Dinesh Aggarwal

Chief Executive Officer of the Company. He joined the Company on December 16, 2022 and is responsible for handling the domestic business administration of the Company.

Himanshu Navinchandra Parmar

Company Secretary and Compliance Officer of the Company. He joined the Company on June 1, 2013 and is responsible for secretarial and legal functions of the Company. Previously, he has worked with MEW Electricals Limited.

Company Profile

- The company manufactures, markets, and sells wires and cables under the RR Kabel brand, and a variety of consumer electrical products, including fans and lights under the ‘RR’ and ‘Luminous Fans and Lights brands.

- RR Kabel was the first company in India to introduce low smoke zero halogens (“LS0H”) insulation technology in their wires and cables products and to introduce unilay core technology products. They have actively diversified and expanded their product portfolio in adjacent areas such as FMEG, both organically and inorganically.

- They have a dedicated team of 60 employees focused on research and development, of which 22 employees exclusively work on research and development involving FMEG products.

- The Company owns and operates two integrated manufacturing facilities which are located at Waghodia, Gujarat, the Waghodia Facility, and Silvassa, Dadra and Nagar Haveli and Daman and Diu (“Silvassa Facility”) in India,

COMPETITIVE STRENGTHS

- Scaled B2C business in the large and growing wire and cables industry. A diverse suite of products with global certifications and accreditations. Extensive domestic and global distribution network.

- Well-recognized consumer brands.

- Technologically advanced and integrated precision manufacturing facilities Well-positioned for growth in the FMEG segment.

- Experienced and committed professional management team.

KEY STRATEGIES

- Expand distribution and establish a leadership position for the wires and cables segment in India. Enhance the geographical footprint of their wires and cables segment.

- Capitalize on the market opportunity in the wires and cables segment. Enhance productivity and operational efficiencies.

KEY CONCERNS

- Increases or fluctuations in raw material prices may have a material adverse effect on the business. Distribution to the overseas market is dependent on a few distributors and significant changes to their business arrangements with these distributors may impact the business.

- The availability of counterfeit products could have an adverse effect on the business and its competitive position.

- They are subject to warranty claims, which may increase in the future and have a material adverse effect on the financial condition.

- The Company faces risks related to foreign currency fluctuations. The company faces significant competitive pressures in the business.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

.webp)

FINANCIALS (RESTATED CONSOLIDATED)

.webp)

OUTLOOK & VALUATION

RR Kabel is a well-established player with strong brand recall and quality products. The company has a diverse product portfolio and an extensive domestic and global distribution network, and it is working on strategies for further enhancement as well. Other than the wire and cable industries, they are also well-positioned for growth in the FMEG segment.

Financial performance has been mixed, where there is growth in revenue and net worth but pressure on its margins with declining profits. The issue size is around 1964 crore, but most of its portion belongs to the offer for sale. Finally, the IPO is coming at a P/E valuation of around 60.5x, which is looking high-priced.

Due to the high valuation and current market sentiments, we will avoid this IPO for listing benefits. However, it could be a good pick for the long term, and investors may consider it during any post-listing correction.

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App