The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

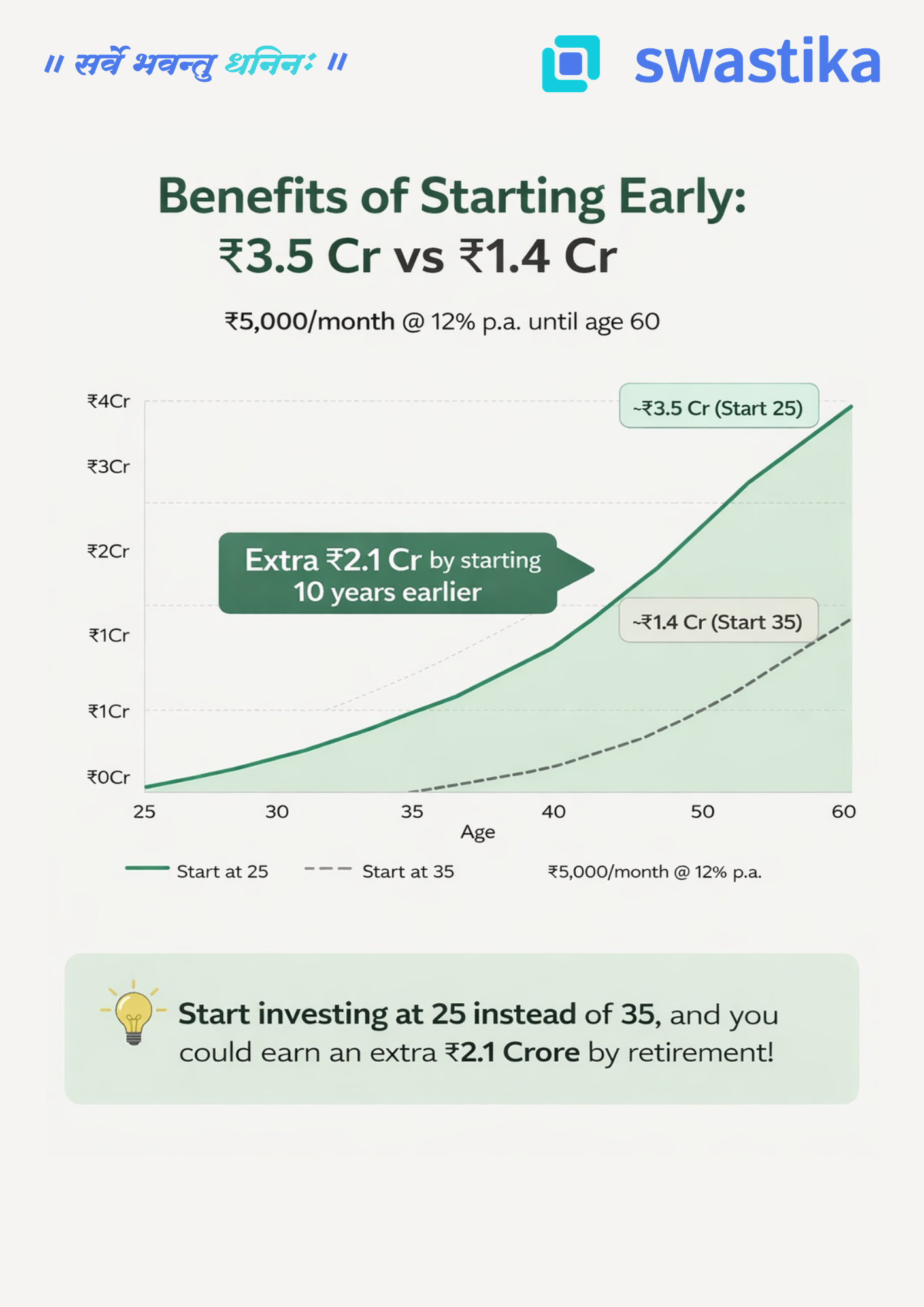

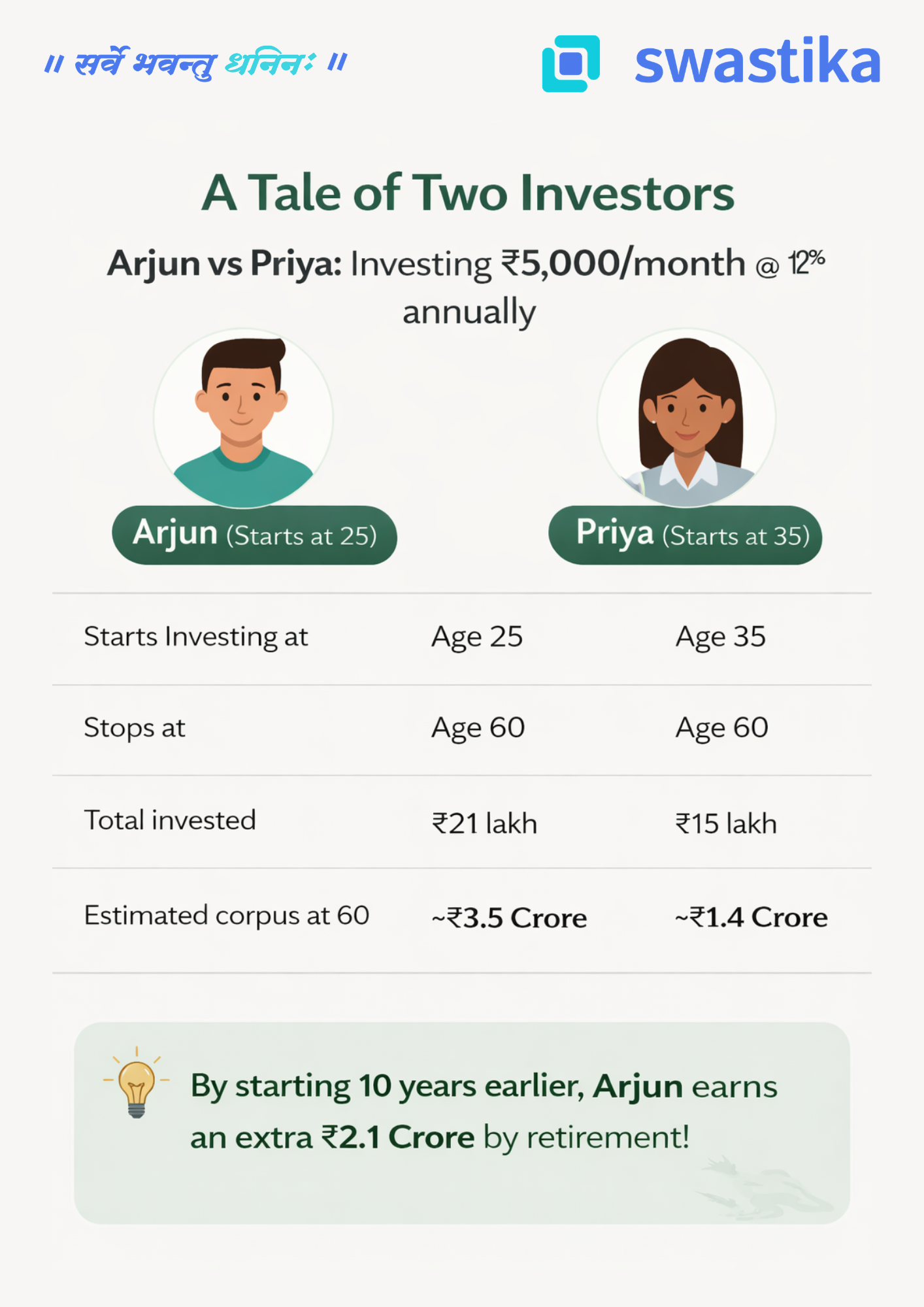

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

National Pension System (NPS): Basics, Features, Advantages, and Disadvantages

National Pension System (NPS)

The National Pension System (NPS) is a government-sponsored retirement savings scheme in India. It was introduced in 2004 and has become increasingly popular among investors looking for a low-cost, long-term savings option for their retirement. In this blog post, we will discuss the basics of NPS, its features, tax benefits, and rules, as well as the advantages and disadvantages of investing in it.

Basics of NPS

The National Pension System is a voluntary, defined-contribution retirement savings scheme that allows subscribers to accumulate savings for their retirement. Under this scheme, subscribers can contribute to their NPS account regularly, and the funds are invested in a mix of equity, debt, and government securities, based on their investment preferences. Upon retirement, subscribers can withdraw a portion of their savings as a lump sum, and the remaining amount is paid out as a monthly pension.

NPS Login

To open an NPS account, subscribers can visit the website of the National Pension System and register themselves by providing their personal and bank details. They can also choose a fund manager and select their investment preferences. Subscribers are given a Permanent Retirement Account Number (PRAN) which is used to manage their account and make contributions. Subscribers can also log in to their NPS account to check their balance, view their transactions, and make contributions.

Features of NPS

The National Pension System offers several features that make it an attractive retirement savings option. Some of the key features include:

- Low Cost: The NPS is a low-cost retirement savings option, with an annual maintenance charge of 0.25% of the account balance, which is significantly lower than other retirement savings options.

- Flexibility: Subscribers have the flexibility to choose their fund manager, investment preferences, and contribution amounts, making it easy for them to tailor their investments to their individual needs.

- Tax Benefits: Subscribers can avail of tax benefits under the NPS, with contributions of up to Rs. 1.5 lakhs per year eligible for tax deductions under Section 80C of the Income Tax Act, and an additional deduction of up to Rs. 50,000 available under Section 80CCD(1B) for the accounting year 2023-24.

- Portability: Subscribers can easily transfer their NPS account from one fund manager to another or from one sector to another, making it easy for them to manage their investments as their needs change.

Rules of NPS

The NPS also has certain rules and regulations that subscribers must follow. For instance, subscribers must contribute regularly to their NPS account, and failure to do so may result in penalties. Additionally, subscribers must keep their contact details and bank account information up to date to ensure that they receive their pension payments in a timely manner.

Advantages of NPS

- Long-term savings: One of the biggest advantages of the National Pension System is that it encourages long-term savings for retirement. This is important because retirement planning requires a long-term perspective and disciplined approach. The NPS, with its tax benefits, low cost, and flexibility, offers an attractive option for investors looking to build a retirement corpus.

- Tax benefits: The NPS offers tax benefits to subscribers, with contributions of up to Rs. 1.5 lakhs per year eligible for tax deductions under Section 80C of the Income Tax Act. Additionally, an additional deduction of up to Rs. 50,000 is available under Section 80CCD(1B). This makes the NPS an attractive option for investors looking to save tax while building a retirement corpus.

- Low cost: The NPS is a low-cost retirement savings option, with an annual maintenance charge of 0.25% of the account balance, which is significantly lower than other retirement savings options. This means that more of the investor's money is invested in the underlying assets, which can help to maximize returns over the long term.

- Flexibility: The NPS offers subscribers the flexibility to choose their fund manager, investment preferences, and contribution amounts, making it easy for them to tailor their investments to their individual needs. This flexibility can help investors to build a retirement corpus that meets their unique requirements.

- Portability: Subscribers can easily transfer their NPS account from one fund manager to another or from one sector to another, making it easy for them to manage their investments as their needs change. This means that investors can make changes to their investments without having to worry about any penalties or fees.

Disadvantages of NPS

- Compulsory Annuity: One of the biggest disadvantages of the National Pension System is that subscribers are required to use at least 40% of the accumulated corpus to purchase an annuity upon retirement. This means that subscribers may not have as much control over their retirement income as they would like.

- Taxation of Withdrawals: While contributions to the NPS are eligible for tax benefits, withdrawals from the NPS are taxable. This means that subscribers may have to pay taxes on the amount they withdraw from their NPS account upon retirement. This can reduce the overall returns that investors receive from their NPS investments.

- Market Risk: The NPS invests in a mix of equity, debt, and government securities, which means that it is subject to market risk. This means that the returns on the NPS investments can vary depending on market conditions, which may not be suitable for investors who are risk-averse.

- Limited Liquidity: The NPS is a long-term investment option, and subscribers are not allowed to withdraw their funds before the age of 60, except in case of certain emergencies. This means that the NPS may not be suitable for investors who require liquidity for short-term goals.

Conclusion

The National Pension System is a popular retirement savings option in India, offering investors a low-cost, flexible, and tax-efficient way to build a retirement corpus. While there are certain disadvantages associated with the NPS, such as compulsory annuity and market risk, the advantages of the scheme outweigh the disadvantages, making it a good option for investors looking to build a retirement corpus over the long term. As always, investors should carefully consider their investment goals and risk tolerance before investing in any financial instrument, including the National Pension System.

.webp)

श्रम बाज़ार में नरमी से तेज़ कीमती धातुए

लगभग दो वर्षों में पहली बार फरवरी में अमेरिकी नौकरियां दस मिलियन से नीचे गई है, यह एक संकेत है कि फेडरल रिजर्व के श्रम बाजार को धीमा करने के प्रयासों का प्रभाव दिखाई देने लगा है। अमेरिकी लेबर डिपार्टमेंट की जोल्ट्स रिपोर्ट में जॉब ओपनिंग घट कर 9.93 मिलियन रह गई जिससे एमसीएक्स जून वायदा सोने के भाव में 2000 रुपये प्रति दस ग्राम और चांदी के भाव में 3000 रुपये प्रति किलो की साप्ताहिक तेज़ी दिखी। फेड द्वारा मई 2022 से शुरू की गई ब्याज दर वृद्धि को अब रोकने के संकेत दिए है क्योकि अमेरिका में मुद्रास्फीति 41 साल के उच्च स्तरों तक पहुंच चुकी थी और इस पर नियंत्रण करने के लिए श्रम बाजार पर फेड का मुख्य टारगेट था। फेड पिछले एक साल में नौ बार ब्याज दरों में बढ़ोतरी कर चुका है जिसका का की कोई खास असर श्रम बाजार में अब तक देखने को नहीं मिला था। हालांकि, ब्याज दर बढ़ोतरी के कारण अमेरिका और यूरोप में आर्थिक मंदी आने की सम्भवना बढ़ गई है जिसका असर अमेरिका के आर्थिक आकड़ो में दिखाई देने लगा है। रिज़र्व बैंक ऑफ़ इंडिया द्वारा अप्रैल की मॉनेटरी पॉलिसी में ब्याज दरों में कोई बदलाव नहीं किया। श्रम बाजार पर बड़ रहे दबाव के चलते यह सम्भावना बढ़ने लगी है की फेड भी आगे ब्याज दरों में बढ़ोतरी नहीं करेगा जिससे कीमती धातुओं में तेज़ी बनी हुई है। अर्थव्यवस्था की विकास गति धीमी होने के कारण कॉमेक्स में सोने के भाव 2036 डॉलर प्रति औंस पर कारोबार कर रहे है, जो 2020 के उच्चतम स्तरों के करीब के भाव है। इस सप्ताह आईएमएफ की बैठक , अमेरिकी सीपीआई, एफओएमसी मीटिंग मिनट्स, रिटेल सेल्स और कंस्यूमर सेंटीमेंट के आंकड़े कीमती धातुओं की चाल पर असर करेंगे।

तकनिकी विश्लेषण:

इस सप्ताह कीमती धातुओं में तेज़ी जारी रहने की सम्भावना है। सोने में सपोर्ट 60000 रुपये पर है और रेजिस्टेंस 61200 रुपये पर है। चांदी में सपोर्ट 72000 रुपये पर है और रेजिस्टेंस 76000 रुपये पर है।

.webp)

Know the Impact of RBI Policy on Stock Market

The Reserve Bank of India (RBI) is the apex banking institution in India responsible for monetary policy formulation and implementation. It aims to maintain price stability and economic growth through various tools and instruments at its disposal. One such tool is the RBI policy, which can have a significant impact on the stock market. In this blog, we will discuss the impact of RBI policy on the stock market and how it affects different asset classes.

Monetary Policy and Equity Markets:

Monetary policy refers to the actions taken by the central bank to manage the money supply and interest rates in an economy. The RBI policy aims to achieve price stability and economic growth through changes in key policy rates, such as the repo rate, reverse repo rate, and the cash reserve ratio (CRR).

The stock market is a reflection of the economy's performance and future prospects. Changes in monetary policy can impact the stock market in many ways. If the RBI decides to tighten monetary policy by raising interest rates, it can lead to a decrease in consumer spending and investment, causing a decline in corporate earnings and ultimately affecting the stock market negatively. Conversely, if the RBI decides to loosen monetary policy by lowering interest rates, it can lead to an increase in consumer spending and investment, resulting in a rise in corporate earnings and potentially boosting the stock market.

Impact of Key Repo Rates on Equity Markets:

The repo rate is the interest rate at which banks can borrow funds from the RBI. The RBI uses the repo rate as a tool to manage inflation and liquidity in the economy. A change in the repo rate can have a significant impact on the stock market.

If the RBI raises the repo rate, it makes borrowing costlier for banks, which can lead to an increase in lending rates for consumers and businesses. This can lead to a decrease in spending and investment, causing a decline in corporate earnings and ultimately negatively impacting the stock market.

On the other hand, if the RBI lowers the repo rate, it makes borrowing cheaper for banks, leading to lower lending rates for consumers and businesses. This can lead to an increase in spending and investment, boosting corporate earnings, and potentially having a positive impact on the stock market.

Impact of Liquidity on the Stock Market:

Liquidity refers to the availability of funds in the economy. The RBI manages liquidity in the economy through various tools such as open market operations (OMOs), CRR, and the statutory liquidity ratio (SLR).

OMOs involve the buying and selling of government securities in the market. When the RBI purchases government securities, it injects liquidity into the market, which can lead to an increase in spending and investment, potentially boosting the stock market.

Similarly, a decrease in the CRR or SLR requirements can also lead to an increase in liquidity in the market. This can lead to an increase in spending and investment, potentially having a positive impact on the stock market.

What happens with Long Term G-Sec Funds?

G-Secs or government securities are bonds issued by the central government to finance its fiscal deficit. These securities are long-term investments that offer a fixed rate of return. The RBI policy can impact G-Sec funds in many ways.

If the RBI decides to tighten monetary policy by raising interest rates, G-Sec funds may offer higher returns, making them a more attractive investment option for investors. This can lead to an increase in demand for G-Secs, causing their prices to rise.

Conversely, if the RBI decides to loosen monetary policy by lowering interest rates, G-Sec funds may offer lower returns, making them a less attractive investment option for investors. This can lead to a decrease in demand for G-Secs, causing their prices to fall.

What about Fixed Income Securities?

The RBI's policies also impact fixed-income securities, such as bonds and government securities. When the RBI lowers interest rates, the yield on fixed-income securities also falls, which can lead to higher demand for the bonds in the market. Conversely, when the RBI raises interest rates, the yield on fixed-income securities increases, which can lead to lower demand for the bonds in the market. Overall, the RBI's policies can impact the returns on fixed-income securities, making them an important consideration for investors seeking stable returns.

Table showing the Impact of RBI policy on the Stock Market

Area

Changes in Policy

Impact

Tentative Impact on Stock Market

Repo Rate

Increase in repo rate: Increase in borrowing cost, decrease in stock prices.

Decrease in repo rate: Decrease in borrowing cost, increase in stock prices.

Reverse Repo Rate

Increase in reverse repo rate: Decrease in liquidity, decrease in stock prices.

Decrease in reverse repo rate: Increase in liquidity, increase in stock prices.

Cash Reserve Ratio

Increase in the cash reserve ratio: Decrease in liquidity, decrease in stock prices.

Decrease in the cash reserve ratio: Increase in liquidity, increase in stock prices.

Statutory Liquidity Ratio

Increase in statutory liquidity ratio: Decrease in liquidity, decrease in stock prices.

Decrease in statutory liquidity ratio: Increase in liquidity, increase in stock prices.

Open Market Operations

Purchase of securities by RBI from the market: Increase in liquidity, increase in stock prices.

Sale of securities by RBI to the market: Decrease in liquidity, decrease in stock prices.

Inflation Targeting

Increase in interest rates: Decrease in borrowing and spending, decrease in stock prices, and a slowdown in economic growth.

Decrease in interest rates: Increase in borrowing and spending, increase in stock prices, and boost in economic growth.

Fiscal Policy

Increase in government spending and decrease in taxes (Expansionary): Increase in economic growth, increase in stock prices.

Decrease in government spending and increase in taxes (Contractionary): Decrease in economic growth, decrease in stock prices.

Note: The above chart represents the general impacts of RBI policy changes on the stock market, and actual impacts may vary depending on various factors and market conditions.

A Beginner's Guide to Alternative Investment Funds and Their Three Categories

What are Alternative Investment Funds?

Alternative Investment Funds (AIFs) are privately pooled investment vehicles that collect funds from sophisticated investors, both Indian and foreign and invest in accordance with a defined investment policy for the benefit of their investors. The Securities and Exchange Board of India (SEBI) regulates the AIFs, which are categorized into three categories based on their investment strategies and levels of risk. In this article, we will discuss the three categories of AIFs in detail.

Category 1 AIFs

Invest in start-up or early-stage ventures, social ventures, SMEs, infrastructure, or other sectors or areas that the government or regulators consider socially or economically desirable. They are typically long-term investors, and the funds raised are used to provide capital to such ventures. These funds also provide business and operational support to help these ventures grow. Venture capital funds, SME funds, social venture funds, and infrastructure funds fall under the Category 1 AIFs.

- Venture Capital Funds invest in start-ups with high growth potential, while SME funds provide capital to small and medium-sized enterprises. Social venture funds invest in ventures with a social impact, while infrastructure funds invest in infrastructure projects.

- Angel Funds, which are a subcategory of venture capital funds, invest in start-ups that are in the pre-revenue stage. Angel Funds provide seed funding to start-ups, and they are often the first investors in a company. Angel Funds are considered to be a critical source of funding for start-ups.

- Social Venture Funds are funds that invest in socially responsible companies that seek to make a positive impact on society while also generating financial returns.

- Infrastructure Funds are funds that invest in infrastructure projects such as highways, airports, power plants, and other public works projects. These funds typically invest in projects that generate stable cash flows over a long period of time and provide an essential service to the community.

Category 2 AIFs

They are those AIFs that do not fall under Category 1 or Category 3 and do not undertake leverage or borrowing, other than to meet day-to-day operational requirements, and as permitted in the SEBI (Alternative Investment Funds) Regulations, 2012. Various types of funds such as real estate funds, private equity funds (PE funds), funds for distressed assets, etc. are registered as Category 2 AIFs.

- Real Estate Funds invest in real estate projects, including residential, commercial, and industrial properties. These funds may invest in properties directly or indirectly through Special Purpose Vehicles (SPVs).

- Private Equity Funds invest in companies that are not listed on the stock exchange. They typically buy a substantial stake in the company and work closely with the management team to improve the company's performance. PE funds are often long-term investors, and they exit their investment through an Initial Public Offering (IPO) or a sale to another company.

- Funds for Distressed Assets invest in assets that are undervalued or are facing financial difficulties. These funds aim to acquire such assets at a low price and sell them when their value increases.

Category 3 AIFs

They employ diverse or complex trading strategies and may employ leverage, including through investment in listed or unlisted derivatives. These AIFs are the riskiest of the three categories and may invest in a wide range of assets, including stocks, bonds, currencies, and commodities.

Hedge funds, PIPE (Private Investment in Public Equity) funds, and other funds that employ complex trading strategies fall under the Category 3 AIFs.

- Hedge Funds are known for their ability to generate high returns but also have a high level of risk. PIPE funds invest in publicly traded companies, typically buying a large stake in the company at a discount to the current market price.

- PIPE Funds refer to Private Investment in Public Equity funds which are funds that invest in publicly-traded companies that are in need of capital but do not want to go through the lengthy and expensive process of a public offering.

Conclusion

Alternative Investment Funds provide a new avenue for investors to diversify their portfolios beyond traditional investments such as stocks and bonds. They offer the potential for high returns, but they also come with higher levels of risk. As a result, it is essential for investors to carefully consider their investment objectives, risk tolerance, and investment horizon before investing in AIFs.

Key differences between IPOs and regular stock investments

Investing in the stock market can be done in various ways, two of the most common being through Initial Public Offerings (IPOs) and regular stock investments. While both involve purchasing shares of a company, they differ in several key aspects. Here’s a closer look at what sets them apart.

What Are IPOs?

An IPO, or Initial Public Offering, is the process where a company offers its shares to the public for the first time. Before an IPO, the company's shares are privately held by founders, early investors, and employees. Going public allows the company to raise capital by selling shares to new investors. The funds raised are typically used for expanding operations, paying off debt, or making acquisitions.

What Are Regular Stock Investments?

Regular stock investments involve buying shares of companies that are already publicly traded on stock exchanges. These shares can be bought and sold at market prices, which fluctuate based on supply and demand. Investors can purchase these stocks through online brokerage platforms like Swastika Investmart.

Key Differences Between IPOs and Regular Stock Investments

1. Availability of Information

- IPOs: Companies going public must file a prospectus with the Securities and Exchange Commission (SEC) or equivalent regulatory body. This document provides detailed information about the company’s financials, management, and operations.

- Regular Stocks: For companies already publicly traded, detailed information is available through regular filings, such as earnings reports, analyst reviews, and news articles. However, the depth of initial information may be less compared to what is provided in an IPO prospectus.

2. Risk and Return

- IPOs: Generally considered riskier because they often involve new or lesser-known companies. The uncertainty around these companies' futures can lead to significant price volatility. While the potential for high returns exists, the risks are also higher.

- Regular Stocks: Investing in established companies is usually less risky, as these firms have proven financial performance and tend to be less volatile. However, the potential for high returns may be lower compared to IPOs..

3. Accessibility

- IPOs: Initially, IPOs are often available primarily to institutional investors like banks and hedge funds, as well as high-net-worth individuals. Retail investors usually get access afterward, sometimes with limited availability.

- Regular Stocks: Available to anyone with a Demat account, making them more accessible to retail investors.

4. Timing

- IPOs: Available for a limited time, usually a few weeks or months, before the shares start trading on the open market. Investors need to act quickly and may not have time for thorough research.

- Regular Stocks: Can be bought or sold at any time, giving investors flexibility to adjust their portfolios based on market conditions and personal investment goals.

Conclusion

Both IPOs and regular stock investments offer unique opportunities for investors. IPOs can provide the potential for high returns but come with higher risk and costs. Regular stock investments are generally less risky and more accessible, making them suitable for a broader range of investors. The choice between IPOs and regular stocks should be guided by your risk tolerance, investment goals, and financial resources.

HOW TO CLAIM FOR HEALTH INSURANCE

Health insurance is an important investment in protecting your health and finances. It covers a variety of medical expenses, from hospitalization to surgery and even medication. However, it is important to know how to claim health insurance to reap the benefits of your policy. In this blog, we will discuss the types of health insurance claims, the documents required to claim health insurance, and how the health insurance claim process works.

Types of Health Insurance Claims:

There are two types of health insurance claims - cashless and reimbursement claims.

Cashless Claims:

In cashless claims, the policyholder has to get treatment from a network hospital that has a tie-up with the insurance company. The policyholder can inform the insurance company about the planned hospitalization, and the insurance company will provide a pre-authorization letter to the hospital. This letter mentions the approved amount for the treatment. After the treatment is completed, the hospital sends the bills directly to the insurance company for payment. The policyholder does not have to pay anything, except for non-medical expenses like food or telephone charges. Policyholders can get reimbursement for pre and post-hospitalization expenses by submitting actual bills to the insurance company.

Reimbursement Claims:

Reimbursement claims are applicable when the policyholder gets treated at a non-network hospital or if the policyholder cannot get cashless treatment due to certain reasons. In this case, the policyholder has to pay for the treatment upfront and then claim reimbursement from the insurance company later. The policyholder has to submit all the required documents to the insurance company within a specified time period. Once the documents are verified, the insurance company reimburses the approved amount to the policyholder.

Documents Required to Claim Health Insurance:

The documents required for health insurance claims vary depending on the type of claim. However, there are some common documents that are required for both cashless and reimbursement claims. These include:

- Claim form: This is a form that needs to be filled out by the policyholder while making the claim. It contains details about the policyholder, the treatment received, and the medical bills.

- Original bills and receipts: Original medical bills and receipts need to be submitted as proof of the medical expenses incurred. These bills should contain the name and address of the hospital, the date of admission and discharge, and a detailed breakup of the expenses incurred.

- Discharge summary: A discharge summary is a document provided by the hospital after the patient is discharged. It contains details about the treatment received, the duration of hospitalization, and the diagnosis.

- Doctor's prescription: The doctor's prescription for the treatment received needs to be submitted.

- Investigation reports: If any diagnostic tests like X-rays or blood tests were done, the reports need to be submitted as proof of the tests and the expenses incurred.

- KYC documents: Know Your Customer (KYC) documents like an Aadhaar card, PAN card, passport, or voter ID must be submitted for verification purposes.

- Pre-authorization letter (for cashless claims): A pre-authorization letter is required for cashless claims. This letter is provided by the insurance company and needs to be submitted to the hospital before the treatment.

Steps Involved in Health Insurance Claim Process

Step 1 - Intimation

The first step in the health insurance claim process is to inform the insurance company about the hospitalization. If it's a planned hospitalization, then the policyholder should inform the insurer in advance. In case of an emergency, the policyholder should inform the insurer within 24 hours of hospitalization.

Step 2 - Filing the Claim

Once the policyholder has informed the insurer, the next step is to file the claim. The policyholder can either opt for a cashless claim or reimbursement claim, depending on the circumstances.

For a cashless claim, the policyholder needs to fill in the pre-authorization form provided by the insurer. This form needs to be submitted to the hospital's insurance desk, which will verify the policy details and send it to the insurer. Once the insurer approves the claim, the hospital will provide cashless treatment to the policyholder.

For a reimbursement claim, the policyholder needs to submit the claim form along with the necessary documents to the insurance company. The claim form is available on the insurer's website or can be obtained from their office. The policyholder needs to ensure that the form is filled out correctly and all the necessary documents are attached to it.

Step 3 - Documentation

The documentation process is an essential part of the health insurance claim process. The policyholder needs to submit the following documents along with the claim form:

- Original hospital bills

- Discharge summary

- Investigation reports

- Prescriptions and receipts for medicines

- Any other relevant documentation as required by the insurer

Step 4 - Claim Settlement

Once the insurer receives the claim form and necessary documents, they will verify the details and approve the claim. In case of a cashless claim, the insurer will settle the medical bills directly with the hospital. In a reimbursement claim, the insurer will verify the expenses incurred and reimburse the policyholder for the same.

Conclusion

The health insurance claim process can be a little complex, but it's essential to understand it to avail of the benefits provided by the policy. The policyholder needs to ensure that all the necessary documents are submitted to the insurer to ensure a smooth and hassle-free claim settlement process.

Say hello to a new way of comparing insurance policies from various insurers across India! Compare and buy insurance products like Term Insurance, Health Insurance, General Insurance, and Investment Plans which are best for you with Hello Policy.

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App