The Power of Compounding – Why Starting Early Matters

Introduction

Albert Einstein reportedly called compound interest the "eighth wonder of the world." Whether or not he actually said it, the math is undeniable. Compounding is the process where your investment returns begin earning their own returns — and over time, this snowball effect becomes truly extraordinary.

The catch? Compounding needs one essential ingredient: time.

The more years you give your money to grow, the more dramatic — and life-changing — the results become. This is exactly why starting your investment journey early, even with a modest amount, can make a difference of crores by the time you retire.

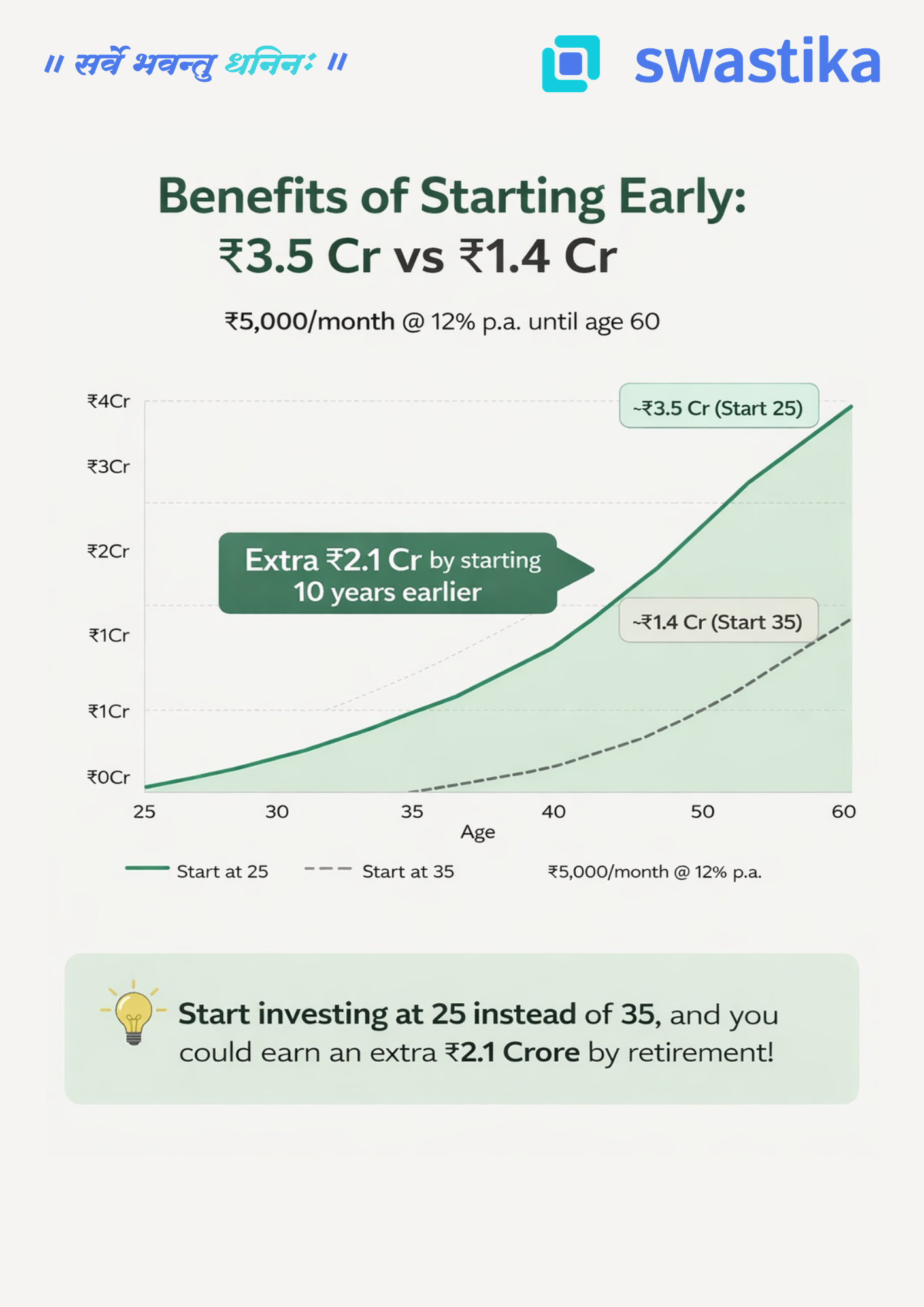

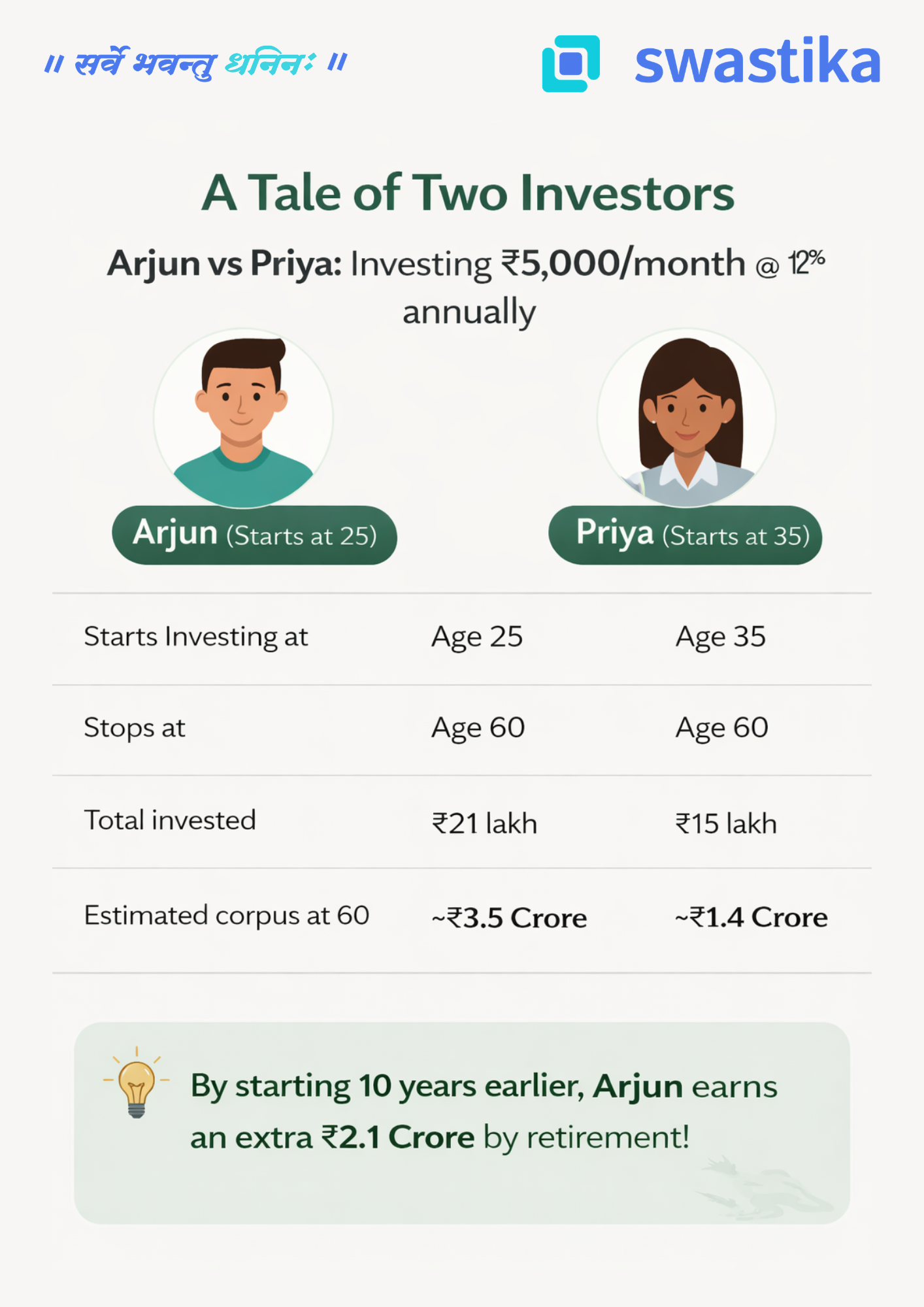

A Tale of Two Investors: Arjun vs Priya

Let's bring this concept to life with a simple, real-world example.

Meet Arjun and Priya. Both are sensible, disciplined investors. Both invest ₹5,000 every month through a SIP (Systematic Investment Plan) in equity mutual funds, earning an average annual return of 12%. Both stop investing at age 60.

The only difference? Arjun starts at 25. Priya starts at 35.

The numbers are striking. Arjun invests just ₹6 lakh more than Priya in absolute terms — yet walks away with ₹2.1 Crore more at retirement.

That extra ₹2.1 Crore didn't come from investing more aggressively or taking bigger risks. It came purely from starting 10 years earlier.

Why Does Time Make Such a Huge Difference?

This is where the magic of compounding reveals itself.

In the early years of investing, growth looks modest and almost unimpressive. But as the years pass, your corpus grows not just on your original investment, but on all the accumulated returns from previous years. The curve goes from almost flat to steeply exponential — and that steep climb happens in the later years.

When Arjun starts at 25, his money has 35 years to ride that exponential curve. Priya's money, starting at 35, only catches the last 25 years — and critically, it misses the steepest part of the climb in the final decade.

Think of it this way: the last 10 years of compounding are worth more than the first 20. That is the counterintuitive truth at the heart of long-term investing.

The Real Cost of Waiting

Many young earners tell themselves, "I'll start investing once I'm more settled — once the salary improves, once the EMI is paid off, once life is a bit easier."

But the numbers show that every year of delay is extraordinarily expensive — far more expensive than any EMI or lifestyle expense. Priya didn't invest carelessly. She invested faithfully for 25 years. Yet she ends up with less than half of what Arjun accumulated — not because she did anything wrong, but simply because she started a decade late.

The cost of waiting 10 years wasn't ₹6 lakh in additional contributions. The cost was ₹2.1 Crore in lost wealth.

Three Principles to Remember

1. Start now, not later.The best time to start investing was yesterday. The second best time is today. Even a SIP of ₹1,000–₹2,000 per month in your 20s is infinitely better than waiting for the "right time."

2. Consistency beats intensity.You don't need to invest large sums all at once. A small, steady, monthly commitment — maintained without interruption — is what unlocks the full power of compounding over decades.

3. Stay invested through market cycles.Compounding works only if you let it work. Exiting during market corrections or stopping your SIP in tough months breaks the chain. Time in the market, not timing the market, is what builds wealth.

The Bottom Line

If you are in your 20s or early 30s, you hold an asset that no amount of money can buy later: time. Use it. Start a SIP today — even a small one. Let compounding do its slow, steady, powerful work.

Because the difference between starting at 25 and starting at 35 is not just 10 years. As Arjun and Priya's story shows, that difference is ₹2.1 Crore.

Big Budget

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

Latest Articles

Portfolio Diversification: A Beginner’s Guide for Asset Allocation

Many of you have heard the saying “ Don't put all the eggs in one basket”.

This means if a farmer gets stumbled while carrying the egg basket, he could end up in a messy situation as all the eggs present inside the basket become messy which makes the whole basket dirty.

The meaning of the words perfectly said that don't risk all of your money on a single investment.

Diversification protects your investment as it allows you to invest in multiple asset classes which in turn saves you from losses that could happen in one particular sector.

Let’s understand with an example: Everyone knows about the equity crash that happened in 2008-09.

As per the reports, during the 2008-09 period, equities crashed by 39%. Had you invested all the money into equities, you would have probably been into major losses.

In any case, if you had spread all of your investment into different asset classes, such as equity trading, debt, commodity trading etc, you would have been saved from huge losses.

In 2008-09, gold gave outstanding stock trading returns of 24%. The same went for debt. In the next two years, post-2008-09, the equities were seeing a rising mode as it would go up by 24% while other asset classes stopped giving good returns.

What is Portfolio Diversification

Portfolio diversification refers to investing your money across multiple asset classes which not only helps your money grow but helps you mitigate your losses to a greater extent.

In diversification, you owe different stocks from multiple industries, countries, commodities and other investments such as gold, silver, bonds, government instruments, and real estate.

Investing money in various sectors minimizes the permanent loss of capital and the volatility of the overall portfolio.

The Real Purpose of Diversification

The primary motive of diversification is to minimize risks. But no one can achieve that by investing in highly safe instruments such as government investment schemes like PPF, Treasury bills, RBI bonds, NSCs etc.

This is because investing all of your money into government schemes will significantly reduce your overall returns. For instance, investing all of your money in NSCs, and PPF debt options won't help you get outstanding returns.

The portfolio should be filled with equity-related instruments, only then you would be able to achieve handsome returns in less time.

For those who believe in government investment schemes, you should remember that most of these schemes have a high tax. Hence, your post-tax return would come out as very low.

Many of you would love to gain good returns over less period of time, that too without taking a risk. This cannot happen in real life. To get ample results from your investments, you need to take a reasonable level of risk.

What Should Be An Ideal Portfolio?

An ideal portfolio should be one that has more than 5 asset classes.

Here are the tips for getting an ideal portfolio:

1) Include 10 + More Stocks Of Various Sectors into your Portfolio

Investing in multiple sectors is the best way to build your portfolio. Stocks of multiple carry their own weightage which will increase your portfolio’s value. Also, stocks of different sectors will minify your risks at a certain level.

Suppose, if the stocks of IT keep on falling and other sectors of stocks of crude oil and pharmaceutical companies grow, will eventually balance your portfolio in a much better way.

Don't fill your stocks with one particular sector. It does look tempting to buy many stocks of the well-known giants, but it’s not a complete diversification.

For instance, if a sector gets affected by the economic slowdown, the company's shares would fall.

2) Reserve a Portion of Portfolio into Fixed Income

Many investors suggest putting a small portion of fixed income assets in their portfolios. Fixed income instruments like government bonds, may give fewer returns compared to equities but they will also reduce a portfolio’s risk profile and volatility.

The stock market is full of volatility. In many cases, we have seen where the investors lose a great amount of money by investing heavily in equities. In such cases, people find fixed income instruments a great way of investment as they provide them with easy and secured returns.

ETFs are the best example of fixed income securities.

3) Invest in Real Estate

Investors who want to make a strong portfolio should invest in real estate. It is seen that putting money into real estate not only increases your return but also minimizes your portfolio’s volatility.

Factors That Impact the Portfolio:

Age

Age is an important factor in asset allocation. Investment experts say that young investors need to invest a lot in the equity segment. Investors aged 25 to 35 should have equity allocations of 75% to 80% while people of age more than 35 years should have lower equity allocations.

Willingness to Take Risks

Investors, especially the young ones, should have a willingness to take a certain risk during their investment journey. This is the time when you can learn a lot of things even from your failures.

Many people are often afraid of the term failure, but the term itself teaches you many lessons in real life.

If you are a beginner but want to earn a lot of wealth from the stock market, there are many things you need to learn. Stock picking is not the easy thing as it seems to be. It requires a lot of stock market research, analysis and most importantly knowing the market volatility.

For generating better returns, you need to put money into the stock market, then only you will get to know how the stock market exactly functions well.

Focus on Long Term Investing

New investors need to understand long term investing. Beginners think that 6 months or 1 year is the best holding period, however, it is not correct. One year of equity holdings will not give you satisfactory returns as there are taxes included in it.

For generating better wealth, you need to hold your equities for at least 5 years.

Don’t Over-Diversify

Many investors think that the more they add stocks to their portfolio, the more will be their wealth. Hence, they keep adding more stocks to their portfolio. Modern portfolio theory says that investors should keep 10-15 stocks of one sector in their portfolio.

Final Thoughts

Portfolio diversification doesn't mean that you will never incur any losses. The role of diversification is to mitigate risks against stock market volatility. Diversification can reduce the risk up to a certain level.

If you want to achieve huge stock trading returns, make the investment a long term journey. Maintain a good balance between risk and return, only then you will become an ace investor.

How Investors Can Receive Compounding Returns

Introduction:

1.What is Compounding?

Compounding refers to the process where the returns earned on an investment generate additional returns over time. This means that investors not only earn returns on their initial investment but also on the returns accumulated in previous periods. The longer you stay invested, the greater the compounding effect, as your returns start generating their own returns, leading to exponential growth.

2. How Compounding Works in Investments

Compounding returns work by reinvesting your earnings back into the principal amount. Over time, these reinvested returns increase the overall value of your investment, leading to more significant returns in the future.

Example:

- If you invest ₹10,000 at an annual interest rate of 10%, your investment will grow to ₹11,000 after one year. In the second year, you’ll earn 10% on ₹11,000 instead of just ₹10,000, and so on.

- After 5 years, this same ₹10,000 will grow to ₹16,105, not just ₹15,000.

3. Strategies to Receive Compounding Returns

a. Long-Term Investing

Staying invested for the long term allows compounding to work its magic. The more time your investment has to grow, the higher your compounding returns will be.

Example:

- HDFC Bank: If you had invested in HDFC Bank's stock in 2010 and held onto it, your returns would have grown manifold over the past decade, driven by both stock appreciation and reinvested dividends.

b. Reinvesting Dividends

Many companies offer dividend payouts to shareholders. By reinvesting these dividends instead of cashing them out, you allow the dividends to start earning returns, adding to the compounding effect.

Example:

- Tata Consultancy Services (TCS): Reinvesting dividends received from TCS over the years would have allowed you to benefit from not only stock price growth but also compounded dividend returns.

c. Regular Contributions to Investments

Adding more money to your investments regularly increases the base amount on which compounding occurs. This strategy accelerates the growth of your investment over time.

Example:

- If you invest ₹5,000 monthly in a mutual fund that offers a 12% annual return, the power of compounding over 10-20 years can significantly multiply your wealth.

d. Investing in Growth Stocks

Growth stocks are companies that reinvest their earnings into expanding their business rather than paying dividends. These stocks tend to appreciate faster, and if held long term, they can offer substantial compounding benefits.

Example:

- Reliance Industries: Investors who purchased Reliance stock over the past decade have seen their investment multiply due to the company’s rapid growth and expansion into various sectors.

e. Start Early

Starting your investment journey as early as possible gives compounding more time to work. Even small contributions made early can grow substantially by the time you retire.

Example:

- If you invest ₹1,00,000 at age 25 and it grows at a 12% annual rate, by the time you turn 50, your investment will be worth more than ₹10,00,000. The earlier you start, the more time compounding has to magnify your wealth.

4. The Rule of 72: Estimating Compounding Growth

The Rule of 72 is a simple formula to estimate how long it will take for your investment to double through compounding. Divide 72 by your expected annual return to find out the approximate number of years.

Example:

- If your investment offers an 8% return, it will take approximately 9 years (72 ÷ 8) for your money to double.

5. Key Factors that Enhance Compounding Returns

- Time Horizon: The longer you stay invested, the more your returns compound.

- Rate of Return: Higher returns accelerate the compounding effect.

- Reinvestment: Reinvesting dividends and capital gains adds to the base investment, boosting compounding.

- Discipline: Regularly contributing to your investments and avoiding impulsive withdrawals can maximize compounding benefits.

6. Conclusion:

The Power of Compounding

Compounding is a powerful strategy for wealth creation, especially when applied over a long time frame. By starting early, reinvesting earnings, and making regular contributions, you can take full advantage of compounding returns. Whether you invest in stocks, bonds, or mutual funds, the key to maximizing compounding returns is patience, discipline, and a long-term perspective.

Loan Against Securities

What is Loan Against Shares and Securities?

A loan against securities or loan against shares is a loan facility given to customers in which the loan bearer needs to pledge its security as collateral to avail of a loan. It has multiple types such as loans against insurance, loans against MFs, loans against National Savings Certificates or more.

A loan against securities is popular among investors as it is an easy way to get a loan without compromising your security. Also, it allows you to receive a loan of up to 80% on multiple financial instruments.

This is a unique kind of service that enables the bearer to take advantage of dual service viz perpetuating ownership on your investment along with receiving their benefits.

Types of Collateral for Loan Against Securities

- DEMAT Account and Shares

- Insurance Policies

- NCD (Non-Convertible Debentures)

- LIC Policies and UTI Bond

- NABARD Bonds

- Mutual Fund Units

- National Savings Certificate

- Kisan Vikas Patra and more.

How Does Loan Against Security Work?

A loan against security is generally offered as an overdraft facility in which you need to pay interest only on the loan amount you use and the period you use for it. This can be done immediately after the securities you offer for the collateral.

Features of Loan Against Shares:

A loan against shares is considered one of the secured forms of loans that can be given against the securities present in your account. The following are the features of loans against shares:

- The loan amount can be given up to 80% of the collateral value.

- The interest rate of loans against shares lies between 9% to 12%.

- The normal tenure of a loan against shares is 1 year but you can extend it for further years.

- Loan against shares is eligible for Indian residents, NRIs, Hindu Undivided Families, Sole Proprietorship, Public and Private funds and more.

- The desired age for the borrower lies between 18 to 65 years.

- Charges for loans against shares are initial processing fees, Annual Maintenance Charges (AMC), stamp duty and more.

Advantages of Using Loans Against Securities

- A loan against shares offers you to remain the owner of your securities.

- It also gives you the facility to receive bonuses and dividends on your investments.

- You can get a high loan value which is up to 80% of the collateral deposited.

- A loan against security requires minimum paperwork, hence you get an instant loan without much.

- It also provides instant liquidity,, which in turn improves investment potential.

- Loan against security allows you a flexible repayment facility along with penalty-free foreclosure.

Eligibility Criteria for Applying for Loans Against Securities

Following are the eligibility criteria for Loan Against Securities

- Residents should be Indian, NRI, or HUF.

- The minimum age to apply for LAS is 21 years.

- You should either be salaried or a self-employed individual.

- The securities you pledge as collateral should be approved by the bank.

From Where Could You Take A Loan Against Shares?

Banks and NBFCs have the authority to sanction loans against securities. Here, we will help you to identify your preferred creditor:

Area Bank NBFC Margin Requirement50% against equity/equity-oriented mutual funds and lenders’ discretion on debt/ debt-based mutual funds.50% against equity/equity-oriented mutual funds and lenders’ discretion on debt/ debt based mutual funds. Capitalization on Loan Amount 10 Lakh against physical shares, 20 Lakh against Demat shares No Cap on the amount of Loan Loan Processing Time consuming process Easy and Fast Process.

It is preferred to take a loan from NBFC as compared to a bank as it is the safe, fast yet most effective way to avail of a loan without much hassle.

Purposes of Taking Loan from Other Securities:

There are different purposes for taking a loan against shares which can be mentioned below:

1) Working capital requirement for business:

Many SMEs take loans against securities just to expand their business. With this new loan amount, businesses usually fulfill their daily working capital requirement which in turn enhances their profits and growth.

2) Business Expansion:

This is the most valid reason SMEs take loans against their securities to increase scalability. This will help businesses to work on new products or open new branches in different cities.

3) Investment in Capital Market:

If you want to increase your investment capital and have confidence in your stock picks, then taking out a loan can be a good option for you as getting a loan on your present investment will help you raise future investments as well.

4) Other Personal Usage:

Loans against shares can also be used for personal purposes such as buying a home, a child’s education and marriage, etc.

Parameters for Credit Underwriting

The Bank or NBFC reviews your loan application to check your creditworthiness before giving you a loan. Here are the following parameters:

1) Checking Client’s Profile, Security Provider and more:

Lenders shall check for market reputation and decide the credibility based on the number of years you have been in a business that is known for vintage.

2) Security Analysis:

In security analysis, the creditors take a detailed insight into your financial securities. He determines the proper value of the security, keeping in mind the several fluctuations happening in the market.

3) Financial Statement:

You need to submit all the necessary financial documents such as the cash flow statement, balance sheet, income statement of your business.

FAQ’s

Can I Get a Loan Against My Securities?

Yes, you can. A loan against shares is offered against the securities you want to pledge your holdings as collateral. This will help you to meet new investment and liquidity requirements.

What is the Concept of Loan Against Securities?

Loan against shares enables borrowers to get loans against financial securities such as bonds, stocks, mutual funds, insurance to meet your requirements. You can apply for a loan against shares for your business purposes or in case of urgent financial aid.

How many loans Can I Get Against Securities?

You can get a loan of Rs 20 Lakh against your securities.

Can I Get a Loan on Equity Shares?

Yes. you can get a loan on equity shares where you can pledge shares in the form of equity to avail the benefit of the loan.

Parameters Affect Gold Prices in India

Gold is considered a very precious commodity and that’s why investors always prefer Gold as a commodity trading instrument because it acts as a safe investment.

In India, gold holds a strong place in people’s hearts as Indian citizens believe it's an auspicious metal that is being worn on every occasion. Also, Indian citizens feel gold is a symbol of richness and power.

It has been seen that the importance of gold has significantly increased over the years as investors keep this metal as a hedging tool during market volatility and inflation.

The price of gold keeps on fluctuating due to several factors. It is interesting to know that the US dollar affects the gold price to a greater extent.

Gold puts strong value not only on a state's strong economy, but even on personal investments.

Here are the Factors that affect the Gold Price most:

1) Demand and Supply

Gold prices heavily depend on demand and supply. When there is a huge demand, the price of gold rises or vice versa.

Since Gold is a commodity that is continuously in demand; factors such as demand and supply play an important role in the gold price.

2) Inflation

Whenever inflation is on the rise, the value of currency starts to decrease. As most financial instruments fail to generate better commodity trading returns, gold acts as a strong hedging tool.

3) Government Reserves

The Government of India holds reserves of gold. Here, the price of gold gets affected when RBI purchases more or sells more gold. If you wonder about the gold prices, government reserves could be one of the reasons.

4) Import Duty

Few of us know that India produces less than 1 per cent of global gold production. However, due to the high demand for gold in the country, the government imports a lot of gold from overseas to meet the demand. Hence, import duty plays an important role in increasing gold prices.

How is the Gold Price affected by the US dollar?

In 1944, 44 countries signed the significant Bretton Woods Agreement. The agreement is about international trading, import and export via the US dollar.

A country will sum up its total US dollar reserve at the end of a year. Then, the country goes to the International Monetary Fund (IMF) with that amount of US dollars.

That means the currencies are convertible to gold. Because of this agreement, the USA eventually took profit from all other countries obliged to trade against the US dollar.

How does Inflation affect Gold Prices?

During the pandemic time, Gold prices were increased. Why does this happen?

Because gold is a safe investment, people started investing in gold during the times of COVID to use it as a currency if they were in financial trouble.

Investors hold the gold as compared to currency. As a result, when Inflation in India is high, the gold price also increases and vice versa.

Due to high demand and less supply, gold prices get high, and the people who hold gold during inflation make a lot of profit.

If an RBI imports gold, it does affect the demand and supply of the currency in the country.

To import gold from another country, the RBI needs to print a larger number of notes to pay for it, and due to an excessive amount of currency notes, inflation is caused in the country, and hence the gold price will also be increased.

How does the Festival affect the Gold Price?

In India, many people buy gold in the form of jewellery, and they give gold as a valuable gift to their loved ones.

India depends on the import of gold as our production of gold is less than 1 per cent of the total world production. Because of the high demand in the festival season, we need to import gold from foreign countries.

During festivals like Diwali and Dhanteras, gold prices increase because of high demand and less supply.

India is increasing the production of gold mines to control the gold imports and fulfill our gold requirements.

How does the Indian Currency affect Gold Prices?

The rupee-dollar equation plays a role in Indian gold rates, although it does not impact global gold prices.

India imports gold, and hence if the rupee is getting weaker against the dollar, it directly affects the gold prices.

So, a depreciating rupee may affect the demand for gold in the country. However, the change in rupee-dollar rates has no impact on gold rates denominated in dollars.

Conclusion

As we discussed factors that affect the gold price in India, Gold prices are volatile and considered a safe investment.

Gold is also a portfolio diversifier for stock market trading investors.

When the market falls, people start investing in gold to diversify their portfolios.

Commodity Trading is considered "sensitive" because stock market experts have seen frequent instances of price manipulation in the past 5 years.

Therefore it is suggested to take advice before starting trading in any commodity. Taking help from a reliable stock broking firm will always be helpful as they have strong stock market research reports and an experienced analyst team.

मजबूत बांड यील्ड से दबाव में सोना-चांदी।

अमेरिका से जारी होने वाले आर्थिक आकड़ो से पिछले सप्ताह बाज़ारो में मिले जुले संकेत रहे, जिससे सोने और चांदी में साप्ताहिक गिरावट दर्ज की गई है। नॉन फॉर्म एम्प्लॉयमेंट चेंज के आंकड़े अप्रैल माह में घट कर 431 हजार रह गए जिससे सोने और चांदी के भाव को सपोर्ट मिला।

जबकि बेरोज़गारी दर में मजबूती देखि गई है। रूस और यूक्रेन के बीच शांति वार्ता में हुई थोड़ी प्रगति से अमेरिकी डॉलर इंडेक्स और बांड यील्ड में निचले स्तरों से सुधार दर्ज किया गया जिसके सोने और चांदी के भाव में दबाव दिखाई दिया।

हालांकि, कीमती धातुओं में कीमते अभी गिरावट के साथ एक सीमित दायरे में चल रही जिससे आगे इनमे उछाल भी देखने को मिल सकता है। जून वायदा सोने के भाव पिछले सप्ताह में 1500 रुपये प्रति दस ग्राम और मई वायदा चांदी के भाव 3200 रुपये प्रति किलो तक टूटने के बाद हिन्दू नव वर्ष की शुरुवात के पहले ही निचले स्तरों से सुधार रहा और सोना पिछले सप्ताह में 1 प्रतिशत और चांदी 2.5 प्रतिशत टूट कर क्रमश 51900 और 67000 के स्तरों पर रहे।

भारतीय सराफा बाज़ारो में शादियों का सीजन शुरू होने के पहले ज्वेलर की मांग बढ़ने की सम्भावना है। निचले स्तरों पर सोने और चांदी की हाजिर मांग आने की सम्भावना से कीमती धातुओं के भाव में उछाल देखने को मिल सकता है।

उधर, ऊर्जा की कीमतों में मजबूती भी सोने और चांदी के भाव को सपोर्ट करती दिख रही है क्योकि पिछले सप्ताह में ओपेक और नॉन ओपेक देशो के समूह की बैठक में पूर्व आधारित योजना के अनुसार ही कच्चे तेल का उत्पादन बढ़ाया जायेगा जबकि बढ़ी हुई तेल की मांग और रूस पर प्रतिबंध के कारण, तेल और गैस के भाव मजबूत है जिसके कारण मुद्रास्फीति के नियंत्रण में ज्यादा वक्त लगेगा।

तकनीकी विश्लेषण

इस सप्ताह सोने और चांदी के भाव सीमित दायरे में रह सकते है। जून वायदा सोने में 51200 रुपये पर सपोर्ट और 52500 रुपये पर प्रतिरोध है। मई वायदा चांदी में 65000 रुपये पर सपोर्ट और 69000 रुपये पर प्रतिरोध है।

The Buybacks vs. Dividends: Understanding the Choices with Indian Stocks

When Indian companies generate profits, they face the decision of how to share that success with their shareholders. Two popular methods are share buybacks and dividends. Let’s explore these concepts and see how they play out with examples from Indian stocks.

What Are Share Buybacks?

Share buybacks occur when a company repurchases its own shares from the market. This reduces the number of shares available, which can lead to an increase in the stock’s price. Buybacks offer flexibility and can signal confidence in a company's future. However, they can also be controversial, as critics argue they might be used to artificially boost share prices.

Tata Consultancy Services (TCS)

In 2023, TCS announced a buyback program worth ₹18,000 crore. This move aimed to return excess cash to shareholders while demonstrating the company’s confidence in its future growth. By reducing the total number of shares, TCS increased its earnings per share (EPS), which positively impacted its stock price.

Advantages of Buybacks:

- Flexibility: Buybacks can be adjusted based on the company's financial situation.

- Tax Efficiency: Shareholders are taxed only when they sell their shares, often at a lower capital gains rate.

- EPS Boost: Fewer shares increase EPS, potentially driving up stock prices.

- Signal of Undervaluation: A buyback can signal to the market that the company believes its shares are undervalued.

What Are Dividends?

Dividends are regular cash payments made to shareholders from a company's profits. They provide a steady income stream, which is particularly attractive to long-term investors seeking consistent returns. Regular dividends often reflect a company’s financial health and stability.

Infosys

Infosys has a strong history of paying regular dividends. In 2023, the company declared a dividend of ₹17.50 per share, continuing its tradition of rewarding shareholders with reliable payouts. For many investors, Infosys' consistent dividend payments are a key reason for holding onto the stock, as they offer dependable income over time.

Advantages of Dividends:

- Consistent Income: Dividends provide a reliable income stream, appealing to income-focused investors.

- Signal of Confidence: Regular dividends can indicate a company’s stable earnings and financial health.

- Lower Market Impact: Dividends do not alter the number of shares in the market.

Which is Better for Investors?

The choice between buybacks and dividends depends on individual investor goals. Buybacks might be more appealing if you’re looking for capital gains, as they can drive up share prices. On the other hand, dividends are favored by those seeking a steady income, such as retirees or conservative investors.

Reliance Industries

Reliance Industries employs both strategies. The company has conducted share buybacks to signal confidence in its stock value while also maintaining a robust dividend policy to reward its shareholders. This balanced approach allows Reliance to cater to a wide range of investor preferences.

Criticism and Risks:

- Buybacks: Critics argue buybacks can inflate stock prices and benefit executives with stock-based compensation, and companies might prioritize buybacks over important investments.

- Dividends: Paying dividends reduces the cash available for reinvestment in the company, potentially limiting growth opportunities.

Market Preferences:

Market reactions can vary depending on the economic environment. For example, in a low-interest-rate environment, buybacks might be more favored due to their tax advantages, whereas in a more stable economic climate, dividends might be preferred for their reliability.

Conclusion

Both buybacks and dividends have their advantages and can play an important role in a company’s strategy to return value to shareholders. In India, companies like TCS, Infosys, and Reliance Industries illustrate how these methods can benefit investors. Whether you prefer the potential for capital appreciation through buybacks or the steady income from dividends, understanding these strategies can help you make more informed investment decisions.

Ultimately, the best approach depends on the specific circumstances of the company and its shareholder base. Many companies use a combination of both strategies to balance short-term returns with long-term growth.

.webp)

.webp)

.webp)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App