Zee FIFA World Cup rights impact on shareholders: A retail investor's geo-SEO guide for 3.3 crore holders

Key Takeaways

- A FIFA World Cup rights deal could be a catalyst for Zee's revenue mix if ad volumes and cross-platform monetization scale.

- Watch early indicators like viewership, subscriber gains, and ad demand on Zee TV and ZEE5 to gauge upside.

- Risks include high upfront costs and leverage that could clip margins if ad demand falters.

- The outcome hinges on execution across platforms and macro demand, not merely the event itself.

When a single sports rights deal touches 3.3 crore shareholders, the real question isn’t how many goals are scored, but how the rights translate into profits for Zee Entertainment’s balance sheet and cash flow. The Economic Times coverage suggests the FIFA World Cup broadcasting deal could act as a meaningful catalyst for Zee’s widely held stock by potentially lifting ad revenue, cross‑platform monetization, and subscriber engagement across TV and its digital arm. For retail investors in India, the question is how this event translates into durable earnings rather than a temporary spike in sentiment.

In this analysis, we weave the article’s premise with a practical investor lens. Zee’s World Cup deal sits at the intersection of content, distribution, and monetization. If Zee can convert fan engagement into incremental advertising revenue and higher digital subscribers, the World Cup rights may incrementally improve near-term earnings and long-term brand value. Yet, the upside is not guaranteed; it depends on execution, market demand for ads, and the company’s ability to monetize across both television and Zee5 without eroding margins. This post is grounded in the Economic Times report but expands into how a retail investor in India should think about the potential impact on 3.3 crore shareholders.

As you read, note the implied geo-focus: India’s diverse media landscape, widespread television penetration, and growing online video consumption all amplify how a marquee event like the FIFA World Cup could influence Zee’s revenue mix. If you want a deeper, data-driven view of this kind of move, Swastika’s Sarthi AI stock assistant provides institutional-style research on Zee and other equities to retail investors seeking edge in Indian markets.

What Zee Entertainment FIFA World Cup rights could mean for India’s 3.3 crore shareholders

The Economic Times article frames the FIFA World Cup rights as a potential lever to improve Zee’s top line in a market where ad budgets are cyclical. In India, big sporting events typically lift viewership across both traditional TV channels and digital platforms, creating a multi‑year tailwind for advertising revenue and for cross‑platform monetization through Zee’s ecosystem. If the deal translates into tangible gains in viewer engagement and ad fill rates, shareholders could see an incremental impact on earnings and a re-rating of the stock on stronger overall visibility.

However, the upside relies on Zee’s ability to monetize the heightened demand across both TV and digital surfaces. The article’s emphasis is on execution: the World Cup must drive incremental revenue and not merely displace existing ad spend or demand. The rights could also help strengthen Zee’s brand as a premier broadcaster of major events, potentially supporting longer‑term subscriber growth on Zee5 and higher engagement across its channels. For 3.3 crore shareholders, the key question is whether this is a one‑off event or the seed of durable, cross‑platform monetization that could sustain improved margins over time.

How the World Cup broadcast deal could translate into ad revenue and subscriber growth for Zee

Sports rights in India have historically unlocked higher advertising yields during peak events. A World Cup rights deal may boost Zee’s TV ad inventory utilization and create spillover benefits for digital advertising on Zee5 as fans flock to streaming for real‑time updates, highlights, and related content. If the fan base translates into longer, more frequent digital sessions, Zee could monetize this through targeted ads, sponsorships, and potential premium digital inventory–beyond traditional TV ad sales. The ET story implies the potential for a meaningful, if measured, uplift in revenue streams across both broadcast and streaming media in the World Cup cycle.

From a retail investor’s standpoint, the critical test is incremental contribution rather than a mere shift in mix. Will the World Cup rights push Zee to higher profit margins, or will the cost of acquiring and exploiting the rights offset the upsides? indieners should watch not only the top line but the accompanying commentary on operating leverage, cost control, and free cash flow generation. The deal’s true value emerges if ad growth and subscriber gains outpace the rights’ funding needs and debt service, enabling sustained cash generation for the company’s equity holders.

Key risks retail investors should watch in a high-cost sports rights cycle

Rights deals for marquee events are capital‑intensive, and the World Cup is no exception. The primary risk for Zee is the burden of upfront or long‑dated payments that could weigh on cash flow if ad volumes or viewership don’t meet expectations. A higher leverage profile could compress margins and reduce financial flexibility in a volatile ad market or during slower macro conditions, which would be a headwind for the stock despite a potential revenue uplift from event-driven demand.

Another risk is the volatility of Indian advertising demand, which can swing with macro cycles and discretionary marketing budgets. If advertiser confidence falters or if the incremental viewers fail to convert into loyal subscribers, the anticipated cross‑platform monetization might underperform relative to expectations. Additionally, regulatory, distribution, or competitive pressures could temper the realized benefits from the rights, limiting the strategic upside for Zee’s balance sheet.

Investors should also consider execution risk–whether Zee can efficiently deploy content, leverage cross‑promotion, and optimize pricing across both TV and digital ecosystems. A rights deal can be a strategic catalyst, but only if the company translates the event into durable earnings growth rather than a temporary boost in reported numbers. The key takeaway is that the deal’s value is contingent on ongoing performance rather than one‑off excitement.

What to watch next: a practical mental model to assess Zee's World Cup deal impact on stock value

One practical mental model is to compare Rights Premium against Operating Leverage. Rights Premium represents the incremental revenue potential from the event itself, while Operating Leverage reflects Zee’s ability to scale profits from higher volumes without a proportionate rise in costs. In other words, does the incremental revenue from the World Cup translate into meaningful EBITDA and free cash flow growth after funding the rights? If yes, the stock’s valuation could re-rate on stronger fundamentals.

Another approach is scenario planning across multiple horizons. Build a base case where ad growth and subscriber gains are modest but steady, a bull case where digital monetization accelerates and cross‑platform engagement surges, and a bear case where ad demand softens or the rights’ amortization weighs on cash flow. Compare these outcomes against Zee’s current debt levels, cash flow, and capital allocation strategy. This framework helps you resist headline-driven moves and focus on underlying profitability and balance‑sheet resilience.

FAQ

What is Zee Entertainment's FIFA World Cup rights deal?

The Economic Times article discusses Zee Entertainment's broadcast rights for the FIFA World Cup in India and its potential to move the needle for Zee's 3.3 crore shareholders.

What potential upside could the deal bring to Zee's revenue and margins?

If ad volumes rise and cross‑platform monetization scales on Zee TV and ZEE5, the World Cup could add incremental ad revenue and higher engagement, potentially boosting earnings.

What are the main risks for Zee from a high-cost sports rights cycle?

High upfront costs and increased leverage could squeeze margins if ad demand softens or viewership underperforms, risking cash flow and balance-sheet health.

How should Indian retail investors assess Zee's stock in this context?

Investors should monitor viewership trends, advertising revenue, subscriber growth, and debt levels, and run scenario analyses for 2024–2026 to gauge potential outcomes.

What practical step can investors take next?

Use a Rights Premium vs. Operating Leverage mental model and leverage Swastika's Sarthi AI stock assistant for deeper institutional‑quality research to validate scenarios.

Conclusion

Bottom line for Indian retail investors right now is that Zee’s FIFA World Cup rights present an optionality risk‑reward setup. The deal could unlock incremental revenue and cross‑platform engagement, but only if Zee translates fan interest into durable earnings, without overburdening the balance sheet. In this context, an investor should treat the World Cup as a catalyst rather than a guarantee, and calibrate expectations around profitability, debt, and cash generation in the World Cup cycle.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

.avif)

सेफ हेवेन मांग से मजबूत सोना-चांदी

भारतीय यूनियन बजट में चांदी और चांदी डोर पर इम्पोर्ट ड्यूटी बढ़ा दी गई है। चांदी पर इम्पोर्ट ड्यूटी, सोने की इम्पोर्ट ड्यूटी के बराबर करने के लिए की गई है, जिससे कीमती धातुओं में इम्पोर्ट ड्यूटी का स्ट्रक्चर सामान रहे। हालांकि, उपकर में बदलाव करके, सोने में इम्पोर्ट ड्यूटी यथावत रखी गई है। इम्पोर्ट ड्यूटी बढ़ाने के बाद, सोने और चांदी में बढ़ोतरी देखि गई। चांदी में कुल इम्पोर्ट ड्यूटी बढ़ा कर 15 प्रतिशत कर दी गई है, जो सोने की ड्यूटी के बराबर है। कीमती धातुओं से बनी ज्वेलरी पर ड्यूटी 22 प्रतिशत से बढ़ा कर 25 प्रतिशत कर दी गई है। हालांकि, अमेरिकी फेड की बैठक के बाद कीमती धातुओं में हेवेन मांग देखि गई। फेड द्वारा अपेक्षाकृत कम, 25 आधार अंको की बढ़ोतरी की गई जिससे सोने की कीमते एमसीएक्स में 58800 प्रति दस ग्राम और चांदी 72700 रुपए प्रति किलो के स्तरों को छू गई। हालांकि, ब्याज दरों के चरम स्तर को फेड ने अनिश्चित बताया है जिससे सप्ताह के अंत में डॉलर इंडेक्स में बढ़त रही और कीमती धातुओं में मुनाफा वसूली हावी हुई। हालांकि, अमेरिकी अर्थव्यवस्था की धीमी विकास दर, फेड को इस साल के मध्य तक ब्याज दरों में बढ़ोतरी रोकने और इसको घटाने के लिए बाधित कर सकता है। यूरोपियन सेंट्रल बैंक और बैंक ऑफ़ इंग्लैंड द्वारा ब्याज दरों में बढ़ोतरी से भी अमेरिकी डॉलर में दबाव बना हुआ है, जो कीमती धातुओं को सपोर्ट कर रहा है। केंद्रीय बैंको की लगातार ब्याज दर बढ़ोतरी से वैश्विक अर्थव्यवस्था दबाव में है, जिससे सोने में सेफ हेवेन मांग बढ़ी है।

इस सप्ताह फेड चेयर जेरोम पॉवेल और एफओएमसी मेंबर विलियम की स्पीच कीमती धातुओं के लिए महत्वपूर्ण रहेगी।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं में तेज़ी रहने की सम्भावना है। सोने में सपोर्ट 57500 रुपये पर है और रेजिस्टेंस 59000 रुपये पर है। चांदी में सपोर्ट 68000 रुपये पर है और रेजिस्टेंस 73000 रुपये पर है।

The Hindenburg vs. Adani Clash: Everything You Need to Know

The Adani Group, one of India’s biggest companies, recently launched the country's largest Follow-on Public Offering (FPO) to raise ₹20,000 crores from investors. However, the response has been surprisingly low, with only 1% of the shares being subscribed and just 2% of the retail portion taken up. This poor response is mainly due to a report released by Hindenburg Research just before the FPO, which has caused a lot of controversy.

What Did Hindenburg Say?

Hindenburg Research, known for investigating companies they believe are overvalued or involved in wrongdoing, published a 106-page report making serious allegations against the Adani Group. Here are the key points:

- Pledged Shares: Hindenburg raised concerns that a large portion of Adani Group shares has been used as collateral for loans. This is risky because if the share prices fall, the lenders might sell these shares, causing prices to drop even more.

- Tax Evasion and Financial Tricks: Despite being one of India’s richest people, Gautam Adani is reportedly only the 10th highest taxpayer. Hindenburg accused the Adani Group of avoiding taxes through activities like diamond trading, over-invoicing, and other financial schemes.

- Offshore Payments: The report highlighted a ₹780 crore payment made by Adani Enterprises to an offshore company in Australia. Hindenburg suggested this payment might not have been transparent because the offshore company was allegedly owned by the Adani Group itself.

- Market Manipulatioeased their holdings, which raised suspicions of manipulation.

- Complicated Corpon: Hindenburg claimed that in 2019, Adani Green, part of the Adani Group, used a broker involved in market rigging for its share sale. After the sale, some foreign investors incrrate Structure: Hindenburg criticized the Adani Group’s complex structure, with 578 subsidiaries and over 6,000 related-party transactions in one year. This complexity makes it hard to track financial activities, raising concerns about transparency.

- Questionable Shareholdings: Hindenburg questioned the large number of Adani Group shares held by offshore funds, suggesting these funds might be controlled by the Adani Group to manipulate stock prices.

- Silencing Journalists: Another serious accusation was that the Adani Group has used its influence to silence journalists who report critically on the company, with some even being jailed.

Hindenburg’s Key Points

Hindenburg’s report wasn’t just about new accusations; it also pointed out existing issues:

- Overvalued Stocks: Hindenburg claimed that the seven key listed companies of the Adani Group are overvalued by as much as 85%, even without considering the new allegations.

- High Debt Levels: The Adani Group has taken on a lot of debt, much of it backed by shares that Hindenburg claims are inflated. This puts the group in a risky financial position.

Financial Health of Adani Group

Despite these allegations, the Adani Group has shown some positive financial trends:

- Lower Debt: The group has managed to reduce its debt-to-EBITDA ratio, meaning its debt is now smaller compared to its earnings.

- Earnings Growth: The group’s earnings have been growing at a healthy rate of 22% per year.

- Continued Borrowing: However, the group’s debt has also been growing, showing it still relies heavily on borrowing.

Adani Group’s Response

In response to the Hindenburg report, the Adani Group issued a 413-page rebuttal, strongly denying all allegations and defending its practices:

- Transparency and Compliance: The group argued that most of the issues raised by Hindenburg were already disclosed in their financial reports.

- Legal Standards: Adani stated that it follows the highest standards of governance and accused Hindenburg of not understanding Indian laws.

- Market Manipulation Claims: The group suggested that Hindenburg’s report was a deliberate attempt to manipulate the market for financial gain, as Hindenburg stands to profit from a decline in Adani’s stock prices.

Impact on Adani Group Stocks

The Hindenburg report has significantly impacted the Adani Group’s stock prices:

- Massive Losses: The group has lost over $48 billion in market value since the report was published, causing a sharp decline in investor confidence.

- Stock Performance:some text

- Adani Enterprises: -1.50%

- Adani Green: -3.08%

- Adani Ports: -6.59%

- Adani Transmission: -8.85%

These sharp declines have also affected the broader Indian stock market, with Adani Group stocks dragging down the indices.

Conclusion

The clash between Hindenburg and the Adani Group has created significant turmoil in the Indian stock market and raised serious questions about the Adani Group’s business practices. While the Adani Group has strongly denied the allegations, the controversy has led to a massive drop in stock prices and a loss of investor confidence. The long-term impact on the Adani Group remains to be seen as the situation continues to unfold.

भारतीय बजट और फेड बैठक से मिलेगी कीमती धातुओं को नई दिशा

कॉमेक्स में सोने की कीमते 9 महीने की उचाई 1941 डॉलर प्रति औंस, की उचाई पर चल रही है जबकि एमसीएक्स में सोना उच्चतम स्तरों पर चल रहा है। हालांकि, चांदी की कीमतों में, औद्योगिक मांग में कमी के रहते दबाव देखने को मिल रहा है। साल 2023 में आर्थिक मंदी का डर अभी बना हुआ है और कीमती धातुओं में निवेशकों को आगे के नज़रिये के लिए अमेरिका के प्रमुख आकड़ो का इंतजार है। पिछले सप्ताह चीन में लूनर न्यू ईयर हॉलिडे के चलते वैश्विक बाज़ारो में कारोबार कम रहा। बेंचमार्क अमेरिकी ट्रेज़री यील्ड में दबाव बना हुआ है जिसके कारण अमेरिकी डॉलर, जो सोने के विपरीत दिशा में चलता है, में दबाव बना हुआ है और पिछले सप्ताह यह 101 के स्तरों को छु चूका है। अमेरिकी फेड द्वारा ब्याज़ दर वृद्धि पर नरमी दिखाई गई है जबकि यूरोपियन सेंट्रल बैंक अगली दो बैठकों में 0.50 प्रतिशत वृद्धि करने का अनुमान है। हाल के सप्ताहों में, कीमती धातुओं के भाव में हैवन मांग और फेडरल रिजर्व द्वारा आने वाले महीनों में ब्याज दरों में वृद्धि की गति को धीमा करने की बढ़ती उम्मीदों से, कीमती धातुओं में तेजी आई है। निवेशकों की इन उम्मीदों से डॉलर और अमेरिकी ट्रेज़री यील्ड में गिरावट आई है और कीमती धातुओं को इससे फायदा हुआ है। हालांकि, फेड द्वारा ब्याज दर वृद्धि को धीमा किया गया है, लेकिन इसके उच्चतम स्तर के बारे में कोई संकेत नहीं है और मुद्रास्फीति अभी भी 40 साल की उचाई के करीब बनी हुई है। अमेरिकी डेब्ट सीलिंग लिमिट की चिंता भी निवेशकों को कीमती धातुओं की और आकर्षित कर रही है।

इस सप्ताह अमेरिकी पैरोल के आंकड़े, एफओएमसी और यूरोपियन सेंट्रल बैंक की बैठक, और भारतीय आम बजट कीमती धातुओं के लिए महत्वपूर्ण है, जिससे इनके भाव को नई दिशा मिल सकती है।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं के भाव में महत्वपूर्ण इवेंट्स के चलते अस्थिरता रहने की सम्भावना है। सोने में सपोर्ट 56000 रुपये पर है और रेजिस्टेंस 58000 रुपये पर है। चांदी में सपोर्ट 66500 रुपये पर है और रेजिस्टेंस 70500 रुपये पर है।

Important Pointers of Economic Survey 2023-24

A day before the Union Budget, which will be unveiled by Finance Minister Nirmala Sitharaman on Wednesday, February 1, 2023, the Economic Survey for 2023–24 was introduced in Parliament on Tuesday, January 31, 2023. The Economic Survey, which is issued every year a day before the budget and analyses the performance of every area of the economy before making recommendations for the future, is a report card on the state of the economy.

Key Highlights

- India's economy will expand by 6.5% in 2023–2024 compared to this fiscal's 7% growth and 2021–2022's 8.7% expansion. In the upcoming fiscal year, nominal GDP (gross domestic product) is expected to reach 11%.

- Private consumption, more capital expenditures, a better corporate balance sheet, increased financing to small enterprises, and the return of migrant workers to cities all contributed to growth.

- Depending on global economic and political developments, real GDP growth is expected to be between 6 and 8.0% in the upcoming fiscal year.

- The probability of additional interest rate increases by the US Fed presents a challenge to the rupee's decline.

- As long as global commodity prices stay high and the pace of economic expansion is maintained, the current account deficit (CAD) may continue to increase. The rupee may see devaluation pressure if CAD widens much more.

According to the most recent Reserve Bank of India (RBI) figures, the nation's current account deficit increased to 4.4% of GDP in the quarter ending in September from 2.2% of GDP during the April-June period as a result of a larger trade imbalance.

- India has enough foreign exchange reserves to cover CAD and participate in the Forex Trading market to control currency volatility.

- The second half of the current fiscal year has seen a slowing in export growth after the first half of the year and the increase in growth rates in 2021–22 caused production processes to move from "mild acceleration" to "cruise mode."

- The loss of export stimulus in the second part of this year was caused by the slowing global economy and declining worldwide commerce.

- On the strength of low inflation and moderate lending costs, bank credit growth is anticipated to be robust in FY24.

- Over 30.5% more credit was extended to small firms between January and November of 2022.

- In the current fiscal year's April to November, central government capital expenditures increased by 63.4%.

- The stock market generated gains in 2022 despite the removal of FPI.

- In the current fiscal year, private consumption and capital formation have driven economic growth and helped create jobs; urban employment rates have decreased while Employee Provident Fund registration has increased.

- The survey suggested that "entrenched inflation" could prolong the tightening cycle, causing borrowing costs to remain higher for longer.

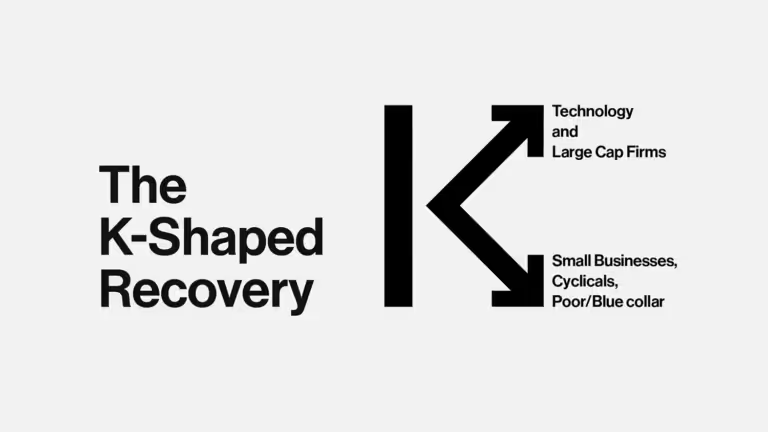

The K-Shaped Economic Recovery Explained

K-Shaped Recovery

A K-shaped recovery happens when various sectors, industries, or groups of people in the economy recover at various speeds, periods, or amounts. In this type of recovery, certain industries flourish while others stagnate or even dip more. K-shaped recoveries are typically brought on by pre-existing discrepancies or by a recession that has distinct effects on different populations and groups.

The image below is an example of a K-shaped recovery wherein certain industries or sectors perform well and grow while others go into decline and continue to stagnate.

(IMG Credits: Drishti IAS)

A K-shaped recovery could be caused by a variety of distinct economic events. First, a K-shaped recovery can represent the creative destruction that takes place in an economy during a recession when new technology and industries displace older ones. Second, it may show how the government has responded to a downturn in terms of fiscal and monetary policy, which might favor particular parts of the economy more than others.

Alternately, it may merely reflect the disparate effects that the initial recession had on the various sectors of the economy, particularly when the recession occurs concurrently with or is brought on by adverse real economic shocks that target particular sectors of the economy and may have longer-lasting effects on those sectors than on others. Keep in mind that these three requirements might not be exclusive of one another; they might all be at work in a particular K-shaped recovery together with additional elements.

It is hard to say for sure if India is experiencing a K-shaped recovery. However, certain indicators which indicate a K-shaped recovery in India are:

- Two-wheelers are a symbol of India's small businesses as well as the economic position of the lower and middle classes. According to a survey by the analytical firm CRISIL, two-wheeler sales are predicted to fall between 3% and 6% in 2021. This is on top of a lower base that was already impacted by the pandemic in 2020. The actual decrease in two-wheeler sales from before the pandemic must be significantly greater as a result of the base effect. Two-wheeler sales are at their second-lowest level in seven years. It is crucial to remember that among two-wheelers, entry-level vehicles are the ones most adversely impacted. The festival season was supposed to address this issue, but it failed to do so. On the other hand, premium cars and premium motorcycles have been resistant to the pandemic slowdown.

- Over 5 lakh people lost jobs after the lockdown started. Post this, there was a need for an increase in NREGA expenditure to accommodate more people for jobs. However, in the year 2021-2022, the Government of India cut its budget allocation towards MGNREGA by 34%. Thus, the unemployment rate didn’t ease off to pre-COVID levels even after the lockdown was lifted.

A deeper dive into the data of disposable income of the lower, middle, and upper class will show a similar trend which is the reason for the K-shaped recovery.

बेहतर रोज़गार के आकड़ो से कीमती धातुओं में सुधार

सोने की कीमते पिछले सप्ताह कॉमेक्स वायदा बाजार में सात महीने के उच्च स्तरों को छू चुकी है जबकि एमसीएक्स में कीमते 56000 रूपये प्रति दस ग्राम के स्तरों को छू चुकी है। हालांकि, अमेरिका से जारी एडीपी नॉन फार्म एम्प्लॉयमेंट चेंज, बेरोज़गारी के दावे और पैरोल के आकड़ो का बेहतर प्रदर्शन से कीमती धातुओं में उच्च स्तरों पर मुनाफ़ा वसूली रही। फेड मीटिंग के मिनट्स के अनुसार छोटी ब्याज दरों में बढ़ोतरी की संभावना ने डॉलर इंडेक्स पर दबाव बनाया है, जिससे 2022 में एक बुल रन के बाद ग्रीनबैक उच्चतम स्तरों से पलट गया है, और आने वाले महीनों में इसकी कमजोरी कीमती धातुओं को सपोर्ट करेंगी। अमेरिकी ट्रेजरी यील्ड, फेड मिनटों के बाद तेजी से गिरकर तीन सप्ताह के निचले स्तर पर आ गई। फेड मिनट्स स्पष्ट हुआ है कि नीति निर्माताओ की प्राथमिकता मुद्रास्फीति को कम करना है, और उच्च ब्याज दरों को लंबे समय तक बनाए रखने के लिए तैयार हैं। जिससे कीमती धातुओं की तेज़ी सीमित रह सकती है।

लेकिन, अन्य प्रमुख अर्थव्यवस्थाओं में धीमी व्यावसायिक गतिविधि के संकेतों का भी कीमती धातुओं के लिए सकारात्मक है। चीन और अमेरिका की मैन्युफैक्चरिंग पीएमआई के आंकड़े 50 के स्तरों के नीचे है, जो आर्थिक मंदी के डर को बढ़ा रहा है। इंटरनेशनल मॉनेटरी फण्ड द्वारा दुनिया की तीन बड़ी अर्थव्यवस्था अमेरिका, चीन और यूरोप की अर्थव्यवस्था को संकट में बताया है, जिससे कीमती धातुओं में सेफ हैवन मांग बनी हुई है।

सप्ताह के आंकड़े

इस सप्ताह अमेरिका से, मंगलवार को फेड चेयर जेरोम पॉवेल की स्पीच, गुरुवार को सीपीआई (मुद्रास्फीति) और शुक्रवार को कंस्यूमर सेंटीमेंट के आंकड़े प्रमुख है।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं में तेज़ी रहने की सम्भावना है। सोने में सपोर्ट 54000 रुपये पर है और रेजिस्टेंस 56100 रुपये पर है। चांदी में सपोर्ट 67000 रुपये पर है और रेजिस्टेंस 70500 रुपये पर है।

ऐसी और कमोडिटी मार्केट की लेटेस्ट अपडेट के लिए आज ही स्वस्तिका में अपना अकाउंट खुलवाएं

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App