Cyient Stock Price Rally: Key Catalysts Behind DLM Upside

Key Takeaways

- Cyient DLM stock price has surged 106% from its March 52-week low of ₹264.95.

- 12-month broker targets span ₹580 to ₹650, with an order book over ₹2,400 crore.

- The revenue mix is diversified: aerospace & defence 48%, industrials 26%, medtech 20%, others 7%.

- Facilities run at 50-60% utilisation with China+1 tailwinds and rising defence and aerospace spends supporting upside.

The cyient stock price has surged 106% from its 52-week low of ₹264.95 touched on March 30, 2026, signaling renewed enthusiasm around Cyient DLM's growth trajectory. Cyient DLM is an integrated Electronics Manufacturing Services (EMS) provider and Design-Led Manufacturing (DLM) provider; a subsidiary of Cyient Limited. With facilities running at 50-60% utilisation, China+1 tailwinds and rising defence and aerospace spends, the company appears well-positioned to grow. The search interest around cyient stock price remains robust, with approximately 110,000 monthly queries indicating sustained investor attention.

As the market applies its lenses on Cyient DLM, the stock price has breached multiple milestones. It hit a 52-week high of ₹546.55, rallying 9% on the BSE intra-day. It also surpassed its previous high ₹523.65 touched on July 3, 2026, and the record high ₹882.90 achieved on February 26, 2024. Across the broader market, the BSE Sensex rose 0.14% to 78,392 at 02:33 PM, providing a steady backdrop for cyclically sensitive names such as Cyient DLM. The ongoing interest in cyient stock price is evident in the trading screens as investors watch new highs and potential for further upside driven by backlog realization and margin expansion.

Cyient Stock Price Rally Fueled By DLM Order Book Momentum

One of the central drivers behind the cyient stock price rally is Cyient DLM's strong order book. Yes Securities reports an order book over ₹2,400 crore with a book-to-bill ratio above 1x, and delayed revenues set to flow into FY27. This suggests more revenues in the next 12–24 months, potentially lifting margins and cash flow as revenues realize the backlog. Motilal Oswal notes a 10-quarter high order book of ₹2,420 crore and a book-to-bill ratio around 2x, indicating expansion opportunities beyond aerospace and defence into automotive, semiconductor equipment, AI infrastructure, and domestic defence opportunities to support the cyient stock price momentum.

With utilisation currently at 50-60%, there is room for higher production without a proportional capex spike. The multi-year growth runway is supported by rising defence and aerospace spends and the broader “China+1” tailwinds that many global electronics manufacturers are prioritising. The sector tailwinds, combined with a robust backlog and improving operating leverage, are what investors are chasing when they look at the cyient stock price trajectory. The theme of rebounding demand and capacity utilisation should be watched closely as the stock price tests prior highs. Retail investors should keep a close eye on quarterly backlog realizations and how quickly delayed revenues start contributing to FY27 numbers.

Cyient DLM Stock Revenue Mix And Growth Prospects Across Aerospace, Defence And Other Segments

The revenue mix for Cyient DLM underscores its diversified exposure. Aerospace & defence contributes 48% of revenue, followed by 26% from industrials, 20% from medtech, and 7% from others. This mix positions Cyient DLM to capitalize on the strongest secular drivers: aerospace and defence outlays and a push into adjacent high-growth electronics segments. Motilal Oswal highlights that the company is expanding beyond traditional aerospace and defence into automotive and semiconductor equipment, AI infrastructure, and domestic defence opportunities, reinforcing the growth trajectory implied by the order book and the cyient stock price momentum.

Analysts point to the potential for revenue growth in FY26-28, with ICICI Securities projecting a CAGR of 24% and PAT CAGR of 35% over FY26-28E. The broker also cites a target price of ₹650 (38x FY28E EPS). These growth expectations align with the 2x book-to-bill ratio and the 10-quarter high order book reported by Motilal Oswal. The combination of diversified revenue streams and a robust order book could translate into a higher revenue base in the next two to three years, supporting a higher cyient stock price if execution remains intact.

Cyient Share Price Target 2025: Analyst Views And Targets

Brokerages are constructive on current levels, with a spread of target prices reflecting different growth assumptions. YES Securities assigns a 12-month target price of ₹580 per share, while ICICI Securities places a target price of ₹650 with a 38x FY28E EPS multiple. The market consensus implies a potential for the cyient share price target 2025 to lie within this range, given the expected revenue growth (24% CAGR FY26-28E) and the ability to double revenues with limited capex. The positive setup is supported by a 10-quarter high order book of ₹2,420 crore in Motilal Oswal's note and the 2x book-to-bill ratio, underscoring how backlog execution could translate into sustained revenue growth in FY27. The cyient stock price trajectory could see further upside if execution remains on track and defence and aerospace demand sustains.

In the longer term, the China+1 tailwinds and rising defence and aerospace spends position Cyient DLM well for growth. ICICI Securities signals a stronger revenue trajectory for FY26-28, while YES Securities highlights the utilisation improvements and the potential for delayed revenues to flow in FY27. For investors watching cyient stock price dynamics, these targets provide useful benchmarks, but the path to those targets will depend on execution, supply chain resilience, and continued demand strength across the aerospace and defence segments. The cyient share price target 2025 should be interpreted in the context of these evolving tailwinds and the company's ability to convert backlog into realized revenue.

Cyient Stock Price Risks And How Investors Can Manage Risk

Despite the optimism around Cyient DLM, there are risks to the cyient stock price move that investors should monitor. The company operates in a capital-intensive sector; despite a robust order book, execution delays, supply chain constraints, or shifts in defence budgets can influence revenue realization. The stock's move to record highs in 2024 and the subsequent strong rally from March 2026 lows reflect a market discount to the potential upside. A key risk is valuation: while brokerages are bullish, the prices might adjust if the growth expectations stall or if incremental capex requirements prove higher than anticipated.

Practical risk management for retail investors includes setting price alerts and defining risk budgets. The Sarthi AI stock assistant from Swastika can be a useful resource to quickly study company fundamentals, sector trends, and alternative ideas. You can explore Swastika's Sarthi AI stock assistant here: Swastika's Sarthi AI stock assistant.

Frequently Asked Questions

What has driven the Cyient stock price rally recently?

The cyient stock price has climbed 106% from its 52-week low of ₹264.95 touched on March 30, 2026, aided by a robust order book (over ₹2,400 crore) and growth from Cyient DLM’s diversified segments — aerospace & defence, industrials, and medtech. A China+1 tailwind and rising defence and aerospace spends underpin the momentum, while a record high in 2024 and recent highs against a generally positive market backdrop add to investor optimism.

What is Cyient DLM's order book and what does it imply for the stock price?

Yes Securities reports an order book over ₹2,400 crore with a book-to-bill ratio above 1x and expects delayed revenues to flow into FY27. Motilal Oswal notes a 10-quarter high order book of ₹2,420 crore and a book-to-bill around 2x, indicating expansion opportunities beyond aerospace and defence into automotive, semiconductor equipment, AI infrastructure, and domestic defence opportunities to support the cyient stock price momentum. These metrics imply potential revenue growth, which could support further upside in Cyient's stock price if execution remains solid.

What are the brokerages' 12-month targets for Cyient stock price?

Brokerages show a bullish range: YES Securities assigns a 12-month target price of ₹580 per share, while ICICI Securities places a target price of ₹650 (38x FY28E EPS). These targets reflect expected revenue growth of about 24% CAGR over FY26-28 and a healthy path to improving margins, supported by a strong order book and tailwinds from defence and aerospace spending.

What is Cyient DLM's revenue mix and why does it matter?

The revenue mix is aerospace & defence 48%, industrials 26%, medtech 20%, and others 7%. This diversification matters because aerospace and defence are typically higher-margin, large-contract sectors with long project cycles, while expansion into automotive, semiconductor equipment, and AI infrastructure (highlighted by Motilal Oswal) could broaden the growth runway for Cyient DLM in FY26-28 and beyond.

What price milestones have Cyient stock price crossed recently and historically?

The stock hit a 52-week high of ₹546.55 and surpassed the previous high ₹523.65 on July 3, 2026. It had previously reached a record high of ₹882.90 on February 26, 2024. In the most recent rally, the price is up approximately 106% from the March 2026 low of ₹264.95, reflecting a strong positive momentum in the market context where the BSE Sensex rose 0.14% to 78,392.

Conclusion

The Cyient stock price is riding on a mix of a high-quality order book, diversified revenue streams, and favourable macro tailwinds like China+1 and rising defence spends. Retail investors now face a pivotal question: is this momentum sustainable, or is it a near-term spike? The answer depends on execution, the pace at which delayed revenues realize, and how the global macro environment evolves for electronics manufacturing and defence sectors. If the path remains intact, the stock could move higher as the cycle consolidates around the strong backlog and the projected FY26-28 growth. The next steps are to monitor the quarterly revenue realisation from the order book, track utilization improvements, and adjust risk controls as the price moves toward broker targets like ₹580 or ₹650.

Latest Articles

Stock Market for Beginners - Equity Market Full Course

Are you new to investing and looking to understand how the stock market works? You're not alone. Many people find the stock market complex and intimidating at first, but with the right information and guidance, anyone can learn to navigate it successfully. This blog will provide you with a complete overview of the stock market, including its processes and guidance for beginners to make learning easier. Whether you're looking to grow your savings, plan for retirement, or just learn more about investing, this guide will equip you with the knowledge you need to navigate the stock market confidently. By the end, you’ll have a solid understanding of how the stock market operates and how to start investing with confidence.

What is the Stock Market?

The stock market is a platform where investors can buy and sell shares of publicly traded companies. Shares, also known as stocks or equities, represent a portion of ownership in a company. When you purchase a stock, you become a shareholder and own a piece of that company.

Key Terms

1. Stocks/Shares/Equities: Units of ownership in a company.

2. Stock Exchange: A marketplace where stocks are bought and sold (e.g., NSE, BSE).

3. IPO (Initial Public Offering): The first sale of a company’s stock to the public.

4. Bull Market: A period when stock prices are rising.

5. Bear Market: A period when stock prices are falling.

Why Invest in the Stock Market?

Investing in the stock market offers several benefits:

1. Potential for High Returns: The Indian stock market has demonstrated strong growth over the years, providing investors with substantial returns. The BSE Sensex, one of the leading stock market indices in India, has shown significant appreciation.

2. Ownership in Companies: When you buy stocks, you own a part of the company and can benefit from its growth and success.

3. Accessibility and Liquidity: The Indian stock market is highly liquid, with significant daily trading volumes. This liquidity ensures that investors can buy and sell stocks with ease, providing flexibility in managing their investments.

Diversification: Investing in a variety of stocks can help spread risk and reduce the impact of any single investment’s poor performance.

4. Stock Market Reforms

Reforms in the Indian stock market have enhanced transparency, efficiency, and investor protection. Regulatory bodies like the Securities and Exchange Board of India (SEBI) ensure a well-regulated and secure trading environment.

The introduction of electronic trading, depository services and stringent regulatory frameworks has made the Indian stock market more accessible and reliable for investors.

Dividend Income

5. Regular Income Streams

Many Indian companies offer attractive dividend yields, providing investors with regular income in addition to capital appreciation.

Process of Investing in the Stock Market

Step 1: Learn the Basics

Before you start investing, it’s important to understand the fundamentals of the stock market. This includes familiarizing yourself with key terms, market dynamics, and basic investment strategies.

Step 2: Open a Trading Account

To buy and sell stocks, you need to open a trading account with a brokerage company like Swastika Investmart, a reputable broker that offers a user-friendly platform and reasonable fees. Also, we provide an easy and secure way to open a trading account.

Step 3: Fund Your Account

After opening your trading account, you need to deposit funds into it. Swastika offers multiple payment options, including bank transfers and online payment systems.

Step 4: Research Stocks

Conduct thorough research before investing in any stock. Look into the company’s financial health, performance history, industry position, and future growth prospects. Use resources like financial news, company reports, and market analysis.

Step 5: Place Your Order

Once you’ve identified a stock you want to buy, place an order through your trading platform. There are different types of orders you can use:

- Market Order: Buy or sell a stock at the current market price.

- Limit Order: Buy or sell a stock at a specified price or better.

- Stop-Loss Order: Sell a stock when it reaches a certain price to limit losses.

Step 6: Monitor Your Investments

Regularly review your investment portfolio to ensure it aligns with your financial goals. Stay updated with market trends and news that could impact your investments. Adjust your portfolio as needed based on your research and market conditions.

Guidance for Beginners

Start Small

As a beginner, it’s wise to start with a small investment amount that you can afford to lose. This helps you gain experience and confidence without risking significant capital.

Diversify Your Portfolio

Don’t put all your money into one stock. Diversify your investments across different sectors and industries to reduce risk. This way, poor performance in one area can be offset by better performance in another.

Focus on Long-Term Goals

The stock market can be volatile in the short term, but historically, it has provided substantial returns over the long term. Avoid making impulsive decisions based on short-term market fluctuations. Instead, focus on your long-term financial goals and stay patient.

Stay Informed

Continuously educate yourself about the stock market. Read books, take courses, follow financial news, and learn from experienced investors. The more knowledge you gain, the better decisions you’ll make.

Use Analytical Tools

Take advantage of analytical tools and resources provided by your broker or other financial platforms. These tools can help you analyze stock performance, track market trends, and make smart investment decisions.

Seek Professional Advice

If you’re unsure about investing on your own, consider seeking advice from a financial advisor. They can provide personalized guidance based on your financial situation and goals.

Different types of Risk

Risks involved in stock market:

Market Volatility: Fluctuations in stock prices can lead to both gains and losses, driven by economic conditions, investor sentiment, and geopolitical events.

Individual Stock Risk: Risks specific to a company include poor financial performance, management changes, industry competition, or regulatory issues.

Liquidity Risk: Some stocks may have low trading volumes, making it difficult to buy or sell shares without affecting the price.

Interest Rate Risk: Changes in interest rates can impact stock prices, especially for sectors sensitive to borrowing costs like financials and utilities.

Currency Risk: For international investments, changes in exchange rates between currencies can affect investment returns.

Inflation Risk: Rising inflation can erode purchasing power and affect corporate profitability and stock prices.

Political and Regulatory Risk: Changes in government policies, regulations, or geopolitical events can impact market stability and stock prices.

Systematic Risk: Market-wide factors that affect all investments, such as recessions, wars, or natural disasters, can lead to widespread declines in stock prices.

Timing Risk: Poor timing of buying or selling investments can result in losses or missed opportunities.

Risk Management Strategies in Stock Market Investing:

Diversification: Spread investments across various asset classes (stocks, bonds, cash equivalents) to reduce exposure to any single investment's risk.

Asset Allocation: Determine the allocation of funds among different asset categories based on risk tolerance, financial goals, and time horizon.

Setting Risk Tolerance: Establish clear boundaries on the amount of risk you are willing to accept in your portfolio to align with your comfort level.

Regular Portfolio Review: Periodically assess and adjust your portfolio to maintain diversification and alignment with your risk tolerance and investment objectives.

Emergency Fund: Maintain a cash reserve for unexpected expenses to avoid the need to liquidate investments during market downturns.

Conclusion

Investing in the stock market can be a rewarding way to grow your wealth, but it’s important to approach it with knowledge and caution. By understanding the basics, doing thorough research, and following a disciplined investment strategy, you can increase your chances of success. Remember to start small, diversify your portfolio, and focus on long-term goals.

Download PDF Guide

By downloading this guide, you’ll gain access to:

- In-depth explanations of stock market concepts

- Step-by-step instructions for opening and funding a trading account

- Tips for researching and selecting stocks

- Strategies for managing and diversifying your portfolio

- Detailed infographics to simplify complex topics

Equip yourself with the knowledge and tools you need to become a confident and successful investor. Download our comprehensive PDF guide today and start your journey in the stock market with Swastika Investmart.

What are Growth Stocks?

Growth stocks are shares of companies with the potential to outperform the market. These stocks grow faster than the market due to strong fundamentals like a solid balance sheet, high earnings per share (EPS), and a good price-to-earnings (P/E) ratio. These factors help increase profits in the medium to long term.

Any share of a firm that is expected to increase at a rate substantially faster than the market average is considered a growth stock. Typically, these stocks don't pay dividends. This is so because companies that issue growth stocks typically seek to reinvest any money they make in order to short-term accelerate growth.

This growth is often due to unique products, innovative business plans, or patents. As these companies expand their market share, their stock prices tend to rise.

For example, technology firms in the late 1920s saw significant growth, which positively affected their stock prices. Today, companies developing innovative products or expanding rapidly in new markets might be considered growth stocks.

They are shares in companies with the potential for big future growth, even if they don't offer immediate benefits.

Example: Let's consider a technology company whose stock price has grown by 20% annually over the past five years. If you invested ₹1,00,000 five years ago, your investment would now be worth around ₹2,48,832.

Characteristics

- High Growth Rate: They grow at a significantly higher rate than the average market growth rate. This means they increase in value faster than the average stock.

- Zero Dividend: They usually do not pay dividends. Instead, these companies reinvest their earnings to boost their revenue-generating capacity.

- Solid Financials: A healthy balance sheet with low debt shows financial stability.

- High Earnings Per Share (EPS): This measures a company's profit per share, indicating its profitability.

- Strong Price-to-Earnings Ratio (P/E Ratio): This compares a stock's price to its earnings, and a higher P/E can indicate growth potential.

Pros

- High Returns: Over time, they have the potential to deliver much higher returns than the average stock.

- Market Leaders: They might become future industry leaders, leading to long-term gains for investors.

- Gradual Investment: You don't need a huge sum to start. You can gradually increase your investment in growth stocks as your budget allows.

Cons:

- High Risk: They can be risky because their future success is not guaranteed.

- No Dividends: Growth companies typically reinvest their profits back into the business to fuel further growth, so they usually don't pay dividends (regular payouts to shareholders).

- Short-Term Performance: Growth may not happen immediately. You might not see significant returns in the short term.

Why Invest?

Investing in growth stocks is an excellent strategy for building wealth over the long term. If you plan to invest for 10 years or more, they can help you accumulate significant wealth. These stocks tend to grow at a faster rate than inflation, which means that the value of your investment increases over time, and your money maintains its buying power.

Growth companies usually reinvest their profits back into the business instead of paying out dividends to shareholders. This reinvestment fuels further growth and innovation, leading to higher stock prices. As a result, your returns benefit from compound interest. For example, if you invest ₹1,00,000 in growth stocks that appreciate by 15% each year, your investment would grow to approximately ₹4,05,000 in 10 years, thanks to the power of compounding.

This compounding effect allows your returns to grow exponentially over time. By continually reinvesting earnings, they can provide substantial returns in the long run. This makes them an ideal choice for investors looking to build wealth and secure their financial future.

Conclusion

Growth stocks are not for everyone. They involve higher risk. Investing can be a smart choice for those looking for high returns and willing to take on more risk. Consider your risk tolerance and investment goals before investing.

Understanding Factors Affecting Share Prices

Share prices fluctuate constantly due to various factors. Understanding these factors can help you make better investment decisions. These factors can be internal or external.

Internal Factors:

- Company's Financial Performance: Profits, revenue, and overall financial health.

- Management Decisions: Strategies, changes in leadership, and business plans.

- Earnings Reports: Quarterly and annual financial statements.

External Factors:

- Economic Indicators: GDP growth, employment rates, inflation, and interest rates.

- Government Policies: Tax regulations, trade policies, and economic reforms.

- Global Events: Wars, pandemics, and international agreements.

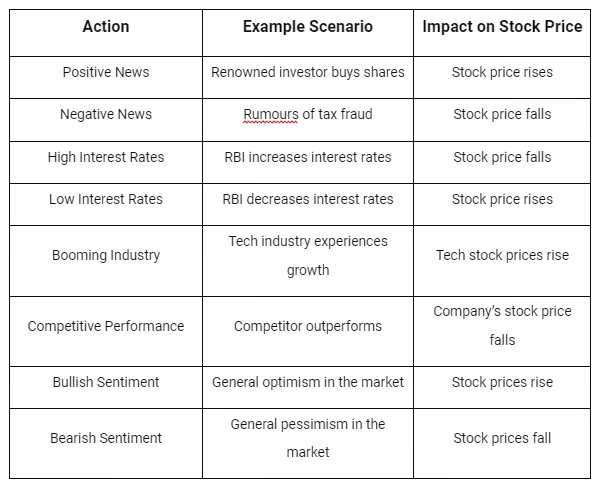

News and Rumours

News and rumours can significantly impact stock prices. For example:

- Positive News: When a famous investor buys shares of a company, its stock price often rises.

- Negative News: Reports of tax fraud can cause the stock price to fall, even without solid evidence.

- Mixed Reactions: News about mergers or acquisitions can either raise or lower the stock price, depending on market perception.

News and rumours impact stock prices mainly when they affect the company's fundamentals.

Political Factors

Political stability plays a crucial role in stock market performance:

- Instability: War threats, weak governments, and political unrest can lower stock prices.

- Elections and Budgets: Announcements can cause market volatility.

- Policies: New economic policies can impact stock prices either positively or negatively.

Interest Rates

Interest rates set by the Reserve Bank of India (RBI) affect stock prices:

- High Interest Rates: Companies face higher loan costs, reducing profits and stock prices.

- Low Interest Rates: Companies can borrow cheaply, increasing profits and stock prices.

Industry Trends

Competing companies often see their stock prices move together:

- Booming Industry: High demand for shares in a thriving industry can push up stock prices.

- Competitive Performance: A company's stock price may rise or fall based on how its competitors are doing.

Market Sentiment

Market sentiment reflects the collective attitude of investors:

- Bullish Sentiment: Positive outlook drives stock prices higher.

- Bearish Sentiment: Negative outlook drives stock prices lower.

Market sentiment influences consumer confidence, spending, and business investment. For instance, during the dot-com bubble, euphoric sentiment drove tech stock prices to unsustainable heights, followed by a significant crash.

Demand and Supply: The Fundamental Principle

The basic economic principle of demand and supply dictates stock prices:

- High Demand: More buyers than sellers push stock prices up.

- High Supply: More sellers than buyers push stock prices down.

Economic Indicators

Broader economic indicators impact overall market sentiment:

- Economic Downturns: Reduced consumer spending affects corporate earnings and lowers share prices.

- Thriving Economy: Higher consumer spending boosts corporate earnings and raises share prices.

Example in INR

Consider a hypothetical example to illustrate these factors:

Conclusion

Understanding the various factors affecting share prices, from company performance to economic indicators, is essential for making informed investment decisions. While this guide covers many key factors, remember that market sentiment can also be highly emotional and unpredictable. Analyzing these elements collectively can help you navigate the complex dynamics of the stock market.

Learn more about financial terminologies with Swastika!

What is a Margin Call?

A margin call is a wake-up call from your broker. When an investor's equity in a margin account drops below the minimum amount required by the broker, a margin call happens. Securities purchased using a combination of the investor's own funds and funds borrowed from the investor's broker are kept in an investor's margin account.

When a broker requests that an investor add more funds or securities to the account, it is known as a "margin call." This occurs when the investor's equity and the account value reach the minimum amount specified by the maintenance requirement.

Example: The Margin Call in Action

Let's say you buy ₹10,000 worth of stock using margin, meaning you borrow ₹5,000 from your broker. The maintenance margin might be 30%, which means the total value of your account (including the borrowed money) needs to stay above ₹7,000 (₹10,000 x 30%).

If the stock price falls, and the value of your account drops below ₹7,000, you'll get a margin call. You'll then need to deposit more money (or sell some stock) to bring the account value back up to the maintenance margin level.

Types of Margin

Margin trading involves borrowing funds from a broker to purchase securities. Here are the three main types of margin used in trading:

1. Initial Margin:

The amount of margin required to open a new position.

Example: If you want to buy ₹50,000 worth of stock, and the initial margin requirement is 50%, you'll need to deposit ₹25,000 in your account.

2. Maintenance Margin:

The minimum amount of equity you must maintain in your account to keep positions open.

Example: If the maintenance margin requirement is 25% and your account equity drops below this level due to losses, you'll receive a margin call.

3. Margin Call:

A demand from the broker for additional funds or securities if your account falls below the maintenance margin.

Example: If your account equity drops below the maintenance margin requirement, your broker will issue a margin call asking you to deposit more funds or securities to meet the margin requirement.

When Does a Margin Call Happen?

A margin call occurs when the value of your securities falls below the maintenance margin set by your broker. This usually happens if the market value of your borrowed securities drops. If this occurs, your broker will ask for more funds or securities to bring the margin back up.

How to Avoid Margin Calls:

Here are some smart moves to avoid getting a margin call:

- Keep cash handy: Just like having some savings for your car, having extra cash in your brokerage account acts as a buffer.

- Watch Your Portfolio: Regularly monitor your account value and the maintenance margin requirement. This way, you can see if you're getting close to a margin call and take action.

- Diversify Your Investments: Don't put all your eggs in one basket! Invest in a variety of stocks, bonds, and other assets to spread out your risk.

- Set Stop-Loss Orders: A stop-loss order automatically sells a stock if the price falls below a certain level. This can help limit potential losses and reduce the chance of a margin call.

The Bottom Line

Margin calls can be stressful, but by understanding them and using good risk management practices, you can avoid them and trade more confidently.

Most investors saving for long-term goals, like retirement, should avoid buying stocks on margin due to the higher risk.

Learn more about financial terminologies with Swastika!

.avif)

Positional Trading

Positional trading is a popular strategy in the stock market where investors hold their positions for an extended period, ranging from weeks to months or even years. This approach is ideal for those who prefer to take a longer-term view of the market and are less concerned with short-term price fluctuations. Let's dive into the details of positional trading and how it works.

What is Positional Trading?

Positional trading involves buying stocks with the expectation that their price will increase over time. Unlike day trading or swing trading, which focus on short-term movements, positional traders look at the bigger picture and hold their investments until their price targets are achieved or market conditions change.

Key Characteristics of Positional Trading

- Long-Term Perspective: Positional traders aim to benefit from long-term trends and fundamental changes in a company or the market.

- Lower Frequency of Trades: Because they hold positions for a longer duration, positional traders make fewer trades compared to day traders or swing traders.

- Fundamental and Technical Analysis: Positional traders use a combination of fundamental analysis (evaluating a company's financial health and growth potential) and technical analysis (studying price charts and indicators) to make decisions.

- Patience and Discipline: This strategy requires patience to wait for the right opportunities and discipline to stick to the plan without being swayed by short-term market movements.

Steps to Start Positional Trading

Research and Analysis:

- Fundamental Analysis: Evaluate a company's financial statements, earnings reports, management quality, industry position, and growth prospects. Look for companies with strong fundamentals that are likely to grow over time.

- Technical Analysis: Use charts and indicators to identify trends and potential entry and exit points. Common tools include moving averages, support and resistance levels, and trend lines.

Set Your Goals:

- Determine your investment goals and risk tolerance. Are you looking for steady growth, or are you willing to take on more risk for higher returns? Your goals will influence your stock selection and holding period.

Create a Trading Plan:

- Develop a clear plan outlining your entry and exit strategies, stop-loss levels, and position size. A well-defined plan helps you stay focused and avoid emotional decisions.

Choose the Right Stocks:

- Select stocks with strong growth potential and favourable market conditions. Look for companies in industries with positive long-term trends.

Monitor Your Positions:

- Regularly review your investments and market conditions. While positional trading requires less frequent monitoring than day trading, it's essential to stay informed about news and events that could impact your stocks.

Advantages of Positional Trading

- Potential for Higher Returns: By holding stocks for a longer period, positional traders can benefit from significant price movements and compound returns.

- Less Stressful: Unlike day trading, positional trading is less stressful as it doesn't require constant monitoring of the market.

- Lower Transaction Costs: Fewer trades mean lower transaction costs, which can add up over time.

- Tax Benefits: In many countries, long-term capital gains are taxed at a lower rate than short-term gains, which can enhance your overall returns.

Risks of Positional Trading

- Market Risk: Market conditions can change unexpectedly, impacting the value of your investments.

- Company-Specific Risk: Negative news or events related to a specific company can cause its stock price to drop significantly.

- Patience Required: Positional trading requires patience and the ability to withstand market volatility without making impulsive decisions.

- Capital Tied Up: Your capital is tied up for a longer period, which might limit your ability to take advantage of other investment opportunities.

Tips for Successful Positional Trading

- Diversify Your Portfolio: Spread your investments across different sectors and industries to reduce risk.

- Stay Informed: Keep up with market news, economic indicators, and company reports to make informed decisions.

- Avoid Emotional Trading: Stick to your trading plan and avoid making decisions based on emotions or short-term market noise.

- Review and Adjust: Periodically review your portfolio and adjust your positions based on changing market conditions and your investment goals.

Conclusion

Positional trading is a viable strategy for investors who prefer a long-term approach and are willing to invest time in research and analysis. By focusing on fundamental and technical factors, setting clear goals, and maintaining discipline, positional traders can potentially achieve substantial returns while managing risk. Whether you're a beginner or an experienced investor, positional trading can be an effective way to build wealth in the stock market.

Stay updated with Swastika for more market insights. JOIN NOW!

Equity Trading in the Share Market

Equity trading, also known as stock trading, is the buying and selling of shares of companies in the stock market. It is a fundamental way for investors to grow their wealth and participate in the financial markets. Let's break down the basics of equity trading in simple language.

What Are Equities?

Equities, or stocks, represent ownership in a company. When you buy a share of a company, you own a small part of that company. This ownership entitles you to a portion of the company's profits, which can be paid out as dividends. Additionally, if the company grows and becomes more valuable, the value of your shares can increase, allowing you to sell them for a profit.

What Is Equity Trading?

Equity trading involves buying and selling these shares on the stock market. The stock market is a platform where investors can trade stocks with each other. The two main types of stock markets are:

- Primary Market: This is where companies sell their shares to the public for the first time through an Initial Public Offering (IPO).

- Secondary Market: This is where existing shares are traded among investors. Most of the trading happens in the secondary market.

How Does Equity Trading Work?

Equity trading typically follows these steps:

- Opening an Account: To start trading, you need to open a trading account with a stockbroker. This account allows you to buy and sell shares.

- Placing an Order: You place an order to buy or sell shares through your trading account. Orders can be placed online, through a mobile app, or by calling your broker.

- Order Execution: Once your order is placed, it is sent to the stock exchange where it gets matched with a corresponding buy or sell order. If there is a match, the trade is executed.

- Settlement: After the trade is executed, the shares are transferred to your account, and the money is deducted or credited accordingly. This process usually takes a couple of days.

Types of Equity Trading

There are different ways to trade equities, including:

- Day Trading: Buying and selling stocks within the same trading day. Day traders take advantage of small price movements and aim for quick profits.

- Swing Trading: Holding stocks for a few days to weeks to benefit from expected price swings. Swing traders use technical analysis to make decisions.

- Long-Term Investing: Buying and holding stocks for months or years. Long-term investors focus on the company's fundamentals and growth potential.

- Scalping: Making numerous small trades to earn small profits on each trade. Scalping requires quick decision-making and fast execution.

Key Concepts in Equity Trading

Market Orders and Limit Orders:

- Market Order: An order to buy or sell a stock immediately at the current market price.

- Limit Order: An order to buy or sell a stock at a specific price or better.

Bid and Ask Price:

- Bid Price: The highest price a buyer is willing to pay for a stock.

- Ask Price: The lowest price a seller is willing to accept for a stock.

The difference between the bid and ask price is called the spread.

Bull and Bear Markets:

- Bull Market: A period when stock prices are rising or expected to rise.

- Bear Market: A period when stock prices are falling or expected to fall.

- Diversification: Spreading investments across different stocks to reduce risk. Diversification helps protect your portfolio from the poor performance of a single stock.

Risks and Rewards of Equity Trading

Rewards:

- Potential for High Returns: Stocks have historically offered higher returns compared to other investments like bonds and savings accounts.

- Ownership: Owning stocks means you have a stake in the company's success and can benefit from its growth.

- Dividends: Some companies pay dividends, providing a regular income stream.

Risks:

- Market Risk: Stock prices can be volatile and unpredictable, leading to potential losses.

- Company-Specific Risk: A company's poor performance or adverse news can negatively impact its stock price.

- Economic Risk: Economic downturns can affect the entire stock market and your investments.

Conclusion

Equity trading is an essential part of the financial markets, offering opportunities for wealth creation and participation in a company's growth. By understanding the basics of how equity trading works, the types of trading, and the associated risks and rewards, you can make decisions and develop effective trading strategies. Whether you are a beginner or an experienced trader, staying informed and disciplined is key to success in the stock market.

Stay updated with Swastika for more market insights. JOIN NOW!

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App