Url Fetch Error And Real-Time Market Data For Indian Retail Investors

Key Takeaways

- url fetch error can disrupt real-time stock quotes and trigger trading delays.

- Verify data feeds against multiple sources before making decisions.

- Use Swastika's Sarthi AI stock assistant to cross-check stock insights.

- Prepare a quick recovery plan to switch feeds when a fetch error occurs.

In the fast-moving Indian stock markets, your screen is only as good as the data feeding it. A url fetch error can flicker quotes, stall charts, and leave you guessing your next move. For retail investors, the stakes are practical: a few seconds of delay can tilt decisions, especially when you track dynamic tick data for names such as reliance industries share price or infosys stock price. In this guide, we unpack what url fetch error means, how to detect it, and what to do when data streams falter.

Understanding data reliability is not about jargon; it is about keeping your portfolio aligned with real prices when the feeds you depend on lag or fail. The digital trading desk rewards discipline: know what to measure, how to spot anomalies, and how to respond quickly when a fetch error interrupts your data stream.

Url Fetch Error In Market Data Feeds: What Retail Investors Should Know

The concept of url fetch error arises when a client tries to retrieve market data from a server and the request fails due to network, DNS, or server issues. In practice, this results in stale quotes, missing candles, or delayed tick-by-tick updates. For retail investors, the immediate consequence is uncertainty: you might see a price that does not reflect the latest trade. The remedy is not simply to refresh; it’s to understand data feeds' architecture and implement safeguards. Most trading desks operate with multiple feeds to cross-verify price points, and many platforms maintain a local cache to bridge brief outages without interrupting decision timelines.

To minimize the risk, investors should treat price data as a probabilistic signal rather than a single guaranteed quote. For example, if a screen shows reliance industries share price with a suspiciously stale timestamp, or if another feed reports a slightly different value, use the timestamp and source notes to guide your next action rather than rushing a trade.

How Reliable Are The Data Feeds For Reliance Industries Share Price And Infosys Stock Price?

Data feed reliability depends on infrastructure, network latency, and how providers handle outages. It is common to see price mismatches during a url fetch error across sources. Investors should cross-check quotes for the same time window when possible; compare the reliance industries share price and infosys stock price across feeds; use time-stamped quotes to ensure accuracy. A practical approach is to monitor two or more feeds in real time and to record any persistent discrepancies. When the feeds disagree, rely on the feed with the tighter latency and the more precise timestamp. This reduces the risk of acting on out-of-date data.

Beyond raw quotes, corporate actions such as dividends also influence price signals. Keep a running log of when corporate actions are announced and how quickly each feed reflects the change. If you notice consistent lag for a specific security–say an index component or a top-name like infosys stock price–you may want to adjust your watchlist or switch to an alternative feed temporarily while the outage lasts.

Mitigating Risk With Real-Time Data: Stock Price Of TCS And Other Major Names

To reduce reliance on a single feed, adopt data redundancy. For example, monitor the stock price of tcs across two independent feeds and verify against official exchange data. In volatile markets, micro-delays can cause divergence between actual trades and reported quotes. Build a routine to refresh data at short intervals and log any anomalies for later review. A robust routine includes setting alert thresholds: if the price moves beyond a pre-set band within a few seconds, trigger a cross-check with another feed before you act.

In practice, a disciplined investor uses risk controls around feed reliability. For example, you can implement a rule: if one feed shows price movement without a matching timestamp or with an out-of-band calculation, do not execute a trade until the other feed confirms. This approach helps prevent impulsive trades during feed outages and protects your capital from sudden, feed-driven whipsaws.

Diversifying Data Feeds: Hdfc Bank Stock Price And Bajaj Finance Limited Stock Price Across Feeds

Major banks and NBFCs can exhibit different update patterns. Investors should compare hdfc bank stock price and bajaj finance limited stock price across feeds for the same timestamps to avoid acting on stale or divergent quotes. A simple practice is to pull quotes from two providers and verify they share a consistent last-trade price and timestamp. If one feed lags, switch to the other and note the discrepancy for post-trade review. In some cases, an outage on one provider can coincide with a faster feed from another, creating an opportunity to arbitrage or simply avoid a mistaken move based on stale data.

| Check | Action |

|---|---|

| Latency | Prefer feeds with lower latency and synchronized timestamps |

| Redundancy | Have at least two independent feeds ready |

| Outages | Switch to backup feed during service interruptions |

| Corporate Actions | Verify dividends, splits, and other actions with official sources |

As part of a robust workflow, consider a quick reference to Swastika's Sarthi AI stock assistant for cross-validation. Swastika's Sarthi AI stock assistant can help you parse live data against model insights and institutional-grade analyses.

Icici Bank Dividend And Data Feed Consistency: How Dividends Tie To Price Data

Corporate actions like the icici bank dividend are key price drivers, and data feeds should reflect these events promptly. When a feed lags on dividend announcements or ex-date changes, price adjustments may appear late in one feed but not in another. Retail investors should track such actions across feeds and rely on official exchange notices to corroborate the timing and amount of the dividend. Consistent reflections across feeds reduce the risk of mispricing around ex-dates and help preserve accurate cost bases for tax planning.

Frequently Asked Questions

What is a url fetch error in market data feeds?

A url fetch error occurs when a data fetch request to a server fails due to network, DNS, or server issues, resulting in missing or delayed price data.

How can retail investors mitigate url fetch error risks?

Use multiple data sources, enable failover, validate quotes across feeds, cache recent prices, and maintain a manual price check during outages.

Which data sources should I trust for price data such as reliance industries share price and infosys stock price?

Rely on official exchange feeds and reputable data providers, then cross-check quotes across sources and use time-stamped data to verify accuracy.

What should I do if icici bank dividend or other corporate actions are not reflected due to a data fetch issue?

Cross-check with official announcements, verify corporate actions across feeds, and note any delays that could affect cost basis and timing of trades.

How can Swastika's Sarthi AI stock assistant help with data reliability?

Swastika's Sarthi AI stock assistant helps cross-validate live data against model insights and institutional analyses, improving decision confidence during feed outages.

Conclusion

Url fetch error is not a barrier to successful investing, but a reminder to design resilient data workflows. Build redundancy, verify quotes across feeds, and keep a clear decision framework so you can act confidently when real-time data flutters. The path forward is to test your data stack, document discrepancies, and stay aligned with reliable sources. By incorporating a structured, multi-source approach, you can reduce risk and stay focused on your investment goals even when data glitches occur.

Open your trading and demat account here

Reference :

1 : Google

Latest Articles

Positional Trading in the Stock Market: Understanding the Basics

In the dynamic world of the stock market, traders employ various strategies to capitalize on market movements and generate profits. One such strategy that has gained popularity among traders is positional trading. But what exactly is positional trading, and how does it differ from other trading approaches? In this blog, we'll break down the basics of positional trading in simple language, exploring its meaning, strategies, and key differences from other trading styles.

What is Positional Trading?

Positional trading is a trading strategy where traders hold positions in stocks or other financial instruments for an extended period, typically ranging from several days to several weeks or even months. Unlike day trading, which involves buying and selling securities within the same trading day, positional traders aim to capture larger price movements over a more extended timeframe.

Understanding the Positional Trade Meaning

In positional trading, traders take positions in anticipation of sustained price movements in the market. They base their trades on thorough analysis of market trends, technical indicators, and fundamental factors, aiming to ride the trend for maximum profit potential. Positional traders are less concerned with short-term fluctuations and focus instead on the broader market direction.

Positional Trading Strategy

Positional traders employ a variety of strategies to identify profitable trading opportunities. Some common positional trading strategies include:

- Trend Following: Positional traders identify market trends and enter positions in the direction of the trend. They use technical indicators such as moving averages, trendlines, and momentum oscillators to confirm the trend and determine entry and exit points.

- Breakout Trading: Positional traders look for breakout opportunities, where a stock or market breaks out of a trading range or consolidation pattern. They enter positions when the price breaks above resistance levels or below support levels, expecting the breakout to lead to a sustained price move.

- Swing Trading: While swing trading and positional trading is similar in some respects, positional traders typically hold their positions for a more extended period compared to swing traders. Swing traders aim to capture short-to-medium-term price swings within the broader market trend.

Position vs. Holding: Clarifying the Difference

In the context of trading, the term "position" refers to the specific securities or contracts that a trader holds in their portfolio at any given time. It represents the trader's exposure to the market and can include both long (buy) and short (sell) positions. "Holding," on the other hand, refers to the act of retaining ownership of securities over an extended period, irrespective of short-term price movements.

Open Position in Stock Market and Trading

An open position in the stock market or trading refers to a trade that has been initiated but not yet closed. It represents the trader's current exposure to the market and can result in either profits or losses depending on subsequent price movements. Traders may choose to close their open positions to realize gains or cut losses.

Positional Trading vs. Swing Trading

While both positional trading and swing trading aim to capture trends in the market, there are some key differences between the two approaches. Positional trading involves holding positions for a more extended period, often weeks or months, to capitalize on broader market trends. In contrast, swing trading typically involves holding positions for a shorter duration, ranging from a few days to a few weeks, to capture shorter-term price swings within the trend.

Conclusion

Positional trading offers traders the opportunity to capitalize on sustained market trends and generate profits over the medium to long term. By understanding the basics of positional trading, employing effective trading strategies, and managing risk appropriately, traders can harness the power of this approach to achieve their financial goals. Whether you're a seasoned trader or just starting, incorporating positional trading into your trading arsenal can provide you with a valuable tool for navigating the dynamic world of the stock market.

Remember, successful positional trading requires patience, discipline, and a thorough understanding of market dynamics. Stay informed, stay focused, and stay committed to your trading plan as you embark on your positional trading journey. With diligence and perseverance, you can unlock the potential of positional trading and take your trading to new heights.

Happy trading!

Future Trading in India

Ever wished you could lock in a stock price today to buy or sell it later? That's futures trading in a nutshell! It's like making a deal beforehand, saying "I'll buy this stock at ₹17,000 in 2 months," no matter what the price actually is then.

What are Futures Contracts and Why Do They Matter?

Imagine a contract that allows you to agree on a price today to buy or sell a specific asset (like a stock index) at a predetermined future date.

Why Futures?

- Boost your gains: If the stock price goes up, you can buy it at the lower locked-in price and sell it higher for a sweet profit!

- Protect yourself: Worried a stock might crash? Buy a futures contract to lock in a selling price so you don't lose too much.

- Hedge against price fluctuations: Protect your stock portfolio by locking in a selling price (if you expect prices to fall) or a buying price (if you expect prices to rise).

- Speculate on price movements: Profit from anticipating future price movements of stocks or indices.

Buying vs. Selling Futures

- Imagine a contract: This agreement says you'll buy or sell a stock (or a group of stocks like Nifty 50) at a set price by a certain date (expiry).

- Margin Money: Like a deposit you give your broker to hold your spot in the deal. It's usually a percentage of the total contract value (e.g., ₹85,000 for a Nifty 50 contract at ₹17,000).

- Lot Size: The number of shares or index points in a single contract (e.g., 50 for Nifty 50).

- Buying: You think a stock (like Nifty 50) will go up. You buy a futures contract at today's price (₹17,000). If it goes up by expiry, you buy at the lower price and sell at the higher market price, making a profit!

- Selling: You think a stock will go down. You sell a futures contract, locking in a selling price. If it goes down by expiry, you can sell at the higher locked-in price, making a profit! (But if it goes up, you'll lose money).

Getting Started:

- Pick a Broker: Find a trustworthy one registered with the Indian stock exchanges (NSE or BSE) that allows futures trading.

- Open a Futures Account: This is different from your regular stock account. Make sure you understand the margin requirements.

- Trading Tools: Use your broker's platform to analyze charts and make informed decisions.

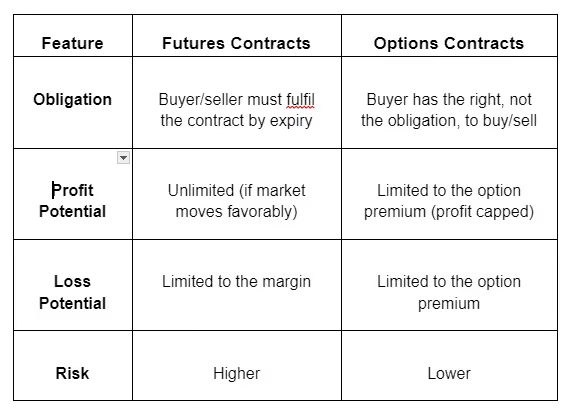

Futures vs. Options: A Quick Comparison

While both futures and options are derivative instruments, key differences exist:

Role of Margin:

A deposit required by the broker, typically a percentage of the contract value, to initiate a futures trade. It acts as a good faith deposit and reduces counterparty risk. (Example: A Nifty 50 contract with a lot size of 50 and a current price of ₹17,000 might require a 10% margin, which translates to ₹85,000).

Let's analyze a hypothetical futures trade to understand the concepts better:

Scenario: You believe the price of Reliance Industries (RIL) will rise due to an upcoming positive earnings report. On 1st March 2024, you buy a Reliance Futures contract (expiry date: 30th April 2024) at a price of ₹2,500 per share. The lot size for Reliance futures is 100 shares, and your broker requires a 15% margin.

Calculations:

- Contract Value (per lot) = Price per Share * Lot Size = ₹2,500 * 100 = ₹2,50,000

- Margin Required (per lot) = 15% of Contract Value = ₹2,50,000 * 15/100 = ₹37,500

Outcome 1: Successful Trade

- By April 30th, the Reliance share price rises to ₹2,800.

- You exercise your right to buy 100 shares at the contracted price of ₹2,500 and immediately sell them at the market price of ₹2,800.

- Profit per share = ₹2,800 - ₹2,500 = ₹300

- Total Profit (excluding brokerage) = Profit per share * Lot size = ₹300 * 100 = ₹30,000

Outcome 2: Unsuccessful Trade

- By April 30th, the Reliance share price falls to ₹2,200.

- You incur a loss, as you're obligated to buy at ₹2,500. The contract is settled in cash, and you realize a loss of ₹300 per share (₹2,500 - ₹2,200).

- Total Loss (excluding brokerage) = Loss per share * Lot size = ₹300 * 100 = ₹30,000

Choosing the Right Futures Contract

With thousands of futures contracts available in the market, it's essential to choose the right one for your trading strategy.

Consider factors such as liquidity, volatility, and expiration dates when selecting a contract. For example, if you're interested in trading agricultural commodities, you might consider contracts for wheat, rice, or soybeans.

Risk Management Strategies

- Risk management is crucial in futures trading to protect your capital and minimize losses.

- Set stop-loss orders to limit potential losses and avoid over-leveraging your positions.

- Diversify your portfolio across different asset classes to spread risk and protect against market downturns.

- Only invest a portion of your money you can afford to lose. Futures trading can be risky!

- Place Stop-loss Orders as they are like an automatic brakes system, these help limit your losses if the price goes against you.

- Learn to read charts to understand past price movements and make better predictions.

The Takeaway:

Futures trading can be a thrilling way to potentially multiply your gains in the Indian stock market. But always prioritize knowledge, manage risks, and never invest more than you can afford to lose.

Happy trading!

Bracket Order vs. Cover Order: A Beginner's Guide to Trading Strategies

Introduction:

Welcome to the world of stock market trading! If you're just starting out, you might feel overwhelmed by all the different terms and strategies. Two strategies you might hear about are Bracket Orders and Cover Orders. In this easy-to-understand guide, we'll explore what these strategies are, how they work, and when you might use them.

Understanding Bracket Orders:

Imagine you're at a carnival playing a game where you have to knock over targets. You set up your throw, and if you hit the target, you win a prize. But you also set up a safety net behind the targets just in case you miss.

That safety net is a bit like a Bracket Order in trading. Here's how it works:

- Initial Order: This is your main trade. It's like saying, "I want to buy this stock at this price.

- Profit Target Order: This is your goal. You decide how much profit you want to make, and if the stock reaches that price, your trade automatically sells to lock in your profit.

- Stop-Loss Order: This is your safety net. If the stock starts going the wrong way and hits a price you're not comfortable with, your trade automatically sells to limit your losses.

Imagine you want to buy shares of a company called XYZ, which is currently selling for ₹100 per share. You set up a Bracket Order like this:

- Initial Buy Order: ₹100 per share

- Profit Target Order: ₹110 per share

- Stop-Loss Order: ₹90 per share

If the stock goes up to ₹110, you sell and make a profit. If it drops to ₹90, you sell to prevent big losses. Otherwise, your initial order stays active until you cancel it.

Understanding Cover Orders:

Now, let's talk about Cover Orders. Think of it like going to a restaurant and ordering a meal with a backup plan. Here's how it works:

- Market Order: This is your main trade. You're saying, "I want to buy or sell this stock at the current market price.

- Stop-Loss Order: This is your backup plan. If things don't go as expected and the stock starts going the wrong way, your trade automatically sells to limit your losses.

Imagine you want to buy shares of XYZ, currently selling for ₹150 per share. You set up a Cover Order like this:

- Market Buy Order: ₹150 per share

- Stop-Loss Order: ₹140 per share

If the stock drops to ₹140 or below, your trade automatically sells to prevent further losses. Otherwise, your market order executes at the current price.

Comparison: Bracket Order vs. Cover Order

Let's compare these two strategies in simple terms:

Conclusion:

Both Bracket Orders and Cover Orders are like safety nets for your trades, helping you manage risks in different ways. Bracket Orders are more like setting specific goals with backup plans, while Cover Orders are more straightforward with a backup plan only.

As a beginner, it's essential to understand these strategies and when to use them. Whether you're aiming for specific goals with Bracket Orders or seeking simplicity with Cover Orders, always remember to manage your risks and make informed decisions.

Understanding Limit Orders: A Beginner's Guide to Navigating the Stock Market

Introduction:

Welcome to the exciting world of stock market trading! If you're new to this realm, you might find the jargon and concepts a bit overwhelming at first. But fear not, as we're here to guide you through one fundamental aspect of trading: limit orders.

In this beginner-friendly guide, we'll break down what limit orders are, how they work, and why they're essential tools for any investor or trader. So, let's dive in!

What is a Limit Order?

A limit order is a type of order to buy or sell a stock at a specific price or better. Unlike market orders, which execute at the current market price, limit orders give you more control over the price at which your trade is executed. This control can be particularly useful when you want to enter or exit a position at a specific price point.

Let's illustrate this with a simple example:

Suppose you want to buy shares of XYZ Company, which is currently trading at ₹100 per share. However, you believe that ₹95 is a fair price to enter the trade. In this case, you can place a limit buy order at ₹95. This means that your order will only execute if the stock's price falls to ₹95 or lower.

Conversely, if you already own shares of XYZ Company and want to sell them at ₹110 per share, you can place a limit sell order at that price. Your order will only execute if the stock's price rises to ₹110 or higher.

How Do Limit Orders Work?

Now that you understand what limit orders are let's delve into how they work. When you place a limit order, you specify the price at which you're willing to buy or sell a stock. Your order will remain active until it either executes or is canceled.

There are two types of limit orders:

- Limit Buy Order: This type of order is used when you want to buy a stock at a specific price or lower. Your order will only execute if the market price reaches your specified limit price or lower.

- Limit Sell Order: Conversely, a limit sell order is used when you want to sell a stock at a specific price or higher. Your order will only execute if the market price reaches your specified limit price or higher.

Let's consider a scenario to understand how limit orders work in practice:

Scenario:

You want to buy shares of ABC Company, which is currently trading at ₹150 per share. However, you believe that ₹140 is a more reasonable price. So, you decide to place a limit buy order at ₹140.

Meanwhile, another investor wants to sell their shares of ABC Company at ₹145 per share and places a limit sell order at that price.

Now, let's see what happens:

- If the market price of ABC Company's stock falls to ₹140 or below, your limit buy order will execute, and you'll purchase shares at your specified price.

- Conversely, if the market price rises to ₹145 or higher, the other investor's limit sell order will execute, and they'll sell their shares at their specified price.

- If the market price remains between ₹140 and ₹145, neither your limit buy order nor the other investor's limit sell order will execute, and both orders will remain active until canceled or until the market price reaches the specified limit prices.

Benefits of Using Limit Orders:

Now that you grasp the concept of limit orders, let's explore why they're beneficial for traders and investors:

- Price Control: Limit orders allow you to specify the exact price at which you want to buy or sell a stock, giving you more control over your trades.

- Avoiding Slippage: Slippage occurs when the market price deviates from the expected price between the time your order is placed and when it's executed. Limit orders help mitigate slippage by ensuring that your trades are executed at your specified price or better.

- Patience Pays Off: If you're willing to wait for the right price, limit orders can be a valuable tool. By setting a limit price, you can patiently wait for the market to reach your desired entry or exit point.

- Strategic Trading: Limit orders are particularly useful for implementing trading strategies that rely on specific price levels, such as buying at support levels or selling at resistance levels.

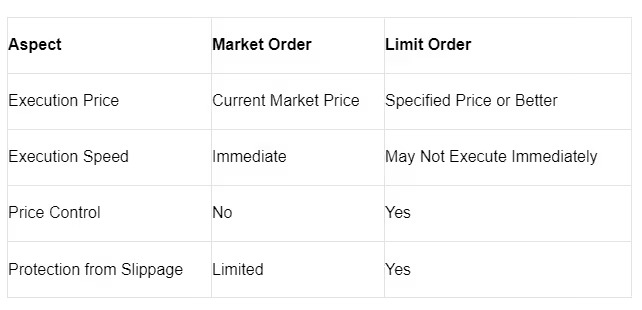

Limit Orders vs. Market Orders:

It's essential to distinguish between limit orders and market orders, as they serve different purposes:

- Market Order: A market order is an instruction to buy or sell a stock at the current market price. Market orders execute immediately but do not guarantee a specific price.

- Limit Order: In contrast, a limit order allows you to specify the price at which you want to buy or sell a stock. While limit orders may not execute immediately, they provide price control and can help you avoid unexpected execution prices.

Let's compare market orders and limit orders using a simple table:

Conclusion:

In conclusion, limit orders are valuable tools for traders and investors looking to exert more control over their trades in the stock market. By specifying the price at which you're willing to buy or sell a stock, you can mitigate risks, avoid slippage, and implement strategic trading strategies effectively.

As you continue your journey into the world of investing, understanding how limit orders work and when to use them will empower you to make more informed trading decisions. So, don't hesitate to incorporate limit orders into your trading arsenal and watch as they enhance your trading experience.

What is a Bracket Order? A Beginner's Guide to Trading Orders

New investors often worry about buying a stock at the wrong time or missing out on profits. Bracket orders can help with this!

In this blog post, we'll explain what bracket orders are and how they can help you manage your trades in the stock market.

What is a Bracket Order?

A bracket order is a powerful tool for new and experienced investors alike. It allows you to place three orders simultaneously:

- Buy or Sell Order (Entry Order): This is your primary order to buy or sell a specific stock at a particular price.

- Take Profit Order (Target Order): This order automatically sells your stock when it reaches a specific price, locking in your gains.

- Stop-Loss Order: This order automatically sells your stock if the price falls below a certain point, minimizing your potential losses.

Think of a bracket order like setting up boundaries for your trade. You define the upside potential (take profit) and the downside risk (stop-loss) you're comfortable with, taking some of the guesswork out of managing your positions.

Why Use Bracket Orders?

Here are some key benefits of using bracket orders:

- Discipline and Risk Management: Bracket orders help you maintain discipline by pre-defining your exit points. This prevents emotional decisions based on market volatility.

- Saves Time: You don't need to constantly monitor the market, as the orders are already placed and will execute automatically.

- Peace of Mind: Bracket orders provide peace of mind knowing you have a safety net in place to limit losses or capture profits.

How Does a Bracket Order Work?

Let's break down how a bracket order works with an example:

- Imagine you want to buy 100 shares of ABC Company stock.

- The current price of ABC is ₹100 per share.

- You believe the price could rise to ₹120, but you're also worried it might fall to ₹80.

Here's how you would set up a bracket order:

- Entry Order: Buy 100 shares of ABC at the market price (₹100).

- Take Profit Order (Target Order): Sell 100 shares of ABC at ₹120 (your profit target).

- Stop-Loss Order: Sell 100 shares of ABC at ₹80 (your stop-loss price).

Here are two possible scenarios:

Scenario 1: Price Goes Up

If the price of ABC increases and reaches ₹120, your take profit order will be triggered automatically, selling your shares and locking in a profit of ₹20 per share (₹120 - ₹100).

Scenario 2: Price Goes Down

If the price of ABC falls and reaches ₹80, your stop-loss order will be triggered, automatically selling your shares and limiting your loss to ₹20 per share (₹100 - ₹80).

Important Note:

There's no guarantee that your take profit or stop-loss orders will be filled at the exact prices you specify. Market conditions can affect the execution price.

Types of Bracket Orders

There are two main types of bracket orders:

- Trailing Stop-Loss Orders: These automatically adjust the stop-loss price as the stock price moves in a favorable direction. This helps lock in even greater profits if the price keeps rising.

- One-Cancels-the-Other (OCO) Orders: With OCO orders, if either the take profit or stop-loss order is triggered, the other order is automatically canceled. This prevents you from accidentally buying or selling more shares than intended.

Are Bracket Orders Right for You?

Bracket orders can be a valuable tool for beginners and experienced investors alike. They help you manage risk, save time, and potentially improve your trading results. However, they are not a magic bullet, and it's essential to consider the following:

- Market Volatility: Bracket orders may not be as effective in highly volatile markets, where prices can swing dramatically.

- Commissions: Some brokers charge fees for each order placed. Frequent use of bracket orders with multiple components can increase your overall trading costs.

- Trading Strategy: Bracket orders work best with a well-defined trading strategy that includes entry and exit points.

Conclusion

Bracket orders can be a powerful tool for managing your trades in the stock market. By understanding how they

By understanding how they work and their limitations, you can decide if they are a good fit for your trading strategy. Remember, the stock market is inherently risky, and no single tool guarantees success. However, bracket orders can help you approach the market with more discipline and potentially improve your overall trading experience.

Here are some additional tips for using bracket orders effectively:

- Do your research: Before placing a bracket order, thoroughly research the stock you're interested in. Understand the company's fundamentals, analyze past price movements, and consider current market conditions.

- Set realistic targets and stop-loss levels: Don't get greedy with your take profit or be overly cautious with your stop-loss. Base them on technical analysis and your risk tolerance.

- Start small: Especially when you're new to bracket orders, start with smaller positions to get comfortable with the mechanics and potential outcomes.

- Review and adjust: Regularly review your bracket orders and adjust them as needed based on market movements and your evolving strategy.

By following these tips and practicing with a demo account before risking real capital, you can leverage bracket orders to become a more confident and disciplined trader.

Bonus: Glossary of Terms

- Market Price: The current price at which a stock is being traded.

- Target Price: The price at which you want to sell your stock for a profit.

- Stop-Loss Price: The price at which you want to sell your stock to limit a loss.

- Trailing Stop-Loss: A stop-loss order that automatically adjusts upwards as the stock price increases.

- One-Cancels-the-Other (OCO) Order: An order where if one part of the order is filled (take profit or stop-loss), the other part is automatically canceled.

How to Choose the Right Savings Bank Account in India 2024

Introduction

Finding the perfect savings account in India's ever-evolving banking landscape can feel overwhelming. But worry not! This guide will equip you with the knowledge and tools to select the ideal account for your financial goals in 2024.

Understanding Savings Bank Accounts in India

First things first, let's talk about what a savings account actually is and why it's important. Think of it as your financial buddy that helps you keep your money safe while also giving you a little something extra in return. Savings accounts are like a safe haven for your cash, allowing you to earn interest on the money you deposit.

The Role of Savings Accounts in Your Financial Portfolio

Your savings account is the foundation of your financial well-being. It allows you to park your money safely while earning interest. This readily accessible pool of funds can be used for emergencies, short-term goals, or as a springboard for future investments.

Recent Changes in the Indian Banking Sector You Should Know About

The Indian banking sector is constantly evolving. In recent years, we've seen a surge in digital banking solutions, with many banks offering zero-balance accounts and simplified KYC procedures. Additionally, keep an eye out for potential changes in interest rates, which can significantly impact your account's returns.

Factors to Consider When Choosing a Savings Account

What factors should you consider when choosing a savings account? Here are a few key things to keep in mind:

- Interest Rates: Look for banks offering competitive interest rates in 2024. The higher the interest rate, the more your money will grow over time.

- Fees and Minimum Balance Requirements: Pay attention to any fees associated with the account and the minimum balance required to avoid them. You don't want your savings to be eaten up by unnecessary charges!

- Digital Banking Features: In this digital age, convenience is key. Check if the bank offers features like online banking, mobile apps, and ATM access for easy management of your account.

- Customer Service and Reputation: A bank's reputation for excellent customer service can make all the difference when you need assistance. Look for reviews and ratings to gauge the bank's reputation.

Types of Savings Accounts Available

Did you know that there are different types of savings accounts tailored to meet specific needs? Here are a few common ones you might come across:

- Regular Savings Accounts: These are your standard savings accounts suitable for everyday use.

- Salary Accounts: Offered by employers to deposit employees' salaries directly into their accounts.

- Women's Savings Accounts: Designed with features like higher interest rates and discounts on services specifically for women.

- Senior Citizen Savings Accounts: Offering benefits such as higher interest rates and special banking privileges for senior citizens.

How to Maximize Your Savings Account Benefits

Here are some tips to get the most out of your savings account:

- Automating Your Savings: Setting Up Recurring Deposits (RD) to automatically transfer a fixed amount from your account at regular intervals. This fosters a disciplined saving habit.

- Utilizing Sweep-in and Sweep-out Facilities: Some banks offer sweep-in/sweep-out facilities, where surplus funds in your savings account are automatically transferred into a fixed deposit (FD) for higher returns.

Opening Your First Savings Account in 2024

The process of opening a savings account has become more streamlined:

- Documentation and KYC Norms Simplified

- KYC (Know Your Customer) norms are essential for verification purposes. Thankfully, the process has been simplified, often requiring minimal documentation.

Opening Your First Savings Account

Ready to open your first savings account? Here's what you need to know:

- Documentation and KYC Norms: Be prepared with the necessary documents like proof of identity, address, and PAN card to fulfill KYC requirements.

- Steps to Open an Account Online: Many banks offer the option to open an account online. Follow the simple steps provided on their website to get started.

Safeguarding Your Savings Account

Last but not least, it's crucial to safeguard your savings account against fraud and other risks. Here's how:

- Understanding the Importance of Nomination: Nominate a trusted individual to receive the funds in case of unforeseen circumstances.

- Tips to Prevent Fraud: Be vigilant and follow best practices to secure your account from online fraudsters.

Conclusion

By carefully considering the factors outlined above, you can select a savings account that aligns perfectly with your financial goals. Remember, the "best" savings account is the one that caters to your specific needs and offers a balance of interest rates, convenience, and security.

Questions:

Q. Which Bank Offers the Highest Interest Rate on Savings Accounts in 2024?

Interest rates can fluctuate. It's best to compare rates offered by different banks at the time of your decision.

Q. Can I Open a Savings Account Entirely Online Without Visiting a Bank Branch?

Yes, many banks allow you to open a savings account completely online.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App