Inside the IPO Filing Process from DRHP to Listing Day

An IPO is often perceived as a single event. In reality, it is a tightly regulated capital markets transaction that tests a company’s governance, financial maturity and disclosure standards. Long before the stock lists, months of preparation go into drafting, verification, regulatory review and investor positioning.

Why the Filing Process Matters

The offer document is the backbone of the IPO. For SEBI, it is a legal disclosure document. For investors, it is the primary source of truth.For the company, it becomes a permanent public record. Gaps in statutory disclosures or inconsistencies in financial reporting may result in approval delays and affect investor confidence.

Phase I: Pre IPO Preparation

The IPO process begins well before drafting the prospectus. At this stage, the company prepares itself to operate as a listed entity. Key actions include finalising the issue structure, converting into a public limited company, updating constitutional documents, strengthening board and committee structures, appointing key managerial personnel and dematerialising shareholding.

Phase II: Due Diligence and DRHP Preparation

This is the most intensive stage of the IPO journey. The Merchant Banker conducts detailed financial, legal and business due diligence, followed by preparation of the Draft Red Herring Prospectus covering company profile, industry overview, risks, financials and utilisation of proceeds.

Phase III: SEBI and Stock Exchange Review

SEBI, along with the stock exchanges, reviews the DRHP to ensurefull and fair disclosures, eligibility, and governance compliance. All queries and observations are addressed before final In-Principal approval.

Phase IV: Issue Management and Investor Outreach

Post regulatory clearances, the Red Herring Prospectus is finalised and the issue pricing is decided. Merchant Bankers, working closely with syndication and underwriting teams, drive investor outreach and roadshows, while market makersplay a role in supporting orderly trading and liquidity (in case of SME-IPO), in line with applicable issue regulations.

Phase V: Post Issue Formalities and Listing

After the issue closes, the basis of allotment is finalised, funds are reconciled by the banker to the issue, and shares are credited to investors’ demat accounts. In cases of oversubscription, allotment is carried out as per category-wise allocation norms, with proportionate or lottery-based distribution and refunds/unblock of excess application amounts. The company then lists on the stock exchanges and enters the post-listing compliance framework. Syndication and underwriting teams continue to support investor engagement, while issuer-led marketing and investor interactions remain ongoing. Anchor investors participate up to one working day prior to the issue opening, helping establish early demand visibility and confidence in the offering.

Role of the Merchant Banker

The Merchant Banker anchors the IPO end-to-end, beginning with comprehensive due diligence and preparation of offer documentation. They act as the primary interface with SEBI and Stock Exchanges, provide valuation and structuring advice, and lead investor marketing efforts. In coordination with syndication and underwriting teams, the merchant banker supports book building, demand aggregation, and risk underwriting. Post listing, they also facilitate market-making arrangements and ensure regulatory and compliance requirements are met, enabling a smooth transition from a privately held company to the public markets.

Closing Thoughts

The IPO process shows how ready a company is to operate in public markets. With the right Merchant Banker guiding the company at every stage, the journey becomes well-planned and manageable, helping the business move smoothly into the listed space and build long-term, sustainable growth.

👉 To Connect with us today, please click here.

Latest Articles

Amber Enterprises Target Price Upgraded; Retains Reduce: What It Means for Retail Investors

Key Takeaways

- HDFC Securities raised Amber Enterprises' target price but retained a Reduce rating.

- The note cites potential earnings growth and margin improvements, offset by valuation risks.

- Retail investors should reassess entry points and strengthen risk management.

- Swastika's Sarthi AI stock assistant can help compare Amber with peers and refine decisions.

When a broker lifts the target price for Amber Enterprises yet keeps a Reduce rating, retail investors are faced with a paradox: optimism on price targets paired with a conservative stance on immediate action. The latest broker note indicates a higher target price for Amber Enterprises while maintaining a Reduce rating, signaling a nuanced view of upside potential versus risk. In the Indian stock market, such moves can influence price action, investor sentiment, and mid term strategy as markets digest both the optimism and caution.

Why HDFC Securities Ups Target Price on Amber Enterprises Yet Retains a Reduce Rating

The note points to factors that could support earnings expansion and margin improvement, including an improving revenue trajectory and a favorable capex cycle. Despite these positives, the rating remains Reduce due to valuation concerns and potential macro headwinds that could cap upside. This combination signals to investors that there is upside in the stock if execution and macro conditions cooperate, but the risk-reward remains skewed toward caution.

What the Amber Enterprises Target Price Upgrade Signals About Growth, Margins, and Orders

With an upgraded target price, the broker hints at confidence in an improving earnings mix, better cost management, and a stronger order book that could translate into higher margins. The view implies Amber Enterprises could benefit from product mix optimization, capex-led capacity additions, and favorable commodity pricing dynamics in the near to medium term. Investors should interpret this as a cautious optimism that earnings visibility might improve, even if the current price already reflects some optimism.

How The Amber Enterprises Update Could Affect Retail Investors' Trading Plans

Retail investors should rethink entry points and risk controls in light of a higher target price and a Reduce rating. The absence of a buy rating means it may be prudent to observe price action, liquidity, and relative valuation versus peers before initiating new positions. A disciplined approach–monitor price action, set stop losses, and align with a defined time horizon–can help manage risk while staying open to upside catalysts.

Key Risks and Valuation Considerations For Amber Enterprises After The Note

Valuation remains a key consideration even after an upgrade, especially if earnings do not accelerate as anticipated. Macroeconomic headwinds, supply chain dynamics, and execution risks on capex could temper upside. Raw material price volatility and currency movements can also affect margins. Investors should weigh these risks against potential catalysts and adopt a balanced view rather than chasing a single narrative.

FAQ

What action did HDFC Securities take on Amber Enterprises in its note?

HDFC Securities raised Amber Enterprises' target price but retained a Reduce rating.

Why did the note upgrade the target price while keeping a Reduce rating?

The note cites potential earnings growth and margin improvement as drivers for a higher target price, but keeps a Reduce rating due to valuation concerns and macro headwinds.

What should a retail investor do after such an update?

Reassess entry points, manage risk with stop losses, compare Amber with peers, and consider waiting for a clearer catalyst before building a new position.

What factors could drive Amber Enterprises' upside according to the note?

A stronger order book, better cost management, margin expansion, and a favorable capex cycle could drive earnings growth and support the higher target price.

Where can investors find more data to evaluate Amber Enterprises against peers?

Investors should refer to primary market data from NSE and BSE price data and review Amber Enterprises' company filings for fundamentals; Swastika also offers Sarthi AI stock research to compare with peers.

Conclusion

Conclusion paragraph one: The combination of a higher target price and a Reduce rating in a broker note signals upside potential tempered by risk. For the retail investor, this means staying vigilant about valuation, tracking execution, and using a structured decision framework to decide whether to hold, add on weakness, or wait for a clearer catalyst.

Gold Price Today on MCX India: Intraday Moves Confirm Gold at Rs 1,44,825 and Silver at Rs 2,28,235

Key Takeaways

- Gold on MCX slipped 0.89% to Rs 1,44,825 per 10 grams as of 9:45 am.

- Silver on MCX fell 2.59% to Rs 2,28,235 per kg at the same time.

- Gold trades below Rs 1.45 lakh on MCX, signaling near-term weakness.

- A stronger dollar and hawkish Fed signals weigh on bullion, with global gold around $4,140/oz.

Gold Price Today on MCX India: Intraday Levels and What They Signal for Retail Investors

Intraday price data from the Multi Commodity Exchange (MCX) shows gold futures under pressure on Tuesday, with the MCX gold July futures contract slipping 0.89% or Rs 1,300 to Rs 1,44,825 per 10 grams as of 9:45 am. This intraday move highlights how Indian price discovery for bullion is responding to a constellation of global and domestic factors, including a stronger greenback and evolving inflation expectations. Retail investors should note that these figures are intraday readings on MCX, and stock exchange data are typically delayed by up to 3 minutes.

The price point of Rs 1,44,825 per 10 grams places gold just under the 1.45 lakh threshold that traders often watch as a near-term mental barrier. Such levels matter for options premia, hedging costs, and the tactical decisions of those who balance risk with potential upside in bullion exposure. If you’re considering a strategic entry or exit, this intraday reference is a key data point for calibrating risk budgets in a volatile macro environment.

Silver Price Today on MCX India: Intraday Levels and How Silver Moves Compare

In the same session, MCX silver futures for July fell 2.59% or Rs 6,075 to Rs 2,28,235 per kilogram, as of 9:45 am. Silver’s larger percentage drop versus gold signals its greater sensitivity to liquidity conditions and dollar-centric dynamics that affect non-yielding assets more acutely. The simultaneous move in both precious metals paints a coherent picture of risk-off sentiment and the way Indian markets price inflation and currency risk into commodity futures.

From a retail-investor lens, this silver move reinforces the importance of diversification within a bullion framework. While both metals moved lower, the magnitude of silver’s drop can influence decisions around average cost strategies, hedges, and position sizing for those who hold both gold and silver futures or related bullion products on MCX.

Why Gold Remains Below Rs 1.45 Lakh on MCX: Key Triggers for the Near Term

The report emphasizes that gold is trading below Rs 1.45 lakh on MCX, with the intraday price at Rs 1,44,825 per 10 grams marking a nuanced moment for traders. This level acts as a psychological and technical focal point; breaching or holding near it can influence short-term momentum and options activity. The intraday moves–0.89% for gold and 1,300 rupees in absolute terms–reflect a broader interplay of inflation expectations, currency movements, and risk appetite. For retail traders, the path forward depends not merely on the absolute level but on the price action around this threshold and the rate at which macro signals shift in the coming sessions.

In practical terms, this is a moment to assess risk controls, confirm exposure size, and consider whether any short-term hedges or tactical trims align with your time horizon and capital allocation strategy. The intraday numbers provide a frame for decision-making rather than a definitive market call, underscoring the importance of disciplined trade management in volatile markets.

Macro Triggers Behind the Move: Inflation, Fed Signals, and the US Dollar

The intraday bullion action is embedded in a wider macro narrative. Global bullion prices declined as inflation concerns and currency dynamics weighed on demand for precious metals. Gold declined as much as 1.2% to around $4,140 per ounce, a level that reflects the currency-hedge dynamics that Indian buyers face when converting rupees to dollars for international price parity. The U.S. dollar strengthened, with data indicating the greenback rose more than 1% since the last Federal Reserve meeting, exerting downward pressure on dollar-denominated commodities including bullion priced on Indian exchanges.

In this context, policy signals from the U.S. Federal Reserve take on added significance. The discussion of a hawkish stance, including commentary associated with Fed Chair Kevin Warsh, amplifies concerns that higher rates can deter non-interest-bearing assets like bullion. The article also notes that inflation remains a global headwind. A top-line takeaway for investors is to monitor how shifts in U.S. monetary policy and inflation trends filter into Indian MCX price action, where currency translation and local demand patterns add further complexity to the price trajectory.

As a backdrop to these movements, Austan Goolsbee, President of the Federal Reserve Bank of Chicago, remarked: We've been dealing with an inflation problem that's well above the target and has been going the wrong way. This sentiment underscores why the market sees continued vigilance on rates and inflation, and why precious metals often struggle when the dollar strengthens and rate expectations become more aggressive.

Historical Context: Bullion Trend Since February War Developments

Looking at a longer horizon, the narrative around bullion has been shaped by geopolitical risk and the evolving inflation-dollar dynamic. Since end-February, as the war context intensified, gold has dipped a fifth, and silver has fallen more than 30%. This historical backdrop contextualizes the current intraday moves: while the longer-term trend has been challenging for bullion as a risk hedge, it remains a tool for diversification and a potential hedge against currency depreciation in slower-growth environments.

Practical Takeaways for Indian Retail Investors

- Track intraday price levels: Gold at Rs 1,44,825 per 10 grams and Silver at Rs 2,28,235 per kg on MCX as of 9:45 am indicate volatility around the 1.45 lakh level and a need for precise exit/entry discipline.

- Assess macro drivers: Dollar strength, inflation expectations, and Fed policy signals continue shaping bullion; adopt a risk-managed approach with clear stop-loss rules and defined position sizes.

- Relate local to global cues: The intraday rupee-priced moves reflect global dynamics–watch the $4,140/oz global benchmark and currency translations to guide Indian strategy.

- Use robust risk controls: Data on stock exchanges is delayed by up to 3 minutes, reinforcing the value of pre-defined risk parameters and disciplined execution.

FAQ

What were the intraday prices for MCX Gold and Silver on June 23, 2026?

Gold MCX July futures were at Rs 1,44,825 per 10 grams after a 0.89% drop (Rs 1,300) as of 9:45 am; Silver MCX July futures stood at Rs 2,28,235 per kg after a 2.59% drop ( Rs 6,075 ).

Why did gold and silver prices move lower on June 23, 2026?

A stronger US dollar, inflation concerns, and hawkish signals from US Federal Reserve policymakers contributed to the decline, with bullion also weighed by potential US-Iran peace developments.

What is the global price context for gold on that day?

Global bullion fell as much as 1.2% to around $4,140 per ounce, reflecting the same inflation and dollar dynamics affecting Indian MCX prices.

How have bullion prices moved since late February amid the ongoing war?

Since the war began by the end of February, gold has dipped about 20% (a fifth) and silver has fallen more than 30%.

What practical steps can a retail investor take based on these moves?

Consider risk-managed exposure, monitor intraday levels, and use research tools like Sarthi to evaluate positions; diversify across asset classes.

Where can Indian retail investors access MCX trading and AI-driven research tools?

Swastika Investmart offers MCX access, research reports, and Sarthi — an AI stock assistant for retail investors seeking institutional-level insights.

Conclusion

The intraday moves on MCX reflect a moment of cautious positioning for Indian retail investors as inflation concerns persist and the dollar strengthens. The combination of a sub-1.45 lakh price barrier for gold, a steeper drop in silver, and global macro signals creates a nuanced environment where disciplined risk management and data-driven decision-making are essential. A practical next step is to calibrate exposure with a clear plan, set stop losses, and use AI-powered research tools to refine your list of potential trades.

Open your trading and demat account here

Piramal Pharma stock surge after global regulatory approvals: a 10%+ rally and what it means for retail investors

Key Takeaways

- Piramal Pharma stock surged over 10% after multiple global regulatory approvals.

- The move signals potential catalysts and pipeline momentum, but exact products or geographies are not disclosed.

- Retail investors should watch upcoming regulatory milestones and earnings for confirmation.

- Sarthi AI stock assistant from Swastika Investmart can provide deeper, institution-grade insights.

On a day when regulatory headlines swing markets, Piramal Pharma’s stock jumped over 10% after multiple global regulatory approvals were announced. For retail investors across India, the move raises a simple question: is this a sustainable catalyst or a one-day spike driven by headlines?

Market data from NSE shows the stock moved over 10% intraday with above-average volume, underscoring genuine participation. The approvals are described as global in scope, hinting at expanded market access and a broader product portfolio that could improve revenue visibility in the near to medium term.

What caused Piramal Pharma stock surge after global regulatory approvals?

The triggering event is the announcement of multiple global regulatory approvals. While the report does not list the exact products or geographies, such regulatory clears are widely viewed as catalysts because they can enable faster commercialization, diversify the revenue base, and reduce execution risk associated with regulatory bottlenecks. A price move of over 10% in a single session typically reflects traders pricing in higher probability of monetization of these regulatory wins.

Which regulatory approvals were granted and what are their implications for Piramal Pharma's pipeline?

The approvals are described as global in scope, with implications for Piramal Pharma’s pipeline and the overall growth story. Such approvals typically unlock opportunities to commercialize products in additional markets, accelerate revenue streams, and potentially extend product lifecycles. The lack of a product-by-product breakdown in the report means investors should await additional disclosures from the company or regulators; still, the general implication is greater optionality for growth, possibly translating into higher long-run revenue and margin potential if launches succeed.

What does a 10%+ intraday rally mean for the near-term outlook of Piramal Pharma?

A rally of this magnitude can shift the near-term sentiment, but it is essential to separate price action from fundamentals. The sustainability of the move depends on actual sales momentum, pipeline progress, partnerships, and earnings signals in upcoming quarters. Investors should consider applying a risk-based framework to position appropriately, rather than chasing the rally. For deeper analysis, Swastika Investmart’s Sarthi AI stock assistant can help quantify how regulatory catalysts might unfold into price action across different scenarios.

What to watch next for Piramal Pharma after the regulatory catalyst?

TLDR

- Piramal Pharma stock surged over 10% after multiple global regulatory approvals.

- The jump reflects a positive catalyst with potential for pipeline expansion, though exact products and geographies are not listed.

- Retail investors should monitor upcoming milestones and earnings for confirmation of the new trajectory.

- Swastika Investmart's Sarthi AI can provide deeper, institutional-grade insights to refine decisions.

FAQ

What triggered Piramal Pharma's stock surge over 10%?

Market data indicate the stock moved higher after reports of multiple global regulatory approvals; such approvals are regarded as catalysts that can broaden market access and improve growth visibility.

Were the products or markets involved named in the report?

No; the report mentions multiple global regulatory approvals without providing a product-by-product list or geography-by-geography breakdown.

What does this mean for Piramal Pharma's near-term prospects?

The approvals increase potential for revenue and expansion, but near-term results depend on monetization through launches, sales, and margins as the company executes.

How should retail investors respond to regulatory-catalyst moves?

Maintain a risk-aware approach, monitor pipeline milestones and earnings, and consider using Swastika Investmart tools like Sarthi AI for deeper insights.

What resources does Swastika Investmart offer to analyze Piramal Pharma's regulatory catalysts?

Swastika Investmart provides research reports, a wide range of investment products, and Sarthi — an AI stock assistant delivering institutional-grade research.

Conclusion

For retail investors, the 10%+ rally signals a fresh round of optimism around Piramal Pharma’s global regulatory momentum. It highlights how regulatory catalysts can rewrite the near-term narrative for a pharmaceutical company and, if monetized, could translate into faster growth and improved margins. The key question is how quickly the company can convert these approvals into actual market launches and revenue, and whether the market’s optimism will hold as more details emerge.

Stocks to Watch Today: JSW Infra, BEL, Vodafone Idea & Info Edge for Indian Retail Investors

Key Takeaways

- JSW Infra, BEL, Vodafone Idea, and Info Edge are on todays watchlist.

- Price action and sector catalysts are highlighted for Indian retail investors.

- Price data references NSE, BSE, and company filings as primary sources.

- Use Sarthi AI for deeper, institution-grade stock insights.

Opening

What if your next investment idea could hinge on four names that sit at the intersection of India's growing infrastructure, defense modernization, telecom upgrades, and online platforms? That situation is unfolding today as JSW Infra, BEL, Vodafone Idea, and Info Edge emerge on the radar of Indian retail investors. This article distills what's moving these stocks, why the moves matter, and how you should think about risk and opportunity in a market that remains sensitive to policy signals and macro data. All price data and market signals referenced here come from primary sources such as the NSE, BSE, and the respective company filings.

JSW Infra stock price action today and what it signals for Indian retail investors

JSW Infra is attracting attention as part of the broader infra capex cycle in India. The stock's price action in today's session reflects renewed interest in infrastructure projects spanning roads, ports, and logistics. Market participants are watching for a potential upswing in order inflows and execution momentum, which would be consistent with a recovering capex environment. The latest price discipline and volume patterns, when viewed against the company's filings, suggest that any near-term move could be tied to project announcements or a tangible improvement in project execution. Retail investors should assess whether this action represents a short-term swing or the start of a multi-quarter re-rating tied to infra growth and policy support.

BEL stock price movement today and its implications for defense and manufacturing pipelines

BEL's stock activity today mirrors investor focus on India's defense modernization and domestic manufacturing push. The company's order book and earnings trajectory are sensitive to defense offsets and domestic production programs, while the broader defense budget signals and policy steps can act as catalysts. In today's data, the price action is consistent with expectations of a steady defense-led earnings engine, though investors should watch for any shifts in order intake or margins that could alter the trajectory. As always, cross-check the latest figures in the company filings and NSE/BSE price data for precise context.

Vodafone Idea stock today: impact of 5G rollout on subscribers and ARPU potential

Vodafone Idea remains vulnerable to the telecom regulatory backdrop and the pace of 5G rollout, but today's movement could reflect evolving investor bets on subscriber growth and data usage. The potential upshot is higher data ARPU if 5G adoption accelerates and data bundles become more competitive. Market watchers compare the stock's price action with sector peers and regulatory cues, using primary market data and the company's filings to gauge resilience in earnings and cash flow. For a retail investor, the key question is whether today's signal translates into a sustainable uptrend or a brief swing on added volatility.

Info Edge India: growth drivers in online recruitment and education portals

Info Edge sits at the heart of India's growing online recruitment and education ecosystems, with several portfolio companies contributing to its top-line exposure. Investor focus centers on growth in job portals, online education, and related tech-enabled platforms, all of which can drive monetizeable user engagement and long-term value. The stock's todays action should be interpreted in the context of platform growth, competition, and capital allocation. Validate any claims in the latest NSE/BSE price data and the company's filings for a grounded view. For deeper insights, Swastika's Sarthi AI stock assistant can help you test theses against institutional benchmarks.

What should Indian retail investors do with these stocks today?

FAQ

Which stocks were highlighted as stocks to watch today?

JSW Infra, BEL, Vodafone Idea, and Info Edge were highlighted as stocks to watch today.

What data sources underpin the price action and catalysts discussed?

Price data and catalysts are anchored in primary sources such as NSE, BSE, and the respective company filings.

What is the recommended approach for Indian retail investors?

Retail investors should assess risk budgets, define time horizons, verify catalysts with fundamentals, avoid headlines, and consider using tools like Swastika's Sarthi AI for deeper insights.

Does Swastika offer an AI stock assistant and how can it help?

Yes, Swastika offers Sarthi, an AI stock assistant that provides institutional-level research to retail investors for deeper analysis of stocks like JSW Infra, BEL, Vodafone Idea, and Info Edge.

Where can I verify current price data for these stocks?

Current price data can be verified on NSE and BSE, with company filings serving as additional primary sources.

What sector catalysts drive these stocks?

JSW Infra is linked to infrastructure capex growth; BEL to defense modernization and domestic manufacturing; Vodafone Idea to telecom 5G rollout; Info Edge to online recruitment and digital platforms.

Conclusion

Retail investors should view today's watchlist as a lens on India's four accelerating narratives: infrastructure investment, defense modernization, telecom data growth, and online ecosystems. The moves in JSW Infra, BEL, Vodafone Idea, and Info Edge can offer opportunities if you align them with sound risk management and a clear time horizon. Start by setting a price alert and a small, predefined risk budget for each name; then use Sarthi AI to test your theses against institutional-grade benchmarks before you commit more capital.

Two quick takeaways: first, focus on checklists rather than chase; second, treat these names as long- to medium-term exposures to secular growth themes in India. Build a watchlist, verify with NSE/BSE data and company filings, and apply a disciplined risk framework to capture potential upside while limiting drawdown.

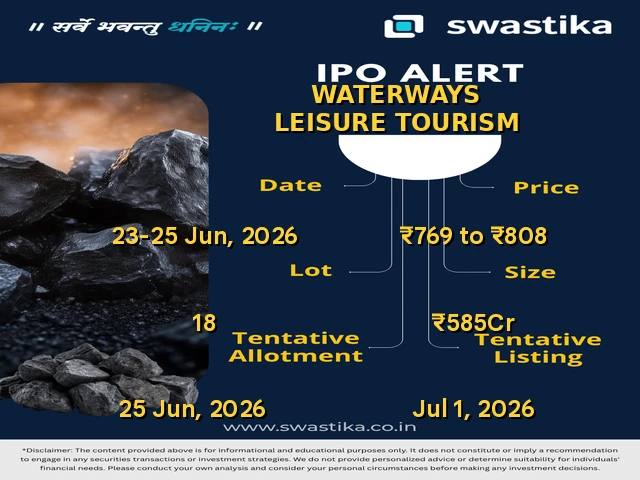

Waterways Leisure Tourism Limited IPO: Apply, Wait, or Avoid Before Listing?

Key Takeaways

- Waterways Leisure Tourism Limited IPO: price band ₹769-₹808, issue size 72,40,099 shares (up to ₹585 Cr), lot size 18.

- GMP signal: Not available yet; no clear listing gain guidance from market demand data.

- Risks: No revenue/profit numbers disclosed in the material; OFS details not announced; high price band.

- Action: Decide based on risk tolerance; consider applying only if you can hold with a post-listing plan; otherwise watchlist.

Waterways Leisure Tourism Limited IPO details: price band, lot size, dates

Waterways Leisure Tourism Limited IPO: business background and promoters

The offer is described as a main-board IPO by Waterways Leisure Tourism Limited, with a fresh issue of 72,40,099 equity shares aggregating up to ₹585 crores. The material does not provide details on promoters or the core business lines beyond stating the issue characteristics. As with many book-built offers, the final valuation will hinge on what the company discloses in the red herring prospectus and how demand shapes up during the bookbuild process. Promoter names and business specifics are not disclosed in the source material, so readers should watch for the IPO document for clarity.

Waterways Leisure Tourism Limited IPO valuation: is the ₹769-₹808 band justified?

Given the supplied data, there are no revenue, net profit, or margin figures to benchmark the ₹769-₹808 price band against peers or historical earnings. The lack of GMP data (GMP: Not available yet) and the absence of disclosed financials means investors cannot assess earnings yield, ROE, or parity with sector peers from the available material. In this context, the price band reads as a premium, and valuation justification will depend on future disclosures in the offer document and how the market responds during the bookbuild.

Waterways Leisure Tourism Limited IPO GMP: what it means for listing gains

The GMP (grey market premium) is not available yet for this issue, which leaves investors without a live signal of possible listing gains. A missing GMP often translates to higher uncertainty about the short-term listing move, especially when no financials are disclosed to anchor expectations. Retail investors should treat the lack of GMP as a caution flag and rely on price action and post-listing data once the shares begin trading on exchanges.

Waterways Leisure Tourism Limited IPO risks: what could go wrong?

Key risks based on the material include a lack of disclosed revenue/profit figures and no GMP data to guide price expectations. The issue is a large fresh capital raise (₹585 crore) at a high band, with OFS details not announced. The absence of concrete financial visibility increases dependence on market demand and post-listing performance, which adds a layer of risk for retail investors with limited capital. In addition, the retail quota is not fully disclosed in the source, so actual allotment odds remain uncertain until the offer document is released.

Waterways Leisure Tourism Limited IPO allotment & listing timeline: what to watch

The IPO opens on 23 June and closes on 25 June 2026, with listing slated for 1 July 2026 on BSE/NSE. Allotment timing will be determined post-bookbuilding, with the registrar and lead managers finalised in the prospectus. Investors should watch for revised guidance on OFS, final registrar details, and the exact allotment percentages across QIB/NII/retail tranches once the offer document is filed and updated. Since the offer is a fresh issue, the full allotment depends on demand vs. supply and the final bookbuild outcome.

Retail investors can apply through platforms like Swastika before the issue closes, making it easier to bid and monitor your bid status as the window nears closure.

FAQ

Is Waterways Leisure Tourism Limited IPO worth applying for at ₹769-₹808?

With no disclosed revenue or profit figures and GMP not yet available, there is no clear value signal. The high price band adds risk, so only risk-tolerant investors who have a post-listing plan should consider applying.

What are the allotment odds and lot size for Waterways Leisure Tourism Limited IPO?

The lot size is 18 shares. Allotment odds depend on demand during the bookbuild; exact odds cannot be predicted from the available data.

When will allotment be announced and listing occur for Waterways Leisure Tourism Limited IPO?

Open date is 23 June 2026, close date is 25 June 2026, and listing is expected on 1 July 2026 on BSE/NSE, subject to bookbuild outcomes.

What does GMP mean for Waterways Leisure Tourism Limited IPO?

GMP is not available yet, so there is no reliable signal of immediate listing gains. Rely on official post-listing performance and fundamentals once trading begins.

What is the key risk and what should I do before applying?

Key risk is the lack of disclosed financials and GMP data. If you are risk-averse, wait for more disclosures; if you have high risk tolerance and a post-listing plan, you may consider applying with controlled capital.

How do I apply via ASBA/UPI for this IPO?

The offer document will publish the official steps. Generally, bids are submitted through your broker’s IPO module with ASBA or UPI-based payment; ensure your details are correct and linked to your bank or payment method.

Conclusion

Waterways Leisure Tourism Limited IPO presents a high-ticket, information-light opportunity where fundamental clarity is lacking due to no disclosed financials and no GMP signal yet. For most retail investors, the prudent stance is to wait for the official offer document with revenue figures and the GMP signal, and to watch how demand shapes up in the bookbuild before committing capital. The absence of concrete numbers and a GMP signal means the risk/reward is unclear today, so consider this a watchlist candidate until more data emerges. Waterways Leisure Tourism Limited IPO is a high-risk proposition best approached with caution, a clear post-listing plan, and capital you can afford to deploy with high risk tolerance. Watchlist – lack of GMP and financial visibility makes it uncertain to commit now.

Advit Jewels Limited IPO: Should You Apply, Avoid, or Wait for the Listing Dip?

Key Takeaways

- Advit Jewels Limited IPO opens 23-25 Jun 2026; price band ₹130-₹138; 1,19,68,000 shares; issue size up to ₹165 crore; lot size 100 shares.

- GMP and live subscription data are not available yet.

- Key risks: no financials disclosed; registrar and lead manager to be announced; OFS to be announced.

- Watchlist for now – if you must, allocate a small amount after more data becomes available.

Advit Jewels IPO background: company profile

Advit Jewels Limited is launching a main board IPO that comprises 1,19,68,000 equity shares of face value ₹10 each, aggregating up to ₹165 crore. The issue price band is ₹130-₹138 per share, and the minimum bid quantity is 100 shares. The IPO opens on 23 Jun 2026 and closes on 25 Jun 2026, with listing scheduled on 1 Jul 2026 on BSE and NSE. Bigshare Services Pvt. Ltd. is the registrar for the issue; the lead manager and OFS details are yet to be announced, and GMP data remains unavailable. The information comes from Chittorgarh.

Advit Jewels IPO details: key numbers at a glance

Business note: Advit Jewels IPO is a main-board IPO of 1,19,68,000 equity shares of the face value ₹10 aggregating up to ₹165 crores. The issue is priced at ₹130 to ₹138. The minimum order quantity is 100. The IPO opens on 23 Jun 2026 and closes on 25 Jun 2026. Bigshare Services Pvt. Ltd. is the registrar; the shares are proposed to be listed on BSE and NSE.

Subscription & GMP signals: what to watch

As of now, there is no GMP data or live subscription information available in the source. Here are the quotas allocated for different investor classes:

- QIB Quota: 23,92,600

- NII Quota: 5,98,400

- Retail Quota: 14

Financial snapshot and valuation context: what numbers are available?

The source does not provide revenue, PAT, or margin figures. Without a financial snapshot or peer comparables, it is not possible to judge whether ₹130-₹138 is fair or rich. The lack of data also makes it hard to assess how the funds will be used beyond generic fresh capital. Until those disclosures open, valuation merits are uncertain.

Risks that could affect your decision

- GMP data is unavailable, so listing gain potential is unknown.

- Registrar and lead manager details are not disclosed yet.

- OFS information is not provided.

- No financials or profitability metrics in the provided source.

- Fresh issue size is significant (₹165 crore) but is not justified by financials in the data.

Allotment & listing timeline: what to expect next

Open 23 Jun 2026; Close 25 Jun 2026; Listing 1 Jul 2026 on BSE and NSE. Details such as allotment date, registrar, and lead manager will be announced later. The registrar is Bigshare Services Pvt. Ltd.; The final allotment and listing outcome will be known after the close date and the exchange's announcements.

Advit Jewels IPO valuation: is the ₹130-₹138 price band justified?

With no revenue or profit data in the source, there is insufficient basis to value the issue accurately. The ₹130-₹138 band is a standard book-building range for a fresh capital issue, but without financial visibility or clear demand signals, the justification remains uncertain. Investors should be cautious about paying a premium without fundamentals or track record data.

FAQ

Is Advit Jewels IPO worth applying at ₹130-₹138?

Given no GMP data or financial snapshot, there is limited basis to justify applying at this stage. The decision hinges on future disclosures and post-listing performance.

What is the GMP signal for Advit Jewels IPO?

GMP data is not available yet.

What is the allotment odds and lot size for retail investors?

Lot size is 100 shares; Allotment odds cannot be determined from the data; Quotas exist for QIB, NII, and Retail (QIB 23,92,600; NII 5,98,400; Retail 14).

How can I apply via UPI/ASBA?

Applications are typically made via ASBA through your bank or through UPI-based channels on supported platforms; specific registrar/lead manager details for this issue are not yet announced.

What are the key risks I should know about Advit Jewels IPO?

No financials, no GMP, OFS to be announced, and registrar/lead manager details are not disclosed yet; these create listing risk and uncertainty about post-listing performance.

Conclusion

In plain terms, Advit Jewels IPO is a small-ticket offering with a high information gap: GMP data is not available and no financials are disclosed. That combination means listing-day volatility and uncertain returns for retail investors who prefer clear data.

Watchlist for now – GMP data is unavailable and the financial picture is unclear, so wait for more clarity before you apply.

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App