Airtel ₹11.9 Lakh Cr — Should You Rebalance Your Portfolio?

Key Takeaways

- Airtel briefly surpassed HDFC Bank in market cap, peaking at ₹11.9 lakh crore before closing second to HDFC.

- The move points to a rotation away from IT and banks toward telecom, potentially impacting sector weights in portfolios.

- Top sector to watch: Telecom — could influence stock selection within consumer and financial services plays.

- Action: Review telecom vs banking/IT exposure in your portfolio and consider a measured rebalancing if you’re overexposed to IT/banks.

What Happened

On Monday, Bharti Airtel briefly edged past HDFC Bank to become India’s second-most valuable company by market cap, with Airtel touching about ₹11.9 lakh crore. By the close of play, HDFC Bank had regained the second spot, underscoring how fleeting leadership can be in a market driven by rotation rather than fundamentals alone. For a retail investor, this intraday swing highlights the current mood where traditional heavyweights like IT and banks are facing headwinds while telecom names show relative resilience.

Why This Matters

Equity markets in India have been shifting away from the old leaders toward sectors that benefited from post-pandemic demand and a more cautious macro outlook. The brief Airtel win suggests investors are rethinking where value sits today, not just in earnings growth but in survivability during choppy times. For you, the takeaway is not to chase one stock but to watch where the money might be reallocated across sectors. The reaction also hints at potential improvements in telecom fundamentals and a re-pricing of risk in financials and IT stocks, which could influence how you structure exposure in the coming weeks.

What This Means For Your Portfolio

Most important for you is understanding sector leadership and how it affects your holdings. A sharp move in Airtel signals telecoms might gain modest defensive traction relative to IT and banking names, but this is not a green light to abandon diversification. If you are overweight IT or banks, consider whether your downside risk is adequately hedged by other exposures. For those with little telecom exposure, this could be a reminder to assess whether your portfolio would benefit from a balanced tilt toward communications services, especially if you already hold consumer-oriented names that could benefit from rising data demand and digital consumption.

Sectors To Watch — Priority Order

1st Priority: Telecom — Relative strength amid rotation suggests you should monitor telecom earnings trajectories and data demand trends.

2nd Priority: Financials (Banks) — After a period of underperformance, banks may see relief rallies but require careful stock-level analysis.

Avoid Now: IT — Ongoing pressure on earnings visibility could keep IT under pressure until clearer demand signals emerge.

Action Points For Investors

- SIP investors: Maintain steady ongoing investments but tilt a small portion toward telecom names if your risk tolerance allows and you already have broad diversification.

- Lumpsum investors: Avoid sudden heavy redeployments into one sector; use a staged rebalancing approach to reduce concentration risk in IT or banks.

- Traders: Watch intraday dispersion among large cap banks, IT bellwethers, and select telecom names for potential short-term setups; set strict stop-loss levels.

Swastika Investmart believes that market leadership can shift quickly in a rotation-driven environment. While a one-day flip in m-cap rankings is not a macro signal, it does indicate where investor interest is concentrated at the moment. The practical takeaway for you is to prioritize risk-managed exposure and keep a close eye on earnings delivery and management commentary across telecom, IT, and financials. In this context, building a diversified framework that can weather sector-specific cycles will help you stay prepared for the next shift in market leadership.

Key Risks To Watch

2-3 risks to monitor: (1) If telecom gains are based on price momentum rather than fundamentals, the rally could stall; (2) Banks and IT could re-enter leadership if earnings surprises materialize or if macro signals improve; (3) Interest rate expectations and macro policy changes could tilt sector performance again, affecting valuation spreads across cyclic and defensive names.

FAQ Details

What happened to Airtel in market cap terms?

Airtel briefly surpassed HDFC Bank to become the second-most valuable company by market cap, peaking around ₹11.9 lakh crore before HDFC Bank reclaimed the position by close.

Should I buy Airtel after this move?

No single-day move should dictate a fresh purchase. Consider your overall diversification, risk tolerance, and whether you already have telecom exposure; use a staged approach if you decide to add.

Which sectors should I watch now?

Telecom looks like the immediate focus, while IT and Banking are under more pressure; monitor earnings and policy signals to gauge if rotation sustains.

What is the one action I should take today?

Review your current sector allocations, ensure you aren’t overly concentrated in IT or banks, and consider incremental adjustments toward telecom exposure only if it fits your plan.

Conclusion

Airtel’s brief leadership in market cap signals rotation but is not a standalone buy signal. Review your exposure, prefer diversification, and watch telecom dynamics as a potential channel of relative strength in the near term.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

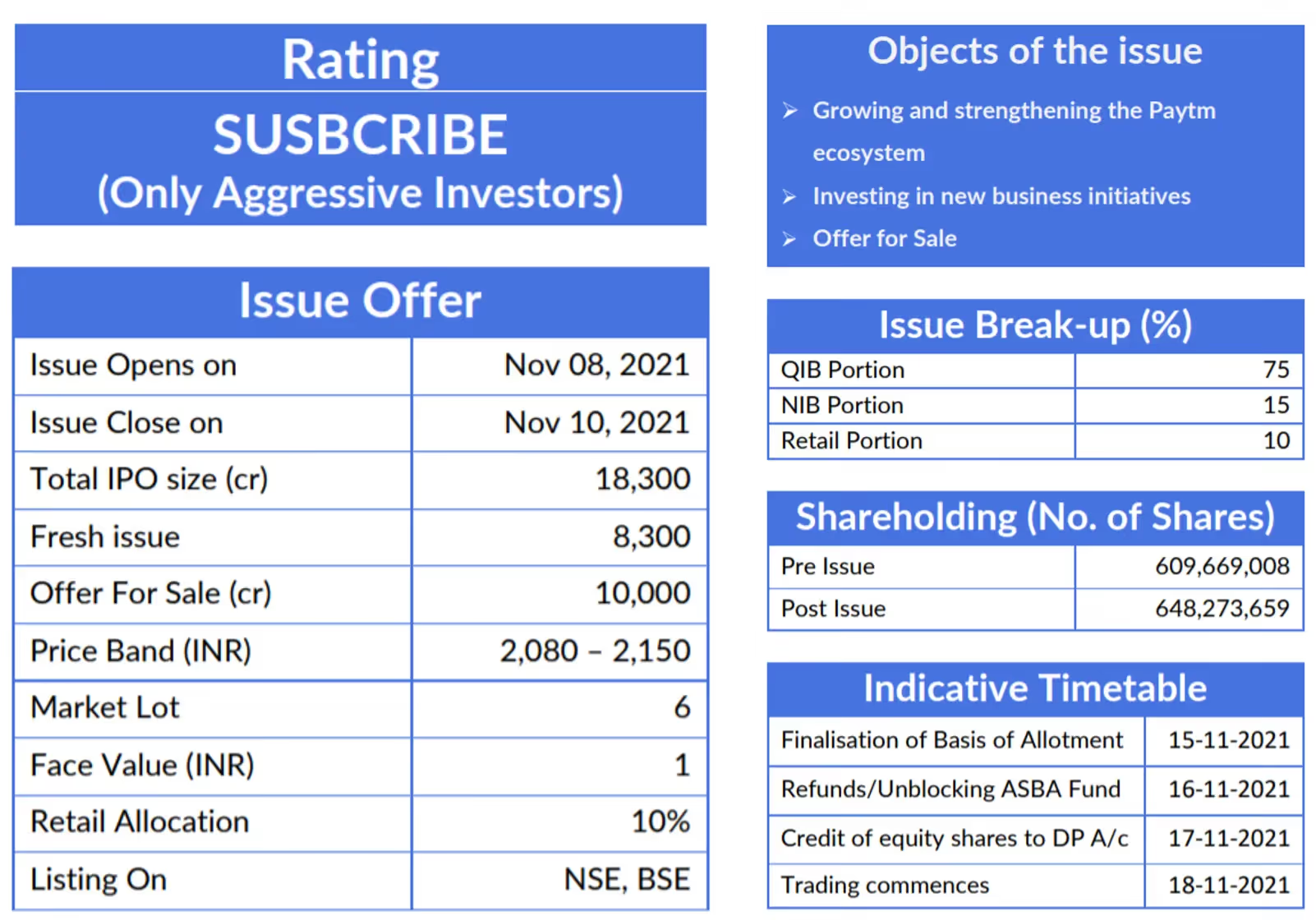

Paytm (One97 Communications Ltd) IPO: Outlook & Valuation

Incorporated in 2000, One97 Communications Limited (Paytm) is India’s leading digital ecosystem for consumers and merchants. Paytm offers ‘Payment Services’, ‘Commerce and Cloud Services’, and ‘Financial Services’ to 33.3 crore consumers and over 2.18 crore merchants registered with them, as of June 30, 2021.

Their 2-sided (consumer and merchant) ecosystem enables commerce, and provides access to financial services, by leveraging technology to improve the lives of their consumers and help their merchants grow their businesses.

In 2009, the company launched the first digital mobile payment platform, "Paytm App" to offer cashless payment services to customers and now, it became India's largest payment platform and the most valuable payments brand with a total brand value of US$6.3 billion as per Kantar Brands India 2020 Report.

The app enables customers to do cashless transactions at stores, top-up mobile phones, online money transfers, pay bills, access digital banking services, purchase tickets, play games online, buy insurance, make investments, and more. However, merchants can use the platform for advertising, online payment solutions, offering products to customers, and loyalty solutions. They have created a payments-led super-app, through which they offer their consumers innovative and intuitive digital products and services. They offer their consumers a wide selection of payment options on the Paytm app, which includes:

- Paytm Payment Instruments, which allow them to use digital wallets, sub-wallets, bank accounts, buy-now-pay-later, and wealth management accounts.

- Major third-party instruments, such as Debit and Credit Cards and Net Banking.

Offer services such as Paytm Wallet, Paytm QR, Paytm Soundbox, Gold investments, and Fixed Deposit, Paytm Postpaid, Merchant Cash Advance and FASTag.

Outlook & Valuation

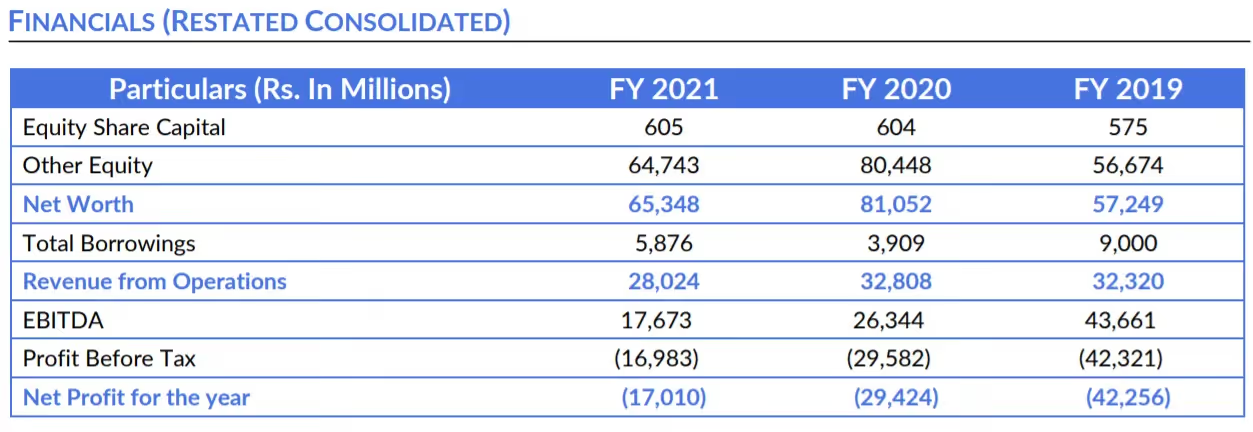

The revenues of the company have been on the declining side, in FY19 revenue was at ₹3,579 cr while in FY21 it was at ₹3,186 cr. Also, it is a loss-making company with a loss of ₹(4,230.9) cr in FY19 which however reduced to ₹(1,701) cr in FY21.

We are in an era of new-age businesses where we have seen many unicorns getting listed recently. It is really arduous to provide a valuation for such types of companies. We expect only leaders will survive over a period of time and only a few such companies will be wealth creators while many can be wealth destroyers. As India is on the verge of digitalization, we may expect the company to get benefited from the same also new acquisition and strengthening of the PAYTM ecosystem from the IPO will be beneficial for the company. Thus we assign a "SUBSCRIBE" rating only for aggressive investors.

KEY MANAGERIAL PERSONNEL

- Vijay Shekhar Sharma is the Founder, Managing Director, and Chief Executive Officer of the company, and the Chairman of the Board. He oversees the Company's key strategic efforts including engineering, design, and marketing.

- Madhur Deora is the President and Group Chief Financial Officer of the company. He has been associated with the company since October 3, 2016.

- Manmeet Singh Dhody is the Chief Technology Officer, Payments. He has been associated with the company since April 1, 2020.

- Vikas Garg is the Chief Financial Officer of the company. He has been associated with the company since May 21, 2014, and was previously associated with the company from August 25, 2008, to September 28, 2012.

- Sudhanshu Gupta is the Chief Operating Officer of Paytm First Games Pvt Ltd, their Subsidiary. He has been associated with Paytm First Games Pvt Ltd since June 1, 2018.

- Bhavesh Gupta is the Chief Executive Officer of the Lending Business of the company. He has been associated with the company since August 4, 2020.

- Renu Satti is the Chief Operating Officer of Offline Payments of the company. She has been associated with the company since October 11, 2006.

- Praveen Kumar Sharma is the Managing Director and Chief Executive Officer of Paytm Payments Services Ltd. He has been associated with the company since September 2, 2019.

- Harinderpal Singh Takhar is the Chief Executive Officer of Paytm Labs Inc, their Subsidiary. He has been associated with Paytm Labs Inc. since June 2013.

COMPETITIVE STRENGTHS

- India's leading digital payment service platform.

- Strong brand identity with a brand value of US$6.3 billion.

- Large customer base with 333 million total customers, 114 million annual transacting users, and 21 million registered merchants.

- Paytm Super-app to access a wide range of digital payment services over mobile phones.

- Strong macro tailwinds.

- Increasing pace of digitization.

- Digital payments in India evolving rapidly

- Under-penetration and rising digitization of financial services

KEY CONCERNS

- They have a history of net losses and we may not be able to achieve profitability.

- The ongoing COVID-19 pandemic and measures intended to prevent its spread have had, and may continue to have, a material and adverse effect on the business and results of operations.

- The company may suffer if they are unable to retain existing customers, acquire new customers, grow the amount of consumer transactions, or increase in the client acquisition expenses.

- Their payment services account for the majority of their income. Their attempts to broaden their service offerings and market reach may not be successful, which might have a negative impact on their income.

- The business might suffer if they do not maintain or develop their technological infrastructure.

COMPARISON WITH LISTED INDUSTRY PEERS

There are no listed companies in India that engage in a business similar to that of the Company. Accordingly, it is not possible to provide an industry comparison in relation to the company

Why Did Paytm Stock Fall Sharply On The First Day Itself?

India’s leading digital payments system company Paytm made history after successfully launching India’s biggest ever IPO in the current month. As per the sources, the total worth of this public offering was Rs 18,300 Crores with the fixed price band at Rs 2080 to Rs 2,150 for each share.

The company hit headlines when the shares of the company made their market debut after much anticipation on Thursday at a 9 per cent discount. Against the expectations, Paytm Stock listed at Rs 1,955 dropped 9% from its issue price on the BSE. After some hours, the stock prices declined further and reached Rs 1,564 a share (a drop of 27.25%) & hit the lower circuit limit at the end of the day trade.

It has been seen that Paytm's market capitalization dropped to about $13.6 billion from its IPO valuation of $20 billion.

Here comes a question: How did India’s greatest IPO fail to give an outstanding performance? Let’s figure it out.

High Valuation Led to Losses for the Investors

Experts said that the company’s high valuation, loss-making business decisions and muted investor’s response are some of the primary reasons for the downfall, even though the company expects to break even by next year or in early 2023.

HNIs or and other powerful investors usually borrow funds for the IPO offerings at highly competitive rates. Hence, the investors will make a profit only if the IPO lists at a higher premium than the cost of funding.

After June 2021, merely 25% of the IPO were listed at a discount which led to a huge loss for the investors.

In the case of Paytm, the debut price was lower than anticipated as the stock opened at Rs 1,955 against the issue price of Rs 2,1050 at the upper end at BSE. The stock price is falling at 9.1 per cent. According to Money control, only aggressive investors were requested to put their money for future investments.

The weak response is being viewed as a sign that investors had become disillusioned with a recent string of IPOs with high valuations.

There are numerous reports out there that have claimed that Paytm’s business model lacks focus and attention.

Macquarie Stock Market Research firm has further said that achieving scale with profitability is the biggest challenge for the company. Also, the target price of Rs 1200 for the stock against its issue price of Rs 2,150 clearly shows the 40 per cent downside risks.

Competition May Drive Down Unit Economics

Also, the research firm points out that competitors of Paytm such as Amazon, Flipkart, Google etc are offering the same services. The competition became tough when new services such as Buy Today Pay Later were launched by the competitors.

This can be clearly seen from the fact that despite Paytm’s offering being much larger than other offerings, the demand was weaker than the recent stock sale. This is because Paytm has lost much of its market share to its competitors like Google and Flipkart.

Stiff Competition with Disruption in Business

Paytm holds its major competition with significant giants in the eCommerce industry like Amazon, GooglePay and Flipkart's Phone Pe. It faces intense competition from these adversaries in specific business areas like purchase currently pay later or buy today and pay later (BTPL)

Although Paytm's Rs. 18,300 crores IPO was listed at the top of the indicator range, it neglected to earn a lot of interest rather than other ongoing IPO events.

The biggest reason behind the market loss to Google Pay and Phone Pe was mainly responsible for this. It is also believed that the company’s FCF (Free cash flow) will not regain its pace till FY 2030.

In addition, the huge development in UPI-based payment structure hampered Paytm's business model.

UPI was presented by GOI in 2019 to build and promote a unified platform for payment in the whole country.

At this point, UPI represents almost 65% of Paytm's GMV, with a strong possibility to reach 85% by FY26

In any case, Paytm actually procures around 70% of its income from the payment business. It is a key part of the mobile wallet section. Nonetheless, this section has lost pertinence because of the advent of UPI payments.

Trouble to Achieve Scale with Profitability

According to a report by Macquarie Research, Paytm needs concentration, innovation and development in its business model. The firm accepts Paytm doesn't have the ability to accomplish scale with productivity.

The digital payment platform is associated with various business verticals, including consumer lending, payment gateway, monetary services etc. It has been consuming a lot of its money while attempting to maintain a few business fragments along with no emphasis on accomplishing benefits. In addition, Paytm procures lower revenue for every dollar it spends through advertising.

As such, the organization has been forced to move into other business segments as it is continuously looking for profitability. In any case, Paytm enjoys a huge client base with 50 million active customers and 22 million merchant banking clients.

Major Decline in Ecommerce Revenue

Paytm Mall, Paytm's internet business arm, contributes around 55% of its income in this income. During FY2019-21, the segment saw a sharp fall in income. This was predominantly because of rising competition from other significant adversaries.

Paytm neglected to stay aware of the internet business giants like Amazon and Walmart-possessed Flipkart. These players accompany a huge client merchant ecosystem and huge buyer offers.

Conclusion

Paytm stock crash tells us a lot. Only a good company is not the one that can offer you amazing benefits. There are certain things you need to ponder before subscribing to an IPO.

Therefore investors, keen to subscribe to SME IPOs must check the company’s financial and fundamentals. Carefully read the financial statements of a company, analyze its strength and weakness and valuations of a company before subscribing to the IPOs.

The IPO Rush: Why 2021 Proves To Be The Best Year of IPOs

Investment bankers and many investors tracking SME IPOs say that 2021 will be a record-breaking year for fundraising.

India is ready to make a record of the biggest IPO launching in the year 2021. In this blog, we will uncover all the reasons that why so many companies are going public this year:

Numerous companies including Policybazaar, Zomato, Paytm have gone public this year. Following the path of these giants, many more firms are expected to launch their IPO later this year.

This year, the companies are planning to raise the highest amount through IPO launching. Despite the impact of COVID 19, the companies are in a rush to go public.

Let’s try to figure out what is the top reason behind the IPO launching:

What is an IPO?

Initial public offering or IPO is a process under which a privately owned company offers its shares to people so that it can generate funds from investors. The process denotes the progress of a privately owned company to a public firm.

If an organization wants to become public, it has to follow two basic processes. Enter in the primary market to launch its IPO. Second, get listed on the stock exchange to become a publicly-traded company.

A few IPOs also include an Offer For Sale (OFS), which permits existing investors or promoters to minimize their shareholding in the listed companies.

Nevertheless, the amount raised through the OFS generally goes to private investors making their value available for sale.

Initial public offerings are a huge achievement for any company. They are raised when the company concludes it requires capital for a specific reason, like development, growth debt clearance, and funding corporate costs.

Any organization or startup doesn't grow immediately since its inception; they in the long run develop over a period to become more profitable and organized.

Different rounds of funding at the beginning stage and the further mixture of capital through private and private supporters lead to a company’s development.

There comes a turning point in any organization where its growth is soaked, and however the development rate may be positive, there is a flattened growth by a reduction in the rate.

At such a period, many companies are planning to go public via IPO to raise capital from the public.

There are times when a company is making a good profit, however, it needs more capital for development, growth and expansion as all the profits generated by it goes into debt clearance.

In such cases, going public not only helps the company to clear its debt but also utilizes its raised capital for the company’s further growth.

How do IPO’s Work?

Before going public, the privately held company seeks approval from the market regulator i.e. SEBI. Once it’s done, it starts revealing key insights regarding the IPO.

The key details include the price band for the IPO, lot size, launching date and distribution of share sales for various types of financial investors — non-institutional financial investors, institutional financial investors, existing employees and angel investors.

When the IPO process has begun, the company’s shares first start trading in the grey market — the informal market for unlisted shares. The process continues to take place till they are listed on the bourses.

It may be noticed that the grey market stocks are exchanged over-the-counter (OTC) and are not presented by the stock exchange; only traders are permitted to deal with them.

Investors normally get a small period i.e. typically 2-3 days to subscribe to a company’s public offering post IPO launching date.

During this period, investors (mostly retail investors) can bid for the offers through different stock trading platforms.

As the time period of IPO gets over, investors are required to check their IPO allotment status at their designation status on accessible channels - either the registrar or at the BSE site.

After the completion of allotment, the shares of the company get listed on the stock exchanges on a predetermined date.

Why IPO Rush: Reasons Why So Many Companies Going Public This year?

It has been seen that Several organizations have gone public regarding fundraising a year ago. Data suggest that organizations raised funds as much as $4.6 billion from IPOs last year. Analysts and investment bankers feel that this sum will be effectively outperformed in 2021 as more organizations are going for public offerings.

A head of investment banking at UBS India told Bloomberg that companies will generate twice the revenue as expected in the last year.

Many organizations have decided on IPOs at the end of 2020, because of the effect of the Covid-19 pandemic on business and the several securities exchange movements.

Experts further suggested that organizations are going public because of the highest performance found in the stock market and higher support of HNIs or high net worth individuals.

A State Bank of India (SBI) report recommended that over 14.2 million new individual investors have taken an interest in the stock market in 2020-21.

Indeed, even as the pandemic hits hard on India's economy, the domestic stock market has not been affected at all.

In fact, stock market indices such as Nifty 50 and BSE 30 have performed better than before.

If we talk about the market performance, a higher percentage of IPOs have done outstandingly well and more investors are hoping to capitalize on this period.

Organizations that are going public either bring capital because of the losses experienced during the Covid-19 pandemic or finance business expansion because of high demand.

Many techs and online delivery companies like Paytm, Nykaa, Zomato have gone public and the key reason is to raise capital and extend the business as the demand grows rapidly.

In the next few years, analysts expect over 50 digital tech companies will get listed on the bourses.

Star Health & Allied Insurance IPO

RatingSUBSCRIBE (Long Term Only)Issue OfferIssue Opens on Nov 30, 2021Issue Close on Dec 02, 2021Total IPO size (cr) 7,249.18Fresh issue 2000.00Offer For Sale (cr) 5,249.18Price Band (INR) 870-900Market Lot 16Face Value (INR) 10Retail Allocation 10%Listing On NSE, BSEObjects of the issue ⮚ To augment the company’s capital base and insolvency level.Issue Break-up (%)QIB Portion 75NIB Portion 15Retail Portion 10Shareholding (No. of Shares)Pre Issue 553,289,944Post Issue 575,620,567Indicative TimetableFinalisation of Basis of Allotment 07-12-2021Refunds/Unblocking ASBA Fund 08-12-2021Credit of equity shares to DP A/c 09-12-2021Trading commences 10-12-2021

SME-IPO of Star Health Insurance is on the boom as Star Health and Allied Insurance Company Ltd is one of the largest private health insurers in India with a market share of 15.8% in Fiscal 2021. From being the first standalone health insurance ("SAHI") company established in India in 2006, it has grown into the largest SAHI company in the overall health insurance market in India, according to CRISIL Research.

Company offer a range of flexible and comprehensive coverage options primarily for retail health, group health, personal accident and overseas travel, which accounted for 87.9%, 10.5%, 1.6% and 0.01%, respectively, of their total Gross written premium (GWP) in Fiscal 2021.

Individual agents are the primary distributors of the company's health insurance plans, accounting for 78.9% of their GWP in Fiscal 2021. In addition, the company has successfully built one of India's largest health insurance hospital networks, with 11,778 hospitals as of September 30, 2021.

⮚ Company consistently ranked first in the retail health insurance market in India based on retail health GWP over the last three Fiscal Years, according to CRISIL Research.

⮚ The retail health market segment is expected to emerge as a key growth driver for the overall health insurance industry in India after the COVID-19 crisis in India.

⮚ As of September 30, 2021 its distribution network had grown to 779 health insurance branches spread across 25 states and 5 union territories in India.

⮚ The company has also successfully built one of the largest health insurance hospital networks in India, with 11,778 hospitals, of which 7,741 hospitals, or 65.7 percent of the total number of hospitals in their network, entered into pre-agreed arrangements with in Fiscal 2021.

Outlook & Company Valuation:

The company has mixed set on financials over the last three years where the company's GWP has increased over the years while the company suffered a loss in FY21. In FY19, the revenues of the company were Rs 3713 cr while in FY21 it grew to 5283 cr.

The Profit was at Rs 128 cr in FY19 while the company suffered a loss of Rs 825 cr in FY21. The health insurance sector is likely to flourish as individuals become more aware of the benefits of health insurance. If we look at the company's financials, we can see that it was doing well until Covid hit last year. The company has the largest market share which is positive for the company however the industry is getting competitive.

The valuation of the company is stretched. At the upper price band of Rs. 900, Star Health is demanding an MCAP to net premium earned multiple of 10.3x, which is at a premium to the peer average.

IPO Note

STAR HEALTH AND ALLIED INSURANCE COMPANY LTD IPO

KEY MANAGERIAL PERSONNEL

⮚ Venkatasamy Jagannathan is the Chairman and CEO of the Company. He holds master’s degree of arts in economics and have more than 47 years of experience in the insurance industry

⮚ Subbarayan Prakash is the Managing Director of the Company. He has several years of experience as a surgeon and has previously worked with Saudi Operation & Maintenance Company Limited.

⮚ Anand Shankar Roy is the Managing Director of our Company. He holds a bachelor’s degree in commerce and he has 21 years of experience in the insurance industry

⮚ Sumir Chadha is a Non-Executive Nominee Director of the Company he has several years of investing experience in Indian companies, both public and private.

⮚ Deepak Ramineedi is a Non-Executive Nominee Director of the Company. He has several years of experience in the private equity industry

⮚ Utpal Hemendra Sheth is a Non-Executive Nominee Director of the Company. He holds a bachelor’s degree in commerce.

⮚ Rohit Bhasin is an Independent Director of the Company

⮚ Anisha Motwani is an Independent Director of the Company.

⮚ Berjis Minoo Desai is an Independent Director of the Company

⮚ Kaarthikeyan Devarayapuram Ramasamy is an Independent Director of the Company

⮚ Rajni Sekhri Sibal is an Independent Director of the Company

⮚ Rajeev Krishnamuralilal Agarwal is an Independent Director of the Company

COMPETITIVE STRENGTHS

⮚ Largest private health insurance company in India with leadership in the attractive retail health segment.

⮚ Largest and well spread distribution network in the health insurance industry.

⮚ Diversified product suite with a focus on innovation and specialized products.

⮚ Strong risk management with superior claims ratio and quality customer services.

⮚ Substantial investment in technology and innovative business processes.

⮚ Demonstrated track record of operating and financial performance.

⮚ Experienced senior management team with strong sponsorship.

KEY CONCERNS

⮚ Star Health Incurred Claim Ratio has increased from average 63.5% (FY2018 to FY2020) to 94% in FY21 and 91% in Q1 FY22. This is the main reason company has negative revenues and losses in the last 1.5 years.

⮚ The recent Covid-19 outbreak has had a significant impact on the company's business and operations.

⮚ They were able to keep their market share because of their strong brand name. However, if they fail to keep such a brand name, their business will suffer.

⮚ Company can be subject to claims by customers and/or regulators for alleged mis-selling.

⮚ Insurance companies depend on the accuracy and completeness of information provided by customers and counter parties for pricing and underwriting their insurance policies.

⮚ Any increase in competition could negatively impact the company’s profitability

IPO Note

STAR HEALTH AND ALLIED INSURANCE COMPANY LTD IPO

COMPARISON WITH LISTED INDUSTRY PEERS (As on 31st March 2021)

Name of the Company EPS (Basic) NAV P/E Net Worth (cr) RoNW (%)Star Health and Allied Insurance Co Ltd (16.54) 63.58 - 3,484.64 (23.69)% Peer GroupICICI Lombard General Insurance Co Ltd.* 32.41 163.56 46.66 7,435.15 19.81%New India Assurance Co Ltd 9.95 112.17 15.30 18,485.38 8.81%

*ICICI Lombard General Insurance Company Ltd. is not strictly comparable with the Company as they operate under general insurance with health insurance not forming a significant component, whereas the Company is a standalone health insurance provider.

FINANCIALS (RESTATED CONSOLIDATED)

Particulars (Rs. In Cr) FY 2021 FY 2020 FY 2019Equity Share Capital 548 491 456Other Equity 3,676 1,153 587Net Worth 4,224 1,644 1,043Total Borrowings 250 250 250Premiums earned (Net) 5,023 4,693 3,580Operating Profit/(Loss) (1,071) 361 165Profit Before Tax (1,046) 413 182Net Profit for the year (825) 268 128

Paytm Debacle Made Mobikwik Firm To Delay its Planned IPO: Key Reasons

A Gurugram based fintech startup Mobikwik, which was planning to go public this year, may defer its plan by two or three months or even more.

The official news of the delayed IPO comes just after Paytm’s gloomy market debut that saw its shares have gone down by 28% or more.

Seeing the current situation in the primary market, the fintech company has been advised to not go ahead with its IPO as it may face difficulties to find right investors both foreign and domestic.

Mobikwik, a small fintech startup compared to Paytm, had submitted its DRHP to SEBI for the SME-IPO in July. This includes a fresh issue of equity of Rs 1500 Crores and an OFfer for Sale (OFS) for another 400 crores.

What was the Original Plan?

The company had plans to hit the markets around Diwali and to raise Rs 1900 Crores approx by issuing its shares to the public. However, the financial advisors had advised the company to wait for the response to Paytm. Also, they suggested not to proceed with the SME-IPO launching, because of the shortening of demand from overseas investors.

After Paytm's debacle, the company is not in a mood to go ahead before January - February 2022.

The firm might have the option to go to the markets in December in case the investors’ reaction is good, if not, the plans might get delayed again.

Paytm's oxymoron listing and proceeding with underperformance, played a vital role in the decision to postpone the IPO plans.

MobiKwik's unlisted stock was trading at around Rs 1,350 before the launch of Paytm's IPO. From that point, the unlisted share price has decreased to about Rs 900, right around 33% lower, according to reports.

MobiKwik has an extraordinary DNA - it was bootstrapped for the initial 4 years and has accomplished its present size of 101 million clients (as of March 2021) having spent just $100 million since its inception.

The fintech startup mainly focuses on Buy Now Pay Later (BNPL) for day to day payments and has the biggest number of pre-supported BNPL users in India at 22.3 million (as of March 2021).

It has consistently adopted a sustainable growth strategy. The organization is seeing solid business development, has a way to productivity and will list at the right time - MobiKwik said according to a report.

Reasons Behind the Fall in the Company Valuations

As Paytm IPO was released with negative reviews, FinTechs have endured the shot and valuations of Mobikwik shares went further downhill by around 30-40 percent.

Indeed, even the retail financial investors are somewhat terrified since the Paytm IPO has drawn down their capital by approx 30%.

In June, the Abu Dhabi Investment Authority put $20 million in MobiKwik, which provided it with a valuation of about $700-750 million. Since the IPO launching, they had been planning to raise a valuation of more than $1 billion. However the reports say that the current financial investors are not in the mood for a public offering.

The interest for anchor books was repressed both from FIIS and domestic financial investors. This could bring about the delaying of the Mobikwik IPO shares. The more demand among anchor financial investors shows the willingness for financial investors to apply for a specific IPO.

A Sneak Peak into Mobikwik

Mobikwik is one of the biggest portable wallets (MobiKwik Wallet) and Buy Now Pay Later (BNPL) players in India dependent on mobile wallet wallet GMV and BNPL GMV, separately, in Fiscal 2021, its DRHP said.

In March, reports recommended that information of almost 110 million clients of MobiKwik was leaked on the dark web available to be purchased by programmers. The dataset included details of KYC documents, Aadhaar cards, Mastercard subtleties, cell phone numbers connected to MobiKwik wallet, and so forth.

The organization, in any case, had denied such information. Resulting reports in October also recommended that this supposed information breach of 3.5 million users at MobiKwik is presently under RBI's scanner.

About MobiKwik

Online wallet firm MobiKwik allows its users to make and get payments across different financial services like loans and insurance protection. It additionally has tie-ups with different monetary firms.

Also, it has been seen that, during the hour of filing DRHP with the SEBI, MobiKwik had a record of conducting nearly 10 Lakh every day transactions on its platform.

Takeaway

Till now, the fintech startup has not published its quarterly monetary outcomes for the Q2 of FY 2021-22. This shows the willingness of the organization to give Mobikwik IPO shares because the evaluated FS of the new quarter should be distributed before somewhere around 135 days after the end of the quarter.

The organization has saved a hole or pre IPO placements for its shares worth up to Rs 400 crore. MobiKwik’s promoters like Upasana Taku, and Bipin Preet Singh, have intended to sell part of their shares in the organization's secondary market according to the papers documented with SEBI.

Like Zomato and Nykaa, numerous different organizations are grappling to produce enough revenue just to legitimize their existence.

Go Fashion (India) Limited IPO

Rating SUBSCRIBE Issue Offer Issue Opens onNov 17, 2021Issue Close onNov 22, 2021Total IPO size (cr)1013.61Fresh issue125Offer For Sale (cr)888.61Price Band (INR)655-690Market Lot21Face Value (INR)10 Retail Allocation10%Listing OnNSE, BSE Issue Break-up (%) QIB Portion75NIB Portion15Retail Portion10Shareholding(No.ofShares)Pre Issue52,197,390Post Issue54,008,984 Indicative Timetable Finalisation of Basis ofAllotment25-11-2021Refunds/Unblocking ASBA Fund26-11-2021Credit of equity shares toDP A/c29-11-2021Trading commences30-11-2021

SME IPO of Go Fashion gathers a lot of attention as the company Go Fashion (India) Limited is one of the largest women's bottom-wear brands in India. The company is engaged in the development, design, sourcing, marketing, and retailing of a range of women's bottom-wear products under the brand, 'Go Colors'.

The company offers one of the widest portfolios of bottom-wear products among women's apparel retailers in terms of colors and styles. It is among the few apparel companies in India to have identified the market opportunity in women’s bottom-wear and have acted as a ‘category creator’ for bottom-wear.

It was the first company to launch a brand exclusively dedicated to women’s bottom-wear category and have leveraged this advantage to create a direct-to-consumer brand with a diversified and differentiated product portfolio of premium quality products at competitive prices. The company’s bottom-wear products, which include churidars, leggings, dhotis, harem pants, Patiala, palazzos, culottes, pants, trousers and jeggings, are sold across multiple categories such as ethnic wear, western wear, fusion wear, at leisure, denim, plus sizes and girls wear making their portfolio ‘universal’ and for every occasion.

- The women’s apparel market is estimated to be approximately 36% of the total apparel market while the women’s bottom-wear market contributed 8.3% of the women’s apparel market in Fiscal 2020

- The women’s clothing market in India has evolved in the past decade from traditional one-piece apparel to two-piece and mix-and-match apparel, with bottom-wear becoming an essential

- The company serve its customers primarily through its extensive network of 459 EBOs (Exclusive Brand Outlets) that are spread across 23 states and union territories in India, as of September 30, 2021.

- The company have its in-house design and merchandising team that designs and develops bottom-wear products across categories with their deep understanding of consumers’ requirements.

Financials and Outlook

The company has mixed set on financials over the last three years where the company's revenue grew in FY20 and fell back in the year FY21. However, the fall in revenue can be due to COVID-19. Profit also turned negative in a recent year where the company reported a loss of Rs (3.53) cr in FY21 VS a profit of Rs 52.63 cr in FY20. Go Colors has a strong brand value but has fluctuating revenues and the company moved into losses in FY21 but as the number of working women is increasing along with the evolving fashion trend it is expected that the company has strong growth momentum. The company has a mixed bag of financials and IPO is arriving at a P/BV of 13.65 based on its NAV of Rs. 50.56 as of Q1FY22, which seems to be attractively priced for the investors. Thus, we assign a "SUBSCRIBE" rating for listing gain and long term.

KEY MANAGERIAL PERSONNEL

- Prakash Kumar Saraogi is the Managing Director of the Company. He is a promoter of the Company and has over 28 years of experience in garment manufacturing, fashion industry and retail industry.

- Gautam Saraogi is an Executive Director and the Chief Executive Officer of the Company. He is also a promoter of the Company and has over 10 years of experience in consumer retail, marketing, brand building and garment

- Rahul Saraogi is a Non-Executive Director of the Company. He is a promoter of the Company and has over 10 years of experience in the garment industry.

- Ravi Shankar Ganapathy Agraharam Venkataraman is a Non-Executive Nominee Director of the Company. He has over 15 years of experience in private equity funds.

- Srinivasan Sridhar is the Chairperson of the Company’s Board and an Independent Director of the Company He has over 38 years of experience in commercial and development banking and is an associate of the Indian Institute of Bankers.

- Rohini Manian is an Independent Director of the She has over 8 years of experience in real estate and management space.

- Dinesh Madanlal Gupta is an Independent Director of the Company. He has over 37 years of experience in the transport and manufacturing industry.

- R Mohan is the Chief Financial Officer of the He has been associated with the company since April 16, 2019.

- Gayathri Venkatesan is the Company Secretary and Compliance Officer of the company. She has been associated with the company since October 25, 2019.

COMPETITIVE STRENGTHS

- Largest women’s bottom-wear brand in India with well-diversified product

- Multi-channel pan-India distribution network with a focus on EBOs, enhancing brand visibility

- Strong unit economics with an efficient operating model

- Extensive procurement base with highly efficient and technology-driven supply chain management

- In-house expertise in developing and designing products

- Demonstrated track record of strong financial performance

- Continue to expand retail network with a focus on EBOs

- Leverage technology to bring cost efficiency and enhance customer experience

KEY CONCERNS

- A major part of the issue is the offer for sale which would go to selling share

- The company carries operations from a single warehouse located in Southern India which could be a geographical limitation

- The company has incurred losses for FY21 for Rs 5 Crores and revenues also declined.

- Covid-19 pandemic has impacted the company and it might continue to impact future

- Dependency on the third party for the major operational part such as transportation and manufacturing

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App