Faalcon Concepts Share Price Jump: 20% Upper Circuit And Rs 101.93 Crore Order

Key Takeaways

- The faalcon concepts share price rose on a 20% upper circuit after a Rs 101.93 crore order.

- The order value is more than three times the company’s market capitalisation around Rs 33.45 crore.

- The contract spans three years with milestones linked to material delivery and execution.

- H2FY26 profitability rose with net profit at Rs 1.92 crore on net sales of Rs 19.5 crore, up 10.98% and 41.51% respectively.

The faalcon concepts share price sprinted into focus after a 20% upper circuit was triggered by a Rs 101.93 crore order for fade systems at Splendor ONYX in Noida. This is not a one-off event; it marks a potential inflection point for a company that designs, engineers, fabricates and installs end-to-end turnkey fade solutions for residential, commercial and institutional projects. The price move is being watched by retail investors who want to know whether this signal translates into durable earnings visibility or just a temporary spike in sentiment.

The company, headquartered in Gurugram, serves clients across multiple Indian states and exports fade materials to West African markets. It holds ISO 9001:2015 certification and offers a portfolio that includes curtain walls, aluminium doors and windows, skylights, canopies, stone and metal cladding, roofing and structural glazing solutions. In the coming sections, we’ll unpack what the deal means in terms of turnover, margins, and risk, so you can judge how the faalcon concepts share price movement might affect your portfolio.

Faalcon Concepts Share Price Drivers After The 20% Upper Circuit

The 20% upper circuit signals more than a one-day rally. The order was awarded for the design, fabrication, construction and installation of aluminum glazing fade works for Splendor ONYX, a flagship commercial building in Sector 142, Noida. With a three-year execution horizon and billing linked to material delivery and milestone achievement, the revenue recognition story is spread rather than front-loaded. For a tiny cap company, milestone-based invoicing can help improve cash flow visibility if milestones are met consistently and supplier credits align with delivery timelines.

From an investor’s vantage point, the market’s reaction hinges on two questions: Can this project become a recurring revenue driver or is it a one-off windfall? While this contract alone may not re-rate the stock overnight, it demonstrates that management can win large blue-chip projects in the fade systems space–an area that includes curtain walls, aluminium glazing and skylights, among other products. The long horizon of the contract also means the company could see revenue recognition events over multiple quarters, potentially supporting a steadier top line in H2FY26 and beyond.

Rs 101.93 Crore Order: What It Means For Faalcon Concepts Turnover And Profitability

The order is scheduled to be executed over three years, with billing linked to material delivery and execution milestones. Importantly, the contract is not a related-party transaction; neither promoters nor the promoter group have any interest in the customer, Splendor Information Technology. The customer relationship and the non-related nature of the contract add a degree of business legitimacy that investors seek in small-cap plays. For turnover and profitability, this order is a potential accelerator if milestones align with income recognition and if raw material prices and conversion costs are contained within margins.

In the broader financial narrative, the company reported a 41.51% increase in net sales to Rs 19.5 crore in H2FY26 versus H1FY26. Net profit rose 10.98% to Rs 1.92 crore on the back of that sales expansion. This combination–significant top-line growth with a positive bottom-line impulse–helps explain why the stock’s price movement is being watched with greater attention by investors who usually demand earnings visibility in a microcap space.

The Splendor ONYX Project In Sector 142 Noida: Growth Prospects For Fade Systems

Faalcon Concepts’ project with Splendor Information Technology centers on the Splendor ONYX commercial building in Sector 142, Noida. The contract covers the design, fabrication, construction and installation of aluminum glazing fade works–an end-to-end turnkey approach. The scope includes curtain walls, aluminium doors and windows, skylights, canopies, and related cladding and roofing solutions. Sector 142 is a busy commercial district, and success on this project could support a pipeline of similar opportunities in the National Capital Region and beyond, especially as developers push for energy-efficient and aesthetically advanced facade systems.

Headquartered in Gurugram, the company already serves clients across multiple Indian states and exports fade materials to West Africa. Its ISO 9001:2015 certification provides a competitive edge in tender processes where quality management and process discipline matter. A single large win can improve perception even if it does not transform the company’s entire order book. Still, management’s ability to execute this three-year engagement will be a key test of delivery capability, project management and supplier coordination in a capital-intensive segment.

Profitability And Revenue Trends In H2FY26: A Glance At The Numbers

On a consolidated basis, the company delivered a robust improvement in profitability in the latest reporting period. Net profit climbed 10.98% to Rs 1.92 crore, while net sales grew 41.51% to Rs 19.5 crore in H2FY26 versus H1FY26. These numbers, while coming from a relatively small base, offer a signal that management is driving margin-enhancing initiatives and capturing higher-value work across the fade systems spectrum. Margins in manufacturing segments like curtain walls and skylights often hinge on material efficiency, labor productivity, and the degree of turnkey control the firm maintains over procurement and installation. If the company can sustain milestone-based revenue recognition while preserving operating margins, the faalcon concepts share price narrative could gain more credibility among small-cap investors.

From a risk perspective, the single large project often creates concentration risk. Investors should monitor how the company diversifies its project mix going forward, whether it builds a broader customer base beyond Splendor Information Technology, and how it manages working capital with milestone billing. The combination of a three-year contract and the company’s ISO certification provides a framework for potential revenue stability, but execution risk remains a key variable that could drive volatility in the faalcon concepts share price over the near term.

Is The Faalcon Concepts Share Price Overvalued Or Justified By Fundamentals?

Valuation discussions for microcap names like Faalcon Concepts hinge on growth potential relative to the scale of the business. With a market capitalisation around Rs 33.45 crore and an order book that includes a Rs 101.93 crore contract spanning three years, investors need to weigh what portion of the growth is embedded in the current price. The company’s product portfolio–curtain walls, aluminium doors and windows, skylights, canopies, stone and metal cladding, roofing and structural glazing–positions it in a niche yet expanding segment of building facades that emphasizes energy efficiency and aesthetics. The presence of ISO 9001:2015 certification adds credibility to its manufacturing and quality processes, which is a critical factor in tender-based project wins.

Fundamental questions to answer include: How sustainable is the order backlog? What is the potential pipeline beyond Splendor ONYX? Can the company translate project milestones into reliable cash flows that support margin expansion? While the numbers in H2FY26 look encouraging, the brief window in time makes it hard to draw definitive conclusions about the stock’s longer-term fair value. For now, the price action may reflect both excitement about a sizeable order and ongoing questions about how scalable the business is beyond a few marquee projects.

Risks And Opportunities For Retail Investors In A Specialist Fade System Maker

Investors in microcap fabricators of building facades should be mindful of several risks. The concentration risk is notable: a big contract with Splendor ONYX offers high potential upside but also adds vulnerability if project execution slows or if a competitor wins similar opportunities. The macro environment–capital expenditure cycles in real estate and construction–will influence order flow in the near term. On the upside, the company’s end-to-end capabilities and ISO 9001:2015 certification can help win tender processes that prioritize quality, safety and timeliness. A broader geographic footprint and a diversified client base could transform this from a one-off win into a multi-quarter growth story.

For retail investors seeking to quantify risk, the rule of thumb is to assess the quality of the order book, the likelihood of additional large orders, the pace of revenue recognition, and the consistency of cash flow from milestones. It’s also prudent to keep an eye on any shifts in raw material costs (aluminium, glass, cladding) and labour costs that affect margins. In a sector where project-based revenue can be lump, the best approach is to monitor a few leading indicators–order intake in relevant quarters, project backlog growth, and the consistency of cash flow from milestones. When used in combination with broader market conditions, these indicators can help you gauge whether the faalcon concepts share price signal is likely to sustain its momentum or retreat in the near term.

Beyond current results, retail investors should watch for updates on milestone attainment, any sign of new project wins, and management commentary about the product mix and pricing power. Milestone-driven revenue can be a double-edged sword: it can stabilize cash flow when projects progress smoothly but may amplify volatility if deliverables slip. A practical approach is to track the progress of Splendor ONYX’s glazing milestones and to listen for any guidance from management on the pace of execution and expected revenue recognition in upcoming quarters.

For deeper stock research tailored to your portfolio, consult Swastika's Sarthi AI stock assistant. It can help you model scenario-based outcomes and compare faalcon Concepts with peers in the niche façade solutions space, factoring in order backlogs, margin trajectory, and capital structure. Remember, this is a small-cap stock with unique exposure to a few high-value contracts, so use due diligence and position sizing to manage risk while exploring growth opportunities.

Frequently Asked Questions

What triggered the 20% upper circuit in faalcon concepts share price?

A Rs 101.93 crore order for the design, fabrication, construction and installation of aluminum glazing fade works for Splendor ONYX in Noida, executed over three years.

How does the Rs 101.93 crore order compare to the company's market capitalisation?

The order value is over three times the company's market capitalisation of about Rs 33.45 crore.

What is Faalcon Concepts' core business?

Faalcon Concepts designs, engineers, fabricates and installs fade systems, including curtain walls, aluminium doors and windows, skylights, canopies, stone and metal cladding, roofing and structural glazing.

What were the H2FY26 profitability figures?

Net profit rose 10.98% to Rs 1.92 crore on a 41.51% increase in net sales to Rs 19.5 crore in H2FY26 over H1FY26.

What should retail investors watch next?

Watch milestone progress on the three-year project, monitor potential new orders, and assess whether the company can sustain revenue growth and margins beyond Splendor ONYX while considering diversification and working capital management.

Conclusion

The near-term signal is that a Rs 101.93 crore order in a niche fade-systems business adds credibility to a microcap growth thesis, with a 20% upper circuit acting as a price anchor rather than a random spike. For the retail investor, the key question is whether management can translate these large, milestone-linked orders into consistent cash flows and margin improvement while diversifying the client base beyond Splendor ONYX. The next steps are to monitor milestone progress, review quarterly backlogs, and use a structured framework–such as scenario analysis and cash-flow tests–to decide how much of the faalcon concepts share price rally is justified by fundamentals and how much remains behavioral or news-driven.

As you evaluate the stock, consider the three-year execution horizon, the portfolio you build around it, and the possibility of more orders in the fade systems niche. If you want a disciplined, data-driven view of how this stock might fit into your strategy, check Swastika's Sarthi AI stock assistant for a deeper, institutional-grade perspective on any stock or index.

Latest Articles

मजबूत बांड यील्ड से दबाव में सोना।

त्यौहार के सीजन से पहले कठोर मौद्रिक नीति के संकेतो से सोने और चांदी के भाव सस्ते हो गए है। और भारत में त्यौहार पर रीती रिवाज़ों के चलते पितृपक्ष के बाद सस्ते भाव होने के कारण इनकी हाज़िर मांग को अच्छा सपोर्ट देखने को मिल सकता है। भारत में पहली तिमाही में सोने की मांग में गिरावट देखने को मिली थी जबकि दूसरी तिमाही में मांग 4 प्रतिशत से बढ़ने का अनुमान है। हालांकि, बांड यील्ड में लगातार बढ़ोतरी होने के कारण गैरउपज वाली संपत्ति सोने से निवेशको ने छोटी अवधि के लिए दुरी बना रखी है। एसपीडीआर गोल्ड ट्रस्ट की सोने में होल्डिंग घट कर चार साल के निचले स्तरों पर पहुंच गई है। अमेरिका में आर्थिक मंदी का डर कम होने के बाद से ही निवेशक लम्बी अवधि के गवर्नमेंट बांड यह मान कर बेच रहे है की अर्थव्यवस्था ज्यादा नहीं सिकुड़ेगी। जबकि चीन, जो अमेरिकी ट्रेज़री का सबसे बड़ा होल्डर है, में आर्थिक मंदी रहने के कारण ट्रेज़री में नई खरीद नहीं हो रही है और अमेरिकी डेब्ट की रेटिंग घटने के बाद फेड द्वारा भी बांड खरीद कम हुई है जिससे बांड यील्ड में बढ़ोतरी हुई है और कीमती धातुओं के भाव में दबाव बना हुआ है। रोज़गार बाजार और मुद्रास्फीति में स्थिरता ब्याज दरों को लम्बी अवधि के लिए उच्च स्तरों पर बनाये रख सकता है, हालांकि ग्लोबल अर्थव्यवस्था की सुस्त चाल और भूराजनीतिक मुद्दो के रहते सोने में लम्बी अवधि की तेज़ क़ायम रह सकती है। पिछले सप्ताह एमसीएक्स दिसंबर वायदा सोने में 2 प्रतिशत की गिरावट के बाद भाव 56500 रुपये प्रति दस ग्राम और चांदी में 4.5 प्रतिशत की गिरावट के बाद भाव 66800 रुपये प्रति किलो पर रहे।

तकनिकी विश्लेषण :

इस सप्ताह कीमती धातुओं के भाव सीमित दायरे में रह सकते है। एमसीएक्स दिसंबर वायदा सोने में सपोर्ट 55000 रुपये पर है और रेजिस्टेंस 58000 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 62000 रुपये पर है और रेजिस्टेंस 70000 रुपये पर है।

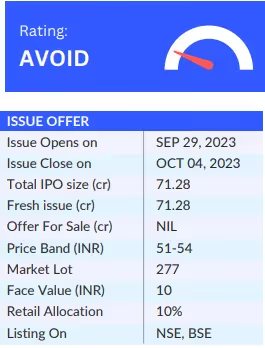

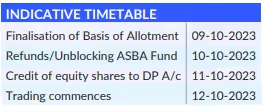

Plaza Wires Limited IPO details

Plaza Wires Limited is engaged in the business of manufacturing and selling wires, and selling and marketing LT aluminum cables and fastmoving electrical goods (“FMEG”) under its flagship brand “PLAZA CABLES” and home brands such as “Action Wires” and “PCG”. Its product mix comprises different type of wires and cables, and FMEG such as electric fans, water heaters, switches and switchgear, PVC insulated electrical tape, and PVC conduit pipe & and accessories.

OBJECTS OF THE ISSUE

- Funding capital expenditure requirements of the Company. Funding the working capital requirements of the company.

- General corporate purposes.

Mr. Sanjay Gupta

Managing Director and one of the Promoters of the Company. He has been on the Board of Directors of the Company since March 12, 2008 and was appointed as the Managing Director and Chairman of the Company since March 10, 2022. He possesses approximately 26 years of experience in the electrical industry.

Mrs. Sonia Gupta

Whole-time Director and one of the Promoters of the Company. She has been on the Board of Director of the Company since March 21, 2008. She has approximately 26 years of work experience in the electrical industry. She has been instrumental in planning and formulating the overall business and commercial strategy and managing the financial planning of the Company.

Mr. Ajay Kumar Batla

Chief Financial Officer of the Company. He joined the Company on April 1, 2009. He has been appointed as CFO of the Company with effect from March 10, 2022. He participates in the key decisions of the Company and inter-alia develops financial and tax strategies and monitors budgeting of the Company.

Ms. Bhavika Kapil

Company Secretary and Compliance Officer of the Company. She was appointed as the Company Secretary and Compliance Officer of the Company with effect from March 10, 2022. She is responsible for handling secretarial compliances in the Company. She has a work experience of approximately 3.5 years as she was appointed in Fiscal 2022.

COMPANY PROFILE

- Plaza Wires Limited’s key products in the wires and cables segment include house wires, single & and multicore round flexible industrial cables, and industrial cables for submersible pumps & and motors up to 1.1kv grade.

- The company also provides other wires and cable products such as LT power control cables, TV dish antenna co-axial cables, telephone & and switchboard industrial cables, computer & LAN networking cables, close circuit television cables and solar cables, PVC insulated tape, and PVC conduit pipe & accessories, through third-party manufacturers.

- The Company sells its products through a variety of distribution channels depending on the geography and industry norms and trends. Its business model includes 1) Its dealer & and distribution network. 2) Securing government tenders, and 3) Direct sales to infrastructure projects

- The existing Manufacturing Unit is located at Baddi, Himachal Pradesh with an installed production capacity of 12,00,000 coils per annum.

COMPETITIVE STRENGTHS

- Product portfolio focused on various customer segments and markets. Distribution network.

- Management and dedicated employee base. Strategically located Manufacturing Facility.

KEY STRATEGIES

- Setting up the Proposed Manufacturing Unit to widen its product portfolio and increase its capacity. Enhance its position in the Wires and Cables Industry.

- Expand its dealer network in existing markets and enter new geographical markets. Strengthen its brand value.

- To use technology to further optimize its sales & and marketing operations.

KEY CONCERNS

- Inadequate or interrupted supply and price fluctuation of its raw materials and packaging materials could adversely affect its business.

- The company requires significant amounts of working capital.

- Its existing and proposed manufacturing facilities are concentrated in a single region.

- The industry segments in which it operates are fragmented, and it face competition from large players.

- It relies on certain third-party manufacturers for manufacturing some of its products.

- Pricing pressure from dealers and distributors may affect its gross margins and ability to increase its prices.

- The Company does not have any long-term or definitive agreements with its dealers or customers.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

FINANCIALS (RESTATED CONSOLIDATED)

OUTLOOK & VALUATION

Plaza Wires operates in the wires and cables segment, and it also offers fast-moving electrical goods. The company is focused on various customer segments and has a large distribution network. Its financial performance has been stable.

However the company relies on certain third-party manufacturers for some of its products, and it also faces competition from large players in the industry. Also, it does not have any long-term contracts with its dealers and customers.

Though the IPO is coming at a fair P/E valuation of 21.95x, considering its small issue size, current market conditions, and other related risks, we will avoid this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

Valiant Laboratories IPO Review - GMP, Price, Details

Valiant Laboratories Limited is an Active Pharmaceutical Ingredient (“API”) / Bulk Drug manufacturing company with having focus on the manufacturing of Paracetamol. The Company manufactures Paracetamol in various grades such as IP/BP/EP/USP, as per the pharmacopeia requirements of its customers.

OBJECTS OF THE ISSUE

- Investment in its wholly-owned subsidiary VASPL for its capital expenditure and working capital requirements.

- General corporate purposes.

Velji Karamshi Gogri

Chairman, Independent and Non- Executive Director of the Company. He has experience of more than 45 years in the Chemical Industry involved in setting up and operating bulk drugs intermediates and fine chemicals manufacturing units and handling different chemical processes and equipment.

Santosh Shantilal Vora

Managing Director of the Company. He has experience of over 7 years in the chemical industry. He is one of the founding members of the Company and looks after the day- to-day affairs of the Company. He handles the responsibility of looking after new product development, infusion and upgradation of technology in operations and production process of the Company.

Paresh Shashikant Shah

Executive Director and Chief Financial Officer of the Company. He has been associated with the Company since 1985. He has experience of over four decades in the chemical industry. He is also one of the founding members of the Company and a director on the Board since incorporation.

Saloni Mehta

The Company Secretary & Compliance Officer of the Company. She is a qualified Company Secretary and is an associate member of the Institute of Company Secretaries of India. She has over two years of experience in the field of company law and SEBI Listing Regulations related compliance. She has been associated with the Company since November 30, 2021

COMPANY PROFILE

- Valiant Laboratories Limited was originally formed in year 1980 as a partnership firm under the name and style of “M/s. Bharat Chemicals” and gradually, commenced manufacturing of Paracetamol by late 1982.

- Its manufacturing unit is located in Palghar, Maharashtra, spread over 2,000 sq. mts. of land with an aggregate annual installed capacity of 9,000 MT per annum.

- Within its Manufacturing Facility located at Tarapur Industrial Area, Palghar, Maharashtra it also has an in-house R&D infrastructure.

- The Company, through its wholly-owned subsidiary, Valiant Advanced Sciences Private Limited intends to establish a greenfield project at Saykha Industrial Area, Bharuch, Gujarat. which shall venture into the manufacture of specialty chemicals and assist it in the backward integration process.

COMPETITIVE STRENGTHS

- Experienced promoters and strong management team.

- Strong financial performance.

- Reducing dependence on import of raw materials.

- Strategically located Manufacturing Facility.

KEY STRATEGIES

- Diversification into new chemistries and industry. Increase in market share.

- Improve operational efficiencies through backward integration of the Proposed Facility. Increase its penetration into international markets including regulated markets.

KEY CONCERNS

- It is a single-product manufacturing company and any changes to the paracetamol API industry or its product demand will adversely affect its business.

- The Company operates out of a single Manufacturing Facility. Any significant social, political, or economic disruption natural calamities, or civil disruptions in this region may impact its business. Subject to strict quality requirements, regular inspections, and audits by our customers and any failure to comply with quality standards may lead to cancellation of existing and future orders. limited number of suppliers for its raw materials which are highly concentrated in the western region of India.

- Dependent on a few customers for a major part of its revenues. The pharmaceutical industry is intensely competitive.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

.avif)

FINANCIALS (RESTATED CONSOLIDATED)

.avif)

OUTLOOK & VALUATION

Valiant Laboratories is a 40-year-old pharmaceutical ingredient manufacturing company with a main focus on paracetamol. Currently, it operates from its only manufacturing unit in Palgarh, Maharashtra; however, it is planning to establish a new project in Gujarat through its subsidiary. Its financial performance has been improving, and it has the benefit of experienced promoters.

But it is a single-product manufacturing company. Secondly, it is dependent on a limited number of suppliers as well as customers. Also, there is intense competition in this industry along with high regulations. The issue is coming at a P/E valuation of 15.7, which seems fair, but considering other risks and current market volatility, we will avoid this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

JSW Infrastructure IPO Details

JSW Infrastructure Limited provides maritime-related services including cargo handling, storage solutions and logistics services. The company develop and operates ports and port terminals under Port Concessions. JSW Infrastructure Limited is part of the JSW Group. JSW Infrastructure is the 2nd largest commercial port operator in the country in terms of cargo handling capacity in Fiscal 2022.

OBJECTS OF THE ISSUE

- Payment of borrowings.

- Financing capital expenditure requirements. General corporate purposes.

Sajjan Jindal

Chairman and Non-Executive Director of the Company. He is the vice chairman of the World Steel Association and is also on the board of directors of JSW Energy Limited. He has over 36 years of experience in the manufacturing and steel industry.

Nirmal Kumar Jain

Vice Chairman and Independent Director of the Company. He joined Jindal Iron & Steel Company Limited in 1992 as general manager – finance. He has over 21 years of experience in the financial services sector.

Arun Sitaram Maheshwari

Joint Managing Director and Chief Executive Officer. He has previously been associated with Jindal Strips Limited, Jindal Iron & Steel Company Limited and Jindal Vijaynagar Steel Limited. He has over 30 years of experience in the areas of marketing, import (raw materials), corporate strategy and infrastructure.

Lalit Chandanmal Singhvi

Whole Time Director and Chief Financial Officer of the Company.He has over 21 years of experience in management and finance. He has been associated with our Company since January 15, 2015 as senior vice president – finance and commercial.

Kantilal Narandas Patel

Non-Executive Director of the Company. He has over 28 years of experience in the financial services sector and the steel industry. He was previously associated with JSW Holdings Limited as joint managing director and chief executive officer.

COMPANY PROFILE

- JSW Infrastructure’s operations have expanded from one Port Concession at Mormugao, Goa which was acquired by the JSW Group in 2002 and commenced operations in 2004, to nine Port Concessions as of June 30, 2023 across India.

- It is the fastest-growing port-related infrastructure company in terms of growth in installed cargo handling capacity and cargo volumes handled from Fiscal 2021 to Fiscal 2023.

- The company has a diversified presence across India with Non-Major Ports located in Maharashtra and port terminals located at Major Ports across the industrial regions of Goa and Karnataka on the west coast, and Odisha and Tamil Nadu on the east coast. The company’s international presence includes 2 terminals at Fujairah and Dibba in the UAE

- The company’s ports and port terminals typically have long concession periods ranging between 30 to 50 years, providing long-term visibility of revenue streams.

COMPETITIVE STRENGTHS

- Fastest growing port-related infrastructure company and second largest commercial port operator in India.

- Strategically located assets at close proximity to JSW Group Customers (Related Parties) and industrial clusters supported by a multi-modal evacuation infrastructure.

- Strong financial metrics with a growing margin profile, return metrics, and growth. Diversified operations in terms of cargo profile, geography, and assets.

- Demonstrated project development, execution, and operational capabilities.

- Benefit from the strong corporate lineage of the JSW Group and a qualified and experienced management team.

KEY STRATEGIES

- Continue to pursue greenfield and brownfield expansions with a focus on Non-Major Ports Pursue acquisition opportunities in similar businesses.

- Increasing third-party customer base.

- Pursue opportunities in synergistic businesses to increase revenue diversification. Focus on building environment friendly and sustainable operations along with growth.

KEY CONCERNS

- A substantial portion of the volume of cargo handled by the company is dependent on a few types of cargo.

- It derives a substantial portion of its revenue from its top five customers Certain of its Subsidiaries have incurred losses in the past.

- It operates in a capital-intensive industry and its current and future expansion plans may require significant capital.

- The company's business operations are subject to a wide range of environmental and other regulations, and any changes to these regulations could increase the company's costs.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

..%252C.avif)

FINANCIALS (RESTATED CONSOLIDATED)

%252C.avif)

OUTLOOK & VALUATION

As a division of the JSW Group, JSW Infrastructure offers logistical, cargo handling, and other maritime-related services. The second-largest commercial port operator in India, the corporation has the fastest rate of growth in the infrastructure associated with ports.

The business's financial performance is quite strong, and both its sales and net worth are increasing. The ratio of debt to equity is 0.54, which is quite favorable. The issue size is about 2800 crore, and the IPO is full of fresh issues. last but not least, coming to the IPO valuation the issue is priced at a P/E valuation of about 28x, and EV/EBITDA is 15.17 which looks reasonable.

We will therefore subscribe to this IPO for listing benefits and for long terms due to valuation and current market sentiments.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.inPhone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

Updater Services IPO Date, Price, GMP, Review, Details

Updater Services Limited is an integrated business services platform in India offering integrated facilities management (“IFM”) services and business support services (“BSS”) to its customers, with a pan-India presence.

OBJECTS OF THE ISSUE

- Payment of certain borrowings.

- Funding the working capital requirements. Pursuing inorganic initiatives.

.webp)

Raghunandana Tangirala

Promoter, Chairman and Managing Director of the Company. He is one of the founding directors of the Company and has been on the board since its incorporation. In the Company, he focuses primarily on corporate governance, organizational development, capital allocation and strategic growth of the Company. He has approximately 30 years of experience.

C. R. Saravanan

Director of business operations of the Company. He has been associated with the Company since October 3, 2016. In the Company, he handles the pan India business operations.

Balaji Swaminathan

Chief Financial Officer of the Company. He has been associated with the Company since December 11, 2019. He handles finance & accounts and compliances of the Company. He holds a bachelor’s degree in commerce from University of Madras. He is an associate member of the Institute of Chartered Accountants in India.

Ravishankar B

Company Secretary of the Company. He has been associated with the Company since March 6, 2023. In the Company, he is responsible for secretarial compliances. He holds a bachelor degree in commerce from the University of Madras. He is an associate member of the Institute of Chartered Accountants of India and an associate member of the Institute of Company Secretaries in India.

COMPANY PROFILE

- Updater Services Limited commenced operations in 1990 as a housekeeping and catering services company situated in Chennai, Tamil Nadu.

- Over the years, it has evolved into an integrated business services platform with a pan-India presence serving customers across industries and business service lines.

- In IFM other service segments include Production Support Services, Soft Services, Engineering Services, Washroom and feminine hygiene, Warehouse management, General Staffing, and more. In the BSS segment, the company offers Audit and Assurance services, employee background verification check services, airport ground handling services, sales enablement services, and more through its subsidiaries.

- All these services are B2B services which are primarily in the nature of annuity-based services whereby the customer, once acquired, generates revenue over an extended period of time.

- It served 2,797 customers across various sectors, including certain marquee global and Indian customers.

COMPETITIVE STRENGTHS

- Leading integrated business services platform, operating across diverse segments. Longstanding relationship with customers across diverse sectors leading to recurring business. Track record of successful acquisition and integration of high-margin business segments.

- Pan India presence with a large and efficient workforce. Technology at the forefront of its current and future business.

- Highly experienced Management team with support from PE Investors.

KEY STRATEGIES

- Retain, strengthen, and grow customer base. Grow market share in key segments.

- Introduce new products and services catering to existing and new customer segments. Pursue inorganic growth through strategic acquisitions.

- Continue to improve operating margins.

KEY CONCERNS

- The Company employs a large workforce of 65,627 employees as of June 30, 2023, thus it faces significant employee-related regulatory risks.

- Operational risks, as it provides services in different business environments.

- It witnessed a reduction in its profit in the Financial Year ending March 31, 2023. Any delay or default in receiving payments for services rendered by the Company.

- The Company is exposed to service-related claims and losses or employee disruptions that could have an adverse effect on its business.

- The industries in which it operates are intensely competitive.

- Certain of the services that it offer to its customers are subject to seasonal variations.

COMPARISON WITH LISTED INDUSTRY PEERS (AS ON 31ST MARCH 2023)

...avif)

FINANCIALS (RESTATED CONSOLIDATED)

..avif)

OUTLOOK & VALUATION

Updater Services Ltd. (UDS) is a leading business services platform that offers a diverse range of services to customers (B2B) across diverse sectors. The company has a pan-India presence and a large workforce.

The financial performance of the company has been mixed, with growing revenue but declining profit. The company faces certain regulatory and operational risks due to the nature of its business. It is also exposed to service-related claims and losses.

Lastly, the issue is priced at a P/E of 44.3x, which is significantly higher than its listed peers. Thus, considering all the factors, we will avoid this IPO.

DISCLAIMER:

The information contained herein are strictly confidential and are meant solely for the information of the recipient and shall not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written permission of Swastika Investmart Ltd. (“SIL”). The contents of this document are for information purpose only. This document is not an investment advice and must not alone be taken as the basis for an investment decision. Before taking any decision to invest, the recipient of this document must read carefully the Red Herring Prospectus (“RHP”) issued to know the details of IPO and various risks and uncertainties associated with the investment in the IPO of the Company. All recipients of this document must before acting on the given information/details, make their own investigation and apply independent judgment based on their specific investment objectives and financial position. They can also seek appropriate professional advice from their own legal and tax consultants, advisors, etc. to understand the risks and investment considerations arising from such investment. The investor should possess appropriate resources to analyze such investment and the suitability of such investment to such investor’s particular circumstances before making any decisions on the investment. The Investor shall be solely responsible for any action taken based on this document. SIL shall not be liable for any direct or indirect losses arising from the use of the information contained in this document and accept no responsibility for statements made otherwise issued or any other source of information received by the investor and the investor would be doing so at his/her/its own risk. The information contained in this document should not be construed as forecast or promise or guarantee or assurance of any kind. The investors are not being offered any assurance or guaranteed or fixed returns on their investments. The users of this document must bear in mind that past performances if any, are not indicative of future results. The actual returns on investment may be materially different than the past. Investments in Securities market products and instruments including in the IPO of the Company are highly risky and they are generally not an appropriate avenue for someone with limited resources/ limited investment and low risk tolerance. Such Investments are subject to market risks including, without limitation, price, volatility and liquidity and capital risks. Therefore, the users of this document must carefully consider all the information given in the RHP including the risks factors before making any investment in the Equity Shares of the Company.

Swastika Investmart Ltd or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither Swastika Investmart Ltd nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. Swastika Investment Ltd may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

CORPORATE & ADMINISTRATIVE OFFICE - 48, Jaora Compound, M.Y.H. Road, Indore - 452 001 | Phone 0731 - 6644000

Compliance Officer: Ms. Sheetal Duraphe Email: compliance@swastika.co.in Phone: (0731) 6644 241

Swastika Investmart Limited, SEBI Reg. No. : NSE/BSE/MSEI: INZ000192732 Merchant Banking: INM000012102 Investment Adviser: INA000009843 MCX/NCDEX: INZ000072532 CDSL/NSDL: IN-DP-115-2015 RBI Reg. No.: B-03-00174 IRDA Reg. No.: 713.

उच्च ब्याज दरों से दबाव में सोना।

फेड बैठक के बाद सोने की कीमते सप्ताह के निचले स्तरों पर आ गई, हालांकि कीमतों में गिरावट सीमित रही जबकि चांदी में 2 प्रतिशत की तेज़ी के बाद भाव 73600 रुपये प्रति किलो पर पहुंच गए। पिछले सप्ताह की बैठक में फेडरल रिजर्व ने तब तक दरें बढ़ाने के संकेत दिए है जब तक कि मुद्रास्फीति अपने वार्षिक लक्ष्य 2 प्रतिशत पर वापस नहीं आ जाती। जिसके कारण एमसीएक्स में सोना 0.20 की साप्ताहिक गिरावट के बाद 58800 रुपये प्रति दस ग्राम के स्तरों पर कारोबार करता दिखा। मौद्रिक नीति पर फेड के कड़े रुख के कारण स्पॉट गोल्ड 1950 डॉलर के महत्वपूर्ण स्तरों को पार नहीं कर पाया है जबकि यह महत्वपूर्ण सपोर्ट 1900 डॉलर के ऊपर बना हुआ है। बेंचमार्क अमेरिकी 10-वर्षीय ट्रेज़री यील्ड 4.5 प्रतिशत के शिखर पर पहुंचने के बाद सोने में दबाव बढ़ गया है, जो 2007 के बाद से सबसे अधिक है, और यह बांड बाजार में भारी बिकवाली को दर्शा रहा है। इस बीच, डॉलर इंडेक्स छह महीने के उच्चतम स्तर पर पहुंच गया, जिससे अन्य मुद्राओं के धारकों द्वारा डॉलर में कारोबार करने वाली वस्तुओं की खरीदारी सीमित कर दी है। पिछले सप्ताह फेड की नीति बैठक में सितंबर के लिए दरों को अपरिवर्तित छोड़ने के बावजूद, फेड द्वारा इस साल के अंत तक ब्याज दरों में एक और 0.25 प्रतिशत वृद्धि का अनुमान लगाया है। ब्याज दरों में बढ़ोतरी रोकने के बाद भी उच्च दरें लम्बी अवधि तक बने रहने के संकेत दिए है, जिससे सोने की कीमतों में दबाव बना रह सकता है जब तक की उच्च ब्याज़ दरों के कारण आर्थिक मंदी हावी नहीं हो जाती है।

तकनिकी विश्लेषण

इस सप्ताह कीमती धातुओं के भाव सिमित दायरे में रहने की सम्भावना है। एमसीएक्स अक्टूबर वायदा सोने में सपोर्ट 58000 रुपये पर है और रेजिस्टेंस 59500 रुपये पर है। दिसंबर वायदा चांदी में सपोर्ट 71000 रुपये पर है और रेजिस्टेंस 75000 रुपये पर है।

Big Budget

Popular Articles

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App