Adani Power ₹4,194 Cr Stake - Should You Buy or Hold in Your Portfolio?

TLDR

- Adani Power to acquire 24% stake in Jaiprakash Power Ventures Ltd for ₹4,194 crore.

- Direct impact on your portfolio may include volatility in energy stocks and potential re-rating of thermal assets.

- Top priority sectors: Power & Utilities and Energy Infrastructure.

- Action: Review exposure to energy names and prepare to adjust on regulatory clarity and integration progress.

News Context and Market Impact

What Happened

Adani Power announced its plan to acquire Jaiprakash Power Ventures Ltd's 24% stake, held by Jaiprakash Associates, in a transaction valued at ₹4,194 crore. The agreement accelerates Adani Power's asset base in the thermal segment and expands its generation footprint through a strategic stake in JPVL's assets.

Why This Matters

The deal signals ongoing consolidation in India's power sector, potential synergies in fuel procurement and capacity utilization, and could influence valuations across listed players in the thermal space. For retail investors, it offers greater visibility into a major expansion move by a prominent player, while also raising questions about debt levels, financing structure, and integration risk.

Portfolio and Strategy Focus

What This Means For Your Portfolio

If you hold Adani Power or related energy names, expect near-term volatility around this deal and its financing details. A prudent approach is to avoid overexposure to a single promoter-led energy bet and maintain a diversified mix. Align your holdings with a balance of growth prospects and risk controls, particularly given debt and asset quality concerns in thermal assets.

Sectors To Watch - Priority Order

- 1st Priority: Power & Utilities - rationale: consolidation can alter asset mix and pricing power.

- 2nd Priority: Energy Infrastructure & M&A - rationale: potential pipeline and funding changes may affect valuations.

- Avoid Now: Real Estate - rationale: not a primary beneficiary of this deal and remains exposed to liquidity risk.

Action Points For Investors

- SIP investors: Maintain diversified contributions and avoid top-heavy bets on a single power stock.

- Lumpsum investors: Consider waiting for regulatory clarity and a fuller financial picture before new commitments in the sector.

- Traders: Prepare for short-term volatility around Adani Power and peers; set stop-loss levels and watch for management commentary on integration plans.

Swastika Investmart notes that this deal highlights the ongoing consolidation in the Indian power sector. For you, it emphasizes the need for a diversified portfolio and careful risk management as asset bases evolve under large corporate buyers. Keep monitoring regulatory approvals and asset performance and adjust exposure accordingly.

Risks and Cautions

Key Risks To Watch

- Execution and integration risk if the deal proceeds with complex regulatory approvals.

- Debt impact and funding requirements that could affect Adani Power’s balance sheet.

- Valuation and asset performance risk if the acquired assets underperform or face operational challenges.

Frequently Asked Questions

What does Adani Power's Jaiprakash deal mean for your investments?

It signals expansion in the thermal space and possible upside for Adani Power, but you should monitor regulatory clearances, financing details, and how the assets perform before adjusting your holdings.

Should you buy Adani Power stock after this deal?

Only if it aligns with your risk tolerance and portfolio plan; do not rush based on a single deal—wait for more details on financing, timing, and integration.

How could this acquisition affect thermal asset valuations?

Valuations may re-rate on expected synergies and utilization improvements, but debt levels and integration risk could constrain upside in the near term.

What near-term catalysts should investors watch?

Regulatory approvals, financing announcements, management commentary on integration plans, and asset performance updates will be key near-term catalysts.

Conclusion

The Adani Power-JPVL deal marks a meaningful step in sector consolidation. Monitor regulatory clearances, financing details, and asset integration progress, and align your holdings with your risk tolerance and diversification goals.

Big Budget

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Latest Articles

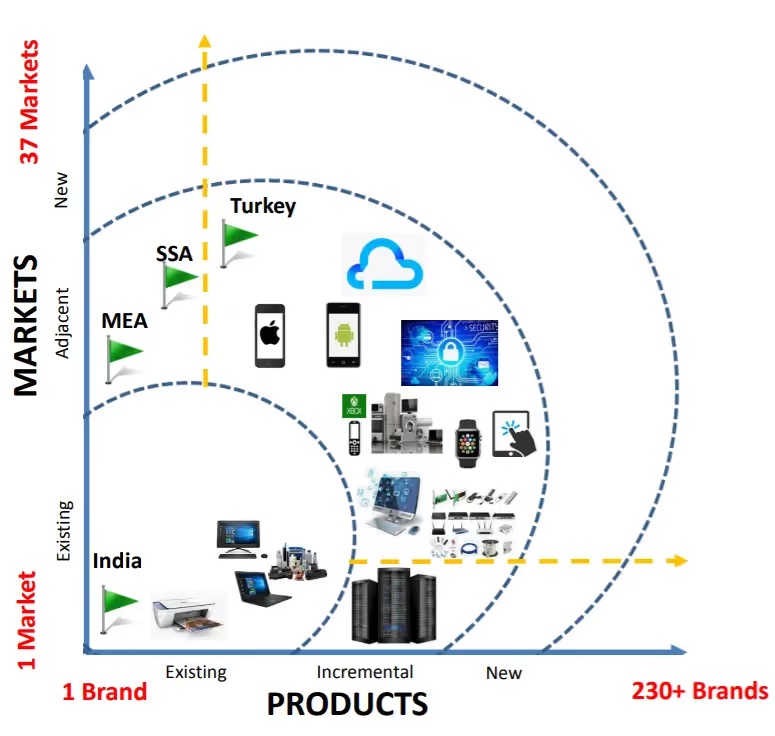

REDINGTON (INDIA) LIMITED

From a “Broadline Distributor” to a “Value Added Distributor” to a “Services & Solutions Company”

Redington is a leading distributor of technology & communication products and provider of services and solutions across 37 emerging markets, Redington will get a positive push government is preparing to unveil another incentive to drive local manufacturing of IT products including tablets, laptops and servers, three sources closely involved in the drafting of the plan told Reuters.

The new performance-linked incentive (PLI) scheme, which offers cash-back to manufacturers for exports, will have a budget of up to 70 billion rupees ($964.5 million) over five years. It's expected to be launched by the end of February.

REDINGTON INDIA -

- 1 Technology distributor in Middle East Asia and No.2 in India

- An Emerging Markets player with an in-country presence

- Expanding the reach & coverage for over 230+ brands

- Portfolio of Marquee brands

- The rich product portfolio consists of diversified Brands and diversified product categories under the same brand.

- Strong and seamless partnerships through 38,230+ partners - Their strong and seamless partnerships and dynamic business model ensure that we stay relevant in the everchanging technological environment.

- Entering into new lines of business - Foraying into new lines of businesses, leading to incremental growth as well as diversification of risk

- Multiple overseas and Indian Subsidiaries- Presence in multiple markets ensures diversification of risk as well as ensuring Kaizen’s continuous improvement.

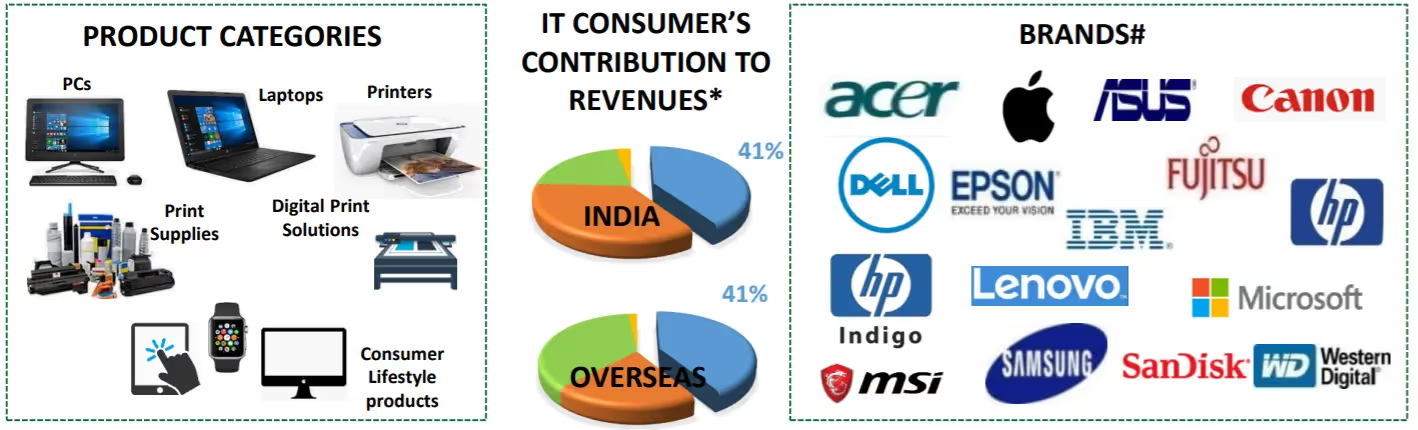

IT Consumer Business -

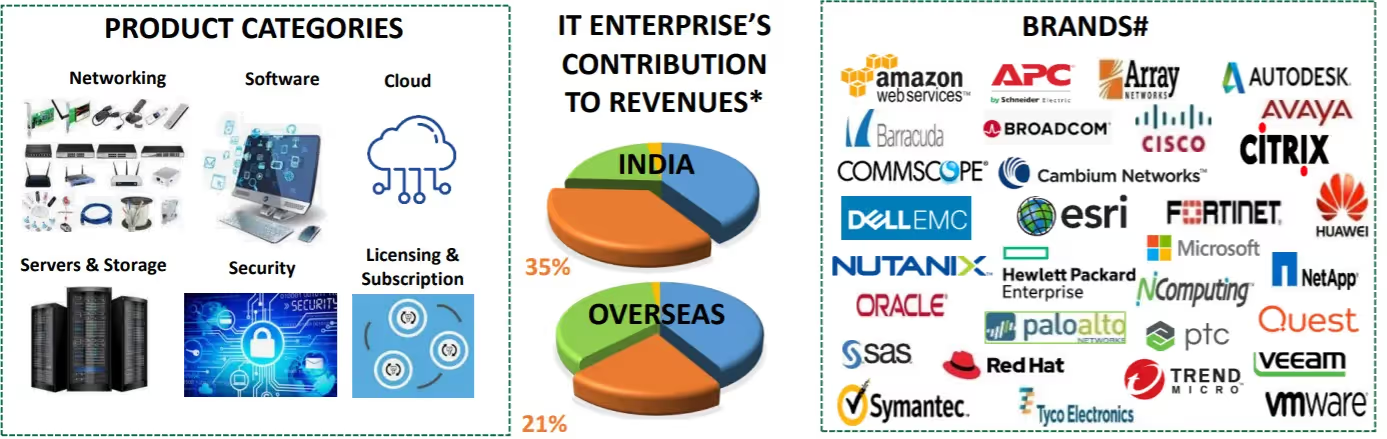

IT Enterprise Business -

- Redington Cloud Business - Unified Digital Cloud Platform, Investments in Manpower, Redington Managed Cloud Solutions, Redington Cloud Academy

Services Business

ProConnect India -

- Wholly Owned Subsidiary of Redington

- Integrated Third Party Logistics partner

- PAN India presence

- 160+ Warehouses

- 20+ Customers across 12+ Industries

MTAR Technologies Limited IPO

Incorporated in 1999, MTAR Technologies is a leading national player in the precision engineering industry. The company is primarily engaged in the manufacturing of mission-critical precision components with close tolerance and in critical assemblies through its precision machining, assembly, specialized fabrication, testing, and quality control processes.

Since its inception, MTAR Technologies has significantly expanded its product portfolio including critical assemblies i.e. Liquid propulsion engines to GSLV Mark III, Base Shroud Assembly & Airframes for Agni Programs, Actuators for LCA, power units for fuel cells, Fuel machining head, Bridge & Column, Drive Mechanisms, Thimble Package, etc. A wide range of complex product portfolios meets the varied requirements of the Indian nuclear, Defense, and Space sector. ISRO, NPCIL, DRDO, Bloom Energy, Rafael, Elbit, etc. are some of the esteem clients.

Currently, the firm has 7 state-of-the-art manufacturing facilities in Hyderabad, Telangana that undertake precision machining, assembly, specialized fabrication, brazing and heat treatment, testing and quality control, and other specialized processes.

Product Portfolio:

Nuclear sector

- Fuel machining head: Used for loading and unloading of fuel bundles in nuclear reactors

- Bridge and column

- Grid plate

- Sealing plug, shielding plug, liner tubes and end fittings

- Drive Mechanisms

Customer Sector

- Ball screws and water-lubricated bearings

- Base shroud assembly and airframes

- Various missile parts

- Valves

- Cryogenic engines (turbopumps, booster pumps, gas generators and injector heads for such engines)

- Ball screws and water-lubricated bearings

Strength of the company:

- Wide range of product portfolio.

- 7 Modern technology manufacturing units.

- Diversified supplier base.

- Strong financial track record.

- Experienced and qualified management.

Risks Relating to Industry

- Company depend on a limited number of customers for a significant portion of their revenue. The loss of one or more of their significant customers or a significant reduction in demand for their products from such significant customers.

- The company depend significantly on orders from the NPCIL, ISRO and DRDO. A decline or re-prioritization of funding in the Indian budget towards the respective departments of the Government of India under which these customers operate or delays in the budget process could adversely affect their ability to grow or maintain our sales, earnings, and cash flow.

- The company primarily rely on purchase orders to govern the volume and other terms of the sales of their products. The company do not have long-term supply agreements with its customers.

- The company are subject to strict quality standards. Any failure to comply with such quality standards may lead to the cancellation of existing and future orders which may adversely affect their reputation, financial conditions, cash flows and results of operations.

- The company could make investments and acquisitions in the future that involve considerable integration costs. The company may be unable to sustain, manage or realize the expected benefits of such growth or may not be able to fund that growth.

- Company may face claims and incur additional rectification costs for delays and/or defects in respect of their precision components and equipment

IPO Details:

IPO Date Mar 3, 2021 to Mar 5, 2021Issue Type Book Built Issue IPO Issue Size Equity Shares of Rs.10 totaling up to Rs. 596.41 Crore Fresh Issue Equity Shares of Rs.10 totaling up to Rs. 123.52croreOffer for Sale Equity Shares of Rs.10 totaling up to Rs.472.89 crore Face Value Rs.10 per equity share IPO Price Per Equity Share: Rs. 574-575 Min Order Quantity 26 Listing At BSE, NSE

IPO Objective :

The company proposes to utilize the Net Proceeds from the Fresh Issue towards funding the following objects:

- Repayment/prepayment in full or in part, of borrowings availed by our Company

- Funding working capital requirements; and

- General Corporate Purposes

Financial Performance:

Particulars For the year/period ended (₹ in million)31-Dec-2031-Mar-2031-Mar-1931-Mar-18 Total Assets3,819.143,462.713,051.582,810.32Total Revenue1,779.912,181.421,859.101,605.45Profit After Tax280.69313.18391.9954.23

Tentative Time Table:

IPO Opening Date: 3rd March 2021IPO Closing Date: 5th March 2021Finalisation of Basis of Allotment: 10th March 2021Initiation of refunds: 12th March 2021Transfer of shares to Demat account: 15th March 2021Listing Date: 16th March 2021

Outlook:

Hyderabad-based MTAR Technologies is a leading player in the precision-engineering industry develops and manufactures equipment for the defense, aerospace, clean energy, and nuclear energy sectors.

The company has long-standing relationships of over three to four decades with customers such as the Indian Space Research Organization (“ISRO”) and the Defense Research and Development Organization (“DRDO”), and have been able to supply specialized products to the Indian space programmes and the Indian missile programme, respectively.

The company’s aggregate Order Book as of November 30, 2020, was Rs.356 crores, comprising Order Book in the nuclear, space and defence, and clean energy sectors of Rs.93 crores, Rs.172 crores and Rs.86 crores respectively. These numbers signify the strength of the company. When it comes to Clean energy which is a boom these days, accounts for 64.34% of its revenues in FY2020 which also depicts its strong hold in the Clean energy sector.

The company is also focusing on its expansion plans and for the same, it is establishing an additional manufacturing facility at Adibatlaand in Hyderabad which is expected to become operational in Fiscal 2022.MTAR Technologies owns a large range of equipment, resulting in increased fixed costs.

When it comes to the financial performance of MTAR Technologies over the last three years highlights significant growth. The total revenue of the company showed a 3-year CAGR growth of 16.57%. Further, between 2018 and 2020, the profit after tax grew at a staggering CAGR of 14.39%. Also, the company’s total assets grew at a CAGR of 11%. The company’s Earnings Per Share is 11.11 and the Price to Earnings ratio stands at 51.75. As a niche player, the company is expected to gain fancy after the listing as it will be the first company to list in this segment.

Easy Trip Planners Limited IPO

Easy Trip Planners is the company behind the online travel booking portal EaseMyTrip.com. The company offers a comprehensive range of travel-related products and services for end-to-end travel solutions, including airline tickets, hotels and holiday packages, rail tickets, bus tickets and taxis as well as ancillary value-added services such as travel insurance, visa processing and tickets for activities and attractions.

As of 30 November 2019, it provided customers with access to more than 400 international and domestic airlines, more than 1,096,400 hotels in India and in international jurisdictions, almost all the railway stations in India as well as bus tickets to and taxi rentals for major cities in India.

The company is among the leading online travel agencies in India in terms of gross booking revenues and had a market share of approximately 3.8%, and 4.5% to 5% in terms of gross booking revenues and gross booking revenues for the airline ticketing segment in India during FY2019.

The company focuses on the B2B2C (business to business to customer), B2C (business to customer), and B2E (business to enterprise) distribution channels.

Product Portfolio:

The company’s products and services are organized primarily in the following segments:

Airline tickets, which consist of the sale of airline tickets as well as airline tickets sold as part of the holiday packages; Hotels and holiday packages, which consist of standalone sales of hotel rooms as well as travel packages (which may include hotel rooms, cruises, travel insurance, and visa processing); and Other services, which consist of rail tickets, bus tickets, taxi rentals and ancillary value-added services such as travel insurance, visa processing and tickets for activities and attractions.

Strengths of the Company

- One of the leading online travel agencies in India.

- Strong brand name and distribution network.

- In-house advanced technology infrastructure.

- Consistent financial track record and operational performance.

RISKS RELATING TO BUSINESS

- Any impact on airline bookings can adversely impact the revenue of the company.

- Any reduction in the commission of GDS and API service providers can affect the company’s business and growth.

- Any disruption to the supply of air, train, and bus tickets could adversely affect operations, turnover, and profitability.

- Any failure to maintain the quality of customer service and deal with complaints could adversely affect its business and operating results.

IPO Details:

IPO Date March 8th, 2021 to March 10th, 2021 Issue Type Book Built Issue IPO Issue Size Eq Shares of ₹2(aggregating up to ₹510.00 Cr) Fresh Issue NIL Offer for Sale Eq Shares of ₹2(aggregating up to ₹510.00 Cr)Face ValueRs.2 per equity share IPO Price Rs.186 to Rs.187per equity share Min Order Quantity 80 Listing At BSE, NSE

IPO Objective:

- To achieve the benefits of listing the equity shares on the stock exchange

- To execute the sale of up to 2,72,72,727equity shares by the promoter selling shareholders aggregating up to Rs.510 Cr

Financial Performance:

Easy Trip Planners’ financial performance (in INR crore)FY2018FY2019FY20209M FY2021Revenue113.6151.1179.781.6Expenses103109.9132.239.7Net income02434.631.1Net margin (%)015.919.338.1

Tentative Time Table:

- Price Band announced on 3 March 2021

- Ease My Trip IPO Anchor List on 7 March 2021

- Ease My Trip IPO Opens on 8 March 2021

- Ease My Trip IPO Closes on 10 March 2021

- Ease My Trip IPO Allotment on 16 March 2021

- Unblocking of ASBA 17 March 2021

- Credit to Demat Accounts 18 March 2021

- Ease My Trip IPO Listing on 19 March 2021

Outlook :

Easy Trip Planners is the second largest online travel agency in India in terms of volume and 3rd largest in terms of revenues. Easy Trip Planners has the lowest sales and marketing expense as a percentage of its gross booking revenues in 2020 as per a report by CRISIL.

The Indian travel industry is expected to grow at a CAGR of 2% from Fiscal 2020 to Fiscal 2023. As people have slowly started resuming air travel after the COVID-19, the air ticketing segment is expected to grow at a CAGR of 1.5% by Fiscal 2023.

Increasing penetration of the internet and smartphones is expected to continue aiding the growth in this segment, the impact of the pandemic might take some time to wear off.

Easy Trip Planners have stable revenue growth over the last 3 years and it is generating consistent and improved margins. Over FY17-20, Company saw a 31.7% CAGR rise in the gross booking revenue which is led by a 52.4% CAGR growth in the gross booking volume. PAT from operations increased by 23.6% CAGR over FY17-20.

At an EPS of 3.19 and at an upper price band of 187, the PE ratio would be 58.62, however as per the RHP company does not have any peers thus it is ascertained whether the issue price is underpriced or overpriced. The company’s net profit margin in FY2020 is 19.3%.

The company is further claiming to be using sophisticated technology which will help in improving the margins growing further. Thus, the fundamentals of the company would also be improving.

The New Definition of MSME

Indian economy fundamentally relies upon two areas, agriculture and manufacturing. While the first has generally stayed unorganized since the start, the last also has not been so till now. The MSME area has gradually come into the spotlight, with expanded concentration from the public authority and other government organizations, corporate bodies and banks.

Strategy based changes; interests in the area; globalization and India's powerful monetary development have started up a few inactive business openings for this area.

MSME represents Micro, Small, and Medium Enterprises. As per the Micro, Small, and Medium Enterprises Development (MSMED) Act in 2006, the ventures are arranged into two divisions.

- Manufacturing enterprises occupied with the assembling or creation of products in any industry

- Service enterprises providing or rendering services

In the modified definition, both the manufacturing and the service sector are grouped together.

Micro:

Manufacturing and Service Industries – Investment ought to be under 1 Crore and Turnover ought to be under 5 Crore.

Small:

Manufacturing and Service Industries – Investment ought to be more than 1 Crore and under 10 Crore. Though, Turnover ought to be more than 5 Crore and under 50 Crore.

Medium:

Manufacturing and Service Industries – Investment ought to be more prominent than 10 Crore and under 20 Crore. Though, Turnover ought to be more than 50 Crore and under 100 Crore.

Some Important Points of MSME

1. Collateral Free Loans

Collateral free loans for organizations has been arranged including MSMEs and emergency credit line to organizations/MSMEs from banks and NBFCs up to 20 per cent of whole extraordinary credit.

2. Equity imbuement of Rs. 50,000 crores for MSMEs via a Fund of Funds

The Government has additionally declared the proposed foundation of a Fund of Funds is proposed to be set up with a corpus of Rs. 10,000 crores and will be worked through a 'Mother Fund' and a couple of daughter funds, through which it expects to use Rs. 50,000 crores of assets. That will straightforwardly put resources into MSMEs and urge them to list on the Indian stock trades.

3. Interest subvention

An interest subvention will be reached out to every one of those brief payees who are making normal installments for a year. Has likewise been declared under Mudra Scheme's Shishu Cover whereby a 2 per cent interest to aid will be permitted on credits up to INR 50,000.

4. Postponement of registration and completion date of real estate projects under RERA

During the underlying days of the lockdown, the Ministry of Finance had assigned the COVID-19 pandemic as a power Majeure occasion under RERA and consequently extended the project completion cutoff times by a time of a half-year.

5. Rs 20 crore subordinated debt for MSMEs

MSMEs ministry has introduced the Credit Guarantee Scheme for Subordinate Debt (CGSSD) which is called 'Distressed Assets Fund–Subordinate Debt for MSMEs'

(i) Promoters of MSMEs will be given credit equivalent to 15% of their stake (e+d) or Rs. 75 lakhs, whichever is lower.

(ii) A moratorium of 7 years on principal payment while maximum extreme tenure for repayment will be 10 years.

(iii) 90% assurance cover for this subordinate debt will be given under the plan/trust and 10% would come from the concerned advertisers.

6. Directions to Public Sector Undertakings to make timely payments

Bearings have been given by the Cabinet Secretary, Expenditure Secretary and Secretary, MSME to all PSUs to take care of remarkable obligations to MSMEs within the time span of 45 days.

7. Extension of the due date for ITR for FY’19-20 to November 30, 2020

As declared by the public authority in a question and answer session, the due date for all income tax returns (ITR) for FY 2019-20 has been stretched out from July 31, 2020, and October 31, 2020, to November 30, 2020, and for the tax audit from September 30, 2020, to October 31 2020

8. ECLG scheme

The ECLG Scheme would apply to all advances authorized or made accessible to MSMEs between 23 May 2020 and 31 October 2020 and the Government has as of now put a general cap of Rs. 3 lakh crores for all credits dispensed under the ECLG Scheme.

9. Measures identifying with the Insolvency and Bankruptcy Code

This alteration will probably profit MSMEs that are under monetary misery because of the financial emergency brought about by COVID-19. The Government on 24 March 2020 expanded the base edge for default from Rs.1 lakh to Rs.1 crore to start the corporate insolvency resolution process under the Insolvency and Bankruptcy Code, 2016 (IBC).

10. Import protection

In a line towards confident India or backing make in India and will likewise assist MSMEs with extending their business. For this, worldwide tenders have been refused in Government acquirement tenders up to INR 200 crore because Indian MSMEs and different organizations have regularly confronted unjustifiable rivalry from foreign organizations.

ओपेक देशों की बैठक से कच्चे तेल की कीमतों को नई दिशा मिलेगी।

ब्रेंट कच्चे तेल की कीमतें 65 डॉलर प्रति बैरल के ऊपर पहुंच गई है लेकिन 68 डॉलर के महत्वपूर्ण प्रतिरोध स्तरों पर है। इस सप्ताह गुरुवार को, पेट्रोलियम निर्यातक देशों और सहयोगियों (ओपेक) की बैठक पर निवेशको की नज़र रहेगी जिसके पहले अन्य बाज़ारो पर दबाव देखा गया है।

कच्चे तेल की कीमतों मे लगातार सुधार होने के कारण, ओपेक और सहयोगी देशो के निर्णय पर बाज़ारों की निगाहें होगी। अधिक आपूर्ति होने से सऊदी अरब ने पिछली बैठक मे अतिरिक्त उत्पादन कटौती पर समझौता किया था। जबकि अन्य तेल निर्यातक देशो ने आपूर्ति को स्थिर रखने पर जोर दिया था। वही रूस उत्पादन मे वृद्धि के पक्ष मे रहा है।

अमेरिकी प्रान्त टेक्सास और आसपास के क्षेत्रों में पिछले सप्ताह की ठंड के कारण 40 लाख बैरल प्रति दिन कच्चे तेल की आपूर्ति बाधित हुई है। जिससे कच्चे तेल की कीमतों में मजबूती है और इस महीने मे ब्रेंट तथा अमेरिकी कच्चे तेल मे 20 प्रतिशत की बढ़त दर्ज की गई है। वैश्विक तेल स्टॉक मे लगातार कमी दर्ज की गई है लेकिन, मौसम के कारण बाधित होने वाले कच्चे तेल उत्पादन में लाखों बैरल की कमी धीरे-धीरे पूरी हो रही है। बांड बाजार टूटने से डॉलर मे तेज़ी होने की सम्भावना है और ऐसा होने पर कच्चे तेल की आपूर्ति बढ़ सकती है।

तकनीकी लेवल

इस सप्ताह कच्चे तेल की कीमतों मे अस्थिरता रहने की सम्भावना है।घरेलु वायदा कच्चे तेल के भाव मे 4700 रुपय पर प्रतिरोध और 4200 रुपय पर सपोर्ट है। ब्रेंट वायदा कच्चे तेल मे 67 डॉलर पर प्रतिरोध तथा 62 डॉलर पर सपोर्ट है।

Effect on Stock Market After Rising COVID 19 Cases: Government Moves and Vaccine Rollout

As the COVID 19 cases had marked a considerable decline in the past few months, the active cases have been on the rise again and with Feb 21, registering new cases of 14,199. However, the cases had seen a sudden decline on Feb 16 with 9,121.

The spectacular fall in the COVID 19 cases for nearly five months, in the states that has shown a resurgence now, had led to a belief that the infection levels in the country had probably reached a new level where the effects of herd immunity had started to play out.

On Monday, the ministry reported 83 deaths with a total tally of over 1.56 lakh. This accounts for 1.42% of more than 1.1 crore coronavirus cases detected in India. Some states including Maharashtra, Kerala have been advised by the centre to increase the proportion of RT-PCR tests and regularly monitor mutant strains.

Maharashtra's government has announced renewed curbs in Pune and Amravati because fresh cases rose nearly up to 5000 per day in the country's worst-hit state.

After the sudden rise of COVID 19 cases, the restrictions have forced the stock market to go down, and with the BSE Sensex which was a little above 1,145 points (2.25 per cent) to close below 50,000 at 49, 744 on Feb 22. The Nifty settled below 14,700 level at close on the same day.

Although the testing rate had not dropped significantly, lockdown restrictions had been eased, festivals, elections had seen people coming out in multiple numbers, political activities had restarted, a farmers’ protest had been going on.

As the active cases of COVID 19 cases rose by 4,421, registering a three per cent increase in the active caseload back to the 1.5 lakh mark. However, the sheer rise has been marked since the beginning of November where there was an increment of 3.85 per cent in the COVID cases. The latest spike has come in Feb where the cases have been continuously rising in Maharashtra, Kerala, Punjab, Chhattisgarh, Madhya Pradesh.

Restrictions are Back

Due to rising cases of COVID 19, the Central government and state government put restrictions in order to minimize the cases in the bud. In Maharashtra, the government has been putting a ban on social gatherings, night curfew in Amravati. Also, surveillance has been increased in the states (Maharashtra, Kerala) where the COVID cases are still rising.

In the last five days, the Sensex lost 2,400 points and there are certain factors responsible for the COVID 19 cases including the rise in the US, domestic bonds, yields, consequent fear of inflation and the rise in crude oil prices.

Recently, the petrol prices are still high i.e. Rs 100 per liter which in turn has triggered fears that the prices of other commodities may rise.

Although the COVID-19 cases and other factors may heavily impact the stock market, analysts attribute the current correction to the valuations. In the recent past, where the market has performed well despite having COVID-19 issues, the recent budget focused on triggering economic growth and the Capex cycle and an aggressive fiscal deficit of 9.5% for FY21 and 6.8% for FY22.

FIIs continue to be Bullish

Foreign Institutional Investors continue to be bullish and have been net buyers worth Rs 23,875 crore till the Feb end. As per provisional data from NSE, the FIIs had turned net sellers offloading over Rs 893 crore.

According to Credit Suisse, a brokerage India has seen a net portfolio investment of $5.2 billion in January. The firm has upgraded its Indian equity market stance overnight from the earlier market weight and said the country was in good condition as compared to other economies in the world.

Bond Yields and RBI’s possible moves

In India, the ten-year-old bond yield has risen for four straight sessions and closed at over 6 per cent on Monday. Now, all the analysts and trader’s eyeing RBI’s special open market operation worth Rs 10,000 crore where it will buy and sell simultaneously. Therefore, any RBI intervention to keep bond yield at or below 6% will be welcomed by equity markets.

Seeking the Bright Side

As India announced its first-ever vaccine against COVID 19, India’s rate has been 3 lakh vaccinations per day but it is only a quarter of the 1.3 million vaccinations target per day. India had proved 11.8 million vaccinations nationwide as of February 22, the beginning of the drive.

Keeping this in mind, the central government has decided to increase the current rate to 5 million vaccines nearly in a day over the next month. It will be a welcoming move in controlling the fear of the second move.

The central government has further decided to involve the private sector in India’s vaccination efforts which in turn bring back the positive sentiments in the stock market. As per the sources of NITI aayog, the details of private privatization in the vaccine drive will be made available soon to buoy the market.

According to the experts, the rise in COVID 19 cases is not a uniform spread in the whole country as it can be the outcome of different testing protocols across the country. Also, it's not clear whether the rising cases of COVID 19 is the beginning of a second wave or not.

A Flitch reporting report has said the decline in the economic activities in the UK and France during the fourth quarter of 2020, were quite less, even though there were lockdowns there. India’s economy and the Indian’s stock market can take an idea from this report.

Conclusion

Even after the COVID 19, the stock market is likely to react positively and bounce back from Monday’s close on the back of private sector involvement in vaccinations, better containment of cases and other major factors such as sustained FII inflows, central bank interventions and more.

.avif)

.avif)

.avif)

START YOUR INVESTMENT JOURNEY

Get personalized advice from our experts

- Dedicated RM Support

- Smooth and Fast Trading App